Corporate and Financial Accounting: Consolidation Report (HA2032)

VerifiedAdded on 2022/11/23

|11

|3371

|377

Report

AI Summary

This report analyzes the corporate and financial accounting aspects of a company takeover, focusing on the acquisition of FAB Limited by JKY Limited. It explores the differences between consolidation and equity accounting methods, detailing how each method impacts the reporting of income and balance sheets, and referencing AASB standards. The report also examines intra-group transactions, emphasizing the need for elimination adjustments to avoid double-counting and ensure accurate financial statements. Additionally, it discusses the effects of disclosing non-controlling interests in the consolidation process, including the required changes for accurate representation of consolidated financial statements as per AASB 101. The analysis covers goodwill recognition, inventory transactions, and the treatment of unrealized profits within a group context, providing a comprehensive overview of the accounting challenges and solutions in corporate takeovers and financial reporting.

Running head: CORPORATE AND FINANCIAL ACCOUNTING

Corporate and Financial Accounting

Name of the Student

Name of the University

Author’s Note

Corporate and Financial Accounting

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE AND FINANCIAL ACCOUNTING

Executive Summary

The findings of the analysis indicates towards the fact that the companies are needed to

consider different principles of recognition as well as measurement at the time of the

acquisition of smaller companies and this can be seen due to the difference between

the methods of equity accounting and consolidation accounting. The findings of the

report also shows that major differences need to be undertaken for the intra-group

transactions in the same companies’ consolidated financial statements.

Executive Summary

The findings of the analysis indicates towards the fact that the companies are needed to

consider different principles of recognition as well as measurement at the time of the

acquisition of smaller companies and this can be seen due to the difference between

the methods of equity accounting and consolidation accounting. The findings of the

report also shows that major differences need to be undertaken for the intra-group

transactions in the same companies’ consolidated financial statements.

2CORPORATE AND FINANCIAL ACCOUNTING

Table of Contents

Introduction........................................................................................................................3

Part A.................................................................................................................................3

Part B.................................................................................................................................5

Part C.................................................................................................................................6

Conclusion.........................................................................................................................8

References.........................................................................................................................9

Table of Contents

Introduction........................................................................................................................3

Part A.................................................................................................................................3

Part B.................................................................................................................................5

Part C.................................................................................................................................6

Conclusion.........................................................................................................................8

References.........................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE AND FINANCIAL ACCOUNTING

Introduction

The main objective of this report can be found in gaining knowledge of various

accounting substances having relation with the acquisition of FAB Limited by JKY

Limited. Providing the necessary description and other information on the consolidated

accounting method and equity accounting method is the main objective of the report’s

first part. The second part of the report aims at discussing the key principles of intra-

group transactions with the help of proper examples. The last part of the report involves

in discussing the effects of the disclosures connected with the non-controlling interests

in the consolidation process.

Part A

In the process of joint ventures, the use of consolidation and equity methods can

be seen. The nature of reporting the income statement and balance sheet in the

partnership determines the selection of appropriate method which implies that there is

difference in the methodology of these two methods.

Consolidation Method of Accounting

This particular method demands the recording of the joint venture’s assets and

liabilities in the balance sheet as per the proportion of percentage of involvement that

the companies have maintained in the partnership. This particular method indicates

towards the major responsibility of the firms towards recording the acquisition process

related incomes and expenses; after that, the developed financial statements must

include these incomes and expenses. The standards of AASB 110 have provided the

companies with the view on what financial substances need to be taken into

consideration from the financial statements of the parent company and its subsidiary

companies; and these financial elements are assets, income, liabilities, expenses and

others (aasb.gov.au 2019). Both the carrying value of the investments of the parent as

well as its subsidiaries and the part of equity of the subsidiaries that the parent company

holds are eliminated in this method. Moreover, this method involves in elimination

adjustment with the aim to eliminate intercompany transactions so that double counting

of the values can be avoided in consolidation process (Lombrano and Zanin 2013).

It can be seen from the standards of AASB 10 that that it is needed for the

companies to comply with the necessary bases to measure different financial items of

the financial reports and the companies are needed to consider the realized value as

the basis for the income and expenses; and fair value is used for measuring these items

(Milojević, Vukoje and Mihajlović 2013). There is a particular criterion for recognizing the

goodwill as per AASB 10, Paragraph 32. It is required for the management of the

acquirer business organization to take into account the greater condition of below

provided conditions in order to measure and recognize the goodwill:

1st Condition: The aggregate of –

Introduction

The main objective of this report can be found in gaining knowledge of various

accounting substances having relation with the acquisition of FAB Limited by JKY

Limited. Providing the necessary description and other information on the consolidated

accounting method and equity accounting method is the main objective of the report’s

first part. The second part of the report aims at discussing the key principles of intra-

group transactions with the help of proper examples. The last part of the report involves

in discussing the effects of the disclosures connected with the non-controlling interests

in the consolidation process.

Part A

In the process of joint ventures, the use of consolidation and equity methods can

be seen. The nature of reporting the income statement and balance sheet in the

partnership determines the selection of appropriate method which implies that there is

difference in the methodology of these two methods.

Consolidation Method of Accounting

This particular method demands the recording of the joint venture’s assets and

liabilities in the balance sheet as per the proportion of percentage of involvement that

the companies have maintained in the partnership. This particular method indicates

towards the major responsibility of the firms towards recording the acquisition process

related incomes and expenses; after that, the developed financial statements must

include these incomes and expenses. The standards of AASB 110 have provided the

companies with the view on what financial substances need to be taken into

consideration from the financial statements of the parent company and its subsidiary

companies; and these financial elements are assets, income, liabilities, expenses and

others (aasb.gov.au 2019). Both the carrying value of the investments of the parent as

well as its subsidiaries and the part of equity of the subsidiaries that the parent company

holds are eliminated in this method. Moreover, this method involves in elimination

adjustment with the aim to eliminate intercompany transactions so that double counting

of the values can be avoided in consolidation process (Lombrano and Zanin 2013).

