Corporate and Financial Accounting Report: Consolidation and Analysis

VerifiedAdded on 2023/01/06

|13

|3110

|34

Report

AI Summary

This report provides a comprehensive analysis of corporate and financial accounting principles. It begins with journal entries and ledger postings related to share applications. The report then delves into the reasons and methods for corporate share capital reduction, differentiating between share buybacks and capital reduction. It explores different types of debt instruments and discusses ways companies expand by obtaining new assets, including the preparation of journal entries for acquisitions. The report also examines intra-group transactions, including journal entries for elimination, profit realization, and the rules for dividend eliminations. Finally, it includes a worksheet, consolidation adjustments, and elimination entries using the NET method.

Corporate and

Financial Accounting

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

a. Journals entries.........................................................................................................................1

b. Recording data in ledger..........................................................................................................1

QUESTION 2...................................................................................................................................2

a. The most common reasons for a corporation to reduce share capital......................................2

b. The allowable methods of reducing share capital....................................................................3

c. Discussion of the differences between share buyback and capital reduction..........................3

d. The different types of debt instruments...................................................................................3

QUESTION 3...................................................................................................................................4

a. Explanation of the ways in which a company may expand by obtaining new assets..............4

b. Preparation of journal entries to record the acquisition by Jamuna River Ltd........................4

QUESTION 4...................................................................................................................................5

a. Preparation of the journal entries required to eliminate the intra-group transactions..............5

b. When are profits realised in relation to inventory transfers within the group.........................6

c. The rules for the elimination entry for intra-group transactions relating to dividend declared

by the parent company and dividend declared by the subsidiary company.................................7

QUESTION 5...................................................................................................................................7

a. Complete the worksheet below using the NET method...........................................................7

b. Prepare the consolidation adjustments and eliminations entries..............................................8

CONCLUSION................................................................................................................................9

REFERENCES .............................................................................................................................10

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

a. Journals entries.........................................................................................................................1

b. Recording data in ledger..........................................................................................................1

QUESTION 2...................................................................................................................................2

a. The most common reasons for a corporation to reduce share capital......................................2

b. The allowable methods of reducing share capital....................................................................3

c. Discussion of the differences between share buyback and capital reduction..........................3

d. The different types of debt instruments...................................................................................3

QUESTION 3...................................................................................................................................4

a. Explanation of the ways in which a company may expand by obtaining new assets..............4

b. Preparation of journal entries to record the acquisition by Jamuna River Ltd........................4

QUESTION 4...................................................................................................................................5

a. Preparation of the journal entries required to eliminate the intra-group transactions..............5

b. When are profits realised in relation to inventory transfers within the group.........................6

c. The rules for the elimination entry for intra-group transactions relating to dividend declared

by the parent company and dividend declared by the subsidiary company.................................7

QUESTION 5...................................................................................................................................7

a. Complete the worksheet below using the NET method...........................................................7

b. Prepare the consolidation adjustments and eliminations entries..............................................8

CONCLUSION................................................................................................................................9

REFERENCES .............................................................................................................................10

INTRODUCTION

Corporate and financial accounting is two different branches that are focused by

businesses while planning to analyse financial strength. In order to determine actual position of

the company both of them are focused as with the help of them information of financial

transactions is recorded in books and performance of entity is evaluated on the basis of same

(Barker, 2019). Present report is focused with assessment of various elements so that

understanding of corporate and financial accounting could be enhanced. There are various types

of elements that are focused while completing this report. These are share application,

corporations reducing share capital, acquisition, elimination of intra-group transactions etc.

Apart from this, consolidated adjustments along with elimination entries are also passed in this

assignment.

QUESTION 1

a. Journals entries

Date Particulars Amount

Dr. Cr.

31/07/1

9

Bank a/c Dr.

To Share Application a/c

1000000

10,00,000

01/08/1

9

Share application a/c Dr.

To Share capital a/c

800000

800000

01/08/1

9

Share Application a/c Dr.

To bank a/c

200000

200000

b. Recording data in ledger

Bank a/c

Date Particulars Amount Date Particulars Amount

31/07/ To share application a/c 1000000 01/08/1 By share application a/c 800000

1

Corporate and financial accounting is two different branches that are focused by

businesses while planning to analyse financial strength. In order to determine actual position of

the company both of them are focused as with the help of them information of financial

transactions is recorded in books and performance of entity is evaluated on the basis of same

(Barker, 2019). Present report is focused with assessment of various elements so that

understanding of corporate and financial accounting could be enhanced. There are various types

of elements that are focused while completing this report. These are share application,

corporations reducing share capital, acquisition, elimination of intra-group transactions etc.

Apart from this, consolidated adjustments along with elimination entries are also passed in this

assignment.

QUESTION 1

a. Journals entries

Date Particulars Amount

Dr. Cr.

31/07/1

9

Bank a/c Dr.

To Share Application a/c

1000000

10,00,000

01/08/1

9

Share application a/c Dr.

To Share capital a/c

800000

800000

01/08/1

9

Share Application a/c Dr.

