Corporate Finance - Coursework

VerifiedAdded on 2020/09/08

|17

|3609

|45

Report

AI Summary

This report analyzes the acquisition of YPF by Repsol, focusing on corporate finance strategies, market implications, and the overall impact on the oil industry. It discusses the strategic position of both companies, the financial aspects of the merger, and the challenges faced during the acquisition process. The report concludes with insights into the effectiveness of the merger and its significance in the context of corporate finance.

Corporate Finance -

Coursework

Coursework

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................1

INTRODUCTION...........................................................................................................................2

1.1 Strategic position of Repsol and its strategic options:..........................................................2

2. YPF is worth as an independent company and potential value after acquiring by the Repsol:

.....................................................................................................................................................6

Q3: Key factors those are effect the level of acquisition............................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

EXECUTIVE SUMMARY.............................................................................................................1

INTRODUCTION...........................................................................................................................2

1.1 Strategic position of Repsol and its strategic options:..........................................................2

2. YPF is worth as an independent company and potential value after acquiring by the Repsol:

.....................................................................................................................................................6

Q3: Key factors those are effect the level of acquisition............................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

EXECUTIVE SUMMARY

Nowadays, this has been observed that each company is applying to make out certain

tools which help out to make certain effective tool which would help the firm to gain sustainable

development. Although, M&A is one of the best effective tool which would help out to make

certain things effective and efficient tool. Acquisition is the tool to redirect and reshape corporate

strategy which has never been higher. There are so many managers today which purchase a firm

for accessing to markets, goods, technology advancement, resources, or the skilled management

talent which is less risky and faster than attainment the similar objectives via inner efforts.

1

Nowadays, this has been observed that each company is applying to make out certain

tools which help out to make certain effective tool which would help the firm to gain sustainable

development. Although, M&A is one of the best effective tool which would help out to make

certain things effective and efficient tool. Acquisition is the tool to redirect and reshape corporate

strategy which has never been higher. There are so many managers today which purchase a firm

for accessing to markets, goods, technology advancement, resources, or the skilled management

talent which is less risky and faster than attainment the similar objectives via inner efforts.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Under this case, this can be observed that the Repsol is intending to buy the YPF

company as Repsol is one of the dominant oil organisation which have its registered office at

Spain. For taking oil reserve and benefits of broad level, Cortina had embarked on the strategy of

acquiring oil assets via Latin America (Brealey and et. al., 2012). He started to take Yacimientos,

Petroliferos Fiscales S.A. (YPF) at the Argentine government declared that this will offer its

block of shares. As, the company was the highest oil organisation throughout the nation, and

twelfth biggest in reserves. Management of YPF had resisted go through a friendly acquisition.

To fulfil a takeover of the organisation, Cortina will have required to appeal to the shareholders

in the form of tender offer in order to buy their shares. Unsolicited tender offers were highly rare

events in the cross-border M&A normally and most importantly between emerging and

developed countries.

1.1 Strategic position of Repsol and its strategic options:

In the international business corporation, organisations need strategic thinking and only

by forming effective strategies which could become strategically competitive. A business

strategy is a complete master plan which incorporate how firm would attain its mission and

objectives (Fracassi, 2011). Strategy is presuming to be the important as this is universal in

nature. This assist companies to make pace with the dynamic environment. This enhance

motivation of the employees and reinforce decision making. This incorporates the basis for

applying the actions.

The main intention of this paper is to make and assess the behaviour of the Argentine

gasoline market and to assess competitive effects on that market of merger between Repsol and

YPF, which emerge in 1999. By doing so, there are following answer which are required to be

answer in the following questions:

(a). Did merger have direct influence on the prices and quantities which are traded in the

market?

(b). What kind of market structure elaborates the behaviour of the industry better?

(c). Did the structure vary as a consequence of the merger?

(d). Which are the welfare implications of that change?

2

Under this case, this can be observed that the Repsol is intending to buy the YPF

company as Repsol is one of the dominant oil organisation which have its registered office at

Spain. For taking oil reserve and benefits of broad level, Cortina had embarked on the strategy of

acquiring oil assets via Latin America (Brealey and et. al., 2012). He started to take Yacimientos,

Petroliferos Fiscales S.A. (YPF) at the Argentine government declared that this will offer its

block of shares. As, the company was the highest oil organisation throughout the nation, and

twelfth biggest in reserves. Management of YPF had resisted go through a friendly acquisition.

To fulfil a takeover of the organisation, Cortina will have required to appeal to the shareholders

in the form of tender offer in order to buy their shares. Unsolicited tender offers were highly rare

events in the cross-border M&A normally and most importantly between emerging and

developed countries.

1.1 Strategic position of Repsol and its strategic options:

In the international business corporation, organisations need strategic thinking and only

by forming effective strategies which could become strategically competitive. A business

strategy is a complete master plan which incorporate how firm would attain its mission and

objectives (Fracassi, 2011). Strategy is presuming to be the important as this is universal in

nature. This assist companies to make pace with the dynamic environment. This enhance

motivation of the employees and reinforce decision making. This incorporates the basis for

applying the actions.

