Corporate and Financial Accounting Assignment Report, Holmes Institute

VerifiedAdded on 2022/12/27

|10

|2960

|78

Report

AI Summary

This report provides a comprehensive analysis of the equity and liability sections of BHP Billiton and Fortescue Metals Group Ltd over a three-year period (2017-2019). It examines the components of owner's equity, including contributed equity, reserves, treasury shares, retained earnings, and non-controlling interests, along with their movements. The liability section is also thoroughly examined, including trade payables, deferred income, borrowings, provisions, and tax liabilities. The report compares the financial performance of the two companies, highlighting changes in equity and liability values. Furthermore, it discusses the advantages and disadvantages of various funding sources, such as shares, debt, preference shares, and debentures, for each company. Finally, it analyzes the reporting and compliance implications for small proprietary, large proprietary, and reporting entities. This report demonstrates an understanding of financial accounting principles and the application of these principles in real-world scenarios.

Running head: CORPORATE AND FINANCIAL ACCOUNTING

Corporate and Financial Accounting

Student Name:

Student Number:

Authors Note:

Corporate and Financial Accounting

Student Name:

Student Number:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE AND FINANCIAL ACCOUNTING

Abstract:

The assessment directly helps in understanding the overall equity and liability

section of BHP Billiton and Fortescue Metals Group Ltd for a period of 3 years. The

relevant reporting requirements adequately analyzed for each type of companies to

detect its impact on their ability to present their financial strength. The analysis has

relatively helped in identifying the overall sources of finance that is used by both the

organizations in their annual report. In addition, adequate information has been

conducted on the types of equity components and liability components that are used

by the organization in their annual report. The process has helped in understanding

the actual performance of both the organization during the period of 2017 to 2019.

Abstract:

The assessment directly helps in understanding the overall equity and liability

section of BHP Billiton and Fortescue Metals Group Ltd for a period of 3 years. The

relevant reporting requirements adequately analyzed for each type of companies to

detect its impact on their ability to present their financial strength. The analysis has

relatively helped in identifying the overall sources of finance that is used by both the

organizations in their annual report. In addition, adequate information has been

conducted on the types of equity components and liability components that are used

by the organization in their annual report. The process has helped in understanding

the actual performance of both the organization during the period of 2017 to 2019.

CORPORATE AND FINANCIAL ACCOUNTING

Table of Contents

Introduction:..................................................................................................................3

Part A:...........................................................................................................................3

i) Explaining about the each item recorded under the owner equity section:..............3

ii) Explaining about the movement in each item recorded under the owner equity

section:..........................................................................................................................3

iii) Explaining the understanding of each items recorded under the liability section:...4

iv) Explaining about the movement in each item recorded under the liability section: 5

v) Explaining the relative advantages or disadvantages of each sources of fund each

selected by the organization:........................................................................................6

Part B:...........................................................................................................................7

Analyzing the implications of being classified as the three types of companies in

terms of compliance and reporting requirements:........................................................7

Conclusion:...................................................................................................................7

References and Bibliography:......................................................................................9

Table of Contents

Introduction:..................................................................................................................3

Part A:...........................................................................................................................3

i) Explaining about the each item recorded under the owner equity section:..............3

ii) Explaining about the movement in each item recorded under the owner equity

section:..........................................................................................................................3

iii) Explaining the understanding of each items recorded under the liability section:...4

iv) Explaining about the movement in each item recorded under the liability section: 5

v) Explaining the relative advantages or disadvantages of each sources of fund each

selected by the organization:........................................................................................6

Part B:...........................................................................................................................7

Analyzing the implications of being classified as the three types of companies in

terms of compliance and reporting requirements:........................................................7

Conclusion:...................................................................................................................7

References and Bibliography:......................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE AND FINANCIAL ACCOUNTING

Introduction:

The analysis selectively helps in evaluating the latest annual reports of the

organization for a period of 3 years to identify the relevant changes in its owners’

equity and liabilities section. The advantages and disadvantages from the relevant

sources of funds that are used by the companies are also evaluated to help in

detecting current capital structure whether it is sufficient for the organization. In

addition, the analysis continues with the detection of the relevant implication that is

faced by small proprietary company, large proprietary company and reporting entity

while preparing their financial report.

Part A:

i) Explaining about the each item recorded under the owner equity section:

The analyses of the items recorded under the owner’s equity section are

depicted as follows.

Contributed equity: Contribution equity is the overall issue capital that is acquired

by the organization after selling its shares in the capital market. The contributed

equity relatively comprises of all the shares that is valued at issue price and listed in

the capital market.

Reserves: Reserves are the overall savings that is conducted by the organization

over the period of time for a specific requirement. Reserves are the credit balance

that is referred to the part of shareholders equity and is considered a liability ( Vogel

2014).

Treasury shares: Treasury stocks are relatively considered a contract entry item,

which reflects the difference between the number of shares issued and the number

of shares outstanding for an organization. Therefore, when an organization holds the

treasury stock a debit balance in the general ledger account, which accounts for the

treasure stock.

Retained earnings: Retained earnings are the overall savings that is conducted by

the organization after declaring dividend to the shareholders. Retained earnings are

maintained by the organization to effectively reduce the negative impact of

unforeseen circumstances and support future projects (Williams and Dobelman

2017).