To bank a/c

200000

200000

b. Recording data in ledger

Bank a/c

Date Particulars Amount Date Particulars Amount

31/07/ To share application a/c 1000000 01/08/1 By share application a/c 800000

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

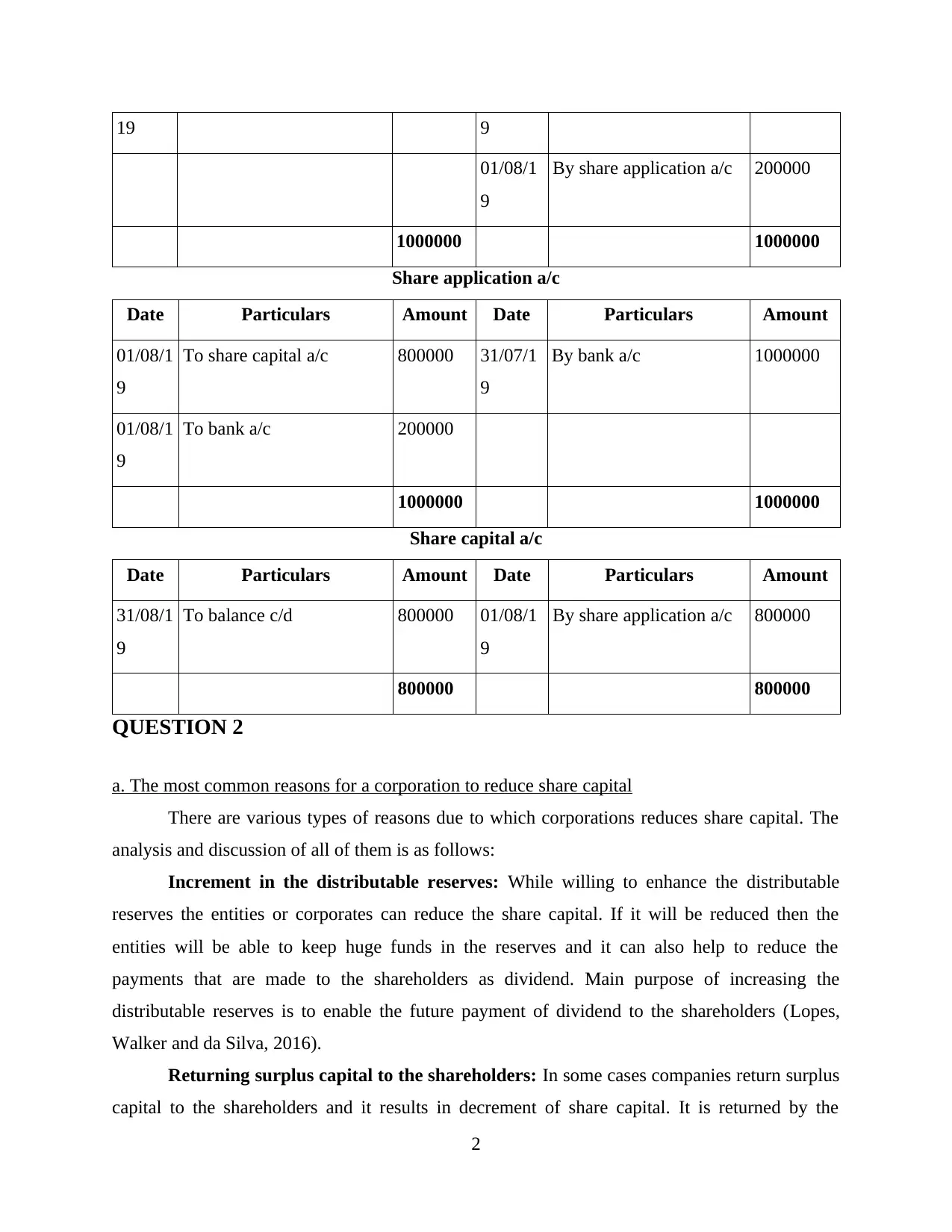

19 9

01/08/1

9

By share application a/c 200000

1000000 1000000

Share application a/c

Date Particulars Amount Date Particulars Amount

01/08/1

9

To share capital a/c 800000 31/07/1

9

By bank a/c 1000000

01/08/1

9

To bank a/c 200000

1000000 1000000

Share capital a/c

Date Particulars Amount Date Particulars Amount

31/08/1

9

To balance c/d 800000 01/08/1

9

By share application a/c 800000

800000 800000

QUESTION 2

a. The most common reasons for a corporation to reduce share capital

There are various types of reasons due to which corporations reduces share capital. The

analysis and discussion of all of them is as follows:

Increment in the distributable reserves: While willing to enhance the distributable

reserves the entities or corporates can reduce the share capital. If it will be reduced then the

entities will be able to keep huge funds in the reserves and it can also help to reduce the

payments that are made to the shareholders as dividend. Main purpose of increasing the

distributable reserves is to enable the future payment of dividend to the shareholders (Lopes,

Walker and da Silva, 2016).

Returning surplus capital to the shareholders: In some cases companies return surplus

capital to the shareholders and it results in decrement of share capital. It is returned by the

2

01/08/1

9

By share application a/c 200000

1000000 1000000

Share application a/c

Date Particulars Amount Date Particulars Amount

01/08/1

9

To share capital a/c 800000 31/07/1

9

By bank a/c 1000000

01/08/1

9

To bank a/c 200000

1000000 1000000

Share capital a/c

Date Particulars Amount Date Particulars Amount

31/08/1

9

To balance c/d 800000 01/08/1

9

By share application a/c 800000

800000 800000

QUESTION 2

a. The most common reasons for a corporation to reduce share capital

There are various types of reasons due to which corporations reduces share capital. The

analysis and discussion of all of them is as follows:

Increment in the distributable reserves: While willing to enhance the distributable

reserves the entities or corporates can reduce the share capital. If it will be reduced then the

entities will be able to keep huge funds in the reserves and it can also help to reduce the

payments that are made to the shareholders as dividend. Main purpose of increasing the

distributable reserves is to enable the future payment of dividend to the shareholders (Lopes,

Walker and da Silva, 2016).

Returning surplus capital to the shareholders: In some cases companies return surplus

capital to the shareholders and it results in decrement of share capital. It is returned by the

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

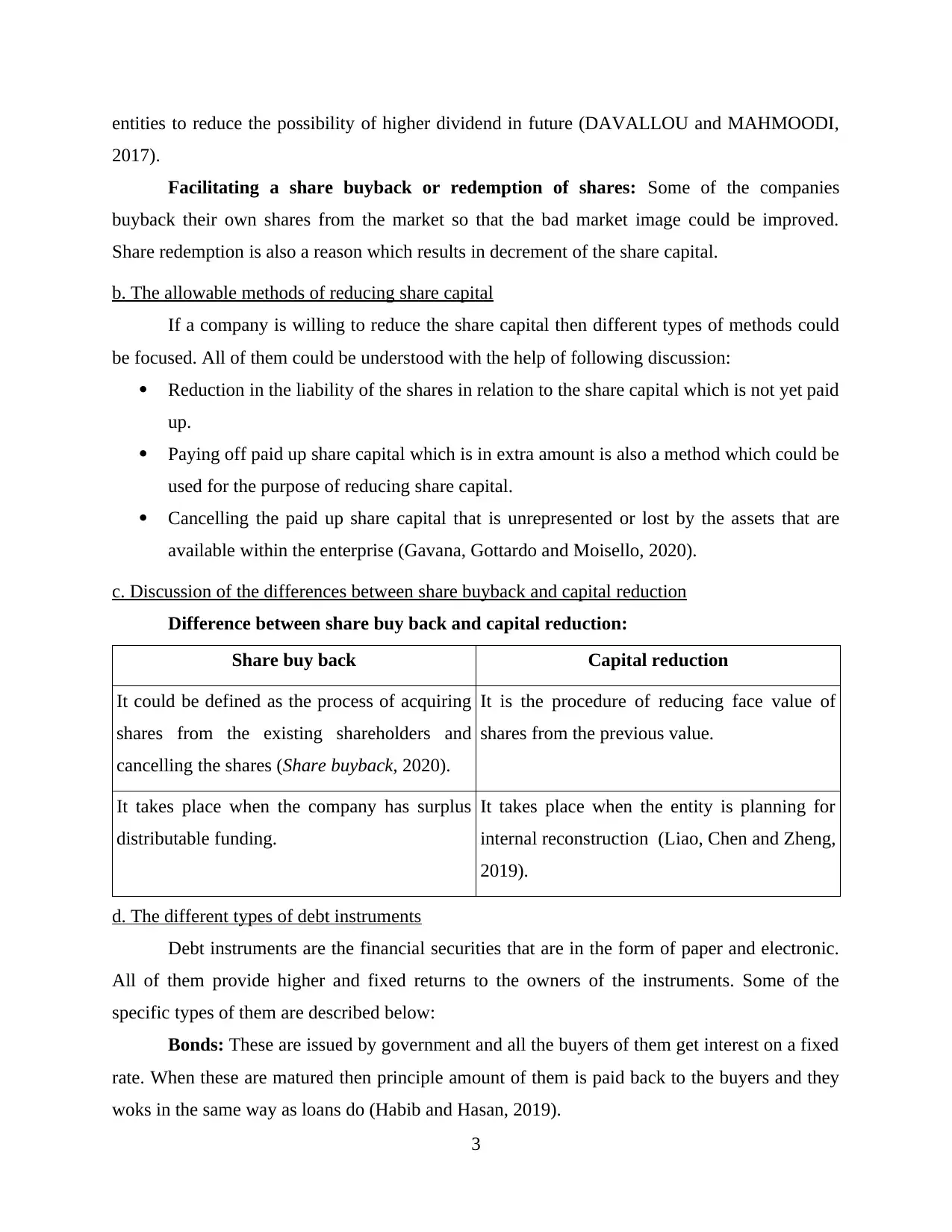

entities to reduce the possibility of higher dividend in future (DAVALLOU and MAHMOODI,

2017).

