Corporate Finance Assignment: Rio Tinto Group CAPM and Dividend Policy

VerifiedAdded on 2022/08/14

|27

|4485

|20

Report

AI Summary

This report provides a comprehensive analysis of the Rio Tinto Group's financial performance, focusing on the application of the Capital Asset Pricing Model (CAPM) to determine the cost of equity. It calculates the cost of equity, ungears the equity beta to derive the asset beta, and examines the company's dividend policy over the past five years using relevant ratios. The report also critically evaluates the suitability of the CAPM-derived cost of equity for investment appraisal, comparing it to the Dividend Growth Model. The analysis includes detailed calculations, justifications for data choices, and a discussion of the implications of the findings for Rio Tinto's financial management and investment decisions. The report also considers the company's dividend payout ratio and its implications for future investments and shareholder value. This analysis is crucial for understanding the financial health and investment potential of Rio Tinto.

Running head: CORPORATE FINANCE 1

Rio Tinto Group CAPM and dividend policy models

Name of the student

Institutional affiliation

Date

Rio Tinto Group CAPM and dividend policy models

Name of the student

Institutional affiliation

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE 2

Introduction

The paper is an assessment regarding the financial aspects of the capital asset pricing

model together with the dividend policy model of a firm. As required, the selected company for

making the analysis is known as Rio Tinto Group. Briefly, Rio Tinto is an Anglo-Australian

multinational entity dealing mining and metals. The company also has its headquarters located

in the United Kingdom, London and it is also listed on the London stock exchange as RIO

(ASX). Therefore, for the purposes of making the CAPM analyses Rio Tinto will be used as the

case study. The structure of the paper comprises of four main sections in which all the required

assessments are provided. For instance in the first section of the paper, calculations regarding

the CAPM are provided. Besides the calculations, the section also includes other elaborate

explanations about the various aspects of CAPM.

The capital asset pricing model refers to a financial approach through which the

relationship between systematic risk and expected returns is analyzed. Majorly, the technique is

used to evaluate stock returns hence its applicability to the selected company of choice.

Primarily, investors and stock holders use the capital asset pricing model to forecast the required

rate of return of any given stock or asset. To effectively make such forecasts of the expected

return, three major factors are put into play. These include the risk free rate of the stock, the

expected market return and the beta value of the asset. Regarding the riot into group, the Capital

Asset Pricing Model is calculated as below with consideration of all the above mentioned

factors:

A): Calculating The Company’s Current Cost of Equity Using the Capital Asset Pricing

Model

Introduction

The paper is an assessment regarding the financial aspects of the capital asset pricing

model together with the dividend policy model of a firm. As required, the selected company for

making the analysis is known as Rio Tinto Group. Briefly, Rio Tinto is an Anglo-Australian

multinational entity dealing mining and metals. The company also has its headquarters located

in the United Kingdom, London and it is also listed on the London stock exchange as RIO

(ASX). Therefore, for the purposes of making the CAPM analyses Rio Tinto will be used as the

case study. The structure of the paper comprises of four main sections in which all the required

assessments are provided. For instance in the first section of the paper, calculations regarding

the CAPM are provided. Besides the calculations, the section also includes other elaborate

explanations about the various aspects of CAPM.

The capital asset pricing model refers to a financial approach through which the

relationship between systematic risk and expected returns is analyzed. Majorly, the technique is

used to evaluate stock returns hence its applicability to the selected company of choice.

Primarily, investors and stock holders use the capital asset pricing model to forecast the required

rate of return of any given stock or asset. To effectively make such forecasts of the expected

return, three major factors are put into play. These include the risk free rate of the stock, the

expected market return and the beta value of the asset. Regarding the riot into group, the Capital

Asset Pricing Model is calculated as below with consideration of all the above mentioned

factors:

A): Calculating The Company’s Current Cost of Equity Using the Capital Asset Pricing

Model

CORPORATE FINANCE 3

As previously mentioned, the capital asset pricing model a measure used to determine

and assess the expected return of an asset, security or stock. In the financial market different

securities have varying levels of risk attached. Due to such a scenario investors are tend to draw

closer attention to the risks associated with particular stocks or assets on the market. Some of the

stocks are highly risky whereas others have low levels of risks attached. It should however be

noted that the highly risky securities also have high levels of return (Boyte-White, 2020). On the

other hand, assets that have low risks have low returns as well. Therefore, to determine the

riskiness of an asset, investors apply the Capital asset pricing model.

On the other hand however, public listed companies seek to raise capital by issuing out

shares on the stock market. It is such a factor that gives rise to the concept of cost of equity of a

firm. Under normal circumstances, a public listed entity uses two main sources of capital and

these include the debt finance ordinary share financing. Therefore where an entity opts to use

equity financing, then this give s rise to the cost of equity. Alternatively, the cost of equity is

also known as the expected return on an investment especially for the shareholder. When using

the capital asset pricing model, the cost of equity also represents the current cost of equity of a

firm. Since the investor or ordinary share holder aims at generating returns, the company is

deemed to declare dividends. It is these dividends that are characterized as the cost of equity.

The capital asset pricing (CAPM) is therefore given by the formula stated as:

E (r) =r f + β ¿ ¿)

According to the above formula, E(r) is the known as the expected return of an asset. r f

on the other hand represents the risk free rate of the asset or stock. The β factor on the other

As previously mentioned, the capital asset pricing model a measure used to determine

and assess the expected return of an asset, security or stock. In the financial market different

securities have varying levels of risk attached. Due to such a scenario investors are tend to draw

closer attention to the risks associated with particular stocks or assets on the market. Some of the

stocks are highly risky whereas others have low levels of risks attached. It should however be

noted that the highly risky securities also have high levels of return (Boyte-White, 2020). On the

other hand, assets that have low risks have low returns as well. Therefore, to determine the

riskiness of an asset, investors apply the Capital asset pricing model.

