Corporate Accounting Report: Dark Horse vs. Aeon Metals Analysis

VerifiedAdded on 2021/01/02

|14

|4273

|105

Report

AI Summary

This report provides a comprehensive comparative analysis of the financial statements of Dark Horse Resources and Aeon Metals Limited, two Australian companies. The report begins with an examination of owner's equity, including a listing of equity items and a comparative analysis of the companies' equity positions over three years. It then delves into cash flow statements, analyzing the debt-equity ratios and listing key items from the cash flow statements, followed by a comparative analysis of their performance. The report also covers comprehensive income statements, detailing the items reported and providing a comparative analysis. Furthermore, the report addresses corporate income tax, including the tax expenses, effective tax rates, deferred tax assets and liabilities, and cash tax calculations. The analysis highlights the financial strengths and weaknesses of both companies, offering insights into their performance and financial strategies. The report provides detailed data and calculations to support its conclusions.

CORPORATE

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK: 1 OWNER'S EQUITY........................................................................................................1

1. Listing items of equity:............................................................................................................1

TASK 2: CASH FLOW STATEMENTS........................................................................................3

2. Comparative analysis of equity and debt position:..................................................................3

3. List of items reported in cash flow statements of both companies: ........................................4

4. Comparative analysis of companies performance of last three years......................................6

TASK 3............................................................................................................................................7

6. List of items reported in comprehensive income statements: .................................................7

7. List of items reported in other comprehensive income statements:.........................................8

8. Comparative analyses of items listed in comprehensive income statements:..........................8

9. Should Comprehensive incomes included while evaluation of manager's performance: .......9

TASK 4: ACCOUNTING FOR CORPORATE INCOME TAX....................................................9

10. List of Tax expenses shown in financial statements of both companies: .............................9

11. Calculation of effective tax rate of both companies :............................................................9

12. List of deferred tax assets or liabilities reported in balance sheet:.....................................10

13. Changes in deferred tax assets or deferred liability:............................................................10

14. Calculation of Cash Tax amount:........................................................................................10

15. Calculation of Cash Tax Rate:.............................................................................................10

16. Difference between Cash Tax and Book Tax :....................................................................11

CONCLUSION............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK: 1 OWNER'S EQUITY........................................................................................................1

1. Listing items of equity:............................................................................................................1

TASK 2: CASH FLOW STATEMENTS........................................................................................3

2. Comparative analysis of equity and debt position:..................................................................3

3. List of items reported in cash flow statements of both companies: ........................................4

4. Comparative analysis of companies performance of last three years......................................6

TASK 3............................................................................................................................................7

6. List of items reported in comprehensive income statements: .................................................7

7. List of items reported in other comprehensive income statements:.........................................8

8. Comparative analyses of items listed in comprehensive income statements:..........................8

9. Should Comprehensive incomes included while evaluation of manager's performance: .......9

TASK 4: ACCOUNTING FOR CORPORATE INCOME TAX....................................................9

10. List of Tax expenses shown in financial statements of both companies: .............................9

11. Calculation of effective tax rate of both companies :............................................................9

12. List of deferred tax assets or liabilities reported in balance sheet:.....................................10

13. Changes in deferred tax assets or deferred liability:............................................................10

14. Calculation of Cash Tax amount:........................................................................................10

15. Calculation of Cash Tax Rate:.............................................................................................10

16. Difference between Cash Tax and Book Tax :....................................................................11

CONCLUSION............................................................................................................................11

REFERENCES..............................................................................................................................12

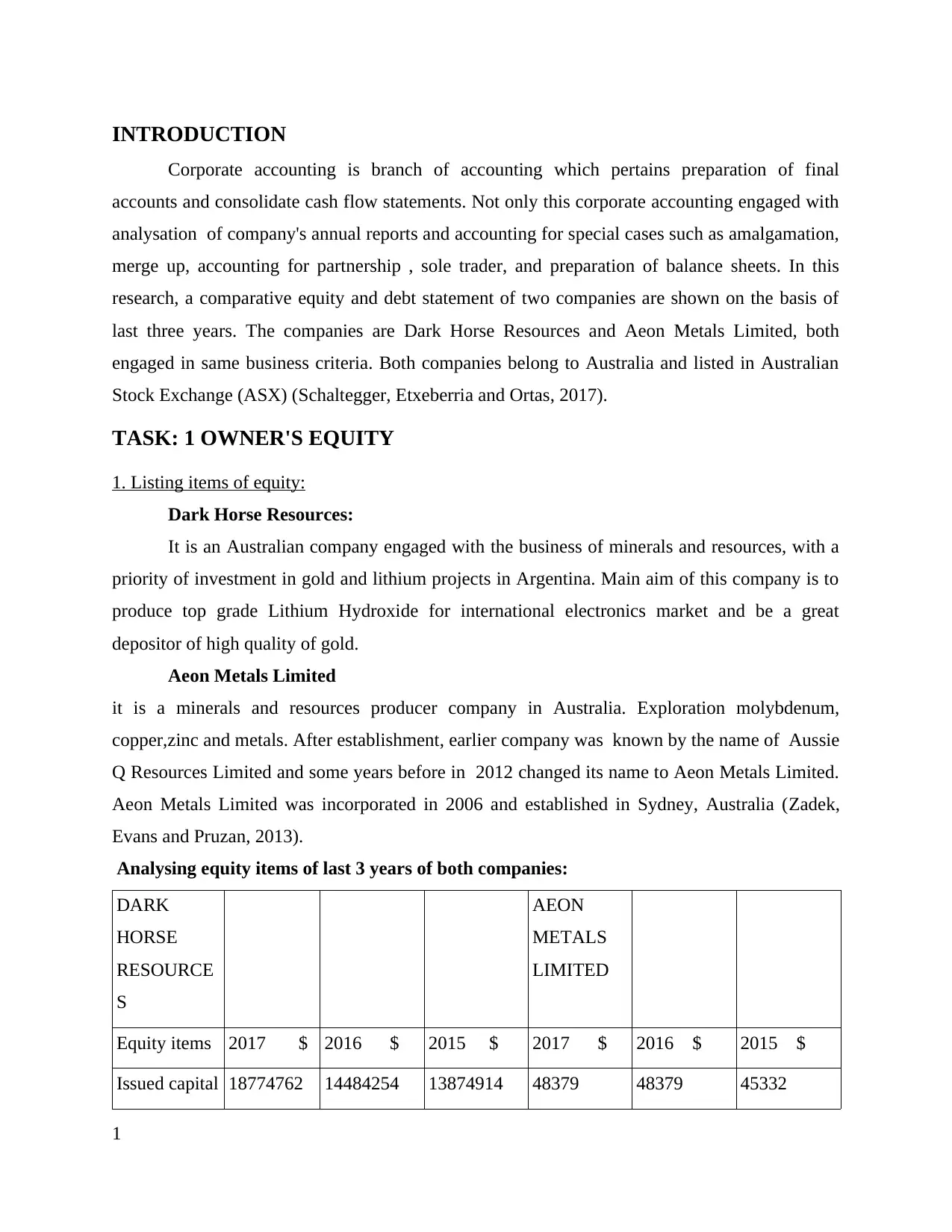

INTRODUCTION

Corporate accounting is branch of accounting which pertains preparation of final

accounts and consolidate cash flow statements. Not only this corporate accounting engaged with

