HA2032 - Corporate Reporting and Disclosure in Business Combination

VerifiedAdded on 2022/11/28

|14

|3655

|147

Report

AI Summary

This report provides an in-depth analysis of corporate and financial accounting practices, specifically focusing on the Australian context. It begins with an executive summary and an introduction, setting the stage for a detailed examination of the conceptual framework for financial reporting and the concept of a reporting entity. The report critically evaluates the strengths and weaknesses of the conceptual framework, particularly concerning the definitions of financial elements such as assets, liabilities, equity, income, and expenses. It also explores the implications of classifying as a reporting entity and the compliance requirements with Australian Accounting Standards and disclosure requirements. Furthermore, the report delves into business combination analysis, including the acquisition of companies, purchase considerations, acquisition costs, and the fair value of net identifiable assets. It also examines the recognized value and fair value of different classes of assets and liabilities. The report utilizes examples of business combinations to illustrate the application of accounting principles. The content is designed to enhance the understanding of financial reporting requirements and business combinations within the Australian context. The report concludes with a summary of the key findings and references supporting the analysis.

CORPORATE AND

FINANCIAL ACCOUNTING

FINANCIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

The study conducted is based on the accounting reporting standards in Australia. It gives an

insight into the understanding of financial reporting requirements, gives information about the

framework’s strengths and weaknesses. Concept of reporting entity has been examined critically

and the implication of classification of reporting entity in terms of accounting standards has been

emphasised. Business combination or acquisition analysis has been illustrated. Questions like

fair value of consideration, components of acquisition costs, acquisition of identifiable assets,

valuation of assets, liabilities and contingent liabilities has been done. It gives an analysis of

company’s disclosure on acquisition or business combination.

The study conducted is based on the accounting reporting standards in Australia. It gives an

insight into the understanding of financial reporting requirements, gives information about the

framework’s strengths and weaknesses. Concept of reporting entity has been examined critically

and the implication of classification of reporting entity in terms of accounting standards has been

emphasised. Business combination or acquisition analysis has been illustrated. Questions like

fair value of consideration, components of acquisition costs, acquisition of identifiable assets,

valuation of assets, liabilities and contingent liabilities has been done. It gives an analysis of

company’s disclosure on acquisition or business combination.

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................4

PART 1............................................................................................................................................4

(i) Conceptual Framework for Financial Reporting....................................................................4

(ii) Reporting Entity.....................................................................................................................6

PART 2............................................................................................................................................8

(i)..................................................................................................................................................8

(ii)................................................................................................................................................8

(iii)...............................................................................................................................................8

(iv)................................................................................................................................................9

(v).................................................................................................................................................9

(vi)..............................................................................................................................................10

(vii)............................................................................................................................................10

(viii)...........................................................................................................................................11

(ix)..............................................................................................................................................11

(x)...............................................................................................................................................11

(xi)..............................................................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES................................................................................................................................1

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................4

PART 1............................................................................................................................................4

(i) Conceptual Framework for Financial Reporting....................................................................4

(ii) Reporting Entity.....................................................................................................................6

PART 2............................................................................................................................................8

(i)..................................................................................................................................................8

(ii)................................................................................................................................................8

(iii)...............................................................................................................................................8

(iv)................................................................................................................................................9

(v).................................................................................................................................................9

(vi)..............................................................................................................................................10

(vii)............................................................................................................................................10

(viii)...........................................................................................................................................11

(ix)..............................................................................................................................................11

(x)...............................................................................................................................................11

(xi)..............................................................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES................................................................................................................................1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The corporate and financial accounting is the most significant part of an organization

because it helps them to record and manage the daily transactions in the books of account. The

report will focus and describe the role and importance of Australian Accounting Standards for

reporting entity in order to prepare and present financial statement.

PART 1

(i) Conceptual Framework for Financial Reporting

It describes the objective and concepts which are required for general purpose financial

reporting. It is a tool which:

a) Helps the IASB- International Accounting Standards Board for developing standards

which are based on concepts which are consistent.

b) Helps preparers for making accounting policies which are consistent in lieu of no

standard applying for a transaction in particular or event or when standard permits a

choice of accounting policy (Garg, Peach and Simnett, 2020).

c) Assistance from others for understanding and interpreting the standards.

The merits which can be seen in the framework assisting financial reporting are:

a) It provides a clarification that information required for meeting the financial reporting

objective includes information which can be used for assessing the management’s

stewardship of the resources’ entity

b) Tells about role of prudence and substance in reporting of financials.

c) Clarification that top level of measurement uncertainty can make the information of

financials less relevant

d) Clarification that prominent decisions on, for instance recognition and measurement are

driven by taking in consideration nature of information resulting about financial

performance and position financially.

e) Providing clarity in definitions of assets and liabilities and guidance extensively on

supporting the definitions.