Facilitating a share buyback or redemption of shares: Some of the companies

buyback their own shares from the market so that the bad market image could be improved.

Share redemption is also a reason which results in decrement of the share capital.

b. The allowable methods of reducing share capital

If a company is willing to reduce the share capital then different types of methods could

be focused. All of them could be understood with the help of following discussion:

Reduction in the liability of the shares in relation to the share capital which is not yet paid

up.

Paying off paid up share capital which is in extra amount is also a method which could be

used for the purpose of reducing share capital.

Cancelling the paid up share capital that is unrepresented or lost by the assets that are

available within the enterprise (Gavana, Gottardo and Moisello, 2020).

c. Discussion of the differences between share buyback and capital reduction

Difference between share buy back and capital reduction:

Share buy back Capital reduction

It could be defined as the process of acquiring

shares from the existing shareholders and

cancelling the shares (Share buyback, 2020).

It is the procedure of reducing face value of

shares from the previous value.

It takes place when the company has surplus

distributable funding.

It takes place when the entity is planning for

internal reconstruction (Liao, Chen and Zheng,

2019).

d. The different types of debt instruments

Debt instruments are the financial securities that are in the form of paper and electronic.

All of them provide higher and fixed returns to the owners of the instruments. Some of the

specific types of them are described below:

Bonds: These are issued by government and all the buyers of them get interest on a fixed

rate. When these are matured then principle amount of them is paid back to the buyers and they

woks in the same way as loans do (Habib and Hasan, 2019).

3

2017).

Facilitating a share buyback or redemption of shares: Some of the companies

buyback their own shares from the market so that the bad market image could be improved.

Share redemption is also a reason which results in decrement of the share capital.

b. The allowable methods of reducing share capital

If a company is willing to reduce the share capital then different types of methods could

be focused. All of them could be understood with the help of following discussion:

Reduction in the liability of the shares in relation to the share capital which is not yet paid

up.

Paying off paid up share capital which is in extra amount is also a method which could be

used for the purpose of reducing share capital.

Cancelling the paid up share capital that is unrepresented or lost by the assets that are

available within the enterprise (Gavana, Gottardo and Moisello, 2020).

c. Discussion of the differences between share buyback and capital reduction

Difference between share buy back and capital reduction:

Share buy back Capital reduction

It could be defined as the process of acquiring

shares from the existing shareholders and

cancelling the shares (Share buyback, 2020).

It is the procedure of reducing face value of

shares from the previous value.

It takes place when the company has surplus

distributable funding.

It takes place when the entity is planning for

internal reconstruction (Liao, Chen and Zheng,

2019).

d. The different types of debt instruments

Debt instruments are the financial securities that are in the form of paper and electronic.

All of them provide higher and fixed returns to the owners of the instruments. Some of the

specific types of them are described below:

Bonds: These are issued by government and all the buyers of them get interest on a fixed

rate. When these are matured then principle amount of them is paid back to the buyers and they

woks in the same way as loans do (Habib and Hasan, 2019).

3

Mortgage: It is a type of loan for residential property and it is secured by a property. If

the borrower gets failed in making payment then the property could be seized.

Debentures: These are the financial instruments that are not backed by any type of

security. The main purpose of using them is to raise medium and long term funding for business.

QUESTION 3

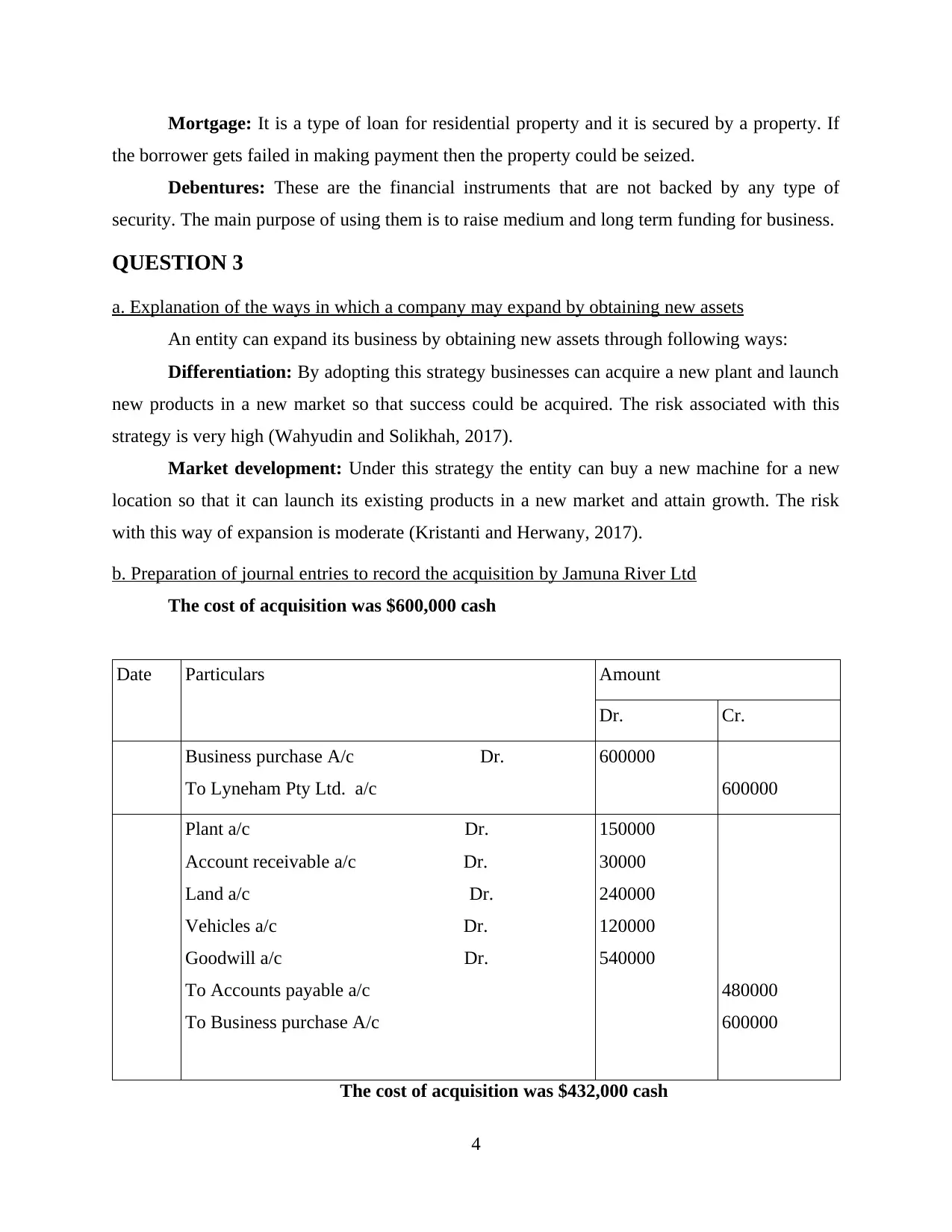

a. Explanation of the ways in which a company may expand by obtaining new assets

An entity can expand its business by obtaining new assets through following ways:

Differentiation: By adopting this strategy businesses can acquire a new plant and launch

new products in a new market so that success could be acquired. The risk associated with this

strategy is very high (Wahyudin and Solikhah, 2017).

Market development: Under this strategy the entity can buy a new machine for a new

location so that it can launch its existing products in a new market and attain growth. The risk

with this way of expansion is moderate (Kristanti and Herwany, 2017).

b. Preparation of journal entries to record the acquisition by Jamuna River Ltd

The cost of acquisition was $600,000 cash

Date Particulars Amount

Dr. Cr.

