Holmes Institute HA2032: Corporate Accounting Funding Sources Report

VerifiedAdded on 2022/10/17

|10

|2694

|207

Report

AI Summary

This report delves into the realm of corporate and financial accounting, presenting an analysis of company funding sources, with a specific focus on the equity and liability sections of financial statements. The report examines two ASX-listed companies, Aurizon Holding Limited and Blue Scope Steel Limited, comparing their financial performance over a three-year period. It explores the significance of contributed equity, reserves, and retained earnings within the equity section, as well as trade payables, borrowing, and other liabilities. Furthermore, the report provides a comparative analysis of the companies' financial health and funding strategies, including the use of debt and equity. The report also differentiates between small and large proprietary companies, discussing their characteristics and regulatory requirements, and defines the concept of a reporting entity, emphasizing its role in providing accurate financial information to stakeholders. The analysis includes the importance of corporate accounting in business activities, the process companies use to carry their accounting information in their financial reports, and the implications of choosing various forms of business organization.

Running head: CORPORATE AND FINANCIAL ACCOUNTING

CORPORATE AND FINANCIAL ACCOUNTING

Name of the Student

Name of the University

Author Note

CORPORATE AND FINANCIAL ACCOUNTING

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CORPORATE AND FINANCIAL ACCOUNTING

Executive Summary

The report shows the importance of corporate accounting in business activities. It

also states about the process that company used to carry their accounting

information in their financial report. The report based upon two companies that have

been listed in Australian Security Exchange and show the equity and liability aspect

of the business unit. Lastly, it shows about different form of business organisation

and the implication of choosing any one of the forms of business.

CORPORATE AND FINANCIAL ACCOUNTING

Executive Summary

The report shows the importance of corporate accounting in business activities. It

also states about the process that company used to carry their accounting

information in their financial report. The report based upon two companies that have

been listed in Australian Security Exchange and show the equity and liability aspect

of the business unit. Lastly, it shows about different form of business organisation

and the implication of choosing any one of the forms of business.

2

CORPORATE AND FINANCIAL ACCOUNTING

Table of Contents

Introduction...................................................................................................................4

PART A.........................................................................................................................4

Overview of the Companies......................................................................................4

Equity Section in Companies Financial Statement...................................................4

Liability Section in Companies Financial Statement.................................................7

Source of fund.........................................................................................................11

Part B..........................................................................................................................11

Small Proprietary Company....................................................................................11

Large Proprietary Company....................................................................................12

Reporting Entity.......................................................................................................12

Conclusion..................................................................................................................13

Reference...................................................................................................................14

CORPORATE AND FINANCIAL ACCOUNTING

Table of Contents

Introduction...................................................................................................................4

PART A.........................................................................................................................4

Overview of the Companies......................................................................................4

Equity Section in Companies Financial Statement...................................................4

Liability Section in Companies Financial Statement.................................................7

Source of fund.........................................................................................................11

Part B..........................................................................................................................11

Small Proprietary Company....................................................................................11

Large Proprietary Company....................................................................................12

Reporting Entity.......................................................................................................12

Conclusion..................................................................................................................13

Reference...................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CORPORATE AND FINANCIAL ACCOUNTING

Introduction

Corporate Accounting is a method of accounting which prepare the cash flow

statement and final account for different companies (Agrawal and Cooper 2017). It

also assists in the analysis of the company financial information in case of merger

and acquisition process as in this the valuation of company is necessary so

corporate accounting helps the manager to value their company financial report.

Accounting for both Private and Public can be done with the help of this accounting

method (Atanasov and Black 2016). The report is based upon two ASX limited

company and shows their equity and liability section and how the company can fund

its business activities. It also states the position of the company in the industry and

whether the company is financially stable or not.

PART A

Overview of the Companies

The report is based upon two companies as Aurizon Holding Limited and Blue

Scope Steel Limited. Aurizon Holding Limited is a rail-based company which is

owned by Government of Queensland and it having it headquarter in Brisbane,

Australia. Blue Scope Steel Limited is a steel manufacturing company which produce

steel from the resources that are available from North America, New Zealand and

Asia. The company was founded in 2002 and having it headquarter in Melbourne,

Victoria Australia.

Equity Section in Companies Financial Statement

The items that listed in both company equity section has been shown below:

Aurizon Holding Limited

2018 2017 2016

Contributed Equity Contributed Equity Contributed Equity

Reserves Reserves Reserves

Retained Earnings Retained Earnings Retained Earnings

Contributed Equity - These signify the amount of cash which the entity gets from

shareholders in exchange of stock (Domino, Wingreen and Blanton 2015). It means

the price which the shareholders pay to get the ownership of the company.

Reserves – Company keep aside some part of its earning in the business as it can

help them in an emergency, that amount which company keep aside termed as

reserves. This amount helps the company in case of any uncertain event had

occurred in the business or case slum situation.

Retained Earnings – It is the amount of profit which entity has earned which is less

of any payment made to the investors (Ermakova et al., 2015). These show the

financial health of the organization as if the company has high retained earnings than

it signifies company is earning good by carrying the business activities.

