Corporate and Financial Reporting: ASX Companies Fund Analysis Report

VerifiedAdded on 2022/11/22

|15

|2817

|242

Report

AI Summary

This report provides a comprehensive analysis of corporate and financial reporting, focusing on the sources of funds and the classification of entities for reporting purposes. The report begins with an examination of the owner's equity section of two ASX-listed companies, Rio Tinto and Woolworths, over a three-year period. It defines and explains the components of owner's equity, including share capital, share premium, retained earnings, and reserves. The report then analyzes the movement of these items for each company, identifying trends and providing explanations for the changes. Next, the report investigates the liabilities section of the balance sheets for both companies, defining current and non-current liabilities. It analyzes the movement of these liabilities over the same three-year period, providing insights into the companies' financial strategies. The report then discusses the advantages and disadvantages of equity and debt financing. Finally, the report addresses the classification of companies, specifically defining a large proprietary company and its reporting requirements. The report uses the provided data to illustrate key financial concepts and provide a comparative analysis of the two companies' financial performance and strategies.

Running Head: CORPORATE AND FINANCIAL REPORTING

1

CORPORATE AND FINANCIAL REPORTING

1

CORPORATE AND FINANCIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: CORPORATE AND FINANCIAL REPORTING

Table of Contents

PART A......................................................................................................................................3

I) Items listed under the Owner’s Equity section of Rio and Woolworths............................3

Share Capital..........................................................................................................................3

Share Premium Account.........................................................................................................3

Retained Earnings...................................................................................................................3

Reserves..................................................................................................................................3

II) Movement of items of Rio (2018,2017, 2016)................................................................4

Movement of items of Woolworths Group (2018, 2017, 2016)................................................5

(iii) Items recorded under the Liabilities section of Rio and Woolworths.................................6

Current liabilities....................................................................................................................6

(iv) Movement of items of Rio (2018, 2017, 2016)...................................................................7

Movement of items of Woolworths (2018, 2017, 2016)............................................................8

Advantage and disadvantages....................................................................................................9

Pros of Equity.........................................................................................................................9

Cons of Equity........................................................................................................................9

Pros of Debt............................................................................................................................9

Cons of debt..........................................................................................................................10

PART B....................................................................................................................................10

Large proprietary company..................................................................................................10

Compliance and Reporting...................................................................................................10

Table of Contents

PART A......................................................................................................................................3

I) Items listed under the Owner’s Equity section of Rio and Woolworths............................3

Share Capital..........................................................................................................................3

Share Premium Account.........................................................................................................3

Retained Earnings...................................................................................................................3

Reserves..................................................................................................................................3

II) Movement of items of Rio (2018,2017, 2016)................................................................4

Movement of items of Woolworths Group (2018, 2017, 2016)................................................5

(iii) Items recorded under the Liabilities section of Rio and Woolworths.................................6

Current liabilities....................................................................................................................6

(iv) Movement of items of Rio (2018, 2017, 2016)...................................................................7

Movement of items of Woolworths (2018, 2017, 2016)............................................................8

Advantage and disadvantages....................................................................................................9

Pros of Equity.........................................................................................................................9

Cons of Equity........................................................................................................................9

Pros of Debt............................................................................................................................9

Cons of debt..........................................................................................................................10

PART B....................................................................................................................................10

Large proprietary company..................................................................................................10

Compliance and Reporting...................................................................................................10

Running Head: CORPORATE AND FINANCIAL REPORTING

Reporting and the non-reporting..........................................................................................11

Compliance and Reporting.......................................................................................................11

References................................................................................................................................12

Reporting and the non-reporting..........................................................................................11

Compliance and Reporting.......................................................................................................11

References................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: CORPORATE AND FINANCIAL REPORTING

PART A

I) Items listed under the Owner’s Equity section of Rio and Woolworths

Share Capital

The total capital of a company is distributed in the form of minimal units which are called

shares. Share capital is that part of the total capital that comes from the issue of the shares of

the company. In other words, capital represented by equity shares is called the share capital.

They represent the ownership position of a company (Lewis and Tan, 2016).

Share Premium Account

It indicates the difference between the par value of a share upon its issue and the total amount

received upon its subscription. The funds in the share premium account cannot be distributed

as dividends and can only be used for some specific purposes (Neilson, 2018).

Retained Earnings

Retained earnings (RE) is the amount of net income (profits) left over for the business after

the payments of its dividends has been duly made. They are an internal source of long- term

funds of an existing company and are readily available to the company (Ball, Gerakos,

Linnainmaa and Nikolaev, 2019).

Reserves

Reserves are a part of a company’s profits (Retained Earnings), which have been kept aside

to strengthen the financial position of the business, and to fulfil any losses that may arise in

future. Reserves are transferred after the payment of taxes has been done but before the

payment of dividends, whereas retained earnings are what is left after paying the dividends to

its shareholders (Bianchi, Hatchondo and Martinez, 2018).

PART A

I) Items listed under the Owner’s Equity section of Rio and Woolworths

Share Capital

The total capital of a company is distributed in the form of minimal units which are called

shares. Share capital is that part of the total capital that comes from the issue of the shares of

the company. In other words, capital represented by equity shares is called the share capital.

They represent the ownership position of a company (Lewis and Tan, 2016).