It can be seen from the standards of AASB 10 that that it is needed for the

companies to comply with the necessary bases to measure different financial items of

the financial reports and the companies are needed to consider the realized value as

the basis for the income and expenses; and fair value is used for measuring these items

(Milojević, Vukoje and Mihajlović 2013). There is a particular criterion for recognizing the

goodwill as per AASB 10, Paragraph 32. It is required for the management of the

acquirer business organization to take into account the greater condition of below

provided conditions in order to measure and recognize the goodwill:

1st Condition: The aggregate of –

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE AND FINANCIAL ACCOUNTING

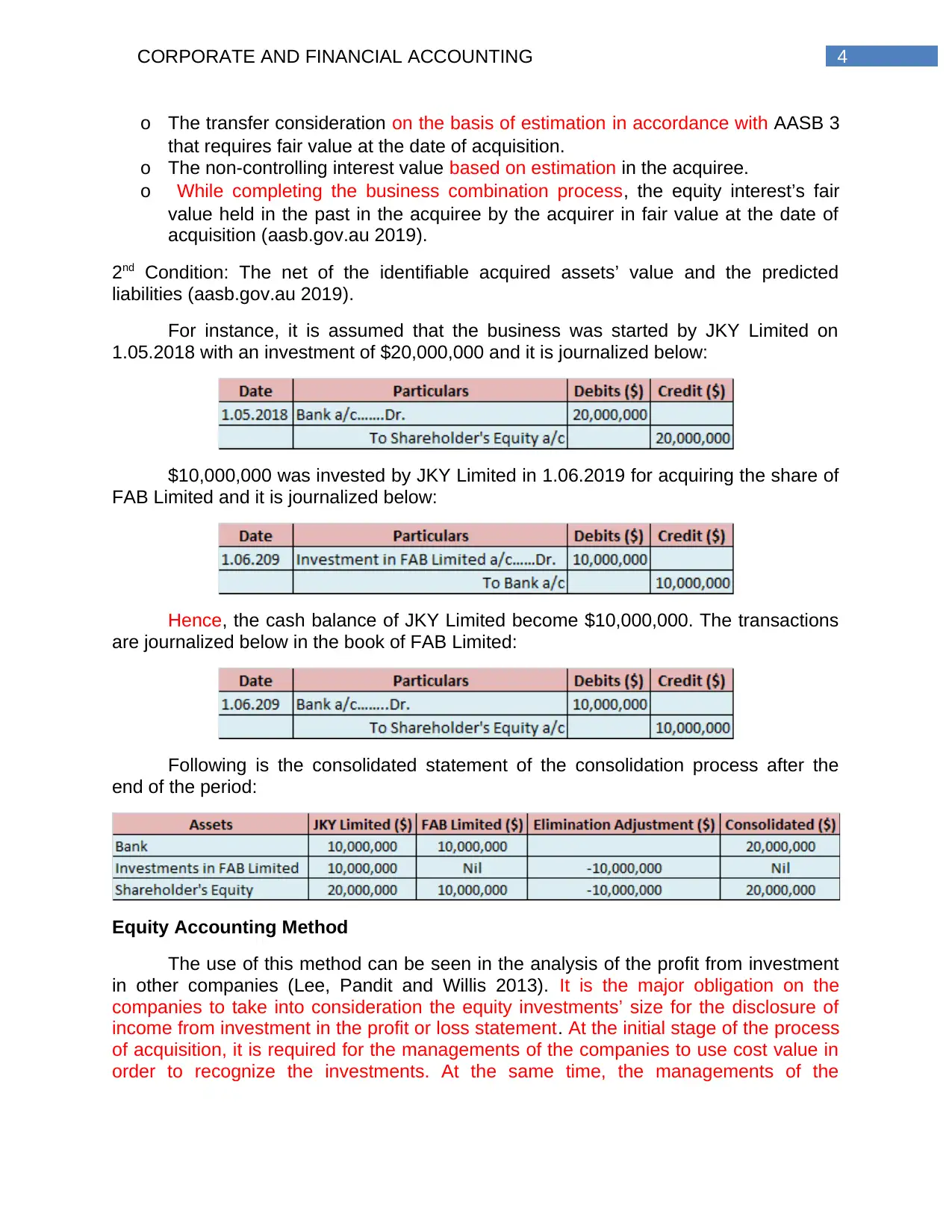

o The transfer consideration on the basis of estimation in accordance with AASB 3

that requires fair value at the date of acquisition.

o The non-controlling interest value based on estimation in the acquiree.

o While completing the business combination process, the equity interest’s fair

value held in the past in the acquiree by the acquirer in fair value at the date of

acquisition (aasb.gov.au 2019).

2nd Condition: The net of the identifiable acquired assets’ value and the predicted

liabilities (aasb.gov.au 2019).

For instance, it is assumed that the business was started by JKY Limited on

1.05.2018 with an investment of $20,000,000 and it is journalized below:

$10,000,000 was invested by JKY Limited in 1.06.2019 for acquiring the share of

FAB Limited and it is journalized below:

Hence, the cash balance of JKY Limited become $10,000,000. The transactions

are journalized below in the book of FAB Limited:

Following is the consolidated statement of the consolidation process after the

end of the period:

Equity Accounting Method

The use of this method can be seen in the analysis of the profit from investment

in other companies (Lee, Pandit and Willis 2013). It is the major obligation on the

companies to take into consideration the equity investments’ size for the disclosure of

income from investment in the profit or loss statement. At the initial stage of the process

of acquisition, it is required for the managements of the companies to use cost value in

order to recognize the investments. At the same time, the managements of the

o The transfer consideration on the basis of estimation in accordance with AASB 3

that requires fair value at the date of acquisition.

o The non-controlling interest value based on estimation in the acquiree.

o While completing the business combination process, the equity interest’s fair

value held in the past in the acquiree by the acquirer in fair value at the date of

acquisition (aasb.gov.au 2019).

2nd Condition: The net of the identifiable acquired assets’ value and the predicted

liabilities (aasb.gov.au 2019).

For instance, it is assumed that the business was started by JKY Limited on

1.05.2018 with an investment of $20,000,000 and it is journalized below:

$10,000,000 was invested by JKY Limited in 1.06.2019 for acquiring the share of

FAB Limited and it is journalized below:

Hence, the cash balance of JKY Limited become $10,000,000. The transactions

are journalized below in the book of FAB Limited:

Following is the consolidated statement of the consolidation process after the

end of the period:

Equity Accounting Method

The use of this method can be seen in the analysis of the profit from investment

in other companies (Lee, Pandit and Willis 2013). It is the major obligation on the

companies to take into consideration the equity investments’ size for the disclosure of

income from investment in the profit or loss statement. At the initial stage of the process

of acquisition, it is required for the managements of the companies to use cost value in

order to recognize the investments. At the same time, the managements of the

5CORPORATE AND FINANCIAL ACCOUNTING

companies are needed to take into account the fair value measurement process for the

recognition of goodwill from acquisition (Grossi et al. 2013).

