Corporate and Financial Accounting Report: ASX Companies Analysis

VerifiedAdded on 2023/06/04

|13

|2866

|248

Report

AI Summary

This report provides a comprehensive analysis of corporate and financial accounting. It begins with an executive summary and introduction, followed by a discussion on corporate regulation, including the critical analysis of financial reporting and accounting regulation, and the importance of standardized information for various stakeholders. The report then delves into the accounting standard-setting process, specifically focusing on the Australian Accounting Standards Board (AASB) and its role in global standard-setting. It also explains the reasons why International Financial Reporting Standards (IFRS) are not mandatory for all IASB member countries. The core of the report analyzes the owner's equity of four selected companies from the Australian Stock Exchange (ASX): Aguia Resources Limited, Alliance Resources Limited, Bauxite Resources Limited, and Jupiter Mines Limited. It examines the contributed equity, reserves, retained earnings, and accumulated losses of each company over several years. Finally, the report conducts a comparative analysis of the debt and equity positions of the chosen companies, highlighting their financial structures and performance, before concluding with a summary of findings and a list of references.

Running head: CORPORATE AND FINANCIAL ACCOUNTING

Corporate and financial accounting

Name of the Student:

Name of the University:

Author’s Note:

Corporate and financial accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE AND FINANCIAL ACCOUNTING

Executive summary:

The report has been divided into three sections consisting of corporate regulation, standard

setting process and owner’s equity. In addition to this, report also elucidates the comparative

analysis of debt and equity position of the public listed companies operating in the same sector.

The companies that have been chose from the ASX includes Bauxite mineral resources, Alliance

resources limited, Aguia resources limited and Jupiter mines limited. Separate analysis of each

items of equity of all the companies have been done along with comparative analysis of equity

and debt position.

Executive summary:

The report has been divided into three sections consisting of corporate regulation, standard

setting process and owner’s equity. In addition to this, report also elucidates the comparative

analysis of debt and equity position of the public listed companies operating in the same sector.

The companies that have been chose from the ASX includes Bauxite mineral resources, Alliance

resources limited, Aguia resources limited and Jupiter mines limited. Separate analysis of each

items of equity of all the companies have been done along with comparative analysis of equity

and debt position.

2CORPORATE AND FINANCIAL ACCOUNTING

Table of Contents

Introduction:....................................................................................................................................3

Discussion:.......................................................................................................................................3

Corporate regulation:.......................................................................................................................3

Critical analysis of financial reporting and accounting regulation:.................................................3

Explanation of setting process of global accounting standard of Australian accounting standard

board:...............................................................................................................................................5

Explanation of why IFRS is not mandatory for IASB member countries:......................................6

Analysis of owner’s equity of four selected companies:.................................................................6

Comparative analysis of debt and equity position of chosen companies:.......................................9

Conclusion:....................................................................................................................................10

References and Bibliography list:..................................................................................................11

Table of Contents

Introduction:....................................................................................................................................3

Discussion:.......................................................................................................................................3

Corporate regulation:.......................................................................................................................3

Critical analysis of financial reporting and accounting regulation:.................................................3

Explanation of setting process of global accounting standard of Australian accounting standard

board:...............................................................................................................................................5

Explanation of why IFRS is not mandatory for IASB member countries:......................................6

Analysis of owner’s equity of four selected companies:.................................................................6

Comparative analysis of debt and equity position of chosen companies:.......................................9

Conclusion:....................................................................................................................................10

References and Bibliography list:..................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE AND FINANCIAL ACCOUNTING

Introduction:

The current paper has been prepared for addressing the importance of regulation of

financial reporting and assessment of voluntarily disclosure of information by managers. The

process of standard setting at the global level by the international accounting standard has been

analyzed in the report. For the analysis of owner’s equity, four companies have been selected

from the Australian stock exchanges namely Alliance resources limited, Aguia resources limited,

Jupiter mines limited and Bauxite resources limited. Aguia resource limited is a company based

in Australia with its primary focus on the development and exploration of mineral resources in

Brazil. Alliance resources limited are a resource company of Australia that is involved in the

exploration of base metals and gold along with having project in Western and South Australia.

Jupiter Mines limited on other hand is a mining company that is engaged in developing and

carrying out activities of mineral resources and is based in Australia. Bauxite resources limited

are another mining company that is primarily engaged in bauxite minerals deposits acquisition,

development and exploration activities in Australia. A comparative analysis of debt and equity

position of all the chosen companies have been demonstrated in the report.