Share Premium Account

It indicates the difference between the par value of a share upon its issue and the total amount

received upon its subscription. The funds in the share premium account cannot be distributed

as dividends and can only be used for some specific purposes (Neilson, 2018).

Retained Earnings

Retained earnings (RE) is the amount of net income (profits) left over for the business after

the payments of its dividends has been duly made. They are an internal source of long- term

funds of an existing company and are readily available to the company (Ball, Gerakos,

Linnainmaa and Nikolaev, 2019).

Reserves

Reserves are a part of a company’s profits (Retained Earnings), which have been kept aside

to strengthen the financial position of the business, and to fulfil any losses that may arise in

future. Reserves are transferred after the payment of taxes has been done but before the

payment of dividends, whereas retained earnings are what is left after paying the dividends to

its shareholders (Bianchi, Hatchondo and Martinez, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: CORPORATE AND FINANCIAL REPORTING

Running Head: CORPORATE AND FINANCIAL REPORTING

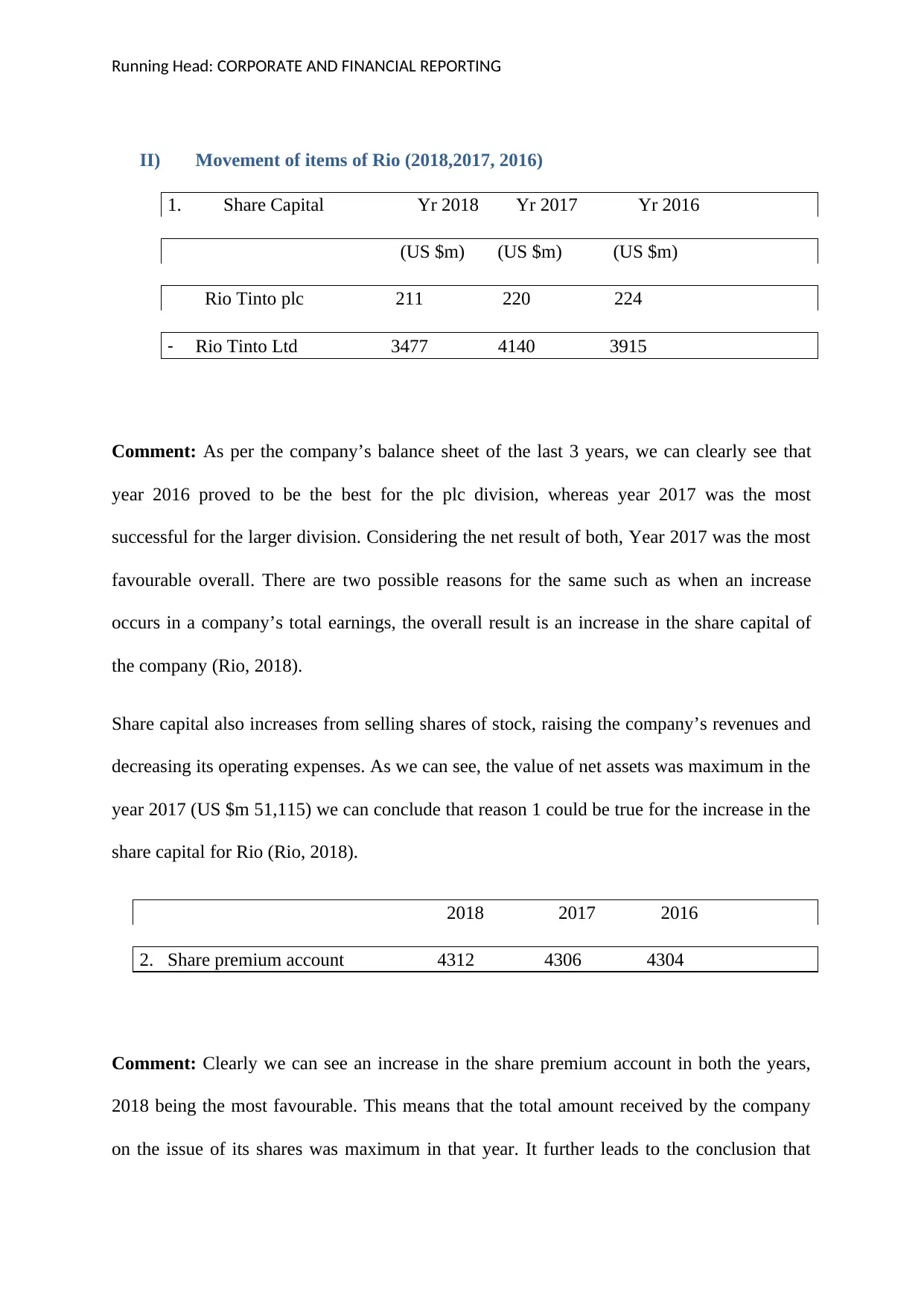

II) Movement of items of Rio (2018,2017, 2016)

1. Share Capital Yr 2018 Yr 2017 Yr 2016

(US $m) (US $m) (US $m)

Rio Tinto plc 211 220 224

- Rio Tinto Ltd 3477 4140 3915

Comment: As per the company’s balance sheet of the last 3 years, we can clearly see that

year 2016 proved to be the best for the plc division, whereas year 2017 was the most

successful for the larger division. Considering the net result of both, Year 2017 was the most

favourable overall. There are two possible reasons for the same such as when an increase

occurs in a company’s total earnings, the overall result is an increase in the share capital of

the company (Rio, 2018).

