Analysis of Funds and Reporting for Corporate Accounting (HA2032)

VerifiedAdded on 2022/10/15

|17

|3557

|9

Report

AI Summary

This report provides a comprehensive analysis of corporate and financial accounting, focusing on the sources of funds utilized by two ASX-listed companies: Investec Australia Property Fund and Carsales. The report examines the equity and liabilities of both companies, including contributed equity, retained earnings, reserves, and non-controlling interests, over a three-year period. It details the movement of these items and discusses the advantages and disadvantages of each source of fund. Furthermore, the report delves into the classification of proprietary companies (large, small, and reporting entities) and their respective compliance and reporting requirements under Australian law. The analysis is based on the companies' annual reports, providing insights into their financial strategies and reporting practices.

Running head: CORPORATE AND FINANCIAL ACCOUNTING

Corporate and Financial Accounting

Name of the Student

Name of the University

Author Note

Corporate and Financial Accounting

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE AND FINANCIAL ACCOUNTING

Executive Summary

The report aims to understand and gain knowledge about the various sources of fund

used by a company. In the discussion, two different companies have been chosen that are

‘Investec Australia Property Fund' and ‘Carsales.' The sources of the fund as equities and

liabilities of both the companies have been discussed. Addition to this, the movement,

advantages, and disadvantages of these sources are also stated in this report. Further, the

report has discussed different types of proprietary companies such as large, small, and

reporting entity. At last, it has been described as various implications in terms of compliance

and reporting requirement to these entities.

Executive Summary

The report aims to understand and gain knowledge about the various sources of fund

used by a company. In the discussion, two different companies have been chosen that are

‘Investec Australia Property Fund' and ‘Carsales.' The sources of the fund as equities and

liabilities of both the companies have been discussed. Addition to this, the movement,

advantages, and disadvantages of these sources are also stated in this report. Further, the

report has discussed different types of proprietary companies such as large, small, and

reporting entity. At last, it has been described as various implications in terms of compliance

and reporting requirement to these entities.

2CORPORATE AND FINANCIAL ACCOUNTING

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................4

(PART A)...................................................................................................................................4

i. Items recorded under Owner’s Equity Section of:..............................................................4

Investec Australia Property Fund....................................................................................4

Carsales...........................................................................................................................4

ii. Movement of items under Owner’s Equity Section............................................................5

iii. Items recorded under Liabilities Section of:...................................................................6

Investec Australia Property Fund....................................................................................6

Carsales...........................................................................................................................7

iv. Movement of Items under Liabilities Section.................................................................7

v. Advantages and disadvantages of Sources of Fund............................................................8

(PART B).................................................................................................................................10

Conditions under which a proprietary company is treated as Large or Small:.............10

Reporting Entity............................................................................................................11

Implications respect to Compliance and Reporting......................................................11

Conclusion................................................................................................................................12

References................................................................................................................................13

Introduction

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................4

(PART A)...................................................................................................................................4

i. Items recorded under Owner’s Equity Section of:..............................................................4

Investec Australia Property Fund....................................................................................4

Carsales...........................................................................................................................4

ii. Movement of items under Owner’s Equity Section............................................................5

iii. Items recorded under Liabilities Section of:...................................................................6

Investec Australia Property Fund....................................................................................6

Carsales...........................................................................................................................7

iv. Movement of Items under Liabilities Section.................................................................7

v. Advantages and disadvantages of Sources of Fund............................................................8

(PART B).................................................................................................................................10

Conditions under which a proprietary company is treated as Large or Small:.............10

Reporting Entity............................................................................................................11

Implications respect to Compliance and Reporting......................................................11

Conclusion................................................................................................................................12

References................................................................................................................................13

Introduction

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE AND FINANCIAL ACCOUNTING

The report has been prepared to develop a clear understanding as well as to answer

the relevant questions related to the various sources of funds that are used by a company to

raise their funds. The preparation of this report is done through a comparative analysis of

sources of fund used by ASX listed two different companies. The companies chosen here for

making this report are ‘Investec Australia Property Fund’ and ‘Carsales.' In the discussion

section, the answer is based on proper analysis of both the company’s annual reports for a

three-year period. It has been discussed about the items as well as the movement of the stated

items in the section of equities and liabilities. Addition to this, it has discussed the several

classifications of the companies for reporting.

