Corporate Accounting Project Report: Financial Statement Analysis

VerifiedAdded on 2023/01/11

|14

|2476

|38

Report

AI Summary

This report delves into various aspects of corporate accounting, commencing with an analysis of acquisition costs, including journal entries and maintenance costs. It then explores the factors influencing debenture pricing and provides calculations for debenture issues, accompanied by relevant journal entries. The report further examines share application and allotment processes, presenting journal entries for share transactions, including forfeitures and calls in arrears. It addresses equity adjustments, differentiating between items affecting profit or loss and those directly impacting equity, such as other comprehensive income and foreign currency transactions. Finally, the report presents a cash flow statement for Fool’s Paradise Ltd, analyzing operating, investing, and financing activities to determine the company's cash position at the end of the year, offering insights into its financial performance.

Corporate Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.......................................................................................................................................3

MAIN BODY..............................................................................................................................................3

Week 1....................................................................................................................................................3

Week 2....................................................................................................................................................5

Week 3....................................................................................................................................................7

Week 4....................................................................................................................................................8

Week 5..................................................................................................................................................10

CONCLUSION.........................................................................................................................................12

REFERENCES..........................................................................................................................................14

INTRODUCTION.......................................................................................................................................3

MAIN BODY..............................................................................................................................................3

Week 1....................................................................................................................................................3

Week 2....................................................................................................................................................5

Week 3....................................................................................................................................................7

Week 4....................................................................................................................................................8

Week 5..................................................................................................................................................10

CONCLUSION.........................................................................................................................................12

REFERENCES..........................................................................................................................................14

INTRODUCTION

Corporate accounting is a separate business accounting division which manages corporate

accounts, prepares final reports and cash flow reports, reviewing and assessing corporate

financial performance and accounting for particular events, including amalgamation,

consolidation and presentation of financial statements (Liu, Zeng and An, 2017). The project

report is based on different types of calculations. The first part of report includes information

about acquisition cost and general entries regards to this. In the second part of report calculation

regards to debentures has been done. As well as the end part of report includes information about

preparation of cash flow of given scenario.