Share capital also increases from selling shares of stock, raising the company’s revenues and

decreasing its operating expenses. As we can see, the value of net assets was maximum in the

year 2017 (US $m 51,115) we can conclude that reason 1 could be true for the increase in the

share capital for Rio (Rio, 2018).

2018 2017 2016

2. Share premium account 4312 4306 4304

Comment: Clearly we can see an increase in the share premium account in both the years,

2018 being the most favourable. This means that the total amount received by the company

on the issue of its shares was maximum in that year. It further leads to the conclusion that

II) Movement of items of Rio (2018,2017, 2016)

1. Share Capital Yr 2018 Yr 2017 Yr 2016

(US $m) (US $m) (US $m)

Rio Tinto plc 211 220 224

- Rio Tinto Ltd 3477 4140 3915

Comment: As per the company’s balance sheet of the last 3 years, we can clearly see that

year 2016 proved to be the best for the plc division, whereas year 2017 was the most

successful for the larger division. Considering the net result of both, Year 2017 was the most

favourable overall. There are two possible reasons for the same such as when an increase

occurs in a company’s total earnings, the overall result is an increase in the share capital of

the company (Rio, 2018).

Share capital also increases from selling shares of stock, raising the company’s revenues and

decreasing its operating expenses. As we can see, the value of net assets was maximum in the

year 2017 (US $m 51,115) we can conclude that reason 1 could be true for the increase in the

share capital for Rio (Rio, 2018).

2018 2017 2016

2. Share premium account 4312 4306 4304

Comment: Clearly we can see an increase in the share premium account in both the years,

2018 being the most favourable. This means that the total amount received by the company

on the issue of its shares was maximum in that year. It further leads to the conclusion that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: CORPORATE AND FINANCIAL REPORTING

because of the exemplary performance by the company in 2017, the market value of its share

must have increased which earned them good return on their issued capital (Rio, 2018).

