Corporate and Financial Accounting: Consolidation Report

VerifiedAdded on 2022/11/14

|15

|3972

|59

Report

AI Summary

This report provides a detailed analysis of corporate and financial accounting principles, focusing on business combinations, consolidation accounting, and equity accounting. It examines the application of Australian Accounting Standards Board (AASB) standards, including AASB 3, AASB 10, and AASB 128, to various scenarios. The report explores the differences between consolidation and equity accounting, the treatment of intragroup transactions, and the disclosure requirements for non-controlling interests (NCI). It includes examples to illustrate the concepts and concludes with recommendations. The report is based on an assignment for the HA2032 Corporate and Financial Accounting course at Holmes Institute, focusing on corporate takeover decision-making and its effects on consolidation accounting.

Running head: Corporate and financial accounting

Corporate And Financial Accounting

Corporate And Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate and financial accounting 1

Executive Summary

AASB 3 Business Combinations was formulated with an aim to improve the comparability,

relevance and reliability of the data provided by a company in its financial records in the

context of a business combination and its impact. AASB 10 Consolidated Financial

Statements was formulated with an objective to present and prepare the consolidated

financial statements when one or more entities are controlled by an entity. AASB 128

Investments in Associates and Joint Ventures advice the accounting methods for investing in

associates along with setting the need for implementation of equity methods while accounting

for investments in joint ventures and associates. This report explains the concepts of

business combinations, various acquisition methods, non-controlling interests and intragroup

transactions along with the use of applicable accounting standards to various case studies.

Executive Summary

AASB 3 Business Combinations was formulated with an aim to improve the comparability,

relevance and reliability of the data provided by a company in its financial records in the

context of a business combination and its impact. AASB 10 Consolidated Financial

Statements was formulated with an objective to present and prepare the consolidated

financial statements when one or more entities are controlled by an entity. AASB 128

Investments in Associates and Joint Ventures advice the accounting methods for investing in

associates along with setting the need for implementation of equity methods while accounting

for investments in joint ventures and associates. This report explains the concepts of

business combinations, various acquisition methods, non-controlling interests and intragroup

transactions along with the use of applicable accounting standards to various case studies.

Corporate and financial accounting 2

Contents

Introduction...........................................................................................................................................................3

Part A....................................................................................................................................................................3

Part B....................................................................................................................................................................5

Part C.................................................................................................................................................................... 8

Recommendations/Conclusion........................................................................................................................11

References.........................................................................................................................................................12

Contents

Introduction...........................................................................................................................................................3

Part A....................................................................................................................................................................3

Part B....................................................................................................................................................................5

Part C.................................................................................................................................................................... 8

Recommendations/Conclusion........................................................................................................................11

References.........................................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate and financial accounting 3

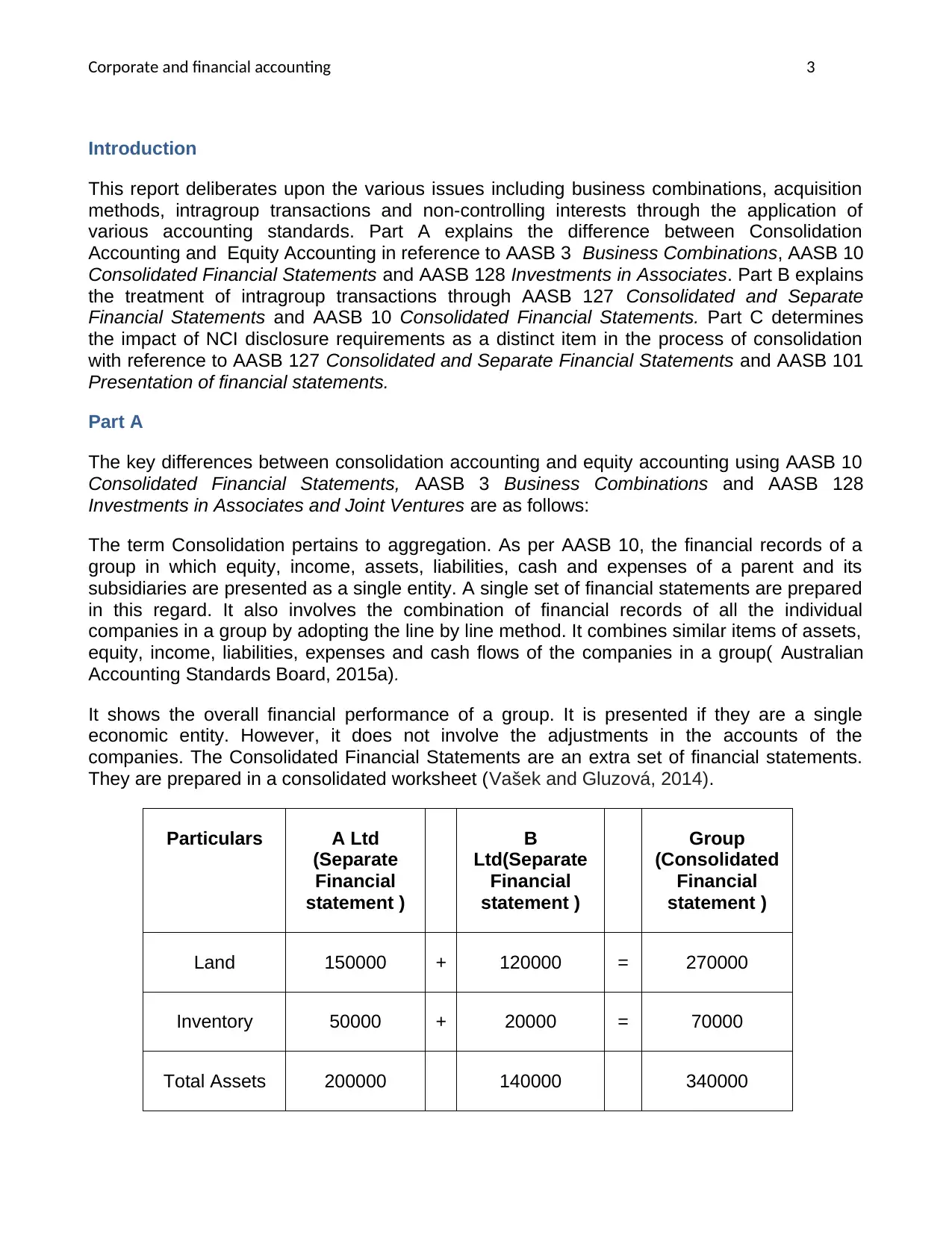

Introduction

This report deliberates upon the various issues including business combinations, acquisition

methods, intragroup transactions and non-controlling interests through the application of

various accounting standards. Part A explains the difference between Consolidation

Accounting and Equity Accounting in reference to AASB 3 Business Combinations, AASB 10

Consolidated Financial Statements and AASB 128 Investments in Associates. Part B explains

the treatment of intragroup transactions through AASB 127 Consolidated and Separate

Financial Statements and AASB 10 Consolidated Financial Statements. Part C determines

the impact of NCI disclosure requirements as a distinct item in the process of consolidation

with reference to AASB 127 Consolidated and Separate Financial Statements and AASB 101

Presentation of financial statements.