Non-controlling interest: Non-controlling interest are also known as the minority

interest where the ownership position is less than 50% of the outstanding shares

while shareholders does not have any kind of control over the decisions made by the

management.

ii) Explaining about the movement in each item recorded under the owner

equity section:

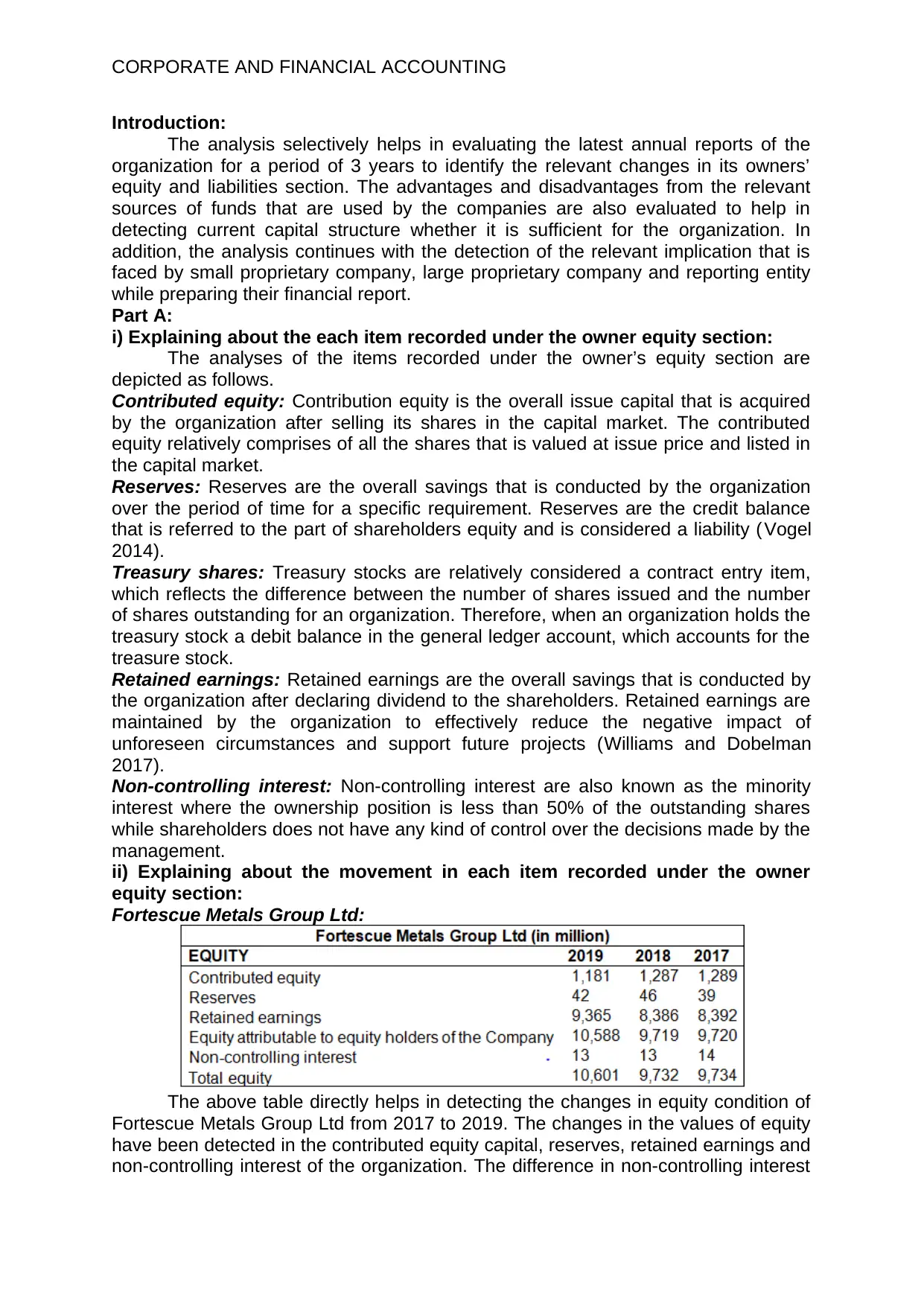

Fortescue Metals Group Ltd:

The above table directly helps in detecting the changes in equity condition of

Fortescue Metals Group Ltd from 2017 to 2019. The changes in the values of equity

have been detected in the contributed equity capital, reserves, retained earnings and

non-controlling interest of the organization. The difference in non-controlling interest

Introduction:

The analysis selectively helps in evaluating the latest annual reports of the

organization for a period of 3 years to identify the relevant changes in its owners’

equity and liabilities section. The advantages and disadvantages from the relevant

sources of funds that are used by the companies are also evaluated to help in

detecting current capital structure whether it is sufficient for the organization. In

addition, the analysis continues with the detection of the relevant implication that is

faced by small proprietary company, large proprietary company and reporting entity

while preparing their financial report.

Part A:

i) Explaining about the each item recorded under the owner equity section:

The analyses of the items recorded under the owner’s equity section are

depicted as follows.

Contributed equity: Contribution equity is the overall issue capital that is acquired

by the organization after selling its shares in the capital market. The contributed

equity relatively comprises of all the shares that is valued at issue price and listed in

the capital market.

Reserves: Reserves are the overall savings that is conducted by the organization

over the period of time for a specific requirement. Reserves are the credit balance

that is referred to the part of shareholders equity and is considered a liability ( Vogel

2014).

Treasury shares: Treasury stocks are relatively considered a contract entry item,

which reflects the difference between the number of shares issued and the number

of shares outstanding for an organization. Therefore, when an organization holds the

treasury stock a debit balance in the general ledger account, which accounts for the

treasure stock.

Retained earnings: Retained earnings are the overall savings that is conducted by

the organization after declaring dividend to the shareholders. Retained earnings are

maintained by the organization to effectively reduce the negative impact of

unforeseen circumstances and support future projects (Williams and Dobelman

2017).