On the other hand however, public listed companies seek to raise capital by issuing out

shares on the stock market. It is such a factor that gives rise to the concept of cost of equity of a

firm. Under normal circumstances, a public listed entity uses two main sources of capital and

these include the debt finance ordinary share financing. Therefore where an entity opts to use

equity financing, then this give s rise to the cost of equity. Alternatively, the cost of equity is

also known as the expected return on an investment especially for the shareholder. When using

the capital asset pricing model, the cost of equity also represents the current cost of equity of a

firm. Since the investor or ordinary share holder aims at generating returns, the company is

deemed to declare dividends. It is these dividends that are characterized as the cost of equity.

The capital asset pricing (CAPM) is therefore given by the formula stated as:

E (r) =r f + β ¿ ¿)

According to the above formula, E(r) is the known as the expected return of an asset. r f

on the other hand represents the risk free rate of the asset or stock. The β factor on the other

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE 4

hand shows the level of systematic risk of the stock. rm is the expected market return of the stock

or security and in this case, riot into is the security of interest.

The CAPM model can however be subdivided into two main parts to include the risk

free rate section and the risk premium (Rio Tinto Plc, 2017). The risk premium component

comprises of the stock’s beta multiplied by the difference between the market risk and the risk

fee rate of the stock. It is this component of the formula that determines the overall risk of the

stock is then obtained. Assuming that an investor is interested in the determining the market

return of Rio Tinto for the past six months, then the following calculation is applied.

Expected market return of Rio Tinto Group for six months would be determined as

follows: market return for 6 months = v1−v0

v0

* 100. Where v1 is the current stock price and v0 as

the starting price per share (Martin and Wagner, 2019). Therefore, to obtain the expected market

return of riot into group for six months the above formula is applied to the stock.

Market return (rm) = 45.58−45.51

45.51 * 100

= 0.08

45.51 * 100

= 0.1758% ≈ 0.2 %

Therefore in the last six months Rio Tinto Group has an average market return of about 0.2%.

The beta value of the stock for Rio Tinto Group is about 0.86 as obtained from yahoo finance in

the same period. It should be noted that beta is an indication of the level of riskiness associated

with an asset. In the market however, all stocks that have beta values exceeding 1 are deemed to

be highly risky (ACCA, 2020). Since Rio Tinto has a beta lower than 1, then it is relatively a

safe stock or asset. To determine the risk free rate, investors normally subtract the rate of

hand shows the level of systematic risk of the stock. rm is the expected market return of the stock

or security and in this case, riot into is the security of interest.

The CAPM model can however be subdivided into two main parts to include the risk

free rate section and the risk premium (Rio Tinto Plc, 2017). The risk premium component

comprises of the stock’s beta multiplied by the difference between the market risk and the risk

fee rate of the stock. It is this component of the formula that determines the overall risk of the

stock is then obtained. Assuming that an investor is interested in the determining the market

return of Rio Tinto for the past six months, then the following calculation is applied.

Expected market return of Rio Tinto Group for six months would be determined as

follows: market return for 6 months = v1−v0

v0

* 100. Where v1 is the current stock price and v0 as

the starting price per share (Martin and Wagner, 2019). Therefore, to obtain the expected market

return of riot into group for six months the above formula is applied to the stock.

Market return (rm) = 45.58−45.51

45.51 * 100

= 0.08

45.51 * 100

= 0.1758% ≈ 0.2 %

Therefore in the last six months Rio Tinto Group has an average market return of about 0.2%.

The beta value of the stock for Rio Tinto Group is about 0.86 as obtained from yahoo finance in

the same period. It should be noted that beta is an indication of the level of riskiness associated

with an asset. In the market however, all stocks that have beta values exceeding 1 are deemed to

be highly risky (ACCA, 2020). Since Rio Tinto has a beta lower than 1, then it is relatively a

safe stock or asset. To determine the risk free rate, investors normally subtract the rate of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE 5

inflation from the rate of return generated by the yield of a treasury bond in the same period.

Therefore assuming that Rio Tinto has a treasury bond with a yield rate of 8.65%, then the risk

free rate can be determined by Lessing the inflation rate in London from the above 8.65%. From

the office of the national statistics, inflation in London is rated around 1.8%. Therefore the risk

free rate of the stock is also obtained as: (8.65-1.8) %. Therefore, the risk free rate of the stock is

obtained as 6.85%. Given the above statistical figures, then the cost of equity for Rio Tinto

Group can be calculated as follows:

Cost of equity for Rio Tinto Group = E (r) =r f + β ¿ ¿). Since the values have been obtained as

explained above, then they can be substituted into the formula to determine Rio Tinto’s Cost of

equity while using the CAPM technique.

Where: rf = 6.85%

Rm = 0.2%

β = 0.8

So, the cost of equity is determined as; E(r) = 6.85% +0.8 (0.2-6.85)

= 6.85% + -5.32%

E(r) =1.5%

Therefore, the current cost of capital (expected return on investment) for Rio Tinto Group

is about 1.5% for the past six months as per the capital asset pricing model. Since the asset is

associated with a low level of risk, then the expected return or cost of equity is also low at only

about 1.5%. It should therefore be noted that the higher the risk of a stock or a security, the

higher the level or return or cost of equity.

