Corporate Finance Report: Capital Structure Impact on WACC at Dynamic

VerifiedAdded on 2023/06/03

|22

|5317

|418

Report

AI Summary

This corporate finance report critically examines a company's capital structure and weighted average cost of capital (WACC) under various scenarios, including changes in debt levels and the introduction of a tax rate. It begins by calculating the market debt-to-equity ratio, cost of levered equity, and current WACC in a perfect market, demonstrating that capital structure is irrelevant in such conditions. The report then analyzes the impact of issuing stock to repurchase debt and introduces a tax rate of 40% along with additional debt issuance to repurchase stock, revealing how these factors influence the WACC in an imperfect market. Furthermore, the report includes an analysis of initial investment outlay, terminal cash flow, and the treatment of working capital for a project, along with a discussion on the evaluation of corporate lifecycle and benefits of different types of financing. Desklib offers this document along with many others to aid students in their studies.

CORPORATE

FINANCE

FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction...........................................................................................................................................3

QUESTION 1........................................................................................................................................4

PART 1..............................................................................................................................................5

a) MARKET DEBT TO EQUITY RATIO................................................................................5

b) Cost of levered equity based on market debt to equity ratio..................................................6

c) Current weighted average cost of capital...............................................................................7

d) When the company issues $ 1 billion in stock to repurchase debt..........................................7

PART 2..............................................................................................................................................9

IMPLICATION OF INTRODUCING TAX RATE OF 40 % AND DEBT ISSUANCE OF $ 5

BILLION TO REPURCHASE STOCK........................................................................................9

QUESTION 2......................................................................................................................................11

a) INITIAL INVESTMENT OUTLAY.......................................................................................12

b) TERMINAL CASH FLOW IN YEAR 6.................................................................................12

c) TREATMENT OF WORKING CAPITAL.............................................................................13

d) IF THE PROJECT’S RATE OF RETURN IS 14% SHOULD THE EQUIPMENT BE

PURCHASED?................................................................................................................................14

e) HOW TO USE DEBT FINANCING TO INCREASE NET PRESENT VALUE....................15

QUESTION 3......................................................................................................................................15

QUESTION 4......................................................................................................................................16

EVALUATION OF CORPORATE LIFECYCLE...........................................................................16

TYPES OF BUSINESS FINANCES...............................................................................................17

BENEFIT OF DIFFERENT TYPES OF FINANCING...................................................................18

Conclusion...........................................................................................................................................18

REFERENCES....................................................................................................................................19

Introduction...........................................................................................................................................3

QUESTION 1........................................................................................................................................4

PART 1..............................................................................................................................................5

a) MARKET DEBT TO EQUITY RATIO................................................................................5

b) Cost of levered equity based on market debt to equity ratio..................................................6

c) Current weighted average cost of capital...............................................................................7

d) When the company issues $ 1 billion in stock to repurchase debt..........................................7

PART 2..............................................................................................................................................9

IMPLICATION OF INTRODUCING TAX RATE OF 40 % AND DEBT ISSUANCE OF $ 5

BILLION TO REPURCHASE STOCK........................................................................................9

QUESTION 2......................................................................................................................................11

a) INITIAL INVESTMENT OUTLAY.......................................................................................12

b) TERMINAL CASH FLOW IN YEAR 6.................................................................................12

c) TREATMENT OF WORKING CAPITAL.............................................................................13

d) IF THE PROJECT’S RATE OF RETURN IS 14% SHOULD THE EQUIPMENT BE

PURCHASED?................................................................................................................................14

e) HOW TO USE DEBT FINANCING TO INCREASE NET PRESENT VALUE....................15

QUESTION 3......................................................................................................................................15

QUESTION 4......................................................................................................................................16

EVALUATION OF CORPORATE LIFECYCLE...........................................................................16

TYPES OF BUSINESS FINANCES...............................................................................................17

BENEFIT OF DIFFERENT TYPES OF FINANCING...................................................................18

Conclusion...........................................................................................................................................18

REFERENCES....................................................................................................................................19

Introduction

The financial leverage and cost of capital are the two important aspects for the

effective business functioning. It is required to set up strong harmonization between both if

company wants to sustain its business in long run. This report has reflected that key

understanding on the optimum capital structure based on the cost of capital and financial

leverage of company. Financial leverage shows the business sustainability risk of company if

it fails to have enough earnings before interest and tax and its interest coverage out of the

available earning. This report has reflected the cost of levered equity, debt funding, capital

structure and use of the capital budgeting tools to determine the terminal values, initial

investment and cash flow for the accepted business projects.

The financial leverage and cost of capital are the two important aspects for the

effective business functioning. It is required to set up strong harmonization between both if

company wants to sustain its business in long run. This report has reflected that key

understanding on the optimum capital structure based on the cost of capital and financial

leverage of company. Financial leverage shows the business sustainability risk of company if

it fails to have enough earnings before interest and tax and its interest coverage out of the

available earning. This report has reflected the cost of levered equity, debt funding, capital

structure and use of the capital budgeting tools to determine the terminal values, initial

investment and cash flow for the accepted business projects.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION 1