Discussion:

Corporate regulation:

Critical analysis of financial reporting and accounting regulation:

Financial reporting or the financial reports published by reporting entities are sought by

wide range of users such as investors, communities, employees, analysts, public and government

Introduction:

The current paper has been prepared for addressing the importance of regulation of

financial reporting and assessment of voluntarily disclosure of information by managers. The

process of standard setting at the global level by the international accounting standard has been

analyzed in the report. For the analysis of owner’s equity, four companies have been selected

from the Australian stock exchanges namely Alliance resources limited, Aguia resources limited,

Jupiter mines limited and Bauxite resources limited. Aguia resource limited is a company based

in Australia with its primary focus on the development and exploration of mineral resources in

Brazil. Alliance resources limited are a resource company of Australia that is involved in the

exploration of base metals and gold along with having project in Western and South Australia.

Jupiter Mines limited on other hand is a mining company that is engaged in developing and

carrying out activities of mineral resources and is based in Australia. Bauxite resources limited

are another mining company that is primarily engaged in bauxite minerals deposits acquisition,

development and exploration activities in Australia. A comparative analysis of debt and equity

position of all the chosen companies have been demonstrated in the report.

Discussion:

Corporate regulation:

Critical analysis of financial reporting and accounting regulation:

Financial reporting or the financial reports published by reporting entities are sought by

wide range of users such as investors, communities, employees, analysts, public and government

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE AND FINANCIAL ACCOUNTING

for their decision making. Regulation of financial report helps in providing standardized

information to the users. For making essential financial decision by the shareholders or investors,

usage and interpretation of financial information is of utmost importance. In the absence of

regulation of financial reports, different entities would create financial report by preparing in a

diversified way. Regulatory framework acts as a balance between different accounting practices

varying from country to country (Donohoe 2015). In addition to this, there also exists asymmetry

information between user groups and directors ad managers of company. Therefore, regulation of

financial report intends to alleviate the problems associated with the lack of comparability and

information asymmetry.

If the contents of published financial information are left to be determined by managers,

it would be uncertain that the external users will be provided with relevant information for

rational decision making. Therefore, there is a likelihood that external participants would be

mislead and would draw the potential investors from making investments. Nevertheless, the

voluntary disclosure concepts are used by managers to communicate the important financial

information to users. This particular platform of voluntary disclosure is used by managers for

communicating the firm’s superior performance and thereby supplementing the reporting that is

mandated. Therefore, the decision to allow the managers to make disclosure of information

voluntarily generates the ambiguous answer. Allowing managers to disclosure information

voluntarily would help internal users and might not be useful for external users in their decision

making (Pownall and Wieczynska 2018).

for their decision making. Regulation of financial report helps in providing standardized

information to the users. For making essential financial decision by the shareholders or investors,

usage and interpretation of financial information is of utmost importance. In the absence of

regulation of financial reports, different entities would create financial report by preparing in a

diversified way. Regulatory framework acts as a balance between different accounting practices

varying from country to country (Donohoe 2015). In addition to this, there also exists asymmetry

information between user groups and directors ad managers of company. Therefore, regulation of

financial report intends to alleviate the problems associated with the lack of comparability and

information asymmetry.

If the contents of published financial information are left to be determined by managers,

it would be uncertain that the external users will be provided with relevant information for

rational decision making. Therefore, there is a likelihood that external participants would be

mislead and would draw the potential investors from making investments. Nevertheless, the

voluntary disclosure concepts are used by managers to communicate the important financial

information to users. This particular platform of voluntary disclosure is used by managers for

communicating the firm’s superior performance and thereby supplementing the reporting that is

mandated. Therefore, the decision to allow the managers to make disclosure of information

voluntarily generates the ambiguous answer. Allowing managers to disclosure information

voluntarily would help internal users and might not be useful for external users in their decision

making (Pownall and Wieczynska 2018).