Non-controlling interest: Non-controlling interest are also known as the minority

interest where the ownership position is less than 50% of the outstanding shares

while shareholders does not have any kind of control over the decisions made by the

management.

ii) Explaining about the movement in each item recorded under the owner

equity section:

Fortescue Metals Group Ltd:

The above table directly helps in detecting the changes in equity condition of

Fortescue Metals Group Ltd from 2017 to 2019. The changes in the values of equity

have been detected in the contributed equity capital, reserves, retained earnings and

non-controlling interest of the organization. The difference in non-controlling interest

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE AND FINANCIAL ACCOUNTING

and reserves are relatively negligible, as the overall values differed from 1 million to

7 million Australian dollars (Fmgl.com.au 2019). However, the contributed equity and

the retained earnings of the organization portrayed the significant changes in the

values of the equity. The values of contributed equity relatively declined by more

than 100 million while the retained earnings increased by more than 1,000 million

Australian dollars.

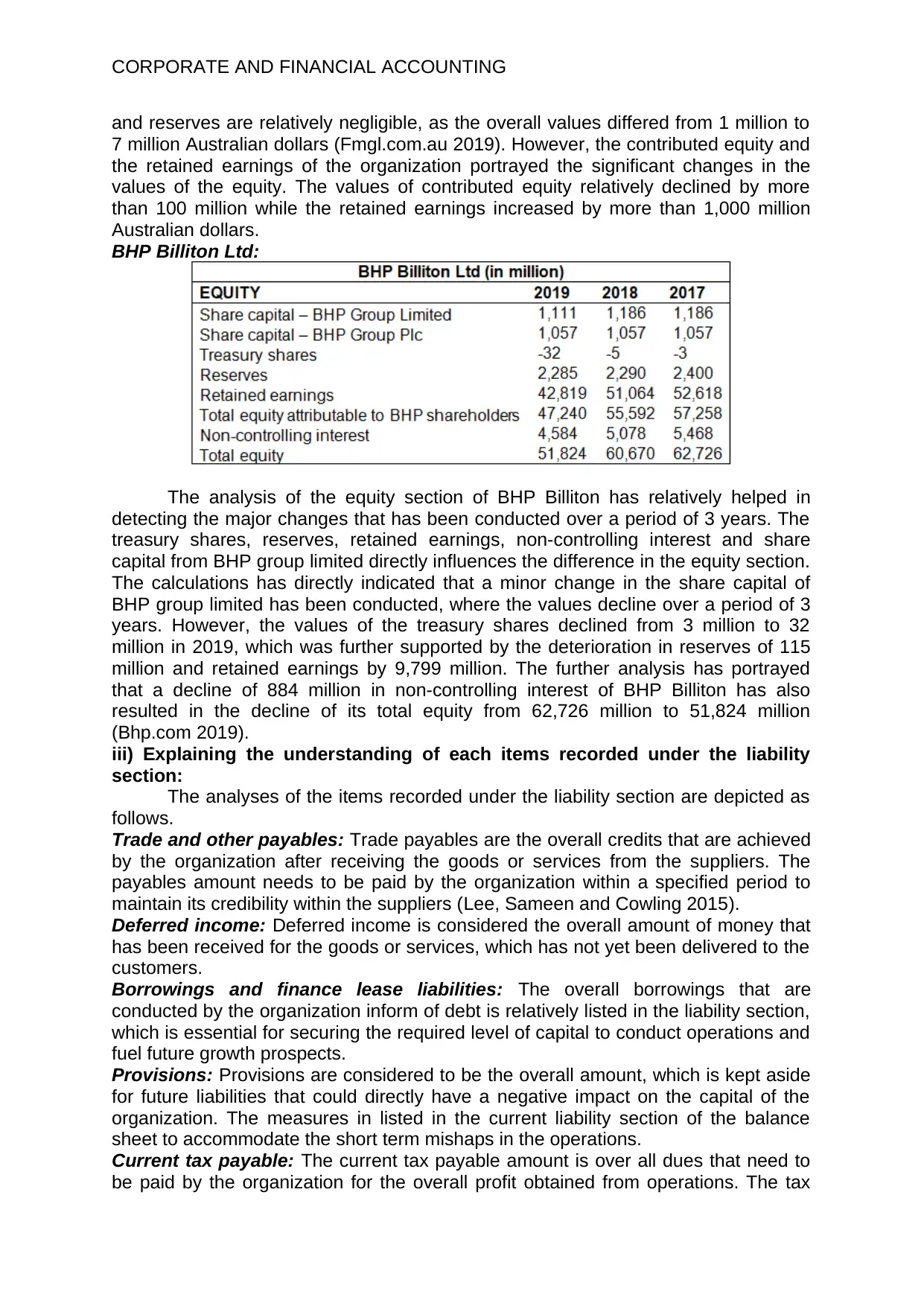

BHP Billiton Ltd:

The analysis of the equity section of BHP Billiton has relatively helped in

detecting the major changes that has been conducted over a period of 3 years. The

treasury shares, reserves, retained earnings, non-controlling interest and share

capital from BHP group limited directly influences the difference in the equity section.

The calculations has directly indicated that a minor change in the share capital of

BHP group limited has been conducted, where the values decline over a period of 3

years. However, the values of the treasury shares declined from 3 million to 32

million in 2019, which was further supported by the deterioration in reserves of 115

million and retained earnings by 9,799 million. The further analysis has portrayed

that a decline of 884 million in non-controlling interest of BHP Billiton has also

resulted in the decline of its total equity from 62,726 million to 51,824 million

(Bhp.com 2019).

iii) Explaining the understanding of each items recorded under the liability

section:

The analyses of the items recorded under the liability section are depicted as

follows.

Trade and other payables: Trade payables are the overall credits that are achieved

by the organization after receiving the goods or services from the suppliers. The

payables amount needs to be paid by the organization within a specified period to

maintain its credibility within the suppliers (Lee, Sameen and Cowling 2015).