Company’s Overview

Investec has started its journey in the year 1974 in South Africa as a small finance

company and entered the UK in the year 1992. Today it is working at an international level

with above 10,000 employees that provides service to the clients within the Specialist

Banking, Asset Management, and Wealth and Investment.

Carsales was founded in the year 1997 that comes under an industry related to media,

internet, and E-Commerce. It works as an online market place where information about

several product/service is given by different third parties. In Australia, Carsales is

additionally associated with the automotive industry. The company is highly specialized in

online marketing for cars automotive, motorbikes as well as marine categorized professional

in Australia.

The report has been prepared to develop a clear understanding as well as to answer

the relevant questions related to the various sources of funds that are used by a company to

raise their funds. The preparation of this report is done through a comparative analysis of

sources of fund used by ASX listed two different companies. The companies chosen here for

making this report are ‘Investec Australia Property Fund’ and ‘Carsales.' In the discussion

section, the answer is based on proper analysis of both the company’s annual reports for a

three-year period. It has been discussed about the items as well as the movement of the stated

items in the section of equities and liabilities. Addition to this, it has discussed the several

classifications of the companies for reporting.

Company’s Overview

Investec has started its journey in the year 1974 in South Africa as a small finance

company and entered the UK in the year 1992. Today it is working at an international level

with above 10,000 employees that provides service to the clients within the Specialist

Banking, Asset Management, and Wealth and Investment.

Carsales was founded in the year 1997 that comes under an industry related to media,

internet, and E-Commerce. It works as an online market place where information about

several product/service is given by different third parties. In Australia, Carsales is

additionally associated with the automotive industry. The company is highly specialized in

online marketing for cars automotive, motorbikes as well as marine categorized professional

in Australia.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE AND FINANCIAL ACCOUNTING

Discussion

(PART A)

