Investment Analysis and Share Price Movement: Corporate Finance

VerifiedAdded on 2020/05/11

|16

|2061

|76

Report

AI Summary

This report analyzes the corporate financial management of Riverlea, focusing on the evaluation of investment options in confectionary production. Part 1 assesses the financial outcomes using investment appraisal techniques such as Net Present Value (NPV), Internal Rate of Return (IRR), payback period, and discounted payback period, under various scenarios including sensitivity analysis with different probabilities of revenue changes. The analysis aims to determine the viability and financial stability of the project, recommending whether Riverlea should commence confectionary production. Part 2 evaluates the impact of announcements on Riverlea's share price, examining market efficiency and potential trading strategies like short selling to generate revenue. The report identifies the influence of market efficiency on share prices and how investors' expectations reflect in the share price movement. The findings suggest that Riverlea's shares are affected by strong market efficiency, and strategies like short selling could be used to capitalize on share price fluctuations.

Running head: CORPORATE FINANCIAL MANAGEMENT

Corporate Financial Management

Name of the Student:

Name of the University:

Authors Note:

Corporate Financial Management

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCIAL MANAGEMENT

1

Executive Summary:

The relevant evaluation of investment options is mainly conducted to understand the financial

outcome, which could be provided from production of confectionaries. There are different

types of scenarios, which could be conducted for determining the overall viability of the

investment option. Relevant scenarios could be conducted for deriving the financial stability

and feasibility of the production of confectionaries. In addition, the overall investment

analysis is mainly conducted on different scenarios, where the range of income that could be

presented from investment is depicted. The investment appraisal techniques mainly represent

the overall financial stability of the new project, which could increase firm value in future.

Therefore, it is advisable to Riverlea to commence with the production of confectionaries in

their production function.

The relevant evaluation is mainly conducted on the share price movement of Riverlea after

the announcement of extra income that will be generated in near future. In addition, the

overall valuation could mainly indicate overall impact of the announcement, which is

conducted on the share price of the company. Relevant calculation is mainly conducted to

detect the probability of the share price value after the announcement. Therefore, from the

evaluation it could be identified that shares of Riverlea is directly affected by strong market

efficiency. In addition, share price movement after the announcement mainly indicates that

the share price of the company adequately reflected to the news. The overall investment

strategy such as short selling could be conducted by the organisation for generating higher

revenue from investment.

1

Executive Summary:

The relevant evaluation of investment options is mainly conducted to understand the financial

outcome, which could be provided from production of confectionaries. There are different

types of scenarios, which could be conducted for determining the overall viability of the

investment option. Relevant scenarios could be conducted for deriving the financial stability

and feasibility of the production of confectionaries. In addition, the overall investment

analysis is mainly conducted on different scenarios, where the range of income that could be

presented from investment is depicted. The investment appraisal techniques mainly represent

the overall financial stability of the new project, which could increase firm value in future.

Therefore, it is advisable to Riverlea to commence with the production of confectionaries in

their production function.

The relevant evaluation is mainly conducted on the share price movement of Riverlea after

the announcement of extra income that will be generated in near future. In addition, the

overall valuation could mainly indicate overall impact of the announcement, which is

conducted on the share price of the company. Relevant calculation is mainly conducted to

detect the probability of the share price value after the announcement. Therefore, from the

evaluation it could be identified that shares of Riverlea is directly affected by strong market

efficiency. In addition, share price movement after the announcement mainly indicates that

the share price of the company adequately reflected to the news. The overall investment

strategy such as short selling could be conducted by the organisation for generating higher

revenue from investment.

CORPORATE FINANCIAL MANAGEMENT

2

Table of Contents

Part 1:.........................................................................................................................................3

1. Introduction:...........................................................................................................................3

2. Findings:.................................................................................................................................3

2.1 Calculating the Discounted Rate:.........................................................................................3

2.2 Drafting the expected cash flows of the project:..................................................................4

2.3 Sensitivity Analysis:.............................................................................................................6

2.3.1 Drafting the cash flow when 40% probability is there for 40% lowers incremental

revenues:....................................................................................................................................6

2.3.2 Drafting the cash flow when 10% probability is there for 20% increase in incremental

revenues:....................................................................................................................................8

3. Concussion and Recommendations:....................................................................................10

Part 2:.......................................................................................................................................10

1. Introduction:.........................................................................................................................10

2. Findings:...............................................................................................................................11

2.1 Determining that stock has semi-strong market efficiency:...............................................11

2.2 Portraying the relevant trading strategy:............................................................................13

3. Concussion and Recommendations:....................................................................................13

Reference and Bibliography:....................................................................................................14

2

Table of Contents

Part 1:.........................................................................................................................................3

1. Introduction:...........................................................................................................................3

2. Findings:.................................................................................................................................3

2.1 Calculating the Discounted Rate:.........................................................................................3

2.2 Drafting the expected cash flows of the project:..................................................................4

2.3 Sensitivity Analysis:.............................................................................................................6

2.3.1 Drafting the cash flow when 40% probability is there for 40% lowers incremental

revenues:....................................................................................................................................6

2.3.2 Drafting the cash flow when 10% probability is there for 20% increase in incremental

revenues:....................................................................................................................................8

3. Concussion and Recommendations:....................................................................................10

Part 2:.......................................................................................................................................10

1. Introduction:.........................................................................................................................10

2. Findings:...............................................................................................................................11

2.1 Determining that stock has semi-strong market efficiency:...............................................11

2.2 Portraying the relevant trading strategy:............................................................................13

3. Concussion and Recommendations:....................................................................................13

Reference and Bibliography:....................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCIAL MANAGEMENT