Blue Scope Steel Limited

2018 2017 2016

Contributed Equity Contributed Equity Contributed Equity

Reserves Reserves Reserves

CORPORATE AND FINANCIAL ACCOUNTING

Introduction

Corporate Accounting is a method of accounting which prepare the cash flow

statement and final account for different companies (Agrawal and Cooper 2017). It

also assists in the analysis of the company financial information in case of merger

and acquisition process as in this the valuation of company is necessary so

corporate accounting helps the manager to value their company financial report.

Accounting for both Private and Public can be done with the help of this accounting

method (Atanasov and Black 2016). The report is based upon two ASX limited

company and shows their equity and liability section and how the company can fund

its business activities. It also states the position of the company in the industry and

whether the company is financially stable or not.

PART A

Overview of the Companies

The report is based upon two companies as Aurizon Holding Limited and Blue

Scope Steel Limited. Aurizon Holding Limited is a rail-based company which is

owned by Government of Queensland and it having it headquarter in Brisbane,

Australia. Blue Scope Steel Limited is a steel manufacturing company which produce

steel from the resources that are available from North America, New Zealand and

Asia. The company was founded in 2002 and having it headquarter in Melbourne,

Victoria Australia.

Equity Section in Companies Financial Statement

The items that listed in both company equity section has been shown below:

Aurizon Holding Limited

2018 2017 2016

Contributed Equity Contributed Equity Contributed Equity

Reserves Reserves Reserves

Retained Earnings Retained Earnings Retained Earnings

Contributed Equity - These signify the amount of cash which the entity gets from

shareholders in exchange of stock (Domino, Wingreen and Blanton 2015). It means

the price which the shareholders pay to get the ownership of the company.

Reserves – Company keep aside some part of its earning in the business as it can

help them in an emergency, that amount which company keep aside termed as

reserves. This amount helps the company in case of any uncertain event had

occurred in the business or case slum situation.

Retained Earnings – It is the amount of profit which entity has earned which is less

of any payment made to the investors (Ermakova et al., 2015). These show the

financial health of the organization as if the company has high retained earnings than

it signifies company is earning good by carrying the business activities.

Blue Scope Steel Limited

2018 2017 2016

Contributed Equity Contributed Equity Contributed Equity

Reserves Reserves Reserves

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CORPORATE AND FINANCIAL ACCOUNTING