Part A

The key differences between consolidation accounting and equity accounting using AASB 10

Consolidated Financial Statements, AASB 3 Business Combinations and AASB 128

Investments in Associates and Joint Ventures are as follows:

The term Consolidation pertains to aggregation. As per AASB 10, the financial records of a

group in which equity, income, assets, liabilities, cash and expenses of a parent and its

subsidiaries are presented as a single entity. A single set of financial statements are prepared

in this regard. It also involves the combination of financial records of all the individual

companies in a group by adopting the line by line method. It combines similar items of assets,

equity, income, liabilities, expenses and cash flows of the companies in a group( Australian

Accounting Standards Board, 2015a).

It shows the overall financial performance of a group. It is presented if they are a single

economic entity. However, it does not involve the adjustments in the accounts of the

companies. The Consolidated Financial Statements are an extra set of financial statements.

They are prepared in a consolidated worksheet (Vašek and Gluzová, 2014).

Particulars A Ltd

(Separate

Financial

statement )

B

Ltd(Separate

Financial

statement )

Group

(Consolidated

Financial

statement )

Land 150000 + 120000 = 270000

Inventory 50000 + 20000 = 70000

Total Assets 200000 140000 340000

Introduction

This report deliberates upon the various issues including business combinations, acquisition

methods, intragroup transactions and non-controlling interests through the application of

various accounting standards. Part A explains the difference between Consolidation

Accounting and Equity Accounting in reference to AASB 3 Business Combinations, AASB 10

Consolidated Financial Statements and AASB 128 Investments in Associates. Part B explains

the treatment of intragroup transactions through AASB 127 Consolidated and Separate

Financial Statements and AASB 10 Consolidated Financial Statements. Part C determines

the impact of NCI disclosure requirements as a distinct item in the process of consolidation

with reference to AASB 127 Consolidated and Separate Financial Statements and AASB 101

Presentation of financial statements.

Part A

The key differences between consolidation accounting and equity accounting using AASB 10

Consolidated Financial Statements, AASB 3 Business Combinations and AASB 128

Investments in Associates and Joint Ventures are as follows:

The term Consolidation pertains to aggregation. As per AASB 10, the financial records of a

group in which equity, income, assets, liabilities, cash and expenses of a parent and its

subsidiaries are presented as a single entity. A single set of financial statements are prepared

in this regard. It also involves the combination of financial records of all the individual

companies in a group by adopting the line by line method. It combines similar items of assets,

equity, income, liabilities, expenses and cash flows of the companies in a group( Australian

Accounting Standards Board, 2015a).

It shows the overall financial performance of a group. It is presented if they are a single

economic entity. However, it does not involve the adjustments in the accounts of the

companies. The Consolidated Financial Statements are an extra set of financial statements.

They are prepared in a consolidated worksheet (Vašek and Gluzová, 2014).

Particulars A Ltd

(Separate

Financial

statement )

B

Ltd(Separate

Financial

statement )

Group

(Consolidated

Financial

statement )

Land 150000 + 120000 = 270000

Inventory 50000 + 20000 = 70000

Total Assets 200000 140000 340000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate and financial accounting 4

Borrowings (80000) + (30000) = (110000)

Net Assets 120000 110000 230000

The equity method is used by the companies to evaluate the profits earned through their

investments in another company. The companies report the earned income on their

investments in their income statements.The reported value is dependent upon the share of

the firm in assets of the company. The reported value is proportionate to the total investments

in equity. AASB 128 Investments in Associates and Joint Ventures explains the concept of

equity accounting. The equity method recognizes the investment in an associate or joint

venture at its cost. The carrying amount is adjusted to analyze investor's share in the profit or

loss of the investee subsequent to the acquisition date (Australian Accounting Standards

Board, 2015b).

The share of the investor in the profit and loss of investee is known as the profit and loss of

investor. The distributions which are received from the investee decrease the carrying amount

of investments.However, the acknowledgment of income on the basis of distribution is not an

appropriate measure for income received by the investor as the distribution has a little or no

relation to the performance of the joint and associated venture( Grossi, 2014). It can be

explained with the help of an example.

If JKY Ltd has 50% controlling interest over FAB Ltd, JKY Ltd would record its investments at

50% of the revenues, assets, liabilities and expenses of FAB Ltd. So, if JKY Ltd has a total

revenue of $100 Million and FAB Ltd has a revenue of $40 Million, then JKY Ltd shall have a

total revenue of $120 Million. Those who the consolidation method of accounting debate that

it provides a more precise and comprehensive record as the true performance of a joint

venture is revealed. It allows each of the firms to analyze their operational effectiveness in the

context of production, shipping costs and the profits.

As per AASB 3 Business Combinations, a business combination is a common control

combination if the combining companies are regulated by one party before and after the

combinations. Moreover, the common control should be permanent (Australian Accounting

Standards Board, 2014). A business combination may be formulated as a result of a parent

entity relationship in which the acquirer is termed as a parent and acquiree is a subsidiary.

The acquirer implements this standard in its consolidated financial statements.It comprises of

the interest of acquirer in the acquiree in its separate financial statements which is

represented by its investment in the subordinate company (CPA Australia, 2015).

Borrowings (80000) + (30000) = (110000)

Net Assets 120000 110000 230000

The equity method is used by the companies to evaluate the profits earned through their

investments in another company. The companies report the earned income on their

investments in their income statements.The reported value is dependent upon the share of

the firm in assets of the company. The reported value is proportionate to the total investments

in equity. AASB 128 Investments in Associates and Joint Ventures explains the concept of

equity accounting. The equity method recognizes the investment in an associate or joint

venture at its cost. The carrying amount is adjusted to analyze investor's share in the profit or

loss of the investee subsequent to the acquisition date (Australian Accounting Standards

Board, 2015b).

The share of the investor in the profit and loss of investee is known as the profit and loss of

investor. The distributions which are received from the investee decrease the carrying amount

of investments.However, the acknowledgment of income on the basis of distribution is not an

appropriate measure for income received by the investor as the distribution has a little or no

relation to the performance of the joint and associated venture( Grossi, 2014). It can be

explained with the help of an example.