3

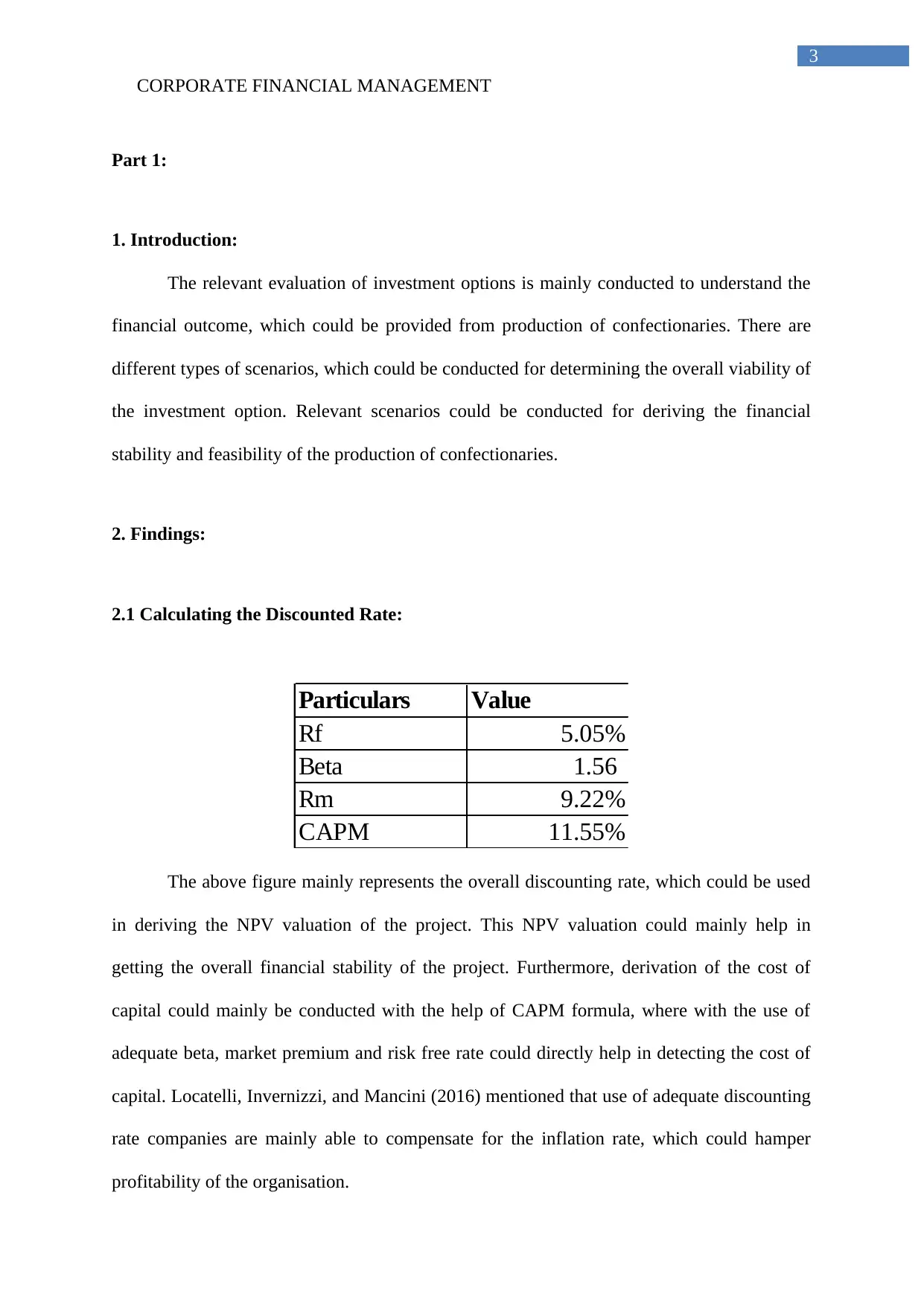

Part 1:

1. Introduction:

The relevant evaluation of investment options is mainly conducted to understand the

financial outcome, which could be provided from production of confectionaries. There are

different types of scenarios, which could be conducted for determining the overall viability of

the investment option. Relevant scenarios could be conducted for deriving the financial

stability and feasibility of the production of confectionaries.

2. Findings:

2.1 Calculating the Discounted Rate:

Particulars Value

Rf 5.05%

Beta 1.56

Rm 9.22%

CAPM 11.55%

The above figure mainly represents the overall discounting rate, which could be used

in deriving the NPV valuation of the project. This NPV valuation could mainly help in

getting the overall financial stability of the project. Furthermore, derivation of the cost of

capital could mainly be conducted with the help of CAPM formula, where with the use of

adequate beta, market premium and risk free rate could directly help in detecting the cost of

capital. Locatelli, Invernizzi, and Mancini (2016) mentioned that use of adequate discounting

rate companies are mainly able to compensate for the inflation rate, which could hamper

profitability of the organisation.

3

Part 1:

1. Introduction:

The relevant evaluation of investment options is mainly conducted to understand the

financial outcome, which could be provided from production of confectionaries. There are

different types of scenarios, which could be conducted for determining the overall viability of

the investment option. Relevant scenarios could be conducted for deriving the financial

stability and feasibility of the production of confectionaries.

2. Findings:

2.1 Calculating the Discounted Rate:

Particulars Value

Rf 5.05%

Beta 1.56

Rm 9.22%

CAPM 11.55%

The above figure mainly represents the overall discounting rate, which could be used

in deriving the NPV valuation of the project. This NPV valuation could mainly help in

getting the overall financial stability of the project. Furthermore, derivation of the cost of

capital could mainly be conducted with the help of CAPM formula, where with the use of

adequate beta, market premium and risk free rate could directly help in detecting the cost of

capital. Locatelli, Invernizzi, and Mancini (2016) mentioned that use of adequate discounting

rate companies are mainly able to compensate for the inflation rate, which could hamper

profitability of the organisation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCIAL MANAGEMENT

4

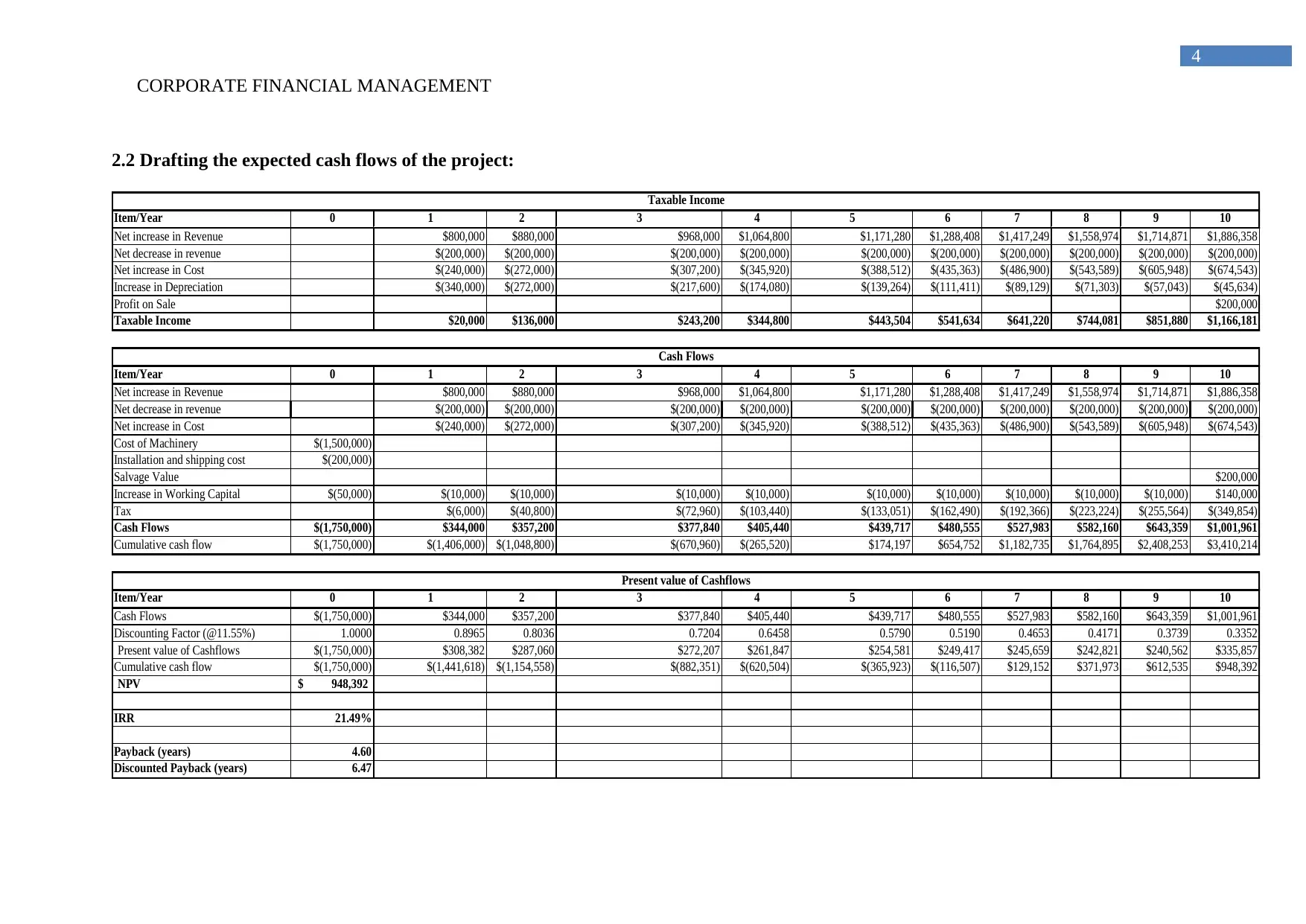

2.2 Drafting the expected cash flows of the project:

Item/Year 0 1 2 3 4 5 6 7 8 9 10

Net increase in Revenue $800,000 $880,000 $968,000 $1,064,800 $1,171,280 $1,288,408 $1,417,249 $1,558,974 $1,714,871 $1,886,358