Effects of the revised framework

The corporate and financial accounting is the most significant part of an organization

because it helps them to record and manage the daily transactions in the books of account. The

report will focus and describe the role and importance of Australian Accounting Standards for

reporting entity in order to prepare and present financial statement.

PART 1

(i) Conceptual Framework for Financial Reporting

It describes the objective and concepts which are required for general purpose financial

reporting. It is a tool which:

a) Helps the IASB- International Accounting Standards Board for developing standards

which are based on concepts which are consistent.

b) Helps preparers for making accounting policies which are consistent in lieu of no

standard applying for a transaction in particular or event or when standard permits a

choice of accounting policy (Garg, Peach and Simnett, 2020).

c) Assistance from others for understanding and interpreting the standards.

The merits which can be seen in the framework assisting financial reporting are:

a) It provides a clarification that information required for meeting the financial reporting

objective includes information which can be used for assessing the management’s

stewardship of the resources’ entity

b) Tells about role of prudence and substance in reporting of financials.

c) Clarification that top level of measurement uncertainty can make the information of

financials less relevant

d) Clarification that prominent decisions on, for instance recognition and measurement are

driven by taking in consideration nature of information resulting about financial

performance and position financially.

e) Providing clarity in definitions of assets and liabilities and guidance extensively on

supporting the definitions.

Effects of the revised framework

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Complete, clear and updated set of concepts help IASB for developing standards which

better meet requirements of investors, creditors and lenders. As the framework guides the

IASB as it develops standards, it will have effect on financials when organisations

implement new standards based on the revised conceptual framework (Garg, Peach, and

Simnett, 2020).

The IASB will not be changing the existing standards being a result of changes to the

framework. Having an existing standard working well in practice, IASB shall not propose

amendment to the standard because of inconsistency with the framework. Any decision

of amending existing standard will need IASB to go through normal process due for

addition of project to the agenda and developing a draft and amendment to the standard.

Analysing strengths and weaknesses with definition of financial elements

Conceptual framework defines the elements in an elaborative manner in paragraphs and

sections. Asset is defined as the economic resource which is controlled by organisation as a

result of events from past. Economic resource has been defined as a right which has potential of

producing benefits which are economical. Liability has been defined as an obligation of the

organisation for transferring economic resource being a result from past events. Equity is the

interest which is residual in the assets of entity after deduction of the liabilities (Davern and

et.al., 2019). Income is the increase and decrease in assets and liabilities respectively which

result in equity increase, other than relating to contributions from holder of equity claims.

Expense are decrease or increase in assets and liabilities respectively which result in equity

decrease, other than ones relating to distribution to holder of equity claims.

Analysing the strengths of framework, it can be said that the draft continues in defining income

and expenses in the terms of change in the liabilities and assets. It lays emphasis at number of

places regarding important decisions, for instance, recognition and measurement which is driven

by taking in consideration nature of resulting information about financial performance and

position financially (Davern and et.al., 2019).

The weaknesses which can be stated are that IASB has not been proposing to bring change

in definition of assets and liabilities for addressing problems which can occur in instrument

classification with features of both liability and equity. The issues with Financial Instruments

better meet requirements of investors, creditors and lenders. As the framework guides the

IASB as it develops standards, it will have effect on financials when organisations

implement new standards based on the revised conceptual framework (Garg, Peach, and

Simnett, 2020).

The IASB will not be changing the existing standards being a result of changes to the

framework. Having an existing standard working well in practice, IASB shall not propose

amendment to the standard because of inconsistency with the framework. Any decision

of amending existing standard will need IASB to go through normal process due for

addition of project to the agenda and developing a draft and amendment to the standard.

Analysing strengths and weaknesses with definition of financial elements

Conceptual framework defines the elements in an elaborative manner in paragraphs and

sections. Asset is defined as the economic resource which is controlled by organisation as a

result of events from past. Economic resource has been defined as a right which has potential of

producing benefits which are economical. Liability has been defined as an obligation of the

organisation for transferring economic resource being a result from past events. Equity is the

interest which is residual in the assets of entity after deduction of the liabilities (Davern and

et.al., 2019). Income is the increase and decrease in assets and liabilities respectively which

result in equity increase, other than relating to contributions from holder of equity claims.

Expense are decrease or increase in assets and liabilities respectively which result in equity

decrease, other than ones relating to distribution to holder of equity claims.