If JKY Ltd has 50% controlling interest over FAB Ltd, JKY Ltd would record its investments at

50% of the revenues, assets, liabilities and expenses of FAB Ltd. So, if JKY Ltd has a total

revenue of $100 Million and FAB Ltd has a revenue of $40 Million, then JKY Ltd shall have a

total revenue of $120 Million. Those who the consolidation method of accounting debate that

it provides a more precise and comprehensive record as the true performance of a joint

venture is revealed. It allows each of the firms to analyze their operational effectiveness in the

context of production, shipping costs and the profits.

As per AASB 3 Business Combinations, a business combination is a common control

combination if the combining companies are regulated by one party before and after the

combinations. Moreover, the common control should be permanent (Australian Accounting

Standards Board, 2014). A business combination may be formulated as a result of a parent

entity relationship in which the acquirer is termed as a parent and acquiree is a subsidiary.

The acquirer implements this standard in its consolidated financial statements.It comprises of

the interest of acquirer in the acquiree in its separate financial statements which is

represented by its investment in the subordinate company (CPA Australia, 2015).

Corporate and financial accounting 5

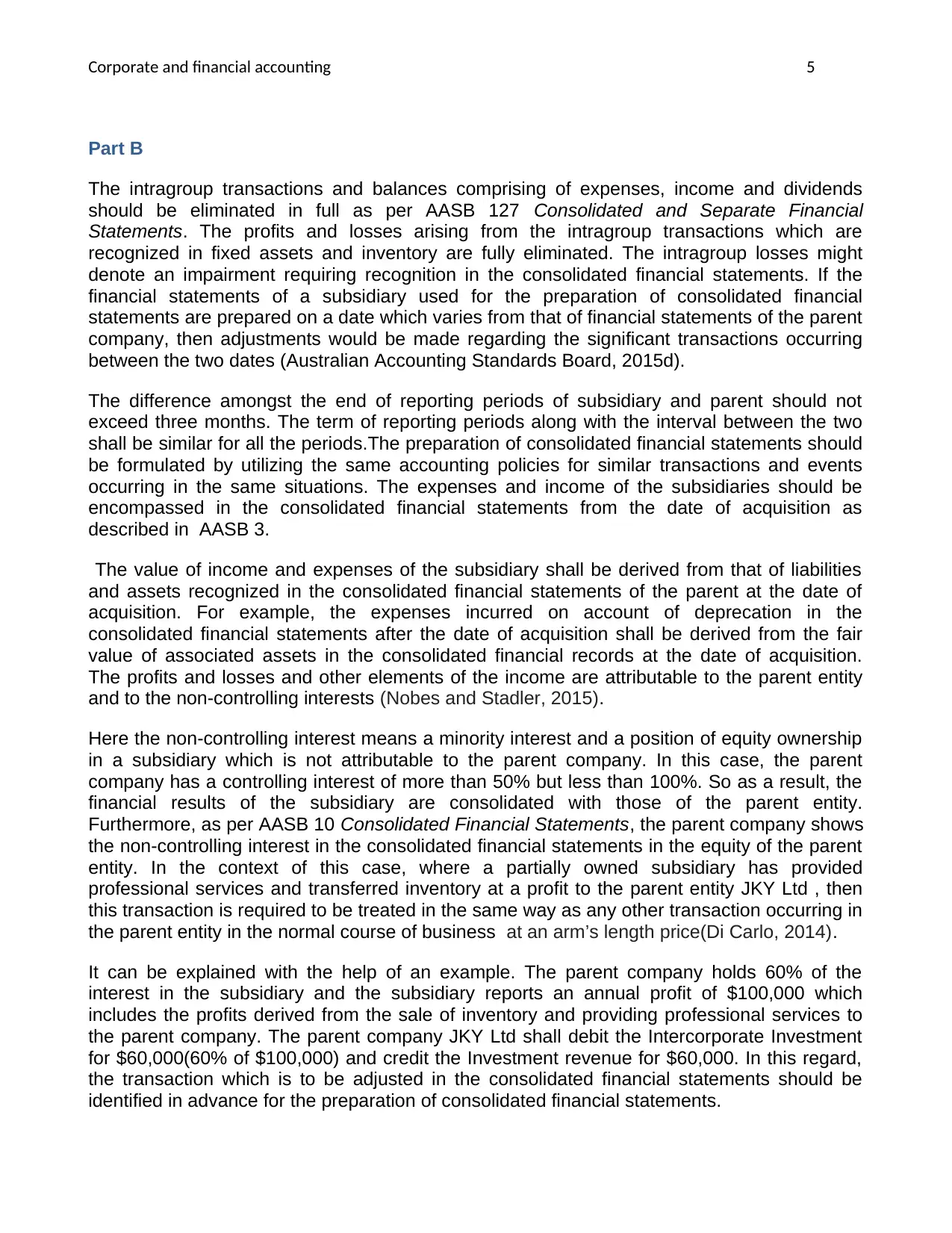

Part B

The intragroup transactions and balances comprising of expenses, income and dividends

should be eliminated in full as per AASB 127 Consolidated and Separate Financial

Statements. The profits and losses arising from the intragroup transactions which are

recognized in fixed assets and inventory are fully eliminated. The intragroup losses might

denote an impairment requiring recognition in the consolidated financial statements. If the

financial statements of a subsidiary used for the preparation of consolidated financial

statements are prepared on a date which varies from that of financial statements of the parent

company, then adjustments would be made regarding the significant transactions occurring

between the two dates (Australian Accounting Standards Board, 2015d).

The difference amongst the end of reporting periods of subsidiary and parent should not

exceed three months. The term of reporting periods along with the interval between the two

shall be similar for all the periods.The preparation of consolidated financial statements should

be formulated by utilizing the same accounting policies for similar transactions and events

occurring in the same situations. The expenses and income of the subsidiaries should be

encompassed in the consolidated financial statements from the date of acquisition as

described in AASB 3.

The value of income and expenses of the subsidiary shall be derived from that of liabilities

and assets recognized in the consolidated financial statements of the parent at the date of

acquisition. For example, the expenses incurred on account of deprecation in the

consolidated financial statements after the date of acquisition shall be derived from the fair

value of associated assets in the consolidated financial records at the date of acquisition.

The profits and losses and other elements of the income are attributable to the parent entity

and to the non-controlling interests (Nobes and Stadler, 2015).

Here the non-controlling interest means a minority interest and a position of equity ownership

in a subsidiary which is not attributable to the parent company. In this case, the parent

company has a controlling interest of more than 50% but less than 100%. So as a result, the

financial results of the subsidiary are consolidated with those of the parent entity.

Furthermore, as per AASB 10 Consolidated Financial Statements, the parent company shows

the non-controlling interest in the consolidated financial statements in the equity of the parent

entity. In the context of this case, where a partially owned subsidiary has provided

professional services and transferred inventory at a profit to the parent entity JKY Ltd , then

this transaction is required to be treated in the same way as any other transaction occurring in

the parent entity in the normal course of business at an arm’s length price(Di Carlo, 2014).