MAIN BODY

Week 1

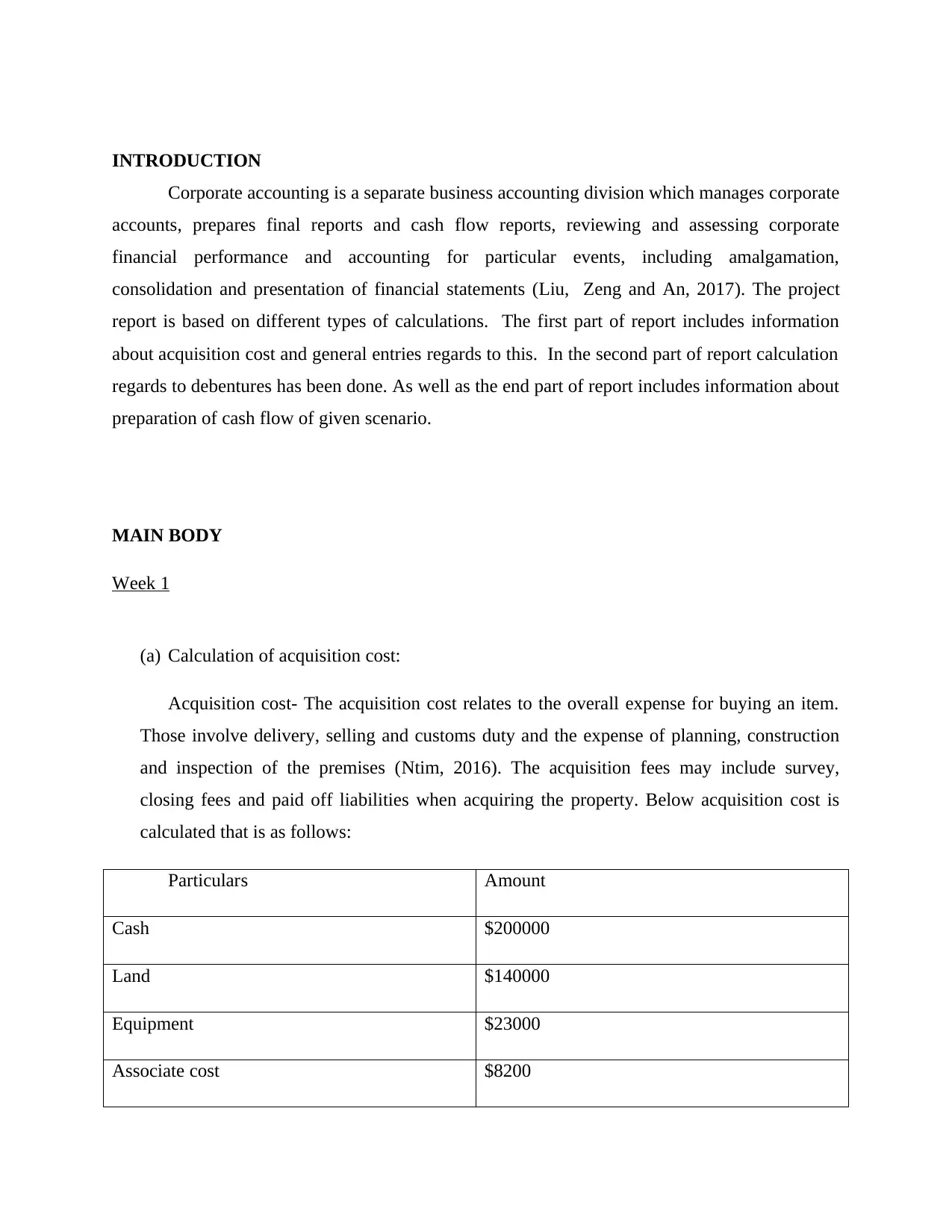

(a) Calculation of acquisition cost:

Acquisition cost- The acquisition cost relates to the overall expense for buying an item.

Those involve delivery, selling and customs duty and the expense of planning, construction

and inspection of the premises (Ntim, 2016). The acquisition fees may include survey,

closing fees and paid off liabilities when acquiring the property. Below acquisition cost is

calculated that is as follows:

Particulars Amount

Cash $200000

Land $140000

Equipment $23000

Associate cost $8200

Corporate accounting is a separate business accounting division which manages corporate

accounts, prepares final reports and cash flow reports, reviewing and assessing corporate

financial performance and accounting for particular events, including amalgamation,

consolidation and presentation of financial statements (Liu, Zeng and An, 2017). The project

report is based on different types of calculations. The first part of report includes information

about acquisition cost and general entries regards to this. In the second part of report calculation

regards to debentures has been done. As well as the end part of report includes information about

preparation of cash flow of given scenario.

MAIN BODY

Week 1

(a) Calculation of acquisition cost:

Acquisition cost- The acquisition cost relates to the overall expense for buying an item.

Those involve delivery, selling and customs duty and the expense of planning, construction

and inspection of the premises (Ntim, 2016). The acquisition fees may include survey,

closing fees and paid off liabilities when acquiring the property. Below acquisition cost is

calculated that is as follows:

Particulars Amount

Cash $200000

Land $140000

Equipment $23000

Associate cost $8200

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Acquisition cost of the machine on the basis of

depreciation

$221200

Working Note:

Associate cost= 5000+2500+700

= 8200

(b) Journal entries:

Journal entries in the books of Gizmo Machine

Date Particulars Debit ($) Credit ($)

Machine account DR

Depreciation account DR

Loss on exchange of equipment account DR

To cash account

To Equipment account

To Land account

To profit on exchange of

land account

To liabilities account

(Being purchase of machine)

221200

20000

7000

28200

50000

100000

40000

30000

Maintained cost calculation

depreciation

$221200

Working Note:

Associate cost= 5000+2500+700

= 8200

(b) Journal entries:

Journal entries in the books of Gizmo Machine

Date Particulars Debit ($) Credit ($)

Machine account DR

Depreciation account DR

Loss on exchange of equipment account DR

To cash account

To Equipment account

To Land account

To profit on exchange of

land account

To liabilities account

(Being purchase of machine)

221200

20000

7000

28200

50000

100000

40000

30000

Maintained cost calculation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Date Particulars Debit Credit

Maintenance expenses account DR

To cash account

650

650

(c) Will the maintenance cost be included in the acquisition cost of the machine?

Inside the acquisition cost of the equipment, the amount of the retained assets is not taken

into consideration as the rule in Australian accounting practice (Balakrishnan, Watts and

Zuo, 2016). Following the acquisition of the property, the expense of upkeep is minimized

and it is paid on the basis of repair expenses, and no vigilance is required. The maintenance

cost entry is reported in the independent accounts and not included in the system acquisition

costs.

