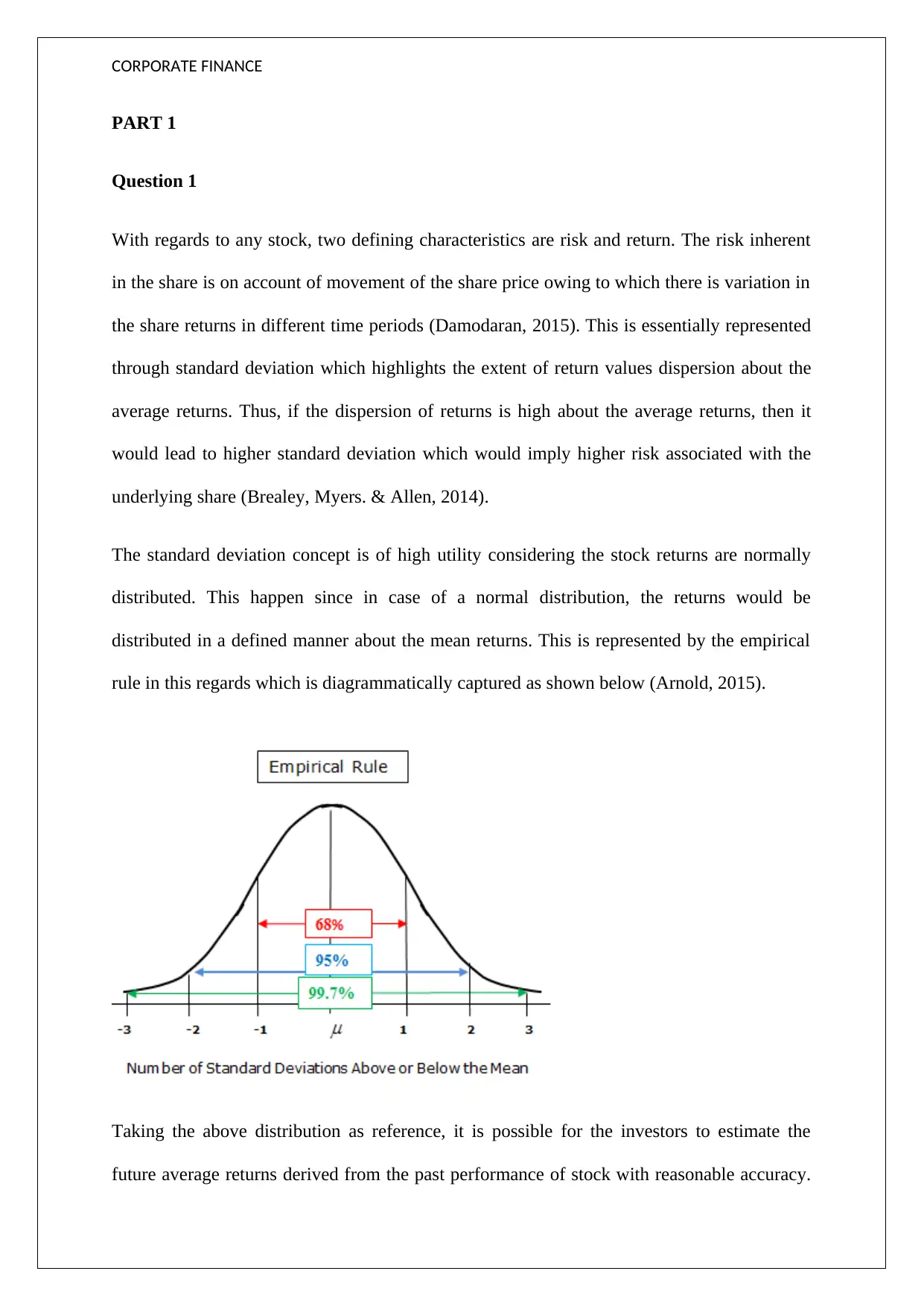

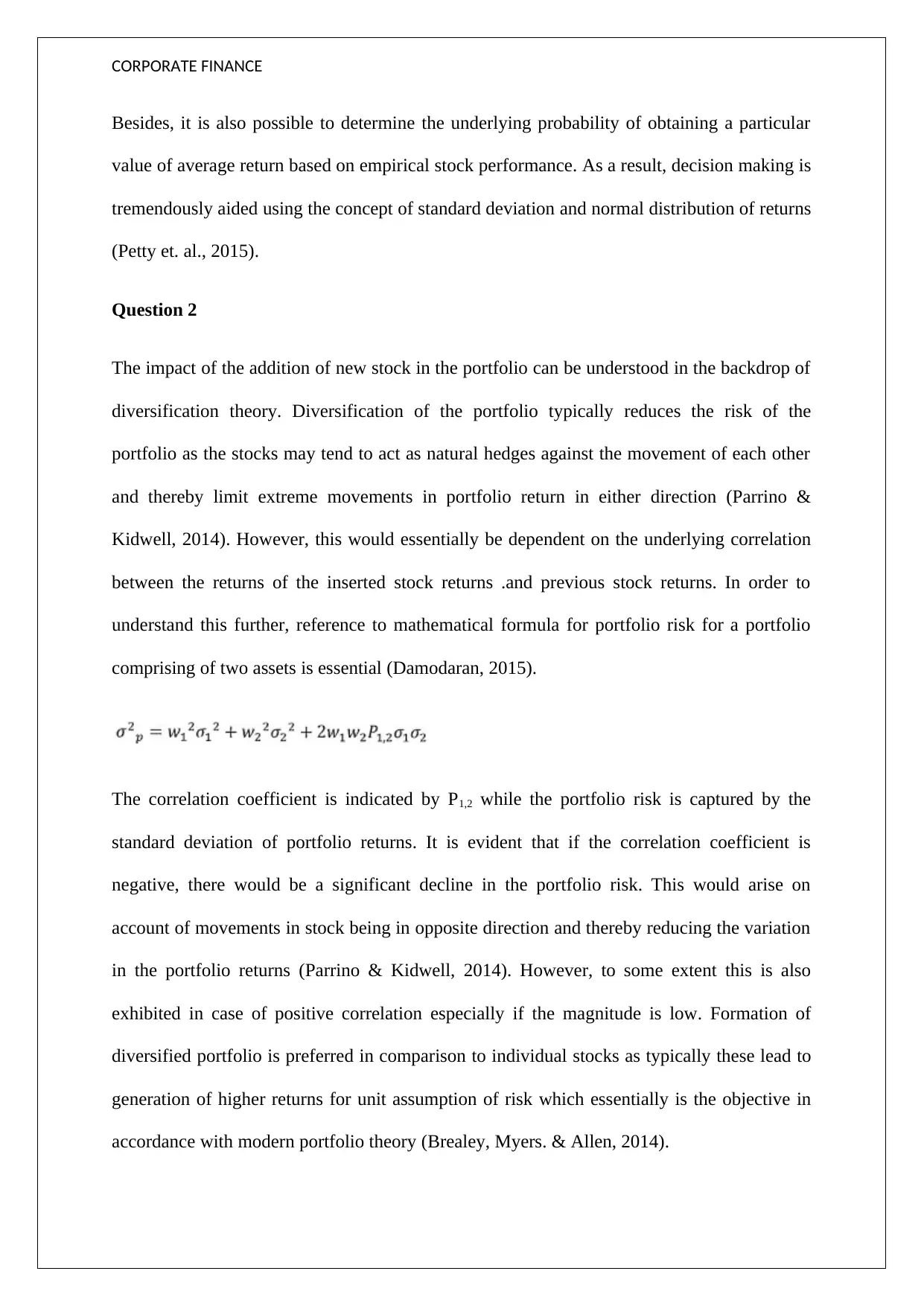

Corporate Finance Assignment: Analyzing Risk, Return, and Portfolios

VerifiedAdded on 2021/11/13

|5

|903

|22

Homework Assignment

AI Summary

This assignment delves into fundamental concepts in corporate finance, examining the relationship between risk and return in stock investments. It explores the use of standard deviation to quantify risk and its implications for investment decisions, particularly in normally distributed return scenarios. The assignment also addresses portfolio diversification, explaining how adding new stocks can reduce overall portfolio risk based on correlation coefficients. Finally, it provides a mathematical analysis of portfolio risk involving a risk-free asset, demonstrating how the portfolio's risk is influenced by the weight and risk of the risky asset. The assignment draws on established financial literature to support its analysis, offering insights into key financial management principles.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.