5CORPORATE AND FINANCIAL ACCOUNTING

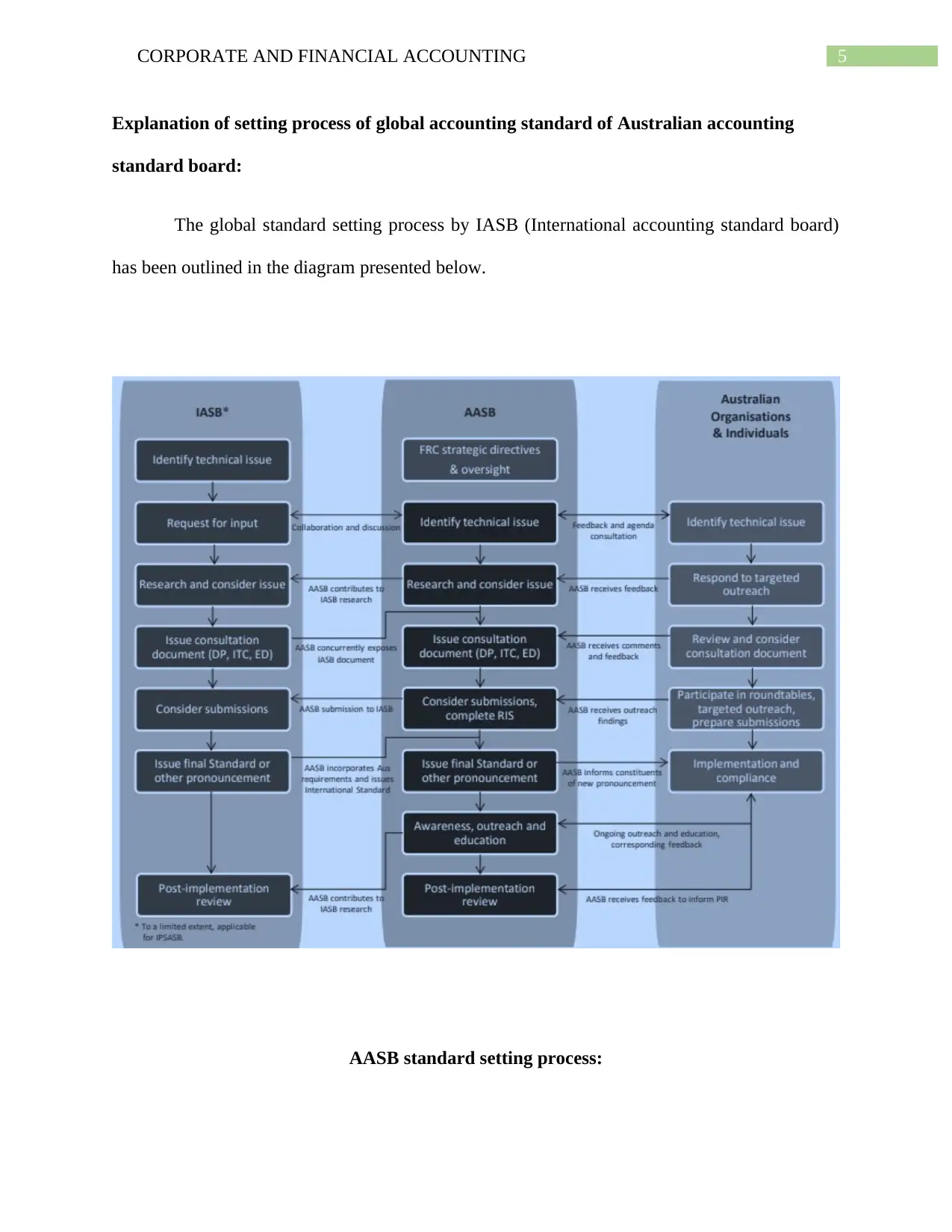

Explanation of setting process of global accounting standard of Australian accounting

standard board:

The global standard setting process by IASB (International accounting standard board)

has been outlined in the diagram presented below.

AASB standard setting process:

Explanation of setting process of global accounting standard of Australian accounting

standard board:

The global standard setting process by IASB (International accounting standard board)

has been outlined in the diagram presented below.

AASB standard setting process:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE AND FINANCIAL ACCOUNTING

(Source: Aasb.gov.au 2018)

The first step requires the international standard to identify the technical issue and the

financial reporting council strategic direction aligns with the adoption of International financial

reporting council. Moreover, the technical issues seeking consideration is also identified. The

work program of public sector accounting program is closely monitored by the accounting board.

