Corporate Finance Report: Impact of Dividends on Bukit Darah PLC

VerifiedAdded on 2020/02/24

|16

|3387

|88

Report

AI Summary

This report provides a detailed analysis of Bukit Darah PLC's corporate finance, focusing on its dividend policy and hedging strategies. It examines the company's financial structure, including its economic and financial resources, and evaluates its dividend payout ratio and dividend yield. The report explores the theories behind dividend policy, including the Modigliani and Miller theory and the Gordon model, and offers recommendations for improving the company's practices. Furthermore, it addresses Bukit Darah PLC's exposure to foreign exchange risk and discusses both internal and external hedging strategies, including the importance of derivatives. The analysis concludes with an assessment of the company's financial decisions and the potential impact of various management strategies.

1

Corporate Finance

Name:

Course

Professor’s name

University name

City, State

Date of submission

Corporate Finance

Name:

Course

Professor’s name

University name

City, State

Date of submission

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Executive Summary

In this report, we aim to analyze the impact of dividends on Bukit Darah PLC and the resultant

effect on every management decision undertaken that may increase the companys hedging

policies. The dividend yield and dividend turnover are majorcontributing factor in this company.

Thus, a dividend policy is the decision in which a company distributes profits made for the year

versus retention of the same for reinvestment in the company. The effect of issuance costs is to

eliminate the indifference between issuing shares to finance dividend payments and domestic

financing. The report summarises all the potential impact of of hedging and dividend risks on

Bukit Darah and whether the management will approve of some decisions based on the

recommendations given.

Executive Summary

In this report, we aim to analyze the impact of dividends on Bukit Darah PLC and the resultant

effect on every management decision undertaken that may increase the companys hedging

policies. The dividend yield and dividend turnover are majorcontributing factor in this company.

Thus, a dividend policy is the decision in which a company distributes profits made for the year

versus retention of the same for reinvestment in the company. The effect of issuance costs is to

eliminate the indifference between issuing shares to finance dividend payments and domestic

financing. The report summarises all the potential impact of of hedging and dividend risks on

Bukit Darah and whether the management will approve of some decisions based on the

recommendations given.

3

Table of Content

Introduction……………………………………………………………………………………….4

Decision of Dividends.....................................................................................................................5

The economic-financial structure of the company..........................................................................6

Dividend policy of Bukit Darah...................................................................................................7

Dividend payout Ratio-................................................................................................................7

Dividend Yield-............................................................................................................................8

Market share value.......................................................................................................................8

Theories on Dividend Policy...........................................................................................................9

Recommendations..........................................................................................................................10

Company’s exposure to foreign exchange risk..............................................................................10

Hedging..........................................................................................................................................12

a) Internal hedging strategies...............................................................................................12

b) External hedging methods:..............................................................................................13

Importance of derivatives in External Hedging includes the following........................................14

Conclusion………………………………………………………………………………………15

Table of Content

Introduction……………………………………………………………………………………….4

Decision of Dividends.....................................................................................................................5

The economic-financial structure of the company..........................................................................6

Dividend policy of Bukit Darah...................................................................................................7

Dividend payout Ratio-................................................................................................................7

Dividend Yield-............................................................................................................................8

Market share value.......................................................................................................................8

Theories on Dividend Policy...........................................................................................................9

Recommendations..........................................................................................................................10

Company’s exposure to foreign exchange risk..............................................................................10

Hedging..........................................................................................................................................12

a) Internal hedging strategies...............................................................................................12

b) External hedging methods:..............................................................................................13

Importance of derivatives in External Hedging includes the following........................................14

Conclusion………………………………………………………………………………………15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Introduction

Bukit Darah PLC is an investment holding company that has interest in many other industries

such as real estate,oil palm plantations, portfolio assets management among others. OIn this

paper, we shall look into the company’s dividend policy, how the company’s share price has

been fairing in the last few years.

Decision of Dividends

The dividend decision consists in determining the optimal profit distribution volume that allows

maintaining an adequate policy of sufficient remuneration and self financing to the actions of the

company (Anil Kumar, Kumar and Mariyappa, 2010). Thus, a dividend policy is the decision in

which a company distributes profits made for the year versus retention of the same for

reinvestment in the company. The main issue that is derived from the dividend decision is

whether market value of the company is independent of the dividend policy followed by the

company.