analysation of company's annual reports and accounting for special cases such as amalgamation,

merge up, accounting for partnership , sole trader, and preparation of balance sheets. In this

research, a comparative equity and debt statement of two companies are shown on the basis of

last three years. The companies are Dark Horse Resources and Aeon Metals Limited, both

engaged in same business criteria. Both companies belong to Australia and listed in Australian

Stock Exchange (ASX) (Schaltegger, Etxeberria and Ortas, 2017).

TASK: 1 OWNER'S EQUITY

1. Listing items of equity:

Dark Horse Resources:

It is an Australian company engaged with the business of minerals and resources, with a

priority of investment in gold and lithium projects in Argentina. Main aim of this company is to

produce top grade Lithium Hydroxide for international electronics market and be a great

depositor of high quality of gold.

Aeon Metals Limited

it is a minerals and resources producer company in Australia. Exploration molybdenum,

copper,zinc and metals. After establishment, earlier company was known by the name of Aussie

Q Resources Limited and some years before in 2012 changed its name to Aeon Metals Limited.

Aeon Metals Limited was incorporated in 2006 and established in Sydney, Australia (Zadek,

Evans and Pruzan, 2013).

Analysing equity items of last 3 years of both companies:

DARK

HORSE

RESOURCE

S

AEON

METALS

LIMITED

Equity items 2017 $ 2016 $ 2015 $ 2017 $ 2016 $ 2015 $

Issued capital 18774762 14484254 13874914 48379 48379 45332

1

Corporate accounting is branch of accounting which pertains preparation of final

accounts and consolidate cash flow statements. Not only this corporate accounting engaged with

analysation of company's annual reports and accounting for special cases such as amalgamation,

merge up, accounting for partnership , sole trader, and preparation of balance sheets. In this

research, a comparative equity and debt statement of two companies are shown on the basis of

last three years. The companies are Dark Horse Resources and Aeon Metals Limited, both

engaged in same business criteria. Both companies belong to Australia and listed in Australian

Stock Exchange (ASX) (Schaltegger, Etxeberria and Ortas, 2017).

TASK: 1 OWNER'S EQUITY

1. Listing items of equity:

Dark Horse Resources:

It is an Australian company engaged with the business of minerals and resources, with a

priority of investment in gold and lithium projects in Argentina. Main aim of this company is to

produce top grade Lithium Hydroxide for international electronics market and be a great

depositor of high quality of gold.

Aeon Metals Limited

it is a minerals and resources producer company in Australia. Exploration molybdenum,

copper,zinc and metals. After establishment, earlier company was known by the name of Aussie

Q Resources Limited and some years before in 2012 changed its name to Aeon Metals Limited.

Aeon Metals Limited was incorporated in 2006 and established in Sydney, Australia (Zadek,

Evans and Pruzan, 2013).

Analysing equity items of last 3 years of both companies:

DARK

HORSE

RESOURCE

S

AEON

METALS

LIMITED

Equity items 2017 $ 2016 $ 2015 $ 2017 $ 2016 $ 2015 $

Issued capital 18774762 14484254 13874914 48379 48379 45332

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Reserves 900888 843667 829762 40960 8830 5523

accumulated

losses

-10588573 -14675068 -13107220 -28163 -24682 -22217

Net equity 9087077 652853 1597456 24312 32527 28638

ISSUED CAPITAL:

The issued capital is part of company's authorised capital which issued to public or

private /existing shareholders. it is that part of capital on which the allotment of shares is made.

Moreover, issued capital of Dark Horse Resources increases year after year, but issued capital of

Aeon Metals Limited is stable since last year.

Reasons behind increment in issued capital of Dark Horse resources may be, company

wants to reduce its debts, or company plans to invest in new project, or may be due to excess of

retained earnings that's why company decided to issue new shares to existing shareholders and

utilise the retained earnings.

But, in case of Aeon metals limited the issued capital is stable since last year means

company wants to increase debts ratio in capital structure of company. In year 2015-16 the

issued capital of company increases but in year 2017 company didn't issue shares. Issued capital

increases by steady rate (DeBusk, 2012).

RESERVES:

Reserves are the assets of company in liquid form, maintained to meet the future payment

and unforeseen or contingent liability. Moreover, it shows the liquidity form of company,

generated from retained earnings and extra profits(profits of share holder not yet distributedas

dividends) of company.

In above comparative statement, reserves increases year after year, reserves depend on

funds availability and shows liquidity performance of company as shown above, both companies

have reserves normally built up from retained earnings and extra profits (Edgerton, 2012).

ACCUMULATED LOSSES:

Accumulated losses are the negative balances of company's retained earnings. Retained

earnings are the undistributed profits or dividends of shareholder held with the company. At the

end of accounting era, the net loss/income transfers from consolidate profit and loss statement to

retained earnings account. The favourable balance of retained earning account is called

2

accumulated

losses

-10588573 -14675068 -13107220 -28163 -24682 -22217

Net equity 9087077 652853 1597456 24312 32527 28638

ISSUED CAPITAL:

The issued capital is part of company's authorised capital which issued to public or

private /existing shareholders. it is that part of capital on which the allotment of shares is made.

Moreover, issued capital of Dark Horse Resources increases year after year, but issued capital of

Aeon Metals Limited is stable since last year.

Reasons behind increment in issued capital of Dark Horse resources may be, company

wants to reduce its debts, or company plans to invest in new project, or may be due to excess of

retained earnings that's why company decided to issue new shares to existing shareholders and

utilise the retained earnings.

But, in case of Aeon metals limited the issued capital is stable since last year means

company wants to increase debts ratio in capital structure of company. In year 2015-16 the

issued capital of company increases but in year 2017 company didn't issue shares. Issued capital

increases by steady rate (DeBusk, 2012).

