Corporate Accounting: Asset Retirement, Depreciation, and More

VerifiedAdded on 2023/06/13

|9

|1354

|316

Homework Assignment

AI Summary

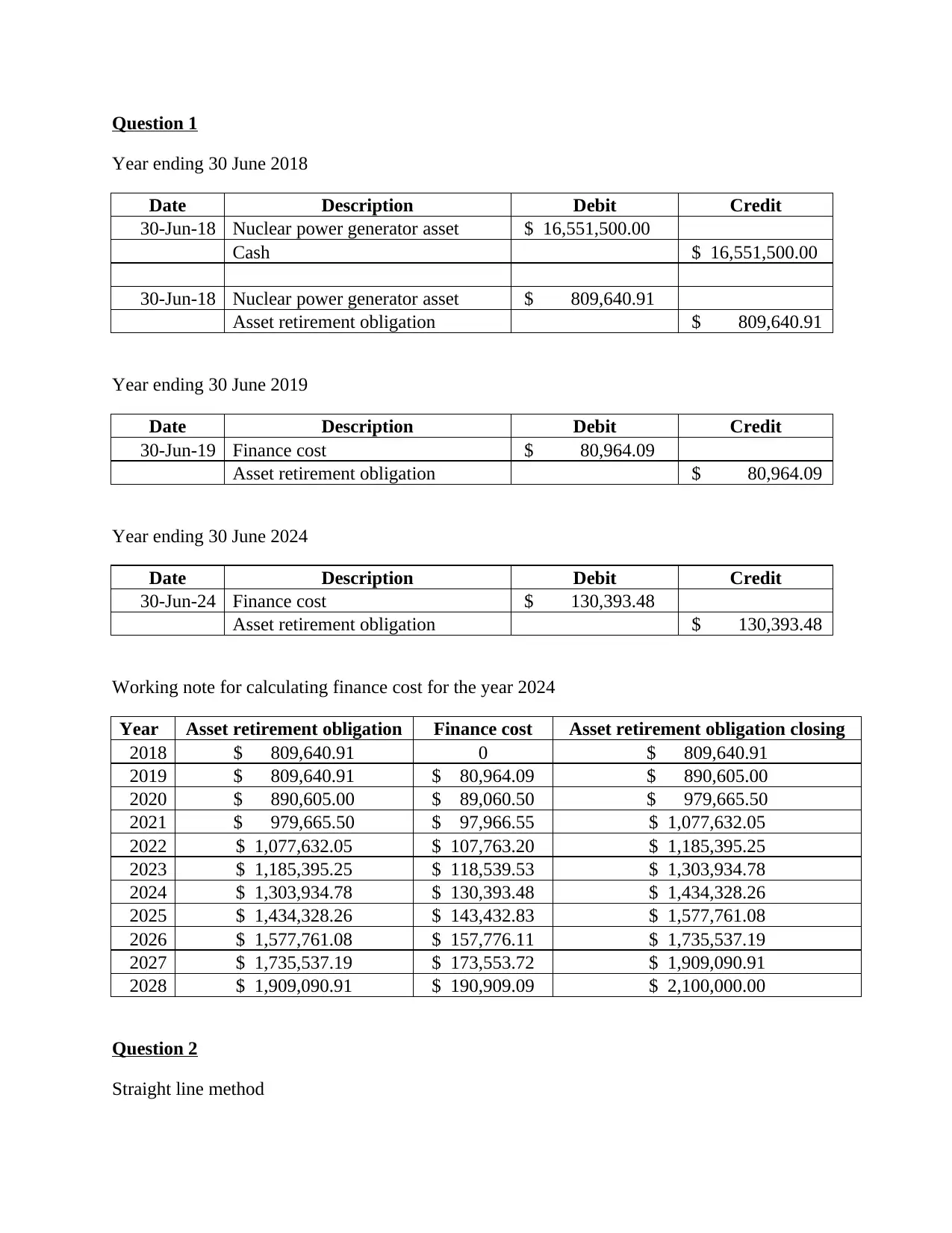

