Corporate Finance Assignment: Calculations, Analysis, and Answers

VerifiedAdded on 2022/09/15

|9

|1400

|22

Homework Assignment

AI Summary

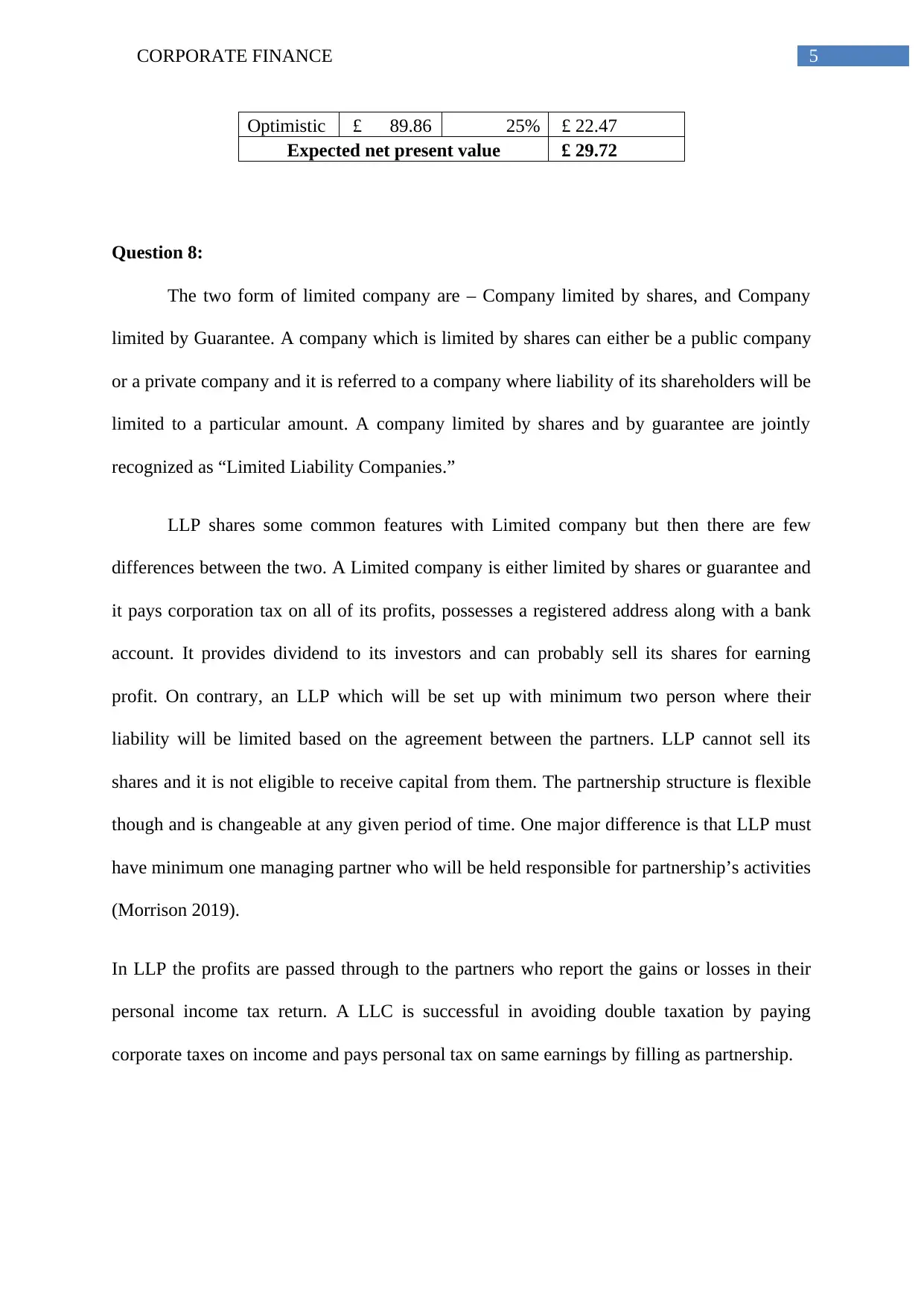

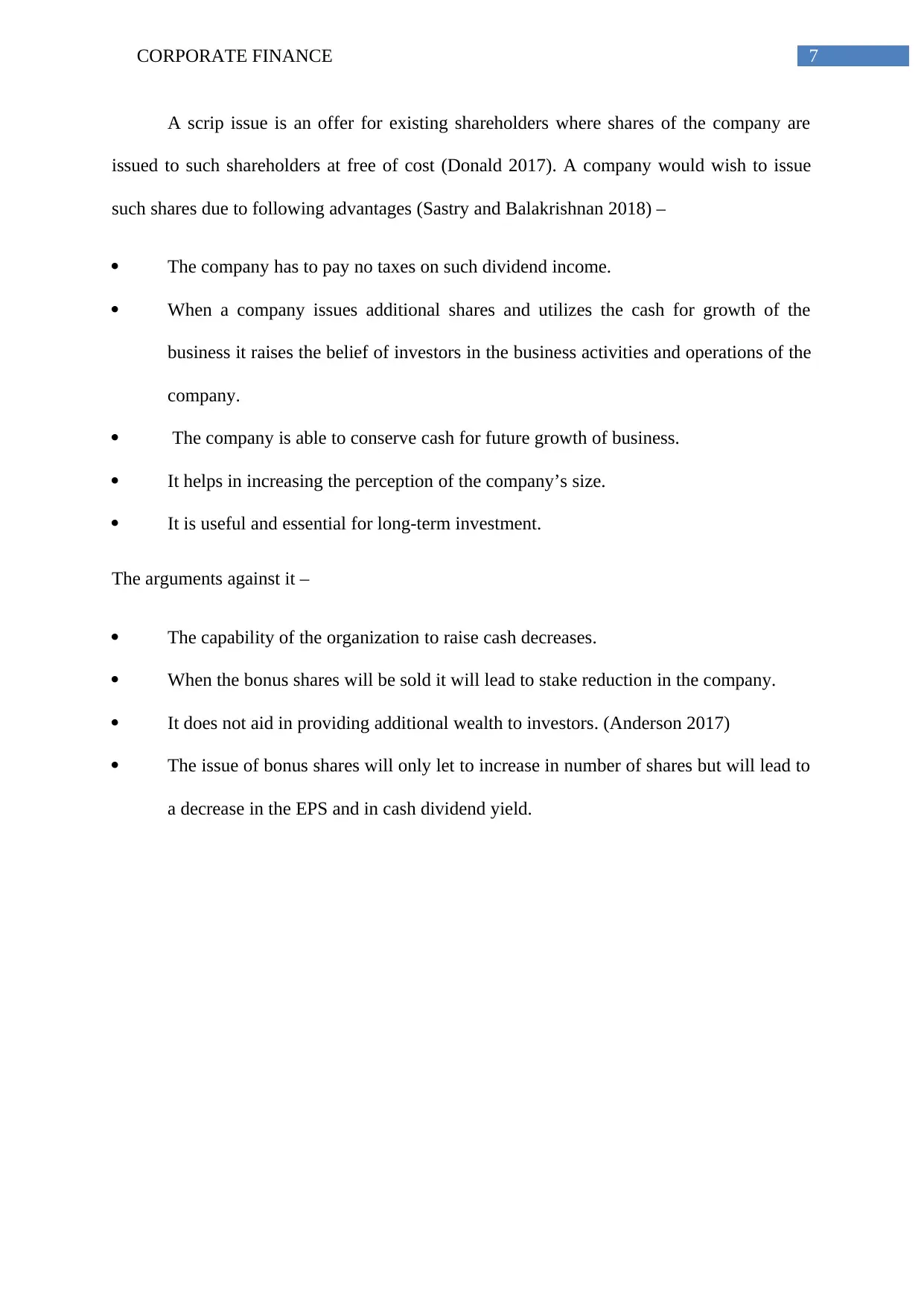

This document presents a comprehensive solution to a corporate finance assignment, addressing key concepts and calculations. The assignment covers a range of topics, including dividend yield, cost of goods sold, geared and ungeared beta, Weighted Average Cost of Capital (WACC) calculation, capital structure decisions, share price analysis, sensitivity analysis, and the differences between limited companies and LLPs. The solution provides detailed workings for each question, including calculations for dividend yield, cost of equity, market capitalization, and the impact of a scrip issue. Furthermore, the assignment delves into the advantages and disadvantages of scrip issues, along with balance sheet adjustments. The document also explores sensitivity analysis to assess the impact of different scenarios on Net Present Value (NPV), and provides a detailed analysis of various financial concepts, making it a valuable resource for students studying corporate finance.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.