It can be explained with the help of an example. The parent company holds 60% of the

interest in the subsidiary and the subsidiary reports an annual profit of $100,000 which

includes the profits derived from the sale of inventory and providing professional services to

the parent company. The parent company JKY Ltd shall debit the Intercorporate Investment

for $60,000(60% of $100,000) and credit the Investment revenue for $60,000. In this regard,

the transaction which is to be adjusted in the consolidated financial statements should be

identified in advance for the preparation of consolidated financial statements.

Part B

The intragroup transactions and balances comprising of expenses, income and dividends

should be eliminated in full as per AASB 127 Consolidated and Separate Financial

Statements. The profits and losses arising from the intragroup transactions which are

recognized in fixed assets and inventory are fully eliminated. The intragroup losses might

denote an impairment requiring recognition in the consolidated financial statements. If the

financial statements of a subsidiary used for the preparation of consolidated financial

statements are prepared on a date which varies from that of financial statements of the parent

company, then adjustments would be made regarding the significant transactions occurring

between the two dates (Australian Accounting Standards Board, 2015d).

The difference amongst the end of reporting periods of subsidiary and parent should not

exceed three months. The term of reporting periods along with the interval between the two

shall be similar for all the periods.The preparation of consolidated financial statements should

be formulated by utilizing the same accounting policies for similar transactions and events

occurring in the same situations. The expenses and income of the subsidiaries should be

encompassed in the consolidated financial statements from the date of acquisition as

described in AASB 3.

The value of income and expenses of the subsidiary shall be derived from that of liabilities

and assets recognized in the consolidated financial statements of the parent at the date of

acquisition. For example, the expenses incurred on account of deprecation in the

consolidated financial statements after the date of acquisition shall be derived from the fair

value of associated assets in the consolidated financial records at the date of acquisition.

The profits and losses and other elements of the income are attributable to the parent entity

and to the non-controlling interests (Nobes and Stadler, 2015).

Here the non-controlling interest means a minority interest and a position of equity ownership

in a subsidiary which is not attributable to the parent company. In this case, the parent

company has a controlling interest of more than 50% but less than 100%. So as a result, the

financial results of the subsidiary are consolidated with those of the parent entity.

Furthermore, as per AASB 10 Consolidated Financial Statements, the parent company shows

the non-controlling interest in the consolidated financial statements in the equity of the parent

entity. In the context of this case, where a partially owned subsidiary has provided

professional services and transferred inventory at a profit to the parent entity JKY Ltd , then

this transaction is required to be treated in the same way as any other transaction occurring in

the parent entity in the normal course of business at an arm’s length price(Di Carlo, 2014).

It can be explained with the help of an example. The parent company holds 60% of the

interest in the subsidiary and the subsidiary reports an annual profit of $100,000 which

includes the profits derived from the sale of inventory and providing professional services to

the parent company. The parent company JKY Ltd shall debit the Intercorporate Investment

for $60,000(60% of $100,000) and credit the Investment revenue for $60,000. In this regard,

the transaction which is to be adjusted in the consolidated financial statements should be

identified in advance for the preparation of consolidated financial statements.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate and financial accounting 6

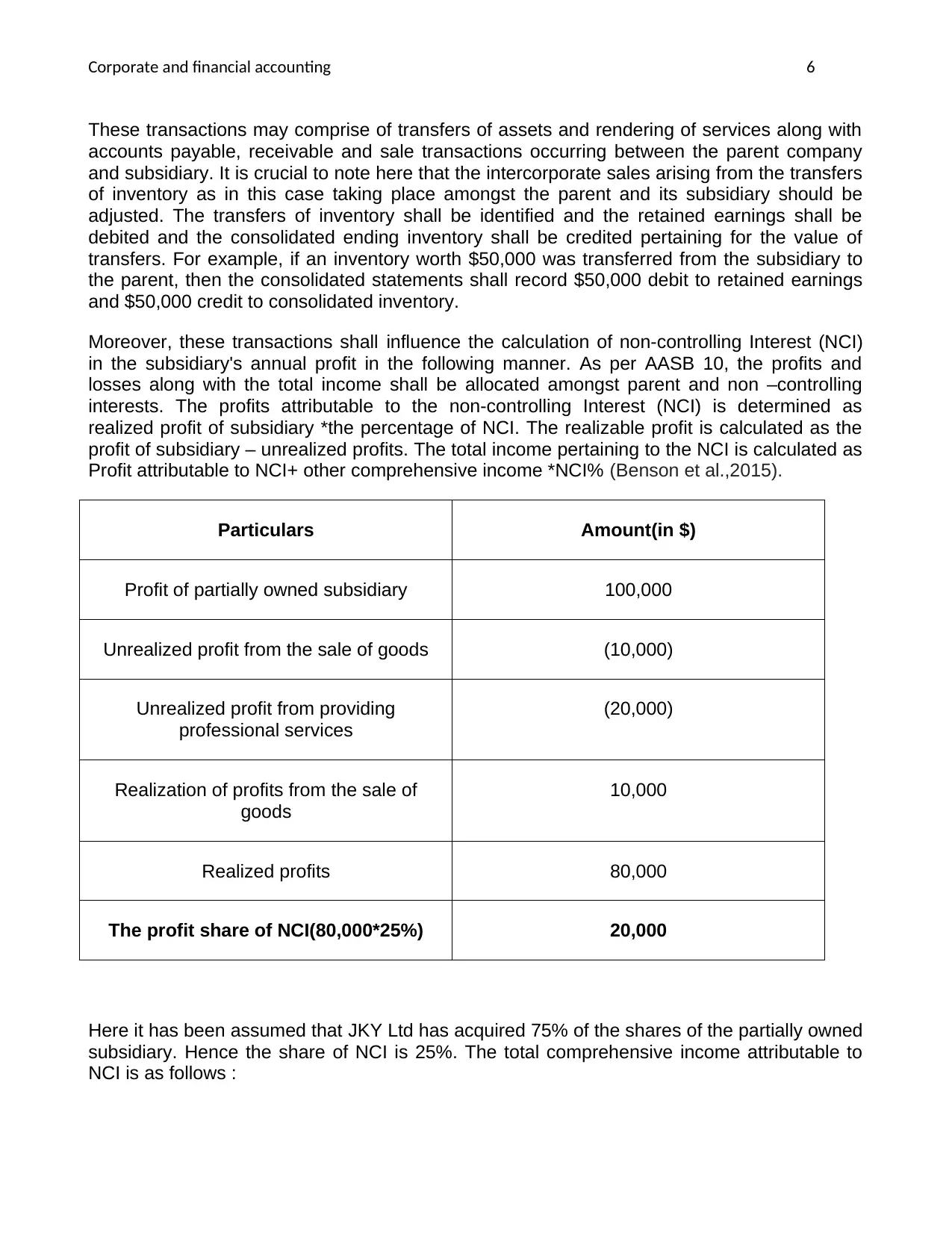

These transactions may comprise of transfers of assets and rendering of services along with

accounts payable, receivable and sale transactions occurring between the parent company

and subsidiary. It is crucial to note here that the intercorporate sales arising from the transfers

of inventory as in this case taking place amongst the parent and its subsidiary should be

adjusted. The transfers of inventory shall be identified and the retained earnings shall be

debited and the consolidated ending inventory shall be credited pertaining for the value of

transfers. For example, if an inventory worth $50,000 was transferred from the subsidiary to

the parent, then the consolidated statements shall record $50,000 debit to retained earnings

and $50,000 credit to consolidated inventory.