Business purchase A/c Dr.

To Lyneham Pty Ltd. a/c

600000

600000

Plant a/c Dr.

Account receivable a/c Dr.

Land a/c Dr.

Vehicles a/c Dr.

Goodwill a/c Dr.

To Accounts payable a/c

To Business purchase A/c

150000

30000

240000

120000

540000

480000

600000

The cost of acquisition was $432,000 cash

4

the borrower gets failed in making payment then the property could be seized.

Debentures: These are the financial instruments that are not backed by any type of

security. The main purpose of using them is to raise medium and long term funding for business.

QUESTION 3

a. Explanation of the ways in which a company may expand by obtaining new assets

An entity can expand its business by obtaining new assets through following ways:

Differentiation: By adopting this strategy businesses can acquire a new plant and launch

new products in a new market so that success could be acquired. The risk associated with this

strategy is very high (Wahyudin and Solikhah, 2017).

Market development: Under this strategy the entity can buy a new machine for a new

location so that it can launch its existing products in a new market and attain growth. The risk

with this way of expansion is moderate (Kristanti and Herwany, 2017).

b. Preparation of journal entries to record the acquisition by Jamuna River Ltd

The cost of acquisition was $600,000 cash

Date Particulars Amount

Dr. Cr.

Business purchase A/c Dr.

To Lyneham Pty Ltd. a/c

600000

600000

Plant a/c Dr.

Account receivable a/c Dr.

Land a/c Dr.

Vehicles a/c Dr.

Goodwill a/c Dr.

To Accounts payable a/c

To Business purchase A/c

150000

30000

240000

120000

540000

480000

600000

The cost of acquisition was $432,000 cash

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

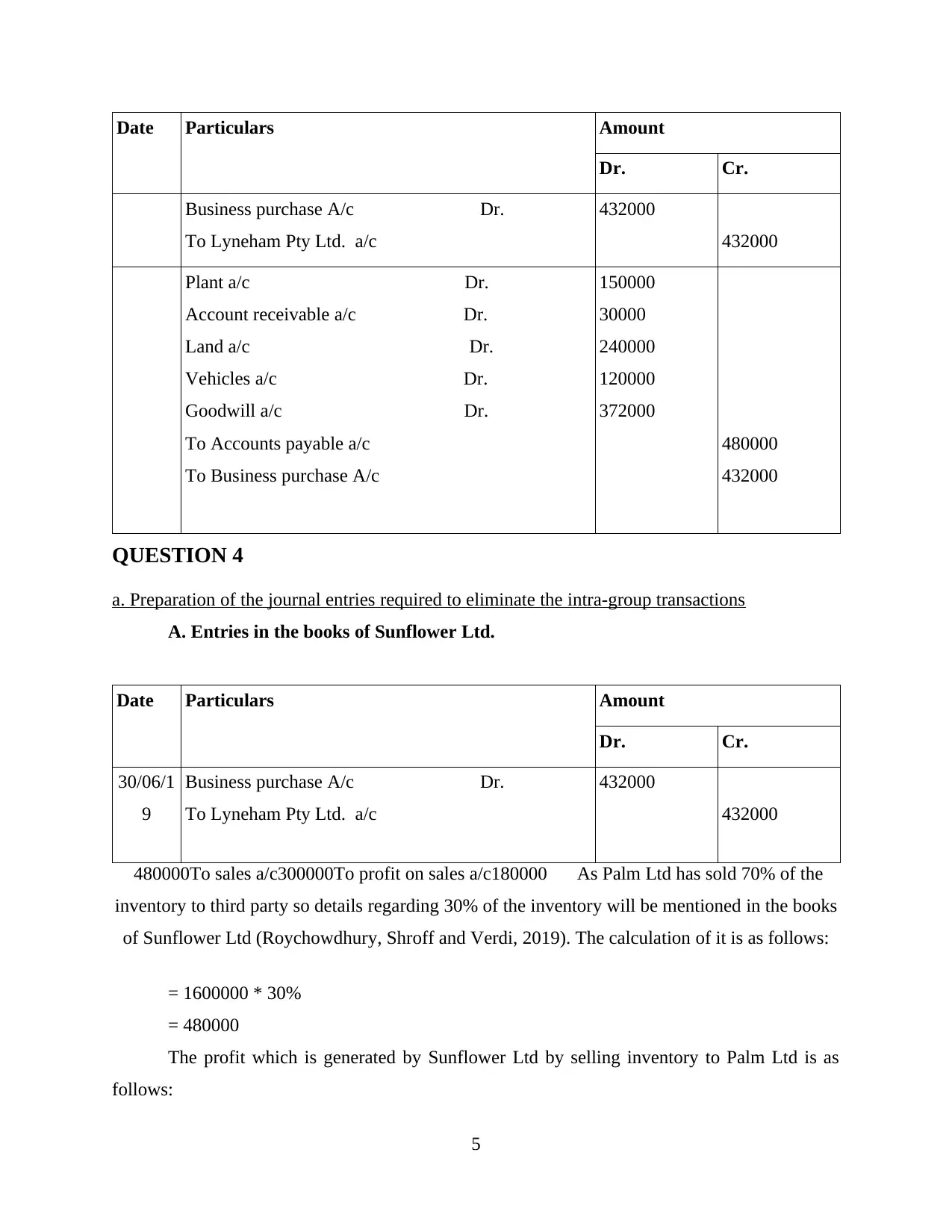

Date Particulars Amount

Dr. Cr.

Business purchase A/c Dr.

To Lyneham Pty Ltd. a/c

432000

432000

Plant a/c Dr.

Account receivable a/c Dr.

Land a/c Dr.

Vehicles a/c Dr.

Goodwill a/c Dr.

To Accounts payable a/c

To Business purchase A/c

150000

30000

240000

120000

372000

480000

432000

QUESTION 4

a. Preparation of the journal entries required to eliminate the intra-group transactions

A. Entries in the books of Sunflower Ltd.

Date Particulars Amount

Dr. Cr.

30/06/1

9

Business purchase A/c Dr.

To Lyneham Pty Ltd. a/c

432000

432000

480000To sales a/c300000To profit on sales a/c180000 As Palm Ltd has sold 70% of the

inventory to third party so details regarding 30% of the inventory will be mentioned in the books

of Sunflower Ltd (Roychowdhury, Shroff and Verdi, 2019). The calculation of it is as follows:

= 1600000 * 30%

= 480000

The profit which is generated by Sunflower Ltd by selling inventory to Palm Ltd is as

follows:

5

Dr. Cr.

Business purchase A/c Dr.

To Lyneham Pty Ltd. a/c

432000

432000

Plant a/c Dr.

Account receivable a/c Dr.

Land a/c Dr.

Vehicles a/c Dr.

Goodwill a/c Dr.

To Accounts payable a/c

To Business purchase A/c

150000

30000

240000

120000

372000

480000

432000

QUESTION 4

a. Preparation of the journal entries required to eliminate the intra-group transactions

A. Entries in the books of Sunflower Ltd.

Date Particulars Amount

Dr. Cr.

30/06/1

9

Business purchase A/c Dr.