Deferred income: Deferred income is considered the overall amount of money that

has been received for the goods or services, which has not yet been delivered to the

customers.

Borrowings and finance lease liabilities: The overall borrowings that are

conducted by the organization inform of debt is relatively listed in the liability section,

which is essential for securing the required level of capital to conduct operations and

fuel future growth prospects.

Provisions: Provisions are considered to be the overall amount, which is kept aside

for future liabilities that could directly have a negative impact on the capital of the

organization. The measures in listed in the current liability section of the balance

sheet to accommodate the short term mishaps in the operations.

Current tax payable: The current tax payable amount is over all dues that need to

be paid by the organization for the overall profit obtained from operations. The tax

and reserves are relatively negligible, as the overall values differed from 1 million to

7 million Australian dollars (Fmgl.com.au 2019). However, the contributed equity and

the retained earnings of the organization portrayed the significant changes in the

values of the equity. The values of contributed equity relatively declined by more

than 100 million while the retained earnings increased by more than 1,000 million

Australian dollars.

BHP Billiton Ltd:

The analysis of the equity section of BHP Billiton has relatively helped in

detecting the major changes that has been conducted over a period of 3 years. The

treasury shares, reserves, retained earnings, non-controlling interest and share

capital from BHP group limited directly influences the difference in the equity section.

The calculations has directly indicated that a minor change in the share capital of

BHP group limited has been conducted, where the values decline over a period of 3

years. However, the values of the treasury shares declined from 3 million to 32

million in 2019, which was further supported by the deterioration in reserves of 115

million and retained earnings by 9,799 million. The further analysis has portrayed

that a decline of 884 million in non-controlling interest of BHP Billiton has also

resulted in the decline of its total equity from 62,726 million to 51,824 million

(Bhp.com 2019).

iii) Explaining the understanding of each items recorded under the liability

section:

The analyses of the items recorded under the liability section are depicted as

follows.

Trade and other payables: Trade payables are the overall credits that are achieved

by the organization after receiving the goods or services from the suppliers. The

payables amount needs to be paid by the organization within a specified period to

maintain its credibility within the suppliers (Lee, Sameen and Cowling 2015).

Deferred income: Deferred income is considered the overall amount of money that

has been received for the goods or services, which has not yet been delivered to the

customers.

Borrowings and finance lease liabilities: The overall borrowings that are

conducted by the organization inform of debt is relatively listed in the liability section,

which is essential for securing the required level of capital to conduct operations and

fuel future growth prospects.

Provisions: Provisions are considered to be the overall amount, which is kept aside

for future liabilities that could directly have a negative impact on the capital of the

organization. The measures in listed in the current liability section of the balance

sheet to accommodate the short term mishaps in the operations.

Current tax payable: The current tax payable amount is over all dues that need to

be paid by the organization for the overall profit obtained from operations. The tax

CORPORATE AND FINANCIAL ACCOUNTING

liability is relatively calculated by detecting the overall transactions that has been

conducted by the company over the period of time (Carley and Spapens 2017).

Deferred tax liabilities: Deferred tax liability is an income that is an income from a

temporary difference between the book expense and the tax deduction that is

recorded in the balance sheet. Deferred tax liability can be considered and income

from the tax obligations of the organization, which will be paid in future accounting

period.

iv) Explaining about the movement in each item recorded under the liability

section:

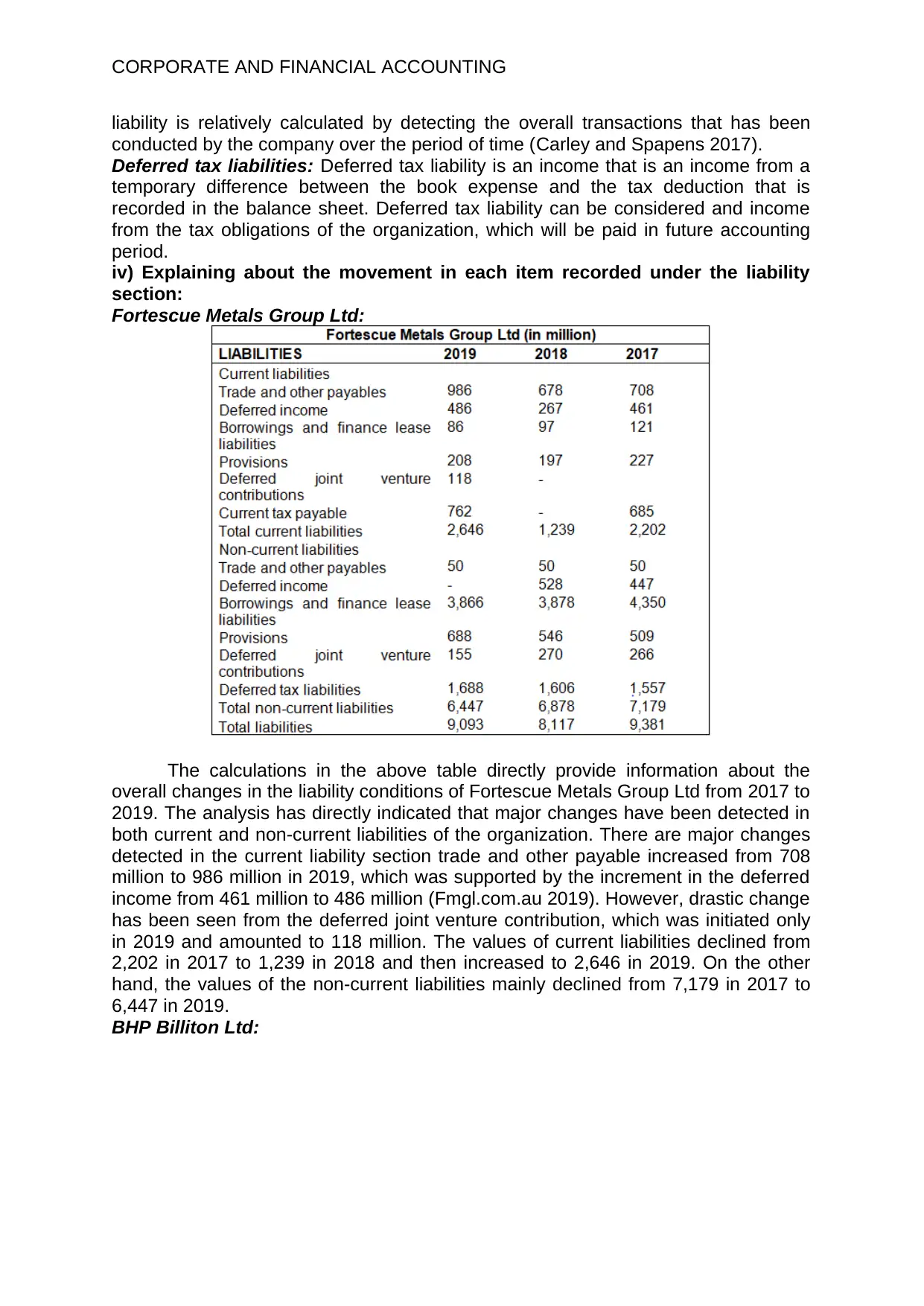

Fortescue Metals Group Ltd:

The calculations in the above table directly provide information about the

overall changes in the liability conditions of Fortescue Metals Group Ltd from 2017 to

2019. The analysis has directly indicated that major changes have been detected in

both current and non-current liabilities of the organization. There are major changes

detected in the current liability section trade and other payable increased from 708

million to 986 million in 2019, which was supported by the increment in the deferred

income from 461 million to 486 million (Fmgl.com.au 2019). However, drastic change

has been seen from the deferred joint venture contribution, which was initiated only

in 2019 and amounted to 118 million. The values of current liabilities declined from

2,202 in 2017 to 1,239 in 2018 and then increased to 2,646 in 2019. On the other

hand, the values of the non-current liabilities mainly declined from 7,179 in 2017 to

6,447 in 2019.

BHP Billiton Ltd:

liability is relatively calculated by detecting the overall transactions that has been

conducted by the company over the period of time (Carley and Spapens 2017).

Deferred tax liabilities: Deferred tax liability is an income that is an income from a

temporary difference between the book expense and the tax deduction that is

recorded in the balance sheet. Deferred tax liability can be considered and income

from the tax obligations of the organization, which will be paid in future accounting

period.

iv) Explaining about the movement in each item recorded under the liability

section:

Fortescue Metals Group Ltd:

The calculations in the above table directly provide information about the

overall changes in the liability conditions of Fortescue Metals Group Ltd from 2017 to

2019. The analysis has directly indicated that major changes have been detected in

both current and non-current liabilities of the organization. There are major changes

detected in the current liability section trade and other payable increased from 708

million to 986 million in 2019, which was supported by the increment in the deferred

income from 461 million to 486 million (Fmgl.com.au 2019). However, drastic change

has been seen from the deferred joint venture contribution, which was initiated only

in 2019 and amounted to 118 million. The values of current liabilities declined from

2,202 in 2017 to 1,239 in 2018 and then increased to 2,646 in 2019. On the other

hand, the values of the non-current liabilities mainly declined from 7,179 in 2017 to

6,447 in 2019.

BHP Billiton Ltd:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE AND FINANCIAL ACCOUNTING