B): Ungearing the Company’s Equity Beta to Derive Its Asset Beta

An asset’s equity beta is used to represent both the financial and business risk of an asset

or stock. It is therefore a technique through which the volatility of an asset is measured as

compare to the general market performance (ACCA, 2020). Stocks with high equity betas that

inflation from the rate of return generated by the yield of a treasury bond in the same period.

Therefore assuming that Rio Tinto has a treasury bond with a yield rate of 8.65%, then the risk

free rate can be determined by Lessing the inflation rate in London from the above 8.65%. From

the office of the national statistics, inflation in London is rated around 1.8%. Therefore the risk

free rate of the stock is also obtained as: (8.65-1.8) %. Therefore, the risk free rate of the stock is

obtained as 6.85%. Given the above statistical figures, then the cost of equity for Rio Tinto

Group can be calculated as follows:

Cost of equity for Rio Tinto Group = E (r) =r f + β ¿ ¿). Since the values have been obtained as

explained above, then they can be substituted into the formula to determine Rio Tinto’s Cost of

equity while using the CAPM technique.

Where: rf = 6.85%

Rm = 0.2%

β = 0.8

So, the cost of equity is determined as; E(r) = 6.85% +0.8 (0.2-6.85)

= 6.85% + -5.32%

E(r) =1.5%

Therefore, the current cost of capital (expected return on investment) for Rio Tinto Group

is about 1.5% for the past six months as per the capital asset pricing model. Since the asset is

associated with a low level of risk, then the expected return or cost of equity is also low at only

about 1.5%. It should therefore be noted that the higher the risk of a stock or a security, the

higher the level or return or cost of equity.

B): Ungearing the Company’s Equity Beta to Derive Its Asset Beta

An asset’s equity beta is used to represent both the financial and business risk of an asset

or stock. It is therefore a technique through which the volatility of an asset is measured as

compare to the general market performance (ACCA, 2020). Stocks with high equity betas that

CORPORATE FINANCE 6

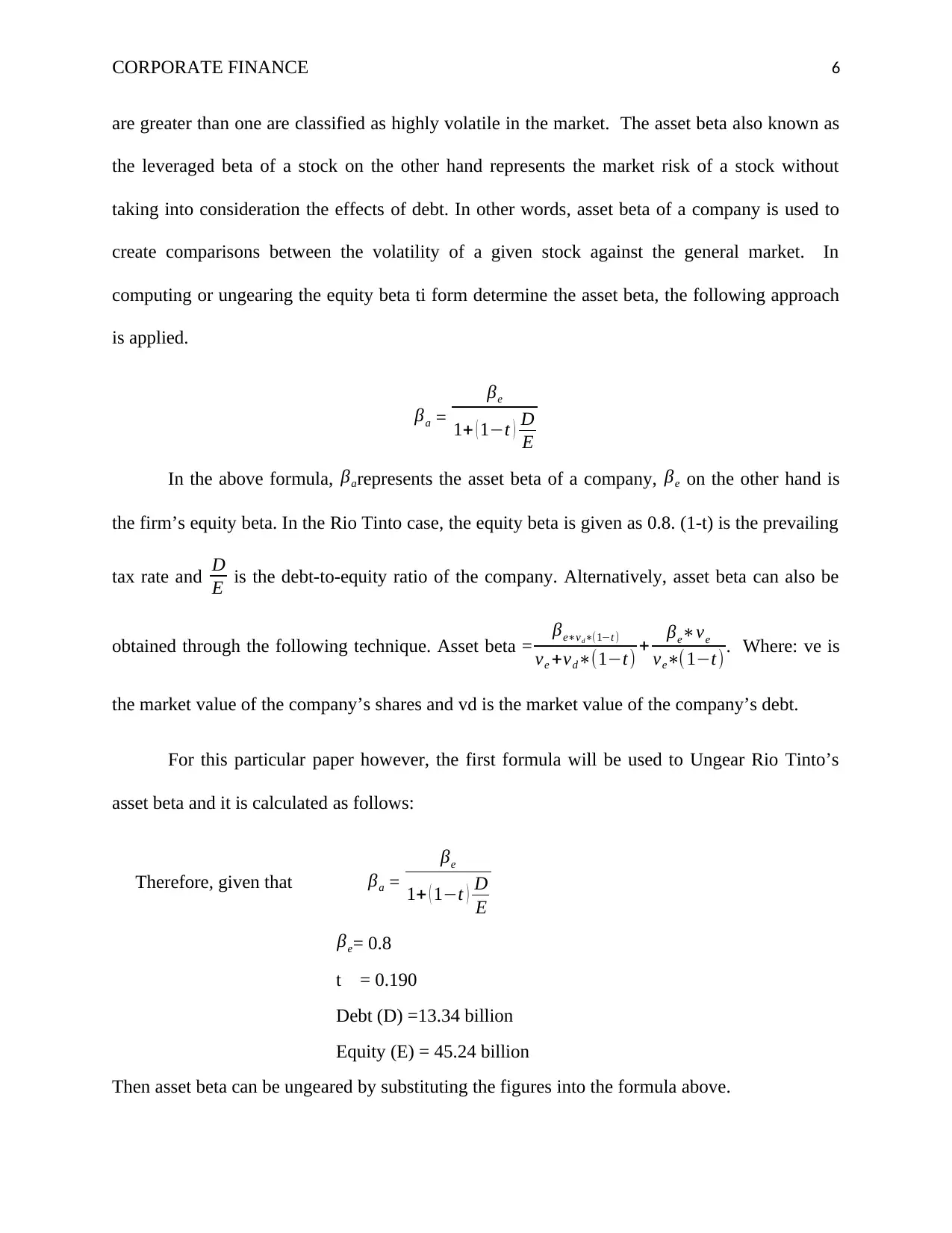

are greater than one are classified as highly volatile in the market. The asset beta also known as

the leveraged beta of a stock on the other hand represents the market risk of a stock without

taking into consideration the effects of debt. In other words, asset beta of a company is used to

create comparisons between the volatility of a given stock against the general market. In

computing or ungearing the equity beta ti form determine the asset beta, the following approach

is applied.