Moreover, these transactions shall influence the calculation of non-controlling Interest (NCI)

in the subsidiary's annual profit in the following manner. As per AASB 10, the profits and

losses along with the total income shall be allocated amongst parent and non –controlling

interests. The profits attributable to the non-controlling Interest (NCI) is determined as

realized profit of subsidiary *the percentage of NCI. The realizable profit is calculated as the

profit of subsidiary – unrealized profits. The total income pertaining to the NCI is calculated as

Profit attributable to NCI+ other comprehensive income *NCI% (Benson et al.,2015).

Particulars Amount(in $)

Profit of partially owned subsidiary 100,000

Unrealized profit from the sale of goods (10,000)

Unrealized profit from providing

professional services

(20,000)

Realization of profits from the sale of

goods

10,000

Realized profits 80,000

The profit share of NCI(80,000*25%) 20,000

Here it has been assumed that JKY Ltd has acquired 75% of the shares of the partially owned

subsidiary. Hence the share of NCI is 25%. The total comprehensive income attributable to

NCI is as follows :

These transactions may comprise of transfers of assets and rendering of services along with

accounts payable, receivable and sale transactions occurring between the parent company

and subsidiary. It is crucial to note here that the intercorporate sales arising from the transfers

of inventory as in this case taking place amongst the parent and its subsidiary should be

adjusted. The transfers of inventory shall be identified and the retained earnings shall be

debited and the consolidated ending inventory shall be credited pertaining for the value of

transfers. For example, if an inventory worth $50,000 was transferred from the subsidiary to

the parent, then the consolidated statements shall record $50,000 debit to retained earnings

and $50,000 credit to consolidated inventory.

Moreover, these transactions shall influence the calculation of non-controlling Interest (NCI)

in the subsidiary's annual profit in the following manner. As per AASB 10, the profits and

losses along with the total income shall be allocated amongst parent and non –controlling

interests. The profits attributable to the non-controlling Interest (NCI) is determined as

realized profit of subsidiary *the percentage of NCI. The realizable profit is calculated as the

profit of subsidiary – unrealized profits. The total income pertaining to the NCI is calculated as

Profit attributable to NCI+ other comprehensive income *NCI% (Benson et al.,2015).

Particulars Amount(in $)

Profit of partially owned subsidiary 100,000

Unrealized profit from the sale of goods (10,000)

Unrealized profit from providing

professional services

(20,000)

Realization of profits from the sale of

goods

10,000

Realized profits 80,000

The profit share of NCI(80,000*25%) 20,000

Here it has been assumed that JKY Ltd has acquired 75% of the shares of the partially owned

subsidiary. Hence the share of NCI is 25%. The total comprehensive income attributable to

NCI is as follows :

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate and financial accounting 7

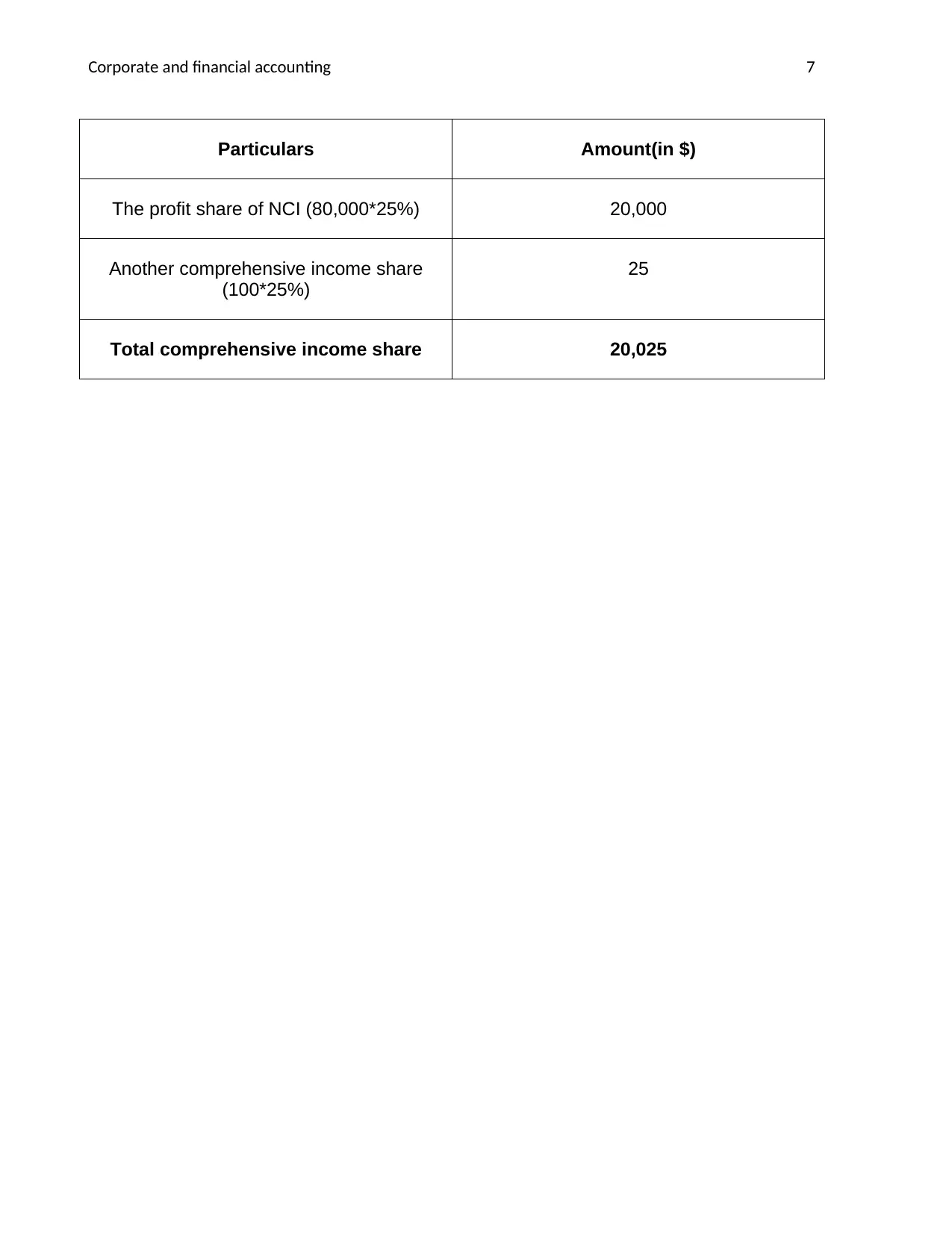

Particulars Amount(in $)