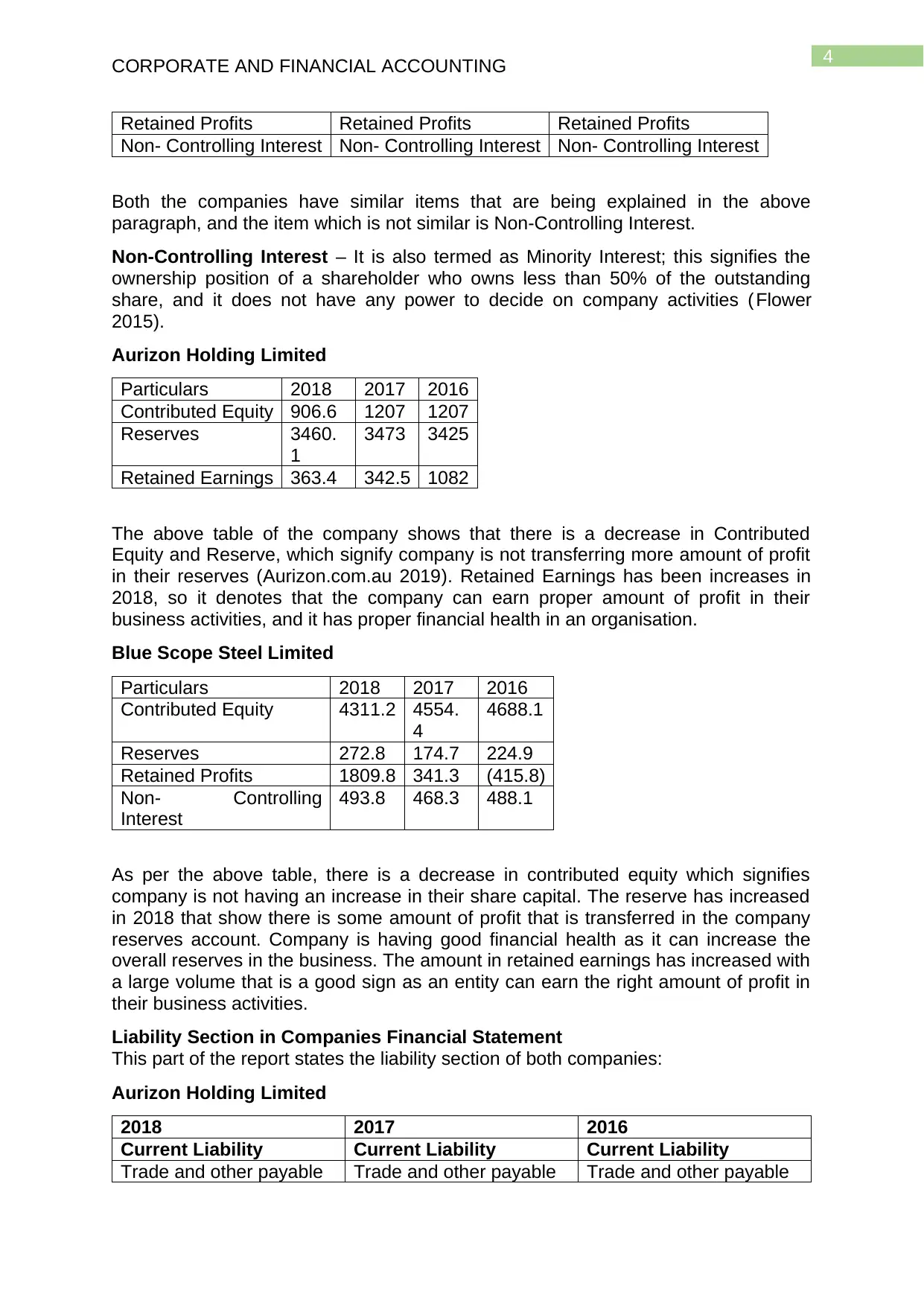

Retained Profits Retained Profits Retained Profits

Non- Controlling Interest Non- Controlling Interest Non- Controlling Interest

Both the companies have similar items that are being explained in the above

paragraph, and the item which is not similar is Non-Controlling Interest.

Non-Controlling Interest – It is also termed as Minority Interest; this signifies the

ownership position of a shareholder who owns less than 50% of the outstanding

share, and it does not have any power to decide on company activities ( Flower

2015).

Aurizon Holding Limited

Particulars 2018 2017 2016

Contributed Equity 906.6 1207 1207

Reserves 3460.

1

3473 3425

Retained Earnings 363.4 342.5 1082

The above table of the company shows that there is a decrease in Contributed

Equity and Reserve, which signify company is not transferring more amount of profit

in their reserves (Aurizon.com.au 2019). Retained Earnings has been increases in

2018, so it denotes that the company can earn proper amount of profit in their

business activities, and it has proper financial health in an organisation.

Blue Scope Steel Limited

Particulars 2018 2017 2016

Contributed Equity 4311.2 4554.

4

4688.1

Reserves 272.8 174.7 224.9

Retained Profits 1809.8 341.3 (415.8)

Non- Controlling

Interest

493.8 468.3 488.1

As per the above table, there is a decrease in contributed equity which signifies

company is not having an increase in their share capital. The reserve has increased

in 2018 that show there is some amount of profit that is transferred in the company

reserves account. Company is having good financial health as it can increase the

overall reserves in the business. The amount in retained earnings has increased with

a large volume that is a good sign as an entity can earn the right amount of profit in

their business activities.

Liability Section in Companies Financial Statement

This part of the report states the liability section of both companies:

Aurizon Holding Limited

2018 2017 2016

Current Liability Current Liability Current Liability

Trade and other payable Trade and other payable Trade and other payable

CORPORATE AND FINANCIAL ACCOUNTING

Retained Profits Retained Profits Retained Profits

Non- Controlling Interest Non- Controlling Interest Non- Controlling Interest

Both the companies have similar items that are being explained in the above

paragraph, and the item which is not similar is Non-Controlling Interest.

Non-Controlling Interest – It is also termed as Minority Interest; this signifies the

ownership position of a shareholder who owns less than 50% of the outstanding

share, and it does not have any power to decide on company activities ( Flower

2015).

Aurizon Holding Limited

Particulars 2018 2017 2016

Contributed Equity 906.6 1207 1207

Reserves 3460.

1

3473 3425

Retained Earnings 363.4 342.5 1082

The above table of the company shows that there is a decrease in Contributed

Equity and Reserve, which signify company is not transferring more amount of profit

in their reserves (Aurizon.com.au 2019). Retained Earnings has been increases in

2018, so it denotes that the company can earn proper amount of profit in their

business activities, and it has proper financial health in an organisation.

Blue Scope Steel Limited

Particulars 2018 2017 2016

Contributed Equity 4311.2 4554.

4

4688.1

Reserves 272.8 174.7 224.9

Retained Profits 1809.8 341.3 (415.8)

Non- Controlling

Interest

493.8 468.3 488.1

As per the above table, there is a decrease in contributed equity which signifies

company is not having an increase in their share capital. The reserve has increased

in 2018 that show there is some amount of profit that is transferred in the company

reserves account. Company is having good financial health as it can increase the

overall reserves in the business. The amount in retained earnings has increased with

a large volume that is a good sign as an entity can earn the right amount of profit in

their business activities.

Liability Section in Companies Financial Statement

This part of the report states the liability section of both companies:

