Corporate Finance: Riverlea Capital Budgeting and Market Impact Report

VerifiedAdded on 2020/03/23

|16

|3226

|37

Report

AI Summary

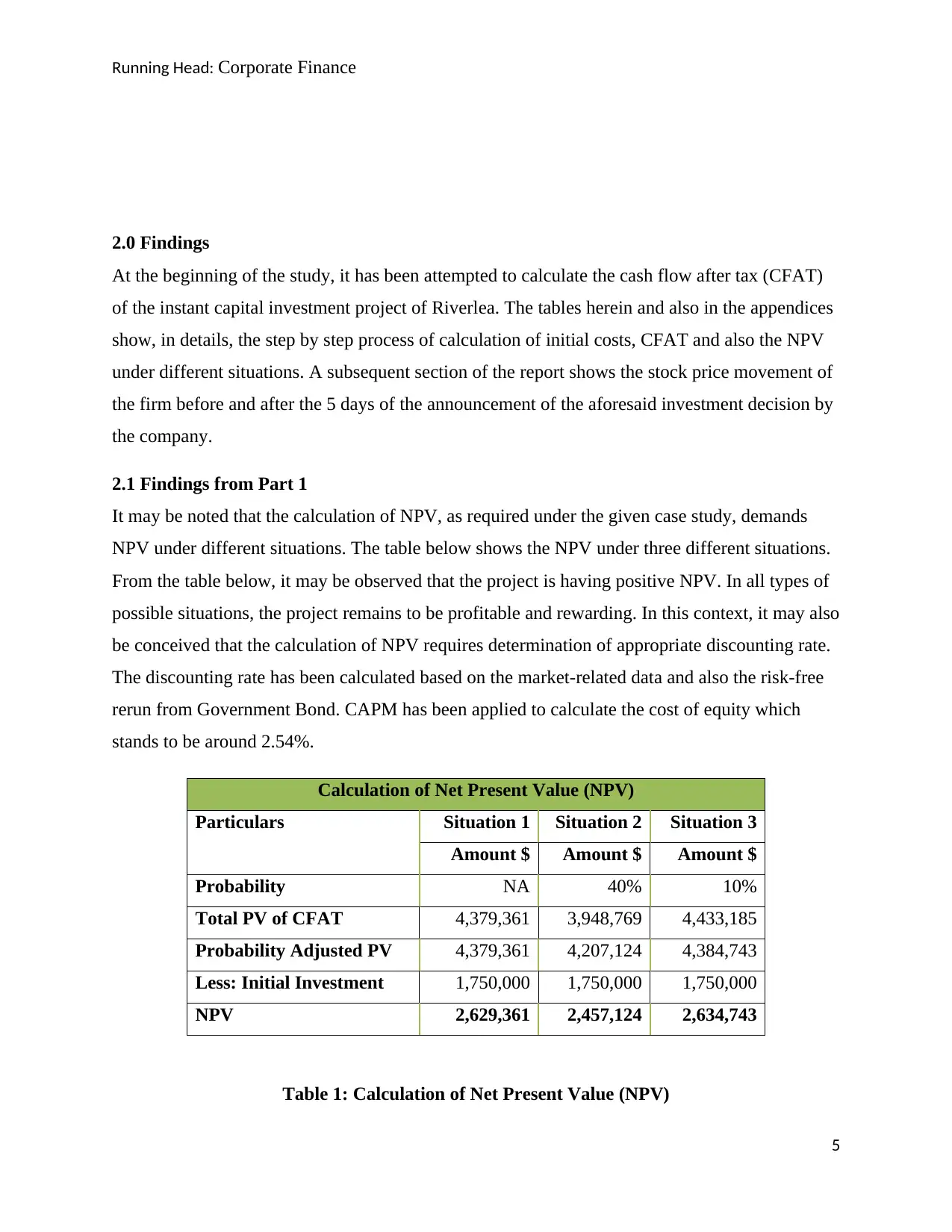

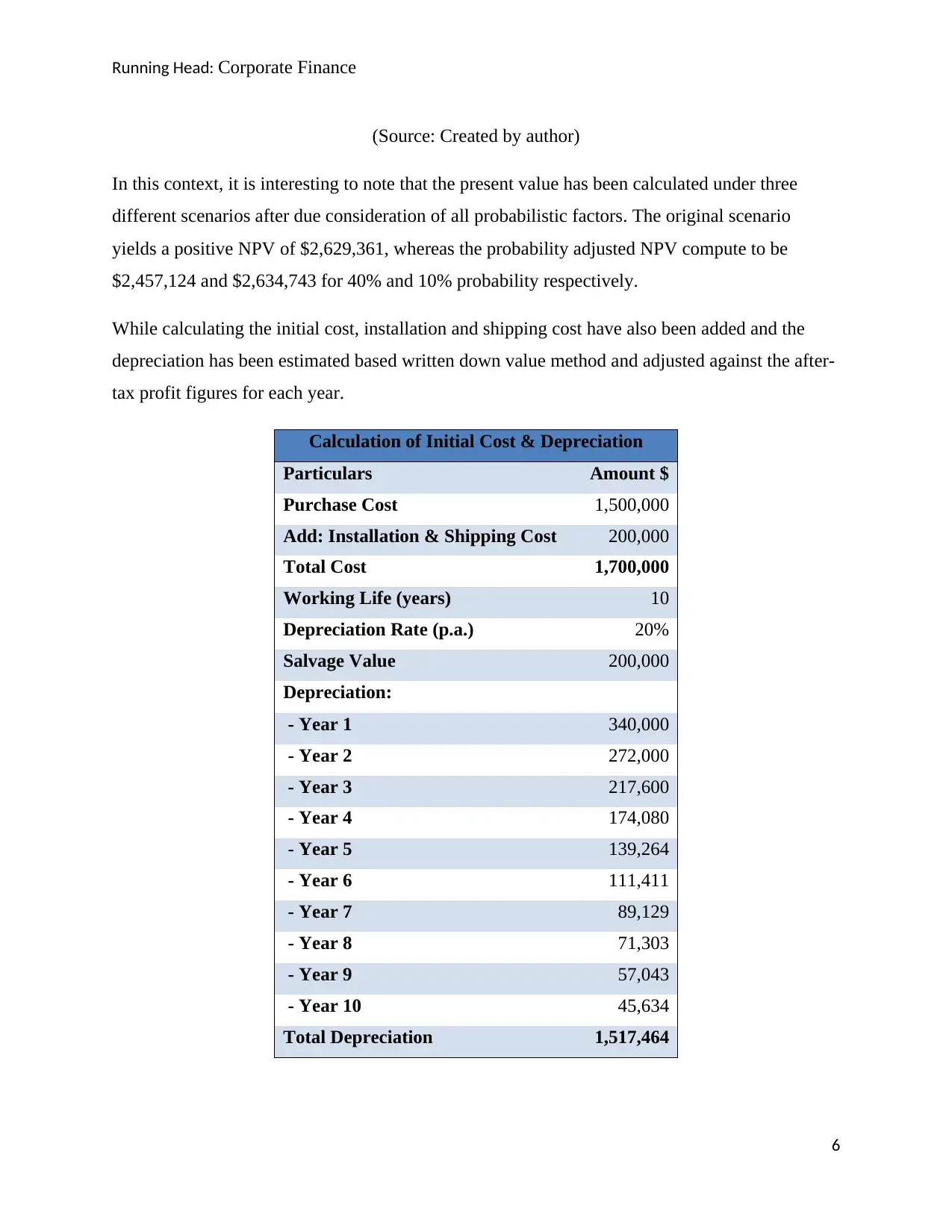

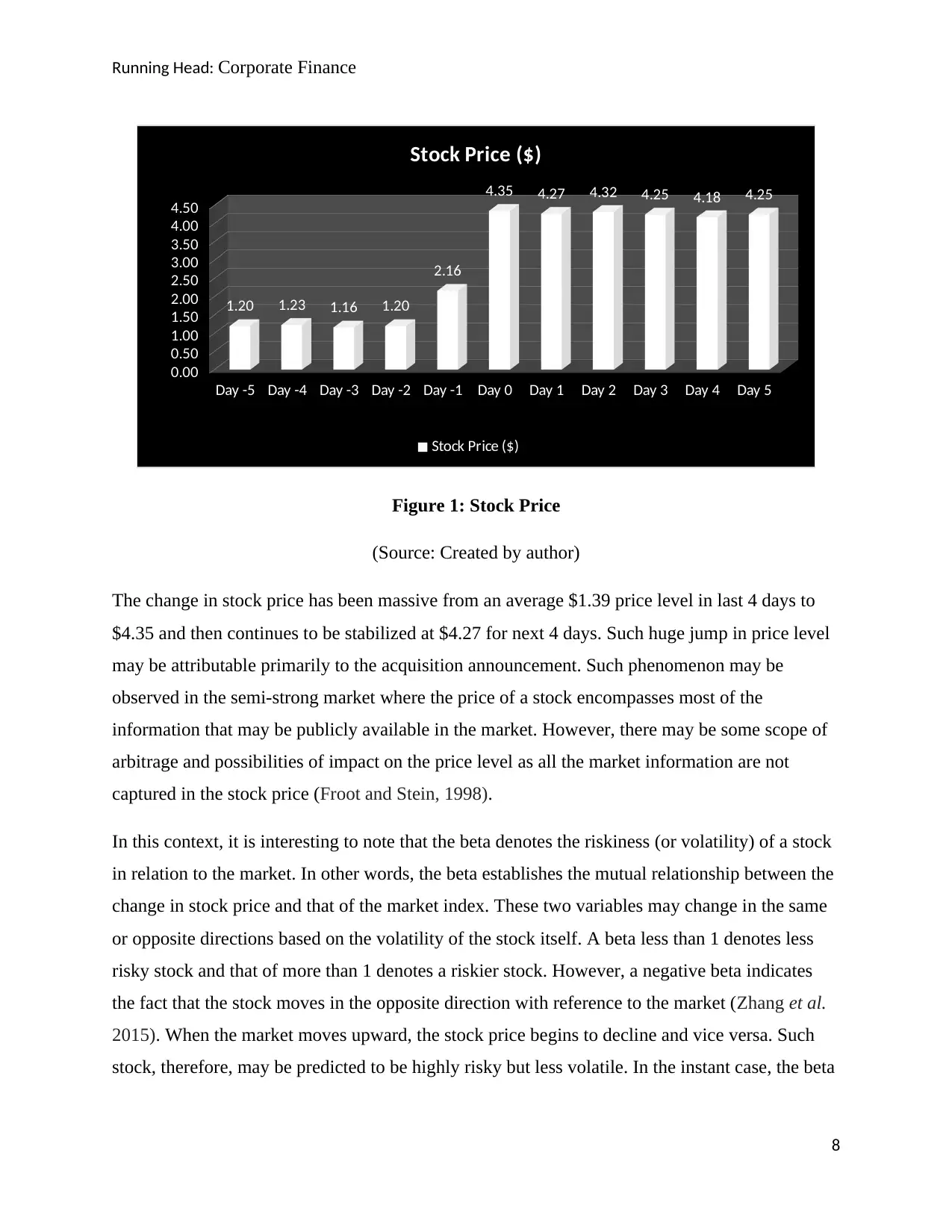

This report presents a comprehensive analysis of Riverlea's capital budgeting project. It begins with an executive summary highlighting the importance of capital budgeting in business management. The report then delves into the calculation of Net Present Value (NPV) under various scenarios, providing detailed tables and appendices to illustrate the step-by-step process of calculating initial costs, CFAT, and NPV. Furthermore, it examines the movement of the company's stock price following the announcement of the investment decision, relating the findings to the semi-strong market hypothesis. The report calculates the cost of equity using CAPM and analyzes initial costs and depreciation. The analysis shows the project's financial viability and recommends acceptance, considering both financial and non-financial factors. The report concludes that the investment has a positive effect on the stock price and recommends that the management should consider the fact that the stock price depends on lots of factors some of which are beyond the control of the firm.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.