Analysing the strengths of framework, it can be said that the draft continues in defining income

and expenses in the terms of change in the liabilities and assets. It lays emphasis at number of

places regarding important decisions, for instance, recognition and measurement which is driven

by taking in consideration nature of resulting information about financial performance and

position financially (Davern and et.al., 2019).

The weaknesses which can be stated are that IASB has not been proposing to bring change

in definition of assets and liabilities for addressing problems which can occur in instrument

classification with features of both liability and equity. The issues with Financial Instruments

with characteristics of equity research project have to be addressed. Amendments have to be

made in a procedural way.

(ii) Reporting Entity

Concept of Reporting Entity

In order to understand the reporting entity, concept the use of general-purpose financial

report (GPFR) is need to be used by the users of the financial statement. This is known as

reporting entity. This is being used by the users to analyse and understand the financial position

and performance of the business in a respective market. After analysing and understanding the

financial reports the users of the company make appropriate decisions. For example; the users of

business such as investors first identify the financial performance via use of ratio analysis tool on

financial items and then make a decision to whether the investment in such company is profitable

or not.

The financial reporting is also used by the company that wants to acquire other company

for expansion purpose. At the time of merger and acquisition, the financial statement and report

is used to calculate the goodwill and purchase consideration. The reporting entity are those

entities that need to prepare a GPFR which states that their business follows all the Australian

Accounting Standards in order to prepare the financial report (Zhong and Li, 2017).

Compliance of Australian Accounting Standards and Disclosure Requirement

In Australia, the disclosure and financial reporting requirement are set on the basis of the public

interest in the entity. The type of entities requires to follow the accounting standards and

discloser requirements are as follow:

The disclosing entities whose share and securities are listed on an Australian stock

exchange as a result of circulation of prospectus. This mainly involve the listed

corporations and registered managed investment schemes.

Unlisted public companies and large proprietary companies having the gross operating

revenue of $10 million or more and gross assets of $5 million or more or the employees

of 50 number or more. Out of this the companies need to meets atleast two criteria.

Small proprietary companies.

made in a procedural way.

(ii) Reporting Entity

Concept of Reporting Entity

In order to understand the reporting entity, concept the use of general-purpose financial

report (GPFR) is need to be used by the users of the financial statement. This is known as

reporting entity. This is being used by the users to analyse and understand the financial position

and performance of the business in a respective market. After analysing and understanding the

financial reports the users of the company make appropriate decisions. For example; the users of

business such as investors first identify the financial performance via use of ratio analysis tool on

financial items and then make a decision to whether the investment in such company is profitable

or not.

The financial reporting is also used by the company that wants to acquire other company

for expansion purpose. At the time of merger and acquisition, the financial statement and report

is used to calculate the goodwill and purchase consideration. The reporting entity are those

entities that need to prepare a GPFR which states that their business follows all the Australian

Accounting Standards in order to prepare the financial report (Zhong and Li, 2017).

Compliance of Australian Accounting Standards and Disclosure Requirement

In Australia, the disclosure and financial reporting requirement are set on the basis of the public

interest in the entity. The type of entities requires to follow the accounting standards and

discloser requirements are as follow:

The disclosing entities whose share and securities are listed on an Australian stock

exchange as a result of circulation of prospectus. This mainly involve the listed

corporations and registered managed investment schemes.

Unlisted public companies and large proprietary companies having the gross operating

revenue of $10 million or more and gross assets of $5 million or more or the employees

of 50 number or more. Out of this the companies need to meets atleast two criteria.

Small proprietary companies.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Under the Australian corporation law, all disclosure entities including companies and registered

managed investment schemes need to follow all the accounting standards and also need to

maintain the accurate recording of financial transaction with no error and omission. Not only

that, the companies also need to enable the preparation of financial statements including the audit

for those financial statements. As per the Australian Accounting Standard Board (AASB), all the

entities need to prepare the annual financial statement except the small proprietary companies.

The component of the annual financial statement includes statement of profit and loss account,

balance sheet and statement of cash flow. The corporation law of the Australia also provides the

consolidated financial statements which must be prepared by the entities having one or more

subsidiaries and associates. And this must be prepared as per the accounting standards

requirement. Despite meeting all the disclosing requirement by the disclosing entities, they also

need to prepare a half-yearly financial statement (Chaplin, 2017).

As per the AASB and corporation law, the annual and half-yearly financial statement

requirement includes the following:

a. Director’s report which includes the information related to the operations of the entity.

b. Directors’ declaration form which state that whether the business comply all the

requirement of the accounting standard or not and also whether the financial position of

the company is showing true and fair view or not. And also state solvent financial

position of the entity.

c. The financial statement of the entity must be audited by the independent auditor of the

company and review the annual as well as half-yearly financial statement of the

company.