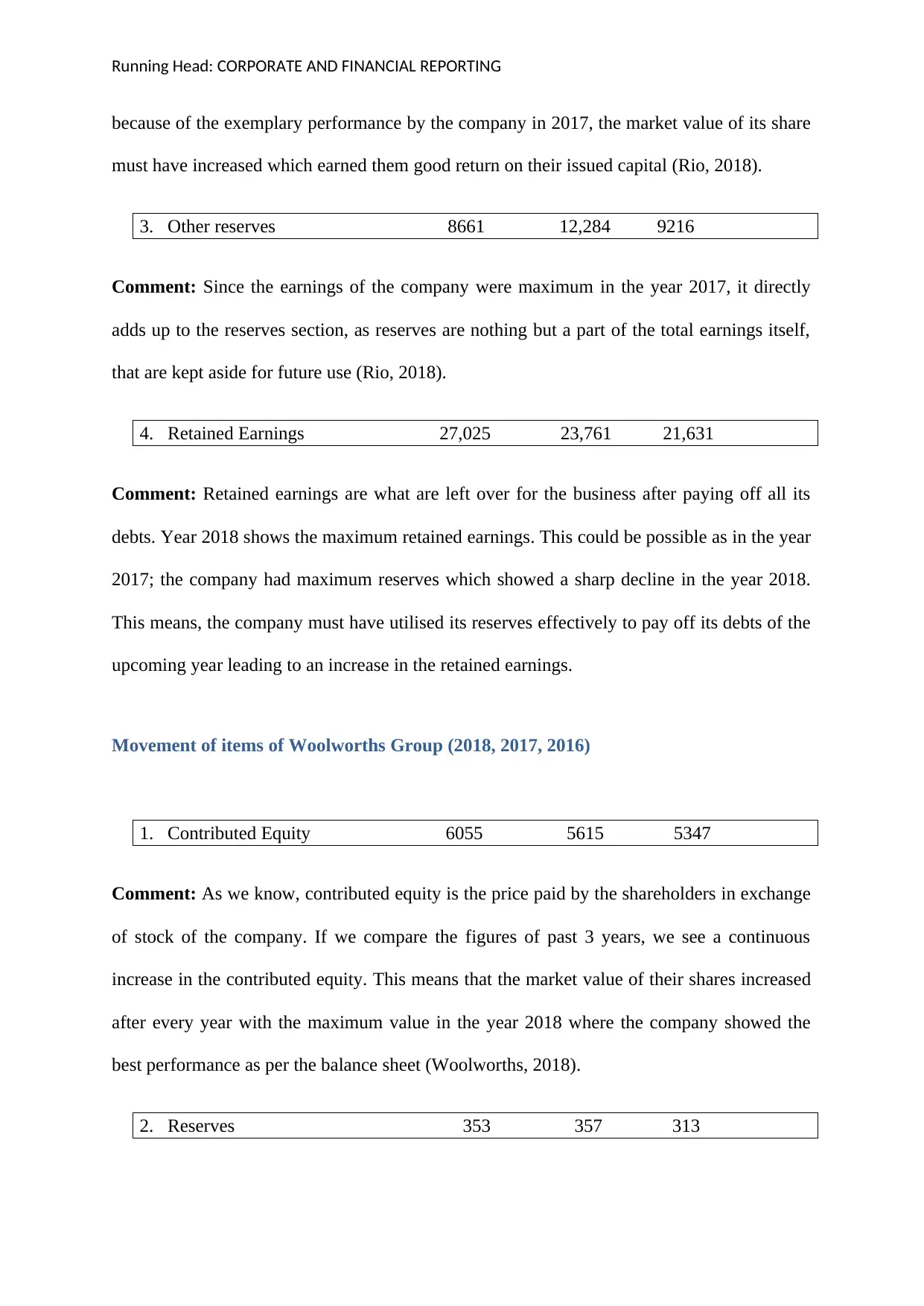

3. Other reserves 8661 12,284 9216

Comment: Since the earnings of the company were maximum in the year 2017, it directly

adds up to the reserves section, as reserves are nothing but a part of the total earnings itself,

that are kept aside for future use (Rio, 2018).

4. Retained Earnings 27,025 23,761 21,631

Comment: Retained earnings are what are left over for the business after paying off all its

debts. Year 2018 shows the maximum retained earnings. This could be possible as in the year

2017; the company had maximum reserves which showed a sharp decline in the year 2018.

This means, the company must have utilised its reserves effectively to pay off its debts of the

upcoming year leading to an increase in the retained earnings.

Movement of items of Woolworths Group (2018, 2017, 2016)

1. Contributed Equity 6055 5615 5347

Comment: As we know, contributed equity is the price paid by the shareholders in exchange

of stock of the company. If we compare the figures of past 3 years, we see a continuous

increase in the contributed equity. This means that the market value of their shares increased

after every year with the maximum value in the year 2018 where the company showed the

best performance as per the balance sheet (Woolworths, 2018).

2. Reserves 353 357 313

because of the exemplary performance by the company in 2017, the market value of its share

must have increased which earned them good return on their issued capital (Rio, 2018).

3. Other reserves 8661 12,284 9216

Comment: Since the earnings of the company were maximum in the year 2017, it directly

adds up to the reserves section, as reserves are nothing but a part of the total earnings itself,

that are kept aside for future use (Rio, 2018).

4. Retained Earnings 27,025 23,761 21,631

Comment: Retained earnings are what are left over for the business after paying off all its

debts. Year 2018 shows the maximum retained earnings. This could be possible as in the year

2017; the company had maximum reserves which showed a sharp decline in the year 2018.

This means, the company must have utilised its reserves effectively to pay off its debts of the

upcoming year leading to an increase in the retained earnings.

Movement of items of Woolworths Group (2018, 2017, 2016)

1. Contributed Equity 6055 5615 5347

Comment: As we know, contributed equity is the price paid by the shareholders in exchange

of stock of the company. If we compare the figures of past 3 years, we see a continuous

increase in the contributed equity. This means that the market value of their shares increased

after every year with the maximum value in the year 2018 where the company showed the

best performance as per the balance sheet (Woolworths, 2018).

2. Reserves 353 357 313

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: CORPORATE AND FINANCIAL REPORTING