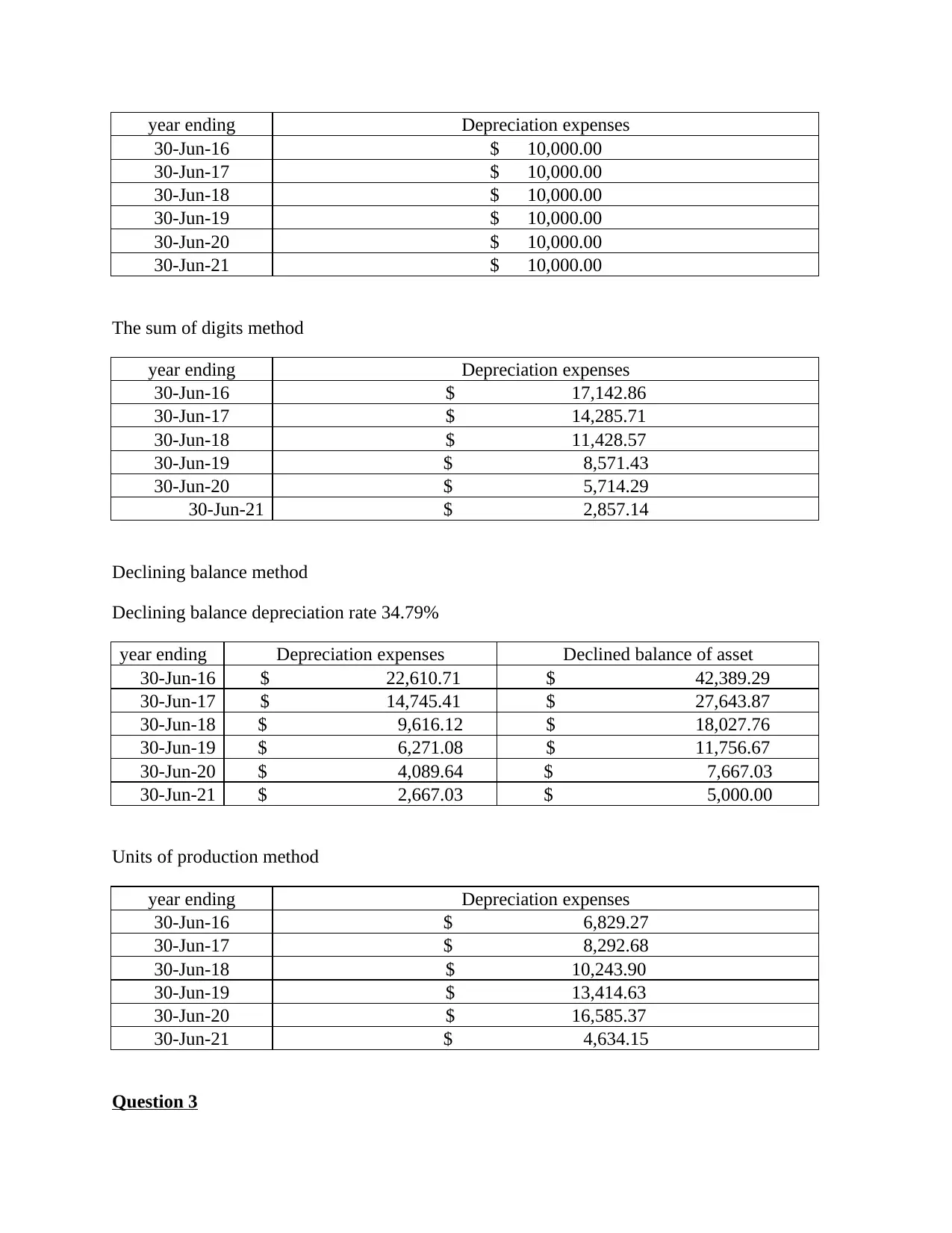

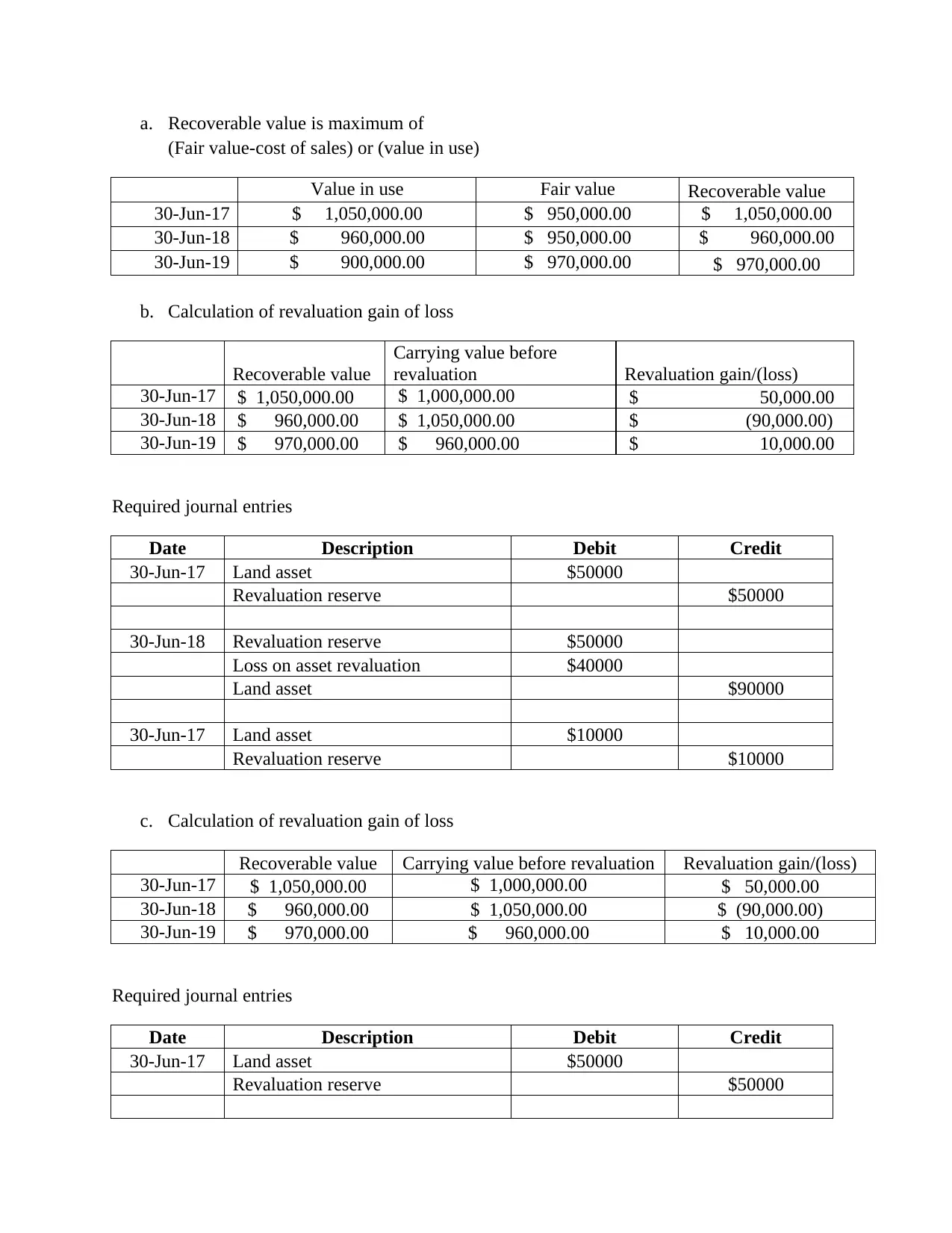

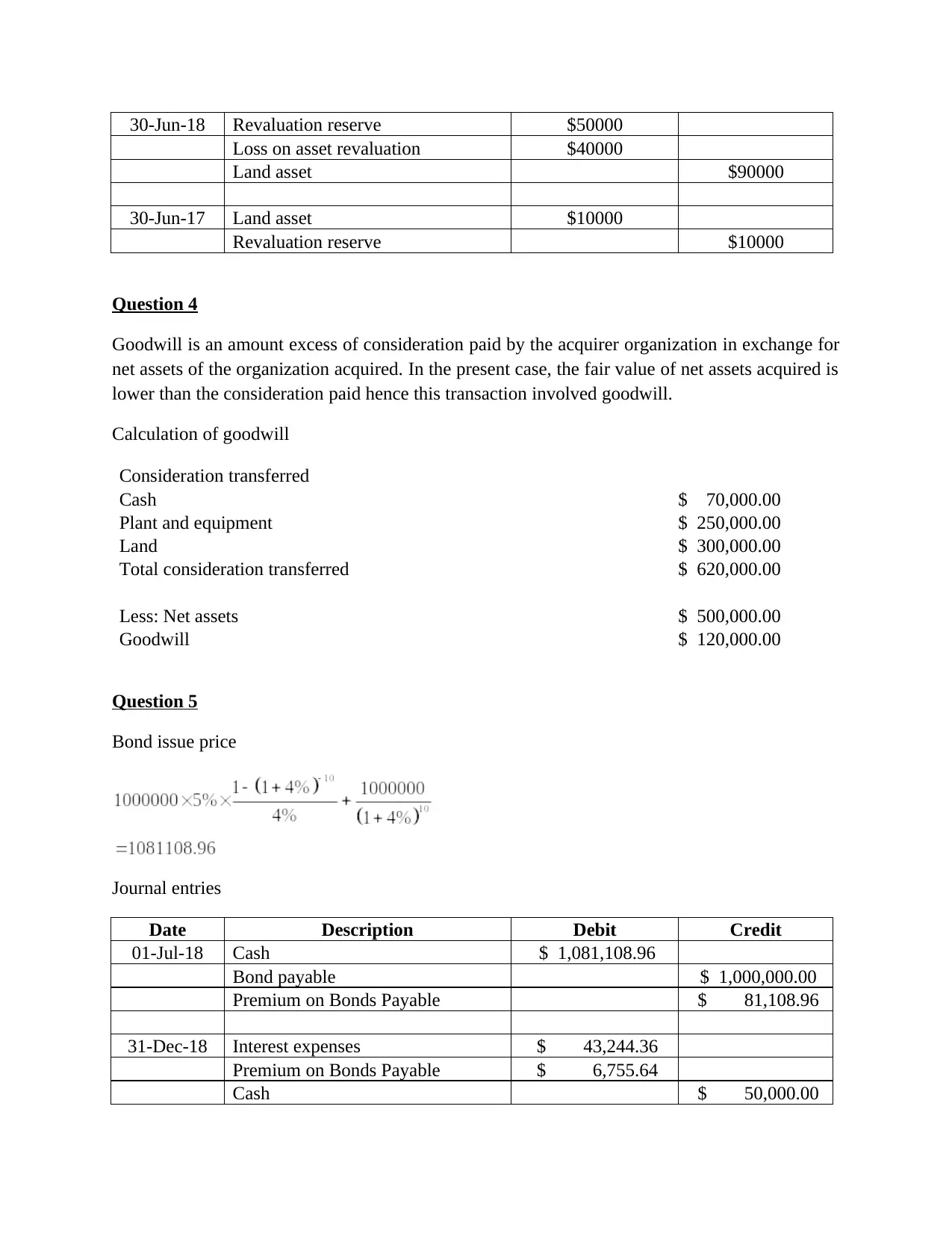

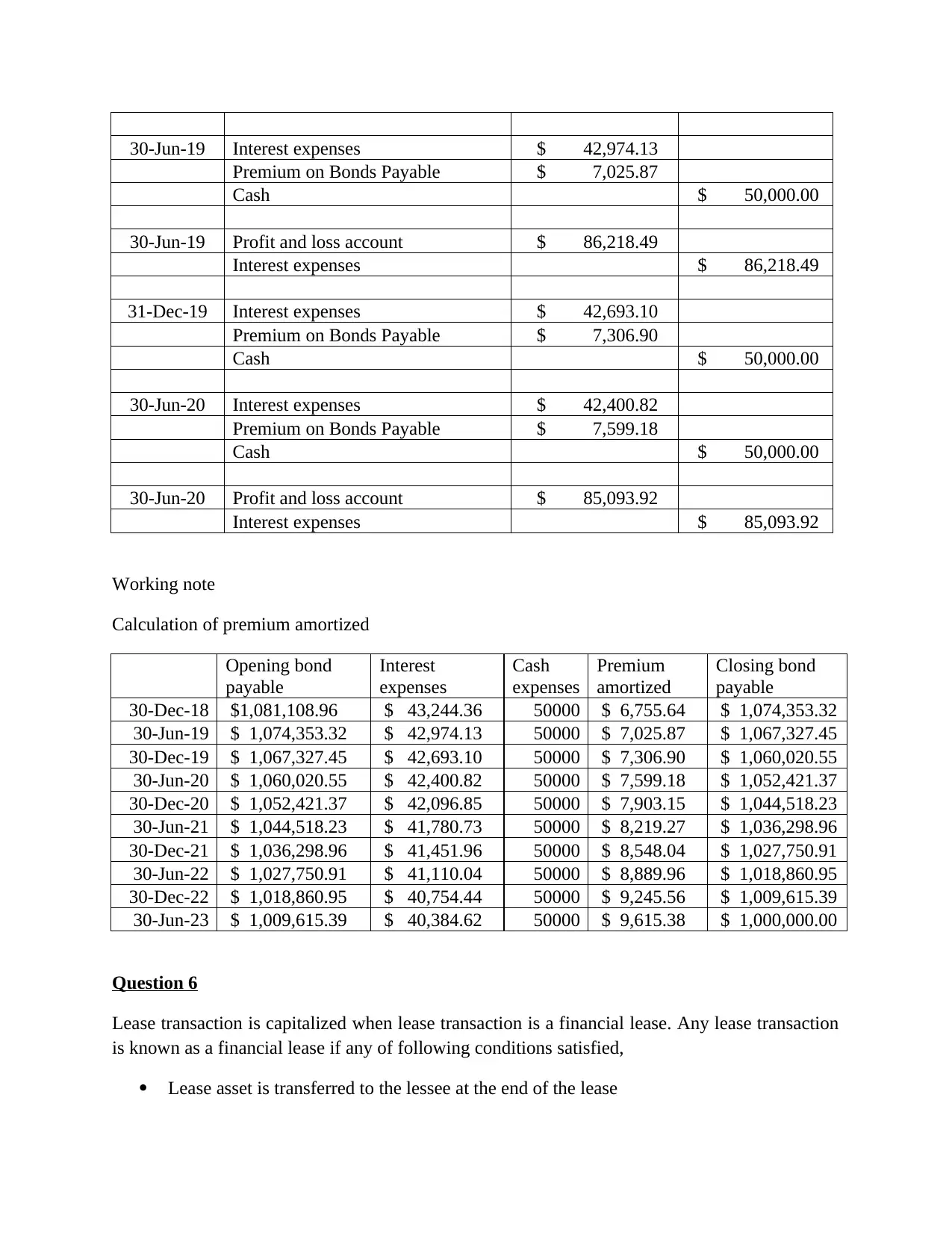

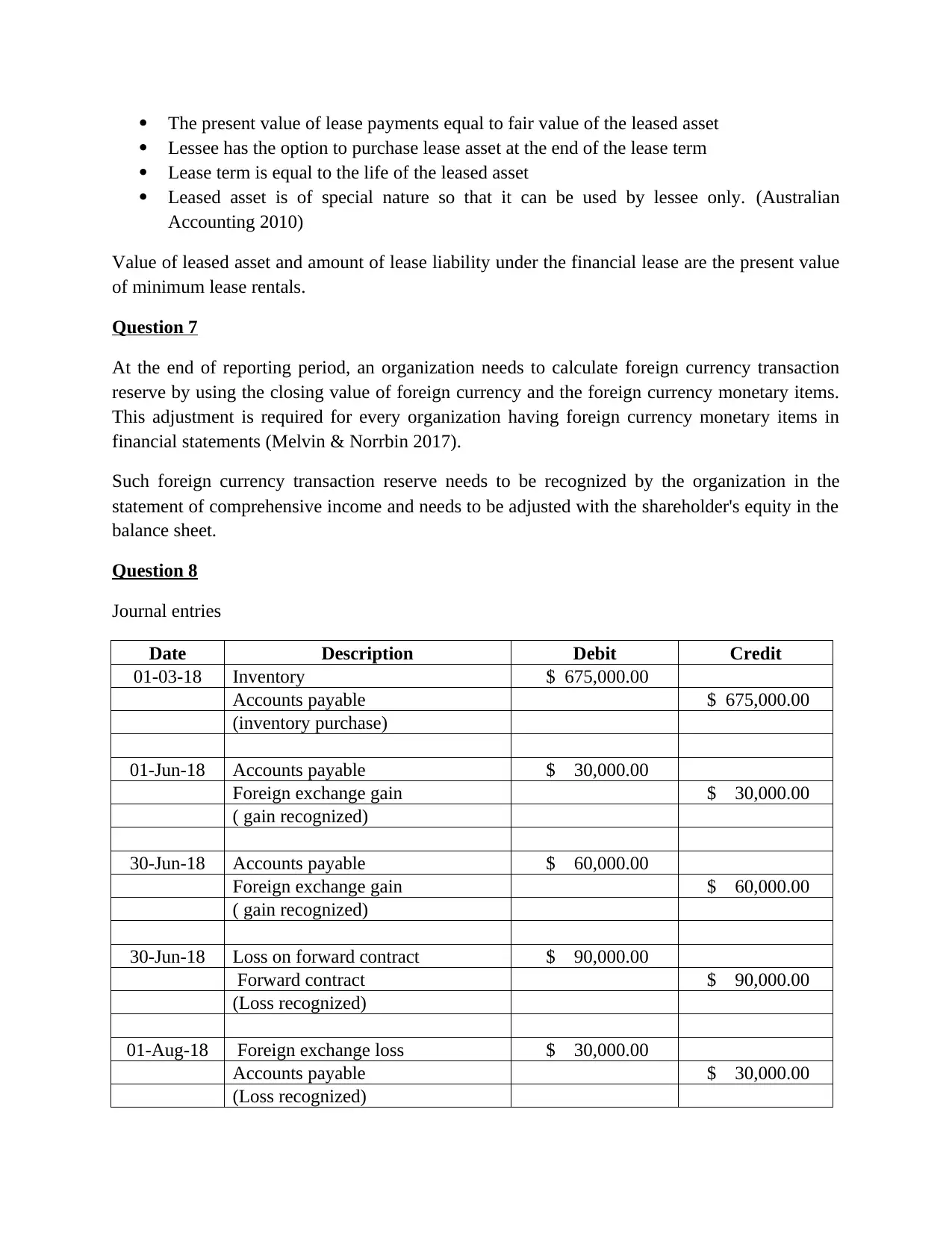