Week 2

(a) What factors should be considered in determining the issue price of a debenture.

There are different types of factors that need to be considered in determining issue of

debenture. Below explanation of these factors is done in such manner:

Credit rating- Credit rating is an estimate of a forward debtor's credit risk, a

forecast of his debt recovery potential and an implied predictor of a debtor's

default likelihood. If credit rating will be good then price of debenture will be

accordingly.

Cash flow of company- It is also an important factor in order to determining issue

price of debenture. This is so because on the behalf of cash flow of company,

debenture’s price is determined. As well as if there will be more number of cash

inflows then it will be easier for them to keep prices of debentures at a higher

level.

Maintenance expenses account DR

To cash account

650

650

(c) Will the maintenance cost be included in the acquisition cost of the machine?

Inside the acquisition cost of the equipment, the amount of the retained assets is not taken

into consideration as the rule in Australian accounting practice (Balakrishnan, Watts and

Zuo, 2016). Following the acquisition of the property, the expense of upkeep is minimized

and it is paid on the basis of repair expenses, and no vigilance is required. The maintenance

cost entry is reported in the independent accounts and not included in the system acquisition

costs.

Week 2

(a) What factors should be considered in determining the issue price of a debenture.

There are different types of factors that need to be considered in determining issue of

debenture. Below explanation of these factors is done in such manner:

Credit rating- Credit rating is an estimate of a forward debtor's credit risk, a

forecast of his debt recovery potential and an implied predictor of a debtor's

default likelihood. If credit rating will be good then price of debenture will be

accordingly.

Cash flow of company- It is also an important factor in order to determining issue

price of debenture. This is so because on the behalf of cash flow of company,

debenture’s price is determined. As well as if there will be more number of cash

inflows then it will be easier for them to keep prices of debentures at a higher

level.

Profitability of company- The profitability of company also plays a key role in

determining issue price of debenture. The reason behind this is that on the basis of

it, debentures’ prices are determined (Killian and O'Regan, Joshi and Li, 2016).

Management past performance- Another key factor that is being considered as a

key element in order to set issue price of debenture. This is so because if a

company is able to manage their past performance in an effective manner then it

becomes essential for them to set their prices of debentures at higher level.

So these are the main factors that play a key role in the context of determining prices of

debentures.

(b) Calculation:

(i) Determine the issue price of the debenture

Face value: 200000

Coupon rate: 8 %

Maturity period 6 years

Interest payment: Semi annually

Numbers of interest payment till debenture maturity: 6*2 = 12

Interest payment= Face value 8 coupon rate /2

200000*8%/2 = 80000

The issue price of debenture 280000

determining issue price of debenture. The reason behind this is that on the basis of

it, debentures’ prices are determined (Killian and O'Regan, Joshi and Li, 2016).

Management past performance- Another key factor that is being considered as a

key element in order to set issue price of debenture. This is so because if a

company is able to manage their past performance in an effective manner then it

becomes essential for them to set their prices of debentures at higher level.

So these are the main factors that play a key role in the context of determining prices of

debentures.

(b) Calculation:

(i) Determine the issue price of the debenture

Face value: 200000

Coupon rate: 8 %

Maturity period 6 years

Interest payment: Semi annually

Numbers of interest payment till debenture maturity: 6*2 = 12

Interest payment= Face value 8 coupon rate /2

200000*8%/2 = 80000

The issue price of debenture 280000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(ii) Journal entry:

Date Particular Debit Credit

Bank a/c Dr

To 8 % debenture application a/c(Being

application money received)

200000

200000

8 % Debenture application a/c Dr

Debenture interest a/c Dr

To 8 % debenture a/c

(Being debenture are redeemable with its

interest price)

200000

800000

280000

Week 3

Journal entries:

Date Particular Debit Credit

July 2018 Bank a/c Dr

To Share application a/c

(Application money being

received for 108 million shares

@ $1 each)

108000000 108000000

15-08- Share application a/c Dr

To Share capital a/c

To share allotment

108000000

90000000

180000000

Date Particular Debit Credit

Bank a/c Dr

To 8 % debenture application a/c(Being

application money received)

200000

200000

8 % Debenture application a/c Dr

Debenture interest a/c Dr

To 8 % debenture a/c

(Being debenture are redeemable with its

interest price)