There are two main positions in economics that disagree with the way dividends are distributed

in the company. Modigliani and Miller (1961) is one of the theories advanced in this topic which

suggests that the dividend policy of a company is not relevant to the market value of the

company (Bingham and Kiesel, 2004). The second position taken by economists is the Gordon

(1962) that suggests that when a firm operate on an optimum dividend policy that is able to

maximize the value of the firm and assumes that the buyer of a share pays its future dividends

(Cassedy, 2004).

Introduction

Bukit Darah PLC is an investment holding company that has interest in many other industries

such as real estate,oil palm plantations, portfolio assets management among others. OIn this

paper, we shall look into the company’s dividend policy, how the company’s share price has

been fairing in the last few years.

Decision of Dividends

The dividend decision consists in determining the optimal profit distribution volume that allows

maintaining an adequate policy of sufficient remuneration and self financing to the actions of the

company (Anil Kumar, Kumar and Mariyappa, 2010). Thus, a dividend policy is the decision in

which a company distributes profits made for the year versus retention of the same for

reinvestment in the company. The main issue that is derived from the dividend decision is

whether market value of the company is independent of the dividend policy followed by the

company.

There are two main positions in economics that disagree with the way dividends are distributed

in the company. Modigliani and Miller (1961) is one of the theories advanced in this topic which

suggests that the dividend policy of a company is not relevant to the market value of the

company (Bingham and Kiesel, 2004). The second position taken by economists is the Gordon

(1962) that suggests that when a firm operate on an optimum dividend policy that is able to

maximize the value of the firm and assumes that the buyer of a share pays its future dividends

(Cassedy, 2004).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

The economic-financial structure of the company

Bukit Darah PLC requires financial resources to carry marketing and other production activities.

It needs financial resources so as to finance the investments necessary to be able to carry out its

productive activity as well as to be able to face the payment of the current expenses originated by

the same (Coyle, n.d.).

The balance, for the economic-financial analysis which is the main model of the company,

includes in the liabilities and the various financial resources that the company uses, while it

relates the materializations of these resources which are investments and jobs (Dalton, 2013). In

simple terms, the asset collects the working capital or productive capital and the working capital

or financing liabilities. The economic structure of Bukit Darah Plc consists of investment in both

current and fixed assets (Hicks, 2000).

The investment in long term Assets which are also called fixed assets for the company is

fundamentally determined by the capacity of absorption of the market, that is to say, by the

demand. There is a necessary unsatisfied demand, which is however not sufficient, condition for

an investment to be made in fixed assets and consequently for the company to grow. The

investment in short term assets ensures the operation of the operating cycle for the company and

is dependent on the value of the fixed assets (Joseph, 2009). Current assets investment is derived

or complementary to the investment in fixed assets.The financial structure of the company

consists of the resources that the company needs to carry out its activity, that is, the different

The economic-financial structure of the company

Bukit Darah PLC requires financial resources to carry marketing and other production activities.

It needs financial resources so as to finance the investments necessary to be able to carry out its

productive activity as well as to be able to face the payment of the current expenses originated by

the same (Coyle, n.d.).

The balance, for the economic-financial analysis which is the main model of the company,

includes in the liabilities and the various financial resources that the company uses, while it

relates the materializations of these resources which are investments and jobs (Dalton, 2013). In

simple terms, the asset collects the working capital or productive capital and the working capital

or financing liabilities. The economic structure of Bukit Darah Plc consists of investment in both

current and fixed assets (Hicks, 2000).

The investment in long term Assets which are also called fixed assets for the company is

fundamentally determined by the capacity of absorption of the market, that is to say, by the

demand. There is a necessary unsatisfied demand, which is however not sufficient, condition for

an investment to be made in fixed assets and consequently for the company to grow. The

investment in short term assets ensures the operation of the operating cycle for the company and

is dependent on the value of the fixed assets (Joseph, 2009). Current assets investment is derived

or complementary to the investment in fixed assets.The financial structure of the company

consists of the resources that the company needs to carry out its activity, that is, the different

6

means of financing, the origin of capital. We will group the financial resources in the following

sections:

Capital and Reserves

The capital stock together with the reserves constitute the own funds of the company. These are

the most stable or permanent sources of financing, since they have no maturity, and at the same

time they are the ones that bear the greatest risk because, in case of bankruptcy, the partners

participate in the value resulting from the liquidation of the company in last place, after having

repaid the other credits (Labbi, 2014).

Dividend policy of Bukit Darah

In the year 2016/17, the company did not pay any dividends t its shareholders, this is the same

case to the year 2015/16, where there was no dividends paid to the shareholders. Judging from

the past two financial years, in which the company has not paid any dividends we can

confidently say that the company dividend policy is a constant pay out ratio (Loader, 2007).