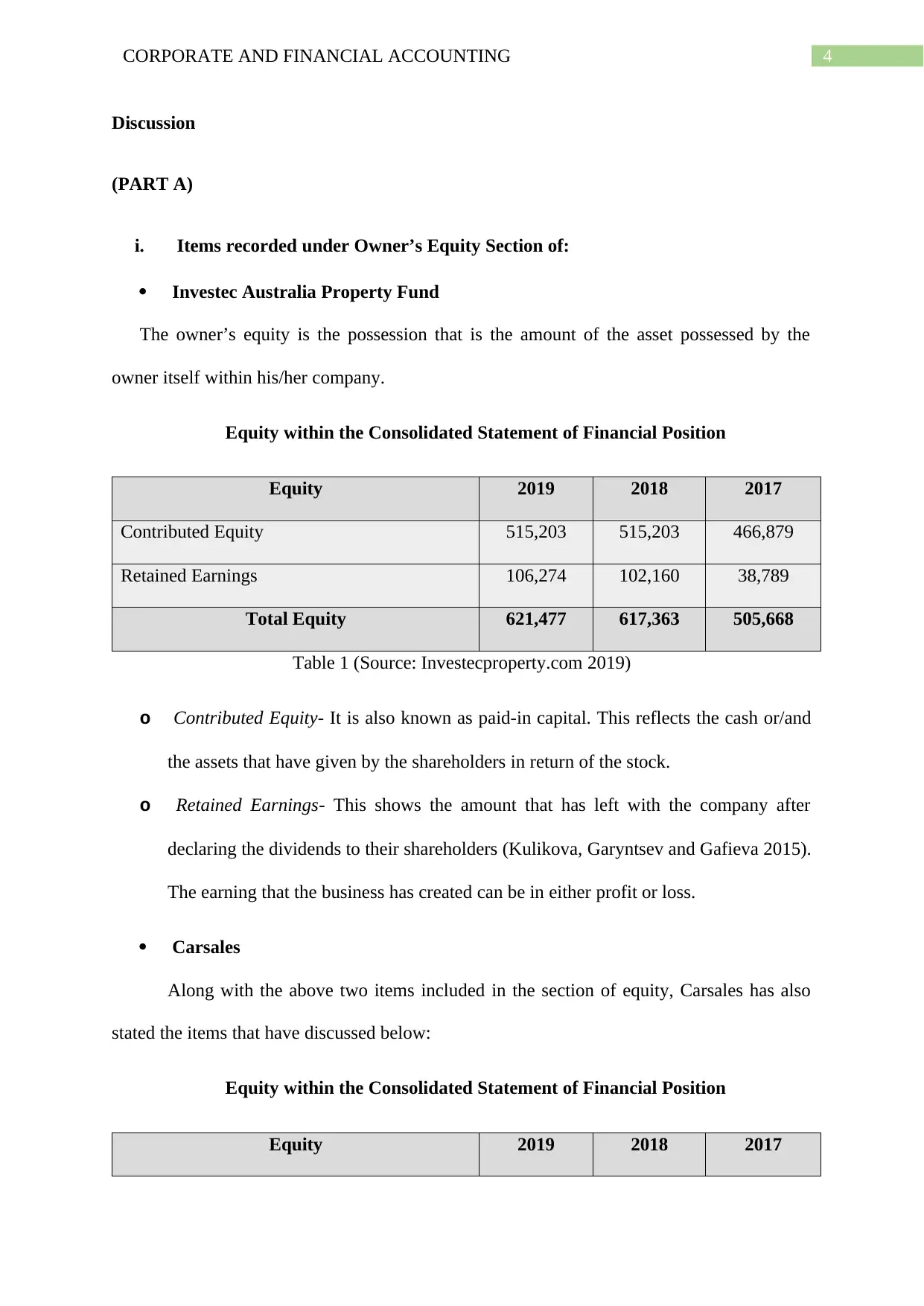

i. Items recorded under Owner’s Equity Section of:

Investec Australia Property Fund

The owner’s equity is the possession that is the amount of the asset possessed by the

owner itself within his/her company.

Equity within the Consolidated Statement of Financial Position

Equity 2019 2018 2017

Contributed Equity 515,203 515,203 466,879

Retained Earnings 106,274 102,160 38,789

Total Equity 621,477 617,363 505,668

Table 1 (Source: Investecproperty.com 2019)

o Contributed Equity- It is also known as paid-in capital. This reflects the cash or/and

the assets that have given by the shareholders in return of the stock.

o Retained Earnings- This shows the amount that has left with the company after

declaring the dividends to their shareholders (Kulikova, Garyntsev and Gafieva 2015).

The earning that the business has created can be in either profit or loss.

Carsales

Along with the above two items included in the section of equity, Carsales has also

stated the items that have discussed below:

Equity within the Consolidated Statement of Financial Position

Equity 2019 2018 2017

Discussion

(PART A)

i. Items recorded under Owner’s Equity Section of:

Investec Australia Property Fund

The owner’s equity is the possession that is the amount of the asset possessed by the

owner itself within his/her company.

Equity within the Consolidated Statement of Financial Position

Equity 2019 2018 2017

Contributed Equity 515,203 515,203 466,879

Retained Earnings 106,274 102,160 38,789

Total Equity 621,477 617,363 505,668

Table 1 (Source: Investecproperty.com 2019)

o Contributed Equity- It is also known as paid-in capital. This reflects the cash or/and

the assets that have given by the shareholders in return of the stock.

o Retained Earnings- This shows the amount that has left with the company after

declaring the dividends to their shareholders (Kulikova, Garyntsev and Gafieva 2015).

The earning that the business has created can be in either profit or loss.

Carsales

Along with the above two items included in the section of equity, Carsales has also

stated the items that have discussed below:

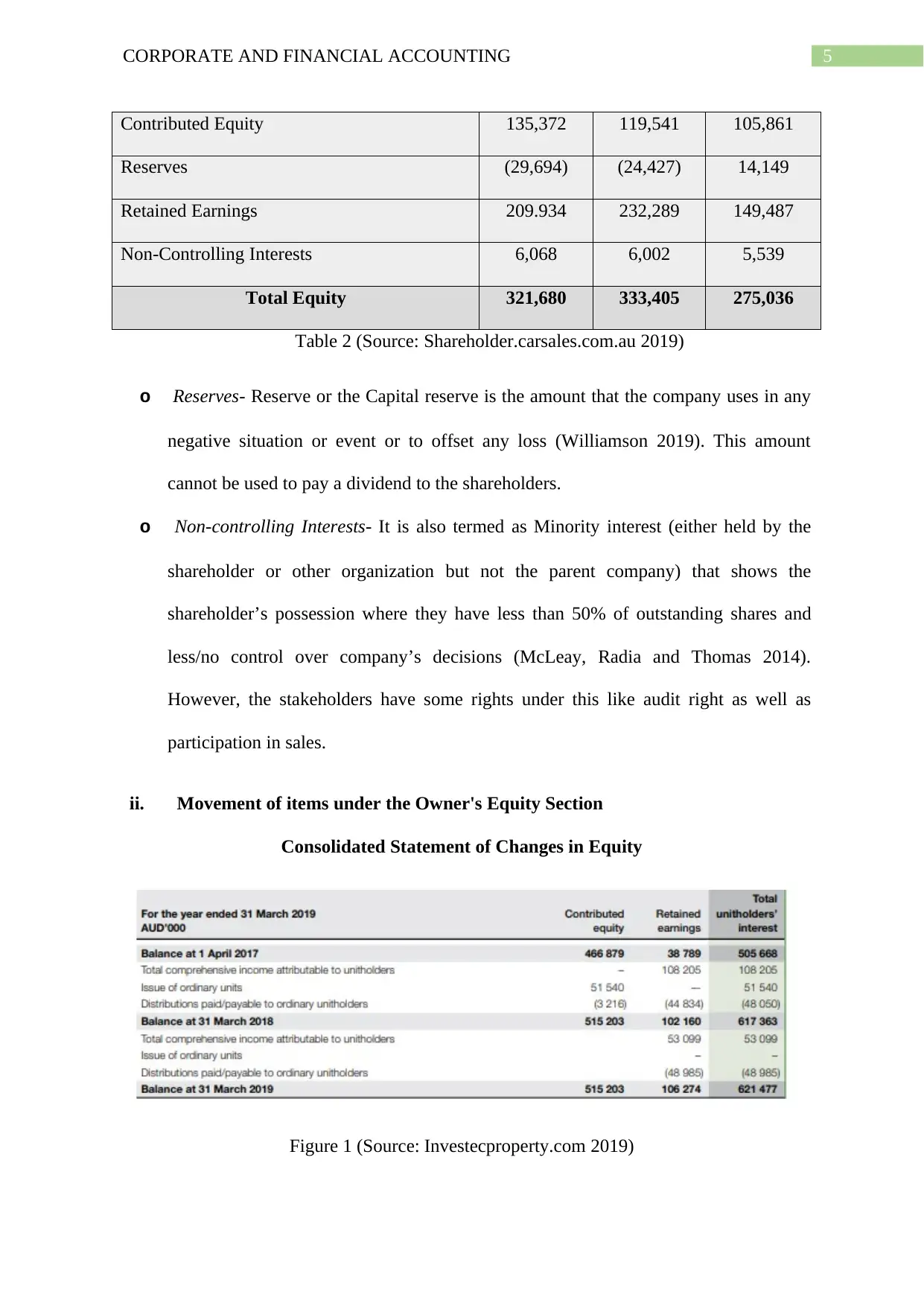

Equity within the Consolidated Statement of Financial Position

Equity 2019 2018 2017

5CORPORATE AND FINANCIAL ACCOUNTING

Contributed Equity 135,372 119,541 105,861

Reserves (29,694) (24,427) 14,149

Retained Earnings 209.934 232,289 149,487

Non-Controlling Interests 6,068 6,002 5,539

Total Equity 321,680 333,405 275,036

Table 2 (Source: Shareholder.carsales.com.au 2019)

o Reserves- Reserve or the Capital reserve is the amount that the company uses in any

negative situation or event or to offset any loss (Williamson 2019). This amount

cannot be used to pay a dividend to the shareholders.

o Non-controlling Interests- It is also termed as Minority interest (either held by the

shareholder or other organization but not the parent company) that shows the

shareholder’s possession where they have less than 50% of outstanding shares and

less/no control over company’s decisions (McLeay, Radia and Thomas 2014).