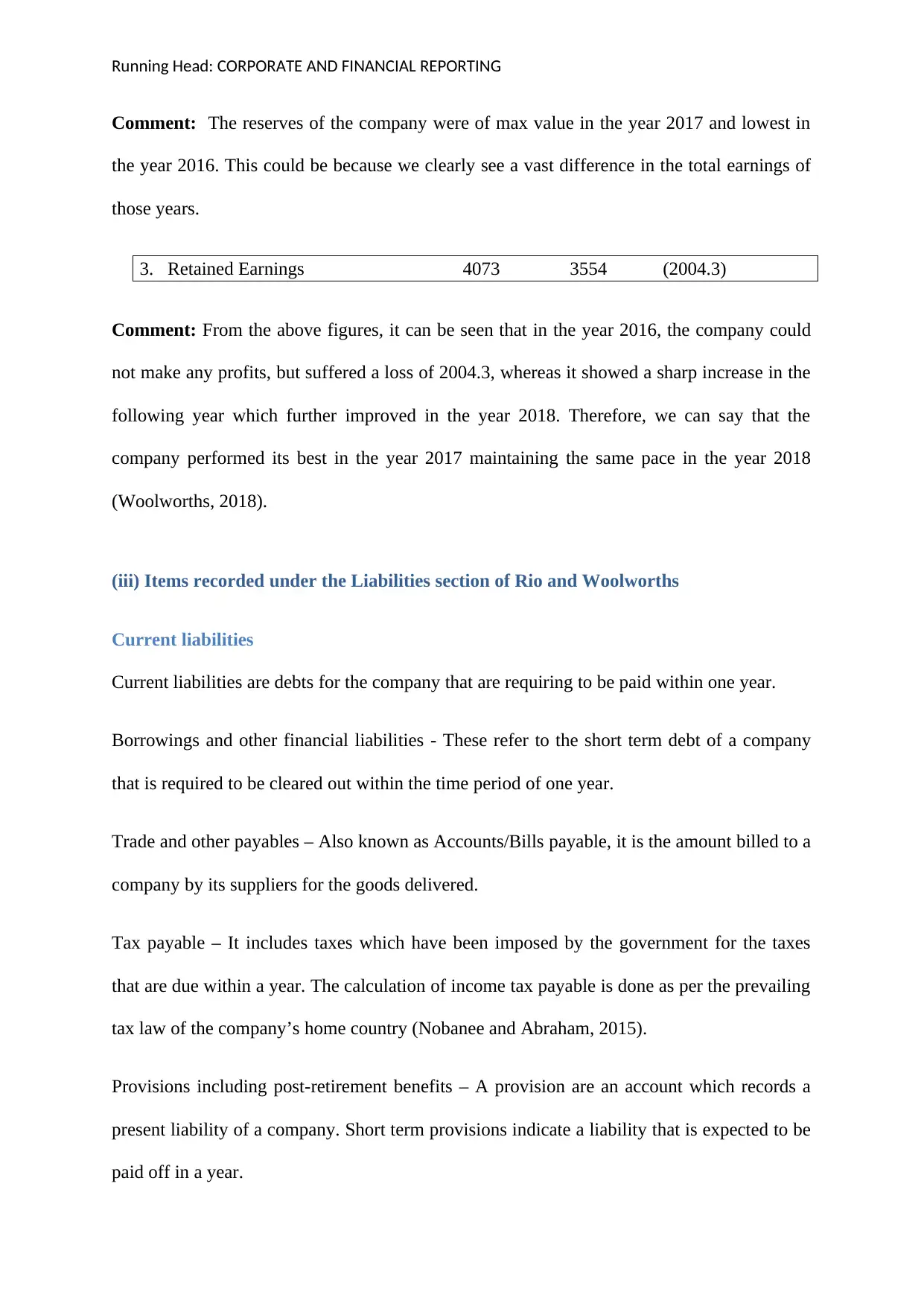

Comment: The reserves of the company were of max value in the year 2017 and lowest in

the year 2016. This could be because we clearly see a vast difference in the total earnings of

those years.

3. Retained Earnings 4073 3554 (2004.3)

Comment: From the above figures, it can be seen that in the year 2016, the company could

not make any profits, but suffered a loss of 2004.3, whereas it showed a sharp increase in the

following year which further improved in the year 2018. Therefore, we can say that the

company performed its best in the year 2017 maintaining the same pace in the year 2018

(Woolworths, 2018).

(iii) Items recorded under the Liabilities section of Rio and Woolworths

Current liabilities

Current liabilities are debts for the company that are requiring to be paid within one year.

Borrowings and other financial liabilities - These refer to the short term debt of a company

that is required to be cleared out within the time period of one year.

Trade and other payables – Also known as Accounts/Bills payable, it is the amount billed to a

company by its suppliers for the goods delivered.

Tax payable – It includes taxes which have been imposed by the government for the taxes

that are due within a year. The calculation of income tax payable is done as per the prevailing

tax law of the company’s home country (Nobanee and Abraham, 2015).

Provisions including post-retirement benefits – A provision are an account which records a

present liability of a company. Short term provisions indicate a liability that is expected to be

paid off in a year.

Comment: The reserves of the company were of max value in the year 2017 and lowest in

the year 2016. This could be because we clearly see a vast difference in the total earnings of

those years.

3. Retained Earnings 4073 3554 (2004.3)

Comment: From the above figures, it can be seen that in the year 2016, the company could

not make any profits, but suffered a loss of 2004.3, whereas it showed a sharp increase in the

following year which further improved in the year 2018. Therefore, we can say that the

company performed its best in the year 2017 maintaining the same pace in the year 2018

(Woolworths, 2018).

(iii) Items recorded under the Liabilities section of Rio and Woolworths

Current liabilities

Current liabilities are debts for the company that are requiring to be paid within one year.

Borrowings and other financial liabilities - These refer to the short term debt of a company

that is required to be cleared out within the time period of one year.

Trade and other payables – Also known as Accounts/Bills payable, it is the amount billed to a

company by its suppliers for the goods delivered.

Tax payable – It includes taxes which have been imposed by the government for the taxes

that are due within a year. The calculation of income tax payable is done as per the prevailing

tax law of the company’s home country (Nobanee and Abraham, 2015).

Provisions including post-retirement benefits – A provision are an account which records a

present liability of a company. Short term provisions indicate a liability that is expected to be

paid off in a year.