RESERVES:

Reserves are the assets of company in liquid form, maintained to meet the future payment

and unforeseen or contingent liability. Moreover, it shows the liquidity form of company,

generated from retained earnings and extra profits(profits of share holder not yet distributedas

dividends) of company.

In above comparative statement, reserves increases year after year, reserves depend on

funds availability and shows liquidity performance of company as shown above, both companies

have reserves normally built up from retained earnings and extra profits (Edgerton, 2012).

ACCUMULATED LOSSES:

Accumulated losses are the negative balances of company's retained earnings. Retained

earnings are the undistributed profits or dividends of shareholder held with the company. At the

end of accounting era, the net loss/income transfers from consolidate profit and loss statement to

retained earnings account. The favourable balance of retained earning account is called

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

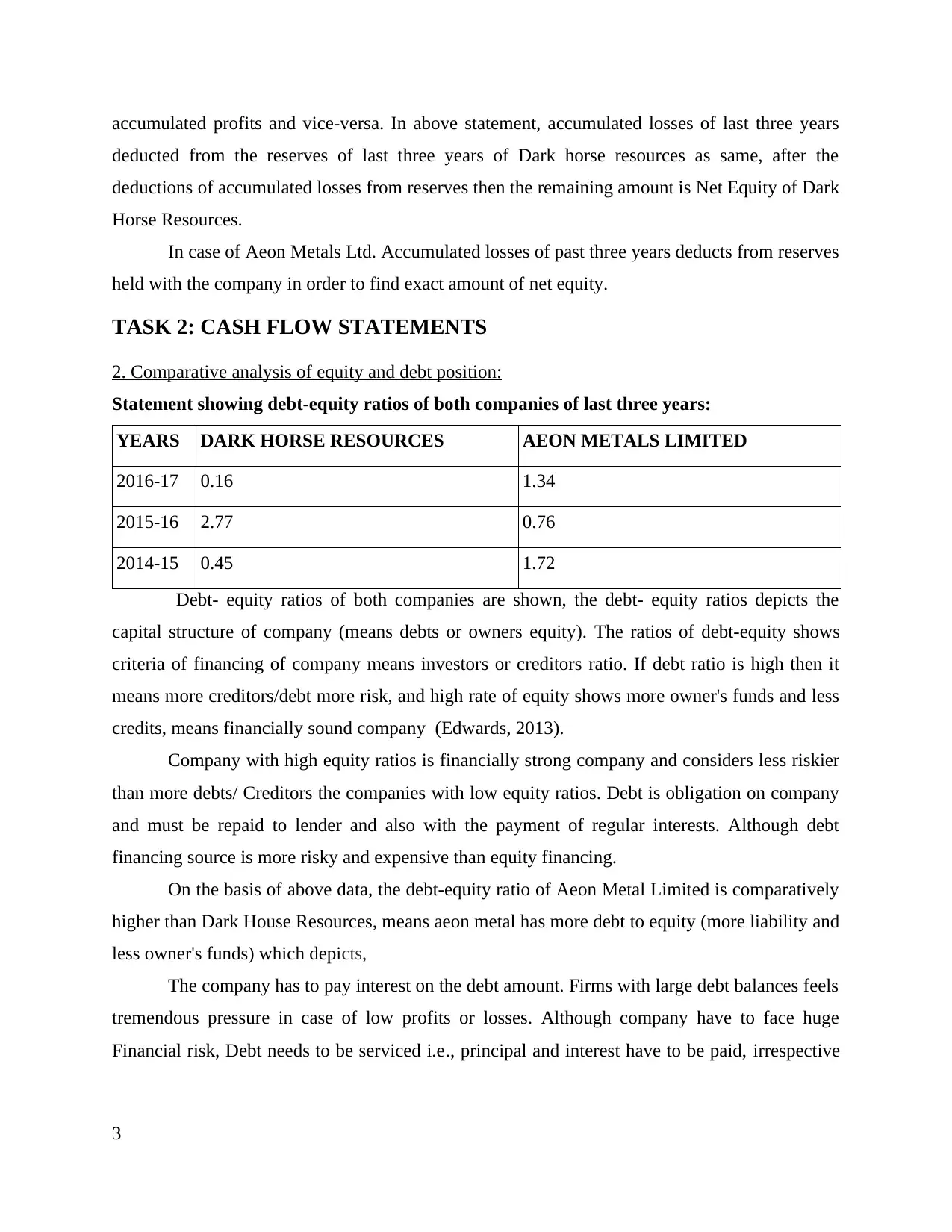

accumulated profits and vice-versa. In above statement, accumulated losses of last three years

deducted from the reserves of last three years of Dark horse resources as same, after the

deductions of accumulated losses from reserves then the remaining amount is Net Equity of Dark

Horse Resources.

In case of Aeon Metals Ltd. Accumulated losses of past three years deducts from reserves

held with the company in order to find exact amount of net equity.

TASK 2: CASH FLOW STATEMENTS

2. Comparative analysis of equity and debt position:

Statement showing debt-equity ratios of both companies of last three years:

YEARS DARK HORSE RESOURCES AEON METALS LIMITED

2016-17 0.16 1.34

2015-16 2.77 0.76

2014-15 0.45 1.72

Debt- equity ratios of both companies are shown, the debt- equity ratios depicts the

capital structure of company (means debts or owners equity). The ratios of debt-equity shows

criteria of financing of company means investors or creditors ratio. If debt ratio is high then it

means more creditors/debt more risk, and high rate of equity shows more owner's funds and less

credits, means financially sound company (Edwards, 2013).

Company with high equity ratios is financially strong company and considers less riskier

than more debts/ Creditors the companies with low equity ratios. Debt is obligation on company

and must be repaid to lender and also with the payment of regular interests. Although debt

financing source is more risky and expensive than equity financing.

On the basis of above data, the debt-equity ratio of Aeon Metal Limited is comparatively

higher than Dark House Resources, means aeon metal has more debt to equity (more liability and

less owner's funds) which depicts,

The company has to pay interest on the debt amount. Firms with large debt balances feels

tremendous pressure in case of low profits or losses. Although company have to face huge

Financial risk, Debt needs to be serviced i.e., principal and interest have to be paid, irrespective

3

deducted from the reserves of last three years of Dark horse resources as same, after the

deductions of accumulated losses from reserves then the remaining amount is Net Equity of Dark

Horse Resources.

In case of Aeon Metals Ltd. Accumulated losses of past three years deducts from reserves

held with the company in order to find exact amount of net equity.