βa =

βe

1+ ( 1−t ) D

E

In the above formula, βarepresents the asset beta of a company, βe on the other hand is

the firm’s equity beta. In the Rio Tinto case, the equity beta is given as 0.8. (1-t) is the prevailing

tax rate and D

E is the debt-to-equity ratio of the company. Alternatively, asset beta can also be

obtained through the following technique. Asset beta = βe∗vd∗(1−t )

ve +vd∗(1−t) + βe∗ve

ve∗(1−t). Where: ve is

the market value of the company’s shares and vd is the market value of the company’s debt.

For this particular paper however, the first formula will be used to Ungear Rio Tinto’s

asset beta and it is calculated as follows:

Therefore, given that βa =

βe

1+ ( 1−t ) D

E

βe= 0.8

t = 0.190

Debt (D) =13.34 billion

Equity (E) = 45.24 billion

Then asset beta can be ungeared by substituting the figures into the formula above.

are greater than one are classified as highly volatile in the market. The asset beta also known as

the leveraged beta of a stock on the other hand represents the market risk of a stock without

taking into consideration the effects of debt. In other words, asset beta of a company is used to

create comparisons between the volatility of a given stock against the general market. In

computing or ungearing the equity beta ti form determine the asset beta, the following approach

is applied.

βa =

βe

1+ ( 1−t ) D

E

In the above formula, βarepresents the asset beta of a company, βe on the other hand is

the firm’s equity beta. In the Rio Tinto case, the equity beta is given as 0.8. (1-t) is the prevailing

tax rate and D

E is the debt-to-equity ratio of the company. Alternatively, asset beta can also be

obtained through the following technique. Asset beta = βe∗vd∗(1−t )

ve +vd∗(1−t) + βe∗ve

ve∗(1−t). Where: ve is

the market value of the company’s shares and vd is the market value of the company’s debt.

For this particular paper however, the first formula will be used to Ungear Rio Tinto’s

asset beta and it is calculated as follows:

Therefore, given that βa =

βe

1+ ( 1−t ) D

E

βe= 0.8

t = 0.190

Debt (D) =13.34 billion

Equity (E) = 45.24 billion

Then asset beta can be ungeared by substituting the figures into the formula above.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE 7