Running Head: CORPORATE AND FINANCIAL REPORTING

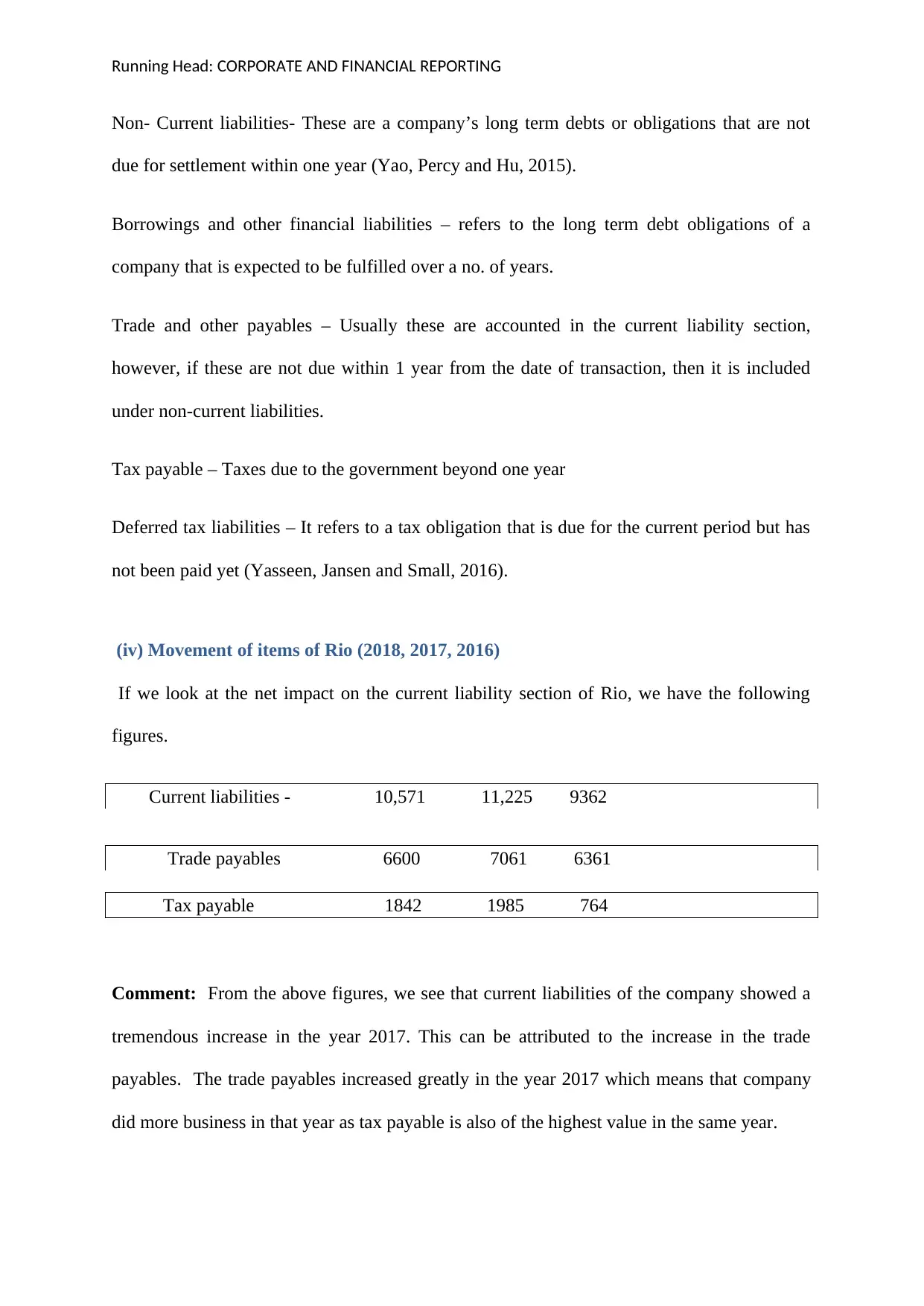

Non- Current liabilities- These are a company’s long term debts or obligations that are not

due for settlement within one year (Yao, Percy and Hu, 2015).

Borrowings and other financial liabilities – refers to the long term debt obligations of a

company that is expected to be fulfilled over a no. of years.

Trade and other payables – Usually these are accounted in the current liability section,

however, if these are not due within 1 year from the date of transaction, then it is included

under non-current liabilities.

Tax payable – Taxes due to the government beyond one year

Deferred tax liabilities – It refers to a tax obligation that is due for the current period but has

not been paid yet (Yasseen, Jansen and Small, 2016).

(iv) Movement of items of Rio (2018, 2017, 2016)

If we look at the net impact on the current liability section of Rio, we have the following

figures.

Current liabilities - 10,571 11,225 9362

Trade payables 6600 7061 6361

Tax payable 1842 1985 764

Comment: From the above figures, we see that current liabilities of the company showed a

tremendous increase in the year 2017. This can be attributed to the increase in the trade

payables. The trade payables increased greatly in the year 2017 which means that company

did more business in that year as tax payable is also of the highest value in the same year.

Non- Current liabilities- These are a company’s long term debts or obligations that are not

due for settlement within one year (Yao, Percy and Hu, 2015).

Borrowings and other financial liabilities – refers to the long term debt obligations of a

company that is expected to be fulfilled over a no. of years.

Trade and other payables – Usually these are accounted in the current liability section,

however, if these are not due within 1 year from the date of transaction, then it is included

under non-current liabilities.

Tax payable – Taxes due to the government beyond one year

Deferred tax liabilities – It refers to a tax obligation that is due for the current period but has

not been paid yet (Yasseen, Jansen and Small, 2016).

(iv) Movement of items of Rio (2018, 2017, 2016)

If we look at the net impact on the current liability section of Rio, we have the following

figures.