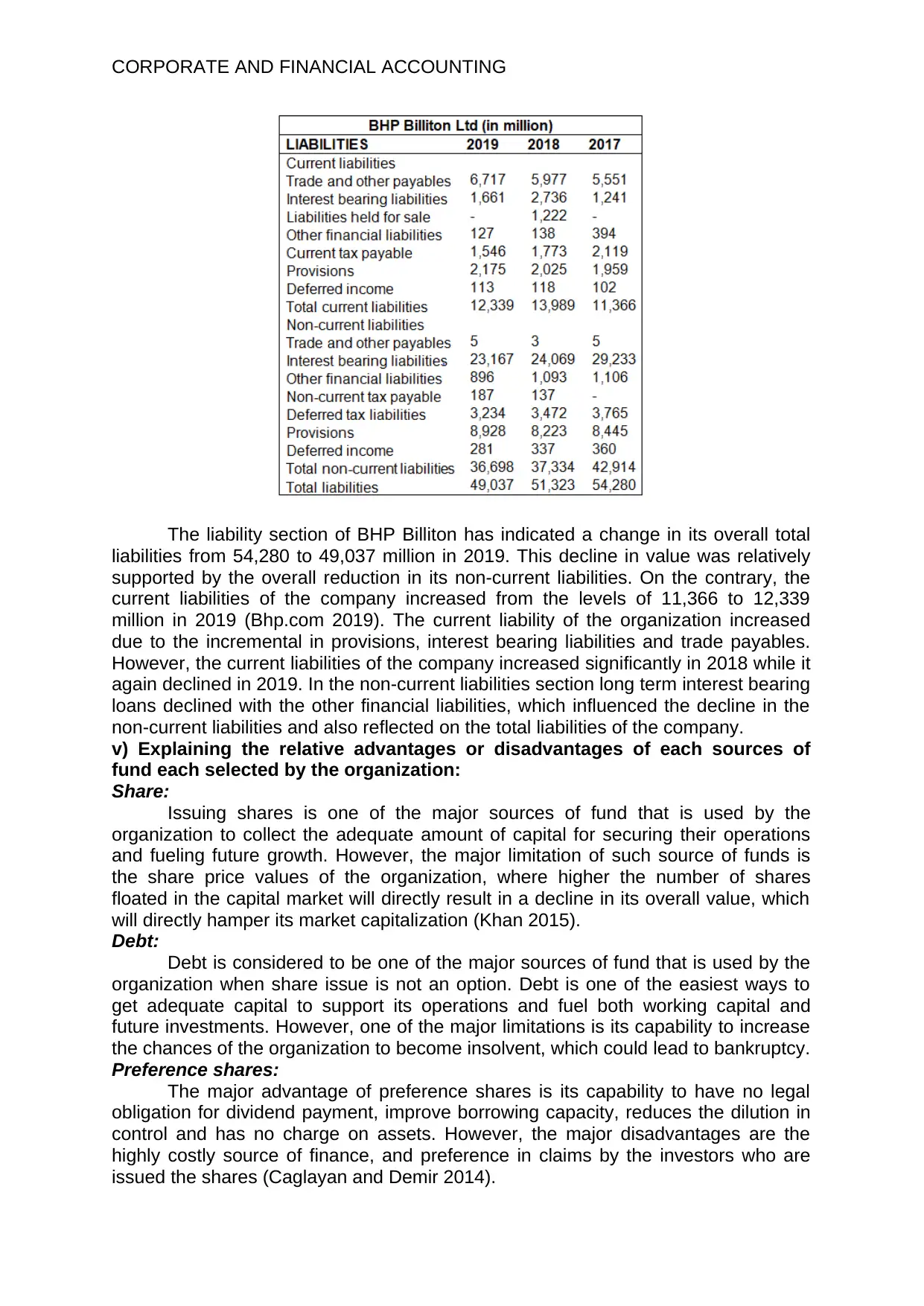

The liability section of BHP Billiton has indicated a change in its overall total

liabilities from 54,280 to 49,037 million in 2019. This decline in value was relatively

supported by the overall reduction in its non-current liabilities. On the contrary, the

current liabilities of the company increased from the levels of 11,366 to 12,339

million in 2019 (Bhp.com 2019). The current liability of the organization increased

due to the incremental in provisions, interest bearing liabilities and trade payables.

However, the current liabilities of the company increased significantly in 2018 while it

again declined in 2019. In the non-current liabilities section long term interest bearing

loans declined with the other financial liabilities, which influenced the decline in the

non-current liabilities and also reflected on the total liabilities of the company.

v) Explaining the relative advantages or disadvantages of each sources of

fund each selected by the organization:

Share:

Issuing shares is one of the major sources of fund that is used by the

organization to collect the adequate amount of capital for securing their operations

and fueling future growth. However, the major limitation of such source of funds is

the share price values of the organization, where higher the number of shares

floated in the capital market will directly result in a decline in its overall value, which

will directly hamper its market capitalization (Khan 2015).

Debt:

Debt is considered to be one of the major sources of fund that is used by the

organization when share issue is not an option. Debt is one of the easiest ways to

get adequate capital to support its operations and fuel both working capital and

future investments. However, one of the major limitations is its capability to increase

the chances of the organization to become insolvent, which could lead to bankruptcy.

Preference shares:

The major advantage of preference shares is its capability to have no legal

obligation for dividend payment, improve borrowing capacity, reduces the dilution in

control and has no charge on assets. However, the major disadvantages are the

highly costly source of finance, and preference in claims by the investors who are

issued the shares (Caglayan and Demir 2014).

The liability section of BHP Billiton has indicated a change in its overall total

liabilities from 54,280 to 49,037 million in 2019. This decline in value was relatively

supported by the overall reduction in its non-current liabilities. On the contrary, the

current liabilities of the company increased from the levels of 11,366 to 12,339

million in 2019 (Bhp.com 2019). The current liability of the organization increased

due to the incremental in provisions, interest bearing liabilities and trade payables.

However, the current liabilities of the company increased significantly in 2018 while it

again declined in 2019. In the non-current liabilities section long term interest bearing

loans declined with the other financial liabilities, which influenced the decline in the

non-current liabilities and also reflected on the total liabilities of the company.

v) Explaining the relative advantages or disadvantages of each sources of

fund each selected by the organization:

Share:

Issuing shares is one of the major sources of fund that is used by the

organization to collect the adequate amount of capital for securing their operations

and fueling future growth. However, the major limitation of such source of funds is

the share price values of the organization, where higher the number of shares

floated in the capital market will directly result in a decline in its overall value, which

will directly hamper its market capitalization (Khan 2015).

Debt:

Debt is considered to be one of the major sources of fund that is used by the

organization when share issue is not an option. Debt is one of the easiest ways to

get adequate capital to support its operations and fuel both working capital and

future investments. However, one of the major limitations is its capability to increase

the chances of the organization to become insolvent, which could lead to bankruptcy.

Preference shares:

The major advantage of preference shares is its capability to have no legal

obligation for dividend payment, improve borrowing capacity, reduces the dilution in

control and has no charge on assets. However, the major disadvantages are the

highly costly source of finance, and preference in claims by the investors who are

issued the shares (Caglayan and Demir 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE AND FINANCIAL ACCOUNTING

Debentures:

Debentures is mainly used by the organization when the capital requirement

is essential, as it helps in gathering the required capital in form of unsecured loan

certificate issued from the company. Debentures are considered a long term security

fixed interest rate for the investor, as the company has to comply even if adequate

profits are not made during the financial year.

Part B:

Analyzing the implications of being classified as the three types of companies

in terms of compliance and reporting requirements:

The implication on the three types of companies is depicted as follows.