TASK 2: CASH FLOW STATEMENTS

2. Comparative analysis of equity and debt position:

Statement showing debt-equity ratios of both companies of last three years:

YEARS DARK HORSE RESOURCES AEON METALS LIMITED

2016-17 0.16 1.34

2015-16 2.77 0.76

2014-15 0.45 1.72

Debt- equity ratios of both companies are shown, the debt- equity ratios depicts the

capital structure of company (means debts or owners equity). The ratios of debt-equity shows

criteria of financing of company means investors or creditors ratio. If debt ratio is high then it

means more creditors/debt more risk, and high rate of equity shows more owner's funds and less

credits, means financially sound company (Edwards, 2013).

Company with high equity ratios is financially strong company and considers less riskier

than more debts/ Creditors the companies with low equity ratios. Debt is obligation on company

and must be repaid to lender and also with the payment of regular interests. Although debt

financing source is more risky and expensive than equity financing.

On the basis of above data, the debt-equity ratio of Aeon Metal Limited is comparatively

higher than Dark House Resources, means aeon metal has more debt to equity (more liability and

less owner's funds) which depicts,

The company has to pay interest on the debt amount. Firms with large debt balances feels

tremendous pressure in case of low profits or losses. Although company have to face huge

Financial risk, Debt needs to be serviced i.e., principal and interest have to be paid, irrespective

3

of the fact whether the company has earned profits in that year or not, thus, it may lead to the

bankruptcy of the company also (Hoskin, Fizzell and Cherry, 2014).

Hence, Dark Horse Resources is well financially sound company in comparison with

Aeon ltd.

3. List of items reported in cash flow statements of both companies:

Some items of Dark horse resources cash flow data:

Activities particulars Years 2017 2016 2015

OPERATING

ACTIVITIES

Payment

to supplier

-304415 -191242 -255667

Interest

received

852 341 826

FINANCING

ACTIVITIES

Issue of

share

capital

1958310 292133 500229

INVESTING

ACTIVITIES

Exploratio

n costs

-2374998 497011 302686

Some items of Aeon Metals Limited cash flow data:

Activities particulars 2017 thou. $ 2016 2015

OPERATING

ACTIVITIES

Payment

to supplier

1674 1394 1622

Interest

received

97 161 102

FINANCING

ACTIVITIES

Issue of

shares

…....... 3260 2094

INVESTING

ACTIVITIES

Exploratio

n costs

3204 2227 4235

4

bankruptcy of the company also (Hoskin, Fizzell and Cherry, 2014).

Hence, Dark Horse Resources is well financially sound company in comparison with

Aeon ltd.

3. List of items reported in cash flow statements of both companies:

Some items of Dark horse resources cash flow data:

Activities particulars Years 2017 2016 2015

OPERATING

ACTIVITIES

Payment

to supplier

-304415 -191242 -255667

Interest

received

852 341 826

FINANCING

ACTIVITIES

Issue of

share

capital

1958310 292133 500229

INVESTING

ACTIVITIES

Exploratio

n costs

-2374998 497011 302686

Some items of Aeon Metals Limited cash flow data:

Activities particulars 2017 thou. $ 2016 2015

OPERATING

ACTIVITIES

Payment

to supplier

1674 1394 1622

Interest

received

97 161 102

FINANCING

ACTIVITIES

Issue of

shares

…....... 3260 2094

INVESTING

ACTIVITIES

Exploratio

n costs

3204 2227 4235

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

From the above analysed data, those items analysed from operating, financing, investing

activities are analysed which are changed year after year, since last three years.

Operating activities:

Payment made to supplier: It means payment to supplier of raw material and

intermediate goods made by cash, cheque or from any other mode, it's a type of

operating activity and directly related to production and amount of supplier's payment

changes due to increase in quantity order of raw material, means when company wants

to increase production.

Interest received: It means operating income in form of interest received, as in case

company engaged in financial services or made investments also. In case of dark horse

resources, the interest received increases year after year but, not in case of aeon metals

limited because no income earned by company in form of interest, due to no investments

shown in the balance sheet of Aeon Metals Ltd. (Huseynov and Klamm, 2012).

Financing Activities:

Issue of shares: In above data it is shown that in case of Dark Horse Resources issue

amount of shares increases year after year. Company wants to expand the business

criteria or for innovations and future growth of organisation. But in case of Aeon Metals

Limited, company raised funds in year 2015 and 2016 not in 2017. In debt-equity

analysation the ratios of debt and equity of Aeon limited are high means company prefer

to raise funds from debts instead of share issue.

Investing Activities:

Exploration costs: it means company incurs exploration costs when it explores or expands

the business criteria. May be company wants to diversify the business or wants to set new

branches in different cities or countries. Each industry wants to expands the business through out

the world as in above data exploration costs of both company’s years after year, means company

wants to expands the business or wants to set new branches at different place or may be wants to

start business in different business sector. (Raiborn and Sivitanides, 2015).

4. Comparative analysis of companies performance of last three years.

DARK HORSE RESOURCES

Inflow of cash from operating, financing, investing activities.

DARK HORSE RESOURCES

5

activities are analysed which are changed year after year, since last three years.

Operating activities:

Payment made to supplier: It means payment to supplier of raw material and

intermediate goods made by cash, cheque or from any other mode, it's a type of

operating activity and directly related to production and amount of supplier's payment

changes due to increase in quantity order of raw material, means when company wants

to increase production.

Interest received: It means operating income in form of interest received, as in case

company engaged in financial services or made investments also. In case of dark horse

resources, the interest received increases year after year but, not in case of aeon metals

limited because no income earned by company in form of interest, due to no investments

shown in the balance sheet of Aeon Metals Ltd. (Huseynov and Klamm, 2012).

Financing Activities:

Issue of shares: In above data it is shown that in case of Dark Horse Resources issue

amount of shares increases year after year. Company wants to expand the business

criteria or for innovations and future growth of organisation. But in case of Aeon Metals

Limited, company raised funds in year 2015 and 2016 not in 2017. In debt-equity

analysation the ratios of debt and equity of Aeon limited are high means company prefer

to raise funds from debts instead of share issue.

Investing Activities:

Exploration costs: it means company incurs exploration costs when it explores or expands

the business criteria. May be company wants to diversify the business or wants to set new

branches in different cities or countries. Each industry wants to expands the business through out

the world as in above data exploration costs of both company’s years after year, means company

wants to expands the business or wants to set new branches at different place or may be wants to

start business in different business sector. (Raiborn and Sivitanides, 2015).