Net decrease in revenue $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000)

Net increase in Cost $(240,000) $(272,000) $(307,200) $(345,920) $(388,512) $(435,363) $(486,900) $(543,589) $(605,948) $(674,543)

Increase in Depreciation $(340,000) $(272,000) $(217,600) $(174,080) $(139,264) $(111,411) $(89,129) $(71,303) $(57,043) $(45,634)

Profit on Sale $200,000

Taxable Income $20,000 $136,000 $243,200 $344,800 $443,504 $541,634 $641,220 $744,081 $851,880 $1,166,181

Item/Year 0 1 2 3 4 5 6 7 8 9 10

Net increase in Revenue $800,000 $880,000 $968,000 $1,064,800 $1,171,280 $1,288,408 $1,417,249 $1,558,974 $1,714,871 $1,886,358

Net decrease in revenue $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000)

Net increase in Cost $(240,000) $(272,000) $(307,200) $(345,920) $(388,512) $(435,363) $(486,900) $(543,589) $(605,948) $(674,543)

Cost of Machinery $(1,500,000)

Installation and shipping cost $(200,000)

Salvage Value $200,000

Increase in Working Capital $(50,000) $(10,000) $(10,000) $(10,000) $(10,000) $(10,000) $(10,000) $(10,000) $(10,000) $(10,000) $140,000

Tax $(6,000) $(40,800) $(72,960) $(103,440) $(133,051) $(162,490) $(192,366) $(223,224) $(255,564) $(349,854)

Cash Flows $(1,750,000) $344,000 $357,200 $377,840 $405,440 $439,717 $480,555 $527,983 $582,160 $643,359 $1,001,961

Cumulative cash flow $(1,750,000) $(1,406,000) $(1,048,800) $(670,960) $(265,520) $174,197 $654,752 $1,182,735 $1,764,895 $2,408,253 $3,410,214

Item/Year 0 1 2 3 4 5 6 7 8 9 10

Cash Flows $(1,750,000) $344,000 $357,200 $377,840 $405,440 $439,717 $480,555 $527,983 $582,160 $643,359 $1,001,961

Discounting Factor (@11.55%) 1.0000 0.8965 0.8036 0.7204 0.6458 0.5790 0.5190 0.4653 0.4171 0.3739 0.3352

Present value of Cashflows $(1,750,000) $308,382 $287,060 $272,207 $261,847 $254,581 $249,417 $245,659 $242,821 $240,562 $335,857

Cumulative cash flow $(1,750,000) $(1,441,618) $(1,154,558) $(882,351) $(620,504) $(365,923) $(116,507) $129,152 $371,973 $612,535 $948,392

NPV 948,392$

IRR 21.49%

Payback (years) 4.60

Discounted Payback (years) 6.47

Taxable Income

Cash Flows

Present value of Cashflows

4

2.2 Drafting the expected cash flows of the project:

Item/Year 0 1 2 3 4 5 6 7 8 9 10

Net increase in Revenue $800,000 $880,000 $968,000 $1,064,800 $1,171,280 $1,288,408 $1,417,249 $1,558,974 $1,714,871 $1,886,358

Net decrease in revenue $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000)

Net increase in Cost $(240,000) $(272,000) $(307,200) $(345,920) $(388,512) $(435,363) $(486,900) $(543,589) $(605,948) $(674,543)

Increase in Depreciation $(340,000) $(272,000) $(217,600) $(174,080) $(139,264) $(111,411) $(89,129) $(71,303) $(57,043) $(45,634)

Profit on Sale $200,000

Taxable Income $20,000 $136,000 $243,200 $344,800 $443,504 $541,634 $641,220 $744,081 $851,880 $1,166,181

Item/Year 0 1 2 3 4 5 6 7 8 9 10

Net increase in Revenue $800,000 $880,000 $968,000 $1,064,800 $1,171,280 $1,288,408 $1,417,249 $1,558,974 $1,714,871 $1,886,358

Net decrease in revenue $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000)

Net increase in Cost $(240,000) $(272,000) $(307,200) $(345,920) $(388,512) $(435,363) $(486,900) $(543,589) $(605,948) $(674,543)

Cost of Machinery $(1,500,000)

Installation and shipping cost $(200,000)

Salvage Value $200,000

Increase in Working Capital $(50,000) $(10,000) $(10,000) $(10,000) $(10,000) $(10,000) $(10,000) $(10,000) $(10,000) $(10,000) $140,000

Tax $(6,000) $(40,800) $(72,960) $(103,440) $(133,051) $(162,490) $(192,366) $(223,224) $(255,564) $(349,854)

Cash Flows $(1,750,000) $344,000 $357,200 $377,840 $405,440 $439,717 $480,555 $527,983 $582,160 $643,359 $1,001,961

Cumulative cash flow $(1,750,000) $(1,406,000) $(1,048,800) $(670,960) $(265,520) $174,197 $654,752 $1,182,735 $1,764,895 $2,408,253 $3,410,214

Item/Year 0 1 2 3 4 5 6 7 8 9 10

Cash Flows $(1,750,000) $344,000 $357,200 $377,840 $405,440 $439,717 $480,555 $527,983 $582,160 $643,359 $1,001,961

Discounting Factor (@11.55%) 1.0000 0.8965 0.8036 0.7204 0.6458 0.5790 0.5190 0.4653 0.4171 0.3739 0.3352

Present value of Cashflows $(1,750,000) $308,382 $287,060 $272,207 $261,847 $254,581 $249,417 $245,659 $242,821 $240,562 $335,857

Cumulative cash flow $(1,750,000) $(1,441,618) $(1,154,558) $(882,351) $(620,504) $(365,923) $(116,507) $129,152 $371,973 $612,535 $948,392