The main intention of this paper is to make and assess the behaviour of the Argentine

gasoline market and to assess competitive effects on that market of merger between Repsol and

YPF, which emerge in 1999. By doing so, there are following answer which are required to be

answer in the following questions:

(a). Did merger have direct influence on the prices and quantities which are traded in the

market?

(b). What kind of market structure elaborates the behaviour of the industry better?

(c). Did the structure vary as a consequence of the merger?

(d). Which are the welfare implications of that change?

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

For answering these kinds of questions, they could implement data set which includes

monthly gasoline price information by province for YPF during 1998-2000. We likewise

implement data on the quantities, market stake, oil prices, population and GDP (Hillier and et.

al., 2014).

This research about effect of Repsol-YPF merger on the Argentine gasoline market which

is mostly a clinic econometric case study in the Pauter’s classification. It crucially could be

appraised by comparing it to some other things which can enter into the similar category. This is

worth value that the acquisition of YPF by Spanish company Repsol is likewise crucial by itself.

This is biggest merger in the Argentine history. However, this can be said that the merger

influenced the market in an effective manner. This was crucial to Repsol's management which an

offer be layout which will attain the support of YPF's shareholders, and repel potential

contenders. A tender offers of this magnitude will be highest by the Spanish organisation, and

also in the energy sector.

Repsol is the international energy firm which is based in Madrid, Spain. This makes out

upstream and downstream activities via entire planet. There are almost higher than 24000

employees throughout the planet. During 1999, Repsol acquired 15% stake of YPF from the

Argentine government which was one of the great deal during that time. Analysts rightly

observed that the price was fair and greeted strategic fit between two organisations, Analysts

rightly observed that this can be said that this will render balance to Repsol’s overexposure in

refining and marketing while YPF had concentrated on exploration and goods. The main

acquisition better positioned Repsol like a multinational firm. Repsol’s acquisition of YPF

likewise enhanced its capital to 288 million shares throughout the planet. Repsol’s is the

company which includes in one of the top organisation in the oil and gas industry. The cited

organisation throughout the entire value chain: exploration and manufacturing, transformation,

development and the marketing of the energy which is more effective and sustainable and

competitive for millions of people (Gullifer and Payne, 2015).

This is presuming to be the goods throughout 87 nations and operates in 37 of them,

forming us a planet us a planet renowned energy organisation. During four years, this can have

invested that over 350million euros in looking for new ways in order to produce sustainable

energy. Strategic plan ensure strength and the capability to form value in the provided situations,

via efficiency and active portfolio management. During 2012, the Argentina federal government

3

monthly gasoline price information by province for YPF during 1998-2000. We likewise

implement data on the quantities, market stake, oil prices, population and GDP (Hillier and et.

al., 2014).

This research about effect of Repsol-YPF merger on the Argentine gasoline market which

is mostly a clinic econometric case study in the Pauter’s classification. It crucially could be

appraised by comparing it to some other things which can enter into the similar category. This is

worth value that the acquisition of YPF by Spanish company Repsol is likewise crucial by itself.

This is biggest merger in the Argentine history. However, this can be said that the merger

influenced the market in an effective manner. This was crucial to Repsol's management which an

offer be layout which will attain the support of YPF's shareholders, and repel potential

contenders. A tender offers of this magnitude will be highest by the Spanish organisation, and

also in the energy sector.

Repsol is the international energy firm which is based in Madrid, Spain. This makes out

upstream and downstream activities via entire planet. There are almost higher than 24000

employees throughout the planet. During 1999, Repsol acquired 15% stake of YPF from the

Argentine government which was one of the great deal during that time. Analysts rightly

observed that the price was fair and greeted strategic fit between two organisations, Analysts

rightly observed that this can be said that this will render balance to Repsol’s overexposure in

refining and marketing while YPF had concentrated on exploration and goods. The main

acquisition better positioned Repsol like a multinational firm. Repsol’s acquisition of YPF

likewise enhanced its capital to 288 million shares throughout the planet. Repsol’s is the

company which includes in one of the top organisation in the oil and gas industry. The cited

organisation throughout the entire value chain: exploration and manufacturing, transformation,

development and the marketing of the energy which is more effective and sustainable and

competitive for millions of people (Gullifer and Payne, 2015).

This is presuming to be the goods throughout 87 nations and operates in 37 of them,

forming us a planet us a planet renowned energy organisation. During four years, this can have

invested that over 350million euros in looking for new ways in order to produce sustainable

energy. Strategic plan ensure strength and the capability to form value in the provided situations,

via efficiency and active portfolio management. During 2012, the Argentina federal government