Small proprietary company:

There are compliance and reporting requirements for small proprietary

companies in Australia where the management needs to obey with the following

requirements.

The company needs to prepare a financial report, which is in accordance with the

Corporation Act 2001. Thus, maintaining detailed accounts for minimizing the

occurrence of manipulations and unethical activities in the operations of the

organization (Asic.gov.au 2019).

The adequate auditing need to be conducted if the ASIC requests under the

Corporation Act to detect the financial condition of the organization. The

preparation of the financial report is essential, as it is required for providing

details regarding the transactions that were conducted in previous financial years.

Large proprietary company:

The compliance and reporting requirements for large proprietary companies

are depicted as follows.

The organization needs to have a consolidated revenue of more than 50 million

dollars for the financial year of the company.

Value of the consolidated gross assets for the end of the financial year needs to

be more than 25 million dollars.

Furthermore, the number of employees that is maintained by the organization

needs to be more than 100 (Asic.gov.au 2019).

The large proprietor companies must prepare and lodge financial report with the

director’s report in each financial year, where the account needs to be audited on

each year unless the ASIC grants relief for the company (Asic.gov.au 2019).

Reporting entity:

The compliance and reporting requirements for reporting entity are depicted

as follows.

The disclosing entity need to follow all the relevant sections of Corporation Act

2001 while preparing both the annual financial reports and half-yearly financial

reports (Asic.gov.au 2019).

The annual report needs to be prepared in accordance with chapter 2M of the

Corporation Act, while it needs to be audited and lodged with ASIC within 3

months of the financial year end and send to the members by the fourth month.

The half-yearly reports needs to be prepared and lodged within 75 days of the

half year end by the company and is subject to audit order as per the

requirements of ASIC (Asic.gov.au 2019).

Conclusion:

The assessment helps in determining the overall items that were recorded in

liability and equity section of the companies and the relevant changes that has been

conducted over a period of 3 years. The further examination has been conducted on

Debentures:

Debentures is mainly used by the organization when the capital requirement

is essential, as it helps in gathering the required capital in form of unsecured loan

certificate issued from the company. Debentures are considered a long term security

fixed interest rate for the investor, as the company has to comply even if adequate

profits are not made during the financial year.

Part B:

Analyzing the implications of being classified as the three types of companies

in terms of compliance and reporting requirements:

The implication on the three types of companies is depicted as follows.

Small proprietary company:

There are compliance and reporting requirements for small proprietary

companies in Australia where the management needs to obey with the following

requirements.

The company needs to prepare a financial report, which is in accordance with the

Corporation Act 2001. Thus, maintaining detailed accounts for minimizing the

occurrence of manipulations and unethical activities in the operations of the

organization (Asic.gov.au 2019).

The adequate auditing need to be conducted if the ASIC requests under the

Corporation Act to detect the financial condition of the organization. The

preparation of the financial report is essential, as it is required for providing

details regarding the transactions that were conducted in previous financial years.

Large proprietary company:

The compliance and reporting requirements for large proprietary companies

are depicted as follows.

The organization needs to have a consolidated revenue of more than 50 million

dollars for the financial year of the company.

Value of the consolidated gross assets for the end of the financial year needs to

be more than 25 million dollars.

Furthermore, the number of employees that is maintained by the organization

needs to be more than 100 (Asic.gov.au 2019).

The large proprietor companies must prepare and lodge financial report with the

director’s report in each financial year, where the account needs to be audited on

each year unless the ASIC grants relief for the company (Asic.gov.au 2019).

Reporting entity:

The compliance and reporting requirements for reporting entity are depicted

as follows.

The disclosing entity need to follow all the relevant sections of Corporation Act

2001 while preparing both the annual financial reports and half-yearly financial

reports (Asic.gov.au 2019).

The annual report needs to be prepared in accordance with chapter 2M of the

Corporation Act, while it needs to be audited and lodged with ASIC within 3

months of the financial year end and send to the members by the fourth month.

The half-yearly reports needs to be prepared and lodged within 75 days of the

half year end by the company and is subject to audit order as per the

requirements of ASIC (Asic.gov.au 2019).

Conclusion:

The assessment helps in determining the overall items that were recorded in

liability and equity section of the companies and the relevant changes that has been

conducted over a period of 3 years. The further examination has been conducted on

CORPORATE AND FINANCIAL ACCOUNTING

the advantages and disadvantages of the sources of finance used by the

organization, which tends to be essential while selecting an appropriate source of

capital. Furthermore, implications on each type of companies is also depicted for

supporting their reporting requirements as it helps the organization to put read the

financial condition in the annual report.

the advantages and disadvantages of the sources of finance used by the

organization, which tends to be essential while selecting an appropriate source of

capital. Furthermore, implications on each type of companies is also depicted for

supporting their reporting requirements as it helps the organization to put read the

financial condition in the annual report.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE AND FINANCIAL ACCOUNTING

References and Bibliography:

Asic.gov.au. 2019. Are you a large or small proprietary company | ASIC - Australian

Securities and Investments Commission . [online] Available at:

https://asic.gov.au/regulatory-resources/financial-reporting-and-audit/preparers-of-

financial-reports/are-you-a-large-or-small-proprietary-company/ [Accessed 24 Sep.

2019].

Asic.gov.au. 2019. Reporting obligations for disclosing entities | ASIC - Australian

Securities and Investments Commission . [online] Available at:

https://asic.gov.au/regulatory-resources/financial-reporting-and-audit/preparers-of-

financial-reports/reporting-obligations-for-disclosing-entities/ [Accessed 24 Sep.

2019].