To Lyneham Pty Ltd. a/c

432000

432000

480000To sales a/c300000To profit on sales a/c180000 As Palm Ltd has sold 70% of the

inventory to third party so details regarding 30% of the inventory will be mentioned in the books

of Sunflower Ltd (Roychowdhury, Shroff and Verdi, 2019). The calculation of it is as follows:

= 1600000 * 30%

= 480000

The profit which is generated by Sunflower Ltd by selling inventory to Palm Ltd is as

follows:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

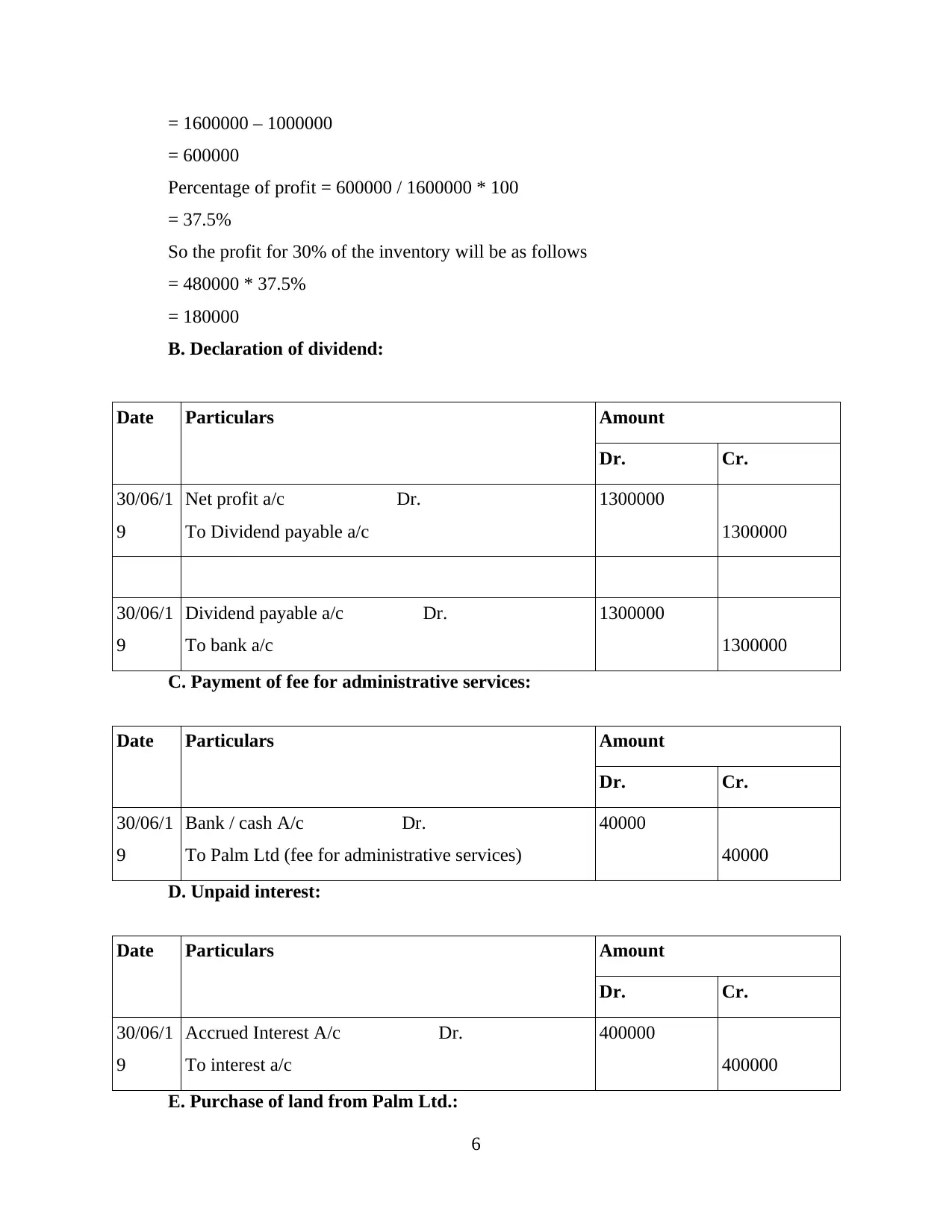

= 1600000 – 1000000

= 600000

Percentage of profit = 600000 / 1600000 * 100

= 37.5%

So the profit for 30% of the inventory will be as follows

= 480000 * 37.5%

= 180000

B. Declaration of dividend:

Date Particulars Amount

Dr. Cr.

30/06/1

9

Net profit a/c Dr.

To Dividend payable a/c

1300000

1300000

30/06/1

9

Dividend payable a/c Dr.

To bank a/c

1300000

1300000

C. Payment of fee for administrative services:

Date Particulars Amount

Dr. Cr.

30/06/1

9

Bank / cash A/c Dr.

To Palm Ltd (fee for administrative services)

40000

40000

D. Unpaid interest:

Date Particulars Amount

Dr. Cr.

30/06/1

9

Accrued Interest A/c Dr.