Besides this, the three most important point or element which every entity excluding small

business entity need to be consider as per the Australian financial reporting framework are as

follow:

The financial statement must be prepared by the entities by complying all the accounting

standards and disclosure requirement such as going concern concept, provision

requirement etc.

While auditing the financial statement of the companies, the independent auditor of the

company needs to comply all the auditing standards in order to give true and fair opinion

on the business financial statements.

managed investment schemes need to follow all the accounting standards and also need to

maintain the accurate recording of financial transaction with no error and omission. Not only

that, the companies also need to enable the preparation of financial statements including the audit

for those financial statements. As per the Australian Accounting Standard Board (AASB), all the

entities need to prepare the annual financial statement except the small proprietary companies.

The component of the annual financial statement includes statement of profit and loss account,

balance sheet and statement of cash flow. The corporation law of the Australia also provides the

consolidated financial statements which must be prepared by the entities having one or more

subsidiaries and associates. And this must be prepared as per the accounting standards

requirement. Despite meeting all the disclosing requirement by the disclosing entities, they also

need to prepare a half-yearly financial statement (Chaplin, 2017).

As per the AASB and corporation law, the annual and half-yearly financial statement

requirement includes the following:

a. Director’s report which includes the information related to the operations of the entity.

b. Directors’ declaration form which state that whether the business comply all the

requirement of the accounting standard or not and also whether the financial position of

the company is showing true and fair view or not. And also state solvent financial

position of the entity.

c. The financial statement of the entity must be audited by the independent auditor of the

company and review the annual as well as half-yearly financial statement of the

company.

Besides this, the three most important point or element which every entity excluding small

business entity need to be consider as per the Australian financial reporting framework are as

follow:

The financial statement must be prepared by the entities by complying all the accounting

standards and disclosure requirement such as going concern concept, provision

requirement etc.

While auditing the financial statement of the companies, the independent auditor of the

company needs to comply all the auditing standards in order to give true and fair opinion

on the business financial statements.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The last element includes the appropriate level of surveillance and enforcement which

further state that the financial report has been prepared by using all the framework and

standards which is basically set by the corporation law and the Australian Accounting

Standard Board.

These elements need to be complied by the reporting entity in order to remove and minimize the

government intervention on the business activities (Chaplin, 2017).

PART 2

(i)

Business combination is basically a transaction between acquire and acquiree company in

which the acquire company borrow and obtain a control over the other business. The After Pay

ltd. acquire total six companies which include the After-pay holdings ltd., After pay US

incorporation, After pay Australia Pty ltd., Touch Corp ltd., clearpay finance ltd. and After pay

Canada ltd. The After-pay ltd. acquire the Touch Corp ltd. in 2017. The other company such as

AP Eager ltd. acquire one company name Automotive Holding group ltd. (AHG) in order to

expand its business. The company recently operates all over the Australia and New Zealand

(Linnenluecke, and et.al., 2017).

(ii)

Purchase consideration is a term which means the amount which need to be paid by the

acquirer company to acquiree company in order to complete the process of business

combination. This consideration may be in the form of cash, share, debentures or any other non-

cash instruments. The fair value of the consideration is paid by the After-pay ltd. to acquire

Touch Corp ltd. is $1 billion (1000 million) and the company hold 90% of its share holdings.

The fair value of consideration paid by AP Eager ltd. include $2.3b (2300 million).

(iii)

Acquisition cost in the term of business combination is known as the payment made by the

acquiring company to the specific shareholders of the acquiree company. The component of

acquisition cost includes cash and non-cash consideration and mixed considerations. The cash

offering includes the cash payment, non-cash offerings include the securities payment to

further state that the financial report has been prepared by using all the framework and

standards which is basically set by the corporation law and the Australian Accounting

Standard Board.

These elements need to be complied by the reporting entity in order to remove and minimize the

government intervention on the business activities (Chaplin, 2017).

PART 2

(i)

Business combination is basically a transaction between acquire and acquiree company in

which the acquire company borrow and obtain a control over the other business. The After Pay

ltd. acquire total six companies which include the After-pay holdings ltd., After pay US

incorporation, After pay Australia Pty ltd., Touch Corp ltd., clearpay finance ltd. and After pay

Canada ltd. The After-pay ltd. acquire the Touch Corp ltd. in 2017. The other company such as

AP Eager ltd. acquire one company name Automotive Holding group ltd. (AHG) in order to

expand its business. The company recently operates all over the Australia and New Zealand

(Linnenluecke, and et.al., 2017).