Current liabilities - 10,571 11,225 9362

Trade payables 6600 7061 6361

Tax payable 1842 1985 764

Comment: From the above figures, we see that current liabilities of the company showed a

tremendous increase in the year 2017. This can be attributed to the increase in the trade

payables. The trade payables increased greatly in the year 2017 which means that company

did more business in that year as tax payable is also of the highest value in the same year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: CORPORATE AND FINANCIAL REPORTING

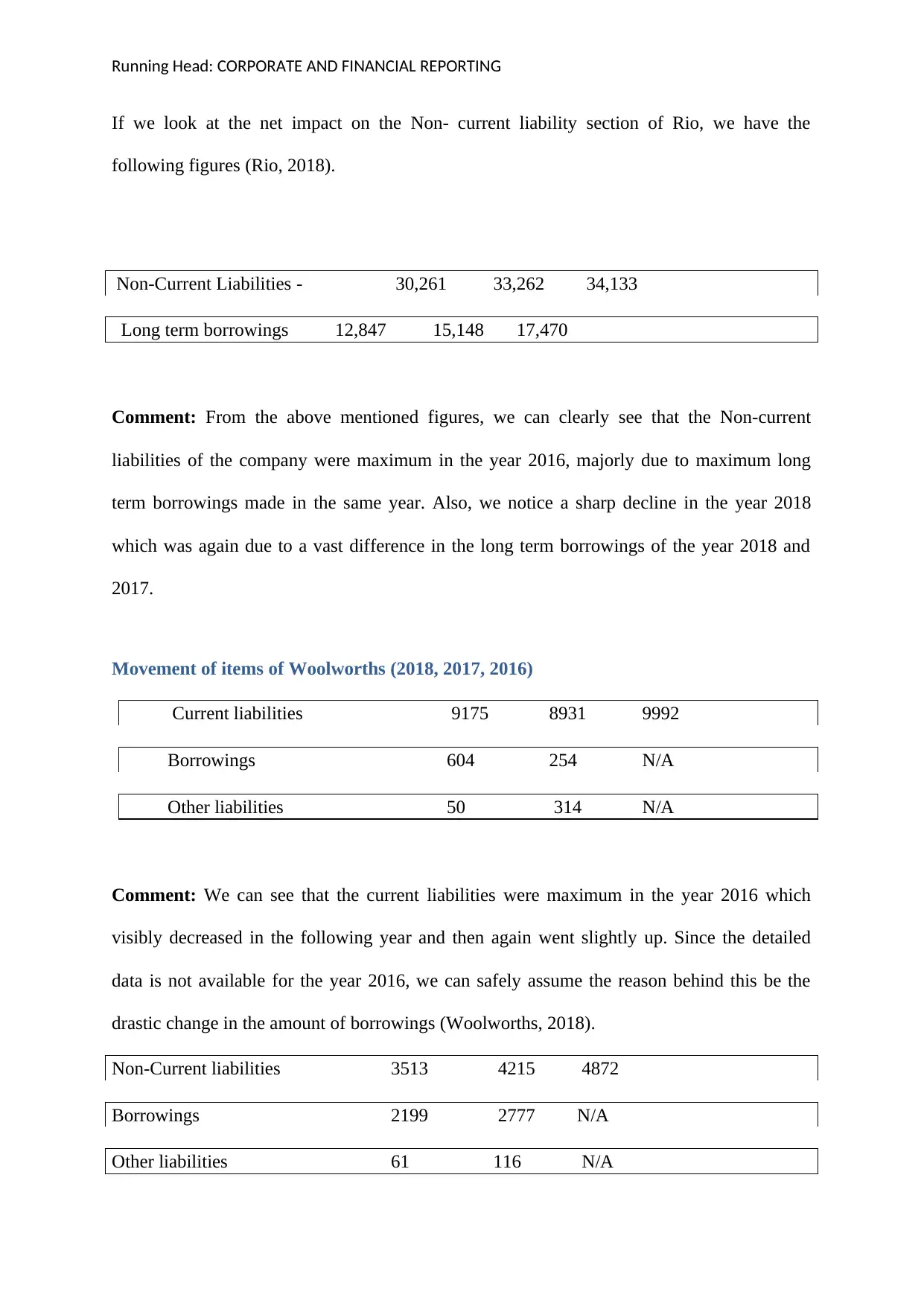

If we look at the net impact on the Non- current liability section of Rio, we have the

following figures (Rio, 2018).

Non-Current Liabilities - 30,261 33,262 34,133

Long term borrowings 12,847 15,148 17,470

Comment: From the above mentioned figures, we can clearly see that the Non-current

liabilities of the company were maximum in the year 2016, majorly due to maximum long

term borrowings made in the same year. Also, we notice a sharp decline in the year 2018

which was again due to a vast difference in the long term borrowings of the year 2018 and

2017.

Movement of items of Woolworths (2018, 2017, 2016)

Current liabilities 9175 8931 9992

Borrowings 604 254 N/A

Other liabilities 50 314 N/A

Comment: We can see that the current liabilities were maximum in the year 2016 which

visibly decreased in the following year and then again went slightly up. Since the detailed

data is not available for the year 2016, we can safely assume the reason behind this be the

drastic change in the amount of borrowings (Woolworths, 2018).

Non-Current liabilities 3513 4215 4872

Borrowings 2199 2777 N/A

Other liabilities 61 116 N/A

If we look at the net impact on the Non- current liability section of Rio, we have the

following figures (Rio, 2018).