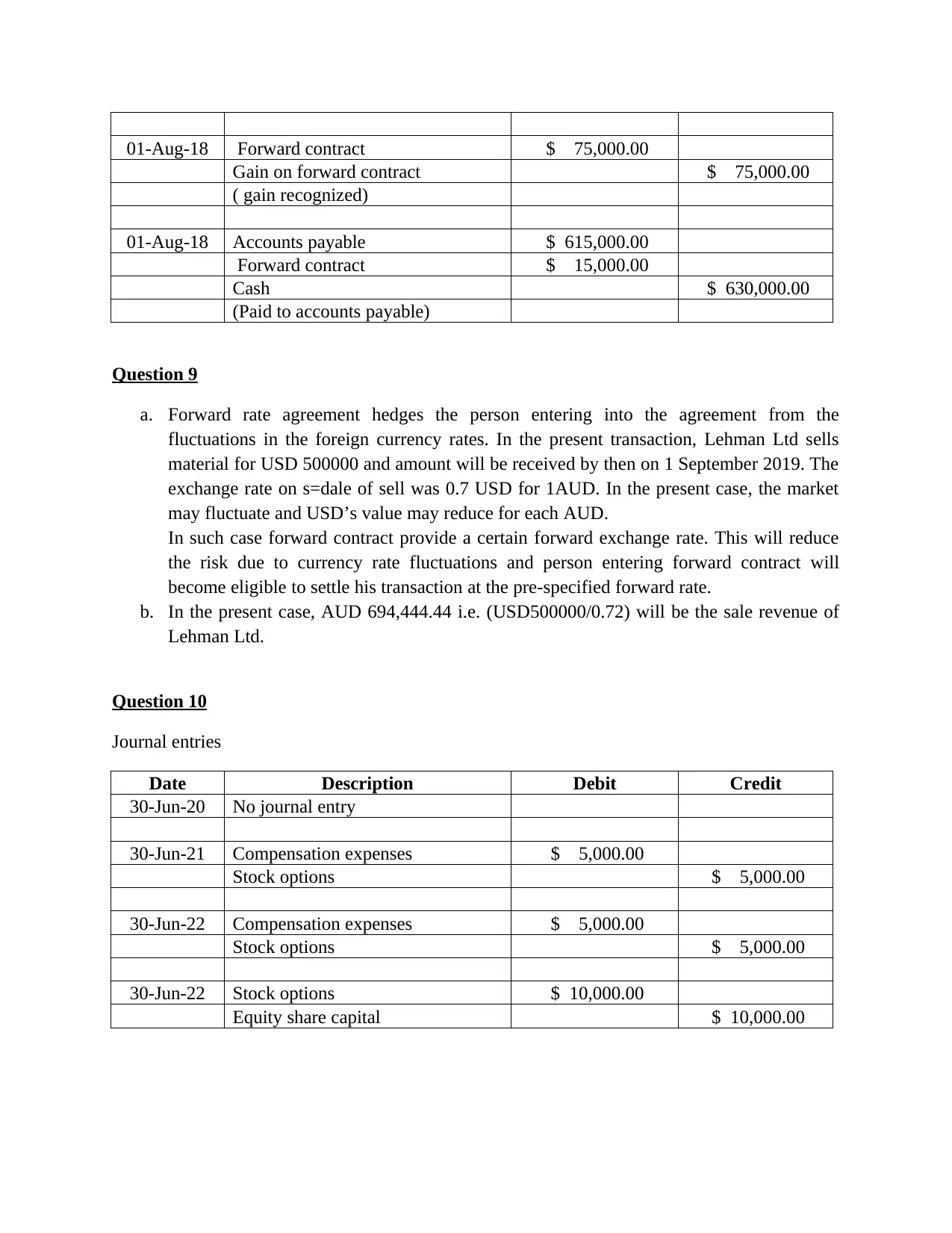

This assignment provides solutions to several accounting problems, including preparing journal entries for a nuclear power generator's asset retirement obligation, calculating depreciation expenses using different methods (straight-line, sum-of-digits, declining balance, and units of production), determining revaluation gains or losses on land assets, calculating goodwill in a business acquisition, and preparing journal entries for bond issuance and premium amortization. It also addresses the conditions for capitalizing a lease transaction as a financial lease, the accounting treatment of foreign currency transactions, and the use of forward rate agreements for hedging foreign currency risks. The solutions include detailed workings and explanations, covering various aspects of corporate accounting and financial analysis.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.