(ii)

Purchase consideration is a term which means the amount which need to be paid by the

acquirer company to acquiree company in order to complete the process of business

combination. This consideration may be in the form of cash, share, debentures or any other non-

cash instruments. The fair value of the consideration is paid by the After-pay ltd. to acquire

Touch Corp ltd. is $1 billion (1000 million) and the company hold 90% of its share holdings.

The fair value of consideration paid by AP Eager ltd. include $2.3b (2300 million).

(iii)

Acquisition cost in the term of business combination is known as the payment made by the

acquiring company to the specific shareholders of the acquiree company. The component of

acquisition cost includes cash and non-cash consideration and mixed considerations. The cash

offering includes the cash payment, non-cash offerings include the securities payment to

shareholder and the mixed offering includes the cash and securities in specified proportion. The

value of the payment is equal to the purchase price or purchase consideration of the company.

The total acquisition cost in addition to the purchase price includes the transaction cost of

acquiring the company such as commission, fees etc (Zhang and Ge, 2017).

(iv)

The fair value of the net identifiable assets is the value which is currently traded on the

market. Basically, this is the market price of the assets and liabilities of the company which may

be high and low than the carrying value of those particular assets and liabilities. Basically, the

fair value of the net identifiable assets of the Touch Corp ltd. which is acquired by the After-pay

ltd. is $900 million and of the AHG which is acquired by the AP Eagers ltd. is $2200 million.

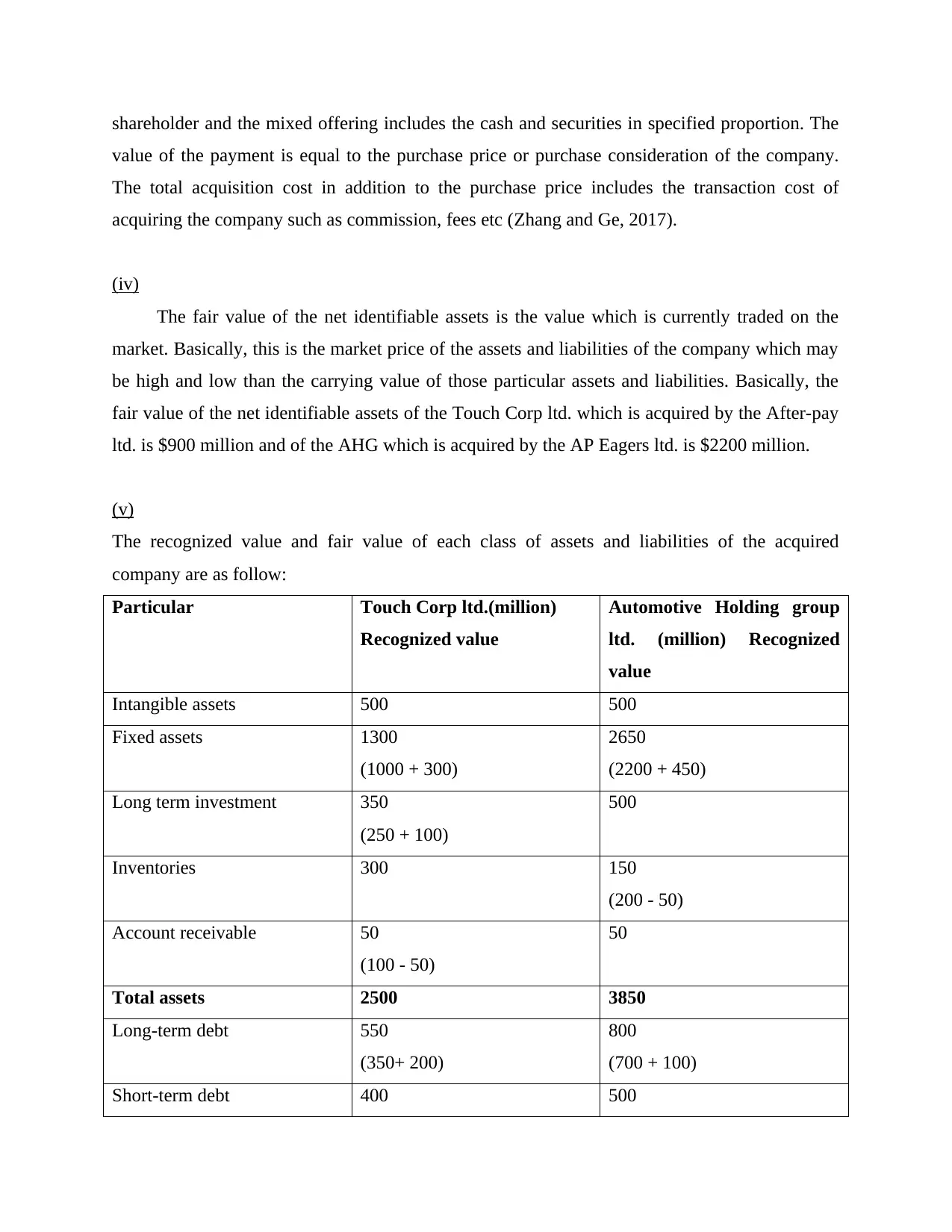

(v)