NPV 948,392$

IRR 21.49%

Payback (years) 4.60

Discounted Payback (years) 6.47

Taxable Income

Cash Flows

Present value of Cashflows

CORPORATE FINANCIAL MANAGEMENT

5

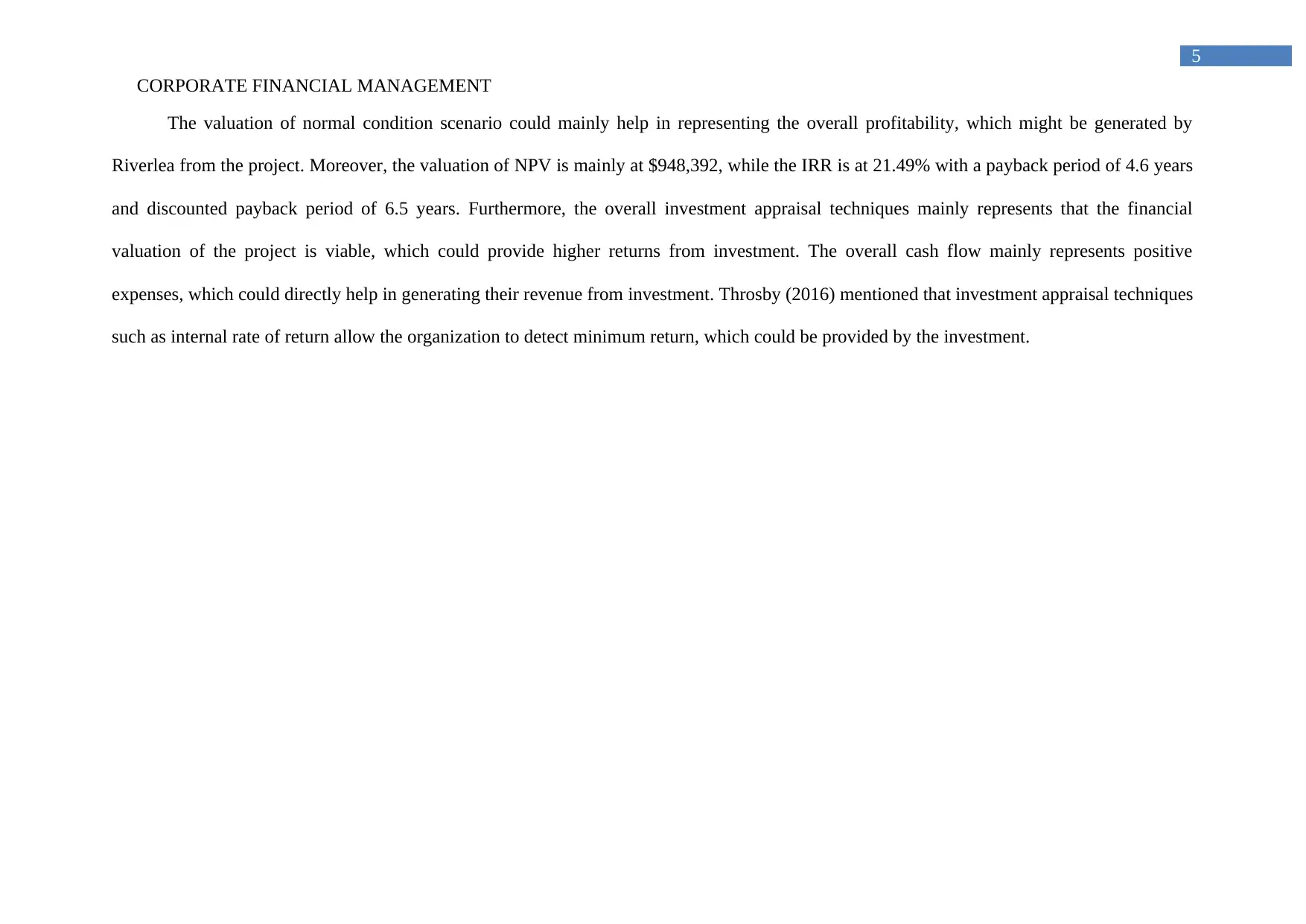

The valuation of normal condition scenario could mainly help in representing the overall profitability, which might be generated by

Riverlea from the project. Moreover, the valuation of NPV is mainly at $948,392, while the IRR is at 21.49% with a payback period of 4.6 years

and discounted payback period of 6.5 years. Furthermore, the overall investment appraisal techniques mainly represents that the financial

valuation of the project is viable, which could provide higher returns from investment. The overall cash flow mainly represents positive

expenses, which could directly help in generating their revenue from investment. Throsby (2016) mentioned that investment appraisal techniques

such as internal rate of return allow the organization to detect minimum return, which could be provided by the investment.

5

The valuation of normal condition scenario could mainly help in representing the overall profitability, which might be generated by

Riverlea from the project. Moreover, the valuation of NPV is mainly at $948,392, while the IRR is at 21.49% with a payback period of 4.6 years

and discounted payback period of 6.5 years. Furthermore, the overall investment appraisal techniques mainly represents that the financial

valuation of the project is viable, which could provide higher returns from investment. The overall cash flow mainly represents positive

expenses, which could directly help in generating their revenue from investment. Throsby (2016) mentioned that investment appraisal techniques

such as internal rate of return allow the organization to detect minimum return, which could be provided by the investment.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCIAL MANAGEMENT