Which means that the company pays out a fixed percentage of the company’s profits, in this

case, the percentage is zero percent of the total earnings.

Dividend payout Ratio-DPR ratio is the total dividends paid to shareholders relative to net

income of the company.It is the percentage of earnings paid out to shareholders. Bukit Darah Plc

has not paid out dividends in the year2015/16 and the year 2016/17, which means that the

dividend pay out is zero.

means of financing, the origin of capital. We will group the financial resources in the following

sections:

Capital and Reserves

The capital stock together with the reserves constitute the own funds of the company. These are

the most stable or permanent sources of financing, since they have no maturity, and at the same

time they are the ones that bear the greatest risk because, in case of bankruptcy, the partners

participate in the value resulting from the liquidation of the company in last place, after having

repaid the other credits (Labbi, 2014).

Dividend policy of Bukit Darah

In the year 2016/17, the company did not pay any dividends t its shareholders, this is the same

case to the year 2015/16, where there was no dividends paid to the shareholders. Judging from

the past two financial years, in which the company has not paid any dividends we can

confidently say that the company dividend policy is a constant pay out ratio (Loader, 2007).

Which means that the company pays out a fixed percentage of the company’s profits, in this

case, the percentage is zero percent of the total earnings.

Dividend payout Ratio-DPR ratio is the total dividends paid to shareholders relative to net

income of the company.It is the percentage of earnings paid out to shareholders. Bukit Darah Plc

has not paid out dividends in the year2015/16 and the year 2016/17, which means that the