200000

800000

280000

Week 3

Journal entries:

Date Particular Debit Credit

July 2018 Bank a/c Dr

To Share application a/c

(Application money being

received for 108 million shares

@ $1 each)

108000000 108000000

15-08- Share application a/c Dr

To Share capital a/c

To share allotment

108000000

90000000

180000000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Being transfer of application

money into share capital a/c)

20-09- Share allotment a/c Dr

To Share capital

( Allotment money due already

18 million received from

application money)

72000000

722000000

20-09- Cash a/c Dr

Calls in arrears a/c Dr

To share allotment a/c

To Share capital a/c

(Being allotment money received

(72-18=54) and 18 million shares

failed to pay allotment money)

54000000

18000000

18000000

54000000

30-09- Share capital a/c Dr

To forfeited shares a/c

To Class in arrears a/c

(Being 18 million shares get

forfeited)

36000000

21600000

14400000

Week 4

Provide some examples of items that would be adjusted directly against equity, rather than being

included as part of profit or loss.

money into share capital a/c)

20-09- Share allotment a/c Dr

To Share capital

( Allotment money due already

18 million received from

application money)

72000000

722000000

20-09- Cash a/c Dr

Calls in arrears a/c Dr

To share allotment a/c

To Share capital a/c

(Being allotment money received

(72-18=54) and 18 million shares

failed to pay allotment money)

54000000

18000000

18000000

54000000

30-09- Share capital a/c Dr

To forfeited shares a/c

To Class in arrears a/c

(Being 18 million shares get

forfeited)

36000000

21600000

14400000

Week 4

Provide some examples of items that would be adjusted directly against equity, rather than being

included as part of profit or loss.

The accounting norm is used to offer guidelines and instructions to corporate

organizations in Australia so that they can manage a corporation effectively without errors and

complications in the documentation and description of accounting transacts. All terms and

conditions in the whole journal pertaining to income and loss will be contained in the profit and

loss document. Nonetheless, the items on which the International Accounting Committee has

found specific guidelines should be disqualified.

The basis is not the change in the number, which does not impact the cash flow statement since

such purchases are viewed as impractical account expenditure. Each of these components will be

known as such products that do not render a declaration about benefit and expense that are

specifically linked to the equity responsibility line (Shroff, 2017).

Many financial issues will specifically affect equity and balance sheet changes which will not

form part of the income which loss statement of the firm.

Other comprehensive income- These are the items not included as part of the benefit and loss

declaration. Such categories are mentioned below the profit and loss declaration. They can be

called unrealized business profit and loss. The benefit aerials from this commodity are used as

the part of certain extensive income for example, once the Resource is available for sale.

Unrealized profit and loss on bonds- If the valuation of the shares to be issued reduces or

decreases, they are called unrealized income.

Foreign currency transaction - When businesses sell their goods and services outside Australia,

the currency of interest increases will be viewed like an unrealized investment, so that would be

improved or lost.

Profit and loss related with pension plans- If the government changes pension schemes and rules,

the income made from those policies should be handled with additional comprehensive revenue.

Australian accounting standard also define the treatment of other comprehensive income- If the

value of businesses' assets increases after the revaluation, they should be treated in the liabilities

side of equity as other overall income and the quantity of profits accruing should be introduced.

And if the reassessment causes the reduction of asset value, then the excess heading in liability-

side equities will be viewed as deductions.

organizations in Australia so that they can manage a corporation effectively without errors and

complications in the documentation and description of accounting transacts. All terms and

conditions in the whole journal pertaining to income and loss will be contained in the profit and

loss document. Nonetheless, the items on which the International Accounting Committee has

found specific guidelines should be disqualified.

The basis is not the change in the number, which does not impact the cash flow statement since

such purchases are viewed as impractical account expenditure. Each of these components will be

known as such products that do not render a declaration about benefit and expense that are

specifically linked to the equity responsibility line (Shroff, 2017).

Many financial issues will specifically affect equity and balance sheet changes which will not

form part of the income which loss statement of the firm.

Other comprehensive income- These are the items not included as part of the benefit and loss

declaration. Such categories are mentioned below the profit and loss declaration. They can be

called unrealized business profit and loss. The benefit aerials from this commodity are used as

the part of certain extensive income for example, once the Resource is available for sale.