The recognized value and fair value of each class of assets and liabilities of the acquired

company are as follow:

Particular Touch Corp ltd.(million)

Recognized value

Automotive Holding group

ltd. (million) Recognized

value

Intangible assets 500 500

Fixed assets 1300

(1000 + 300)

2650

(2200 + 450)

Long term investment 350

(250 + 100)

500

Inventories 300 150

(200 - 50)

Account receivable 50

(100 - 50)

50

Total assets 2500 3850

Long-term debt 550

(350+ 200)

800

(700 + 100)

Short-term debt 400 500

value of the payment is equal to the purchase price or purchase consideration of the company.

The total acquisition cost in addition to the purchase price includes the transaction cost of

acquiring the company such as commission, fees etc (Zhang and Ge, 2017).

(iv)

The fair value of the net identifiable assets is the value which is currently traded on the

market. Basically, this is the market price of the assets and liabilities of the company which may

be high and low than the carrying value of those particular assets and liabilities. Basically, the

fair value of the net identifiable assets of the Touch Corp ltd. which is acquired by the After-pay

ltd. is $900 million and of the AHG which is acquired by the AP Eagers ltd. is $2200 million.

(v)

The recognized value and fair value of each class of assets and liabilities of the acquired

company are as follow:

Particular Touch Corp ltd.(million)

Recognized value

Automotive Holding group

ltd. (million) Recognized

value

Intangible assets 500 500

Fixed assets 1300

(1000 + 300)

2650

(2200 + 450)

Long term investment 350

(250 + 100)

500

Inventories 300 150

(200 - 50)

Account receivable 50

(100 - 50)

50

Total assets 2500 3850

Long-term debt 550

(350+ 200)

800

(700 + 100)

