Corporate Accounting Analysis: Virgin Australia Financials

VerifiedAdded on 2021/05/31

|11

|2179

|52

Report

AI Summary

This report provides a comprehensive analysis of corporate accounting principles, focusing on the cash flow statement, other comprehensive income statement, and accounting for corporate income tax. The report examines the financial statements of Virgin Australia (VAH), a publicly listed airline company, to illustrate key concepts. The cash flow statement analysis includes operating, investing, and financing activities, highlighting trends and significant items from 2015 to 2017. The other comprehensive income statement components, such as income tax benefit, foreign currency translation reserve, and cash flow hedge reserve, are also assessed. The report further delves into corporate income tax, including tax expenses, deferred tax assets and liabilities, and current tax assets. The analysis includes a discussion of Virgin Australia's tax benefits and their impact on the financial statements. The report references multiple academic sources to support its findings, providing a thorough examination of corporate accounting practices.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE ACCOUNTING

Table of Contents

Cash flow statement:........................................................................................................................2

Requirement (i):...........................................................................................................................2

Requirement (ii):..........................................................................................................................3

Other comprehensive income statement:.........................................................................................5

Requirement (iii):.........................................................................................................................5

Requirement (iv):.........................................................................................................................5

Requirement (v):..........................................................................................................................5

Accounting for corporate income tax:.............................................................................................6

Requirement (vi):.........................................................................................................................6

Requirement (vii):........................................................................................................................6

Requirement (viii):.......................................................................................................................6

Requirement (ix):.........................................................................................................................7

Requirement (x):..........................................................................................................................7

Requirement (xi):.........................................................................................................................7

References........................................................................................................................................9

Table of Contents

Cash flow statement:........................................................................................................................2

Requirement (i):...........................................................................................................................2

Requirement (ii):..........................................................................................................................3

Other comprehensive income statement:.........................................................................................5

Requirement (iii):.........................................................................................................................5

Requirement (iv):.........................................................................................................................5

Requirement (v):..........................................................................................................................5

Accounting for corporate income tax:.............................................................................................6

Requirement (vi):.........................................................................................................................6

Requirement (vii):........................................................................................................................6

Requirement (viii):.......................................................................................................................6

Requirement (ix):.........................................................................................................................7

Requirement (x):..........................................................................................................................7

Requirement (xi):.........................................................................................................................7

References........................................................................................................................................9

2CORPORATE ACCOUNTING

Cash flow statement:

Requirement (i):

The reporting areas of the assignment has been considered with “Virgin Australia” which

is recognised as one of the top airline companies listed under ASX and coded as VAH. The

depictions of the cash flow statement have been segregated into “financing activities, investing

activities and operating activities” (Virginaustralia.com, 2018). Some of the main classification

of the items are listed below as follows:

Cash flows from operating activities:

Some of the main items in this section is considered with receiving financing income,

payments made to staff, finance costs paid and payment to suppliers. The amount obtained from

the credit sales are known as customer receives in this case. With particular reference to virgin

Australia, the overall increase in the cash inflow is discerned as “$5,567.40 million in 2016 to

$5,657.10 million in 2017”. This is mainly due to the fact of strict credit policy adopted by the

company. The payments made to the staff and suppliers are amounts which are purchased on

credit and staff payments include the salaries (Virginaustralia.com, 2018). The increasing trend

under these subheadings are evident in the case of Virgin with an increasing trend of additional

purchases from suppliers. It is further noted that finance income is received to utilise money for

repayment on demand or at a specified period. In addition to this, the increase in this section is

seen to be writing off the considerable portion of as uncollectible. In 2017, the finance costs have

shown certain decrease due to lesser amount of interest payment on loans (Virginaustralia.com,

2018).