Issues might be raised in the context of improving reliability and relevance of financial

information. Second step requires development of project proposal after the identification of

technical issue (Watts and Zuo 2016). The decision to undertake the project is taken after project

proposal is reviewed. The decision to formally report to the board agenda decision can be done

after adding or not adding issue to agenda. Furthermore, the agenda papers are discussed and

developed by AASB staff after the issue has been incorporated in agenda. The output timings,

issue scope and alternative approaches are addressed in the agenda papers. For compatible

requirements development, consideration of issues can be done jointly with the accounting

standard board of New Zealand (Campbell et al. 2017). After the completion of research work,

the related documents are made available for discussing with the stakeholders and for public

comments.

Explanation of why IFRS is not mandatory for IASB member countries:

The International accounting standard board has implemented the International financial

reporting. However, there are some drawbacks of the standard that does not make the adoption of

the standard mandatory for all the member countries. It is so because complete adoption of the

standard would make financial report some qualities. One of the members of IASB that is United

States does not intend to adopt the standard because of the market incentive (Epstein 2018).

(Source: Aasb.gov.au 2018)

The first step requires the international standard to identify the technical issue and the

financial reporting council strategic direction aligns with the adoption of International financial

reporting council. Moreover, the technical issues seeking consideration is also identified. The

work program of public sector accounting program is closely monitored by the accounting board.

Issues might be raised in the context of improving reliability and relevance of financial

information. Second step requires development of project proposal after the identification of

technical issue (Watts and Zuo 2016). The decision to undertake the project is taken after project

proposal is reviewed. The decision to formally report to the board agenda decision can be done

after adding or not adding issue to agenda. Furthermore, the agenda papers are discussed and

developed by AASB staff after the issue has been incorporated in agenda. The output timings,

issue scope and alternative approaches are addressed in the agenda papers. For compatible

requirements development, consideration of issues can be done jointly with the accounting

standard board of New Zealand (Campbell et al. 2017). After the completion of research work,

the related documents are made available for discussing with the stakeholders and for public

comments.

Explanation of why IFRS is not mandatory for IASB member countries:

The International accounting standard board has implemented the International financial

reporting. However, there are some drawbacks of the standard that does not make the adoption of

the standard mandatory for all the member countries. It is so because complete adoption of the

standard would make financial report some qualities. One of the members of IASB that is United

States does not intend to adopt the standard because of the market incentive (Epstein 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE AND FINANCIAL ACCOUNTING

Analysis of owner’s equity of four selected companies:

Contributed equity or issued capital- Contributed equity is the amount that is

contributed by shareholders or owners of company in the form of paid up capital in exchange for

stocks or shares held by them.

Reserves- Reserves are the amount that have been apportioned from the profits of

company and is set aside for specific purpose such as for repair and maintenance, bonus

payment, legal settlement and purchasing of fixed assets (Edwards et al. 2015).

Retained earnings- Retained earnings are the amount of profit that is used by business

for reinvestment and they are not distributed in the form of dividends to shareholders.

Accumulated loss- It is the amount of loss that is incurred by business which is also

impacted by the distribution of dividends to shareholders.

Analysis of each item of Aguia resources limited:

Equity of Aguia resources consist of accumulated loss, issued capital ad retained

earnings. It can be seen from the equity section as presented in the balance sheet that the issued

capital stood at $ 72912689 and $ 81895554 in year 2015 and 2016 compared to $ 93849407 and

$ 100972143 in year 2017 and 2018 respectively. Figure indicates that the value of capital

contributed by owners has been increasing year on year. Reserves value stood is negative figure

that decreased from $ 1971174 in year 2015 to $ 1013025 in year 2016 and thereafter increased

to $ 1927956 and $ 3838650 in year 2017 and 2018. Accumulated loss incurred has been on a

continuous rise from $ 50932966 in year 2015 and $ 56806178 in year 2016 which further

Analysis of owner’s equity of four selected companies:

Contributed equity or issued capital- Contributed equity is the amount that is

contributed by shareholders or owners of company in the form of paid up capital in exchange for

stocks or shares held by them.

Reserves- Reserves are the amount that have been apportioned from the profits of

company and is set aside for specific purpose such as for repair and maintenance, bonus

payment, legal settlement and purchasing of fixed assets (Edwards et al. 2015).

Retained earnings- Retained earnings are the amount of profit that is used by business

for reinvestment and they are not distributed in the form of dividends to shareholders.

Accumulated loss- It is the amount of loss that is incurred by business which is also

impacted by the distribution of dividends to shareholders.