6

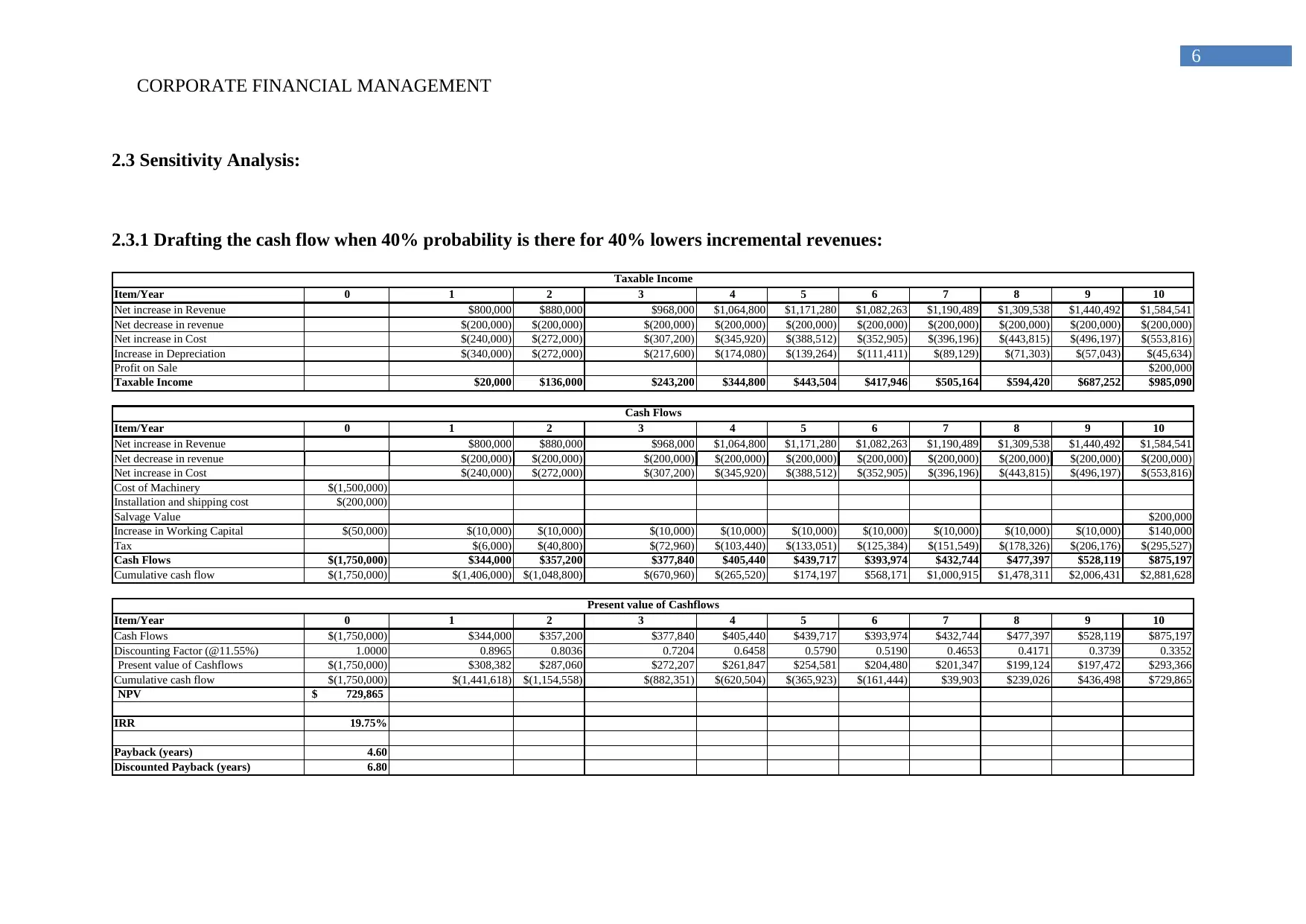

2.3 Sensitivity Analysis:

2.3.1 Drafting the cash flow when 40% probability is there for 40% lowers incremental revenues:

Item/Year 0 1 2 3 4 5 6 7 8 9 10

Net increase in Revenue $800,000 $880,000 $968,000 $1,064,800 $1,171,280 $1,082,263 $1,190,489 $1,309,538 $1,440,492 $1,584,541

Net decrease in revenue $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000)

Net increase in Cost $(240,000) $(272,000) $(307,200) $(345,920) $(388,512) $(352,905) $(396,196) $(443,815) $(496,197) $(553,816)

Increase in Depreciation $(340,000) $(272,000) $(217,600) $(174,080) $(139,264) $(111,411) $(89,129) $(71,303) $(57,043) $(45,634)

Profit on Sale $200,000

Taxable Income $20,000 $136,000 $243,200 $344,800 $443,504 $417,946 $505,164 $594,420 $687,252 $985,090

Item/Year 0 1 2 3 4 5 6 7 8 9 10

Net increase in Revenue $800,000 $880,000 $968,000 $1,064,800 $1,171,280 $1,082,263 $1,190,489 $1,309,538 $1,440,492 $1,584,541

Net decrease in revenue $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000)

Net increase in Cost $(240,000) $(272,000) $(307,200) $(345,920) $(388,512) $(352,905) $(396,196) $(443,815) $(496,197) $(553,816)

Cost of Machinery $(1,500,000)

Installation and shipping cost $(200,000)

Salvage Value $200,000

Increase in Working Capital $(50,000) $(10,000) $(10,000) $(10,000) $(10,000) $(10,000) $(10,000) $(10,000) $(10,000) $(10,000) $140,000

Tax $(6,000) $(40,800) $(72,960) $(103,440) $(133,051) $(125,384) $(151,549) $(178,326) $(206,176) $(295,527)

Cash Flows $(1,750,000) $344,000 $357,200 $377,840 $405,440 $439,717 $393,974 $432,744 $477,397 $528,119 $875,197

Cumulative cash flow $(1,750,000) $(1,406,000) $(1,048,800) $(670,960) $(265,520) $174,197 $568,171 $1,000,915 $1,478,311 $2,006,431 $2,881,628

Item/Year 0 1 2 3 4 5 6 7 8 9 10

Cash Flows $(1,750,000) $344,000 $357,200 $377,840 $405,440 $439,717 $393,974 $432,744 $477,397 $528,119 $875,197

Discounting Factor (@11.55%) 1.0000 0.8965 0.8036 0.7204 0.6458 0.5790 0.5190 0.4653 0.4171 0.3739 0.3352

Present value of Cashflows $(1,750,000) $308,382 $287,060 $272,207 $261,847 $254,581 $204,480 $201,347 $199,124 $197,472 $293,366

Cumulative cash flow $(1,750,000) $(1,441,618) $(1,154,558) $(882,351) $(620,504) $(365,923) $(161,444) $39,903 $239,026 $436,498 $729,865

NPV 729,865$

IRR 19.75%

Payback (years) 4.60

Discounted Payback (years) 6.80

Taxable Income

Cash Flows

Present value of Cashflows

6

2.3 Sensitivity Analysis:

2.3.1 Drafting the cash flow when 40% probability is there for 40% lowers incremental revenues:

Item/Year 0 1 2 3 4 5 6 7 8 9 10

Net increase in Revenue $800,000 $880,000 $968,000 $1,064,800 $1,171,280 $1,082,263 $1,190,489 $1,309,538 $1,440,492 $1,584,541

Net decrease in revenue $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000)

Net increase in Cost $(240,000) $(272,000) $(307,200) $(345,920) $(388,512) $(352,905) $(396,196) $(443,815) $(496,197) $(553,816)

Increase in Depreciation $(340,000) $(272,000) $(217,600) $(174,080) $(139,264) $(111,411) $(89,129) $(71,303) $(57,043) $(45,634)

Profit on Sale $200,000

Taxable Income $20,000 $136,000 $243,200 $344,800 $443,504 $417,946 $505,164 $594,420 $687,252 $985,090

Item/Year 0 1 2 3 4 5 6 7 8 9 10

Net increase in Revenue $800,000 $880,000 $968,000 $1,064,800 $1,171,280 $1,082,263 $1,190,489 $1,309,538 $1,440,492 $1,584,541

Net decrease in revenue $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000)

Net increase in Cost $(240,000) $(272,000) $(307,200) $(345,920) $(388,512) $(352,905) $(396,196) $(443,815) $(496,197) $(553,816)

Cost of Machinery $(1,500,000)

Installation and shipping cost $(200,000)

Salvage Value $200,000

Increase in Working Capital $(50,000) $(10,000) $(10,000) $(10,000) $(10,000) $(10,000) $(10,000) $(10,000) $(10,000) $(10,000) $140,000

Tax $(6,000) $(40,800) $(72,960) $(103,440) $(133,051) $(125,384) $(151,549) $(178,326) $(206,176) $(295,527)

Cash Flows $(1,750,000) $344,000 $357,200 $377,840 $405,440 $439,717 $393,974 $432,744 $477,397 $528,119 $875,197

Cumulative cash flow $(1,750,000) $(1,406,000) $(1,048,800) $(670,960) $(265,520) $174,197 $568,171 $1,000,915 $1,478,311 $2,006,431 $2,881,628

Item/Year 0 1 2 3 4 5 6 7 8 9 10

Cash Flows $(1,750,000) $344,000 $357,200 $377,840 $405,440 $439,717 $393,974 $432,744 $477,397 $528,119 $875,197

Discounting Factor (@11.55%) 1.0000 0.8965 0.8036 0.7204 0.6458 0.5790 0.5190 0.4653 0.4171 0.3739 0.3352

Present value of Cashflows $(1,750,000) $308,382 $287,060 $272,207 $261,847 $254,581 $204,480 $201,347 $199,124 $197,472 $293,366

Cumulative cash flow $(1,750,000) $(1,441,618) $(1,154,558) $(882,351) $(620,504) $(365,923) $(161,444) $39,903 $239,026 $436,498 $729,865