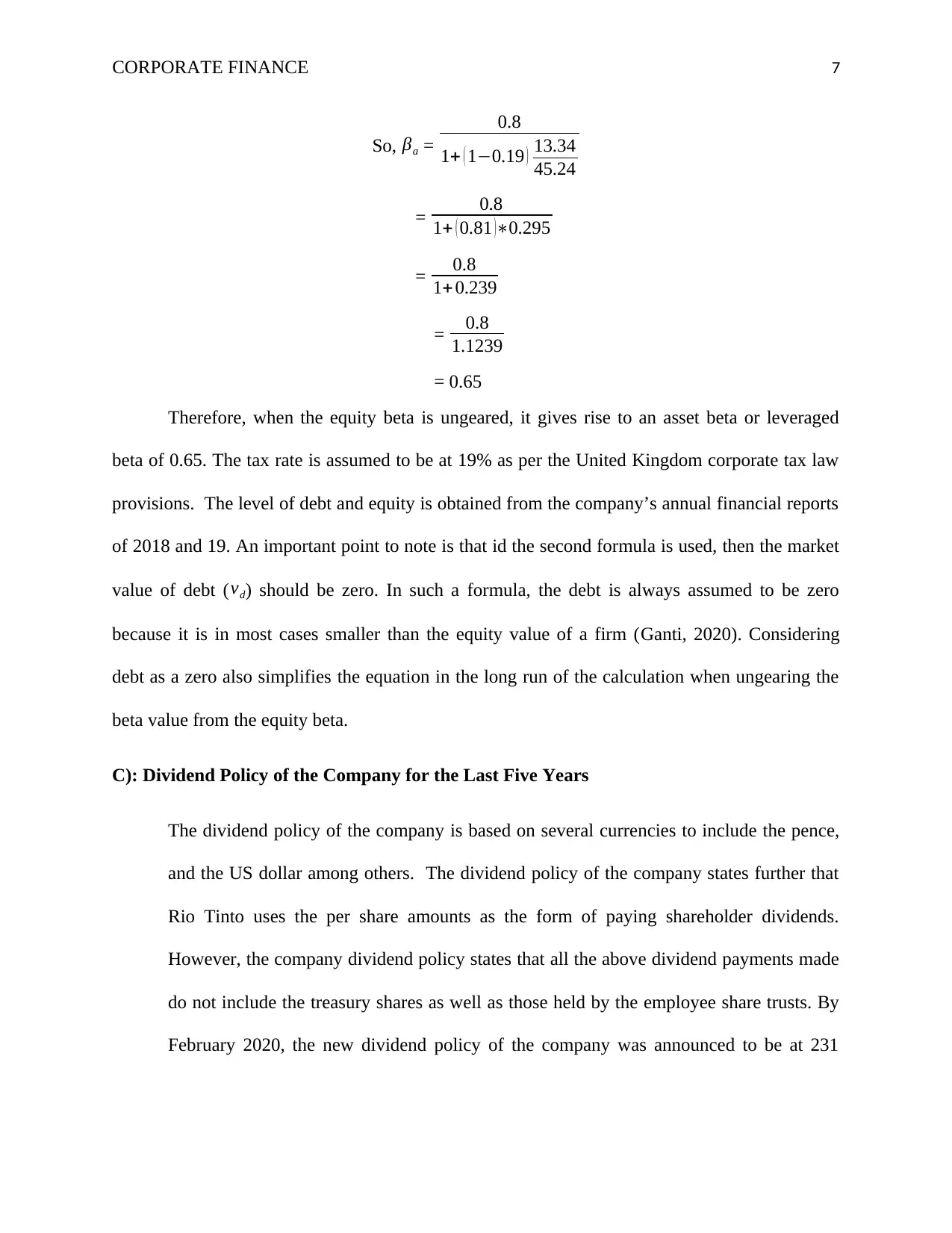

So, βa =

0.8

1+ ( 1−0.19 ) 13.34

45.24

= 0.8

1+ ( 0.81 )∗0.295

= 0.8

1+ 0.239

= 0.8

1.1239

= 0.65

Therefore, when the equity beta is ungeared, it gives rise to an asset beta or leveraged

beta of 0.65. The tax rate is assumed to be at 19% as per the United Kingdom corporate tax law

provisions. The level of debt and equity is obtained from the company’s annual financial reports

of 2018 and 19. An important point to note is that id the second formula is used, then the market

value of debt ( vd) should be zero. In such a formula, the debt is always assumed to be zero

because it is in most cases smaller than the equity value of a firm (Ganti, 2020). Considering

debt as a zero also simplifies the equation in the long run of the calculation when ungearing the

beta value from the equity beta.

C): Dividend Policy of the Company for the Last Five Years

The dividend policy of the company is based on several currencies to include the pence,

and the US dollar among others. The dividend policy of the company states further that

Rio Tinto uses the per share amounts as the form of paying shareholder dividends.

However, the company dividend policy states that all the above dividend payments made

do not include the treasury shares as well as those held by the employee share trusts. By

February 2020, the new dividend policy of the company was announced to be at 231

So, βa =

0.8

1+ ( 1−0.19 ) 13.34

45.24

= 0.8

1+ ( 0.81 )∗0.295

= 0.8

1+ 0.239

= 0.8

1.1239

= 0.65

Therefore, when the equity beta is ungeared, it gives rise to an asset beta or leveraged

beta of 0.65. The tax rate is assumed to be at 19% as per the United Kingdom corporate tax law

provisions. The level of debt and equity is obtained from the company’s annual financial reports

of 2018 and 19. An important point to note is that id the second formula is used, then the market

value of debt ( vd) should be zero. In such a formula, the debt is always assumed to be zero

because it is in most cases smaller than the equity value of a firm (Ganti, 2020). Considering

debt as a zero also simplifies the equation in the long run of the calculation when ungearing the

beta value from the equity beta.

C): Dividend Policy of the Company for the Last Five Years

The dividend policy of the company is based on several currencies to include the pence,

and the US dollar among others. The dividend policy of the company states further that

Rio Tinto uses the per share amounts as the form of paying shareholder dividends.

However, the company dividend policy states that all the above dividend payments made

do not include the treasury shares as well as those held by the employee share trusts. By

February 2020, the new dividend policy of the company was announced to be at 231

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE 8

cents per share. The policy also provides all dividend payments will be franked from the