Cash flow statement:

Requirement (i):

The reporting areas of the assignment has been considered with “Virgin Australia” which

is recognised as one of the top airline companies listed under ASX and coded as VAH. The

depictions of the cash flow statement have been segregated into “financing activities, investing

activities and operating activities” (Virginaustralia.com, 2018). Some of the main classification

of the items are listed below as follows:

Cash flows from operating activities:

Some of the main items in this section is considered with receiving financing income,

payments made to staff, finance costs paid and payment to suppliers. The amount obtained from

the credit sales are known as customer receives in this case. With particular reference to virgin

Australia, the overall increase in the cash inflow is discerned as “$5,567.40 million in 2016 to

$5,657.10 million in 2017”. This is mainly due to the fact of strict credit policy adopted by the

company. The payments made to the staff and suppliers are amounts which are purchased on

credit and staff payments include the salaries (Virginaustralia.com, 2018). The increasing trend

under these subheadings are evident in the case of Virgin with an increasing trend of additional

purchases from suppliers. It is further noted that finance income is received to utilise money for

repayment on demand or at a specified period. In addition to this, the increase in this section is

seen to be writing off the considerable portion of as uncollectible. In 2017, the finance costs have

shown certain decrease due to lesser amount of interest payment on loans (Virginaustralia.com,

2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE ACCOUNTING

Cash flows from investing activities:

The primary items listed under the cash from investing activities have been considered

with equity distributions, proceed from borrowings and several other items. The borrowings have

been further able to signify the total amount disbursed to the borrower under the terms of

agreement of loan (Virginaustralia.com, 2018). It needs to be further assessed from the annual

report that the borrowings have decreased in 2017, whereas there is increase in the repayment of

borrowings during the same year. Additionally, the distribution of equity has signified on the

total amount disbursed to the borrower on part of the lender as per the agreement of the loan. It

needs to be further observed that the annual report of Virgin Australia has considered the

proceeds from shareholders and the total amount has reduced due to increased retained earnings

(Scott, 2015).