NPV 729,865$

IRR 19.75%

Payback (years) 4.60

Discounted Payback (years) 6.80

Taxable Income

Cash Flows

Present value of Cashflows

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCIAL MANAGEMENT

7

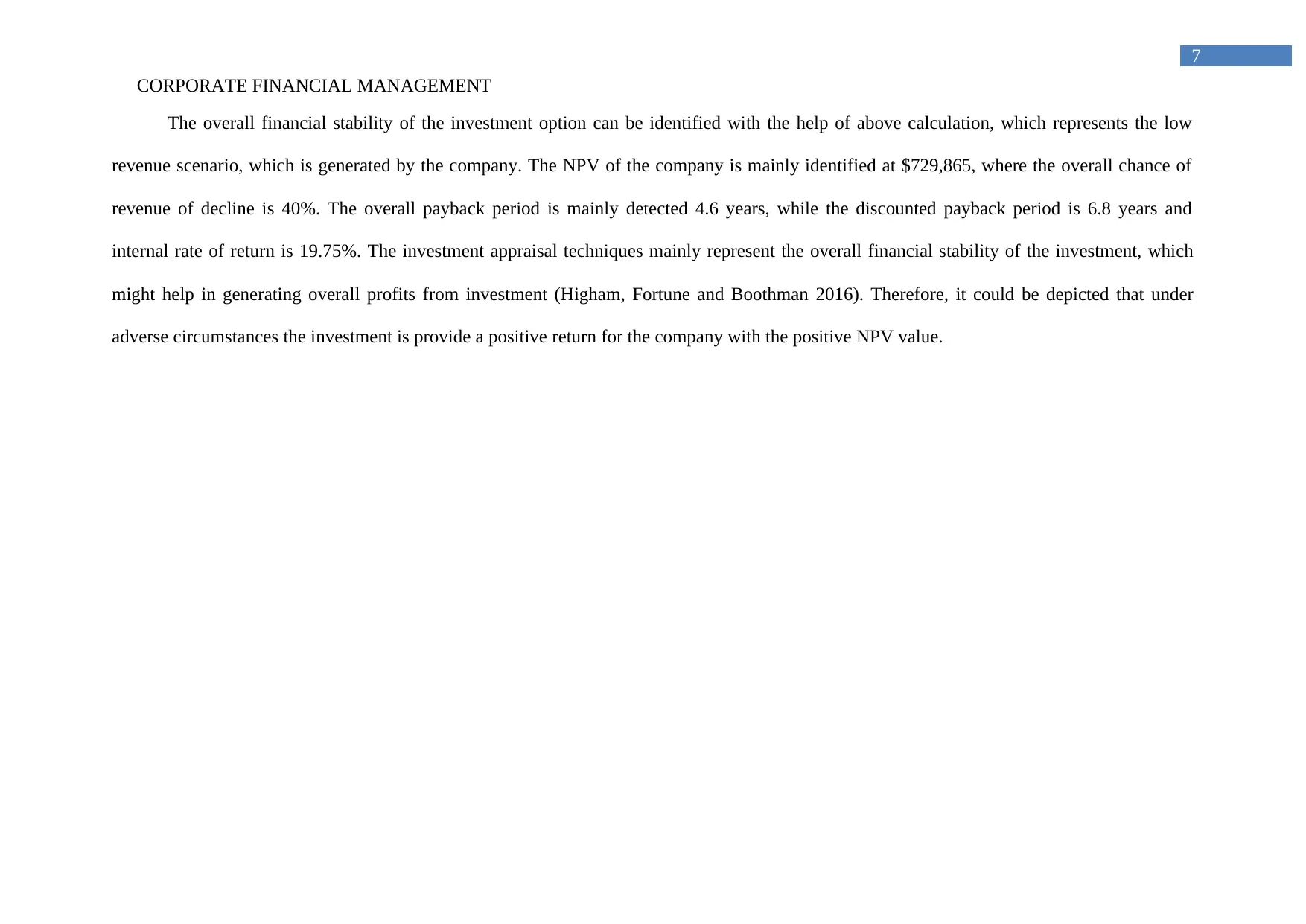

The overall financial stability of the investment option can be identified with the help of above calculation, which represents the low

revenue scenario, which is generated by the company. The NPV of the company is mainly identified at $729,865, where the overall chance of

revenue of decline is 40%. The overall payback period is mainly detected 4.6 years, while the discounted payback period is 6.8 years and

internal rate of return is 19.75%. The investment appraisal techniques mainly represent the overall financial stability of the investment, which

might help in generating overall profits from investment (Higham, Fortune and Boothman 2016). Therefore, it could be depicted that under

adverse circumstances the investment is provide a positive return for the company with the positive NPV value.

7

The overall financial stability of the investment option can be identified with the help of above calculation, which represents the low

revenue scenario, which is generated by the company. The NPV of the company is mainly identified at $729,865, where the overall chance of

revenue of decline is 40%. The overall payback period is mainly detected 4.6 years, while the discounted payback period is 6.8 years and

internal rate of return is 19.75%. The investment appraisal techniques mainly represent the overall financial stability of the investment, which

might help in generating overall profits from investment (Higham, Fortune and Boothman 2016). Therefore, it could be depicted that under

adverse circumstances the investment is provide a positive return for the company with the positive NPV value.