To interest a/c

400000

400000

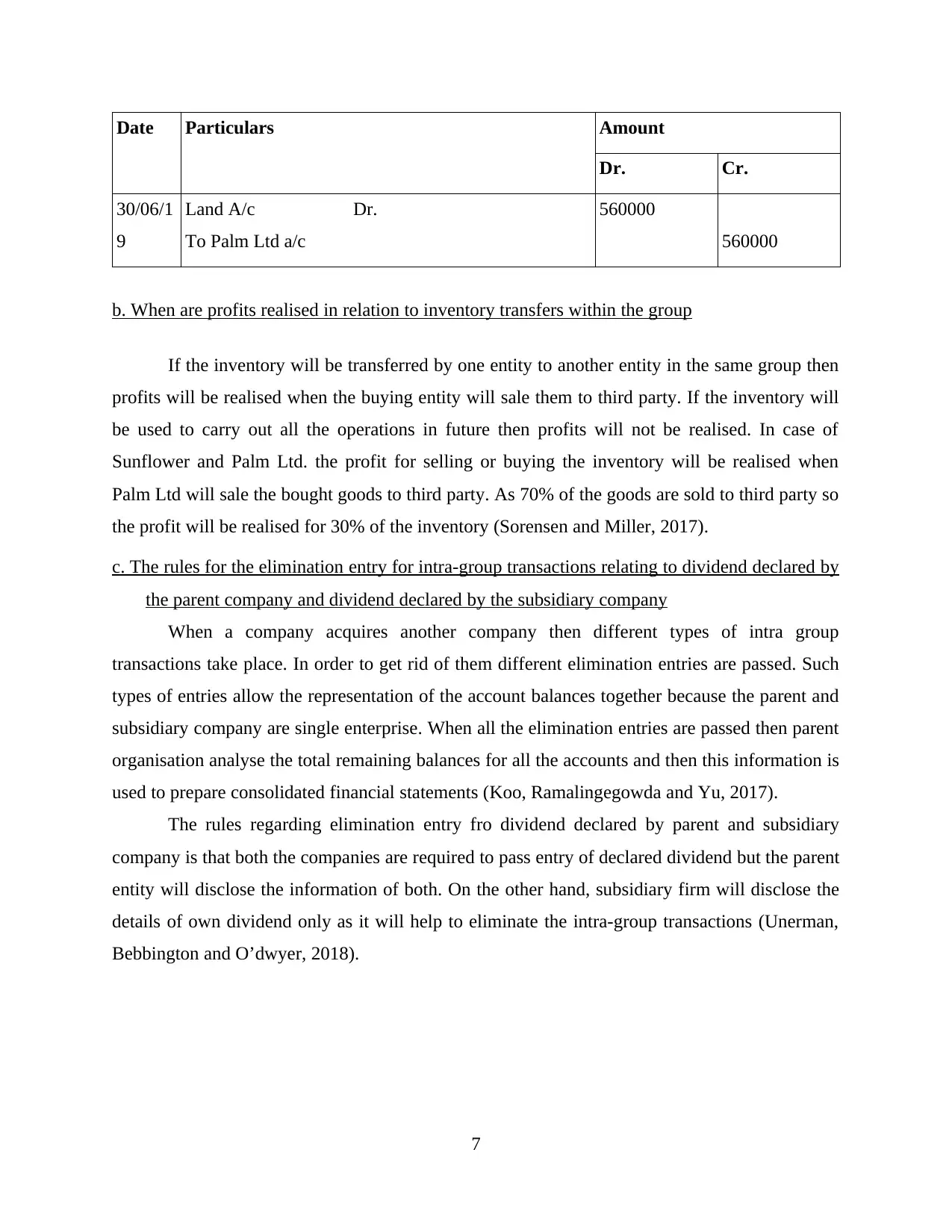

E. Purchase of land from Palm Ltd.:

6

= 600000

Percentage of profit = 600000 / 1600000 * 100

= 37.5%

So the profit for 30% of the inventory will be as follows

= 480000 * 37.5%

= 180000

B. Declaration of dividend:

Date Particulars Amount

Dr. Cr.

30/06/1

9

Net profit a/c Dr.

To Dividend payable a/c

1300000

1300000

30/06/1

9

Dividend payable a/c Dr.

To bank a/c

1300000

1300000

C. Payment of fee for administrative services:

Date Particulars Amount

Dr. Cr.

30/06/1

9

Bank / cash A/c Dr.

To Palm Ltd (fee for administrative services)

40000

40000

D. Unpaid interest:

Date Particulars Amount

Dr. Cr.

30/06/1

9

Accrued Interest A/c Dr.

To interest a/c

400000

400000

E. Purchase of land from Palm Ltd.:

6

Date Particulars Amount

Dr. Cr.

30/06/1

9

Land A/c Dr.

To Palm Ltd a/c

560000

560000

b. When are profits realised in relation to inventory transfers within the group

If the inventory will be transferred by one entity to another entity in the same group then

profits will be realised when the buying entity will sale them to third party. If the inventory will

be used to carry out all the operations in future then profits will not be realised. In case of

Sunflower and Palm Ltd. the profit for selling or buying the inventory will be realised when

Palm Ltd will sale the bought goods to third party. As 70% of the goods are sold to third party so

the profit will be realised for 30% of the inventory (Sorensen and Miller, 2017).

c. The rules for the elimination entry for intra-group transactions relating to dividend declared by

the parent company and dividend declared by the subsidiary company

When a company acquires another company then different types of intra group

transactions take place. In order to get rid of them different elimination entries are passed. Such

types of entries allow the representation of the account balances together because the parent and

subsidiary company are single enterprise. When all the elimination entries are passed then parent

organisation analyse the total remaining balances for all the accounts and then this information is

used to prepare consolidated financial statements (Koo, Ramalingegowda and Yu, 2017).

The rules regarding elimination entry fro dividend declared by parent and subsidiary

company is that both the companies are required to pass entry of declared dividend but the parent

entity will disclose the information of both. On the other hand, subsidiary firm will disclose the

details of own dividend only as it will help to eliminate the intra-group transactions (Unerman,

Bebbington and O’dwyer, 2018).

7

Dr. Cr.

30/06/1

9

Land A/c Dr.

To Palm Ltd a/c

560000

560000

b. When are profits realised in relation to inventory transfers within the group

If the inventory will be transferred by one entity to another entity in the same group then

profits will be realised when the buying entity will sale them to third party. If the inventory will

be used to carry out all the operations in future then profits will not be realised. In case of

Sunflower and Palm Ltd. the profit for selling or buying the inventory will be realised when

Palm Ltd will sale the bought goods to third party. As 70% of the goods are sold to third party so

the profit will be realised for 30% of the inventory (Sorensen and Miller, 2017).

c. The rules for the elimination entry for intra-group transactions relating to dividend declared by

the parent company and dividend declared by the subsidiary company

When a company acquires another company then different types of intra group

transactions take place. In order to get rid of them different elimination entries are passed. Such

types of entries allow the representation of the account balances together because the parent and

subsidiary company are single enterprise. When all the elimination entries are passed then parent

organisation analyse the total remaining balances for all the accounts and then this information is

used to prepare consolidated financial statements (Koo, Ramalingegowda and Yu, 2017).

The rules regarding elimination entry fro dividend declared by parent and subsidiary

company is that both the companies are required to pass entry of declared dividend but the parent

entity will disclose the information of both. On the other hand, subsidiary firm will disclose the

details of own dividend only as it will help to eliminate the intra-group transactions (Unerman,

Bebbington and O’dwyer, 2018).