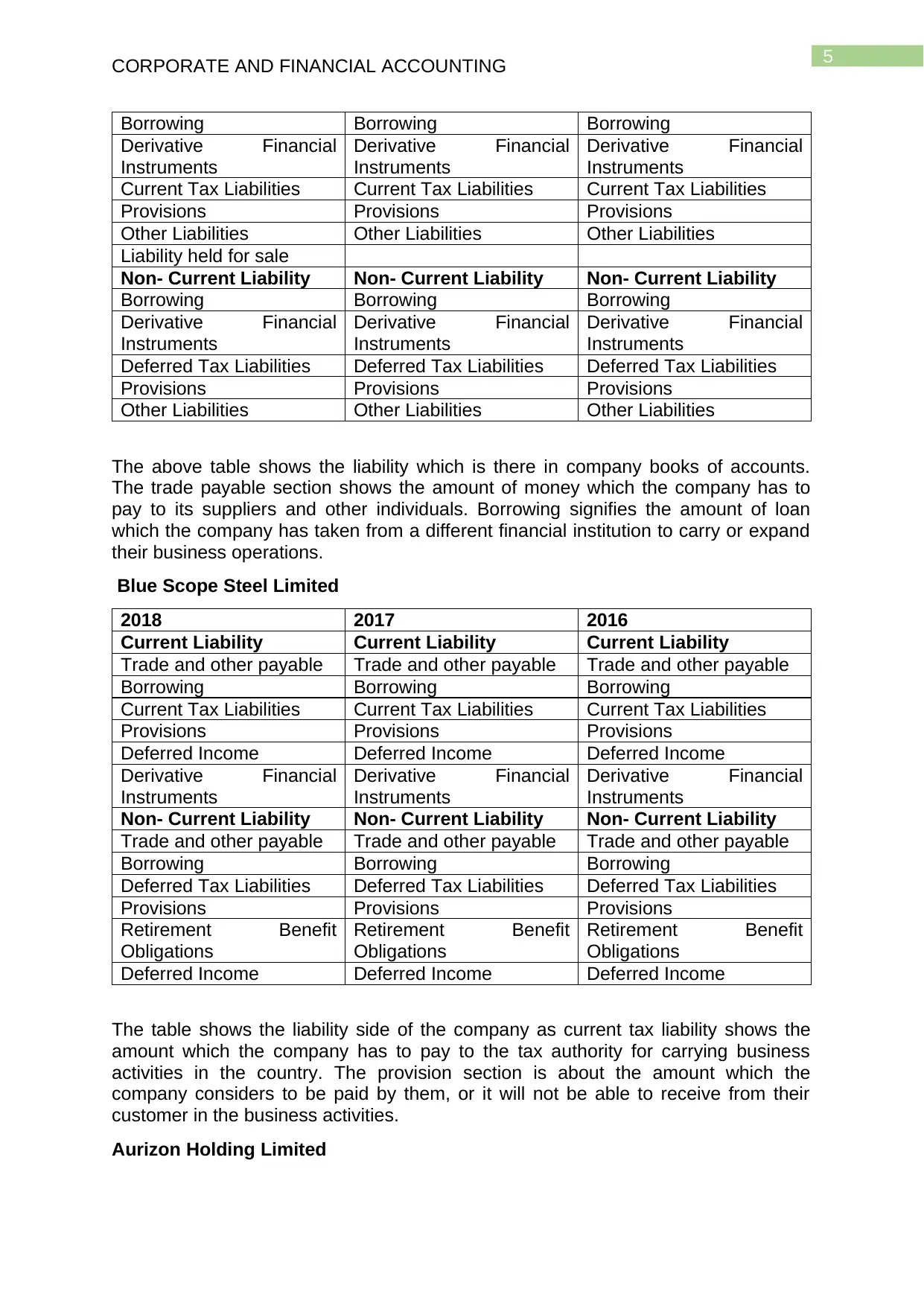

Aurizon Holding Limited

2018 2017 2016

Current Liability Current Liability Current Liability

Trade and other payable Trade and other payable Trade and other payable

5

CORPORATE AND FINANCIAL ACCOUNTING

Borrowing Borrowing Borrowing

Derivative Financial

Instruments

Derivative Financial

Instruments

Derivative Financial

Instruments

Current Tax Liabilities Current Tax Liabilities Current Tax Liabilities

Provisions Provisions Provisions

Other Liabilities Other Liabilities Other Liabilities

Liability held for sale

Non- Current Liability Non- Current Liability Non- Current Liability

Borrowing Borrowing Borrowing

Derivative Financial

Instruments

Derivative Financial

Instruments

Derivative Financial

Instruments

Deferred Tax Liabilities Deferred Tax Liabilities Deferred Tax Liabilities

Provisions Provisions Provisions

Other Liabilities Other Liabilities Other Liabilities

The above table shows the liability which is there in company books of accounts.

The trade payable section shows the amount of money which the company has to

pay to its suppliers and other individuals. Borrowing signifies the amount of loan

which the company has taken from a different financial institution to carry or expand

their business operations.

Blue Scope Steel Limited

2018 2017 2016

Current Liability Current Liability Current Liability

Trade and other payable Trade and other payable Trade and other payable

Borrowing Borrowing Borrowing

Current Tax Liabilities Current Tax Liabilities Current Tax Liabilities

Provisions Provisions Provisions

Deferred Income Deferred Income Deferred Income

Derivative Financial

Instruments

Derivative Financial

Instruments

Derivative Financial

Instruments

Non- Current Liability Non- Current Liability Non- Current Liability

Trade and other payable Trade and other payable Trade and other payable

Borrowing Borrowing Borrowing

Deferred Tax Liabilities Deferred Tax Liabilities Deferred Tax Liabilities

Provisions Provisions Provisions

Retirement Benefit

Obligations

Retirement Benefit

Obligations

Retirement Benefit

Obligations

Deferred Income Deferred Income Deferred Income

The table shows the liability side of the company as current tax liability shows the

amount which the company has to pay to the tax authority for carrying business

activities in the country. The provision section is about the amount which the

company considers to be paid by them, or it will not be able to receive from their

customer in the business activities.