present franking credits coming from income tax payments

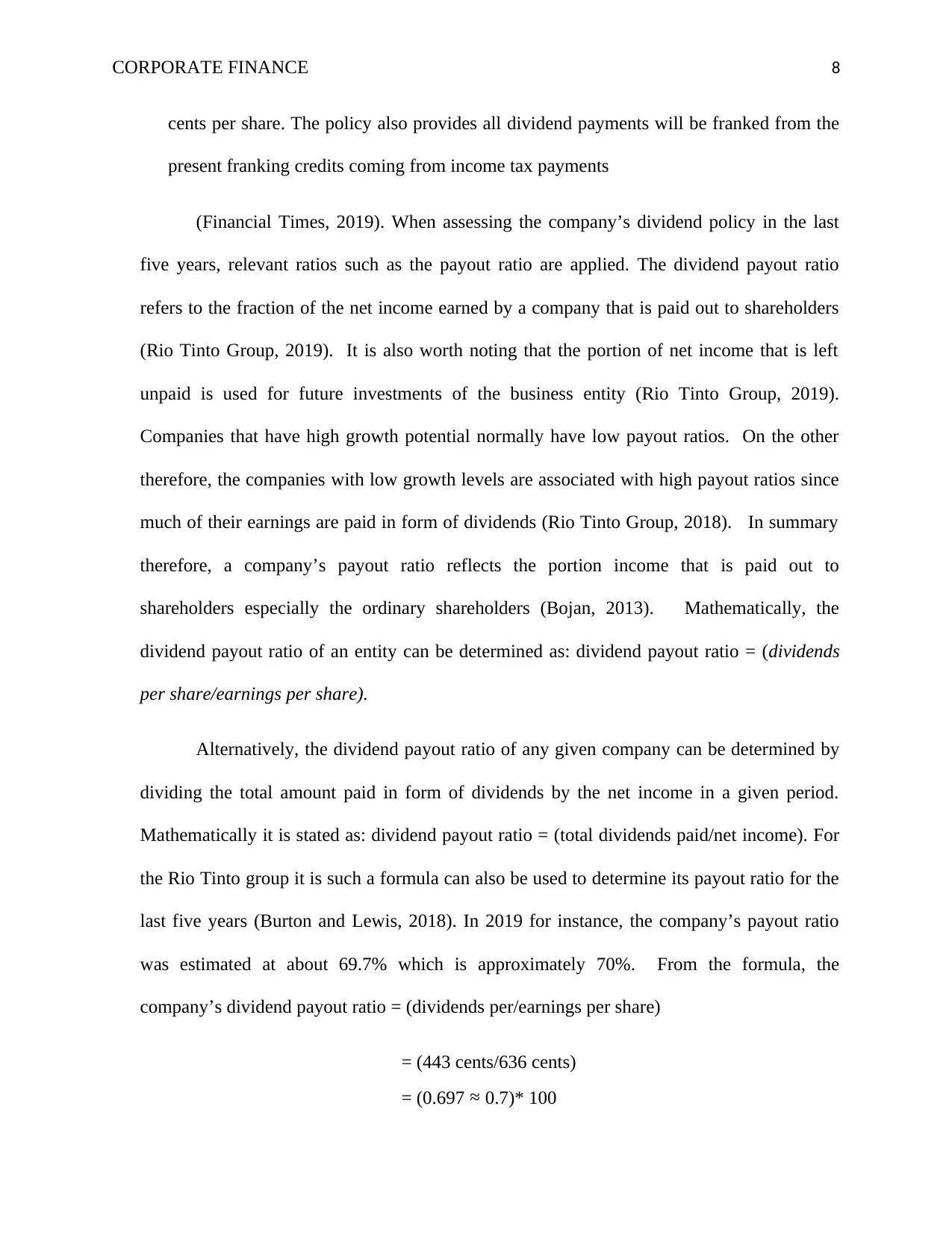

(Financial Times, 2019). When assessing the company’s dividend policy in the last

five years, relevant ratios such as the payout ratio are applied. The dividend payout ratio

refers to the fraction of the net income earned by a company that is paid out to shareholders

(Rio Tinto Group, 2019). It is also worth noting that the portion of net income that is left

unpaid is used for future investments of the business entity (Rio Tinto Group, 2019).

Companies that have high growth potential normally have low payout ratios. On the other

therefore, the companies with low growth levels are associated with high payout ratios since

much of their earnings are paid in form of dividends (Rio Tinto Group, 2018). In summary

therefore, a company’s payout ratio reflects the portion income that is paid out to

shareholders especially the ordinary shareholders (Bojan, 2013). Mathematically, the

dividend payout ratio of an entity can be determined as: dividend payout ratio = (dividends

per share/earnings per share).

Alternatively, the dividend payout ratio of any given company can be determined by

dividing the total amount paid in form of dividends by the net income in a given period.

Mathematically it is stated as: dividend payout ratio = (total dividends paid/net income). For

the Rio Tinto group it is such a formula can also be used to determine its payout ratio for the

last five years (Burton and Lewis, 2018). In 2019 for instance, the company’s payout ratio

was estimated at about 69.7% which is approximately 70%. From the formula, the

company’s dividend payout ratio = (dividends per/earnings per share)

= (443 cents/636 cents)

= (0.697 ≈ 0.7)* 100

cents per share. The policy also provides all dividend payments will be franked from the

present franking credits coming from income tax payments

(Financial Times, 2019). When assessing the company’s dividend policy in the last

five years, relevant ratios such as the payout ratio are applied. The dividend payout ratio

refers to the fraction of the net income earned by a company that is paid out to shareholders

(Rio Tinto Group, 2019). It is also worth noting that the portion of net income that is left

unpaid is used for future investments of the business entity (Rio Tinto Group, 2019).

Companies that have high growth potential normally have low payout ratios. On the other

therefore, the companies with low growth levels are associated with high payout ratios since

much of their earnings are paid in form of dividends (Rio Tinto Group, 2018). In summary

therefore, a company’s payout ratio reflects the portion income that is paid out to

shareholders especially the ordinary shareholders (Bojan, 2013). Mathematically, the

dividend payout ratio of an entity can be determined as: dividend payout ratio = (dividends

per share/earnings per share).

Alternatively, the dividend payout ratio of any given company can be determined by

dividing the total amount paid in form of dividends by the net income in a given period.

Mathematically it is stated as: dividend payout ratio = (total dividends paid/net income). For

the Rio Tinto group it is such a formula can also be used to determine its payout ratio for the

last five years (Burton and Lewis, 2018). In 2019 for instance, the company’s payout ratio

was estimated at about 69.7% which is approximately 70%. From the formula, the

company’s dividend payout ratio = (dividends per/earnings per share)

= (443 cents/636 cents)

= (0.697 ≈ 0.7)* 100

CORPORATE FINANCE 9

= 70%

Therefore, according to the calculation, the company’s payout ratio is over 50%

implying that Rio Tinto group has sufficient earnings to cover its dividend payments.

