ACCT2002 Corporate Accounting Assignment: Financial Analysis Report

VerifiedAdded on 2022/09/07

|8

|1418

|17

Report

AI Summary

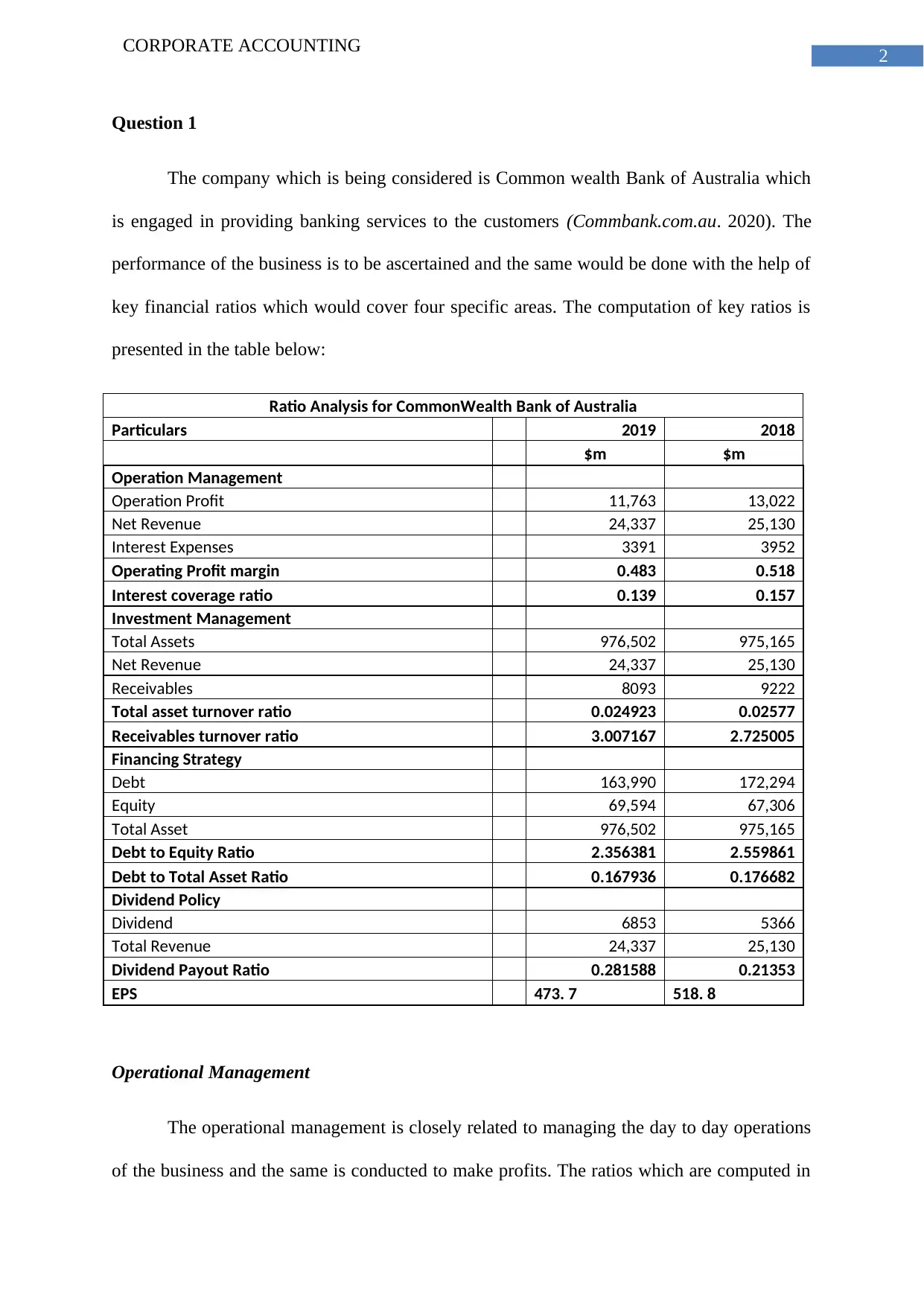

This report presents a detailed analysis of a corporate accounting assignment, focusing on the financial performance of Commonwealth Bank of Australia (CBA). The assignment includes a comprehensive ratio analysis covering operational management, investment management, financing strategy, and dividend policies. Key financial ratios such as operating profit margin, interest coverage ratio, total asset turnover ratio, debt-to-equity ratio, and dividend payout ratio are calculated and interpreted for the years 2018 and 2019. The report also addresses the business strategy of CBA, encompassing customer service, business banking, technology, and operational excellence. Furthermore, the assignment delves into consolidation processes, including journal entries, worksheet completion, and the preparation of consolidated financial statements. The analysis covers adjustments for plant and machinery valuation, depreciation, and pre-acquisition entries, demonstrating the student's understanding of consolidation principles and financial statement preparation. The assignment provides a practical application of accounting concepts and financial analysis techniques.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.