Aurizon Holding Limited

CORPORATE AND FINANCIAL ACCOUNTING

Borrowing Borrowing Borrowing

Derivative Financial

Instruments

Derivative Financial

Instruments

Derivative Financial

Instruments

Current Tax Liabilities Current Tax Liabilities Current Tax Liabilities

Provisions Provisions Provisions

Other Liabilities Other Liabilities Other Liabilities

Liability held for sale

Non- Current Liability Non- Current Liability Non- Current Liability

Borrowing Borrowing Borrowing

Derivative Financial

Instruments

Derivative Financial

Instruments

Derivative Financial

Instruments

Deferred Tax Liabilities Deferred Tax Liabilities Deferred Tax Liabilities

Provisions Provisions Provisions

Other Liabilities Other Liabilities Other Liabilities

The above table shows the liability which is there in company books of accounts.

The trade payable section shows the amount of money which the company has to

pay to its suppliers and other individuals. Borrowing signifies the amount of loan

which the company has taken from a different financial institution to carry or expand

their business operations.

Blue Scope Steel Limited

2018 2017 2016

Current Liability Current Liability Current Liability

Trade and other payable Trade and other payable Trade and other payable

Borrowing Borrowing Borrowing

Current Tax Liabilities Current Tax Liabilities Current Tax Liabilities

Provisions Provisions Provisions

Deferred Income Deferred Income Deferred Income

Derivative Financial

Instruments

Derivative Financial

Instruments

Derivative Financial

Instruments

Non- Current Liability Non- Current Liability Non- Current Liability

Trade and other payable Trade and other payable Trade and other payable

Borrowing Borrowing Borrowing

Deferred Tax Liabilities Deferred Tax Liabilities Deferred Tax Liabilities

Provisions Provisions Provisions

Retirement Benefit

Obligations

Retirement Benefit

Obligations

Retirement Benefit

Obligations

Deferred Income Deferred Income Deferred Income

The table shows the liability side of the company as current tax liability shows the

amount which the company has to pay to the tax authority for carrying business

activities in the country. The provision section is about the amount which the

company considers to be paid by them, or it will not be able to receive from their

customer in the business activities.

Aurizon Holding Limited

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CORPORATE AND FINANCIAL ACCOUNTING