CORPORATE FINANCIAL MANAGEMENT

8

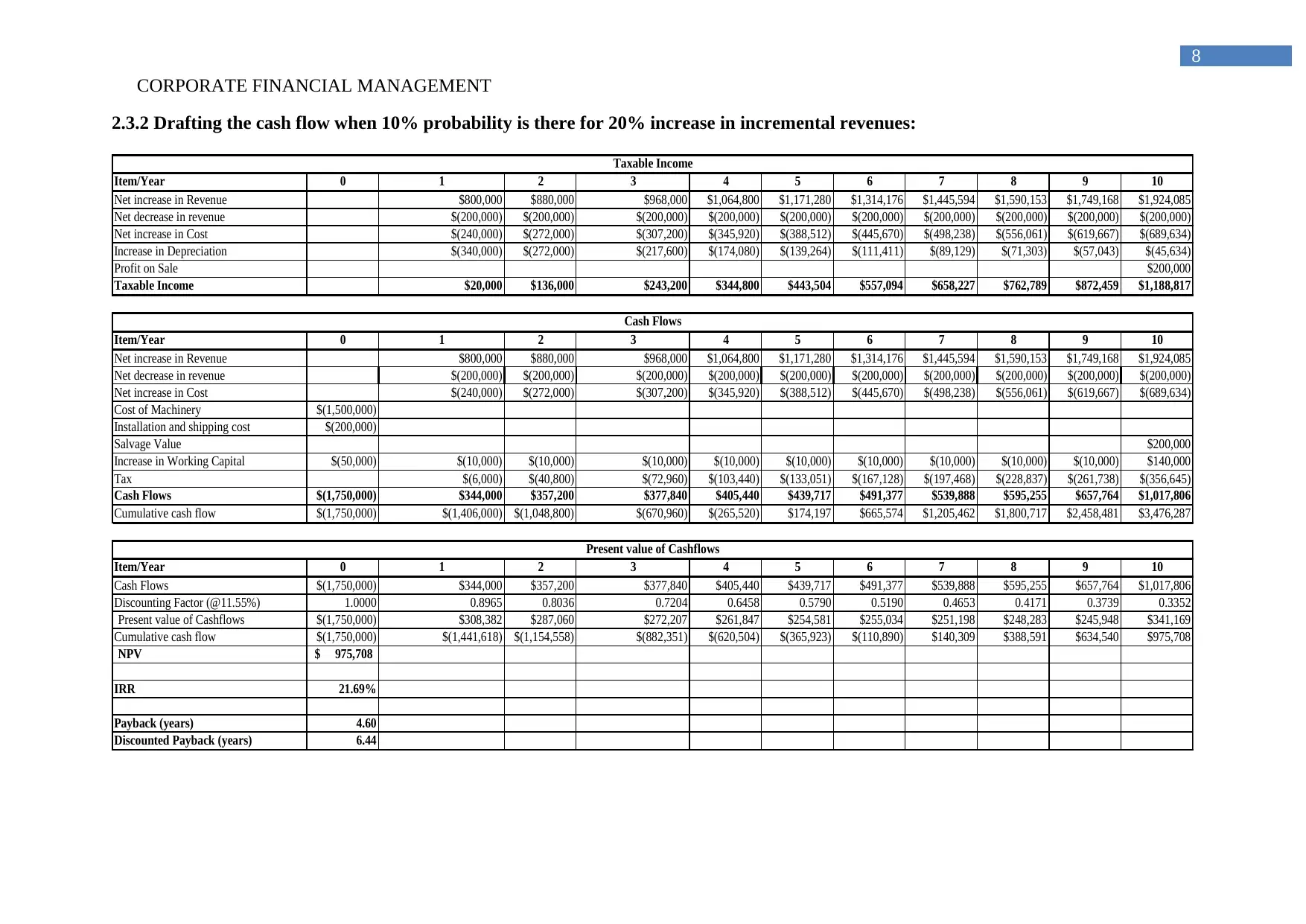

2.3.2 Drafting the cash flow when 10% probability is there for 20% increase in incremental revenues:

Item/Year 0 1 2 3 4 5 6 7 8 9 10

Net increase in Revenue $800,000 $880,000 $968,000 $1,064,800 $1,171,280 $1,314,176 $1,445,594 $1,590,153 $1,749,168 $1,924,085

Net decrease in revenue $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000)

Net increase in Cost $(240,000) $(272,000) $(307,200) $(345,920) $(388,512) $(445,670) $(498,238) $(556,061) $(619,667) $(689,634)

Increase in Depreciation $(340,000) $(272,000) $(217,600) $(174,080) $(139,264) $(111,411) $(89,129) $(71,303) $(57,043) $(45,634)

Profit on Sale $200,000

Taxable Income $20,000 $136,000 $243,200 $344,800 $443,504 $557,094 $658,227 $762,789 $872,459 $1,188,817

Item/Year 0 1 2 3 4 5 6 7 8 9 10

Net increase in Revenue $800,000 $880,000 $968,000 $1,064,800 $1,171,280 $1,314,176 $1,445,594 $1,590,153 $1,749,168 $1,924,085

Net decrease in revenue $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000)

Net increase in Cost $(240,000) $(272,000) $(307,200) $(345,920) $(388,512) $(445,670) $(498,238) $(556,061) $(619,667) $(689,634)

Cost of Machinery $(1,500,000)

Installation and shipping cost $(200,000)

Salvage Value $200,000

Increase in Working Capital $(50,000) $(10,000) $(10,000) $(10,000) $(10,000) $(10,000) $(10,000) $(10,000) $(10,000) $(10,000) $140,000

Tax $(6,000) $(40,800) $(72,960) $(103,440) $(133,051) $(167,128) $(197,468) $(228,837) $(261,738) $(356,645)

Cash Flows $(1,750,000) $344,000 $357,200 $377,840 $405,440 $439,717 $491,377 $539,888 $595,255 $657,764 $1,017,806

Cumulative cash flow $(1,750,000) $(1,406,000) $(1,048,800) $(670,960) $(265,520) $174,197 $665,574 $1,205,462 $1,800,717 $2,458,481 $3,476,287

Item/Year 0 1 2 3 4 5 6 7 8 9 10

Cash Flows $(1,750,000) $344,000 $357,200 $377,840 $405,440 $439,717 $491,377 $539,888 $595,255 $657,764 $1,017,806

Discounting Factor (@11.55%) 1.0000 0.8965 0.8036 0.7204 0.6458 0.5790 0.5190 0.4653 0.4171 0.3739 0.3352

Present value of Cashflows $(1,750,000) $308,382 $287,060 $272,207 $261,847 $254,581 $255,034 $251,198 $248,283 $245,948 $341,169

Cumulative cash flow $(1,750,000) $(1,441,618) $(1,154,558) $(882,351) $(620,504) $(365,923) $(110,890) $140,309 $388,591 $634,540 $975,708

NPV 975,708$

IRR 21.69%

Payback (years) 4.60

Discounted Payback (years) 6.44

Taxable Income

Cash Flows

Present value of Cashflows

8

2.3.2 Drafting the cash flow when 10% probability is there for 20% increase in incremental revenues:

Item/Year 0 1 2 3 4 5 6 7 8 9 10

Net increase in Revenue $800,000 $880,000 $968,000 $1,064,800 $1,171,280 $1,314,176 $1,445,594 $1,590,153 $1,749,168 $1,924,085

Net decrease in revenue $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000)

Net increase in Cost $(240,000) $(272,000) $(307,200) $(345,920) $(388,512) $(445,670) $(498,238) $(556,061) $(619,667) $(689,634)

Increase in Depreciation $(340,000) $(272,000) $(217,600) $(174,080) $(139,264) $(111,411) $(89,129) $(71,303) $(57,043) $(45,634)

Profit on Sale $200,000

Taxable Income $20,000 $136,000 $243,200 $344,800 $443,504 $557,094 $658,227 $762,789 $872,459 $1,188,817

Item/Year 0 1 2 3 4 5 6 7 8 9 10

Net increase in Revenue $800,000 $880,000 $968,000 $1,064,800 $1,171,280 $1,314,176 $1,445,594 $1,590,153 $1,749,168 $1,924,085

Net decrease in revenue $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000) $(200,000)

Net increase in Cost $(240,000) $(272,000) $(307,200) $(345,920) $(388,512) $(445,670) $(498,238) $(556,061) $(619,667) $(689,634)

Cost of Machinery $(1,500,000)

Installation and shipping cost $(200,000)

Salvage Value $200,000

Increase in Working Capital $(50,000) $(10,000) $(10,000) $(10,000) $(10,000) $(10,000) $(10,000) $(10,000) $(10,000) $(10,000) $140,000

Tax $(6,000) $(40,800) $(72,960) $(103,440) $(133,051) $(167,128) $(197,468) $(228,837) $(261,738) $(356,645)

Cash Flows $(1,750,000) $344,000 $357,200 $377,840 $405,440 $439,717 $491,377 $539,888 $595,255 $657,764 $1,017,806

Cumulative cash flow $(1,750,000) $(1,406,000) $(1,048,800) $(670,960) $(265,520) $174,197 $665,574 $1,205,462 $1,800,717 $2,458,481 $3,476,287

Item/Year 0 1 2 3 4 5 6 7 8 9 10

Cash Flows $(1,750,000) $344,000 $357,200 $377,840 $405,440 $439,717 $491,377 $539,888 $595,255 $657,764 $1,017,806

Discounting Factor (@11.55%) 1.0000 0.8965 0.8036 0.7204 0.6458 0.5790 0.5190 0.4653 0.4171 0.3739 0.3352

Present value of Cashflows $(1,750,000) $308,382 $287,060 $272,207 $261,847 $254,581 $255,034 $251,198 $248,283 $245,948 $341,169

Cumulative cash flow $(1,750,000) $(1,441,618) $(1,154,558) $(882,351) $(620,504) $(365,923) $(110,890) $140,309 $388,591 $634,540 $975,708

NPV 975,708$

IRR 21.69%

Payback (years) 4.60

Discounted Payback (years) 6.44

Taxable Income

Cash Flows

Present value of Cashflows

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCIAL MANAGEMENT

9

The overall above figure mainly represent the calculation of the investment scope provided to Riverlea under positive circumstances.