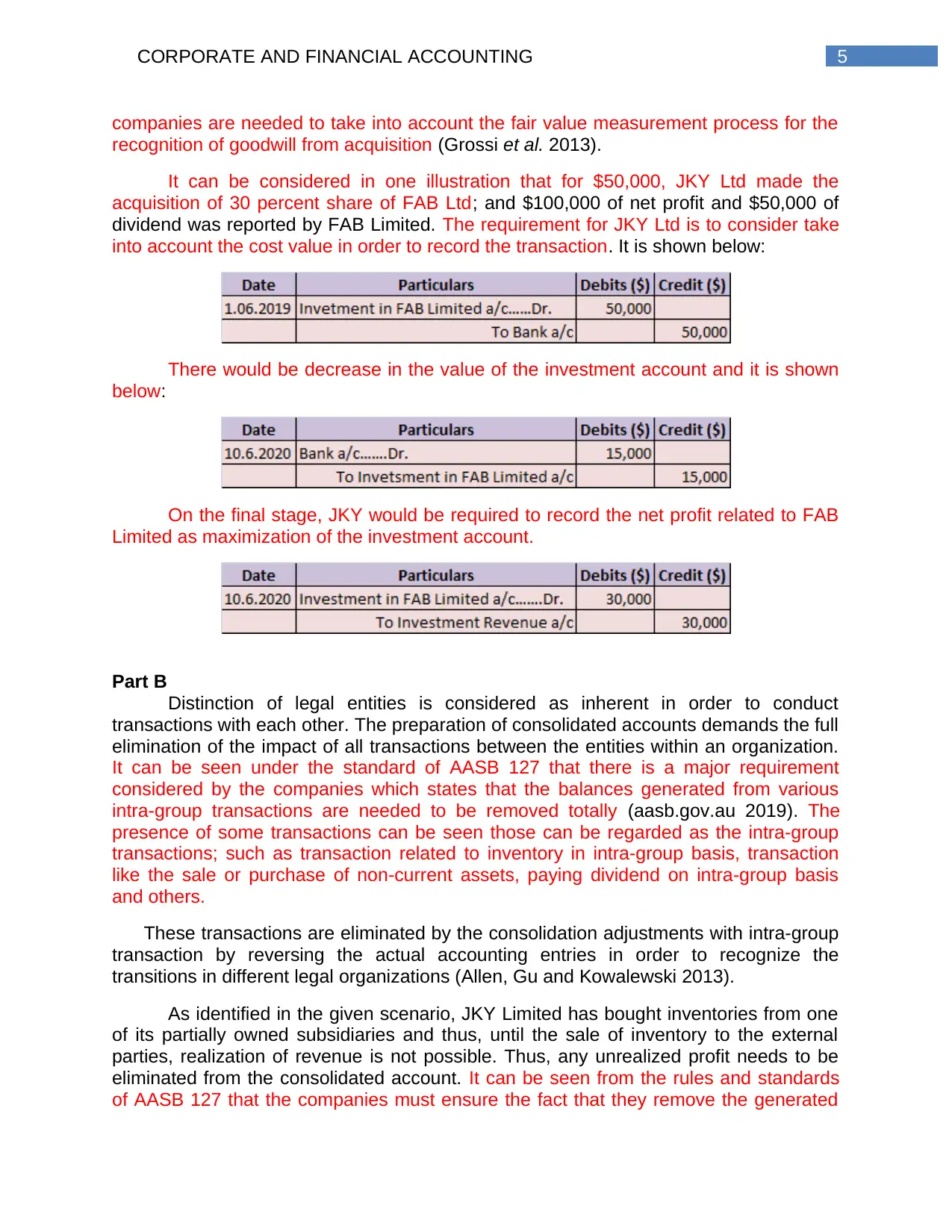

It can be considered in one illustration that for $50,000, JKY Ltd made the

acquisition of 30 percent share of FAB Ltd; and $100,000 of net profit and $50,000 of

dividend was reported by FAB Limited. The requirement for JKY Ltd is to consider take

into account the cost value in order to record the transaction. It is shown below:

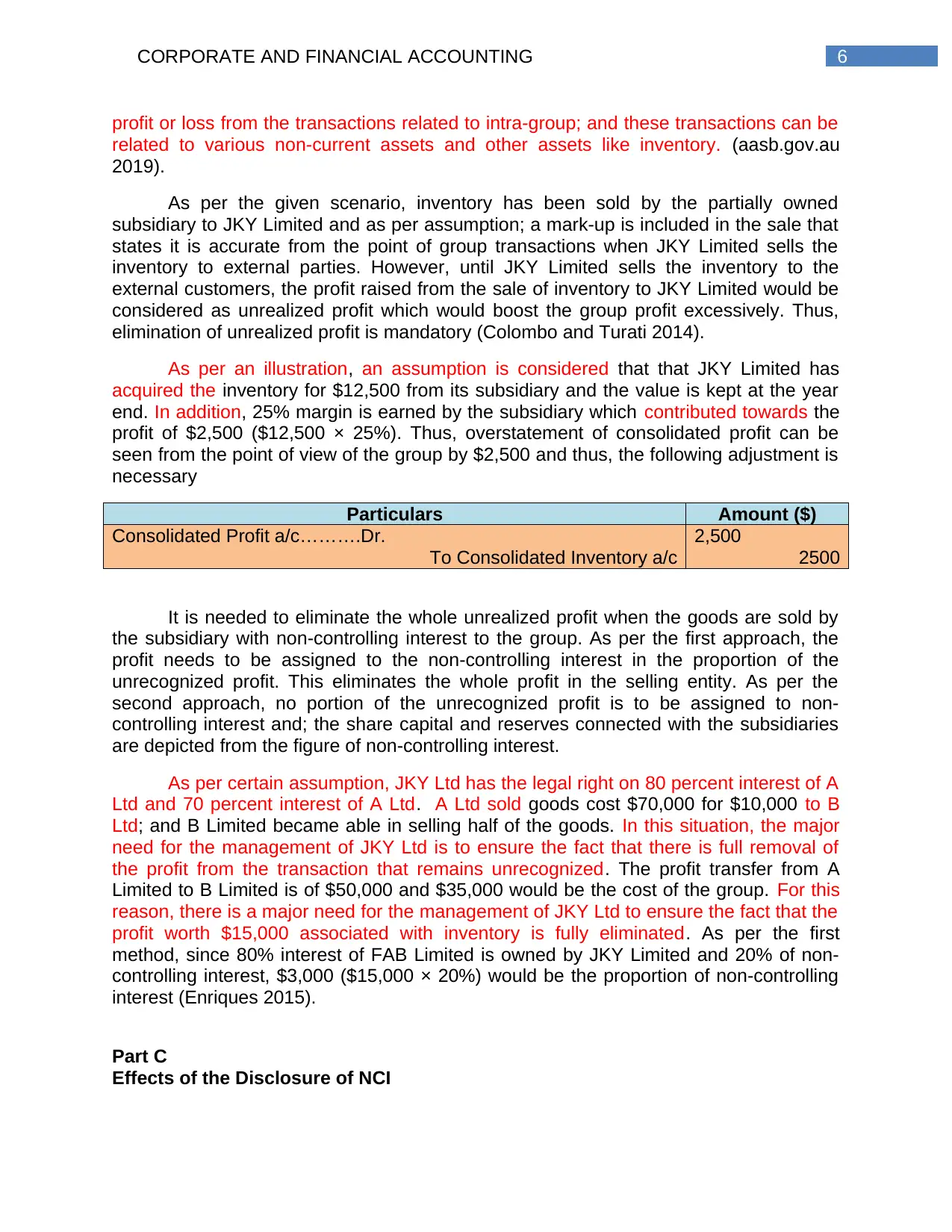

There would be decrease in the value of the investment account and it is shown

below:

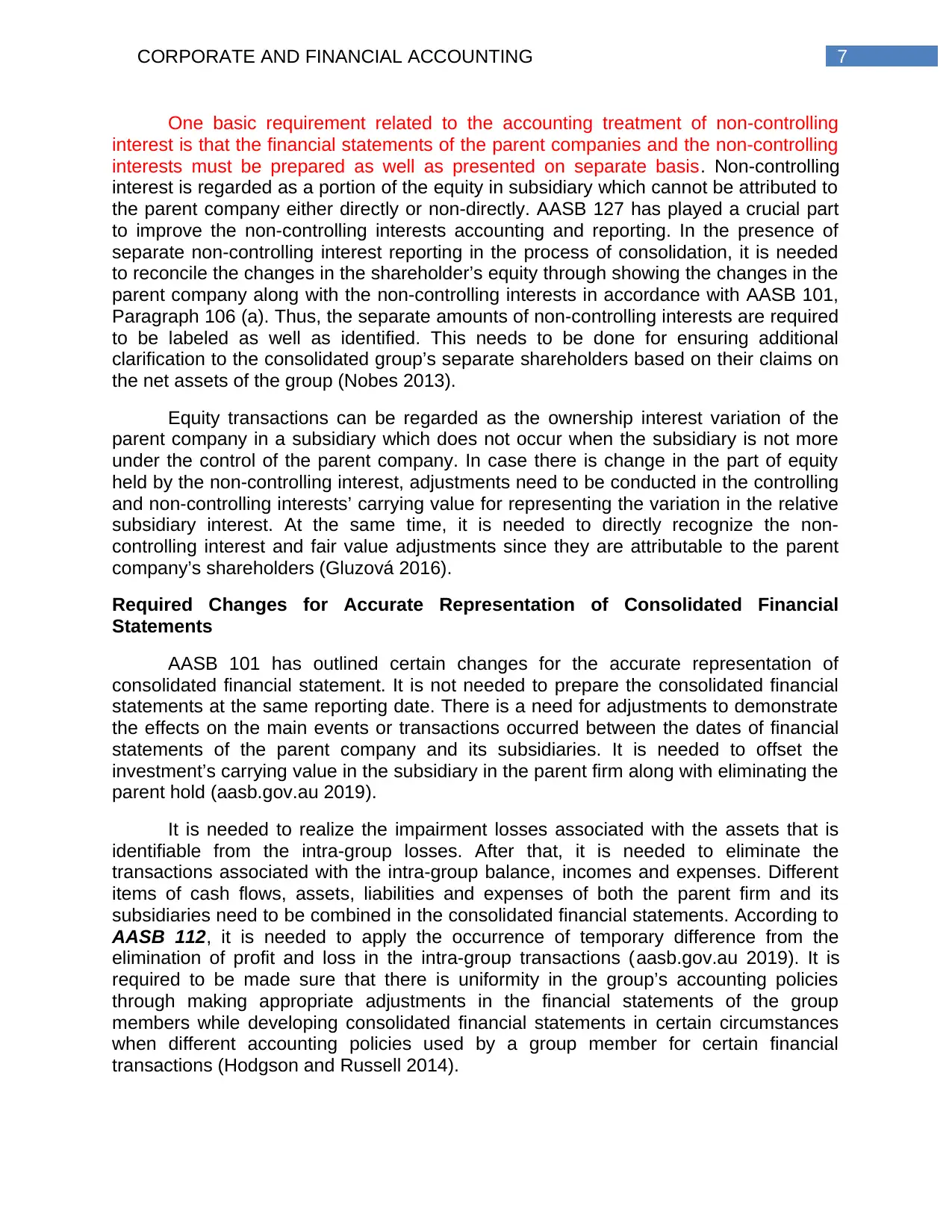

On the final stage, JKY would be required to record the net profit related to FAB

Limited as maximization of the investment account.

Part B

Distinction of legal entities is considered as inherent in order to conduct

transactions with each other. The preparation of consolidated accounts demands the full

elimination of the impact of all transactions between the entities within an organization.

It can be seen under the standard of AASB 127 that there is a major requirement

considered by the companies which states that the balances generated from various

intra-group transactions are needed to be removed totally (aasb.gov.au 2019). The

presence of some transactions can be seen those can be regarded as the intra-group

transactions; such as transaction related to inventory in intra-group basis, transaction

like the sale or purchase of non-current assets, paying dividend on intra-group basis

and others.

These transactions are eliminated by the consolidation adjustments with intra-group

transaction by reversing the actual accounting entries in order to recognize the

transitions in different legal organizations (Allen, Gu and Kowalewski 2013).

As identified in the given scenario, JKY Limited has bought inventories from one

of its partially owned subsidiaries and thus, until the sale of inventory to the external

parties, realization of revenue is not possible. Thus, any unrealized profit needs to be

eliminated from the consolidated account. It can be seen from the rules and standards

of AASB 127 that the companies must ensure the fact that they remove the generated

companies are needed to take into account the fair value measurement process for the

recognition of goodwill from acquisition (Grossi et al. 2013).