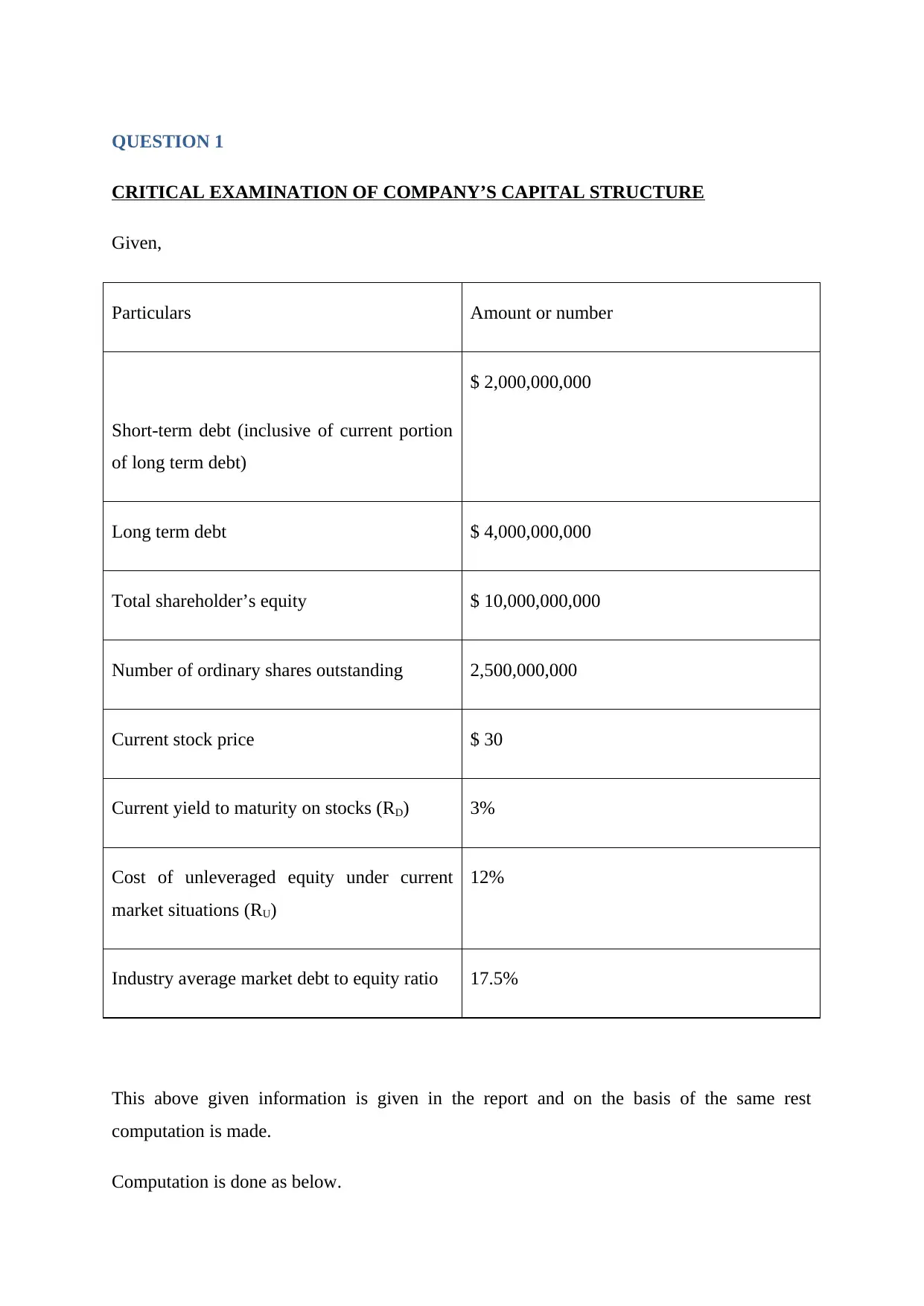

CRITICAL EXAMINATION OF COMPANY’S CAPITAL STRUCTURE

Given,

Particulars Amount or number

Short-term debt (inclusive of current portion

of long term debt)

$ 2,000,000,000

Long term debt $ 4,000,000,000

Total shareholder’s equity $ 10,000,000,000

Number of ordinary shares outstanding 2,500,000,000

Current stock price $ 30

Current yield to maturity on stocks (RD) 3%

Cost of unleveraged equity under current

market situations (RU)

12%

Industry average market debt to equity ratio 17.5%

This above given information is given in the report and on the basis of the same rest

computation is made.

Computation is done as below.

CRITICAL EXAMINATION OF COMPANY’S CAPITAL STRUCTURE

Given,

Particulars Amount or number

Short-term debt (inclusive of current portion

of long term debt)

$ 2,000,000,000

Long term debt $ 4,000,000,000

Total shareholder’s equity $ 10,000,000,000

Number of ordinary shares outstanding 2,500,000,000

Current stock price $ 30

Current yield to maturity on stocks (RD) 3%

Cost of unleveraged equity under current

market situations (RU)

12%

Industry average market debt to equity ratio 17.5%

This above given information is given in the report and on the basis of the same rest

computation is made.

Computation is done as below.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Particulars Amount

Market value of equity (E) (2,500,000,000 x 30)

= $ 75,000,000,000

Total liabilities (D) 2,000,000,000 + 4,000,000,000

= $ 6,000,000,000

PART 1

All the discussions made in this part are regarding the perfect market. The perfect

markets are those in which there are no tax rates, or any transactions costs. The value of the

firm in this kind of market is not affected anyhow by the capital structure. The calculation of

the market value is just equivalent to the cash flows that the company has generated. The has

also been argued by the Franco Modigliani and Merton Miller while stating the fact that with

the perfect capital market where there is no effect of taxes, bankruptcy costs, agency costs,

and asymmetric information, and other external factors then the value of a firm is unaffected

by how that firm is financed and what capital structure it has been maintaining. Therefore,

low and high financial leverage and use of tax deductible expenses will have no role to play

while determining the capital structure.