Short-term debt 400 500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

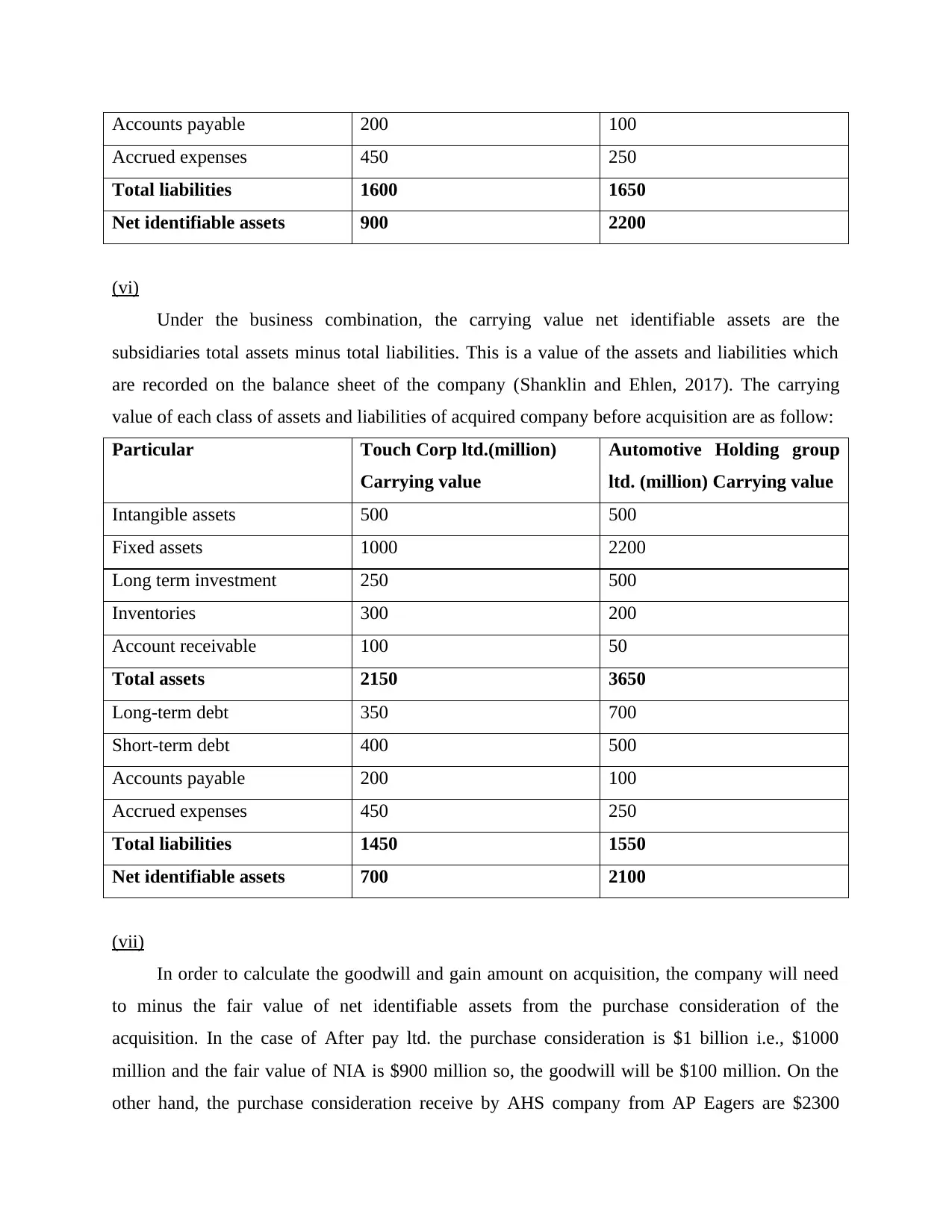

Accounts payable 200 100

Accrued expenses 450 250

Total liabilities 1600 1650

Net identifiable assets 900 2200

(vi)

Under the business combination, the carrying value net identifiable assets are the

subsidiaries total assets minus total liabilities. This is a value of the assets and liabilities which

are recorded on the balance sheet of the company (Shanklin and Ehlen, 2017). The carrying

value of each class of assets and liabilities of acquired company before acquisition are as follow:

Particular Touch Corp ltd.(million)

Carrying value

Automotive Holding group

ltd. (million) Carrying value

Intangible assets 500 500

Fixed assets 1000 2200

Long term investment 250 500

Inventories 300 200

Account receivable 100 50

Total assets 2150 3650

Long-term debt 350 700

Short-term debt 400 500

Accounts payable 200 100

Accrued expenses 450 250

Total liabilities 1450 1550

Net identifiable assets 700 2100

(vii)

In order to calculate the goodwill and gain amount on acquisition, the company will need

to minus the fair value of net identifiable assets from the purchase consideration of the

acquisition. In the case of After pay ltd. the purchase consideration is $1 billion i.e., $1000

million and the fair value of NIA is $900 million so, the goodwill will be $100 million. On the

other hand, the purchase consideration receive by AHS company from AP Eagers are $2300

Accrued expenses 450 250

Total liabilities 1600 1650

Net identifiable assets 900 2200

(vi)

Under the business combination, the carrying value net identifiable assets are the

subsidiaries total assets minus total liabilities. This is a value of the assets and liabilities which

are recorded on the balance sheet of the company (Shanklin and Ehlen, 2017). The carrying

value of each class of assets and liabilities of acquired company before acquisition are as follow:

Particular Touch Corp ltd.(million)

Carrying value

Automotive Holding group

ltd. (million) Carrying value

Intangible assets 500 500

Fixed assets 1000 2200

Long term investment 250 500

Inventories 300 200

Account receivable 100 50

Total assets 2150 3650

Long-term debt 350 700

Short-term debt 400 500

Accounts payable 200 100

Accrued expenses 450 250

Total liabilities 1450 1550

Net identifiable assets 700 2100

(vii)

In order to calculate the goodwill and gain amount on acquisition, the company will need

to minus the fair value of net identifiable assets from the purchase consideration of the

acquisition. In the case of After pay ltd. the purchase consideration is $1 billion i.e., $1000

million and the fair value of NIA is $900 million so, the goodwill will be $100 million. On the

other hand, the purchase consideration receive by AHS company from AP Eagers are $2300

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

million and fair value of the net identifiable assets is $2200 million so the goodwill is $100

million (Mixon, 2019).

(viii)

The factors that contributed towards the recognition and calculation of goodwill or gain on

bargain purchase are as follow:

A) Consideration transferred by the acquire company to the acquiree company which is

measured predominantly at fair value.

B) The fair value of the net identifiable assets which is recognized at the market price and

make adjustment on the carrying value of the assets and liabilities. This is calculated by

subtracting the total liabilities from the total assets of the company (Rikhardsson and

Yigitbasioglu, 2018).