The profit share of NCI (80,000*25%) 20,000

Another comprehensive income share

(100*25%)

25

Total comprehensive income share 20,025

Particulars Amount(in $)

The profit share of NCI (80,000*25%) 20,000

Another comprehensive income share

(100*25%)

25

Total comprehensive income share 20,025

Corporate and financial accounting 8

Part C

As per AASB 127 Consolidated and Separate Financial Statements and AASB 101

Presentation of Financial Statements, with regards to the disclosure requirements of NCI as a

distinct item in the consolidation process, the materiality should be evaluated by the parent

entity on the basis of its consolidated financial records. The parent entity should determine

both qualitative aspects such as the nature of subsidiary and qualitative aspects like the size

of a subsidiary. As per the disclosure requirements, the parent entity shall reveal the

information which assists the users of consolidated financial statements to comprehend the

structure of the group. It should also enable them to understand the stake of non-controlling

interests in the activities of the group along with the cash flows (Australian Accounting

Standards Board, 2015c).

The parent entity shall disclose the material NCI of each of its subsidiaries separately in the

consolidation process. The disclosure requirements shall be met by the parent entity by

revealing the disaggregated data from the values included in the consolidated financial

statements of the parent entity. It should be done in the context of subsidiaries having a non-

controlling interest material to the parent entity. In this context, the reporting entity shall apply

its judgment for considering the amount of disaggregation of this data if the parent entity

presenting the data about the subsidiary having a substantial controlling interest (Nobes,

2014).

The required information should be presented on the basis of the subsidiary with the

investees. Furthermore, it also necessitates in accomplishing the requirements of disclosure

to segregate the information to be presented about the individual subsidiaries which have a

substantial non-controlling interest within the group. The parent entity shall also reveal the

summarized balance sheet and other financial statements about the liabilities, assets, profits,

losses and cash flows of its subsidiaries which assist the users to contemplate about the

subsidiaries having the non-controlling interests in the activities of the group along with the

cash flows (Alayemi,2015).

Moreover, with regards to the allocation of other comprehensive profit to the NCI, the parent

entity should categorize and evaluate those profits in the consolidated financial statements on

the basis of their economic substantiality. As a result, these profits shall be accordingly

classified as non-controlling interests in the financial statements of a parent entity. If these

profits do not possess the characteristics of materiality, then they would not be classified as

non-controlling interests. In such cases, the parent entity shall categorize the comprehensive

profit as a profit-sharing arrangement instead as a no controlling interest (Ignatowski and

Zatoń, 2015).

With regards to the valuation of assets, AASB 101 Presentation of Financial Statements

states that the entity should measure the fair value of assets and liabilities as per AASB 13

Fair Value Measurement.The fair value measurement considers the ability of the participants

in the market to utilize the assets at their best. Also, if any financial asset is reclassified out of

the category of amortized cost measurement so it is evaluated at its fair value through profit

or loss and any profits arising from the differences between the earlier amortized costs of the

Part C

As per AASB 127 Consolidated and Separate Financial Statements and AASB 101

Presentation of Financial Statements, with regards to the disclosure requirements of NCI as a

distinct item in the consolidation process, the materiality should be evaluated by the parent

entity on the basis of its consolidated financial records. The parent entity should determine

both qualitative aspects such as the nature of subsidiary and qualitative aspects like the size

of a subsidiary. As per the disclosure requirements, the parent entity shall reveal the

information which assists the users of consolidated financial statements to comprehend the

structure of the group. It should also enable them to understand the stake of non-controlling

interests in the activities of the group along with the cash flows (Australian Accounting

Standards Board, 2015c).

The parent entity shall disclose the material NCI of each of its subsidiaries separately in the

consolidation process. The disclosure requirements shall be met by the parent entity by

revealing the disaggregated data from the values included in the consolidated financial

statements of the parent entity. It should be done in the context of subsidiaries having a non-

controlling interest material to the parent entity. In this context, the reporting entity shall apply

its judgment for considering the amount of disaggregation of this data if the parent entity

presenting the data about the subsidiary having a substantial controlling interest (Nobes,

2014).

The required information should be presented on the basis of the subsidiary with the

investees. Furthermore, it also necessitates in accomplishing the requirements of disclosure

to segregate the information to be presented about the individual subsidiaries which have a

substantial non-controlling interest within the group. The parent entity shall also reveal the

summarized balance sheet and other financial statements about the liabilities, assets, profits,

losses and cash flows of its subsidiaries which assist the users to contemplate about the

subsidiaries having the non-controlling interests in the activities of the group along with the

cash flows (Alayemi,2015).

Moreover, with regards to the allocation of other comprehensive profit to the NCI, the parent

entity should categorize and evaluate those profits in the consolidated financial statements on

the basis of their economic substantiality. As a result, these profits shall be accordingly

classified as non-controlling interests in the financial statements of a parent entity. If these

profits do not possess the characteristics of materiality, then they would not be classified as

non-controlling interests. In such cases, the parent entity shall categorize the comprehensive

profit as a profit-sharing arrangement instead as a no controlling interest (Ignatowski and

Zatoń, 2015).