Analysis of each item of Aguia resources limited:

Equity of Aguia resources consist of accumulated loss, issued capital ad retained

earnings. It can be seen from the equity section as presented in the balance sheet that the issued

capital stood at $ 72912689 and $ 81895554 in year 2015 and 2016 compared to $ 93849407 and

$ 100972143 in year 2017 and 2018 respectively. Figure indicates that the value of capital

contributed by owners has been increasing year on year. Reserves value stood is negative figure

that decreased from $ 1971174 in year 2015 to $ 1013025 in year 2016 and thereafter increased

to $ 1927956 and $ 3838650 in year 2017 and 2018. Accumulated loss incurred has been on a

continuous rise from $ 50932966 in year 2015 and $ 56806178 in year 2016 which further

8CORPORATE AND FINANCIAL ACCOUNTING

increased to $ 60629927 and $ 62872918 in year 2017 and 2018 respectively

(Aguiaresources.com.au 2018).

Analysis of each items of equity of Bauxite resources limited:

The amount of contributed equity for Bauxite resources declined from $ 87651716 in

year 2014 to $ 78401613 in year 2015 compared to $ 66631264 in year 2016 and $ 66641060 in

year 2015 respectively. Value of reserves initially increased to $ 690892 in year 2015 from $

580953 in year 2014 compared to $ 571240 in year 2016 and $ 561219 in year 2017 respectively.

Retained earnings figure were negative for consecutive years with value recorded at $ 41166374

in year 2014 and $ 51788573 2015 compared to $ 47450689 and $ 47949155 in year 2016 and

2017 respectively (Bauxiteresource.com.au 2018).

Analysis of each items of equity of Alliance resources limited:

Equity of Alliance resources limited consist of contributed equity, accumulated loss,

reserves and non controlling entities. Value of contributed equity has increased in the initial

years of analysis and reduced subsequently. Equity increased from $ 98918022 in year 2014 to $

103475639 in year 2015. This amount reduced drastically to $ 55841095 in year 2017 and $

47494743 respectively. Looking at the figures of accumulated loss, it can be seen that the

amount of loss incurred from $ 75097294 in year 2014 to $ 78222860 in year 2015 which

reduced further to $ 30981165 and $ 32130741 in year 2017 and 2018 respectively. Reserves

value was in negative figure of amount of $ 781145 in year 2015 compared to $ 363809 in year

2014 and the negative value increased to $ 63509 and $ 1375436 in year 2016 and 2017

increased to $ 60629927 and $ 62872918 in year 2017 and 2018 respectively

(Aguiaresources.com.au 2018).

Analysis of each items of equity of Bauxite resources limited:

The amount of contributed equity for Bauxite resources declined from $ 87651716 in

year 2014 to $ 78401613 in year 2015 compared to $ 66631264 in year 2016 and $ 66641060 in

year 2015 respectively. Value of reserves initially increased to $ 690892 in year 2015 from $

580953 in year 2014 compared to $ 571240 in year 2016 and $ 561219 in year 2017 respectively.

Retained earnings figure were negative for consecutive years with value recorded at $ 41166374

in year 2014 and $ 51788573 2015 compared to $ 47450689 and $ 47949155 in year 2016 and

2017 respectively (Bauxiteresource.com.au 2018).

Analysis of each items of equity of Alliance resources limited:

Equity of Alliance resources limited consist of contributed equity, accumulated loss,

reserves and non controlling entities. Value of contributed equity has increased in the initial

years of analysis and reduced subsequently. Equity increased from $ 98918022 in year 2014 to $

103475639 in year 2015. This amount reduced drastically to $ 55841095 in year 2017 and $

47494743 respectively. Looking at the figures of accumulated loss, it can be seen that the

amount of loss incurred from $ 75097294 in year 2014 to $ 78222860 in year 2015 which

reduced further to $ 30981165 and $ 32130741 in year 2017 and 2018 respectively. Reserves

value was in negative figure of amount of $ 781145 in year 2015 compared to $ 363809 in year

2014 and the negative value increased to $ 63509 and $ 1375436 in year 2016 and 2017

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE AND FINANCIAL ACCOUNTING

respectively. Financial year 2017 recorded non controlling entities of amount $ 901937

(Allianceresources.com.au 2018).