Non-Current Liabilities - 30,261 33,262 34,133

Long term borrowings 12,847 15,148 17,470

Comment: From the above mentioned figures, we can clearly see that the Non-current

liabilities of the company were maximum in the year 2016, majorly due to maximum long

term borrowings made in the same year. Also, we notice a sharp decline in the year 2018

which was again due to a vast difference in the long term borrowings of the year 2018 and

2017.

Movement of items of Woolworths (2018, 2017, 2016)

Current liabilities 9175 8931 9992

Borrowings 604 254 N/A

Other liabilities 50 314 N/A

Comment: We can see that the current liabilities were maximum in the year 2016 which

visibly decreased in the following year and then again went slightly up. Since the detailed

data is not available for the year 2016, we can safely assume the reason behind this be the

drastic change in the amount of borrowings (Woolworths, 2018).

Non-Current liabilities 3513 4215 4872

Borrowings 2199 2777 N/A

Other liabilities 61 116 N/A

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: CORPORATE AND FINANCIAL REPORTING

Comment: We see a similar fashion in the values of Non-current liabilities as well. Since the

complete data is not available, we can safely assume that whatever changes took place in the

Non-current liabilities were mainly due to the changes in the borrowings.

Advantage and disadvantages

Generally the sources of funds that are used by the Rio and Woolworths have been equity and

debt either in the form of short -term or in the form of long term nature. Further the

advantages as well as disadvantages have been listed below.

Pros of Equity

There is a less risk associated with the equity share capital as the fixed instalment of

the interest is not required to be paid.

Equity share capital is beneficial for the start-up companies which are not having

much income in the starting to proceed with the business.

Equity financing keeps the assets of the company to run the operations of the business

(Lewis and Tan, 2016).

Cons of Equity

Under the equity method the owner has to leave the ownership and control when the

funds take on extra financial specialists. The equity shareholders are given the returns

only after the debenture holder are paid off.

Pros of Debt

The relationship with the debenture holders is such that the relationship gets over

when the maturity of the debentures occurs. The loan specialist doesn't have any state

in how the proprietor maintains his business.

Comment: We see a similar fashion in the values of Non-current liabilities as well. Since the

complete data is not available, we can safely assume that whatever changes took place in the

Non-current liabilities were mainly due to the changes in the borrowings.

Advantage and disadvantages

Generally the sources of funds that are used by the Rio and Woolworths have been equity and

debt either in the form of short -term or in the form of long term nature. Further the

advantages as well as disadvantages have been listed below.

Pros of Equity

There is a less risk associated with the equity share capital as the fixed instalment of

the interest is not required to be paid.

Equity share capital is beneficial for the start-up companies which are not having

much income in the starting to proceed with the business.

Equity financing keeps the assets of the company to run the operations of the business

(Lewis and Tan, 2016).

Cons of Equity

Under the equity method the owner has to leave the ownership and control when the

funds take on extra financial specialists. The equity shareholders are given the returns

only after the debenture holder are paid off.

Pros of Debt

The relationship with the debenture holders is such that the relationship gets over

when the maturity of the debentures occurs. The loan specialist doesn't have any state

in how the proprietor maintains his business.

Running Head: CORPORATE AND FINANCIAL REPORTING

Loan interest is charge deductible, while extra profits paid to investors are most

certainly not (Lewis and Tan, 2016).

Cons of debt

When most of the funds are acquired through debt than in that case the financial

burden or leverage increases and the financial specialists makes it aware that the risk

is higher than expected.

Lenders will commonly request that necessary items of the company be held as

security, and it is the duty of the proprietor to frequently record the advances.

PART B

Small proprietary company is the company that are not able to meet the requirements

stipulated for the large proprietary companies.

Large proprietary company

A company can be classified as the large proprietary company when it tech basically satisfies

the two major criteria than such company can be entitled to large proprietary company.

The conditions are consolidated revenue for the financial year of the organization and

any elements it controls is $50 at least million.

The estimation of the united gross resources toward the part of the arrangement year

of the organization and any elements it controls is $25 at least million, and

The organization and any substances it controls have at least 100 representatives

toward the part of the bargain year.

Compliance and Reporting

The companies are required to file a financial as well as director’s report. The accounts are

compulsorily required to be audited, unless the grant is received by ASIC.

Loan interest is charge deductible, while extra profits paid to investors are most

certainly not (Lewis and Tan, 2016).

Cons of debt

When most of the funds are acquired through debt than in that case the financial

burden or leverage increases and the financial specialists makes it aware that the risk

is higher than expected.

Lenders will commonly request that necessary items of the company be held as

security, and it is the duty of the proprietor to frequently record the advances.

PART B

Small proprietary company is the company that are not able to meet the requirements

stipulated for the large proprietary companies.

Large proprietary company

A company can be classified as the large proprietary company when it tech basically satisfies

the two major criteria than such company can be entitled to large proprietary company.

The conditions are consolidated revenue for the financial year of the organization and

any elements it controls is $50 at least million.

The estimation of the united gross resources toward the part of the arrangement year

of the organization and any elements it controls is $25 at least million, and

The organization and any substances it controls have at least 100 representatives

toward the part of the bargain year.

Compliance and Reporting

The companies are required to file a financial as well as director’s report. The accounts are

compulsorily required to be audited, unless the grant is received by ASIC.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.