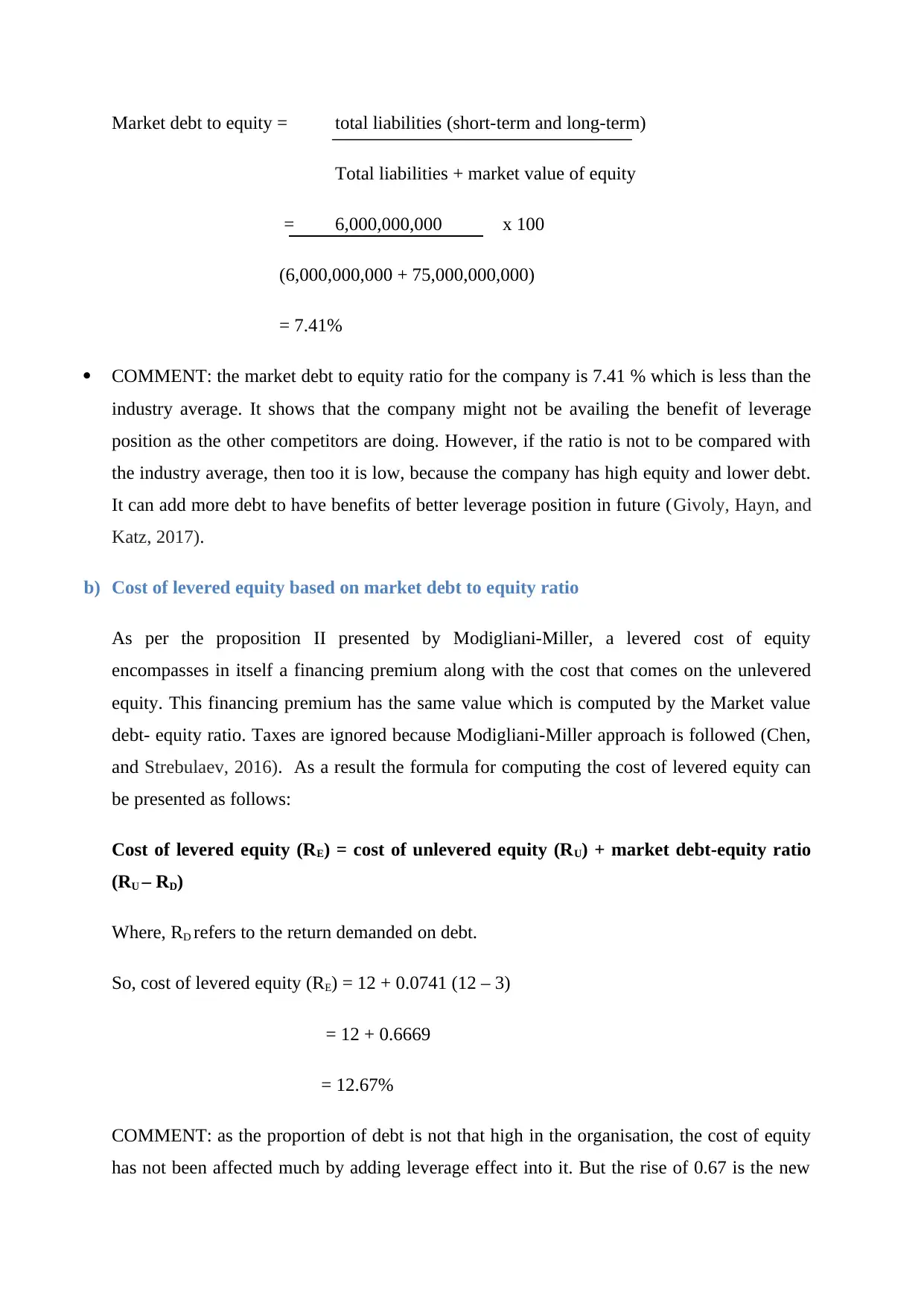

a) MARKET DEBT TO EQUITY RATIO

Market debt to equity ratio shows the ratio of the debt that the company has in comparison to

the current value that the entity has in the market. As the current market value of the

company is used, this ratio helps in providing a better measure for analysing the solvency

position of the organisation (Lewis, and Tan, 2016). The formula used for calculating the

market debt to equity ratio is stated as follows:

Market value of equity (E) (2,500,000,000 x 30)

= $ 75,000,000,000

Total liabilities (D) 2,000,000,000 + 4,000,000,000

= $ 6,000,000,000

PART 1

All the discussions made in this part are regarding the perfect market. The perfect

markets are those in which there are no tax rates, or any transactions costs. The value of the

firm in this kind of market is not affected anyhow by the capital structure. The calculation of

the market value is just equivalent to the cash flows that the company has generated. The has

also been argued by the Franco Modigliani and Merton Miller while stating the fact that with

the perfect capital market where there is no effect of taxes, bankruptcy costs, agency costs,

and asymmetric information, and other external factors then the value of a firm is unaffected

by how that firm is financed and what capital structure it has been maintaining. Therefore,

low and high financial leverage and use of tax deductible expenses will have no role to play

while determining the capital structure.

a) MARKET DEBT TO EQUITY RATIO

Market debt to equity ratio shows the ratio of the debt that the company has in comparison to

the current value that the entity has in the market. As the current market value of the

company is used, this ratio helps in providing a better measure for analysing the solvency

position of the organisation (Lewis, and Tan, 2016). The formula used for calculating the

market debt to equity ratio is stated as follows:

Market debt to equity = total liabilities (short-term and long-term)

Total liabilities + market value of equity

= 6,000,000,000 x 100

(6,000,000,000 + 75,000,000,000)

= 7.41%

COMMENT: the market debt to equity ratio for the company is 7.41 % which is less than the

industry average. It shows that the company might not be availing the benefit of leverage

position as the other competitors are doing. However, if the ratio is not to be compared with

the industry average, then too it is low, because the company has high equity and lower debt.

It can add more debt to have benefits of better leverage position in future (Givoly, Hayn, and

Katz, 2017).

b) Cost of levered equity based on market debt to equity ratio

As per the proposition II presented by Modigliani-Miller, a levered cost of equity

encompasses in itself a financing premium along with the cost that comes on the unlevered

equity. This financing premium has the same value which is computed by the Market value

debt- equity ratio. Taxes are ignored because Modigliani-Miller approach is followed (Chen,

and Strebulaev, 2016). As a result the formula for computing the cost of levered equity can

be presented as follows:

Cost of levered equity (RE) = cost of unlevered equity (RU) + market debt-equity ratio

(RU – RD)

Where, RD refers to the return demanded on debt.

So, cost of levered equity (RE) = 12 + 0.0741 (12 – 3)

= 12 + 0.6669

= 12.67%

COMMENT: as the proportion of debt is not that high in the organisation, the cost of equity

has not been affected much by adding leverage effect into it. But the rise of 0.67 is the new

Total liabilities + market value of equity

= 6,000,000,000 x 100

(6,000,000,000 + 75,000,000,000)

= 7.41%

COMMENT: the market debt to equity ratio for the company is 7.41 % which is less than the

industry average. It shows that the company might not be availing the benefit of leverage

position as the other competitors are doing. However, if the ratio is not to be compared with

the industry average, then too it is low, because the company has high equity and lower debt.