4. Comparative analysis of companies performance of last three years.

DARK HORSE RESOURCES

Inflow of cash from operating, financing, investing activities.

DARK HORSE RESOURCES

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACTIVITIES YEAR 2017 YEAR 2016 YEAR 2015

OPERATING 280220 190901 254870

FINANCING 2782755 823740 540210

INVESTING 2378903 470061 288647

AEON METALS LIMITED

ACTIVITIES YEAR 2017 000 $ YEAR 2016 000 $ YEAR 2015 000 $

OPERATING 1577 677 1077

FINANCING …............... 7836 1912

INVESTING 3184 2252 4264

From the above data, income from three categories of activities of both companies are

stated.

Operating activities: it means activities which are related directly to production and

calculation of gross profit made on the basis of direct expenses and income. funds raised from

financing and investing activities is quite more than operating activities. For example, raw

material, wages and salaries etc.

Financing Activities: it means activities which are related to finance and raising funds

for future growth of organisation. These activities include financing funds from different sources

and dividend payment interest on debentures and loan. Funds raised from financing activities are

generally more than revenue earned from operating and investing activities (Rogoff, 2017).

Investing Activities: it means activities which are related to investments are come under

investing activities. Investments are crucial for business growth and also for exploration of

business. Investment is essential for earning revenues and incomes besides with operating and

financing activities.

5. Comparative analysation of two companies:

DARK HORSE RESOURES AEON METALS LIMITED

In flows from operating activities increases

year after, and maximises the profit, because

Inflows from operating activities decreases

year after year and affects companies

6

OPERATING 280220 190901 254870

FINANCING 2782755 823740 540210

INVESTING 2378903 470061 288647

AEON METALS LIMITED

ACTIVITIES YEAR 2017 000 $ YEAR 2016 000 $ YEAR 2015 000 $

OPERATING 1577 677 1077

FINANCING …............... 7836 1912

INVESTING 3184 2252 4264

From the above data, income from three categories of activities of both companies are

stated.

Operating activities: it means activities which are related directly to production and

calculation of gross profit made on the basis of direct expenses and income. funds raised from

financing and investing activities is quite more than operating activities. For example, raw

material, wages and salaries etc.

Financing Activities: it means activities which are related to finance and raising funds

for future growth of organisation. These activities include financing funds from different sources

and dividend payment interest on debentures and loan. Funds raised from financing activities are

generally more than revenue earned from operating and investing activities (Rogoff, 2017).

Investing Activities: it means activities which are related to investments are come under

investing activities. Investments are crucial for business growth and also for exploration of

business. Investment is essential for earning revenues and incomes besides with operating and

financing activities.

5. Comparative analysation of two companies:

DARK HORSE RESOURES AEON METALS LIMITED

In flows from operating activities increases

year after, and maximises the profit, because

Inflows from operating activities decreases

year after year and affects companies

6

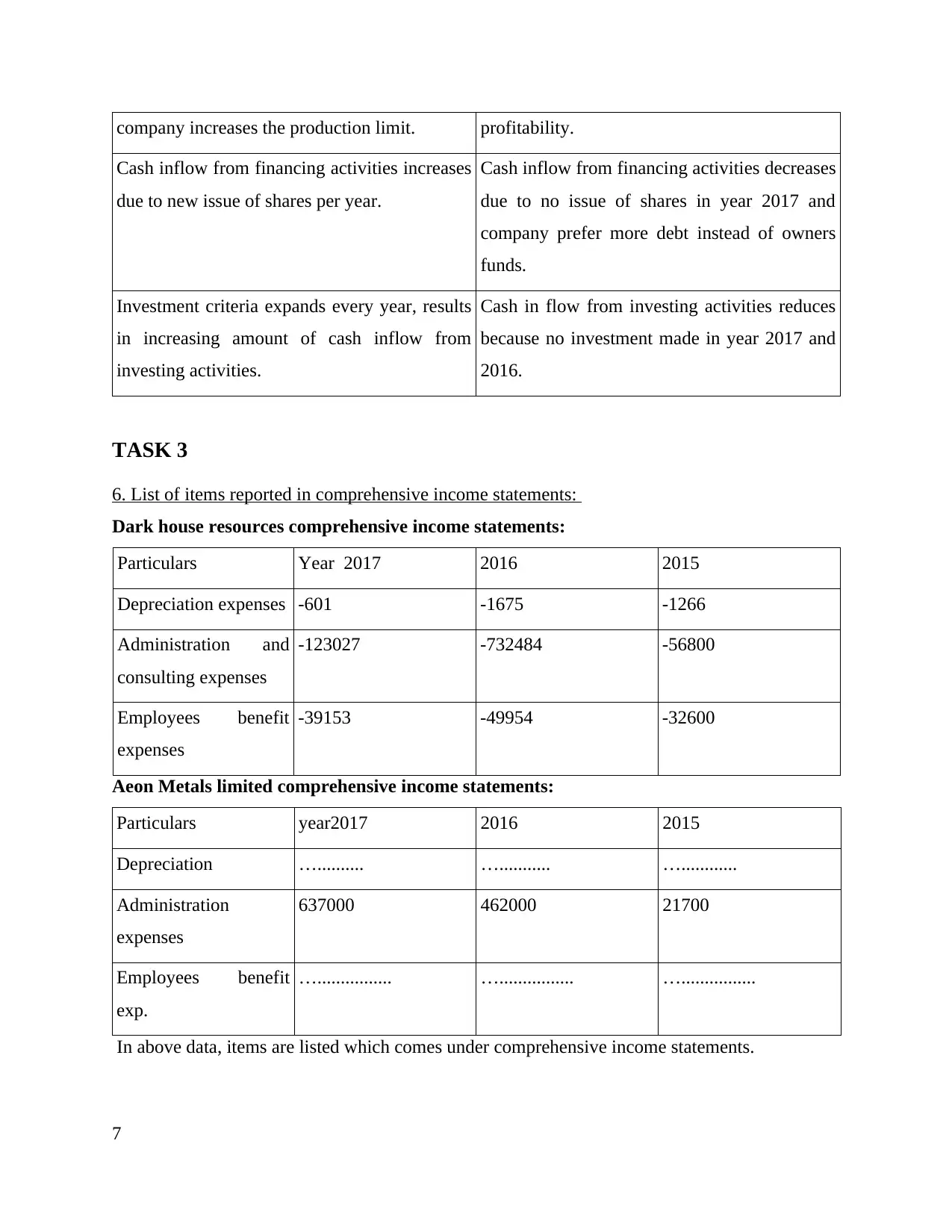

company increases the production limit. profitability.