3

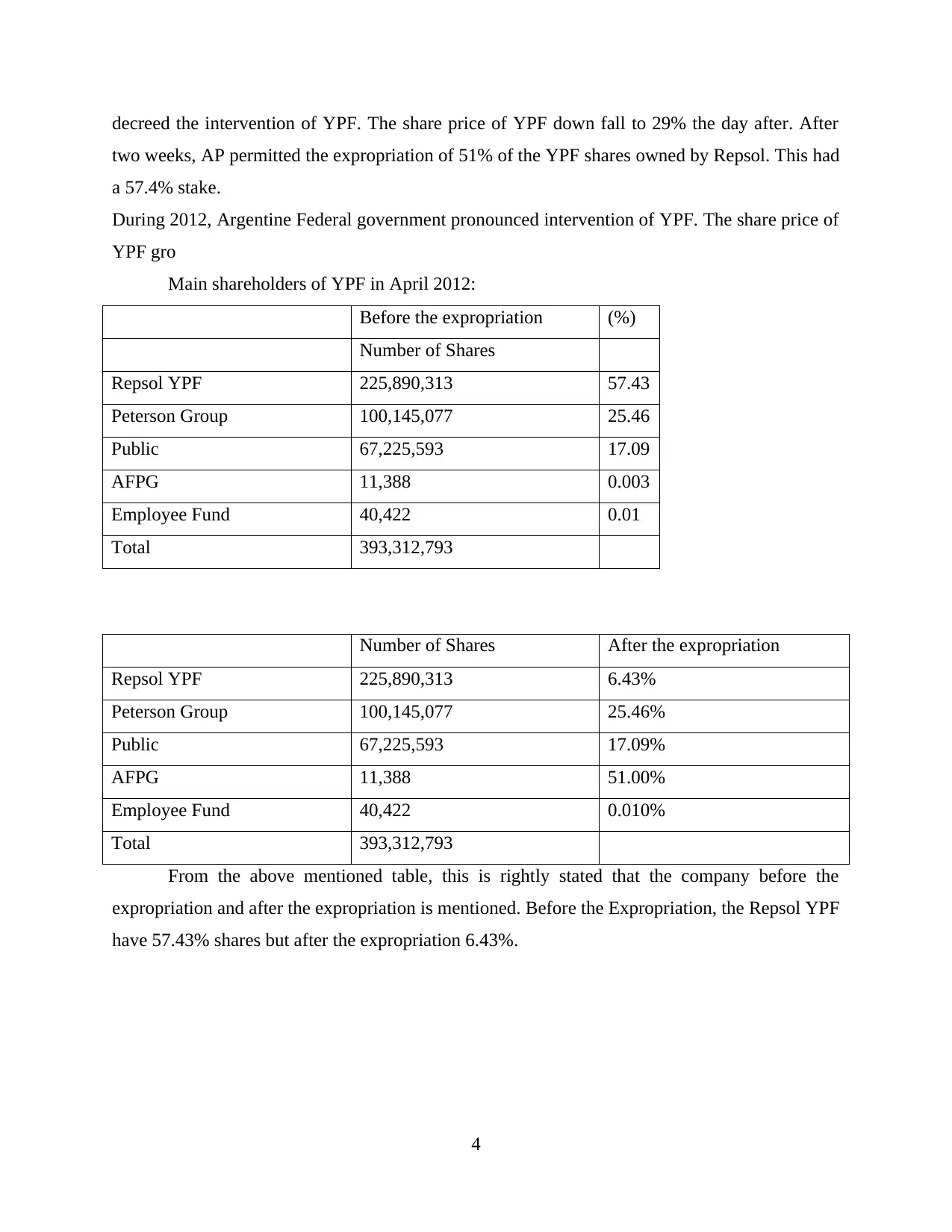

decreed the intervention of YPF. The share price of YPF down fall to 29% the day after. After

two weeks, AP permitted the expropriation of 51% of the YPF shares owned by Repsol. This had

a 57.4% stake.

During 2012, Argentine Federal government pronounced intervention of YPF. The share price of

YPF gro

Main shareholders of YPF in April 2012:

Before the expropriation (%)

Number of Shares

Repsol YPF 225,890,313 57.43

Peterson Group 100,145,077 25.46

Public 67,225,593 17.09

AFPG 11,388 0.003

Employee Fund 40,422 0.01

Total 393,312,793

Number of Shares After the expropriation

Repsol YPF 225,890,313 6.43%

Peterson Group 100,145,077 25.46%

Public 67,225,593 17.09%

AFPG 11,388 51.00%

Employee Fund 40,422 0.010%

Total 393,312,793

From the above mentioned table, this is rightly stated that the company before the

expropriation and after the expropriation is mentioned. Before the Expropriation, the Repsol YPF

have 57.43% shares but after the expropriation 6.43%.

4

two weeks, AP permitted the expropriation of 51% of the YPF shares owned by Repsol. This had

a 57.4% stake.