With regards to the valuation of assets, AASB 101 Presentation of Financial Statements

states that the entity should measure the fair value of assets and liabilities as per AASB 13

Fair Value Measurement.The fair value measurement considers the ability of the participants

in the market to utilize the assets at their best. Also, if any financial asset is reclassified out of

the category of amortized cost measurement so it is evaluated at its fair value through profit

or loss and any profits arising from the differences between the earlier amortized costs of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate and financial accounting 9

financial assets and their fair value should be at the reclassification date (Sotti, Rinaldi and

Gavana, 2015).

financial assets and their fair value should be at the reclassification date (Sotti, Rinaldi and

Gavana, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate and financial accounting 10

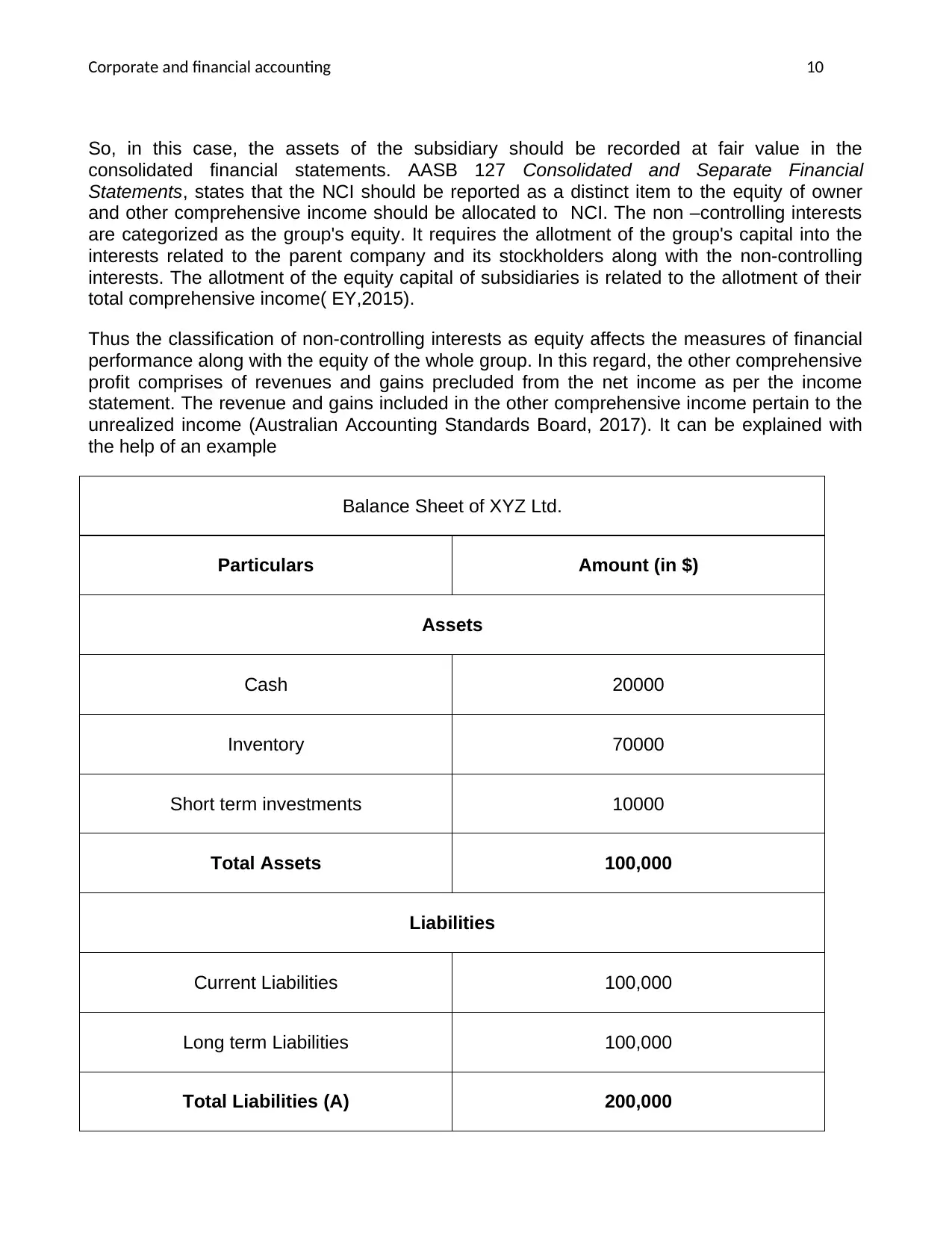

So, in this case, the assets of the subsidiary should be recorded at fair value in the

consolidated financial statements. AASB 127 Consolidated and Separate Financial

Statements, states that the NCI should be reported as a distinct item to the equity of owner

and other comprehensive income should be allocated to NCI. The non –controlling interests

are categorized as the group's equity. It requires the allotment of the group's capital into the

interests related to the parent company and its stockholders along with the non-controlling

interests. The allotment of the equity capital of subsidiaries is related to the allotment of their

total comprehensive income( EY,2015).

Thus the classification of non-controlling interests as equity affects the measures of financial

performance along with the equity of the whole group. In this regard, the other comprehensive

profit comprises of revenues and gains precluded from the net income as per the income

statement. The revenue and gains included in the other comprehensive income pertain to the

unrealized income (Australian Accounting Standards Board, 2017). It can be explained with

the help of an example

Balance Sheet of XYZ Ltd.

Particulars Amount (in $)

Assets

Cash 20000

Inventory 70000

Short term investments 10000

Total Assets 100,000

Liabilities

Current Liabilities 100,000

Long term Liabilities 100,000

Total Liabilities (A) 200,000

So, in this case, the assets of the subsidiary should be recorded at fair value in the

consolidated financial statements. AASB 127 Consolidated and Separate Financial

Statements, states that the NCI should be reported as a distinct item to the equity of owner

and other comprehensive income should be allocated to NCI. The non –controlling interests

are categorized as the group's equity. It requires the allotment of the group's capital into the

interests related to the parent company and its stockholders along with the non-controlling

interests. The allotment of the equity capital of subsidiaries is related to the allotment of their

total comprehensive income( EY,2015).

Thus the classification of non-controlling interests as equity affects the measures of financial

performance along with the equity of the whole group. In this regard, the other comprehensive

profit comprises of revenues and gains precluded from the net income as per the income

statement. The revenue and gains included in the other comprehensive income pertain to the

unrealized income (Australian Accounting Standards Board, 2017). It can be explained with

the help of an example

Balance Sheet of XYZ Ltd.