However, the stakeholders have some rights under this like audit right as well as

participation in sales.

ii. Movement of items under the Owner's Equity Section

Consolidated Statement of Changes in Equity

Figure 1 (Source: Investecproperty.com 2019)

Contributed Equity 135,372 119,541 105,861

Reserves (29,694) (24,427) 14,149

Retained Earnings 209.934 232,289 149,487

Non-Controlling Interests 6,068 6,002 5,539

Total Equity 321,680 333,405 275,036

Table 2 (Source: Shareholder.carsales.com.au 2019)

o Reserves- Reserve or the Capital reserve is the amount that the company uses in any

negative situation or event or to offset any loss (Williamson 2019). This amount

cannot be used to pay a dividend to the shareholders.

o Non-controlling Interests- It is also termed as Minority interest (either held by the

shareholder or other organization but not the parent company) that shows the

shareholder’s possession where they have less than 50% of outstanding shares and

less/no control over company’s decisions (McLeay, Radia and Thomas 2014).

However, the stakeholders have some rights under this like audit right as well as

participation in sales.

ii. Movement of items under the Owner's Equity Section

Consolidated Statement of Changes in Equity

Figure 1 (Source: Investecproperty.com 2019)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE AND FINANCIAL ACCOUNTING

The changes in the figures of equity of the Investec Company is shown in Figure 1 is

of the recent three years. The data shows that the company has gradually increased in the unit

holder's interest in the last three years. The earning of the company is increasing every year.

Even though distribution to the unitholders is higher in 2018 than the year 2017, the retained

earnings of the company are showing its figure positively increased (Investec 2019). The

contributed equity in the company is increased in the year 2017 because of the issuance of

51,540 ordinary units. However, the company did not issue further in 2018. Therefore, there

is stability in the figures.

The changes in the figures of equity of the company Carsales has stated in Table 1 that

shows four different items under it. The company’s reserve balance is showing a negative

figure of 29,694 in 2019 because a high amount of acquisition reserve under non-controlling

interest is deducted. Several other amounts like foreign currency translation reserve as well as

assets at fair value also have been deducted under share-based payment reserve

(Shareholder.carsales.com.au 2019). The amount of 2,120 was deducted in the retained

earnings due to the impact of changes in accounting policy in the year 2018. However, net

profit after dividend distribution is lower in 2019, but it has declared a high dividend in the

same year.

iii. Items recorded under Liabilities Section of:

Investec Australia Property Fund

The items that the company has shown in the Liability section of their financial report are

classified under Non-current liabilities and Current Liabilities.

Non-current Liabilities are those liabilities can also be termed as Long-term liability.

These long-term obligations are for more than 12 months. The company includes Long-term

The changes in the figures of equity of the Investec Company is shown in Figure 1 is

of the recent three years. The data shows that the company has gradually increased in the unit

holder's interest in the last three years. The earning of the company is increasing every year.

Even though distribution to the unitholders is higher in 2018 than the year 2017, the retained

earnings of the company are showing its figure positively increased (Investec 2019). The

contributed equity in the company is increased in the year 2017 because of the issuance of

51,540 ordinary units. However, the company did not issue further in 2018. Therefore, there

is stability in the figures.

The changes in the figures of equity of the company Carsales has stated in Table 1 that

shows four different items under it. The company’s reserve balance is showing a negative

figure of 29,694 in 2019 because a high amount of acquisition reserve under non-controlling

interest is deducted. Several other amounts like foreign currency translation reserve as well as

assets at fair value also have been deducted under share-based payment reserve

(Shareholder.carsales.com.au 2019). The amount of 2,120 was deducted in the retained

earnings due to the impact of changes in accounting policy in the year 2018. However, net

profit after dividend distribution is lower in 2019, but it has declared a high dividend in the

same year.

iii. Items recorded under Liabilities Section of:

Investec Australia Property Fund

The items that the company has shown in the Liability section of their financial report are

classified under Non-current liabilities and Current Liabilities.

Non-current Liabilities are those liabilities can also be termed as Long-term liability.

These long-term obligations are for more than 12 months. The company includes Long-term

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE AND FINANCIAL ACCOUNTING

borrowings as well as trade and other payable within it on 31 March 2018. The further

financial value held at the fair value of also included within it.

Current liabilities are those obligations of the company that is considered as a short-term

debt of the company that has the due within a year and not more than that (Rodrigues Bastos,

Kamil and Sutton 2015). This occurrence has resulted from the daily activity of the company.