It can add more debt to have benefits of better leverage position in future (Givoly, Hayn, and

Katz, 2017).

b) Cost of levered equity based on market debt to equity ratio

As per the proposition II presented by Modigliani-Miller, a levered cost of equity

encompasses in itself a financing premium along with the cost that comes on the unlevered

equity. This financing premium has the same value which is computed by the Market value

debt- equity ratio. Taxes are ignored because Modigliani-Miller approach is followed (Chen,

and Strebulaev, 2016). As a result the formula for computing the cost of levered equity can

be presented as follows:

Cost of levered equity (RE) = cost of unlevered equity (RU) + market debt-equity ratio

(RU – RD)

Where, RD refers to the return demanded on debt.

So, cost of levered equity (RE) = 12 + 0.0741 (12 – 3)

= 12 + 0.6669

= 12.67%

COMMENT: as the proportion of debt is not that high in the organisation, the cost of equity

has not been affected much by adding leverage effect into it. But the rise of 0.67 is the new

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

demand which the shareholders are expecting for their investments and returns on the same

gets riskier after debt are introduced in the company. Even though the equity returns are

increased after debts are introduced, still more risk comes uninvited (Boyer, Lim, and Lyons,

2017).

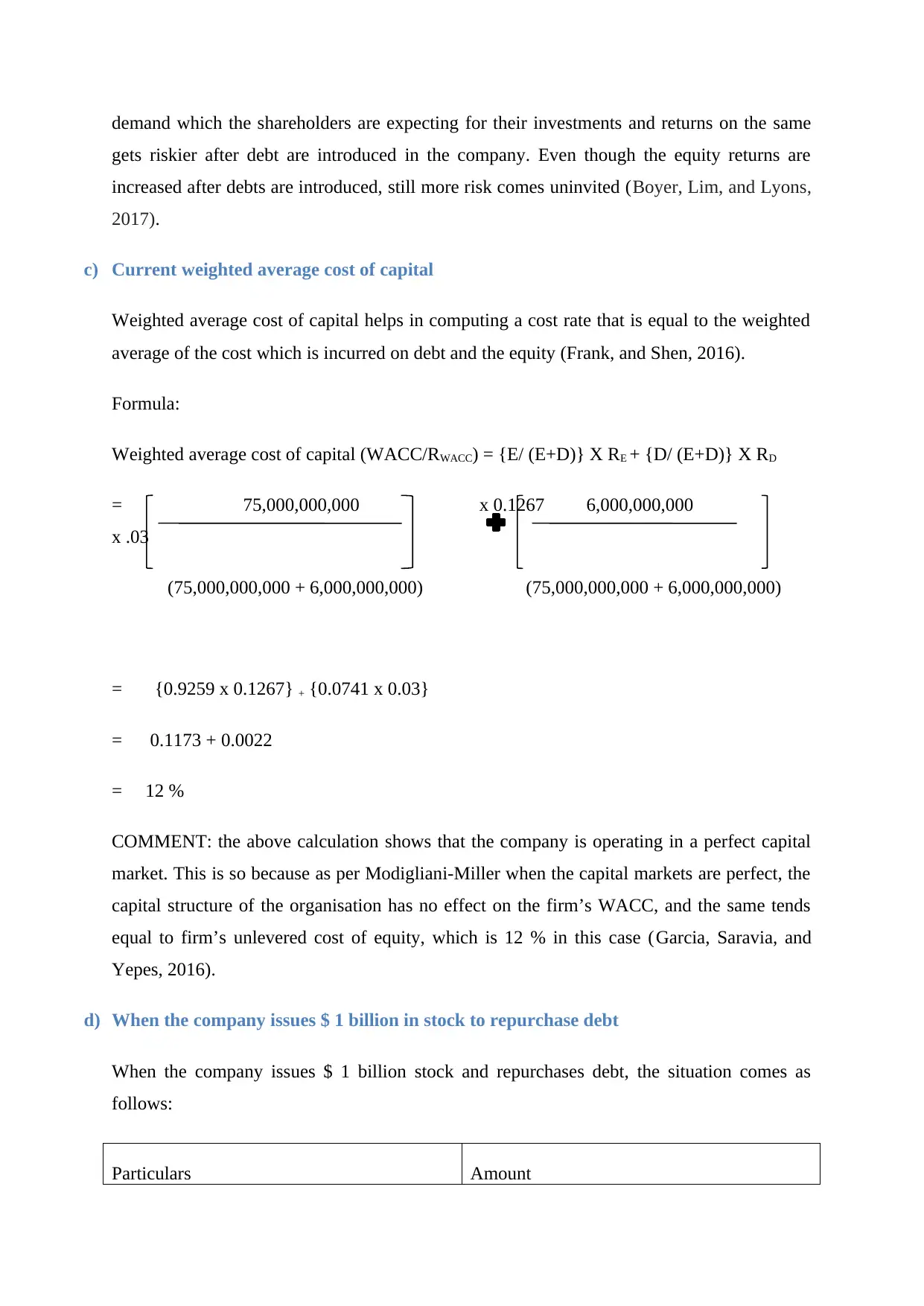

c) Current weighted average cost of capital

Weighted average cost of capital helps in computing a cost rate that is equal to the weighted

average of the cost which is incurred on debt and the equity (Frank, and Shen, 2016).