During 2012, Argentine Federal government pronounced intervention of YPF. The share price of

YPF gro

Main shareholders of YPF in April 2012:

Before the expropriation (%)

Number of Shares

Repsol YPF 225,890,313 57.43

Peterson Group 100,145,077 25.46

Public 67,225,593 17.09

AFPG 11,388 0.003

Employee Fund 40,422 0.01

Total 393,312,793

Number of Shares After the expropriation

Repsol YPF 225,890,313 6.43%

Peterson Group 100,145,077 25.46%

Public 67,225,593 17.09%

AFPG 11,388 51.00%

Employee Fund 40,422 0.010%

Total 393,312,793

From the above mentioned table, this is rightly stated that the company before the

expropriation and after the expropriation is mentioned. Before the Expropriation, the Repsol YPF

have 57.43% shares but after the expropriation 6.43%.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

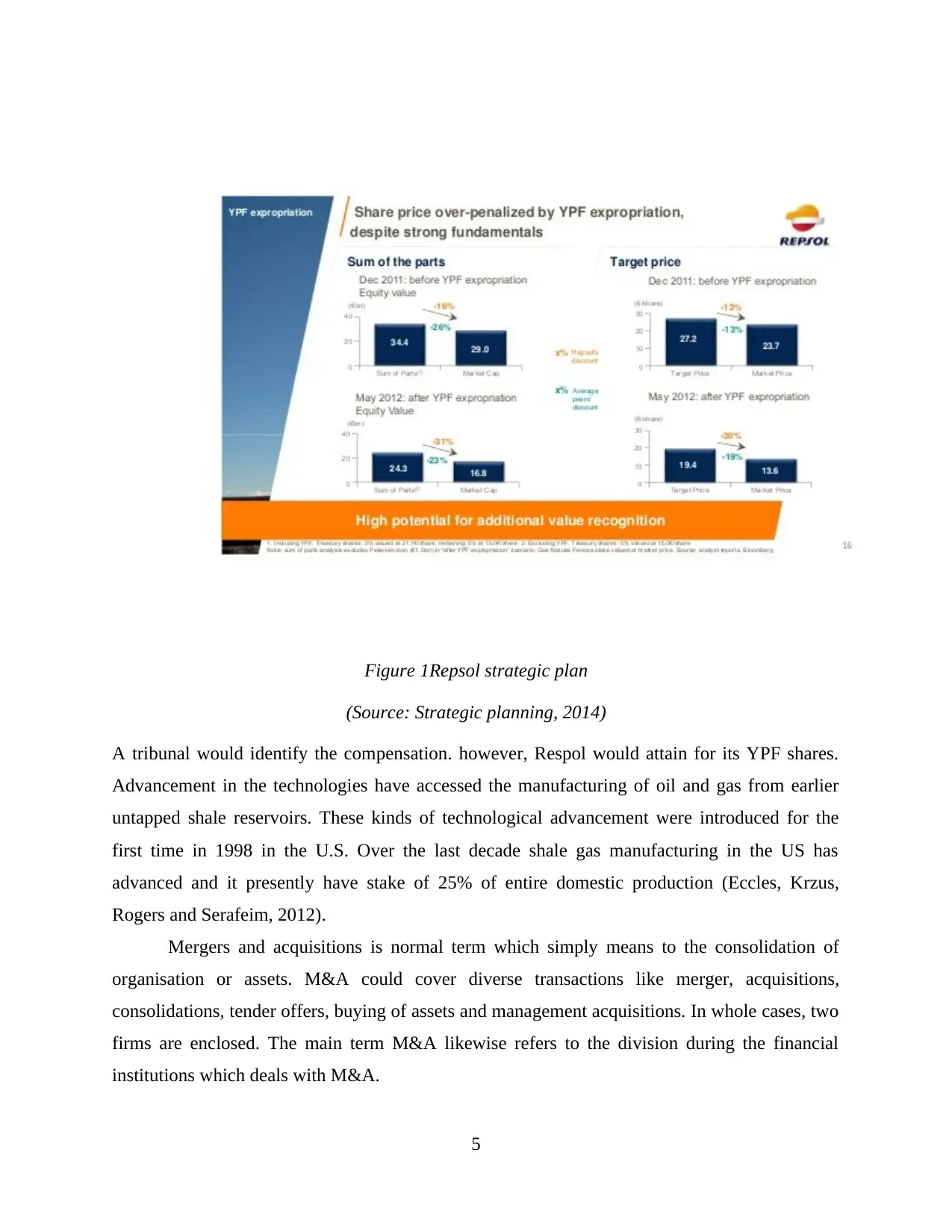

Figure 1Repsol strategic plan

(Source: Strategic planning, 2014)

A tribunal would identify the compensation. however, Respol would attain for its YPF shares.

Advancement in the technologies have accessed the manufacturing of oil and gas from earlier

untapped shale reservoirs. These kinds of technological advancement were introduced for the

first time in 1998 in the U.S. Over the last decade shale gas manufacturing in the US has

advanced and it presently have stake of 25% of entire domestic production (Eccles, Krzus,

Rogers and Serafeim, 2012).

Mergers and acquisitions is normal term which simply means to the consolidation of

organisation or assets. M&A could cover diverse transactions like merger, acquisitions,

consolidations, tender offers, buying of assets and management acquisitions. In whole cases, two

firms are enclosed. The main term M&A likewise refers to the division during the financial

institutions which deals with M&A.

5

(Source: Strategic planning, 2014)

A tribunal would identify the compensation. however, Respol would attain for its YPF shares.

Advancement in the technologies have accessed the manufacturing of oil and gas from earlier

untapped shale reservoirs. These kinds of technological advancement were introduced for the

first time in 1998 in the U.S. Over the last decade shale gas manufacturing in the US has

advanced and it presently have stake of 25% of entire domestic production (Eccles, Krzus,

Rogers and Serafeim, 2012).