The company includes trade and other payables as well as unitholders for distribution and

declared total liability of amount 381,276 within their reports.

Carsales

In the current and non-current liabilities, Carsales has shown its liabilities of trade and

other payables, borrowings, derivative liabilities, deferred tax liabilities, and revenue,

provisions. The company has declared its total liabilities of amount 601,219 in the year.

However, in the year 2018, it was 577,116.

iv. Movement of Items under Liabilities Section

The company Investec stand with the net current liability of amount AUD 46 million on

31 March 2019 and declared due for 12 March 2020. Therefore, it is treated under going

concern. Trade payables of amount 5,265 of short-term and 6,898 of long-term are measured

by using effective interest method. In the year 2018, the company has shown its current

liability of 30.662 and increases in the year 2019 up to 60,320 because of the effect of Long-

term borrowings that have been measured at risk of credit (Investec 2019). The non-current

figure is shown as 350,614 in the year 2018 and that increased up to 401,614 in 2019.

Investment property for future benefits includes several expenses for its maintenance as well

as for up-gradation.

The reports of Carsales declares their liability based on the long term of amount 78,053

and short-term amount of 523,166 in the year 2019. However, the company has increased its

borrowings as well as trade and other payable within it on 31 March 2018. The further

financial value held at the fair value of also included within it.

Current liabilities are those obligations of the company that is considered as a short-term

debt of the company that has the due within a year and not more than that (Rodrigues Bastos,

Kamil and Sutton 2015). This occurrence has resulted from the daily activity of the company.

The company includes trade and other payables as well as unitholders for distribution and

declared total liability of amount 381,276 within their reports.

Carsales

In the current and non-current liabilities, Carsales has shown its liabilities of trade and

other payables, borrowings, derivative liabilities, deferred tax liabilities, and revenue,

provisions. The company has declared its total liabilities of amount 601,219 in the year.

However, in the year 2018, it was 577,116.

iv. Movement of Items under Liabilities Section

The company Investec stand with the net current liability of amount AUD 46 million on

31 March 2019 and declared due for 12 March 2020. Therefore, it is treated under going

concern. Trade payables of amount 5,265 of short-term and 6,898 of long-term are measured

by using effective interest method. In the year 2018, the company has shown its current

liability of 30.662 and increases in the year 2019 up to 60,320 because of the effect of Long-

term borrowings that have been measured at risk of credit (Investec 2019). The non-current

figure is shown as 350,614 in the year 2018 and that increased up to 401,614 in 2019.

Investment property for future benefits includes several expenses for its maintenance as well

as for up-gradation.

The reports of Carsales declares their liability based on the long term of amount 78,053

and short-term amount of 523,166 in the year 2019. However, the company has increased its

8CORPORATE AND FINANCIAL ACCOUNTING

total obligation from 577,116 in the year 2018 to amount 601,219 in 2019

(Shareholder.carsales.com.au 2019). This is because the company has highly reduced its

current obligation of their previous year that is from 325,728 to 78,053 and further raised its

liabilities from the borrowings based on long-term. This resulted in an increase of amount

from 251,388 to 523,166 in the latest year.

v. Advantages and disadvantages of Sources of Fund

‘Equity’

Advantages:

o A solution to the problem of Credit: If the company is having some problem of

crediting, then this will be beneficial for them as debt can impose a high rate of

interest on them.

o Maintains Cash flow: The source of fund from equity helps in eliminating the

chance of going out of funds from their business (Hasan, Hossain and Habib 2015).

Equity investors bring inflow in cash within the company.

o Plans for long-term: As the shareholders do not need their money invested in equity

as immediate. Therefore this shows a view based on long-term to the company.

o Less risk: It reduces the risk of payment for various loans on a fixed interval of time.