dividend pay out is zero.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

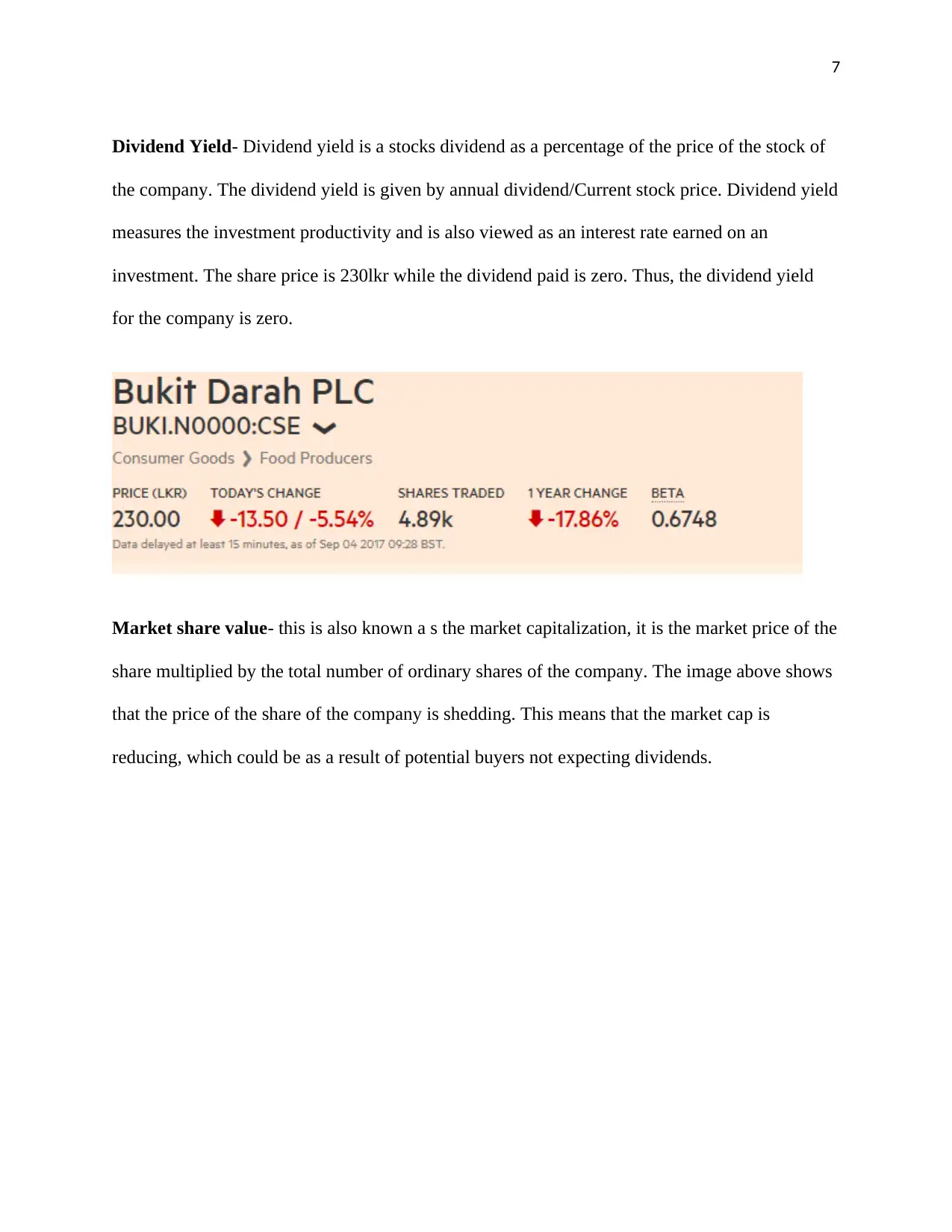

Dividend Yield- Dividend yield is a stocks dividend as a percentage of the price of the stock of

the company. The dividend yield is given by annual dividend/Current stock price. Dividend yield

measures the investment productivity and is also viewed as an interest rate earned on an

investment. The share price is 230lkr while the dividend paid is zero. Thus, the dividend yield

for the company is zero.

Market share value- this is also known a s the market capitalization, it is the market price of the

share multiplied by the total number of ordinary shares of the company. The image above shows

that the price of the share of the company is shedding. This means that the market cap is

reducing, which could be as a result of potential buyers not expecting dividends.

Dividend Yield- Dividend yield is a stocks dividend as a percentage of the price of the stock of

the company. The dividend yield is given by annual dividend/Current stock price. Dividend yield

measures the investment productivity and is also viewed as an interest rate earned on an

investment. The share price is 230lkr while the dividend paid is zero. Thus, the dividend yield

for the company is zero.

Market share value- this is also known a s the market capitalization, it is the market price of the

share multiplied by the total number of ordinary shares of the company. The image above shows

that the price of the share of the company is shedding. This means that the market cap is

reducing, which could be as a result of potential buyers not expecting dividends.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

Theories on Dividend Policy

Between the two previous positions there is a set of theories that are developed theoretically:

residual dividend theory, the clientele effect, the informative value of dividends, dividend policy

and agency or the theory of expectations. Theory of Residual Dividends :The Theory of Residual

Dividends promotes its distribution only when all the investment opportunities have been

satisfied; this is when there are residual benefits once the investment policy of the company has

been established. The Theory of MM( Modigiliani and Miller) establishes the hypothesis that

there is no brokerage expenses, that is to say, there are no expenses of issuing shares; however,

the real situation is that there are emission costs in the market, so that the company is more

expensive the money coming from the issuance of shares than it gets via retained earnings (Yip,

2008). The effect of issuance costs is to eliminate the indifference between issuing shares to

finance dividend payments and domestic financing. The maxims are: - Keep the debt ratio

constant for future investment projects. - Accept an investment project only if its net present

value is positive. - Finance the part of the disbursement of new projects from the ordinary shares,

Theories on Dividend Policy

Between the two previous positions there is a set of theories that are developed theoretically:

residual dividend theory, the clientele effect, the informative value of dividends, dividend policy

and agency or the theory of expectations. Theory of Residual Dividends :The Theory of Residual

Dividends promotes its distribution only when all the investment opportunities have been

satisfied; this is when there are residual benefits once the investment policy of the company has

been established. The Theory of MM( Modigiliani and Miller) establishes the hypothesis that

there is no brokerage expenses, that is to say, there are no expenses of issuing shares; however,

the real situation is that there are emission costs in the market, so that the company is more

expensive the money coming from the issuance of shares than it gets via retained earnings (Yip,

2008). The effect of issuance costs is to eliminate the indifference between issuing shares to

finance dividend payments and domestic financing. The maxims are: - Keep the debt ratio

constant for future investment projects. - Accept an investment project only if its net present

value is positive. - Finance the part of the disbursement of new projects from the ordinary shares,

9

first through internal financing and when it is exhausted, through the issuance of new securities.-

If any internal financing remains unapplied after allocating the investment projects, it will be

distributed via dividends (Yip, 2008). Otherwise there will be no dividend payment. According

to this theory the dividend policy has a passive influence and does not directly affect the market

value of the shares

Recommendations

For a company to use the best practices it should set a non binding policy to the company.