Cash inflow from financing activities increases

due to new issue of shares per year.

Cash inflow from financing activities decreases

due to no issue of shares in year 2017 and

company prefer more debt instead of owners

funds.

Investment criteria expands every year, results

in increasing amount of cash inflow from

investing activities.

Cash in flow from investing activities reduces

because no investment made in year 2017 and

2016.

TASK 3

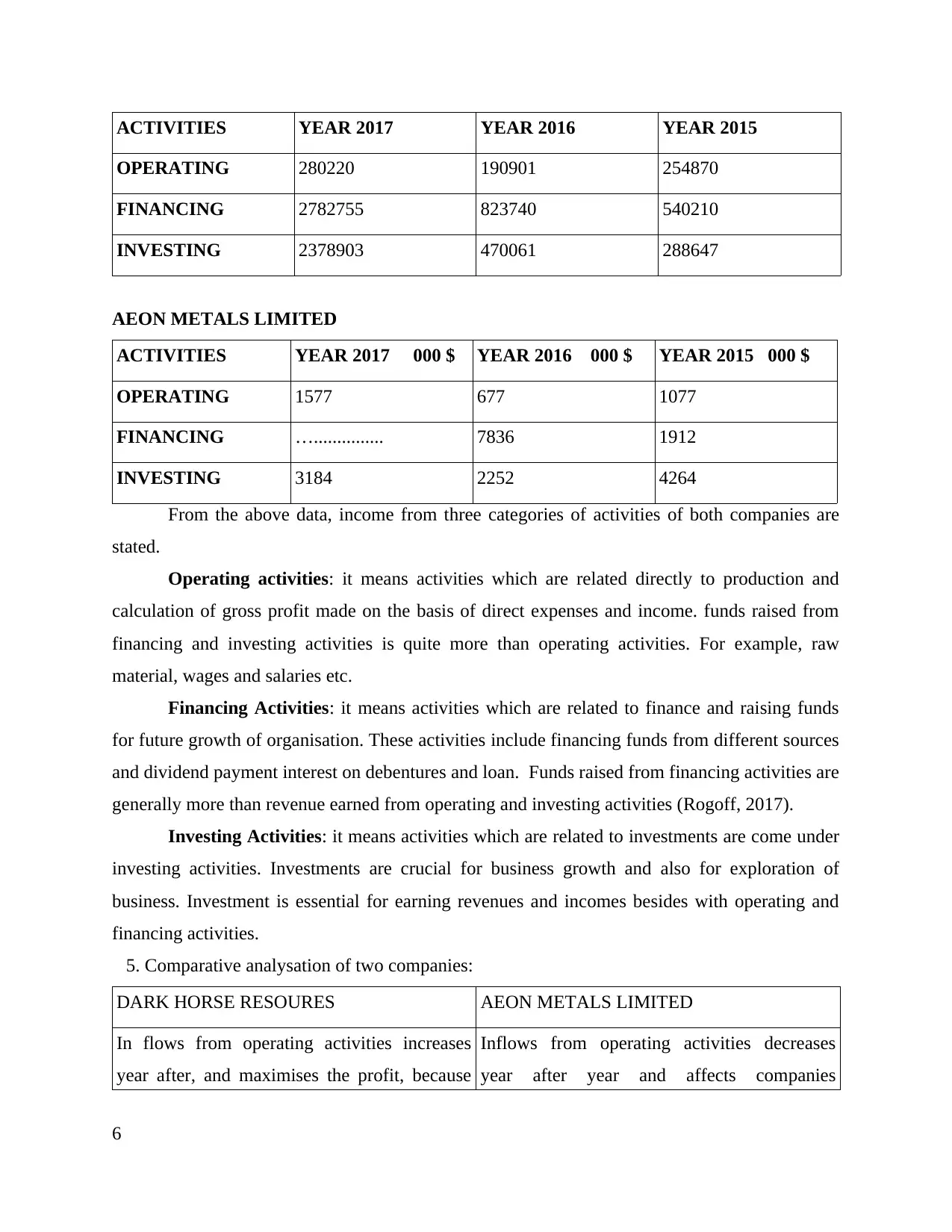

6. List of items reported in comprehensive income statements:

Dark house resources comprehensive income statements:

Particulars Year 2017 2016 2015

Depreciation expenses -601 -1675 -1266

Administration and

consulting expenses

-123027 -732484 -56800

Employees benefit

expenses

-39153 -49954 -32600

Aeon Metals limited comprehensive income statements:

Particulars year2017 2016 2015

Depreciation ….......... …........... …............

Administration

expenses

637000 462000 21700

Employees benefit

exp.

…................ …................ …................

In above data, items are listed which comes under comprehensive income statements.

7

Cash inflow from financing activities increases

due to new issue of shares per year.

Cash inflow from financing activities decreases

due to no issue of shares in year 2017 and

company prefer more debt instead of owners

funds.

Investment criteria expands every year, results

in increasing amount of cash inflow from

investing activities.

Cash in flow from investing activities reduces

because no investment made in year 2017 and

2016.

TASK 3

6. List of items reported in comprehensive income statements:

Dark house resources comprehensive income statements:

Particulars Year 2017 2016 2015

Depreciation expenses -601 -1675 -1266

Administration and

consulting expenses

-123027 -732484 -56800

Employees benefit

expenses

-39153 -49954 -32600

Aeon Metals limited comprehensive income statements:

Particulars year2017 2016 2015

Depreciation ….......... …........... …............

Administration

expenses

637000 462000 21700

Employees benefit

exp.

…................ …................ …................

In above data, items are listed which comes under comprehensive income statements.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