Formula:

Weighted average cost of capital (WACC/RWACC) = {E/ (E+D)} X RE + {D/ (E+D)} X RD

= 75,000,000,000 x 0.1267 6,000,000,000

x .03

(75,000,000,000 + 6,000,000,000) (75,000,000,000 + 6,000,000,000)

= {0.9259 x 0.1267} + {0.0741 x 0.03}

= 0.1173 + 0.0022

= 12 %

COMMENT: the above calculation shows that the company is operating in a perfect capital

market. This is so because as per Modigliani-Miller when the capital markets are perfect, the

capital structure of the organisation has no effect on the firm’s WACC, and the same tends

equal to firm’s unlevered cost of equity, which is 12 % in this case (Garcia, Saravia, and

Yepes, 2016).

d) When the company issues $ 1 billion in stock to repurchase debt

When the company issues $ 1 billion stock and repurchases debt, the situation comes as

follows:

Particulars Amount

gets riskier after debt are introduced in the company. Even though the equity returns are

increased after debts are introduced, still more risk comes uninvited (Boyer, Lim, and Lyons,

2017).

c) Current weighted average cost of capital

Weighted average cost of capital helps in computing a cost rate that is equal to the weighted

average of the cost which is incurred on debt and the equity (Frank, and Shen, 2016).

Formula:

Weighted average cost of capital (WACC/RWACC) = {E/ (E+D)} X RE + {D/ (E+D)} X RD

= 75,000,000,000 x 0.1267 6,000,000,000

x .03

(75,000,000,000 + 6,000,000,000) (75,000,000,000 + 6,000,000,000)

= {0.9259 x 0.1267} + {0.0741 x 0.03}

= 0.1173 + 0.0022

= 12 %

COMMENT: the above calculation shows that the company is operating in a perfect capital

market. This is so because as per Modigliani-Miller when the capital markets are perfect, the

capital structure of the organisation has no effect on the firm’s WACC, and the same tends

equal to firm’s unlevered cost of equity, which is 12 % in this case (Garcia, Saravia, and

Yepes, 2016).

d) When the company issues $ 1 billion in stock to repurchase debt

When the company issues $ 1 billion stock and repurchases debt, the situation comes as

follows:

Particulars Amount

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Market value of equity (E) (2,500,000,000 x 30) + 1,000,000,000

= $ 76,000,000,000

Total liabilities (D) 2,000,000,000 + 4,000,000,000 –

1,000,000,000

= $ 5,000,000,000

COST OF LEVERED EQUITY BASED ON MARKET DEBT TO EQUITY RATIO

For this market debt to equity is to be recalculated. It can be done as follows:

Market debt to equity = 5,000,000,000

(5,000,000,000 + 76,000,000,000)

= 6.17 %

COMMENT: the debt in comparison to equity has further reduced.

COST OF LEVERED EQUITY BASED ON MARKET DEBT TO EQUITY RATIO

The cost of levered equity comes to (new RE) = 12 + 0.0617 (12 – 3)

= 12.43%

COMMENT: the lessening of debt in the capital structure do not does away with the risks.

Risks are present till the date debts are there and hence results in increasing the return

demanded by the shareholders.

WEIGHTED AVERAGE COST OF CAPITAL

The weighted average cost of capital is computed as follows:

New WACC (new RWACC)

= 76,000,000,000 x 0.1243 5,000,000,000

x .03

(76,000,000,000 + 5,000,000,000) (76,000,000,000 + 5,000,000,000)

= 12 %

= $ 76,000,000,000

Total liabilities (D) 2,000,000,000 + 4,000,000,000 –

1,000,000,000

= $ 5,000,000,000

COST OF LEVERED EQUITY BASED ON MARKET DEBT TO EQUITY RATIO

For this market debt to equity is to be recalculated. It can be done as follows:

Market debt to equity = 5,000,000,000

(5,000,000,000 + 76,000,000,000)

= 6.17 %

COMMENT: the debt in comparison to equity has further reduced.

COST OF LEVERED EQUITY BASED ON MARKET DEBT TO EQUITY RATIO

The cost of levered equity comes to (new RE) = 12 + 0.0617 (12 – 3)

= 12.43%

COMMENT: the lessening of debt in the capital structure do not does away with the risks.

Risks are present till the date debts are there and hence results in increasing the return

demanded by the shareholders.

WEIGHTED AVERAGE COST OF CAPITAL

The weighted average cost of capital is computed as follows:

New WACC (new RWACC)

= 76,000,000,000 x 0.1243 5,000,000,000

x .03

(76,000,000,000 + 5,000,000,000) (76,000,000,000 + 5,000,000,000)

= 12 %

COMMENT: hence, there is no impact of change in the capital structure on the weighted

average cost of capital of the organisation. It is still 12%. The reason is same. The perfect

capita markets are not affected by any change that happens in the capital structure of the

organisation. The weighted average cost of capital always comes equal to the unlevered cost

of equity (Arrow, 2017).

PART 2

IMPLICATION OF INTRODUCING TAX RATE OF 40 % AND DEBT ISSUANCE

OF $ 5 BILLION TO REPURCHASE STOCK

When the company raises $ 5 billion debt and repurchases stock, the situation comes as

follows:

Particulars Amount

Market value of equity (E) (2,500,000,000 x 30) - 5,000,000,000

= $ 70,000,000,000

Total liabilities (D) 2,000,000,000 + 4,000,000,000 +

5,000,000,000

= $ 11,000,000,000

a) MARKET DEBT TO EQUITY RATIO

Applying the formula used above, the market debt to equity ratio comes down to be:

Market debt to equity = 11,000,000,000

(70,000,000,000 + 11,000,000,000)

= 13.58 %

COMMENT: the market debt to equity has improved after the company has raised a further

debt of $ 5,000,000,000. The capital structure value remains the same, only the components

have changed.

average cost of capital of the organisation. It is still 12%. The reason is same. The perfect

capita markets are not affected by any change that happens in the capital structure of the

organisation. The weighted average cost of capital always comes equal to the unlevered cost

of equity (Arrow, 2017).