1. The company should at least strive to pay its shareholders who have not been paid for the

last two years by putting in place cost cutting measures to increase profits.

2. the dividend policy of the company should be linked to the economic situation of the

company and also its long term strategy so that it cannot affect future operations and

investments to be made by the company.

Company’s exposure to foreign exchange risk

Exchange rate risk is one of the modalities of so-called market risk, which refers to price

variations, and also includes interest rates, financial asset value and commodity prices (raw

materials, grains, etc.). It is called this because it is the risk that is run because of fluctuations in

the exchange rate.

It is particularly relevant for Indonesia and Malaysia.

Sources of foreign exchange risk

An organization, business or other, or a person, is exposed to exchange rate risk in essentially the

following ways: by the mere fact of receiving income in foreign currency or having expenses in

first through internal financing and when it is exhausted, through the issuance of new securities.-

If any internal financing remains unapplied after allocating the investment projects, it will be

distributed via dividends (Yip, 2008). Otherwise there will be no dividend payment. According

to this theory the dividend policy has a passive influence and does not directly affect the market

value of the shares

Recommendations

For a company to use the best practices it should set a non binding policy to the company.

1. The company should at least strive to pay its shareholders who have not been paid for the

last two years by putting in place cost cutting measures to increase profits.

2. the dividend policy of the company should be linked to the economic situation of the

company and also its long term strategy so that it cannot affect future operations and

investments to be made by the company.

Company’s exposure to foreign exchange risk

Exchange rate risk is one of the modalities of so-called market risk, which refers to price

variations, and also includes interest rates, financial asset value and commodity prices (raw

materials, grains, etc.). It is called this because it is the risk that is run because of fluctuations in

the exchange rate.

It is particularly relevant for Indonesia and Malaysia.

Sources of foreign exchange risk

An organization, business or other, or a person, is exposed to exchange rate risk in essentially the

following ways: by the mere fact of receiving income in foreign currency or having expenses in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

it when one operates essentially in local currency; there is always a risk that these revenues or

expenses will be lower or higher, depending on the case, at the time of making them; the time

factor is exacerbated when the time of receipt or payment is longer, as this increases the

likelihood of an unfavorable exchange rate variation. Exporters and importers are well aware of

this risk, which in extreme cases can destroy their margins, by what is called foreign exchange

losses, and make them work at a loss.

Importance of foreign exchange risks

Debts that can be commercial and especially financial; the risk is even greater if you have

income in local currency, because with these you may have to pay more than you had

anticipated. Many will think at the time of their mortgage or vehicle debts, which in Indonesia

are heavily dollarized - with 45% of the loans being dollarized in general.

This type of risk is the one that has caused to break in times of crisis to numerous companies in

the most varied countries. During the Asian crisis, dollar debts multiplied as a result of

devaluations by 1.5 or more times in countries like Malaysia, and Thailand, Indonesia being an

extreme case (up to 6 times at any given time, for finish in more than 3 times) (Verma, 2008).

By having deposits and other financial assets in foreign currency; these can earn or lose value in

local currency equivalent with exchange rate variations. Of course, many will think of their

dollar deposits that have lost value from about 3-4 years ago, for example, but losses only

materialize when one has to sell them, and in the meantime they are only potential (WARREN,

2018). The same thing happens to companies, which can thus lose a part of their cash reserves,

and also to banks, which may have had much of their liquidity in dollars and lose money for it.

due to the fact of having debts in foreign currency.

it when one operates essentially in local currency; there is always a risk that these revenues or

expenses will be lower or higher, depending on the case, at the time of making them; the time

factor is exacerbated when the time of receipt or payment is longer, as this increases the

likelihood of an unfavorable exchange rate variation. Exporters and importers are well aware of

this risk, which in extreme cases can destroy their margins, by what is called foreign exchange

losses, and make them work at a loss.

Importance of foreign exchange risks

Debts that can be commercial and especially financial; the risk is even greater if you have

income in local currency, because with these you may have to pay more than you had

anticipated. Many will think at the time of their mortgage or vehicle debts, which in Indonesia

are heavily dollarized - with 45% of the loans being dollarized in general.

This type of risk is the one that has caused to break in times of crisis to numerous companies in

the most varied countries. During the Asian crisis, dollar debts multiplied as a result of

devaluations by 1.5 or more times in countries like Malaysia, and Thailand, Indonesia being an

extreme case (up to 6 times at any given time, for finish in more than 3 times) (Verma, 2008).