The goodwill is recognized by A – B

(ix)

In order to calculate the amount of goodwill as a percentage of total consideration paid the

following formula need to be used such as Goodwill/ Total Purchase consideration* 100

In the case of Touch Corp ltd. = $300 million/ $1000 million* 100 = 10%

In the case of AHS ltd. = $100 million/ $2300 million* 100 = 4.35%

This is an amount of goodwill that the paid by the acquire company to the acquiree company

above the fair value of its net identifiable assets. This is basically paid by Afterpay ltd. and AP

Eager ltd. respectively (Bastos, Silva and Poza-Lujan, 2020).

(x)

The percentage of fair value of net identifiable assets to the total consideration paid is

calculated by using the following formula such as Net Identifiable Assets/ Total purchase

consideration*100

In the case of acquisition of Touch Corp ltd. by Afterpay ltd. = 900/1000* 100 = 90 %

And in the case of acquisition of AHS ltd. by AP Eagers ltd. = 2200/2300* 100 = 95.65%

This percentage reflects the amount of fair value of net identifiable assets to the total

consideration paid by the company in this acquisition (Musweu, 2021).

million (Mixon, 2019).

(viii)

The factors that contributed towards the recognition and calculation of goodwill or gain on

bargain purchase are as follow:

A) Consideration transferred by the acquire company to the acquiree company which is

measured predominantly at fair value.

B) The fair value of the net identifiable assets which is recognized at the market price and

make adjustment on the carrying value of the assets and liabilities. This is calculated by

subtracting the total liabilities from the total assets of the company (Rikhardsson and

Yigitbasioglu, 2018).

The goodwill is recognized by A – B

(ix)

In order to calculate the amount of goodwill as a percentage of total consideration paid the

following formula need to be used such as Goodwill/ Total Purchase consideration* 100

In the case of Touch Corp ltd. = $300 million/ $1000 million* 100 = 10%

In the case of AHS ltd. = $100 million/ $2300 million* 100 = 4.35%

This is an amount of goodwill that the paid by the acquire company to the acquiree company

above the fair value of its net identifiable assets. This is basically paid by Afterpay ltd. and AP

Eager ltd. respectively (Bastos, Silva and Poza-Lujan, 2020).

(x)

The percentage of fair value of net identifiable assets to the total consideration paid is

calculated by using the following formula such as Net Identifiable Assets/ Total purchase

consideration*100

In the case of acquisition of Touch Corp ltd. by Afterpay ltd. = 900/1000* 100 = 90 %

And in the case of acquisition of AHS ltd. by AP Eagers ltd. = 2200/2300* 100 = 95.65%

This percentage reflects the amount of fair value of net identifiable assets to the total

consideration paid by the company in this acquisition (Musweu, 2021).

(xi)

From the above two companies’ business combination analysis, it is identified that both the

company have provide equal amount of goodwill to their acquiree company. But the percentage

and amount of goodwill paid by the Afterpay ltd. on the basis of their total consideration was

high as compared to the goodwill paid by AP Eagers ltd. This analysis interpretate that, even if

the companies net assets are low it does not mean that their goodwill will be also low. This also

state that both the company is competitive in their own place but the Touch Crop ltd is more

competitive to Afterpay ltd. That’s why the company paid high amount goodwill because their

goodwill in the market is high (Molon, 2018).

CONCLUSION

This report concludes the two companies’ business combination analysis by using the

various accounting techniques. The report also concludes the goodwill and net identifiable assets

of the acquiree company before the acquisition and also the market price of their assets and

liabilities. This report also states the importance of goodwill at the time of recognising the gain

on bargain purchase. At last, the report analyses that the Afterpay ltd is became more

competitive because they acquire the company whose goodwill in the market is high despite of

asset and profitability.

From the above two companies’ business combination analysis, it is identified that both the

company have provide equal amount of goodwill to their acquiree company. But the percentage

and amount of goodwill paid by the Afterpay ltd. on the basis of their total consideration was

high as compared to the goodwill paid by AP Eagers ltd. This analysis interpretate that, even if

the companies net assets are low it does not mean that their goodwill will be also low. This also

state that both the company is competitive in their own place but the Touch Crop ltd is more

competitive to Afterpay ltd. That’s why the company paid high amount goodwill because their

goodwill in the market is high (Molon, 2018).

CONCLUSION

This report concludes the two companies’ business combination analysis by using the

various accounting techniques. The report also concludes the goodwill and net identifiable assets

of the acquiree company before the acquisition and also the market price of their assets and

liabilities. This report also states the importance of goodwill at the time of recognising the gain

on bargain purchase. At last, the report analyses that the Afterpay ltd is became more

competitive because they acquire the company whose goodwill in the market is high despite of

asset and profitability.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.