PART 2

IMPLICATION OF INTRODUCING TAX RATE OF 40 % AND DEBT ISSUANCE

OF $ 5 BILLION TO REPURCHASE STOCK

When the company raises $ 5 billion debt and repurchases stock, the situation comes as

follows:

Particulars Amount

Market value of equity (E) (2,500,000,000 x 30) - 5,000,000,000

= $ 70,000,000,000

Total liabilities (D) 2,000,000,000 + 4,000,000,000 +

5,000,000,000

= $ 11,000,000,000

a) MARKET DEBT TO EQUITY RATIO

Applying the formula used above, the market debt to equity ratio comes down to be:

Market debt to equity = 11,000,000,000

(70,000,000,000 + 11,000,000,000)

= 13.58 %

COMMENT: the market debt to equity has improved after the company has raised a further

debt of $ 5,000,000,000. The capital structure value remains the same, only the components

have changed.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

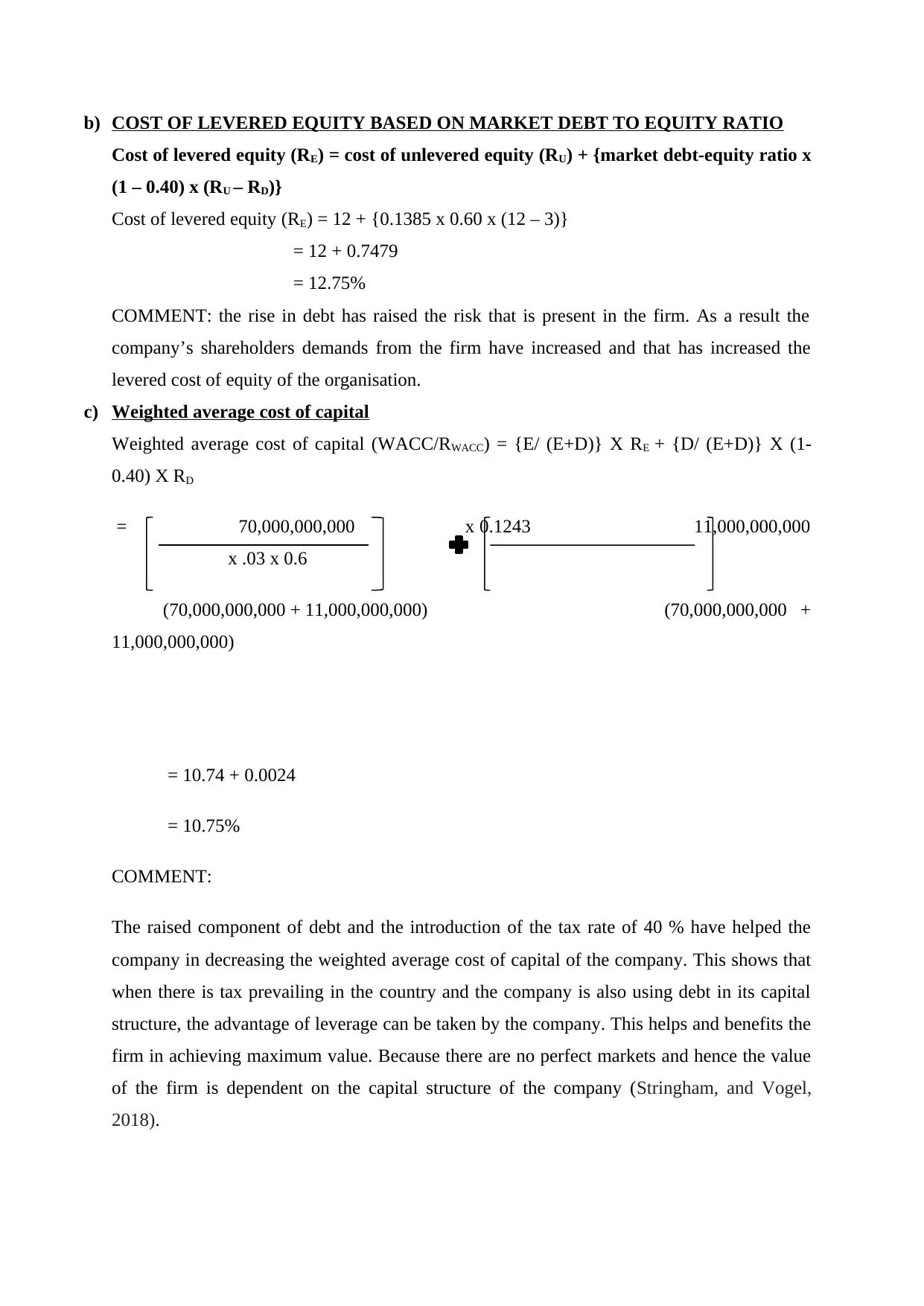

b) COST OF LEVERED EQUITY BASED ON MARKET DEBT TO EQUITY RATIO

Cost of levered equity (RE) = cost of unlevered equity (RU) + {market debt-equity ratio x

(1 – 0.40) x (RU – RD)}

Cost of levered equity (RE) = 12 + {0.1385 x 0.60 x (12 – 3)}

= 12 + 0.7479

= 12.75%

COMMENT: the rise in debt has raised the risk that is present in the firm. As a result the

company’s shareholders demands from the firm have increased and that has increased the

levered cost of equity of the organisation.

c) Weighted average cost of capital

Weighted average cost of capital (WACC/RWACC) = {E/ (E+D)} X RE + {D/ (E+D)} X (1-

0.40) X RD

= 70,000,000,000 x 0.1243 11,000,000,000

x .03 x 0.6

(70,000,000,000 + 11,000,000,000) (70,000,000,000 +

11,000,000,000)

= 10.74 + 0.0024

= 10.75%

COMMENT:

The raised component of debt and the introduction of the tax rate of 40 % have helped the

company in decreasing the weighted average cost of capital of the company. This shows that

when there is tax prevailing in the country and the company is also using debt in its capital

structure, the advantage of leverage can be taken by the company. This helps and benefits the

firm in achieving maximum value. Because there are no perfect markets and hence the value

of the firm is dependent on the capital structure of the company (Stringham, and Vogel,

2018).