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

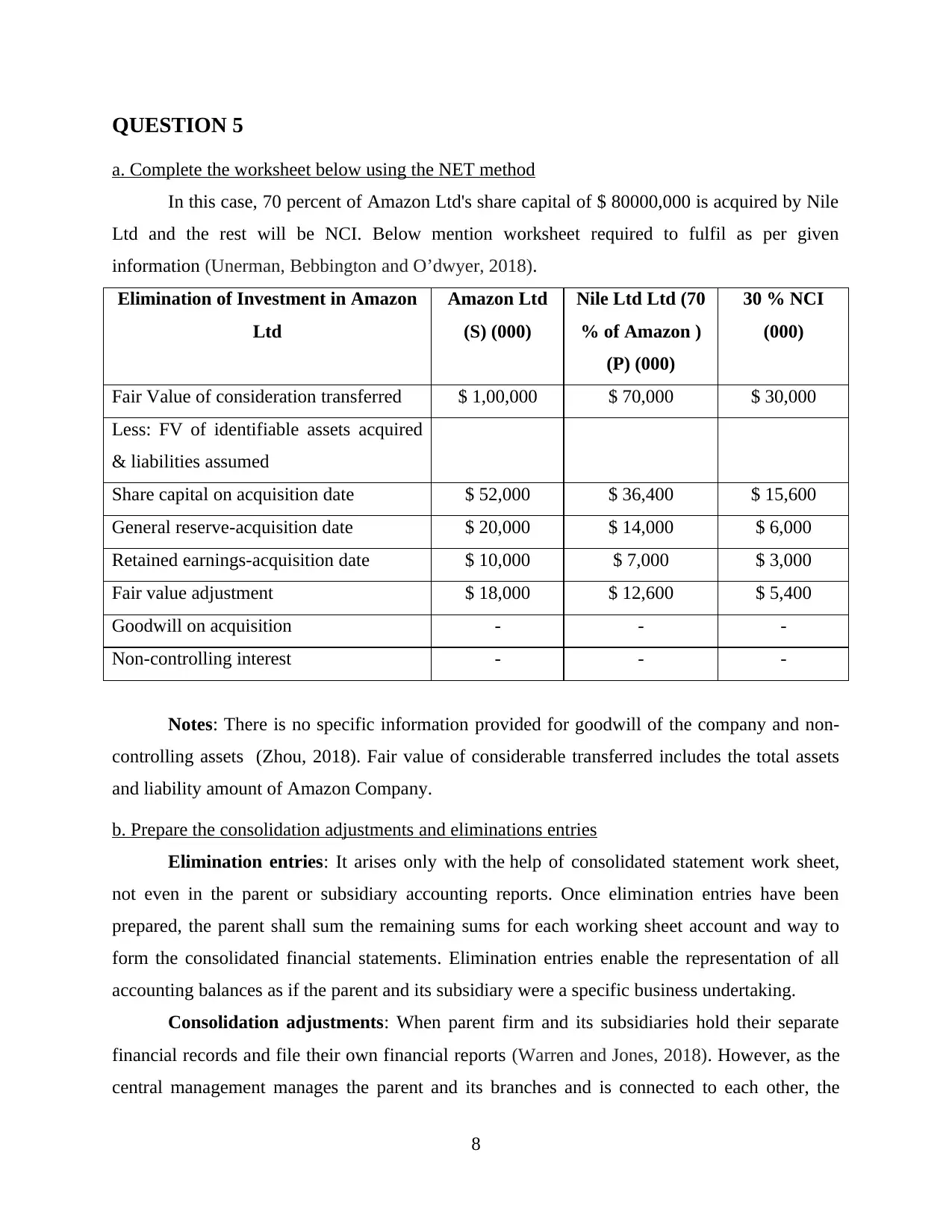

QUESTION 5

a. Complete the worksheet below using the NET method

In this case, 70 percent of Amazon Ltd's share capital of $ 80000,000 is acquired by Nile

Ltd and the rest will be NCI. Below mention worksheet required to fulfil as per given

information (Unerman, Bebbington and O’dwyer, 2018).

Elimination of Investment in Amazon

Ltd

Amazon Ltd

(S) (000)

Nile Ltd Ltd (70

% of Amazon )

(P) (000)

30 % NCI

(000)

Fair Value of consideration transferred $ 1,00,000 $ 70,000 $ 30,000

Less: FV of identifiable assets acquired

& liabilities assumed

Share capital on acquisition date $ 52,000 $ 36,400 $ 15,600

General reserve-acquisition date $ 20,000 $ 14,000 $ 6,000

Retained earnings-acquisition date $ 10,000 $ 7,000 $ 3,000

Fair value adjustment $ 18,000 $ 12,600 $ 5,400

Goodwill on acquisition - - -

Non-controlling interest - - -

Notes: There is no specific information provided for goodwill of the company and non-

controlling assets (Zhou, 2018). Fair value of considerable transferred includes the total assets

and liability amount of Amazon Company.

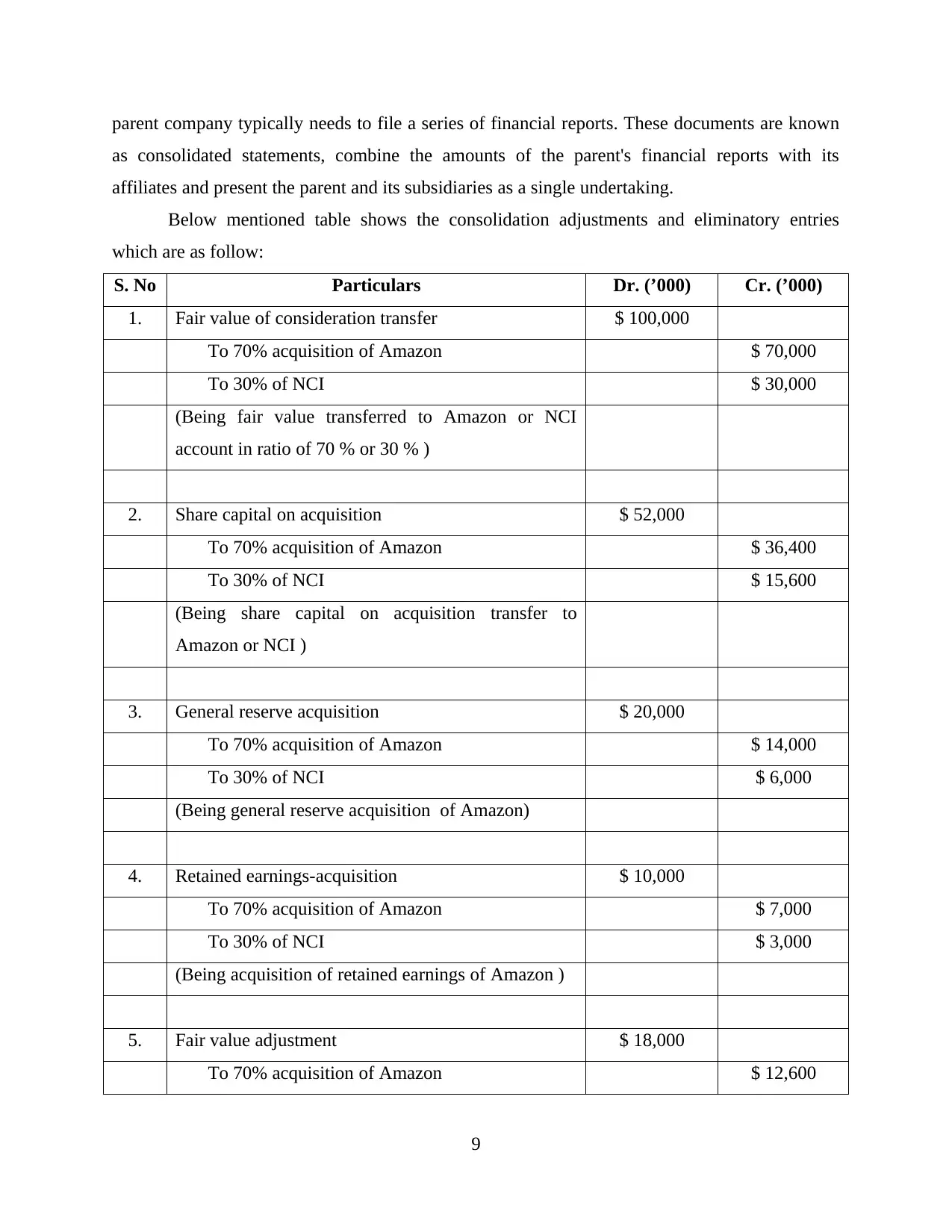

b. Prepare the consolidation adjustments and eliminations entries

Elimination entries: It arises only with the help of consolidated statement work sheet,

not even in the parent or subsidiary accounting reports. Once elimination entries have been

prepared, the parent shall sum the remaining sums for each working sheet account and way to

form the consolidated financial statements. Elimination entries enable the representation of all

accounting balances as if the parent and its subsidiary were a specific business undertaking.

Consolidation adjustments: When parent firm and its subsidiaries hold their separate

financial records and file their own financial reports (Warren and Jones, 2018). However, as the

central management manages the parent and its branches and is connected to each other, the

8

a. Complete the worksheet below using the NET method

In this case, 70 percent of Amazon Ltd's share capital of $ 80000,000 is acquired by Nile

Ltd and the rest will be NCI. Below mention worksheet required to fulfil as per given

information (Unerman, Bebbington and O’dwyer, 2018).

Elimination of Investment in Amazon

Ltd

Amazon Ltd

(S) (000)

Nile Ltd Ltd (70

% of Amazon )

(P) (000)

30 % NCI

(000)

Fair Value of consideration transferred $ 1,00,000 $ 70,000 $ 30,000

Less: FV of identifiable assets acquired

& liabilities assumed

Share capital on acquisition date $ 52,000 $ 36,400 $ 15,600

General reserve-acquisition date $ 20,000 $ 14,000 $ 6,000

Retained earnings-acquisition date $ 10,000 $ 7,000 $ 3,000

Fair value adjustment $ 18,000 $ 12,600 $ 5,400

Goodwill on acquisition - - -

Non-controlling interest - - -

Notes: There is no specific information provided for goodwill of the company and non-

controlling assets (Zhou, 2018). Fair value of considerable transferred includes the total assets

and liability amount of Amazon Company.

b. Prepare the consolidation adjustments and eliminations entries

Elimination entries: It arises only with the help of consolidated statement work sheet,

not even in the parent or subsidiary accounting reports. Once elimination entries have been

prepared, the parent shall sum the remaining sums for each working sheet account and way to

form the consolidated financial statements. Elimination entries enable the representation of all

accounting balances as if the parent and its subsidiary were a specific business undertaking.