It can be considered in one illustration that for $50,000, JKY Ltd made the

acquisition of 30 percent share of FAB Ltd; and $100,000 of net profit and $50,000 of

dividend was reported by FAB Limited. The requirement for JKY Ltd is to consider take

into account the cost value in order to record the transaction. It is shown below:

There would be decrease in the value of the investment account and it is shown

below:

On the final stage, JKY would be required to record the net profit related to FAB

Limited as maximization of the investment account.

Part B

Distinction of legal entities is considered as inherent in order to conduct

transactions with each other. The preparation of consolidated accounts demands the full

elimination of the impact of all transactions between the entities within an organization.

It can be seen under the standard of AASB 127 that there is a major requirement

considered by the companies which states that the balances generated from various

intra-group transactions are needed to be removed totally (aasb.gov.au 2019). The

presence of some transactions can be seen those can be regarded as the intra-group

transactions; such as transaction related to inventory in intra-group basis, transaction

like the sale or purchase of non-current assets, paying dividend on intra-group basis

and others.

These transactions are eliminated by the consolidation adjustments with intra-group

transaction by reversing the actual accounting entries in order to recognize the

transitions in different legal organizations (Allen, Gu and Kowalewski 2013).

As identified in the given scenario, JKY Limited has bought inventories from one

of its partially owned subsidiaries and thus, until the sale of inventory to the external

parties, realization of revenue is not possible. Thus, any unrealized profit needs to be

eliminated from the consolidated account. It can be seen from the rules and standards

of AASB 127 that the companies must ensure the fact that they remove the generated

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE AND FINANCIAL ACCOUNTING

profit or loss from the transactions related to intra-group; and these transactions can be

related to various non-current assets and other assets like inventory. (aasb.gov.au

2019).

As per the given scenario, inventory has been sold by the partially owned

subsidiary to JKY Limited and as per assumption; a mark-up is included in the sale that

states it is accurate from the point of group transactions when JKY Limited sells the

inventory to external parties. However, until JKY Limited sells the inventory to the

external customers, the profit raised from the sale of inventory to JKY Limited would be

considered as unrealized profit which would boost the group profit excessively. Thus,

elimination of unrealized profit is mandatory (Colombo and Turati 2014).

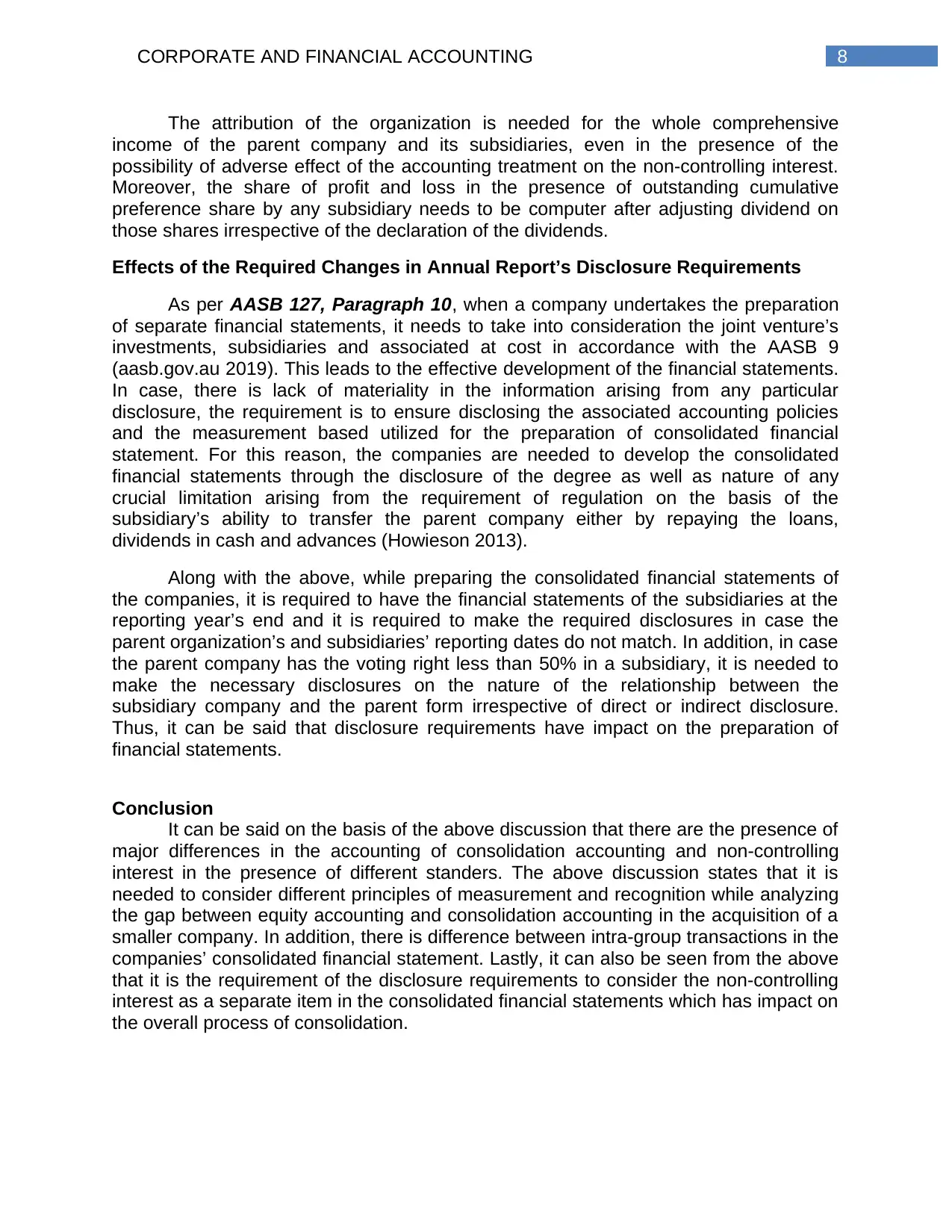

As per an illustration, an assumption is considered that that JKY Limited has

acquired the inventory for $12,500 from its subsidiary and the value is kept at the year

end. In addition, 25% margin is earned by the subsidiary which contributed towards the

profit of $2,500 ($12,500 × 25%). Thus, overstatement of consolidated profit can be

seen from the point of view of the group by $2,500 and thus, the following adjustment is

necessary

Particulars Amount ($)

Consolidated Profit a/c……….Dr.