Disadvantages:

o Cost to Investor: The investors who have spent their money in a company expects

some good return for it. The owner of the company must have to share some part of

their profit with the investors. Therefore, it a cost that a company bears to meet its

shareholder's expectations.

total obligation from 577,116 in the year 2018 to amount 601,219 in 2019

(Shareholder.carsales.com.au 2019). This is because the company has highly reduced its

current obligation of their previous year that is from 325,728 to 78,053 and further raised its

liabilities from the borrowings based on long-term. This resulted in an increase of amount

from 251,388 to 523,166 in the latest year.

v. Advantages and disadvantages of Sources of Fund

‘Equity’

Advantages:

o A solution to the problem of Credit: If the company is having some problem of

crediting, then this will be beneficial for them as debt can impose a high rate of

interest on them.

o Maintains Cash flow: The source of fund from equity helps in eliminating the

chance of going out of funds from their business (Hasan, Hossain and Habib 2015).

Equity investors bring inflow in cash within the company.

o Plans for long-term: As the shareholders do not need their money invested in equity

as immediate. Therefore this shows a view based on long-term to the company.

o Less risk: It reduces the risk of payment for various loans on a fixed interval of time.

Disadvantages:

o Cost to Investor: The investors who have spent their money in a company expects

some good return for it. The owner of the company must have to share some part of

their profit with the investors. Therefore, it a cost that a company bears to meet its

shareholder's expectations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE AND FINANCIAL ACCOUNTING

o Less Control: The additional investors get some benefit to participating in the

meetings so that they can also share their view in important decisions taken by a

company. Further, they receive some control over the company by the company's

owner. This leads to some loss of control.

o Conflict: There is a chance of arising conflict in the company’s decisions and

investors view. It can be due to different opinions and not comfortable with the

management point of view. ‘Liabilities’

Advantages:

o Temporary obligation to pay: The Company who takes loans is made for a certain

period. It has an obligation to pay within that period which is temporary. The

financier does not interfere in the business conditions until their money is repaid.

o Tax Deduction: In taking loans, the company gets a certain benefit for a tax

deduction (Renko et al 2016). However, it does not get any deduction while the

distribution of dividends to the shareholders.

o Obviousness: the amount of principal, along with interest, is already made known to

the investor by the lender. Therefore, the company has an idea about future

obligations. It makes it easier for the company to make decisions and work

considering their cash balance and any monetary activities.

Disadvantages:

o Fixed date of payment: Company that has changeable situation related to cash flow

within their company have the chances to meet complications on the time of making

payment of loans. Decline or high fluctuations in cash flow can raise the problem. As

o Less Control: The additional investors get some benefit to participating in the

meetings so that they can also share their view in important decisions taken by a

company. Further, they receive some control over the company by the company's

owner. This leads to some loss of control.

o Conflict: There is a chance of arising conflict in the company’s decisions and

investors view. It can be due to different opinions and not comfortable with the

management point of view. ‘Liabilities’

Advantages:

o Temporary obligation to pay: The Company who takes loans is made for a certain

period. It has an obligation to pay within that period which is temporary. The

financier does not interfere in the business conditions until their money is repaid.

o Tax Deduction: In taking loans, the company gets a certain benefit for a tax

deduction (Renko et al 2016). However, it does not get any deduction while the

distribution of dividends to the shareholders.

o Obviousness: the amount of principal, along with interest, is already made known to

the investor by the lender. Therefore, the company has an idea about future

obligations. It makes it easier for the company to make decisions and work

considering their cash balance and any monetary activities.

Disadvantages:

o Fixed date of payment: Company that has changeable situation related to cash flow

within their company have the chances to meet complications on the time of making

payment of loans. Decline or high fluctuations in cash flow can raise the problem. As

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE AND FINANCIAL ACCOUNTING

the time of paying loan amount is fixed and the company has to pay within that period

only.

o Cash outflow: The Company can have a problem if they have raised more liabilities

for them (Tkachuk 2019). This results in more cash outflow from the company is

paying for their obligations. This creates a negative view of the minds of the investor

and prefers to invest in equity.

o Surety: The investor has the demand to keep specific assets as collateral by the

company. Therefore, the owner has to give personal surety about the liability they

hold with them.

(PART B)

As per the Law of Australia, a Proprietary Company is defined within the

Corporation Act 2001 in “Section 45A (1)”. It is a type of company that is held privately in

Australia as well as in South Africa. This can be either Private limited (Pty Ltd) or unlimited

(Pty). Similar to Public Company, it depends on some legal authority. A proprietary

company has stated as Small and Large.