Analysis of each items of equity of Jupiter mines limited:

For both the year 2017, 2016 and 2015, the amount of issued capital is recorded at $

526639293 which declined to $ 433003602 in year 2018. Reserves amount was recorded at $

979639 in year 2014 which declined to zero in year 2015. For financial year 2017 and 2018, the

amount of reserves is recorded at $ 180488 and $ 1105503 respectively. Accumulated loss is

recorded at amount of $ 79098969 and $ 241495298 in year 2015 and 2016 and the loss further

increased to $ 51395961 in year 2017 (Jupitermines.com 2018). However, year 2018 generated

accumulated profit of amount $ 32048589.

Comparative analysis of debt and equity position of chosen companies:

The total value of equity of Aguia resources limited increased from $ 31291524 in year

2017 compared to $ 34260575 in year 2016 indicating that the value has increased in recent year.

Financial year 2018 and 2017 did not record any loan, borrowings and therefore it does not have

debt. However, financial year 2015 and 2016 recorded borrowing of amount $ 1000000 and $

213949.

For Alliance resources limited, total value of equity is recorded at amount $ 24796421 in

year 2016 which reduced to $ 14890503 in year 2017 indicating that equity value declined in

recent year. Total amount of debt for year 2017 is recorded at $ 74287 compared to $ 81841 in

year 2017. The amount of equity is considerably higher than the amount of debt recorded.

respectively. Financial year 2017 recorded non controlling entities of amount $ 901937

(Allianceresources.com.au 2018).

Analysis of each items of equity of Jupiter mines limited:

For both the year 2017, 2016 and 2015, the amount of issued capital is recorded at $

526639293 which declined to $ 433003602 in year 2018. Reserves amount was recorded at $

979639 in year 2014 which declined to zero in year 2015. For financial year 2017 and 2018, the

amount of reserves is recorded at $ 180488 and $ 1105503 respectively. Accumulated loss is

recorded at amount of $ 79098969 and $ 241495298 in year 2015 and 2016 and the loss further

increased to $ 51395961 in year 2017 (Jupitermines.com 2018). However, year 2018 generated

accumulated profit of amount $ 32048589.

Comparative analysis of debt and equity position of chosen companies:

The total value of equity of Aguia resources limited increased from $ 31291524 in year

2017 compared to $ 34260575 in year 2016 indicating that the value has increased in recent year.

Financial year 2018 and 2017 did not record any loan, borrowings and therefore it does not have

debt. However, financial year 2015 and 2016 recorded borrowing of amount $ 1000000 and $

213949.

For Alliance resources limited, total value of equity is recorded at amount $ 24796421 in

year 2016 which reduced to $ 14890503 in year 2017 indicating that equity value declined in

recent year. Total amount of debt for year 2017 is recorded at $ 74287 compared to $ 81841 in

year 2017. The amount of equity is considerably higher than the amount of debt recorded.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE AND FINANCIAL ACCOUNTING

For bauxite resources, total amount of equity recorded has increased from $ 19751815 in

year 2016 compared to $ 19253124 in year 2017respectively. On other hand, there was no

borrowing recorded in the recent years and therefore, no debt exists for year 2017 and 2016.

There were fewer declines in the amount of total equity of Jupiter mines limited from $

475423820 in year 2017 compared to $ 466157694 in year 2018. Debt stood in the form of

deferred tax liabilities for both the year 2018 and 2017 at amount of $ 2581865 and $ 3537977

indicating decline in the tax liabilities. Figure suggests that the debt burden is lower than the

equity position of company.

From the analysis of the above figures of debt and equity, it can be concluded that Jupiter mine

limited has higher equity value compared to other companies operating in material sector. One of

the surprising facts deduced from analysis is that Jupiter mines limited has higher debt burden,

however, no companies have financial leverage in the form of increasing debt burden.

Conclusion:

The report prepared helped in addressing different accounting aspects in terms of

regulation, owner’s equity and standard setting process. It has been found that regulatory

framework plays a very important role in standardizing the financial report and alleviating

several problems associated with reliability, comparability and relevance of financial

information. Moreover, the global standard setting process has been outlined which depicts that

it takes various steps to complete the process by the international accounting standard. Analysis

of owners equity position of the companies have deduced the fact that equity position of Jupiter

mines limited is favorable compared to other companies. In addition to this, it has also been

ascertained that there is no debt that is owed by Bauxite resources limited.