Mergers and acquisitions is normal term which simply means to the consolidation of

organisation or assets. M&A could cover diverse transactions like merger, acquisitions,

consolidations, tender offers, buying of assets and management acquisitions. In whole cases, two

firms are enclosed. The main term M&A likewise refers to the division during the financial

institutions which deals with M&A.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

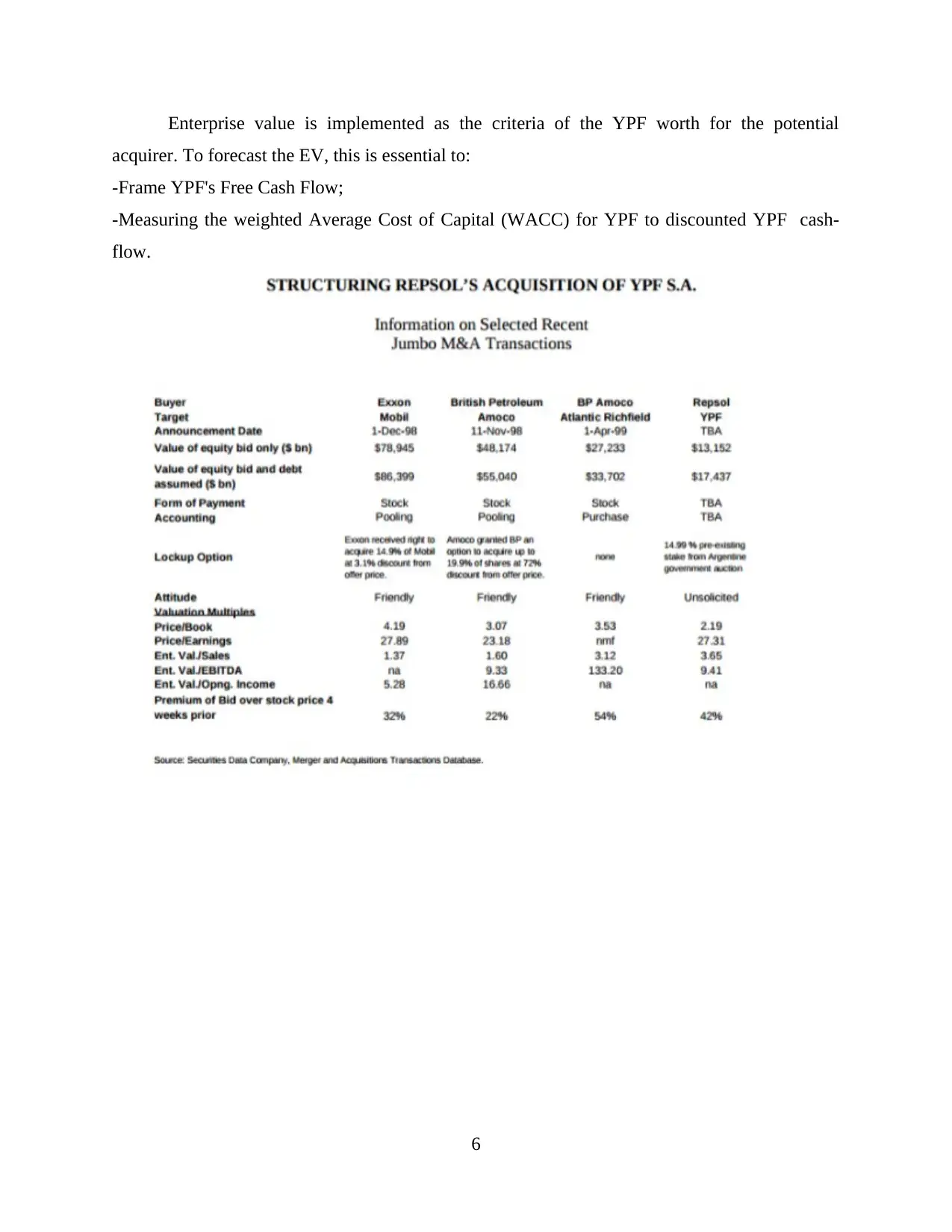

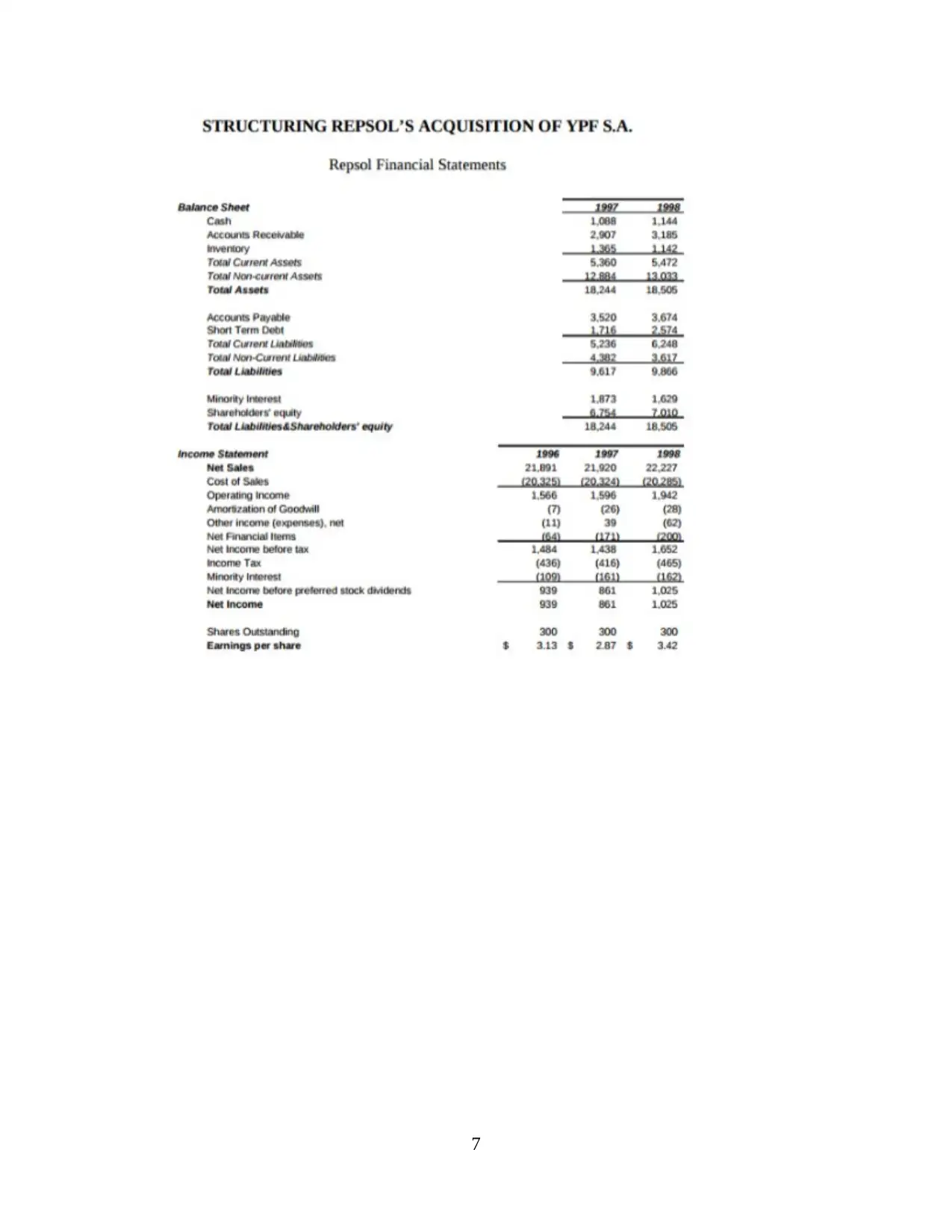

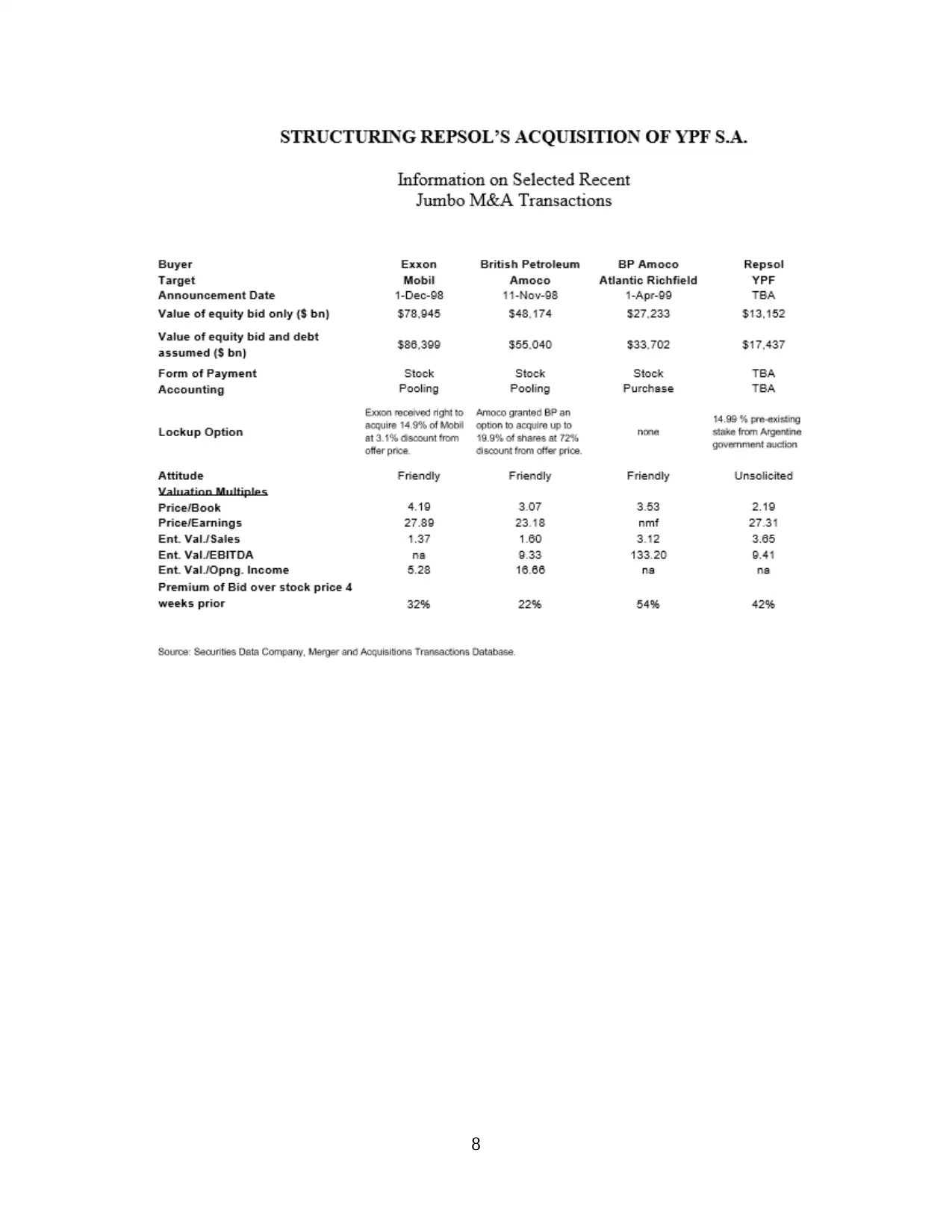

Enterprise value is implemented as the criteria of the YPF worth for the potential

acquirer. To forecast the EV, this is essential to:

-Frame YPF's Free Cash Flow;

-Measuring the weighted Average Cost of Capital (WACC) for YPF to discounted YPF cash-

flow.

6