Particulars Amount (in $)

Assets

Cash 20000

Inventory 70000

Short term investments 10000

Total Assets 100,000

Liabilities

Current Liabilities 100,000

Long term Liabilities 100,000

Total Liabilities (A) 200,000

Corporate and financial accounting 11

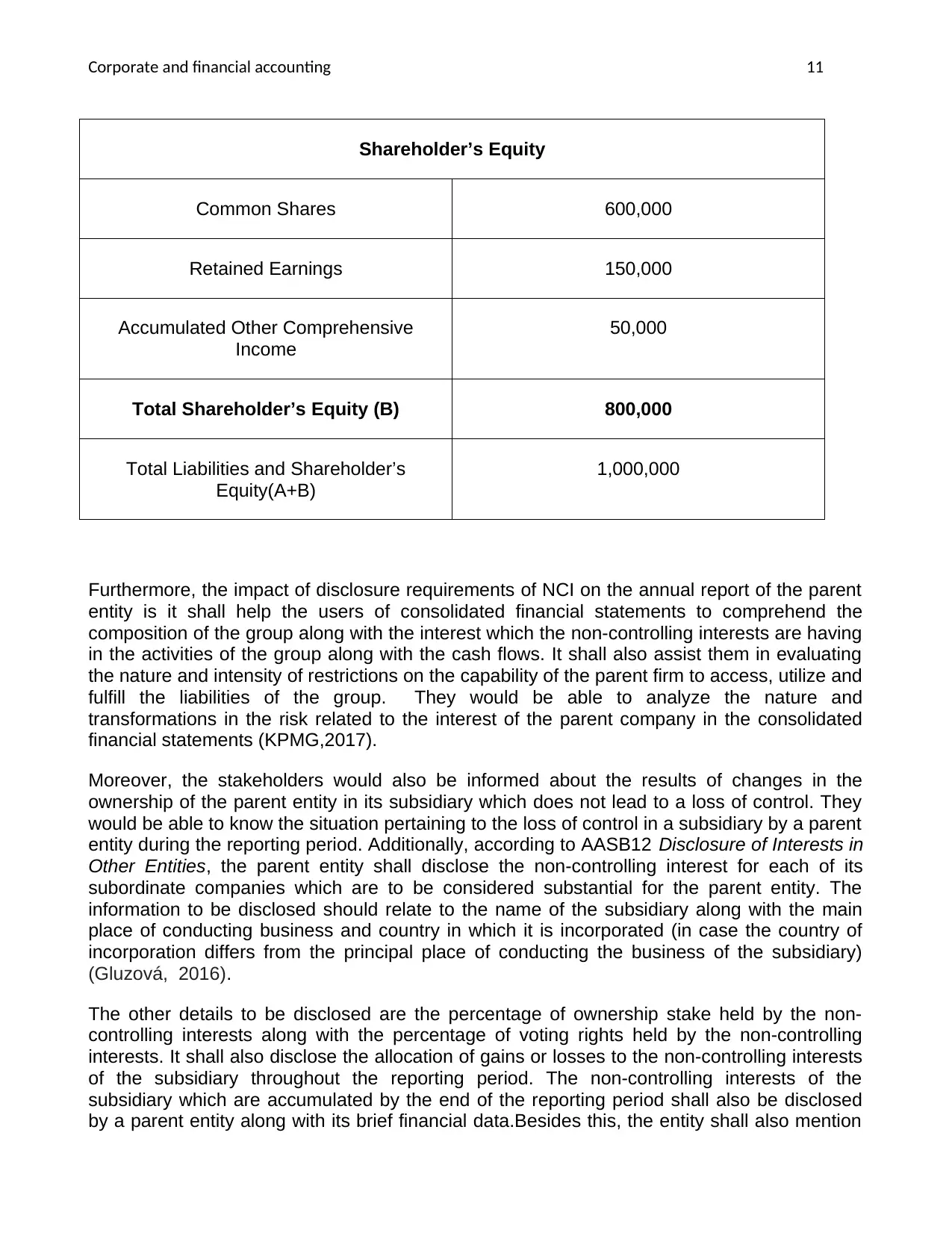

Shareholder’s Equity

Common Shares 600,000

Retained Earnings 150,000

Accumulated Other Comprehensive

Income

50,000

Total Shareholder’s Equity (B) 800,000

Total Liabilities and Shareholder’s

Equity(A+B)

1,000,000

Furthermore, the impact of disclosure requirements of NCI on the annual report of the parent

entity is it shall help the users of consolidated financial statements to comprehend the

composition of the group along with the interest which the non-controlling interests are having

in the activities of the group along with the cash flows. It shall also assist them in evaluating

the nature and intensity of restrictions on the capability of the parent firm to access, utilize and

fulfill the liabilities of the group. They would be able to analyze the nature and

transformations in the risk related to the interest of the parent company in the consolidated

financial statements (KPMG,2017).

Moreover, the stakeholders would also be informed about the results of changes in the

ownership of the parent entity in its subsidiary which does not lead to a loss of control. They

would be able to know the situation pertaining to the loss of control in a subsidiary by a parent

entity during the reporting period. Additionally, according to AASB12 Disclosure of Interests in

Other Entities, the parent entity shall disclose the non-controlling interest for each of its

subordinate companies which are to be considered substantial for the parent entity. The

information to be disclosed should relate to the name of the subsidiary along with the main

place of conducting business and country in which it is incorporated (in case the country of

incorporation differs from the principal place of conducting the business of the subsidiary)

(Gluzová, 2016).

The other details to be disclosed are the percentage of ownership stake held by the non-

controlling interests along with the percentage of voting rights held by the non-controlling

interests. It shall also disclose the allocation of gains or losses to the non-controlling interests

of the subsidiary throughout the reporting period. The non-controlling interests of the

subsidiary which are accumulated by the end of the reporting period shall also be disclosed

by a parent entity along with its brief financial data.Besides this, the entity shall also mention

Shareholder’s Equity

Common Shares 600,000

Retained Earnings 150,000

Accumulated Other Comprehensive

Income

50,000

Total Shareholder’s Equity (B) 800,000

Total Liabilities and Shareholder’s

Equity(A+B)

1,000,000

Furthermore, the impact of disclosure requirements of NCI on the annual report of the parent

entity is it shall help the users of consolidated financial statements to comprehend the

composition of the group along with the interest which the non-controlling interests are having

in the activities of the group along with the cash flows. It shall also assist them in evaluating

the nature and intensity of restrictions on the capability of the parent firm to access, utilize and

fulfill the liabilities of the group. They would be able to analyze the nature and

transformations in the risk related to the interest of the parent company in the consolidated

financial statements (KPMG,2017).

Moreover, the stakeholders would also be informed about the results of changes in the

ownership of the parent entity in its subsidiary which does not lead to a loss of control. They

would be able to know the situation pertaining to the loss of control in a subsidiary by a parent

entity during the reporting period. Additionally, according to AASB12 Disclosure of Interests in

Other Entities, the parent entity shall disclose the non-controlling interest for each of its

subordinate companies which are to be considered substantial for the parent entity. The

information to be disclosed should relate to the name of the subsidiary along with the main

place of conducting business and country in which it is incorporated (in case the country of

incorporation differs from the principal place of conducting the business of the subsidiary)

(Gluzová, 2016).

The other details to be disclosed are the percentage of ownership stake held by the non-

controlling interests along with the percentage of voting rights held by the non-controlling

interests. It shall also disclose the allocation of gains or losses to the non-controlling interests

of the subsidiary throughout the reporting period. The non-controlling interests of the

subsidiary which are accumulated by the end of the reporting period shall also be disclosed

by a parent entity along with its brief financial data.Besides this, the entity shall also mention

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.