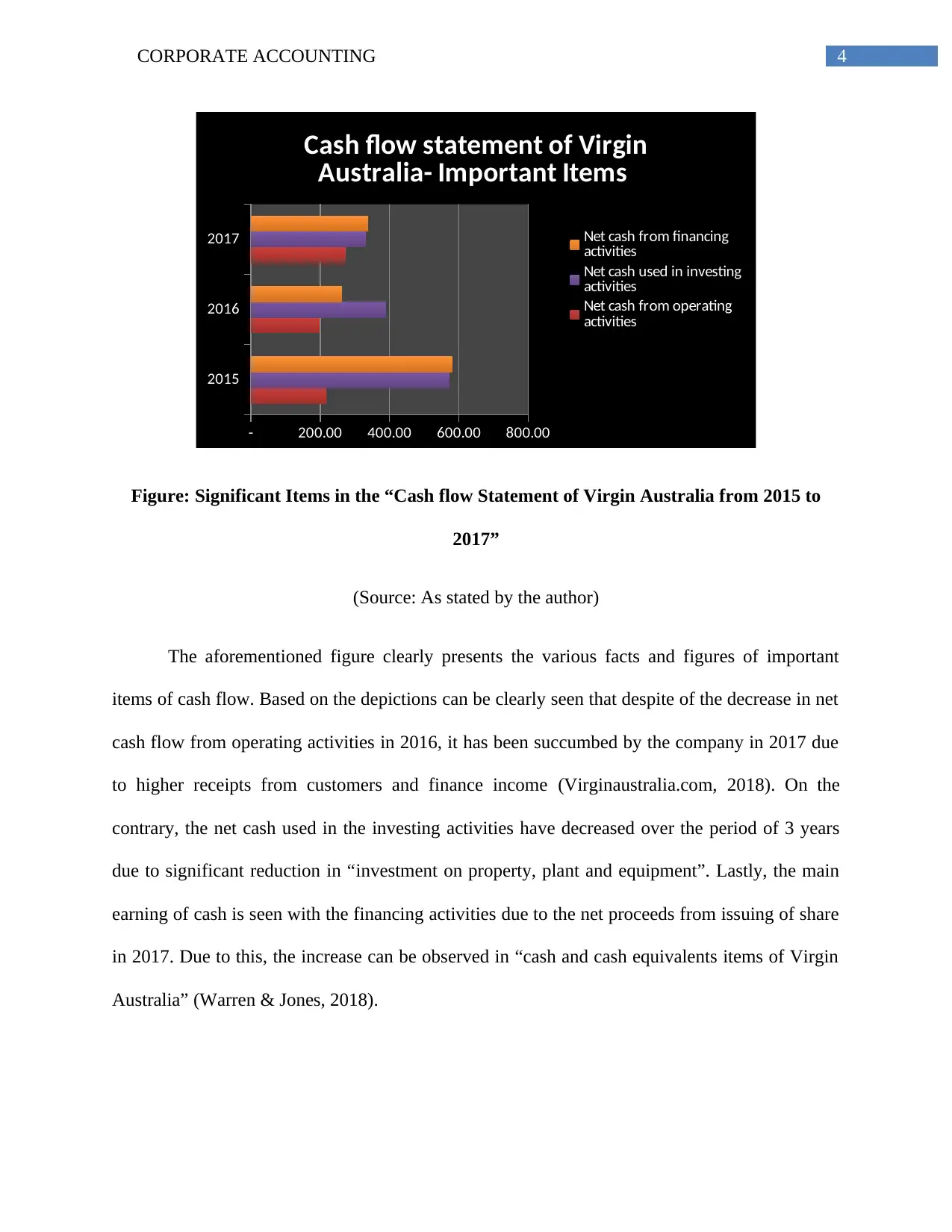

Requirement (ii):

The evidence of three categories of cash flows such as “financing activities, operating

activities and investing activities” can be traced from the annual report published by Virgin

Australia. Moreover, the comparative analysis in these categories have been shown with the use

of bar diagram as follows:

Cash flows from investing activities:

The primary items listed under the cash from investing activities have been considered

with equity distributions, proceed from borrowings and several other items. The borrowings have

been further able to signify the total amount disbursed to the borrower under the terms of

agreement of loan (Virginaustralia.com, 2018). It needs to be further assessed from the annual

report that the borrowings have decreased in 2017, whereas there is increase in the repayment of

borrowings during the same year. Additionally, the distribution of equity has signified on the

total amount disbursed to the borrower on part of the lender as per the agreement of the loan. It

needs to be further observed that the annual report of Virgin Australia has considered the

proceeds from shareholders and the total amount has reduced due to increased retained earnings

(Scott, 2015).

Requirement (ii):

The evidence of three categories of cash flows such as “financing activities, operating

activities and investing activities” can be traced from the annual report published by Virgin

Australia. Moreover, the comparative analysis in these categories have been shown with the use

of bar diagram as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE ACCOUNTING

2015

2016

2017

- 200.00 400.00 600.00 800.00

Cash flow statement of Virgin

Australia- Important Items

Net cash from financing

activities

Net cash used in investing

activities

Net cash from operating

activities

Figure: Significant Items in the “Cash flow Statement of Virgin Australia from 2015 to

2017”

(Source: As stated by the author)

The aforementioned figure clearly presents the various facts and figures of important

items of cash flow. Based on the depictions can be clearly seen that despite of the decrease in net

cash flow from operating activities in 2016, it has been succumbed by the company in 2017 due

to higher receipts from customers and finance income (Virginaustralia.com, 2018). On the

contrary, the net cash used in the investing activities have decreased over the period of 3 years

due to significant reduction in “investment on property, plant and equipment”. Lastly, the main

earning of cash is seen with the financing activities due to the net proceeds from issuing of share

in 2017. Due to this, the increase can be observed in “cash and cash equivalents items of Virgin

Australia” (Warren & Jones, 2018).

2015

2016

2017

- 200.00 400.00 600.00 800.00

Cash flow statement of Virgin

Australia- Important Items

Net cash from financing

activities

Net cash used in investing

activities

Net cash from operating

activities

Figure: Significant Items in the “Cash flow Statement of Virgin Australia from 2015 to

2017”

(Source: As stated by the author)

The aforementioned figure clearly presents the various facts and figures of important

items of cash flow. Based on the depictions can be clearly seen that despite of the decrease in net

cash flow from operating activities in 2016, it has been succumbed by the company in 2017 due

to higher receipts from customers and finance income (Virginaustralia.com, 2018). On the

contrary, the net cash used in the investing activities have decreased over the period of 3 years

due to significant reduction in “investment on property, plant and equipment”. Lastly, the main

earning of cash is seen with the financing activities due to the net proceeds from issuing of share

in 2017. Due to this, the increase can be observed in “cash and cash equivalents items of Virgin

Australia” (Warren & Jones, 2018).

5CORPORATE ACCOUNTING

Other comprehensive income statement:

Requirement (iii):

The assessment of annual report by the company in 2017, the important items in the

comprehensive income statement has been comprised of income tax benefit our expense, foreign

currency translation reserve and cash flow hedge reserve (Virginaustralia.com, 2018).