acquirer. To forecast the EV, this is essential to:

-Frame YPF's Free Cash Flow;

-Measuring the weighted Average Cost of Capital (WACC) for YPF to discounted YPF cash-

flow.

6

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

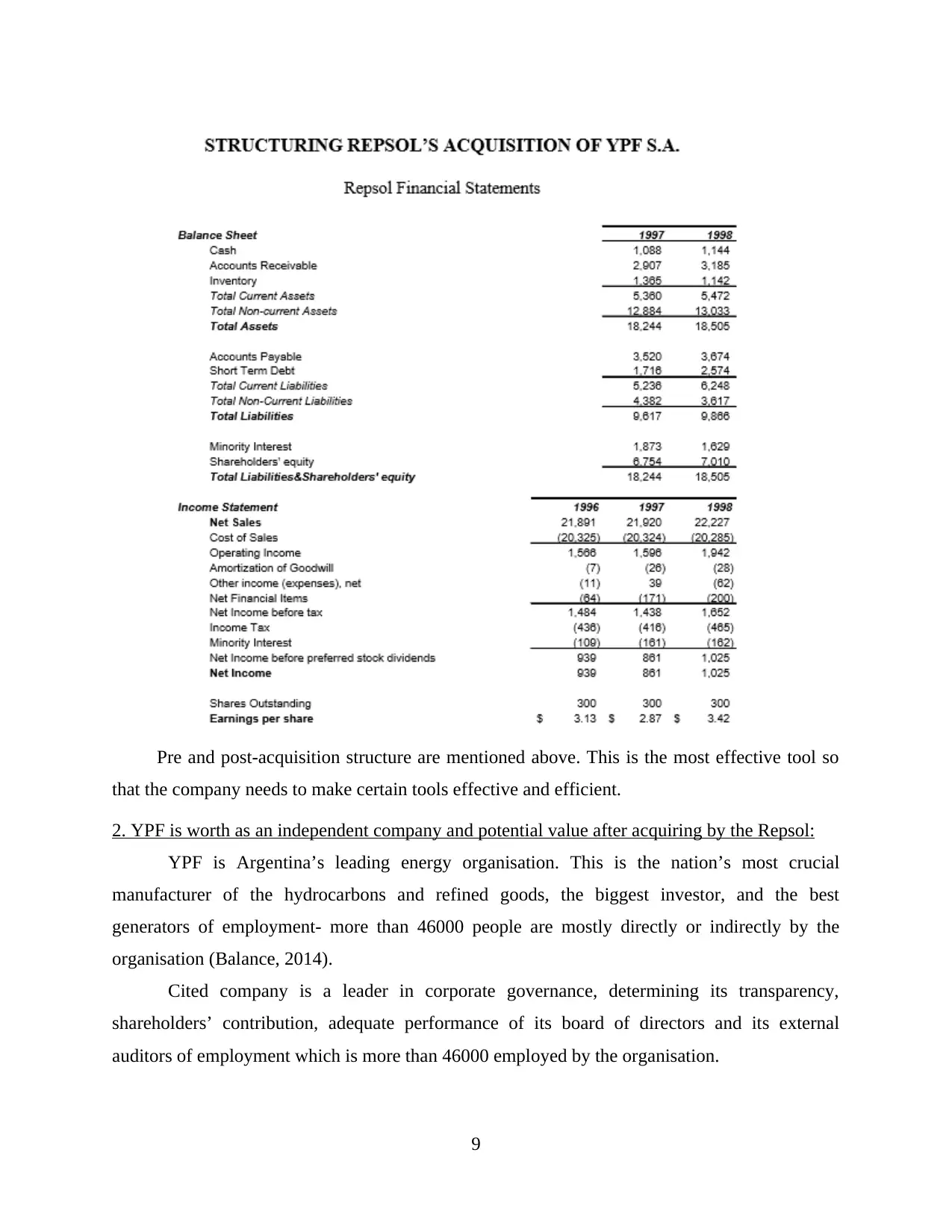

Pre and post-acquisition structure are mentioned above. This is the most effective tool so

that the company needs to make certain tools effective and efficient.