On average, in the last five years the company has also registered a trailing twelve-

month payout ratio of about 58.59%.

D) A Critical Evaluation Of CAPM And The Dividend Growth Model For Rio Tinto

Group

For an investor to effectively manage a security or a portfolio of stocks, an investor

has to critically evaluate the factors and aspects. Due to such a condition, the need to evaluate

an asset with various approaches. The dividend growth model and the capital asset pricing

model are some of the common methods through which an investment can be assessed.

Unlike the Capital Asset Pricing Model, the dividend growth model primarily focuses on the

amount of dividends that can be generated from a particular stock (Corporate Finance

Institute, 2020). The capital asset pricing model on the other hand emphasizes other external

factors such as risk and rate of return that of an asset. For the Rio Tinto Group therefore, the

both techniques are critically important. Therefore, it is important to note that investors are

more interested in the return that an asset can bring. Therefore, to attract such investors Rio

Tinto needs to apply the dividend growth model.

On the other hand however, the capital asset pricing model is also a significant

technique for the company. Since Rio Tinto Group is a public listed entity, there evaluate its

market performance against the general market average. Ultimately the need to apply the

CAPM is inevitable for the company of Rio Tinto Group. Therefore, the student takes the

= 70%

Therefore, according to the calculation, the company’s payout ratio is over 50%

implying that Rio Tinto group has sufficient earnings to cover its dividend payments.

On average, in the last five years the company has also registered a trailing twelve-

month payout ratio of about 58.59%.

D) A Critical Evaluation Of CAPM And The Dividend Growth Model For Rio Tinto

Group

For an investor to effectively manage a security or a portfolio of stocks, an investor

has to critically evaluate the factors and aspects. Due to such a condition, the need to evaluate

an asset with various approaches. The dividend growth model and the capital asset pricing

model are some of the common methods through which an investment can be assessed.

Unlike the Capital Asset Pricing Model, the dividend growth model primarily focuses on the

amount of dividends that can be generated from a particular stock (Corporate Finance

Institute, 2020). The capital asset pricing model on the other hand emphasizes other external

factors such as risk and rate of return that of an asset. For the Rio Tinto Group therefore, the

both techniques are critically important. Therefore, it is important to note that investors are

more interested in the return that an asset can bring. Therefore, to attract such investors Rio

Tinto needs to apply the dividend growth model.

On the other hand however, the capital asset pricing model is also a significant

technique for the company. Since Rio Tinto Group is a public listed entity, there evaluate its

market performance against the general market average. Ultimately the need to apply the

CAPM is inevitable for the company of Rio Tinto Group. Therefore, the student takes the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE 10

stand that both the dividend growth model and the capital asset pricing model are

significantly important for the company (Ker, 2016). The decision to use only one technique

has several underlying adverse outcomes that have the potential to negatively impact

business. The dividend growth model of the company is applicable is critical when

ascertaining the stock shares depending on the company’s future dividends (Martin, 2016).

Therefore, by using the dividend growth model, Rio Tinto Group can ably determine its

dividend value for the future periods. It has to be noted however that such future projections

can only be applicable for five years. Beyond such a period the company is then deemed to

less detailed projections. The mathematical formula of the model is then applied and the

future values of the company’s dividends. Discounting such future dividends will then be

used as a way of determining the present value of the company (Team, 2019).

The capital asset pricing model approach on the other hand is suitable for purposes of

analyzing the market conditions. With the capital asset pricing model, decision making takes

a broader perspective which includes the market risk, risk free rate the beta factor and the

expected cost of capital. Since the model allows comparisons between the company

performance against the market average return (Pan, 2020). The most outstanding benefit of

using the capital asset pricing model is that an investor or the company can easily assess the

riskiness of the stock on the market. In a broader perspective, the capital asset pricing model

is a slightly more applicable than the dividend growth model.

Because the capital asset pricing model provides a detailed view of the entity, the

investment appraisal estimates are more reliable than the dividend payout ratio estimates.

Most investors put significant emphasis on matters of risk and yet the dividend growth model

stand that both the dividend growth model and the capital asset pricing model are

significantly important for the company (Ker, 2016). The decision to use only one technique

has several underlying adverse outcomes that have the potential to negatively impact

business. The dividend growth model of the company is applicable is critical when

ascertaining the stock shares depending on the company’s future dividends (Martin, 2016).

Therefore, by using the dividend growth model, Rio Tinto Group can ably determine its

dividend value for the future periods. It has to be noted however that such future projections

can only be applicable for five years. Beyond such a period the company is then deemed to

less detailed projections. The mathematical formula of the model is then applied and the

future values of the company’s dividends. Discounting such future dividends will then be

used as a way of determining the present value of the company (Team, 2019).

The capital asset pricing model approach on the other hand is suitable for purposes of

analyzing the market conditions. With the capital asset pricing model, decision making takes

a broader perspective which includes the market risk, risk free rate the beta factor and the

expected cost of capital. Since the model allows comparisons between the company

performance against the market average return (Pan, 2020). The most outstanding benefit of

using the capital asset pricing model is that an investor or the company can easily assess the

riskiness of the stock on the market. In a broader perspective, the capital asset pricing model

is a slightly more applicable than the dividend growth model.

Because the capital asset pricing model provides a detailed view of the entity, the

investment appraisal estimates are more reliable than the dividend payout ratio estimates.

Most investors put significant emphasis on matters of risk and yet the dividend growth model

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE 11

does not reflect such scenarios (Nel, 2011). Therefore, analyzing the investment appraisal

process while using the dividend growth model is to a certain level unreliable.