Conditions under which a proprietary company is treated as Large or Small:

If the company or any entity is starting its financial year on or after 1 July 2019:

o The combined profits are $50 million or more than that within that financial year

o The combined gross assets value holds $25 million or more at the end of the financial

year, and

o At the end of the financial year, if it has 100 or more than 100 employees.

If any two conditions are satisfied with any company or entity, then it will be treated

as Large Proprietary Company. Otherwise, it will be treated as Small Proprietary Company

(Potter et al 2019). Addition to this large proprietary company have to make and file a

the time of paying loan amount is fixed and the company has to pay within that period

only.

o Cash outflow: The Company can have a problem if they have raised more liabilities

for them (Tkachuk 2019). This results in more cash outflow from the company is

paying for their obligations. This creates a negative view of the minds of the investor

and prefers to invest in equity.

o Surety: The investor has the demand to keep specific assets as collateral by the

company. Therefore, the owner has to give personal surety about the liability they

hold with them.

(PART B)

As per the Law of Australia, a Proprietary Company is defined within the

Corporation Act 2001 in “Section 45A (1)”. It is a type of company that is held privately in

Australia as well as in South Africa. This can be either Private limited (Pty Ltd) or unlimited

(Pty). Similar to Public Company, it depends on some legal authority. A proprietary

company has stated as Small and Large.

Conditions under which a proprietary company is treated as Large or Small:

If the company or any entity is starting its financial year on or after 1 July 2019:

o The combined profits are $50 million or more than that within that financial year

o The combined gross assets value holds $25 million or more at the end of the financial

year, and

o At the end of the financial year, if it has 100 or more than 100 employees.

If any two conditions are satisfied with any company or entity, then it will be treated

as Large Proprietary Company. Otherwise, it will be treated as Small Proprietary Company

(Potter et al 2019). Addition to this large proprietary company have to make and file a

11CORPORATE AND FINANCIAL ACCOUNTING

financial report as well as the Director's report each year. The small proprietary company has

to file a financial report in some specific situations.

If the company or any entity is starting its financial year on or after 30 June 2019:

o The combined profits are $25 million or more than that within that financial year

o The combined gross assets value holds $12.5 million or more at the end of the

financial year, and

o At the end of the financial year, if it has 50 or more than 50 employees.

If any two conditions are satisfied with any company or entity, then it will be treated

as Large Proprietary Company. Otherwise, it will be treated as Small Proprietary Company.

Addition to this, the large proprietary company have to get audited their accounts except

ASIC allow relief for it and small proprietary company have to file a financial report in some

specific situations.

Reporting Entity

An entity or a company where it is practical to assume that the users somehow get

dependent on a specific report that is General Purpose Financial Report. This provides the

user to have a proper understanding of the position of the company and know the

performance of the company. So that the user will take a better decision for themselves based

on these financial report. Such an entity is termed as the Reporting entity.

Implications respect to Compliance and Reporting

o Small Proprietary Company:

These companies are the one who satisfies with any two conditions mentioned within

“Section 45A (2)”. The conditions are:

a. The combined operating profits are less than $25 million within that financial year

financial report as well as the Director's report each year. The small proprietary company has

to file a financial report in some specific situations.

If the company or any entity is starting its financial year on or after 30 June 2019:

o The combined profits are $25 million or more than that within that financial year

o The combined gross assets value holds $12.5 million or more at the end of the

financial year, and

o At the end of the financial year, if it has 50 or more than 50 employees.

If any two conditions are satisfied with any company or entity, then it will be treated

as Large Proprietary Company. Otherwise, it will be treated as Small Proprietary Company.

Addition to this, the large proprietary company have to get audited their accounts except

ASIC allow relief for it and small proprietary company have to file a financial report in some

specific situations.

Reporting Entity

An entity or a company where it is practical to assume that the users somehow get

dependent on a specific report that is General Purpose Financial Report. This provides the

user to have a proper understanding of the position of the company and know the

performance of the company. So that the user will take a better decision for themselves based

on these financial report. Such an entity is termed as the Reporting entity.

Implications respect to Compliance and Reporting

o Small Proprietary Company:

These companies are the one who satisfies with any two conditions mentioned within

“Section 45A (2)”. The conditions are:

a. The combined operating profits are less than $25 million within that financial year

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.