2. YPF is worth as an independent company and potential value after acquiring by the Repsol:

YPF is Argentina’s leading energy organisation. This is the nation’s most crucial

manufacturer of the hydrocarbons and refined goods, the biggest investor, and the best

generators of employment- more than 46000 people are mostly directly or indirectly by the

organisation (Balance, 2014).

Cited company is a leader in corporate governance, determining its transparency,

shareholders’ contribution, adequate performance of its board of directors and its external

auditors of employment which is more than 46000 employed by the organisation.

9

that the company needs to make certain tools effective and efficient.

2. YPF is worth as an independent company and potential value after acquiring by the Repsol:

YPF is Argentina’s leading energy organisation. This is the nation’s most crucial

manufacturer of the hydrocarbons and refined goods, the biggest investor, and the best

generators of employment- more than 46000 people are mostly directly or indirectly by the

organisation (Balance, 2014).

Cited company is a leader in corporate governance, determining its transparency,

shareholders’ contribution, adequate performance of its board of directors and its external

auditors of employment which is more than 46000 employed by the organisation.

9

This operates an entire integrated chain of oil and gas organisation, with market

leadership in entire segments of its activity. To grow its firm and get the effective corporate

governance level it desires, the organisation has a BODs which assumes management of the

organisation in a diligent and prudent manner, as per with effective business practice as per the

Argentine Corporation Law.

The board enables the strategic plan, and well as management objectives and annual

budgets, for which it assesses the investment and financial policies with the macro-economic

situation.

Throughout the board:

YPF normally has 17 consistent directors, and 5 are independent. This number of directors is

presuming to be an appropriate for the scope of the firm, and experience rendered by its

members is mostly positive for the firm’s management. Under this, shareholders are required that

the board of directors is bestowed on the individuals of the well identified domestic and global

solvency, know-how and expertise from the best varied corporate fields (Martínez-Sola, García-

Teruel and Martínez-Solano, 2014).

In the line with effective corporate governance practice, the board of director and applied

rule of ethics and convene implementing to the board and entire govern the convene the

organisation and its employees in regards with their positions and commercial relations.

Due to another part of its policies, YPF implemented a code of conduct of the

organisation and its employees with respect to their positions and business and professional

relations.

As other part of its policies, YPS enables and applied a code of conduct in the context of

the securities market- elaborating its system framework for action to stimulate transparency and

save legitimate interest of the investment community.

Stocks and shares:

YPF’s upstream operations covers of the exploration, emergence and manufacturing of

crude oil, natural gas and LPG. Downstream operations cover refining, marketing, transportation

and distribution of oil and a huge range of petroleum goods, petroleum derivatives,

petrochemicals, LPG. This is likewise active in the gas separation and natural gas distribution

industry- both directly and via its investment in diverse linked organisations.

10

leadership in entire segments of its activity. To grow its firm and get the effective corporate

governance level it desires, the organisation has a BODs which assumes management of the

organisation in a diligent and prudent manner, as per with effective business practice as per the

Argentine Corporation Law.

The board enables the strategic plan, and well as management objectives and annual

budgets, for which it assesses the investment and financial policies with the macro-economic

situation.

Throughout the board:

YPF normally has 17 consistent directors, and 5 are independent. This number of directors is

presuming to be an appropriate for the scope of the firm, and experience rendered by its

members is mostly positive for the firm’s management. Under this, shareholders are required that

the board of directors is bestowed on the individuals of the well identified domestic and global

solvency, know-how and expertise from the best varied corporate fields (Martínez-Sola, García-

Teruel and Martínez-Solano, 2014).

In the line with effective corporate governance practice, the board of director and applied

rule of ethics and convene implementing to the board and entire govern the convene the

organisation and its employees in regards with their positions and commercial relations.

Due to another part of its policies, YPF implemented a code of conduct of the

organisation and its employees with respect to their positions and business and professional

relations.

As other part of its policies, YPS enables and applied a code of conduct in the context of

the securities market- elaborating its system framework for action to stimulate transparency and

save legitimate interest of the investment community.

Stocks and shares:

YPF’s upstream operations covers of the exploration, emergence and manufacturing of

crude oil, natural gas and LPG. Downstream operations cover refining, marketing, transportation

and distribution of oil and a huge range of petroleum goods, petroleum derivatives,

petrochemicals, LPG. This is likewise active in the gas separation and natural gas distribution

industry- both directly and via its investment in diverse linked organisations.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.