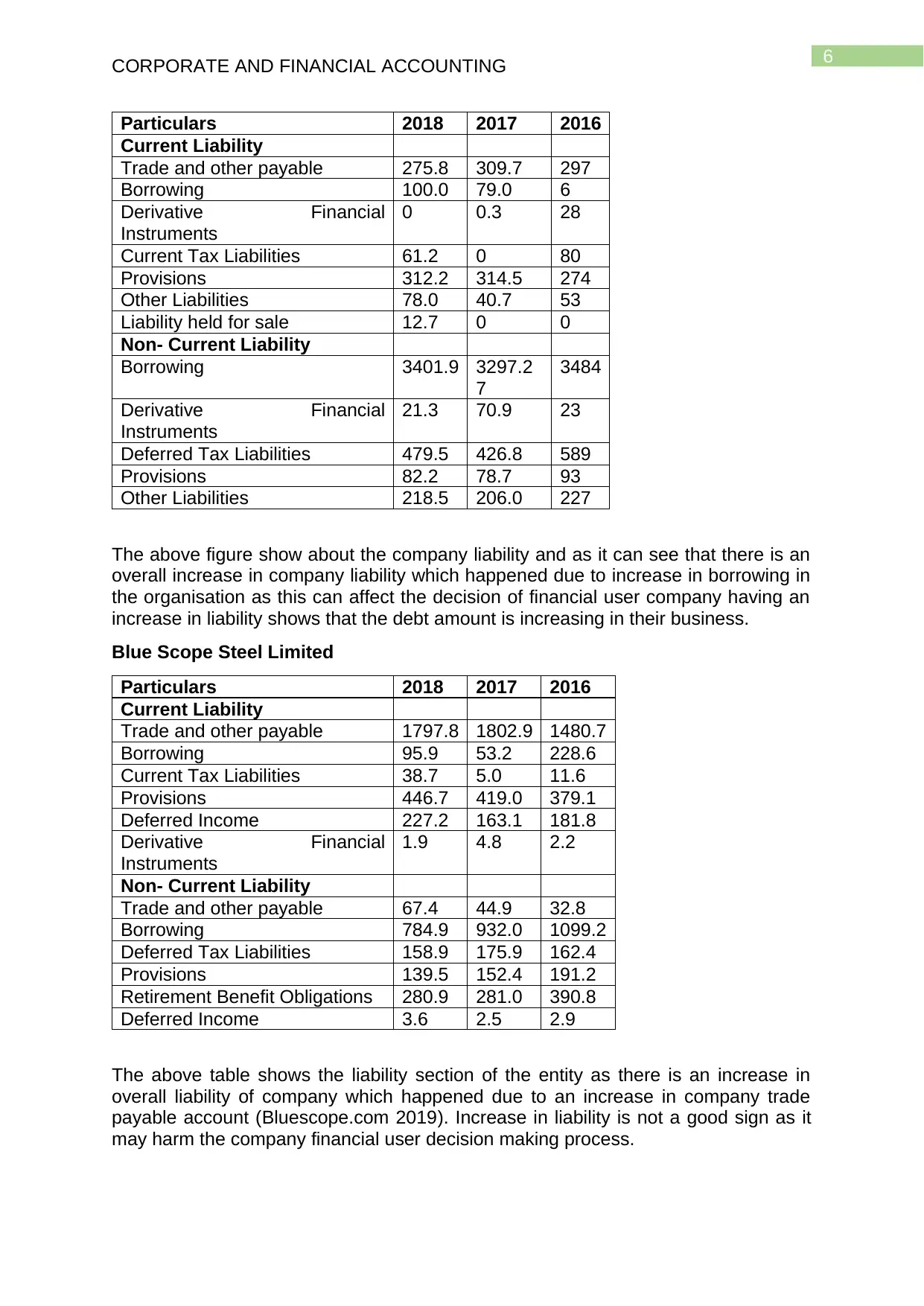

Particulars 2018 2017 2016

Current Liability

Trade and other payable 275.8 309.7 297

Borrowing 100.0 79.0 6

Derivative Financial

Instruments

0 0.3 28

Current Tax Liabilities 61.2 0 80

Provisions 312.2 314.5 274

Other Liabilities 78.0 40.7 53

Liability held for sale 12.7 0 0

Non- Current Liability

Borrowing 3401.9 3297.2

7

3484

Derivative Financial

Instruments

21.3 70.9 23

Deferred Tax Liabilities 479.5 426.8 589

Provisions 82.2 78.7 93

Other Liabilities 218.5 206.0 227

The above figure show about the company liability and as it can see that there is an

overall increase in company liability which happened due to increase in borrowing in

the organisation as this can affect the decision of financial user company having an

increase in liability shows that the debt amount is increasing in their business.

Blue Scope Steel Limited

Particulars 2018 2017 2016

Current Liability

Trade and other payable 1797.8 1802.9 1480.7

Borrowing 95.9 53.2 228.6

Current Tax Liabilities 38.7 5.0 11.6

Provisions 446.7 419.0 379.1

Deferred Income 227.2 163.1 181.8

Derivative Financial

Instruments

1.9 4.8 2.2

Non- Current Liability

Trade and other payable 67.4 44.9 32.8

Borrowing 784.9 932.0 1099.2

Deferred Tax Liabilities 158.9 175.9 162.4

Provisions 139.5 152.4 191.2

Retirement Benefit Obligations 280.9 281.0 390.8

Deferred Income 3.6 2.5 2.9

The above table shows the liability section of the entity as there is an increase in

overall liability of company which happened due to an increase in company trade

payable account (Bluescope.com 2019). Increase in liability is not a good sign as it

may harm the company financial user decision making process.

CORPORATE AND FINANCIAL ACCOUNTING

Particulars 2018 2017 2016

Current Liability

Trade and other payable 275.8 309.7 297

Borrowing 100.0 79.0 6

Derivative Financial

Instruments

0 0.3 28

Current Tax Liabilities 61.2 0 80

Provisions 312.2 314.5 274

Other Liabilities 78.0 40.7 53

Liability held for sale 12.7 0 0

Non- Current Liability

Borrowing 3401.9 3297.2

7

3484

Derivative Financial

Instruments

21.3 70.9 23

Deferred Tax Liabilities 479.5 426.8 589

Provisions 82.2 78.7 93

Other Liabilities 218.5 206.0 227

The above figure show about the company liability and as it can see that there is an

overall increase in company liability which happened due to increase in borrowing in

the organisation as this can affect the decision of financial user company having an

increase in liability shows that the debt amount is increasing in their business.

Blue Scope Steel Limited

Particulars 2018 2017 2016

Current Liability

Trade and other payable 1797.8 1802.9 1480.7

Borrowing 95.9 53.2 228.6

Current Tax Liabilities 38.7 5.0 11.6

Provisions 446.7 419.0 379.1

Deferred Income 227.2 163.1 181.8

Derivative Financial

Instruments

1.9 4.8 2.2

Non- Current Liability

Trade and other payable 67.4 44.9 32.8

Borrowing 784.9 932.0 1099.2

Deferred Tax Liabilities 158.9 175.9 162.4

Provisions 139.5 152.4 191.2

Retirement Benefit Obligations 280.9 281.0 390.8

Deferred Income 3.6 2.5 2.9

The above table shows the liability section of the entity as there is an increase in

overall liability of company which happened due to an increase in company trade

payable account (Bluescope.com 2019). Increase in liability is not a good sign as it

may harm the company financial user decision making process.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE AND FINANCIAL ACCOUNTING

Source of fund

The company financial report states the entity Aurizon Holding Limited is

properly financed by both the equity and debt in their business (Grossi and Steccolini

2015) as the company is managing the proper combination of debt and equity which

help them to carry the business activities easily in the industry.

Blue Scope Steel Limited is also appropriately financed by both debt and

equity that helps them to carry their business operation easily in their business.

Company is expanding its operation. As a result, there is an increase in overall

borrowing of the organisation.