Cost of levered equity (RE) = cost of unlevered equity (RU) + {market debt-equity ratio x

(1 – 0.40) x (RU – RD)}

Cost of levered equity (RE) = 12 + {0.1385 x 0.60 x (12 – 3)}

= 12 + 0.7479

= 12.75%

COMMENT: the rise in debt has raised the risk that is present in the firm. As a result the

company’s shareholders demands from the firm have increased and that has increased the

levered cost of equity of the organisation.

c) Weighted average cost of capital

Weighted average cost of capital (WACC/RWACC) = {E/ (E+D)} X RE + {D/ (E+D)} X (1-

0.40) X RD

= 70,000,000,000 x 0.1243 11,000,000,000

x .03 x 0.6

(70,000,000,000 + 11,000,000,000) (70,000,000,000 +

11,000,000,000)

= 10.74 + 0.0024

= 10.75%

COMMENT:

The raised component of debt and the introduction of the tax rate of 40 % have helped the

company in decreasing the weighted average cost of capital of the company. This shows that

when there is tax prevailing in the country and the company is also using debt in its capital

structure, the advantage of leverage can be taken by the company. This helps and benefits the

firm in achieving maximum value. Because there are no perfect markets and hence the value

of the firm is dependent on the capital structure of the company (Stringham, and Vogel,

2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

OVERALL COMMENT: when the capital markets are imperfect the dependency of the

firm on debt up to a certain level helps the organisation in achieving maximum value for

itself. This is because of the tax shield that is enjoyed on the interest paid. The overall costs

are lowered for the company. This is also synthesised by the pecked order theory. As per this

approach an optimal level of debt is must to attain optimal value for the organisation. And as

per traditional approach also, the weighted average cost is able to be lowered with an

optimum mix of debt and equity (Graham, et. al 2017).

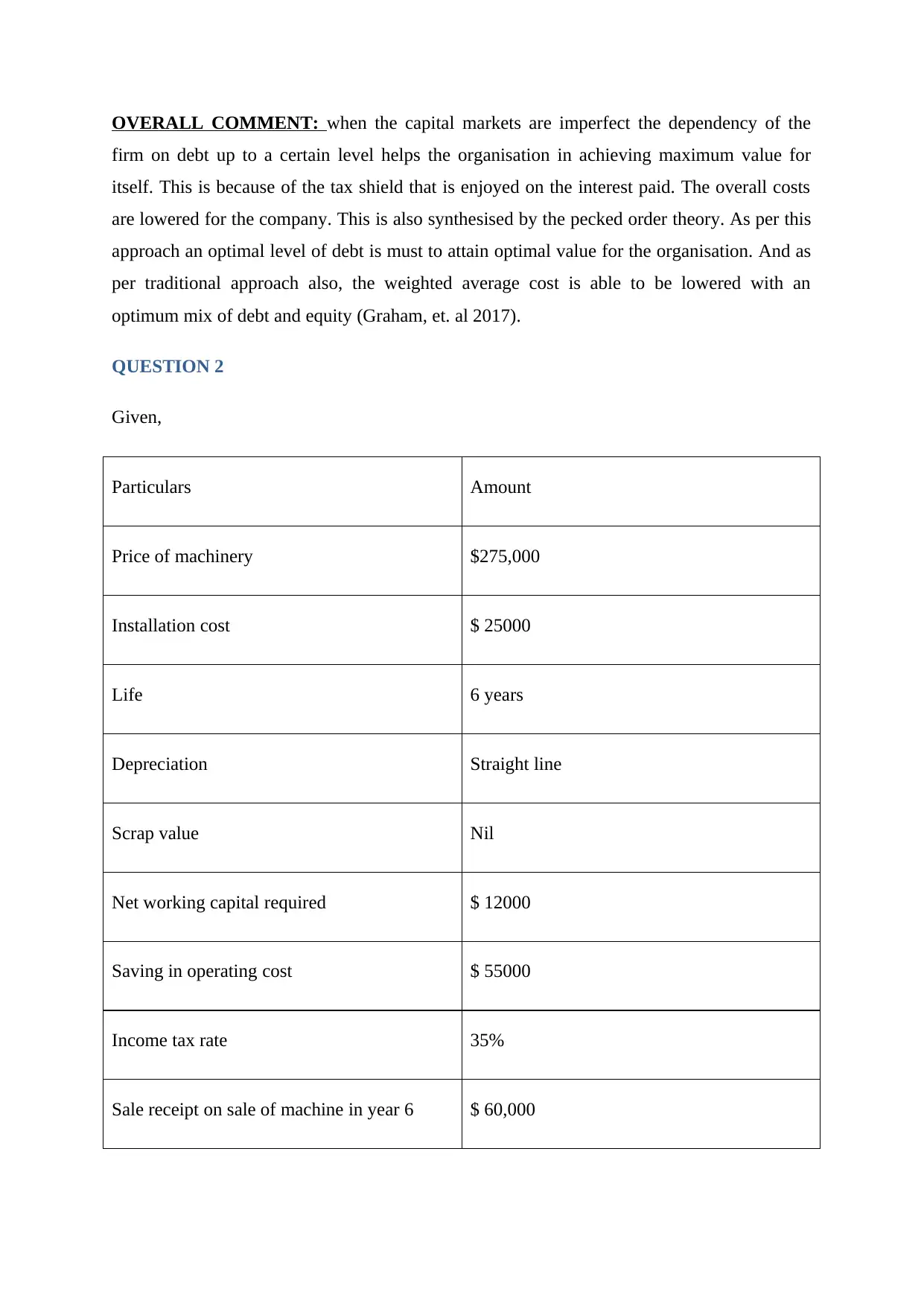

QUESTION 2

Given,

Particulars Amount

Price of machinery $275,000

Installation cost $ 25000

Life 6 years

Depreciation Straight line

Scrap value Nil

Net working capital required $ 12000

Saving in operating cost $ 55000

Income tax rate 35%

Sale receipt on sale of machine in year 6 $ 60,000

firm on debt up to a certain level helps the organisation in achieving maximum value for

itself. This is because of the tax shield that is enjoyed on the interest paid. The overall costs

are lowered for the company. This is also synthesised by the pecked order theory. As per this

approach an optimal level of debt is must to attain optimal value for the organisation. And as

per traditional approach also, the weighted average cost is able to be lowered with an

optimum mix of debt and equity (Graham, et. al 2017).