Consolidation adjustments: When parent firm and its subsidiaries hold their separate

financial records and file their own financial reports (Warren and Jones, 2018). However, as the

central management manages the parent and its branches and is connected to each other, the

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

parent company typically needs to file a series of financial reports. These documents are known

as consolidated statements, combine the amounts of the parent's financial reports with its

affiliates and present the parent and its subsidiaries as a single undertaking.

Below mentioned table shows the consolidation adjustments and eliminatory entries

which are as follow:

S. No Particulars Dr. (’000) Cr. (’000)

1. Fair value of consideration transfer $ 100,000

To 70% acquisition of Amazon $ 70,000

To 30% of NCI $ 30,000

(Being fair value transferred to Amazon or NCI

account in ratio of 70 % or 30 % )

2. Share capital on acquisition $ 52,000

To 70% acquisition of Amazon $ 36,400

To 30% of NCI $ 15,600

(Being share capital on acquisition transfer to

Amazon or NCI )

3. General reserve acquisition $ 20,000

To 70% acquisition of Amazon $ 14,000

To 30% of NCI $ 6,000

(Being general reserve acquisition of Amazon)

4. Retained earnings-acquisition $ 10,000

To 70% acquisition of Amazon $ 7,000

To 30% of NCI $ 3,000

(Being acquisition of retained earnings of Amazon )

5. Fair value adjustment $ 18,000

To 70% acquisition of Amazon $ 12,600

9

as consolidated statements, combine the amounts of the parent's financial reports with its

affiliates and present the parent and its subsidiaries as a single undertaking.

Below mentioned table shows the consolidation adjustments and eliminatory entries

which are as follow:

S. No Particulars Dr. (’000) Cr. (’000)

1. Fair value of consideration transfer $ 100,000

To 70% acquisition of Amazon $ 70,000

To 30% of NCI $ 30,000

(Being fair value transferred to Amazon or NCI

account in ratio of 70 % or 30 % )

2. Share capital on acquisition $ 52,000

To 70% acquisition of Amazon $ 36,400

To 30% of NCI $ 15,600

(Being share capital on acquisition transfer to

Amazon or NCI )

3. General reserve acquisition $ 20,000

To 70% acquisition of Amazon $ 14,000

To 30% of NCI $ 6,000

(Being general reserve acquisition of Amazon)

4. Retained earnings-acquisition $ 10,000

To 70% acquisition of Amazon $ 7,000

To 30% of NCI $ 3,000

(Being acquisition of retained earnings of Amazon )

5. Fair value adjustment $ 18,000

To 70% acquisition of Amazon $ 12,600

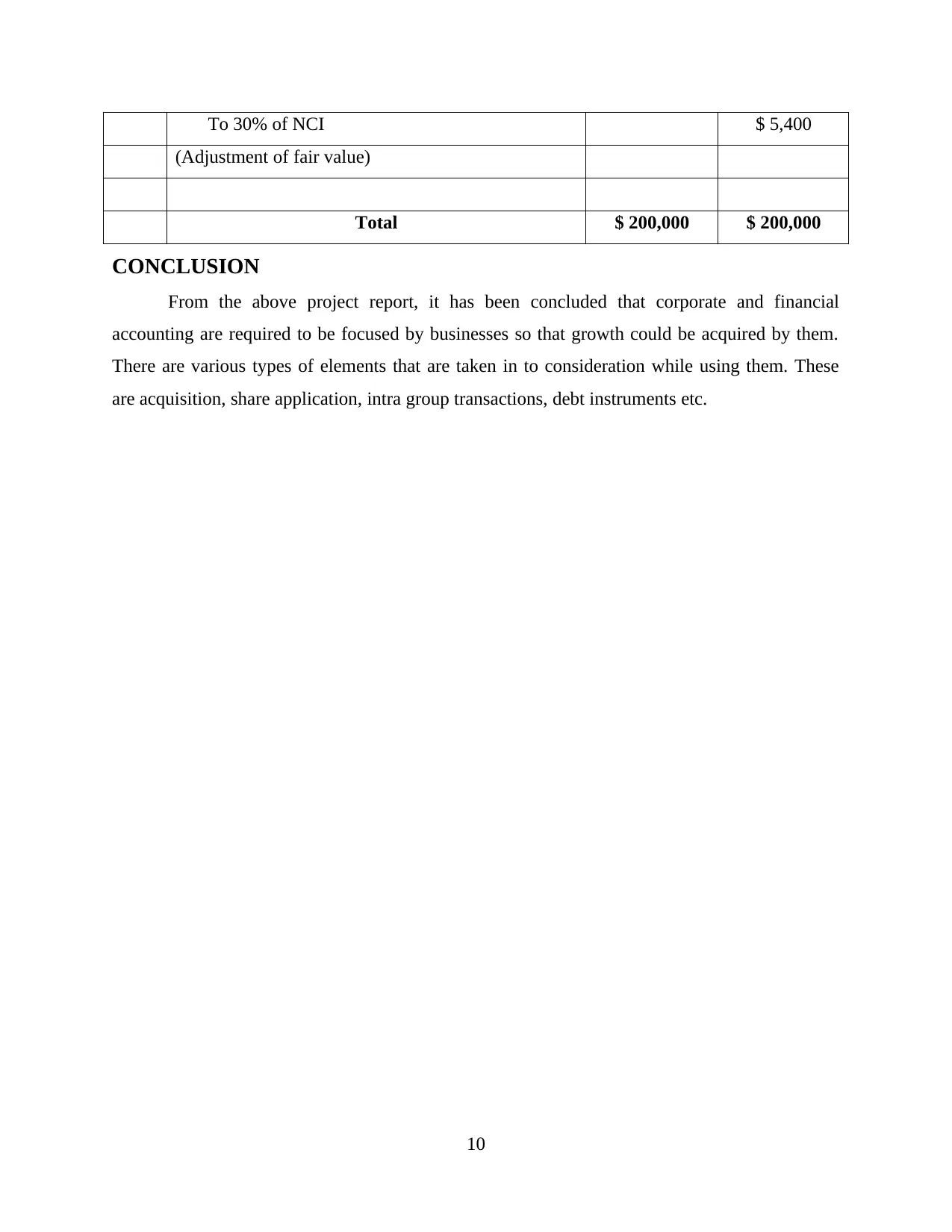

9

To 30% of NCI $ 5,400

(Adjustment of fair value)

Total $ 200,000 $ 200,000

CONCLUSION

From the above project report, it has been concluded that corporate and financial

accounting are required to be focused by businesses so that growth could be acquired by them.

There are various types of elements that are taken in to consideration while using them. These

are acquisition, share application, intra group transactions, debt instruments etc.

10

(Adjustment of fair value)

Total $ 200,000 $ 200,000

CONCLUSION

From the above project report, it has been concluded that corporate and financial

accounting are required to be focused by businesses so that growth could be acquired by them.

There are various types of elements that are taken in to consideration while using them. These

are acquisition, share application, intra group transactions, debt instruments etc.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.