Requirement (iv):

The foreign currency has been further put forward to use with the conversion of outcomes

associated to foreign subsidiaries to the reporting currency by the parent firm. The utilisation of

“cash flow hedge reserve” is seen with the main intention to reduce the various exposures

pertaining to variations in the cash flow of liability or asset and particular changes in the risk

associated to interest rate of that instrument related to floating rate. On the contrary, the “IT

expense” is the amount which is incurred as per PBT of the company (Dyreng, Hoopes & Wilde,

2016).

Requirement (v):

The elaborated view on net income is taken into consideration with other comprehensive

income. Virgin Airlines have used the net income to provide significant details on values

mentioned above. The main rationale for these items are included in the justification of other

comprehensive income statement. According to this, the income statement provides a holistic

summary of main driver is associated to business operations and therefore they are not disclosed

in the income statement (Taylor, G., & Richardson, 2014).

Other comprehensive income statement:

Requirement (iii):

The assessment of annual report by the company in 2017, the important items in the

comprehensive income statement has been comprised of income tax benefit our expense, foreign

currency translation reserve and cash flow hedge reserve (Virginaustralia.com, 2018).

Requirement (iv):

The foreign currency has been further put forward to use with the conversion of outcomes

associated to foreign subsidiaries to the reporting currency by the parent firm. The utilisation of

“cash flow hedge reserve” is seen with the main intention to reduce the various exposures

pertaining to variations in the cash flow of liability or asset and particular changes in the risk

associated to interest rate of that instrument related to floating rate. On the contrary, the “IT

expense” is the amount which is incurred as per PBT of the company (Dyreng, Hoopes & Wilde,

2016).

Requirement (v):

The elaborated view on net income is taken into consideration with other comprehensive

income. Virgin Airlines have used the net income to provide significant details on values

mentioned above. The main rationale for these items are included in the justification of other

comprehensive income statement. According to this, the income statement provides a holistic

summary of main driver is associated to business operations and therefore they are not disclosed

in the income statement (Taylor, G., & Richardson, 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE ACCOUNTING

Accounting for corporate income tax:

Requirement (vi):

Some of the main tax expenses are further taken into account with important consideration

of the organisation because of “federal, municipal and state governments of the nation”. With

reference to the selected organisation, Virgin Australia has not incurred any IT expense. Instead,

it has obtained the benefit in both 2016 and 2017. In 2017, the company obtained IT benefit of

“$103.8 million in compared to $201.9 million in 2016” (Dowling, 2014).

Requirement (vii):

Based on the annual report of “Virgin Australia in 2017”, it can be discerned that

organisation has suffered losses before IT in 2016 and 2017. It is clearly noted that the airline

charges of 30% on PBT has been taken into consideration to compute the net income. Despite of

this, the airline incurred significant loss due to the IT expense. Therefore, it cannot be

determined a possible reason is whether IT is calculated by the consideration of 30% tax rate on

PBIT (Beatty & Liao, 2014).

Requirement (viii):

The consideration for “deferred tax assets” are included in those situations when the firm

needs to make prepayments of taxes or additional taxes on the financial assets. On the contrary,

deferred tax liabilities are able to highlight several variations in “profit of the corporate entities

and tax in the carrying amount” (Virginaustralia.com, 2018). The deferred taxes of the airliner

have amounted “$1,017.6 million in 2017, which was depicted as $857.9 million in 2016”. On

the contrary, the “deferred tax liability” is being seen as “$463.4 million in 2017 when compared

with $434.4 million in 2016”.

Accounting for corporate income tax:

Requirement (vi):

Some of the main tax expenses are further taken into account with important consideration

of the organisation because of “federal, municipal and state governments of the nation”. With

reference to the selected organisation, Virgin Australia has not incurred any IT expense. Instead,

it has obtained the benefit in both 2016 and 2017. In 2017, the company obtained IT benefit of

“$103.8 million in compared to $201.9 million in 2016” (Dowling, 2014).

Requirement (vii):

Based on the annual report of “Virgin Australia in 2017”, it can be discerned that

organisation has suffered losses before IT in 2016 and 2017. It is clearly noted that the airline

charges of 30% on PBT has been taken into consideration to compute the net income. Despite of

this, the airline incurred significant loss due to the IT expense. Therefore, it cannot be

determined a possible reason is whether IT is calculated by the consideration of 30% tax rate on

PBIT (Beatty & Liao, 2014).