Asic.gov.au. 2019. Small proprietary companies (not controlled by a foreign

company) where ASIC requests a financial report | ASIC - Australian Securities and

Investments Commission . [online] Available at: https://asic.gov.au/regulatory-

resources/financial-reporting-and-audit/preparers-of-financial-reports/small-

proprietary-companies/small-proprietary-companies-not-controlled-by-a-foreign-

company-where-asic-requests-a-financial-report/ [Accessed 24 Sep. 2019].

Bhp.com. 2019. [online] Available at:

https://www.bhp.com/-/media/documents/investors/annual-reports/2019/

bhpannualreport2019.pdf [Accessed 24 Sep. 2019].

Bhp.com. 2019. [online] Available at:

https://www.bhp.com/-/media/documents/investors/annual-reports/2018/

bhpannualreport2018.pdf [Accessed 24 Sep. 2019].

Caglayan, M. and Demir, F., 2014. Firm productivity, exchange rate movements,

sources of finance, and export orientation. World Development, 54, pp.204-219.

Carley, M. and Spapens, P., 2017. Sharing the world: sustainable living and global

equity in the 21st century. Routledge.

Fmgl.com.au. 2019. [online] Available at: https://www.fmgl.com.au/docs/default-

source/announcements/fy19-annual-report-including-appendix-4e.pdf?

sfvrsn=7a1c8a9a_7 [Accessed 24 Sep. 2019].

Fmgl.com.au. 2019. [online] Available at: https://www.fmgl.com.au/docs/default-

source/announcements/fy18-annual-report-including-appendix-4e.pdf?

sfvrsn=3137e4ae_8 [Accessed 24 Sep. 2019].

Khan, S., 2015. Impact of sources of finance on the growth of SMEs: evidence from

Pakistan. Decision, 42(1), pp.3-10.

Lee, N., Sameen, H. and Cowling, M., 2015. Access to finance for innovative SMEs

since the financial crisis. Research policy, 44(2), pp.370-380.

Morrell, P.S., 2018. Airline finance. Routledge.

Robinson, T.R., Henry, E., Pirie, W.L. and Broihahn, M.A., 2015. International

financial statement analysis. John Wiley & Sons.

Vogel, H.L., 2014. Entertainment industry economics: A guide for financial analysis.

Cambridge University Press.

Wahlen, J.M., Baginski, S.P. and Bradshaw, M., 2014. Financial reporting, financial

statement analysis and valuation. Nelson Education.

Williams, E.E. and Dobelman, J.A., 2017. Financial statement analysis. World

Scientific Book Chapters, pp.109-169.

References and Bibliography:

Asic.gov.au. 2019. Are you a large or small proprietary company | ASIC - Australian

Securities and Investments Commission . [online] Available at:

https://asic.gov.au/regulatory-resources/financial-reporting-and-audit/preparers-of-

financial-reports/are-you-a-large-or-small-proprietary-company/ [Accessed 24 Sep.

2019].

Asic.gov.au. 2019. Reporting obligations for disclosing entities | ASIC - Australian

Securities and Investments Commission . [online] Available at:

https://asic.gov.au/regulatory-resources/financial-reporting-and-audit/preparers-of-

financial-reports/reporting-obligations-for-disclosing-entities/ [Accessed 24 Sep.

2019].

Asic.gov.au. 2019. Small proprietary companies (not controlled by a foreign

company) where ASIC requests a financial report | ASIC - Australian Securities and

Investments Commission . [online] Available at: https://asic.gov.au/regulatory-

resources/financial-reporting-and-audit/preparers-of-financial-reports/small-

proprietary-companies/small-proprietary-companies-not-controlled-by-a-foreign-

company-where-asic-requests-a-financial-report/ [Accessed 24 Sep. 2019].

Bhp.com. 2019. [online] Available at:

https://www.bhp.com/-/media/documents/investors/annual-reports/2019/

bhpannualreport2019.pdf [Accessed 24 Sep. 2019].

Bhp.com. 2019. [online] Available at:

https://www.bhp.com/-/media/documents/investors/annual-reports/2018/

bhpannualreport2018.pdf [Accessed 24 Sep. 2019].

Caglayan, M. and Demir, F., 2014. Firm productivity, exchange rate movements,

sources of finance, and export orientation. World Development, 54, pp.204-219.

Carley, M. and Spapens, P., 2017. Sharing the world: sustainable living and global

equity in the 21st century. Routledge.

Fmgl.com.au. 2019. [online] Available at: https://www.fmgl.com.au/docs/default-

source/announcements/fy19-annual-report-including-appendix-4e.pdf?

sfvrsn=7a1c8a9a_7 [Accessed 24 Sep. 2019].

Fmgl.com.au. 2019. [online] Available at: https://www.fmgl.com.au/docs/default-

source/announcements/fy18-annual-report-including-appendix-4e.pdf?

sfvrsn=3137e4ae_8 [Accessed 24 Sep. 2019].

Khan, S., 2015. Impact of sources of finance on the growth of SMEs: evidence from

Pakistan. Decision, 42(1), pp.3-10.

Lee, N., Sameen, H. and Cowling, M., 2015. Access to finance for innovative SMEs

since the financial crisis. Research policy, 44(2), pp.370-380.

Morrell, P.S., 2018. Airline finance. Routledge.

Robinson, T.R., Henry, E., Pirie, W.L. and Broihahn, M.A., 2015. International

financial statement analysis. John Wiley & Sons.

Vogel, H.L., 2014. Entertainment industry economics: A guide for financial analysis.

Cambridge University Press.

Wahlen, J.M., Baginski, S.P. and Bradshaw, M., 2014. Financial reporting, financial

statement analysis and valuation. Nelson Education.

Williams, E.E. and Dobelman, J.A., 2017. Financial statement analysis. World

Scientific Book Chapters, pp.109-169.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.