For bauxite resources, total amount of equity recorded has increased from $ 19751815 in

year 2016 compared to $ 19253124 in year 2017respectively. On other hand, there was no

borrowing recorded in the recent years and therefore, no debt exists for year 2017 and 2016.

There were fewer declines in the amount of total equity of Jupiter mines limited from $

475423820 in year 2017 compared to $ 466157694 in year 2018. Debt stood in the form of

deferred tax liabilities for both the year 2018 and 2017 at amount of $ 2581865 and $ 3537977

indicating decline in the tax liabilities. Figure suggests that the debt burden is lower than the

equity position of company.

From the analysis of the above figures of debt and equity, it can be concluded that Jupiter mine

limited has higher equity value compared to other companies operating in material sector. One of

the surprising facts deduced from analysis is that Jupiter mines limited has higher debt burden,

however, no companies have financial leverage in the form of increasing debt burden.

Conclusion:

The report prepared helped in addressing different accounting aspects in terms of

regulation, owner’s equity and standard setting process. It has been found that regulatory

framework plays a very important role in standardizing the financial report and alleviating

several problems associated with reliability, comparability and relevance of financial

information. Moreover, the global standard setting process has been outlined which depicts that

it takes various steps to complete the process by the international accounting standard. Analysis

of owners equity position of the companies have deduced the fact that equity position of Jupiter

mines limited is favorable compared to other companies. In addition to this, it has also been

ascertained that there is no debt that is owed by Bauxite resources limited.

11CORPORATE AND FINANCIAL ACCOUNTING

References and Bibliography list:

Aasb.gov.au., 2018. The standard-setting process . [online] Available at:

https://www.aasb.gov.au/About-the-AASB/The-standard-setting-process.aspx [Accessed 19 Sep.

2018].

Aguiaresources.com.au., 2018. Retrieved 26 September 2018, from

https://www.amcor.com/investors/financial-information/annual-reports

Allianceresources.com.au., 2018. Retrieved 26 September 2018, from

https://www.amcor.com/investors/financial-information/annual-reports

Baños-Caballero, S., García-Teruel, P.J. and Martínez-Solano, P., 2014. Working capital

management, corporate performance, and financial constraints. Journal of Business

Research, 67(3), pp.332-338.

Bauxiteresource.com.au., 2018. Retrieved 26 September 2018, from

https://www.amcor.com/investors/financial-information/annual-reports

Campbell, J.L., Khan, U. and Pierce, S., 2017. The effect of mandatory disclosure on market

inefficiencies: Evidence from Statement of Financial Accounting Standard Number 161.

Capkun, V., Collins, D. and Jeanjean, T., 2016. The effect of IAS/IFRS adoption on earnings

management (smoothing): A closer look at competing explanations. Journal of Accounting and

Public Policy, 35(4), pp.352-394.

Donohoe, M.P., 2015. The economic effects of financial derivatives on corporate tax

avoidance. Journal of Accounting and Economics, 59(1), pp.1-24.

References and Bibliography list:

Aasb.gov.au., 2018. The standard-setting process . [online] Available at:

https://www.aasb.gov.au/About-the-AASB/The-standard-setting-process.aspx [Accessed 19 Sep.

2018].

Aguiaresources.com.au., 2018. Retrieved 26 September 2018, from

https://www.amcor.com/investors/financial-information/annual-reports

Allianceresources.com.au., 2018. Retrieved 26 September 2018, from

https://www.amcor.com/investors/financial-information/annual-reports

Baños-Caballero, S., García-Teruel, P.J. and Martínez-Solano, P., 2014. Working capital

management, corporate performance, and financial constraints. Journal of Business

Research, 67(3), pp.332-338.

Bauxiteresource.com.au., 2018. Retrieved 26 September 2018, from

https://www.amcor.com/investors/financial-information/annual-reports

Campbell, J.L., Khan, U. and Pierce, S., 2017. The effect of mandatory disclosure on market

inefficiencies: Evidence from Statement of Financial Accounting Standard Number 161.

Capkun, V., Collins, D. and Jeanjean, T., 2016. The effect of IAS/IFRS adoption on earnings

management (smoothing): A closer look at competing explanations. Journal of Accounting and

Public Policy, 35(4), pp.352-394.

Donohoe, M.P., 2015. The economic effects of financial derivatives on corporate tax

avoidance. Journal of Accounting and Economics, 59(1), pp.1-24.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.