Requirement (viii):

The consideration for “deferred tax assets” are included in those situations when the firm

needs to make prepayments of taxes or additional taxes on the financial assets. On the contrary,

deferred tax liabilities are able to highlight several variations in “profit of the corporate entities

and tax in the carrying amount” (Virginaustralia.com, 2018). The deferred taxes of the airliner

have amounted “$1,017.6 million in 2017, which was depicted as $857.9 million in 2016”. On

the contrary, the “deferred tax liability” is being seen as “$463.4 million in 2017 when compared

with $434.4 million in 2016”.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

The recognition for “deferred tax assets” is considered due to the excess amount of

depreciation as an outcome of differences in taxable depreciation rate and total amount of

depreciation. Moreover, the “deferred tax liability” is incurred due to the temporary variation in

profits which were attained in both 2016 and 2017 (Henderso et al., 2015).

Requirement (ix):

The total payable amount of “current tax assets/income tax assets” is comprised of

important depictions associated to Australian business organisations. The information published

in the financial statement of Virgin Australia is evaluated in terms of “current tax assets” which

have been able to contribute to the expected amount of tax payable or receivable on the taxable

income or loss for a certain period. This is measured with the help of several tax laws and tax

rates published in the reporting year. Since it is observed that Virgin Australia obtained total IT

benefit of “$201.9 million 2016 and $103.8 million in 2017”, these amounts are reported for

reconsideration of net loss to net cash from operations in the annual report of the company. The

main rationale for this, is evaluated with non-existence of excess tax expenses on the part of

companies in both the years (Virginaustralia.com, 2018).

Requirement (x):

Referring to the annual report of 2017, it is identified that organisation did not incur any

IT in 2016 and 2017. Instead of this, it earned significant IT benefits which is the main rationale

that IT was not included in the cash flow statement (Virginaustralia.com, 2018).

Requirement (xi):

Based on the critical assessment of treatment of tax for “Virgin Australia” it is found that

the organisation suffered considerable amount of losses before incurring of IT expense in both

The recognition for “deferred tax assets” is considered due to the excess amount of

depreciation as an outcome of differences in taxable depreciation rate and total amount of

depreciation. Moreover, the “deferred tax liability” is incurred due to the temporary variation in

profits which were attained in both 2016 and 2017 (Henderso et al., 2015).

Requirement (ix):

The total payable amount of “current tax assets/income tax assets” is comprised of

important depictions associated to Australian business organisations. The information published

in the financial statement of Virgin Australia is evaluated in terms of “current tax assets” which

have been able to contribute to the expected amount of tax payable or receivable on the taxable

income or loss for a certain period. This is measured with the help of several tax laws and tax

rates published in the reporting year. Since it is observed that Virgin Australia obtained total IT

benefit of “$201.9 million 2016 and $103.8 million in 2017”, these amounts are reported for

reconsideration of net loss to net cash from operations in the annual report of the company. The

main rationale for this, is evaluated with non-existence of excess tax expenses on the part of

companies in both the years (Virginaustralia.com, 2018).

Requirement (x):

Referring to the annual report of 2017, it is identified that organisation did not incur any

IT in 2016 and 2017. Instead of this, it earned significant IT benefits which is the main rationale

that IT was not included in the cash flow statement (Virginaustralia.com, 2018).

Requirement (xi):

Based on the critical assessment of treatment of tax for “Virgin Australia” it is found that

the organisation suffered considerable amount of losses before incurring of IT expense in both

8CORPORATE ACCOUNTING

thousand 17 and 2016. Due to this, it earned significant amount of IT benefit. Due to this, it has

brought several complicacies in relating the real tax expense paid in compared to prevailing tax

rate in the country (Virginaustralia.com, 2018). Moreover, as there is no IT incurred by the

company, there is no disclosure associated to payment of IT in the cash flow statement of Virgin

Australia. By consideration of the several types of depictions made in the study can be duly

stated that IT benefits obtained by the company have been conducive in acquiring several

knowledges about tax treatment (Virginaustralia.com, 2018).

thousand 17 and 2016. Due to this, it earned significant amount of IT benefit. Due to this, it has

brought several complicacies in relating the real tax expense paid in compared to prevailing tax

rate in the country (Virginaustralia.com, 2018). Moreover, as there is no IT incurred by the

company, there is no disclosure associated to payment of IT in the cash flow statement of Virgin

Australia. By consideration of the several types of depictions made in the study can be duly

stated that IT benefits obtained by the company have been conducive in acquiring several

knowledges about tax treatment (Virginaustralia.com, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE ACCOUNTING

References

Beatty, A., & Liao, S. (2014). Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics, 58(2-3), 339-383.