Part B

Small Proprietary Company

These are a kind of private companies which do not have the right to invite the

public to invest in the business (Maas, Schaltegger and Crutzen 2016). A company

is considered to be small proprietary if it able to satisfy any two criteria mentioned

below:

It has less than “$10 million gross operating revenue” in the accounting year

At the end of the accounting year, it is own not more than $5 million in assets.

The maximum employee company have 50

In this business structure, shareholder liability is limited to the amount they have

invested in the company. The taxed that imposed upon the shareholder and director

is standard rate and not the corporate tax rate, so this helps them to save some

amount of tax in their business activities (Schaltegger, Etxeberria and Ortas 2017).

An individual personal asset cannot be used to pay the liability of the entity. The

ownership can be easily transferred to other individuals.

Large Proprietary Company

The large proprietary company is those private company which carries their business

activities in Australia and not able to make public offerings (Velte and Stawinoga

2017). To become a large proprietary company, it should satisfy all the criteria

mentioned below:

The entity has more than $12.5 million worth asset at the end of the financial

year

Company has more than 50 employees in their business operations

The entity is having more than $25 million in its gross operating revenue in the

same financial year.

Being a large proprietary firm, it should get its financial statement audited and should

present the same to its different shareholders. It has to comply with more rules and

regulation while carrying their business activities (Watson 2015). The company

should do proper preparation of the financial report, and it can only get the relief of

not carrying the audit process is by asking relief from ASIC.

Reporting Entity

It means that the company is aware of the financial user obtaining proper

information from the listed financial information which signifies that the company

should present the information accurately in their books of account that can help the

user to take proper decision in regards of company business (Wu, Bacon and Hoque

2014). The entity should prepare the report by taking into consideration of all the

CORPORATE AND FINANCIAL ACCOUNTING

Source of fund

The company financial report states the entity Aurizon Holding Limited is

properly financed by both the equity and debt in their business (Grossi and Steccolini

2015) as the company is managing the proper combination of debt and equity which

help them to carry the business activities easily in the industry.

Blue Scope Steel Limited is also appropriately financed by both debt and

equity that helps them to carry their business operation easily in their business.

Company is expanding its operation. As a result, there is an increase in overall

borrowing of the organisation.

Part B

Small Proprietary Company

These are a kind of private companies which do not have the right to invite the

public to invest in the business (Maas, Schaltegger and Crutzen 2016). A company

is considered to be small proprietary if it able to satisfy any two criteria mentioned

below:

It has less than “$10 million gross operating revenue” in the accounting year

At the end of the accounting year, it is own not more than $5 million in assets.

The maximum employee company have 50

In this business structure, shareholder liability is limited to the amount they have

invested in the company. The taxed that imposed upon the shareholder and director

is standard rate and not the corporate tax rate, so this helps them to save some

amount of tax in their business activities (Schaltegger, Etxeberria and Ortas 2017).

An individual personal asset cannot be used to pay the liability of the entity. The

ownership can be easily transferred to other individuals.

Large Proprietary Company

The large proprietary company is those private company which carries their business

activities in Australia and not able to make public offerings (Velte and Stawinoga

2017). To become a large proprietary company, it should satisfy all the criteria

mentioned below:

The entity has more than $12.5 million worth asset at the end of the financial

year

Company has more than 50 employees in their business operations

The entity is having more than $25 million in its gross operating revenue in the

same financial year.

Being a large proprietary firm, it should get its financial statement audited and should

present the same to its different shareholders. It has to comply with more rules and

regulation while carrying their business activities (Watson 2015). The company

should do proper preparation of the financial report, and it can only get the relief of

not carrying the audit process is by asking relief from ASIC.

Reporting Entity

It means that the company is aware of the financial user obtaining proper

information from the listed financial information which signifies that the company

should present the information accurately in their books of account that can help the

user to take proper decision in regards of company business (Wu, Bacon and Hoque

2014). The entity should prepare the report by taking into consideration of all the

8

CORPORATE AND FINANCIAL ACCOUNTING

norms and accounting standard in their financial information. If the entity has been

considered to be a reporting entity, then it should follow all the Australian Accounting

Standard in the preparation of their financial report as well as it should consider all

other norms in the preparation of books of accounts. GPFR should be prepared by

the reporting entity in their business activities.

Conclusion

It can conclude from the above discussion about corporate accounting is that

it assists the company to prepare its financial statement properly for the financial

users. These branch of accounting helps the user to value and interpret the company

financial information quickly and effectively. The report shows two companies as

both carry their business activities in Australia. It states the various aspects of equity

and liability in the company and the movement in both of the listed items. Lastly, it

shows the different types of business form as small proprietary business, large

proprietary, and reporting entity. The implication of each business has explained in

the report.

CORPORATE AND FINANCIAL ACCOUNTING

norms and accounting standard in their financial information. If the entity has been

considered to be a reporting entity, then it should follow all the Australian Accounting

Standard in the preparation of their financial report as well as it should consider all

other norms in the preparation of books of accounts. GPFR should be prepared by

the reporting entity in their business activities.