By having deposits and other financial assets in foreign currency; these can earn or lose value in

local currency equivalent with exchange rate variations. Of course, many will think of their

dollar deposits that have lost value from about 3-4 years ago, for example, but losses only

materialize when one has to sell them, and in the meantime they are only potential (WARREN,

2018). The same thing happens to companies, which can thus lose a part of their cash reserves,

and also to banks, which may have had much of their liquidity in dollars and lose money for it.

due to the fact of having debts in foreign currency.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

Hedging

It is important to pay attention to the fact that the index in question has the greatest possible

degree of correlation with the assets of the portfolio. If for example the portfolio has a dominant

presence of companies in the technology sector, a benchmark index could be the money markets,

which focuses mainly on assets in the sector (Sims and Clift, 2001).

It is very important to keep in mind that this type of hedging strategies will probably have less

return than an uncovered buying position in a period of strong market rises. The cost of accessing

lower volatility and lower levels of risk is the lower return offered by hedged strategies during

upward periods (Ullrich, 2009).

Some investors also prefer to give a dynamic approach to the coverage scheme. In these cases,

for example, the level of coverage can be increased when it is considered that the market

circumstances so warrant (Rheinländer and Sexton, 2011) .

a) Internal hedging strategies

Due to the fact that companies have both payables and receivables in foreign exchange currency

but the companies that have these two classificationsin this respect;

They can be classified as

A) Hedging of currencies that values are to appreciate

B) Hedging of currencies that values are to depreciate

Hedging

It is important to pay attention to the fact that the index in question has the greatest possible

degree of correlation with the assets of the portfolio. If for example the portfolio has a dominant

presence of companies in the technology sector, a benchmark index could be the money markets,

which focuses mainly on assets in the sector (Sims and Clift, 2001).

It is very important to keep in mind that this type of hedging strategies will probably have less

return than an uncovered buying position in a period of strong market rises. The cost of accessing

lower volatility and lower levels of risk is the lower return offered by hedged strategies during

upward periods (Ullrich, 2009).

Some investors also prefer to give a dynamic approach to the coverage scheme. In these cases,

for example, the level of coverage can be increased when it is considered that the market

circumstances so warrant (Rheinländer and Sexton, 2011) .

a) Internal hedging strategies

Due to the fact that companies have both payables and receivables in foreign exchange currency

but the companies that have these two classificationsin this respect;

They can be classified as

A) Hedging of currencies that values are to appreciate

B) Hedging of currencies that values are to depreciate

12

The types of hedging in internal strategies include the following

1) Denomination in currency of local value- the exchange can be completely avoided if the

transaction is only done in local currency. To make the things equitable, the invoice

transaction risk is the invoice value in spirit (Rana, 2010). This process only distributes

the spread risk appropriately between the contracting parties but does not hedge the risk.

2) Leads and lags – this is done especially importers and exporters in forecasting of

transactions and whether the currency will weaken or not. This means that the currency

will be devalued or depreciated or strengthened for future transactions (Mukherjee and

Mohammed Hanif., 2006). According to the expectations, the exporters and importers

may like to postpone the payment or receipt of the foreign currency. Manipulation of

foreign currency will depend on the timing and the expectations of change in currency..

In a hedging strategy instead, we have a buy position in a stock portfolio combined with a sales

position in an equity index. In these cases, it is key that the stock portfolio generates a higher

return than the rise of the long-term indexes, otherwise it would be more convenient to apply

another kind of risk control strategies (Michayluk, 2007)

.

b) External hedging methods:

The types of hedging in internal strategies include the following

1) Denomination in currency of local value- the exchange can be completely avoided if the

transaction is only done in local currency. To make the things equitable, the invoice

transaction risk is the invoice value in spirit (Rana, 2010). This process only distributes

the spread risk appropriately between the contracting parties but does not hedge the risk.

2) Leads and lags – this is done especially importers and exporters in forecasting of

transactions and whether the currency will weaken or not. This means that the currency

will be devalued or depreciated or strengthened for future transactions (Mukherjee and

Mohammed Hanif., 2006). According to the expectations, the exporters and importers

may like to postpone the payment or receipt of the foreign currency. Manipulation of

foreign currency will depend on the timing and the expectations of change in currency..

In a hedging strategy instead, we have a buy position in a stock portfolio combined with a sales

position in an equity index. In these cases, it is key that the stock portfolio generates a higher

return than the rise of the long-term indexes, otherwise it would be more convenient to apply

another kind of risk control strategies (Michayluk, 2007)

.

b) External hedging methods:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.