To Consolidated Inventory a/c

2,500

2500

It is needed to eliminate the whole unrealized profit when the goods are sold by

the subsidiary with non-controlling interest to the group. As per the first approach, the

profit needs to be assigned to the non-controlling interest in the proportion of the

unrecognized profit. This eliminates the whole profit in the selling entity. As per the

second approach, no portion of the unrecognized profit is to be assigned to non-

controlling interest and; the share capital and reserves connected with the subsidiaries

are depicted from the figure of non-controlling interest.

As per certain assumption, JKY Ltd has the legal right on 80 percent interest of A

Ltd and 70 percent interest of A Ltd. A Ltd sold goods cost $70,000 for $10,000 to B

Ltd; and B Limited became able in selling half of the goods. In this situation, the major

need for the management of JKY Ltd is to ensure the fact that there is full removal of

the profit from the transaction that remains unrecognized. The profit transfer from A

Limited to B Limited is of $50,000 and $35,000 would be the cost of the group. For this

reason, there is a major need for the management of JKY Ltd to ensure the fact that the

profit worth $15,000 associated with inventory is fully eliminated. As per the first

method, since 80% interest of FAB Limited is owned by JKY Limited and 20% of non-

controlling interest, $3,000 ($15,000 × 20%) would be the proportion of non-controlling

interest (Enriques 2015).

Part C

Effects of the Disclosure of NCI

profit or loss from the transactions related to intra-group; and these transactions can be

related to various non-current assets and other assets like inventory. (aasb.gov.au

2019).

As per the given scenario, inventory has been sold by the partially owned

subsidiary to JKY Limited and as per assumption; a mark-up is included in the sale that

states it is accurate from the point of group transactions when JKY Limited sells the

inventory to external parties. However, until JKY Limited sells the inventory to the

external customers, the profit raised from the sale of inventory to JKY Limited would be

considered as unrealized profit which would boost the group profit excessively. Thus,

elimination of unrealized profit is mandatory (Colombo and Turati 2014).

As per an illustration, an assumption is considered that that JKY Limited has

acquired the inventory for $12,500 from its subsidiary and the value is kept at the year

end. In addition, 25% margin is earned by the subsidiary which contributed towards the

profit of $2,500 ($12,500 × 25%). Thus, overstatement of consolidated profit can be

seen from the point of view of the group by $2,500 and thus, the following adjustment is

necessary

Particulars Amount ($)

Consolidated Profit a/c……….Dr.

To Consolidated Inventory a/c

2,500

2500

It is needed to eliminate the whole unrealized profit when the goods are sold by

the subsidiary with non-controlling interest to the group. As per the first approach, the

profit needs to be assigned to the non-controlling interest in the proportion of the

unrecognized profit. This eliminates the whole profit in the selling entity. As per the

second approach, no portion of the unrecognized profit is to be assigned to non-

controlling interest and; the share capital and reserves connected with the subsidiaries

are depicted from the figure of non-controlling interest.

As per certain assumption, JKY Ltd has the legal right on 80 percent interest of A

Ltd and 70 percent interest of A Ltd. A Ltd sold goods cost $70,000 for $10,000 to B

Ltd; and B Limited became able in selling half of the goods. In this situation, the major

need for the management of JKY Ltd is to ensure the fact that there is full removal of

the profit from the transaction that remains unrecognized. The profit transfer from A

Limited to B Limited is of $50,000 and $35,000 would be the cost of the group. For this

reason, there is a major need for the management of JKY Ltd to ensure the fact that the

profit worth $15,000 associated with inventory is fully eliminated. As per the first

method, since 80% interest of FAB Limited is owned by JKY Limited and 20% of non-

controlling interest, $3,000 ($15,000 × 20%) would be the proportion of non-controlling

interest (Enriques 2015).

Part C

Effects of the Disclosure of NCI

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE AND FINANCIAL ACCOUNTING

One basic requirement related to the accounting treatment of non-controlling

interest is that the financial statements of the parent companies and the non-controlling

interests must be prepared as well as presented on separate basis. Non-controlling

interest is regarded as a portion of the equity in subsidiary which cannot be attributed to

the parent company either directly or non-directly. AASB 127 has played a crucial part

to improve the non-controlling interests accounting and reporting. In the presence of

separate non-controlling interest reporting in the process of consolidation, it is needed

to reconcile the changes in the shareholder’s equity through showing the changes in the

parent company along with the non-controlling interests in accordance with AASB 101,

Paragraph 106 (a). Thus, the separate amounts of non-controlling interests are required

to be labeled as well as identified. This needs to be done for ensuring additional

clarification to the consolidated group’s separate shareholders based on their claims on

the net assets of the group (Nobes 2013).

Equity transactions can be regarded as the ownership interest variation of the

parent company in a subsidiary which does not occur when the subsidiary is not more

under the control of the parent company. In case there is change in the part of equity

held by the non-controlling interest, adjustments need to be conducted in the controlling

and non-controlling interests’ carrying value for representing the variation in the relative

subsidiary interest. At the same time, it is needed to directly recognize the non-

controlling interest and fair value adjustments since they are attributable to the parent

company’s shareholders (Gluzová 2016).

Required Changes for Accurate Representation of Consolidated Financial

Statements

AASB 101 has outlined certain changes for the accurate representation of

consolidated financial statement. It is not needed to prepare the consolidated financial

statements at the same reporting date. There is a need for adjustments to demonstrate

the effects on the main events or transactions occurred between the dates of financial

statements of the parent company and its subsidiaries. It is needed to offset the

investment’s carrying value in the subsidiary in the parent firm along with eliminating the

parent hold (aasb.gov.au 2019).

It is needed to realize the impairment losses associated with the assets that is

identifiable from the intra-group losses. After that, it is needed to eliminate the

transactions associated with the intra-group balance, incomes and expenses. Different

items of cash flows, assets, liabilities and expenses of both the parent firm and its

subsidiaries need to be combined in the consolidated financial statements. According to

AASB 112, it is needed to apply the occurrence of temporary difference from the

elimination of profit and loss in the intra-group transactions (aasb.gov.au 2019). It is

required to be made sure that there is uniformity in the group’s accounting policies

through making appropriate adjustments in the financial statements of the group

members while developing consolidated financial statements in certain circumstances

when different accounting policies used by a group member for certain financial

transactions (Hodgson and Russell 2014).