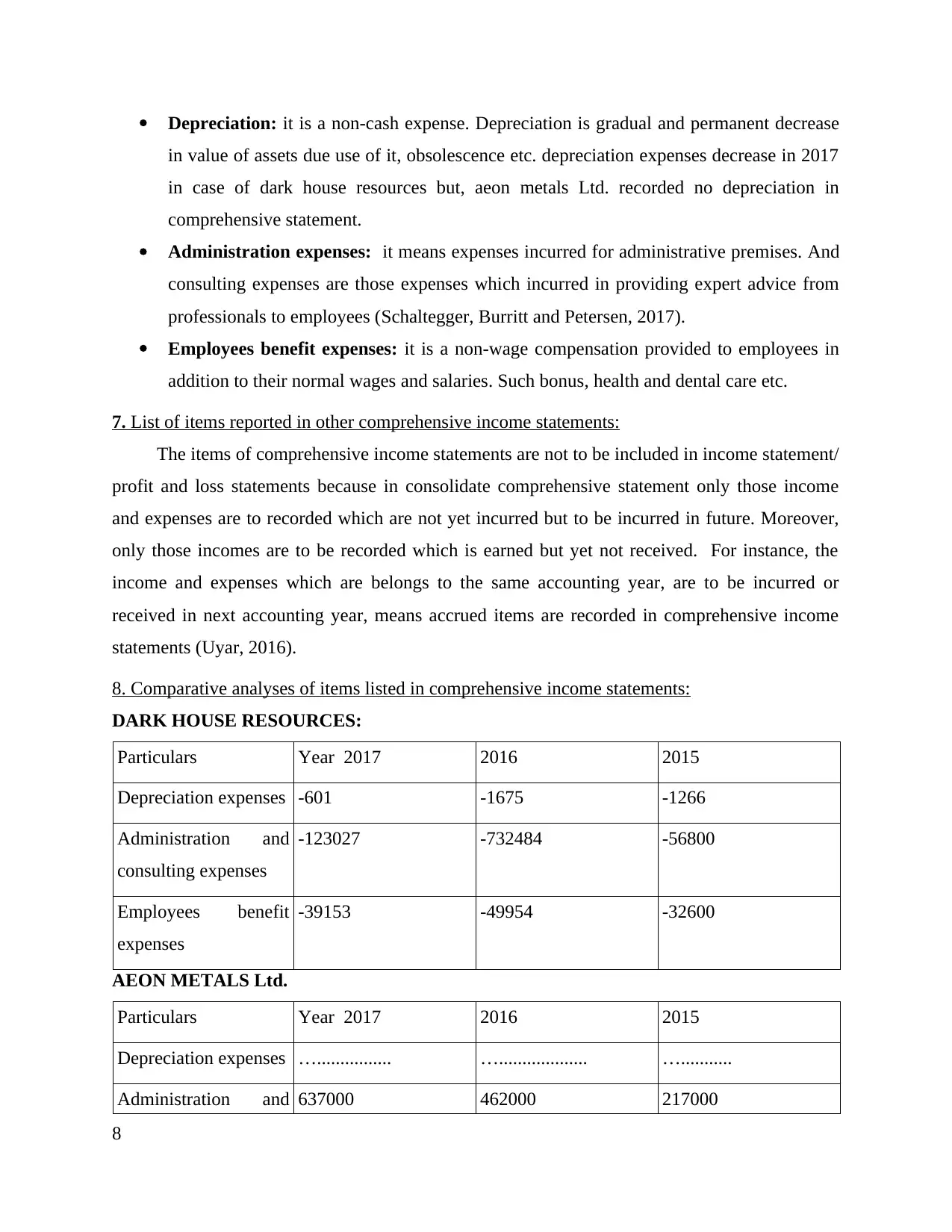

Depreciation: it is a non-cash expense. Depreciation is gradual and permanent decrease

in value of assets due use of it, obsolescence etc. depreciation expenses decrease in 2017

in case of dark house resources but, aeon metals Ltd. recorded no depreciation in

comprehensive statement.

Administration expenses: it means expenses incurred for administrative premises. And

consulting expenses are those expenses which incurred in providing expert advice from

professionals to employees (Schaltegger, Burritt and Petersen, 2017).

Employees benefit expenses: it is a non-wage compensation provided to employees in

addition to their normal wages and salaries. Such bonus, health and dental care etc.

7. List of items reported in other comprehensive income statements:

The items of comprehensive income statements are not to be included in income statement/

profit and loss statements because in consolidate comprehensive statement only those income

and expenses are to recorded which are not yet incurred but to be incurred in future. Moreover,

only those incomes are to be recorded which is earned but yet not received. For instance, the

income and expenses which are belongs to the same accounting year, are to be incurred or

received in next accounting year, means accrued items are recorded in comprehensive income

statements (Uyar, 2016).

8. Comparative analyses of items listed in comprehensive income statements:

DARK HOUSE RESOURCES:

Particulars Year 2017 2016 2015

Depreciation expenses -601 -1675 -1266

Administration and

consulting expenses

-123027 -732484 -56800

Employees benefit

expenses

-39153 -49954 -32600

AEON METALS Ltd.

Particulars Year 2017 2016 2015

Depreciation expenses …................ …................... …...........

Administration and 637000 462000 217000

8

in value of assets due use of it, obsolescence etc. depreciation expenses decrease in 2017

in case of dark house resources but, aeon metals Ltd. recorded no depreciation in

comprehensive statement.

Administration expenses: it means expenses incurred for administrative premises. And

consulting expenses are those expenses which incurred in providing expert advice from

professionals to employees (Schaltegger, Burritt and Petersen, 2017).

Employees benefit expenses: it is a non-wage compensation provided to employees in

addition to their normal wages and salaries. Such bonus, health and dental care etc.

7. List of items reported in other comprehensive income statements:

The items of comprehensive income statements are not to be included in income statement/

profit and loss statements because in consolidate comprehensive statement only those income

and expenses are to recorded which are not yet incurred but to be incurred in future. Moreover,

only those incomes are to be recorded which is earned but yet not received. For instance, the

income and expenses which are belongs to the same accounting year, are to be incurred or

received in next accounting year, means accrued items are recorded in comprehensive income

statements (Uyar, 2016).

8. Comparative analyses of items listed in comprehensive income statements:

DARK HOUSE RESOURCES:

Particulars Year 2017 2016 2015

Depreciation expenses -601 -1675 -1266

Administration and

consulting expenses

-123027 -732484 -56800

Employees benefit

expenses

-39153 -49954 -32600

AEON METALS Ltd.

Particulars Year 2017 2016 2015

Depreciation expenses …................ …................... …...........

Administration and 637000 462000 217000

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

consulting expenses

Employees benefit

expenses

…............. …............. ….............

If these items of comprehensive income statements are to be recorded in profit and loss

account, then it affects the performance of organisation and unnecessarily minimises the profit.

Because expenses/ income are to be recorded in comprehensive statements are at estimated

values not on their actual values. In profit and loss account items are recorded on accrual basis

and only those expenses and income are recorded which are actually incurred or received. If

these item added to profit and loss account, the profit attributable to shareholders minimises

unnecessarily.