This situation mainly indicates that there is a 10% probability that the overall revenue of the company will rise by 20%. Therefore, the situation

mainly represents that investment appraisal techniques such as NPV, IRR, payback period and discounted payback period could be used in

evaluating the overall viability of the project (Bai, Dhavale and Sarkis 2016). The positive sensation mainly indicates that NPV is $975,708, IRR

is 21.69%, payback period is 4.6 years, and discounted payback is 6.4 years. The overall valuation of the investment appraisal techniques mainly

use in generating higher revenue from investment.

9

The overall above figure mainly represent the calculation of the investment scope provided to Riverlea under positive circumstances.

This situation mainly indicates that there is a 10% probability that the overall revenue of the company will rise by 20%. Therefore, the situation

mainly represents that investment appraisal techniques such as NPV, IRR, payback period and discounted payback period could be used in

evaluating the overall viability of the project (Bai, Dhavale and Sarkis 2016). The positive sensation mainly indicates that NPV is $975,708, IRR

is 21.69%, payback period is 4.6 years, and discounted payback is 6.4 years. The overall valuation of the investment appraisal techniques mainly

use in generating higher revenue from investment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCIAL MANAGEMENT

10

3. Concussion and Recommendations:

From the overall evaluation of the investment opportunity, which is presented to

Riverlea is a viable approach. In addition, the overall investment analysis is mainly

conducted on different scenarios, where the range of income that could be presented from

investment is depicted. The investment appraisal techniques mainly represent the overall

financial stability of the new project, which could increase firm value in future. Therefore, it

is advisable to Riverlea to commence with the production of confectionaries in their

production function.

Part 2:

1. Introduction:

The relevant evaluation is mainly conducted on the share price movement of Riverlea

after the announcement of extra income that will be generated in near future. In addition, the

overall valuation could mainly indicate overall impact of the announcement, which is

conducted on the share price of the company. Relevant calculation is mainly conducted to

detect the probability of the share price value after the announcement.

10

3. Concussion and Recommendations:

From the overall evaluation of the investment opportunity, which is presented to

Riverlea is a viable approach. In addition, the overall investment analysis is mainly

conducted on different scenarios, where the range of income that could be presented from

investment is depicted. The investment appraisal techniques mainly represent the overall

financial stability of the new project, which could increase firm value in future. Therefore, it

is advisable to Riverlea to commence with the production of confectionaries in their

production function.

Part 2:

1. Introduction:

The relevant evaluation is mainly conducted on the share price movement of Riverlea

after the announcement of extra income that will be generated in near future. In addition, the

overall valuation could mainly indicate overall impact of the announcement, which is

conducted on the share price of the company. Relevant calculation is mainly conducted to

detect the probability of the share price value after the announcement.

CORPORATE FINANCIAL MANAGEMENT

11

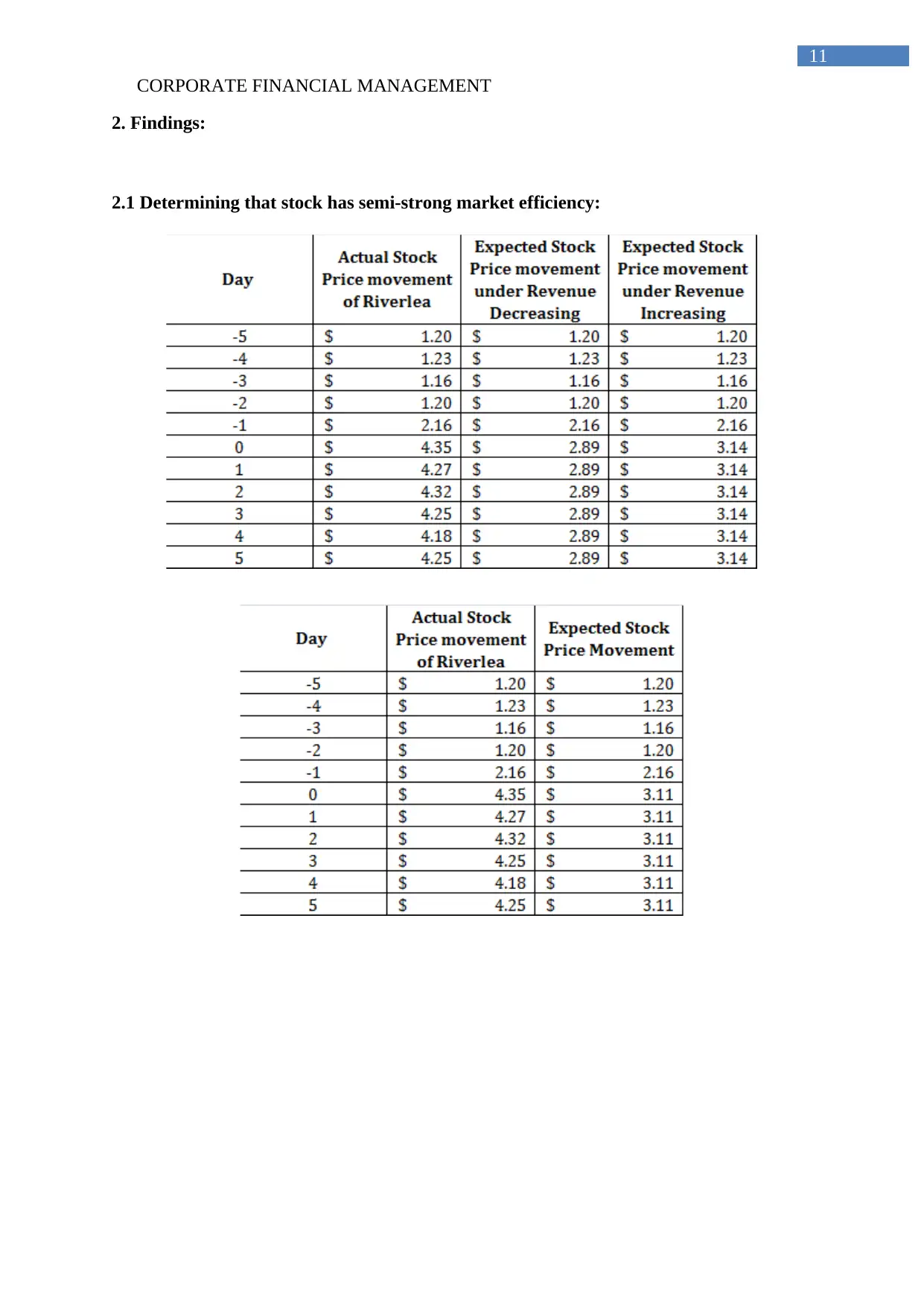

2. Findings:

2.1 Determining that stock has semi-strong market efficiency:

11

2. Findings:

2.1 Determining that stock has semi-strong market efficiency:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.