One basic requirement related to the accounting treatment of non-controlling

interest is that the financial statements of the parent companies and the non-controlling

interests must be prepared as well as presented on separate basis. Non-controlling

interest is regarded as a portion of the equity in subsidiary which cannot be attributed to

the parent company either directly or non-directly. AASB 127 has played a crucial part

to improve the non-controlling interests accounting and reporting. In the presence of

separate non-controlling interest reporting in the process of consolidation, it is needed

to reconcile the changes in the shareholder’s equity through showing the changes in the

parent company along with the non-controlling interests in accordance with AASB 101,

Paragraph 106 (a). Thus, the separate amounts of non-controlling interests are required

to be labeled as well as identified. This needs to be done for ensuring additional

clarification to the consolidated group’s separate shareholders based on their claims on

the net assets of the group (Nobes 2013).

Equity transactions can be regarded as the ownership interest variation of the

parent company in a subsidiary which does not occur when the subsidiary is not more

under the control of the parent company. In case there is change in the part of equity

held by the non-controlling interest, adjustments need to be conducted in the controlling

and non-controlling interests’ carrying value for representing the variation in the relative

subsidiary interest. At the same time, it is needed to directly recognize the non-

controlling interest and fair value adjustments since they are attributable to the parent

company’s shareholders (Gluzová 2016).

Required Changes for Accurate Representation of Consolidated Financial

Statements

AASB 101 has outlined certain changes for the accurate representation of

consolidated financial statement. It is not needed to prepare the consolidated financial

statements at the same reporting date. There is a need for adjustments to demonstrate

the effects on the main events or transactions occurred between the dates of financial

statements of the parent company and its subsidiaries. It is needed to offset the

investment’s carrying value in the subsidiary in the parent firm along with eliminating the

parent hold (aasb.gov.au 2019).

It is needed to realize the impairment losses associated with the assets that is

identifiable from the intra-group losses. After that, it is needed to eliminate the

transactions associated with the intra-group balance, incomes and expenses. Different

items of cash flows, assets, liabilities and expenses of both the parent firm and its

subsidiaries need to be combined in the consolidated financial statements. According to

AASB 112, it is needed to apply the occurrence of temporary difference from the

elimination of profit and loss in the intra-group transactions (aasb.gov.au 2019). It is

required to be made sure that there is uniformity in the group’s accounting policies

through making appropriate adjustments in the financial statements of the group

members while developing consolidated financial statements in certain circumstances

when different accounting policies used by a group member for certain financial

transactions (Hodgson and Russell 2014).

8CORPORATE AND FINANCIAL ACCOUNTING

The attribution of the organization is needed for the whole comprehensive

income of the parent company and its subsidiaries, even in the presence of the

possibility of adverse effect of the accounting treatment on the non-controlling interest.

Moreover, the share of profit and loss in the presence of outstanding cumulative

preference share by any subsidiary needs to be computer after adjusting dividend on

those shares irrespective of the declaration of the dividends.

Effects of the Required Changes in Annual Report’s Disclosure Requirements

As per AASB 127, Paragraph 10, when a company undertakes the preparation

of separate financial statements, it needs to take into consideration the joint venture’s

investments, subsidiaries and associated at cost in accordance with the AASB 9

(aasb.gov.au 2019). This leads to the effective development of the financial statements.

In case, there is lack of materiality in the information arising from any particular

disclosure, the requirement is to ensure disclosing the associated accounting policies

and the measurement based utilized for the preparation of consolidated financial

statement. For this reason, the companies are needed to develop the consolidated

financial statements through the disclosure of the degree as well as nature of any

crucial limitation arising from the requirement of regulation on the basis of the

subsidiary’s ability to transfer the parent company either by repaying the loans,

dividends in cash and advances (Howieson 2013).

Along with the above, while preparing the consolidated financial statements of

the companies, it is required to have the financial statements of the subsidiaries at the

reporting year’s end and it is required to make the required disclosures in case the

parent organization’s and subsidiaries’ reporting dates do not match. In addition, in case

the parent company has the voting right less than 50% in a subsidiary, it is needed to

make the necessary disclosures on the nature of the relationship between the

subsidiary company and the parent form irrespective of direct or indirect disclosure.

Thus, it can be said that disclosure requirements have impact on the preparation of

financial statements.

Conclusion

It can be said on the basis of the above discussion that there are the presence of

major differences in the accounting of consolidation accounting and non-controlling

interest in the presence of different standers. The above discussion states that it is

needed to consider different principles of measurement and recognition while analyzing

the gap between equity accounting and consolidation accounting in the acquisition of a

smaller company. In addition, there is difference between intra-group transactions in the

companies’ consolidated financial statement. Lastly, it can also be seen from the above

that it is the requirement of the disclosure requirements to consider the non-controlling

interest as a separate item in the consolidated financial statements which has impact on

the overall process of consolidation.

The attribution of the organization is needed for the whole comprehensive

income of the parent company and its subsidiaries, even in the presence of the

possibility of adverse effect of the accounting treatment on the non-controlling interest.

Moreover, the share of profit and loss in the presence of outstanding cumulative

preference share by any subsidiary needs to be computer after adjusting dividend on

those shares irrespective of the declaration of the dividends.

Effects of the Required Changes in Annual Report’s Disclosure Requirements

As per AASB 127, Paragraph 10, when a company undertakes the preparation

of separate financial statements, it needs to take into consideration the joint venture’s

investments, subsidiaries and associated at cost in accordance with the AASB 9

(aasb.gov.au 2019). This leads to the effective development of the financial statements.

In case, there is lack of materiality in the information arising from any particular

disclosure, the requirement is to ensure disclosing the associated accounting policies

and the measurement based utilized for the preparation of consolidated financial

statement. For this reason, the companies are needed to develop the consolidated

financial statements through the disclosure of the degree as well as nature of any

crucial limitation arising from the requirement of regulation on the basis of the

subsidiary’s ability to transfer the parent company either by repaying the loans,

dividends in cash and advances (Howieson 2013).

Along with the above, while preparing the consolidated financial statements of

the companies, it is required to have the financial statements of the subsidiaries at the

reporting year’s end and it is required to make the required disclosures in case the

parent organization’s and subsidiaries’ reporting dates do not match. In addition, in case

the parent company has the voting right less than 50% in a subsidiary, it is needed to

make the necessary disclosures on the nature of the relationship between the

subsidiary company and the parent form irrespective of direct or indirect disclosure.