Dowling, G. R. (2014). The curious case of corporate tax avoidance: Is it socially

irresponsible?. Journal of Business Ethics, 124(1), 173-184.

Dyreng, S. D., Hoopes, J. L., & Wilde, J. H. (2016). Public pressure and corporate tax

behavior. Journal of Accounting Research, 54(1), 147-186.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

Scott, W. R. (2015). Financial accounting theory (Vol. 2, No. 0, p. 0). Prentice Hall.

Taylor, G., & Richardson, G. (2014). Incentives for corporate tax planning and reporting:

Empirical evidence from Australia. Journal of Contemporary Accounting &

Economics, 10(1), 1-15.

Virginaustralia.com. (2018). [online] Available at:

https://www.virginaustralia.com/cs/groups/internetcontent/@wc/documents/

webcontent/~edisp/2017-annual-report.pdf [Accessed 19 May 2018].

Virginaustralia.com. (2018). [online] Available at:

https://www.virginaustralia.com/cs/groups/internetcontent/@wc/documents/

webcontent/~edisp/2016-annual-report.pdf [Accessed 19 May 2018].

References

Beatty, A., & Liao, S. (2014). Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics, 58(2-3), 339-383.

Dowling, G. R. (2014). The curious case of corporate tax avoidance: Is it socially

irresponsible?. Journal of Business Ethics, 124(1), 173-184.

Dyreng, S. D., Hoopes, J. L., & Wilde, J. H. (2016). Public pressure and corporate tax

behavior. Journal of Accounting Research, 54(1), 147-186.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

Scott, W. R. (2015). Financial accounting theory (Vol. 2, No. 0, p. 0). Prentice Hall.

Taylor, G., & Richardson, G. (2014). Incentives for corporate tax planning and reporting:

Empirical evidence from Australia. Journal of Contemporary Accounting &

Economics, 10(1), 1-15.

Virginaustralia.com. (2018). [online] Available at:

https://www.virginaustralia.com/cs/groups/internetcontent/@wc/documents/

webcontent/~edisp/2017-annual-report.pdf [Accessed 19 May 2018].

Virginaustralia.com. (2018). [online] Available at:

https://www.virginaustralia.com/cs/groups/internetcontent/@wc/documents/

webcontent/~edisp/2016-annual-report.pdf [Accessed 19 May 2018].

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE ACCOUNTING

Virginaustralia.com. (2018). [online] Available at:

https://www.virginaustralia.com/cs/groups/internetcontent/@wc/documents/

webcontent/~edisp/2015-annual-report.pdf [Accessed 19 May 2018].

Virginaustralia.com. (2018). [online] Available at:

https://www.virginaustralia.com/cs/groups/internetcontent/@wc/documents/

webcontent/~edisp/2014-annual-report.pdf [Accessed 19 May 2018].

Virginaustralia.com. (2018). Retrieved from

https://www.virginaustralia.com/cs/groups/internetcontent/@wc/documents/

webcontent/~edisp/2017-annual-report.pdf

Warren, C. S., & Jones, J. (2018). Corporate financial accounting. Cengage Learning.

Virginaustralia.com. (2018). [online] Available at:

https://www.virginaustralia.com/cs/groups/internetcontent/@wc/documents/

webcontent/~edisp/2015-annual-report.pdf [Accessed 19 May 2018].

Virginaustralia.com. (2018). [online] Available at:

https://www.virginaustralia.com/cs/groups/internetcontent/@wc/documents/

webcontent/~edisp/2014-annual-report.pdf [Accessed 19 May 2018].

Virginaustralia.com. (2018). Retrieved from

https://www.virginaustralia.com/cs/groups/internetcontent/@wc/documents/

webcontent/~edisp/2017-annual-report.pdf

Warren, C. S., & Jones, J. (2018). Corporate financial accounting. Cengage Learning.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.