On the contrary however, none of the two methods of investment appraisal techniques

is perfect. The fact that both approaches depend on various assumptions regarding the future,

the estimates are always subjected to flaws and errors (Kenton, 2019). In order to predict

long term investment, an entity has to forecast a dividend policy of over five or ten years

ahead. In the real life of investment such predictions are not realistic due to the numerous

uncertainties in the market. The capital asset pricing model on the other hand does not take

into consideration factors such as unsystematic risks. The unsystematic risks in such a sense

represent those risks that occur in a particular industry or type of market alone. Therefore, for

companies that are highly specialized such as the Rio Tinto Group, the capital asset pricing

model may not be highly reliable (Toms, 2012).

In the financial market, daily information and data is associated with several non-

trading periods and such a situation results in an inaccurate systematic risk as used by the

capital asset pricing model. In most cases, the full effect resulting from new market

information is in most cases not immediately reflected in the share prices of the stock or

security. Such a tendency is due to the fact there are significant delays in adjusting stock

prices Coffie and Chukwulobelu, 2012). For instance, in the mining industry price changes

for mineral assets or stocks take long periods before reacting to the prevailing information

and market data. Consequently, when an investor uses short return interval the systematic

risks in the model are erroneous. It is therefore very advisable to use the long term return

interval such as monthly intervals, six-month intervals among others (Nhleko and

Musingwini, 2016). The long term intervals are help in reducing the price adjustment biases.

does not reflect such scenarios (Nel, 2011). Therefore, analyzing the investment appraisal

process while using the dividend growth model is to a certain level unreliable.

On the contrary however, none of the two methods of investment appraisal techniques

is perfect. The fact that both approaches depend on various assumptions regarding the future,

the estimates are always subjected to flaws and errors (Kenton, 2019). In order to predict

long term investment, an entity has to forecast a dividend policy of over five or ten years

ahead. In the real life of investment such predictions are not realistic due to the numerous

uncertainties in the market. The capital asset pricing model on the other hand does not take

into consideration factors such as unsystematic risks. The unsystematic risks in such a sense

represent those risks that occur in a particular industry or type of market alone. Therefore, for

companies that are highly specialized such as the Rio Tinto Group, the capital asset pricing

model may not be highly reliable (Toms, 2012).

In the financial market, daily information and data is associated with several non-

trading periods and such a situation results in an inaccurate systematic risk as used by the

capital asset pricing model. In most cases, the full effect resulting from new market

information is in most cases not immediately reflected in the share prices of the stock or

security. Such a tendency is due to the fact there are significant delays in adjusting stock

prices Coffie and Chukwulobelu, 2012). For instance, in the mining industry price changes

for mineral assets or stocks take long periods before reacting to the prevailing information

and market data. Consequently, when an investor uses short return interval the systematic

risks in the model are erroneous. It is therefore very advisable to use the long term return

interval such as monthly intervals, six-month intervals among others (Nhleko and

Musingwini, 2016). The long term intervals are help in reducing the price adjustment biases.

CORPORATE FINANCE 12

Therefore, as earlier stated, the capital asset pricing model is a relatively better investment

appraisal approach for the Rio Tinto Group.

Conclusion

The capital asset pricing model is the most commonly used approach for determining the

cost of equity for the public listed companies. Several investors find the model’s return and risk

factors very intuitive in investment practices. Although there is still limited research supporting

the application of the technique, the capital asset pricing model is strongly backed theoretically.

On the other, the dividend growth model of investment appraisal is considered as the easiest

approach for valuing a stock or an asset. To determine the present value of a particular stock, the

model only requires an individual to discount down all the future dividend payments. The

growth of a company is therefore estimated to follow a constant infinite rate and trend (Nhleko,

2015).It is however, limited by the fact that there is no significant evidence supporting the

constant growth infinite growth rate in of dividends. Therefore, it is largely advisable for Rio

Tinto Group to use a combination of the two types of investment appraisal techniques. Relying

on a single method can significantly affect the overall performance of the company especially in

cases of critical uncertainties (Piplovic, 2018).The dividend growth model allows the company to

ascertain the dividends as well as measuring the company’s growth. The capital asset pricing

model on the other hand is then used to determine and asses underlying factors such as

systematic risk and expected return.

Therefore, as earlier stated, the capital asset pricing model is a relatively better investment

appraisal approach for the Rio Tinto Group.

Conclusion

The capital asset pricing model is the most commonly used approach for determining the

cost of equity for the public listed companies. Several investors find the model’s return and risk

factors very intuitive in investment practices. Although there is still limited research supporting

the application of the technique, the capital asset pricing model is strongly backed theoretically.

On the other, the dividend growth model of investment appraisal is considered as the easiest

approach for valuing a stock or an asset. To determine the present value of a particular stock, the

model only requires an individual to discount down all the future dividend payments. The

growth of a company is therefore estimated to follow a constant infinite rate and trend (Nhleko,

2015).It is however, limited by the fact that there is no significant evidence supporting the

constant growth infinite growth rate in of dividends. Therefore, it is largely advisable for Rio

Tinto Group to use a combination of the two types of investment appraisal techniques. Relying

on a single method can significantly affect the overall performance of the company especially in

cases of critical uncertainties (Piplovic, 2018).The dividend growth model allows the company to

ascertain the dividends as well as measuring the company’s growth. The capital asset pricing

model on the other hand is then used to determine and asses underlying factors such as

systematic risk and expected return.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.