9. Should Comprehensive incomes included while evaluation of manager's performance:

No, comprehensive income included while evaluating the performance of the managers of

the company because If income of comprehensive statements is to be added in income/expenses

statement, then it gives irrelevant and unfair result of profit. Because income recorded in

comprehensive statements are not at its actual value, at its estimated value. And it affects badly

the performance of managers of organisation. Not only this, in case of non-cash expenses like

depreciation, only the actual amount of depreciation of same year is charged by profit and loss

account, because if estimated amount which is to be depreciate not yet now but in future, if

charged by P/L, it minimises the profit as well as decrease value of assets unfairly.

TASK 4: ACCOUNTING FOR CORPORATE INCOME TAX

10. List of Tax expenses shown in financial statements of both companies:

Income tax expense the computation of the tax expense is considerably more complex. Tax

law may provide for different treatment of items of income and expenses as a result of tax policy.

The differences may be of permanent or temporary nature. Permanent items are in the form of

non-taxable income and non-taxable expenses. Things such as expenses considered not

deductible by taxing authorities the range of tax rates applicable to various levels of income,

different tax rates in different jurisdictions. In case of dark horse resources there is no income tax

expense in year2017 but in 2016 (665A$) were the income tax expense. And in case of Aeon

metals Ltd. There is no income tax expense since last two years.

9

Employees benefit

expenses

…............. …............. ….............

If these items of comprehensive income statements are to be recorded in profit and loss

account, then it affects the performance of organisation and unnecessarily minimises the profit.

Because expenses/ income are to be recorded in comprehensive statements are at estimated

values not on their actual values. In profit and loss account items are recorded on accrual basis

and only those expenses and income are recorded which are actually incurred or received. If

these item added to profit and loss account, the profit attributable to shareholders minimises

unnecessarily.

9. Should Comprehensive incomes included while evaluation of manager's performance:

No, comprehensive income included while evaluating the performance of the managers of

the company because If income of comprehensive statements is to be added in income/expenses

statement, then it gives irrelevant and unfair result of profit. Because income recorded in

comprehensive statements are not at its actual value, at its estimated value. And it affects badly

the performance of managers of organisation. Not only this, in case of non-cash expenses like

depreciation, only the actual amount of depreciation of same year is charged by profit and loss

account, because if estimated amount which is to be depreciate not yet now but in future, if

charged by P/L, it minimises the profit as well as decrease value of assets unfairly.

TASK 4: ACCOUNTING FOR CORPORATE INCOME TAX

10. List of Tax expenses shown in financial statements of both companies:

Income tax expense the computation of the tax expense is considerably more complex. Tax

law may provide for different treatment of items of income and expenses as a result of tax policy.

The differences may be of permanent or temporary nature. Permanent items are in the form of

non-taxable income and non-taxable expenses. Things such as expenses considered not

deductible by taxing authorities the range of tax rates applicable to various levels of income,

different tax rates in different jurisdictions. In case of dark horse resources there is no income tax

expense in year2017 but in 2016 (665A$) were the income tax expense. And in case of Aeon

metals Ltd. There is no income tax expense since last two years.

9

11. Calculation of effective tax rate of both companies :

Effective tax rate is the rate by which tax is calculated on earning before tax. Effective tax

rate= income tax expense /earning before tax, now there is no information regarding income

tax expense of dark horse resources of year 2017 but in 2016 the tax expenses were 665 A$.

hence tax rate of year 2016 is 0.000423.

In case of Aeon metals Ltd. There are no tax expenses incurred by company since last two

years then we assume that '0' is the tax expense then, tax rate is 0. hence tax rate of Dark Horse

resources is higher than Aeon metal Ltd.

12. List of deferred tax assets or liabilities reported in balance sheet:

Deferred tax is either has a positive impact as 'assets' or negative impact as 'liability' on

balance sheet because of tax owed and tax overpaid due to temporary differences. Deferred tax

can fall into one of two categories, one is deferred tax assets and second is deferred tax liability,

will appeared as entries on balance sheet and represents the negative or positive amount of tax

owed. But there can be one without another, a company can have only deferred tax liability and

deferred tax assets. Deferred tax liability of Dark Horse Resources is 1931A$ and there is no

deferred tax assets or liability in Aeon Metals Ltd. Annual reports.

13. Changes in deferred tax assets or deferred liability:

Yes, in case of Dark horse resources in year 2016 deferred tax liability of 1931 A$ and in

year 2017 all were written off. but in case of Aeon Metals Ltd. There were no tax liability or

deferred tax assets (financial statements, 2017).

14. Calculation of Cash Tax amount:

Cash tax amount is calculated by adding current tax with deferred tax and including all in

adjustments regarding tax and tax expenses. Current tax +deferred tax (including all

adjustments)

Cash tax amount for the year is 2207140 A$. After adding all adjustments with tax. And

in year 2016 the deferred tax liability was 665A$ and in next year all were written off. Except

this there is no deferred tax assets or deferred tax liability since last two years in case of aeon

metals Ltd.

10

Effective tax rate is the rate by which tax is calculated on earning before tax. Effective tax

rate= income tax expense /earning before tax, now there is no information regarding income

tax expense of dark horse resources of year 2017 but in 2016 the tax expenses were 665 A$.

hence tax rate of year 2016 is 0.000423.

In case of Aeon metals Ltd. There are no tax expenses incurred by company since last two

years then we assume that '0' is the tax expense then, tax rate is 0. hence tax rate of Dark Horse

resources is higher than Aeon metal Ltd.

12. List of deferred tax assets or liabilities reported in balance sheet:

Deferred tax is either has a positive impact as 'assets' or negative impact as 'liability' on

balance sheet because of tax owed and tax overpaid due to temporary differences. Deferred tax

can fall into one of two categories, one is deferred tax assets and second is deferred tax liability,

will appeared as entries on balance sheet and represents the negative or positive amount of tax

owed. But there can be one without another, a company can have only deferred tax liability and

deferred tax assets. Deferred tax liability of Dark Horse Resources is 1931A$ and there is no

deferred tax assets or liability in Aeon Metals Ltd. Annual reports.

13. Changes in deferred tax assets or deferred liability:

Yes, in case of Dark horse resources in year 2016 deferred tax liability of 1931 A$ and in

year 2017 all were written off. but in case of Aeon Metals Ltd. There were no tax liability or

deferred tax assets (financial statements, 2017).

14. Calculation of Cash Tax amount:

Cash tax amount is calculated by adding current tax with deferred tax and including all in

adjustments regarding tax and tax expenses. Current tax +deferred tax (including all

adjustments)

Cash tax amount for the year is 2207140 A$. After adding all adjustments with tax. And

in year 2016 the deferred tax liability was 665A$ and in next year all were written off. Except

this there is no deferred tax assets or deferred tax liability since last two years in case of aeon

metals Ltd.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.