Conclusion

It can conclude from the above discussion about corporate accounting is that

it assists the company to prepare its financial statement properly for the financial

users. These branch of accounting helps the user to value and interpret the company

financial information quickly and effectively. The report shows two companies as

both carry their business activities in Australia. It states the various aspects of equity

and liability in the company and the movement in both of the listed items. Lastly, it

shows the different types of business form as small proprietary business, large

proprietary, and reporting entity. The implication of each business has explained in

the report.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CORPORATE AND FINANCIAL ACCOUNTING

Reference

Agrawal, A. and Cooper, T., 2017. Corporate governance consequences of

accounting scandals: Evidence from top management, CFO and auditor

turnover. Quarterly Journal of Finance, 7(01), p.1650014.

Atanasov, V.A. and Black, B.S., 2016. Shock-based causal inference in corporate

finance and accounting research. Critical Finance Review, 5, pp.207-304.

Aurizon.com.au (2019). 2018. [online] Aurizon.com.au. Available at:

https://www.aurizon.com.au/investors/documents-and-webcasts/2018 [Accessed 24

Sep. 2019].

Bluescope.com (2019). Annual Reports - BlueScope Corporate. [online]

Bluescope.com. Available at: https://www.bluescope.com/investors/annual-reports/

[Accessed 24 Sep. 2019].

Domino, M.A., Wingreen, S.C. and Blanton, J.E., 2015. Social cognitive theory: The

antecedents and effects of ethical climate fit on organizational attitudes of corporate

accounting professionals—a reflection of client narcissism and fraud attitude

risk. Journal of Business Ethics, 131(2), pp.453-467.

Ermakova, A.N., Vaytsekhovskaya, S.S., Malitskaya, V.B. and Prodanova, N.А.,

2016. Investment attractiveness of small innovational business under the conditions

of globalisation and integration.

Flower, J., 2015. The international integrated reporting council: a story of

failure. Critical Perspectives on Accounting, 27, pp.1-17.

Grossi, G. and Steccolini, I., 2015. Pursuing private or public accountability in the

public sector? Applying IPSASs to define the reporting entity in municipal

consolidation. International Journal of Public Administration, 38(4), pp.325-334.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability

assessment, management accounting, control, and reporting. Journal of Cleaner

Production, 136, pp.237-248.

Schaltegger, S., Etxeberria, I.Á. and Ortas, E., 2017. Innovating corporate

accounting and reporting for sustainability–attributes and challenges. Sustainable

Development, 25(2), pp.113-122.

Velte, P. and Stawinoga, M., 2017. Integrated reporting: The current state of

empirical research, limitations and future research implications. Journal of

Management Control, 28(3), pp.275-320.

Watson, L., 2015. Corporate social responsibility research in accounting. Journal of

Accounting Literature, 34, pp.1-16.

Wu, N., Bacon, N. and Hoque, K., 2014. The adoption of high performance work

practices in small businesses: the influence of markets, business characteristics and

HR expertise. The International Journal of Human Resource Management, 25(8),

pp.1149-1169.

CORPORATE AND FINANCIAL ACCOUNTING

Reference

Agrawal, A. and Cooper, T., 2017. Corporate governance consequences of

accounting scandals: Evidence from top management, CFO and auditor

turnover. Quarterly Journal of Finance, 7(01), p.1650014.

Atanasov, V.A. and Black, B.S., 2016. Shock-based causal inference in corporate

finance and accounting research. Critical Finance Review, 5, pp.207-304.

Aurizon.com.au (2019). 2018. [online] Aurizon.com.au. Available at:

https://www.aurizon.com.au/investors/documents-and-webcasts/2018 [Accessed 24

Sep. 2019].

Bluescope.com (2019). Annual Reports - BlueScope Corporate. [online]

Bluescope.com. Available at: https://www.bluescope.com/investors/annual-reports/

[Accessed 24 Sep. 2019].

Domino, M.A., Wingreen, S.C. and Blanton, J.E., 2015. Social cognitive theory: The

antecedents and effects of ethical climate fit on organizational attitudes of corporate

accounting professionals—a reflection of client narcissism and fraud attitude

risk. Journal of Business Ethics, 131(2), pp.453-467.

Ermakova, A.N., Vaytsekhovskaya, S.S., Malitskaya, V.B. and Prodanova, N.А.,

2016. Investment attractiveness of small innovational business under the conditions

of globalisation and integration.

Flower, J., 2015. The international integrated reporting council: a story of

failure. Critical Perspectives on Accounting, 27, pp.1-17.

Grossi, G. and Steccolini, I., 2015. Pursuing private or public accountability in the

public sector? Applying IPSASs to define the reporting entity in municipal

consolidation. International Journal of Public Administration, 38(4), pp.325-334.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability

assessment, management accounting, control, and reporting. Journal of Cleaner

Production, 136, pp.237-248.

Schaltegger, S., Etxeberria, I.Á. and Ortas, E., 2017. Innovating corporate

accounting and reporting for sustainability–attributes and challenges. Sustainable

Development, 25(2), pp.113-122.

Velte, P. and Stawinoga, M., 2017. Integrated reporting: The current state of

empirical research, limitations and future research implications. Journal of

Management Control, 28(3), pp.275-320.

Watson, L., 2015. Corporate social responsibility research in accounting. Journal of

Accounting Literature, 34, pp.1-16.

Wu, N., Bacon, N. and Hoque, K., 2014. The adoption of high performance work

practices in small businesses: the influence of markets, business characteristics and

HR expertise. The International Journal of Human Resource Management, 25(8),

pp.1149-1169.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.