QUESTION 2

Given,

Particulars Amount

Price of machinery $275,000

Installation cost $ 25000

Life 6 years

Depreciation Straight line

Scrap value Nil

Net working capital required $ 12000

Saving in operating cost $ 55000

Income tax rate 35%

Sale receipt on sale of machine in year 6 $ 60,000

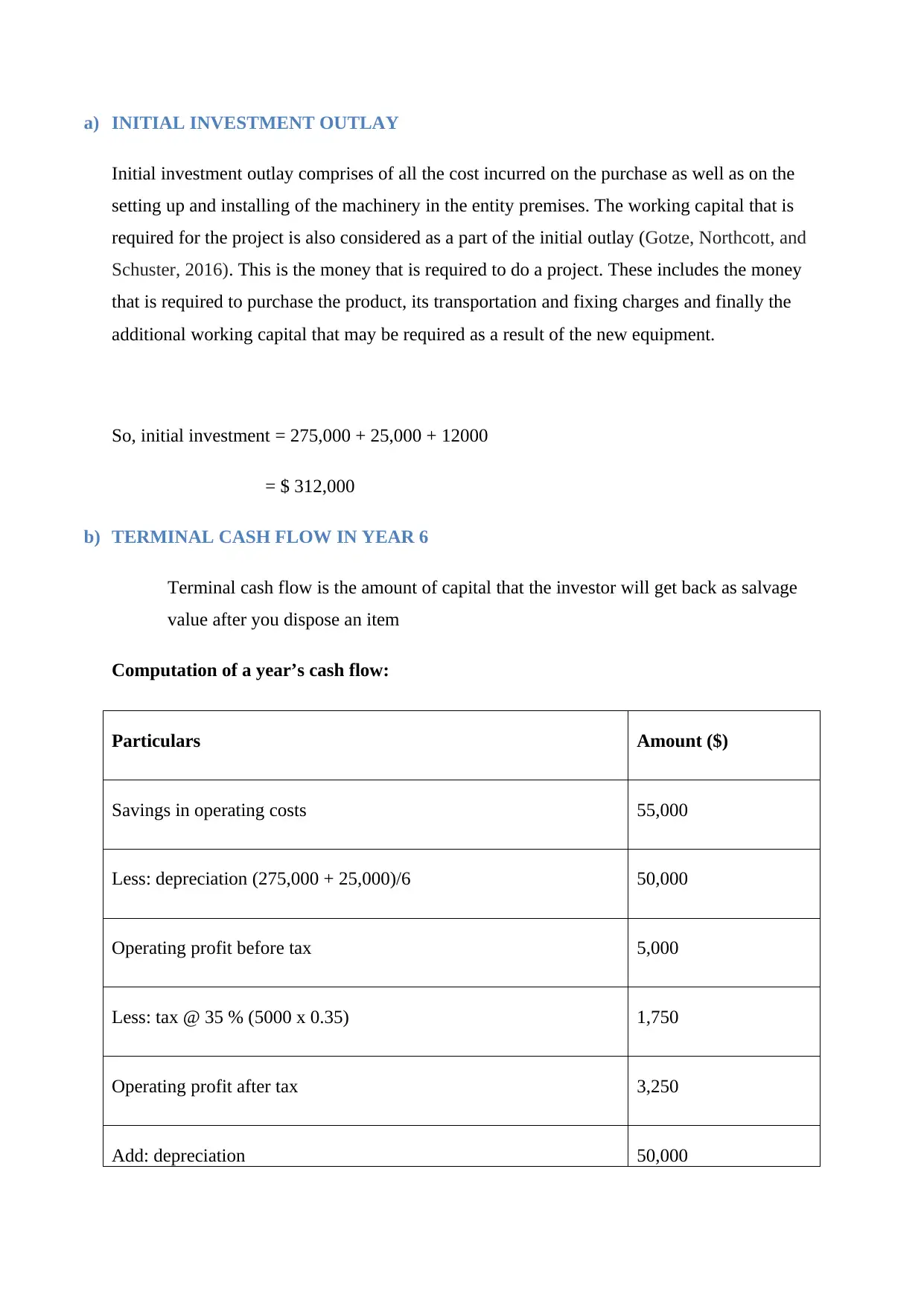

a) INITIAL INVESTMENT OUTLAY

Initial investment outlay comprises of all the cost incurred on the purchase as well as on the

setting up and installing of the machinery in the entity premises. The working capital that is

required for the project is also considered as a part of the initial outlay (Gotze, Northcott, and

Schuster, 2016). This is the money that is required to do a project. These includes the money

that is required to purchase the product, its transportation and fixing charges and finally the

additional working capital that may be required as a result of the new equipment.

So, initial investment = 275,000 + 25,000 + 12000

= $ 312,000

b) TERMINAL CASH FLOW IN YEAR 6

Terminal cash flow is the amount of capital that the investor will get back as salvage

value after you dispose an item

Computation of a year’s cash flow:

Particulars Amount ($)

Savings in operating costs 55,000

Less: depreciation (275,000 + 25,000)/6 50,000

Operating profit before tax 5,000

Less: tax @ 35 % (5000 x 0.35) 1,750

Operating profit after tax 3,250

Add: depreciation 50,000

Initial investment outlay comprises of all the cost incurred on the purchase as well as on the

setting up and installing of the machinery in the entity premises. The working capital that is

required for the project is also considered as a part of the initial outlay (Gotze, Northcott, and

Schuster, 2016). This is the money that is required to do a project. These includes the money

that is required to purchase the product, its transportation and fixing charges and finally the

additional working capital that may be required as a result of the new equipment.

So, initial investment = 275,000 + 25,000 + 12000

= $ 312,000

b) TERMINAL CASH FLOW IN YEAR 6

Terminal cash flow is the amount of capital that the investor will get back as salvage

value after you dispose an item

Computation of a year’s cash flow:

Particulars Amount ($)

Savings in operating costs 55,000

Less: depreciation (275,000 + 25,000)/6 50,000

Operating profit before tax 5,000

Less: tax @ 35 % (5000 x 0.35) 1,750

Operating profit after tax 3,250

Add: depreciation 50,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.