Thus, it can be said that disclosure requirements have impact on the preparation of

financial statements.

Conclusion

It can be said on the basis of the above discussion that there are the presence of

major differences in the accounting of consolidation accounting and non-controlling

interest in the presence of different standers. The above discussion states that it is

needed to consider different principles of measurement and recognition while analyzing

the gap between equity accounting and consolidation accounting in the acquisition of a

smaller company. In addition, there is difference between intra-group transactions in the

companies’ consolidated financial statement. Lastly, it can also be seen from the above

that it is the requirement of the disclosure requirements to consider the non-controlling

interest as a separate item in the consolidated financial statements which has impact on

the overall process of consolidation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE AND FINANCIAL ACCOUNTING

References

Aasb.gov.au., 2019. Business Combinations. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15.pdf [Accessed 26 May

2019].

Aasb.gov.au., 2019. Consolidated Financial Statements. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB10_08-11.pdf [Accessed 26

May 2019].

Aasb.gov.au., 2019. Investments in Associates and Joint Ventures. [online] Available

at: https://www.aasb.gov.au/admin/file/content105/c9/AASB128_08-11.pdf [Accessed

26 May 2019].

Aasb.gov.au., 2019. Presentation of Financial Statements. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf [Accessed 26

May 2019].

Aasb.gov.au., 2019. Separate Financial Statements. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB127_08-11_COMPjan15_07-

15.pdf [Accessed 26 May 2019].

Allen, F., Gu, X. and Kowalewski, O., 2013. Corporate governance and intra-group

transactions in European bank holding companies during the crisis. In Global Banking,

Financial Markets and Crises (pp. 365-431). Emerald Group Publishing Limited.

Colombo, L.V. and Turati, G., 2014. Why do acquiring banks in mergers concentrate in

well-developed areas? Regional development and mergers and acquisitions (M&As) in

banking. Regional Studies, 48(2), pp.363-381.

Enriques, L., 2015. Related party transactions: Policy options and real-world challenges

(with a critique of the European Commission proposal). European Business

Organization Law Review, 16(1), pp.1-37.

Gluzová, T., 2016. Disclosure of subsidiaries with non-controlling interest in accordance

with IFRS 12: case of materiality. Acta Universitatis Agriculturae et Silviculturae

Mendelianae Brunensis, 64(1), pp.275-281.

Hanlon, D., Navissi, F. and Soepriyanto, G., 2014. The value relevance of deferred tax

attributed to asset revaluations. Journal of Contemporary Accounting &

Economics, 10(2), pp.87-99.

Hodgson, A. and Russell, M., 2014. Comprehending comprehensive income. Australian

Accounting Review, 24(2), pp.100-110.

Howieson, B., 2013. Defining the Reporting Entity in the Not‐for‐Profit Public Sector:

Implementation Issues Associated with the Control Test. Australian Accounting

Review, 23(1), pp.29-42.

References

Aasb.gov.au., 2019. Business Combinations. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15.pdf [Accessed 26 May

2019].

Aasb.gov.au., 2019. Consolidated Financial Statements. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB10_08-11.pdf [Accessed 26

May 2019].

Aasb.gov.au., 2019. Investments in Associates and Joint Ventures. [online] Available

at: https://www.aasb.gov.au/admin/file/content105/c9/AASB128_08-11.pdf [Accessed

26 May 2019].

Aasb.gov.au., 2019. Presentation of Financial Statements. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf [Accessed 26

May 2019].

Aasb.gov.au., 2019. Separate Financial Statements. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB127_08-11_COMPjan15_07-

15.pdf [Accessed 26 May 2019].

Allen, F., Gu, X. and Kowalewski, O., 2013. Corporate governance and intra-group

transactions in European bank holding companies during the crisis. In Global Banking,

Financial Markets and Crises (pp. 365-431). Emerald Group Publishing Limited.

Colombo, L.V. and Turati, G., 2014. Why do acquiring banks in mergers concentrate in

well-developed areas? Regional development and mergers and acquisitions (M&As) in

banking. Regional Studies, 48(2), pp.363-381.

Enriques, L., 2015. Related party transactions: Policy options and real-world challenges

(with a critique of the European Commission proposal). European Business

Organization Law Review, 16(1), pp.1-37.

Gluzová, T., 2016. Disclosure of subsidiaries with non-controlling interest in accordance

with IFRS 12: case of materiality. Acta Universitatis Agriculturae et Silviculturae

Mendelianae Brunensis, 64(1), pp.275-281.

Hanlon, D., Navissi, F. and Soepriyanto, G., 2014. The value relevance of deferred tax

attributed to asset revaluations. Journal of Contemporary Accounting &

Economics, 10(2), pp.87-99.

Hodgson, A. and Russell, M., 2014. Comprehending comprehensive income. Australian

Accounting Review, 24(2), pp.100-110.

Howieson, B., 2013. Defining the Reporting Entity in the Not‐for‐Profit Public Sector:

Implementation Issues Associated with the Control Test. Australian Accounting

Review, 23(1), pp.29-42.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE AND FINANCIAL ACCOUNTING

Lee, S., Pandit, S. and Willis, R.H., 2013. Equity method investments and sell-side

analysts' information environment. The Accounting Review, 88(6), pp.2089-2115.

Lombrano, A. and Zanin, L., 2013. IPSAS and local government consolidated financial

statements—proposal for a territorial consolidation method. Public Money &

Management, 33(6), pp.429-436.

Milojević, I., Vukoje, A. and Mihajlović, M., 2013. Accounting consolidation of the

balance by the acquisition method. Economics of Agriculture, 60(297-2016-3534),

p.237.

Nobes, C., 2013. The continued survival of international differences under

IFRS. Accounting and Business Research, 43(2), pp.83-111.

Lee, S., Pandit, S. and Willis, R.H., 2013. Equity method investments and sell-side

analysts' information environment. The Accounting Review, 88(6), pp.2089-2115.

Lombrano, A. and Zanin, L., 2013. IPSAS and local government consolidated financial

statements—proposal for a territorial consolidation method. Public Money &

Management, 33(6), pp.429-436.

Milojević, I., Vukoje, A. and Mihajlović, M., 2013. Accounting consolidation of the

balance by the acquisition method. Economics of Agriculture, 60(297-2016-3534),

p.237.

Nobes, C., 2013. The continued survival of international differences under

IFRS. Accounting and Business Research, 43(2), pp.83-111.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.