Unrealized profit and loss on bonds- If the valuation of the shares to be issued reduces or

decreases, they are called unrealized income.

Foreign currency transaction - When businesses sell their goods and services outside Australia,

the currency of interest increases will be viewed like an unrealized investment, so that would be

improved or lost.

Profit and loss related with pension plans- If the government changes pension schemes and rules,

the income made from those policies should be handled with additional comprehensive revenue.

Australian accounting standard also define the treatment of other comprehensive income- If the

value of businesses' assets increases after the revaluation, they should be treated in the liabilities

side of equity as other overall income and the quantity of profits accruing should be introduced.

And if the reassessment causes the reduction of asset value, then the excess heading in liability-

side equities will be viewed as deductions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Unrealized gains or losses on derivatives held as cash flow hedges- Cash Flow Hedges: drive it

in OCI and the inefficient fraction flows via P&L while the remaining cash flow will align the

cash flow it is designed to hedge if this cash flow impacts income.

Unrealized gains or losses on derivatives held as cash flow hedges-The Fair value hedge is an

exposure hedge that could be due to a certain danger and that may impact benefit or loss through

adjustments in the fair value of a recognized commodity, responsibility or unrecognizable

undertaking or part of some such object.

Value of unclear dividend- Dividends may be defined as a part of the income earned by the

company or the company. The equity side of the financial statement should be added by unclear

divided. How is the potential dividend interest allocated to shareholders in the potential.

All these items are deemed part of the balance sheet and either contributes to the surplus assets

on the asset portion of the balance sheet or merit the benefit of income and savings or excess

funds on an asset hand. These products are used to change adverse costs and damages within

businesses.

Foreign Currency related to the translation gain and losses- The organization's operating

performance and financial status can be calculated by its usable money, the money the firm uses

in much of its commercial activities. In the case that a foreign company operates mainly

throughout one country and does not depend on the parent corporation, the exchange rate where

it operates is the exchange rate in the country in which it operates. Other international entities

also are more closely related to the parent's operations and are financed largely through the

parent or other dollar-using sources.

Week 5

Cash flows of Fool’s Paradise Ltd for the year to 31 December 2019.

Cash flow- It can be expressed in the form used to undertake strategic the cash inflow value and

outflow activity. Cash flows are used in annual reporting and can be measured for industry

explicitly and indirectly (Warren and Jones, 2018). The calculation of the required cash

generated of each project, which corresponds to the cumulative cash flow resulting from each

project, is the most critical capital expenditure assessments activity. Because businesses depend

in OCI and the inefficient fraction flows via P&L while the remaining cash flow will align the

cash flow it is designed to hedge if this cash flow impacts income.

Unrealized gains or losses on derivatives held as cash flow hedges-The Fair value hedge is an

exposure hedge that could be due to a certain danger and that may impact benefit or loss through

adjustments in the fair value of a recognized commodity, responsibility or unrecognizable

undertaking or part of some such object.

Value of unclear dividend- Dividends may be defined as a part of the income earned by the

company or the company. The equity side of the financial statement should be added by unclear

divided. How is the potential dividend interest allocated to shareholders in the potential.

All these items are deemed part of the balance sheet and either contributes to the surplus assets

on the asset portion of the balance sheet or merit the benefit of income and savings or excess

funds on an asset hand. These products are used to change adverse costs and damages within

businesses.

Foreign Currency related to the translation gain and losses- The organization's operating

performance and financial status can be calculated by its usable money, the money the firm uses

in much of its commercial activities. In the case that a foreign company operates mainly

throughout one country and does not depend on the parent corporation, the exchange rate where

it operates is the exchange rate in the country in which it operates. Other international entities

also are more closely related to the parent's operations and are financed largely through the

parent or other dollar-using sources.

Week 5

Cash flows of Fool’s Paradise Ltd for the year to 31 December 2019.

Cash flow- It can be expressed in the form used to undertake strategic the cash inflow value and

outflow activity. Cash flows are used in annual reporting and can be measured for industry

explicitly and indirectly (Warren and Jones, 2018). The calculation of the required cash

generated of each project, which corresponds to the cumulative cash flow resulting from each

project, is the most critical capital expenditure assessments activity. Because businesses depend

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

on accrual accounts rather than on cash, modifications to extract cash flows from the traditional

accounting documents are important. Estimating cash flows is crucial since incorrect or faulty

details can corrupt the whole process of capital budgeting.

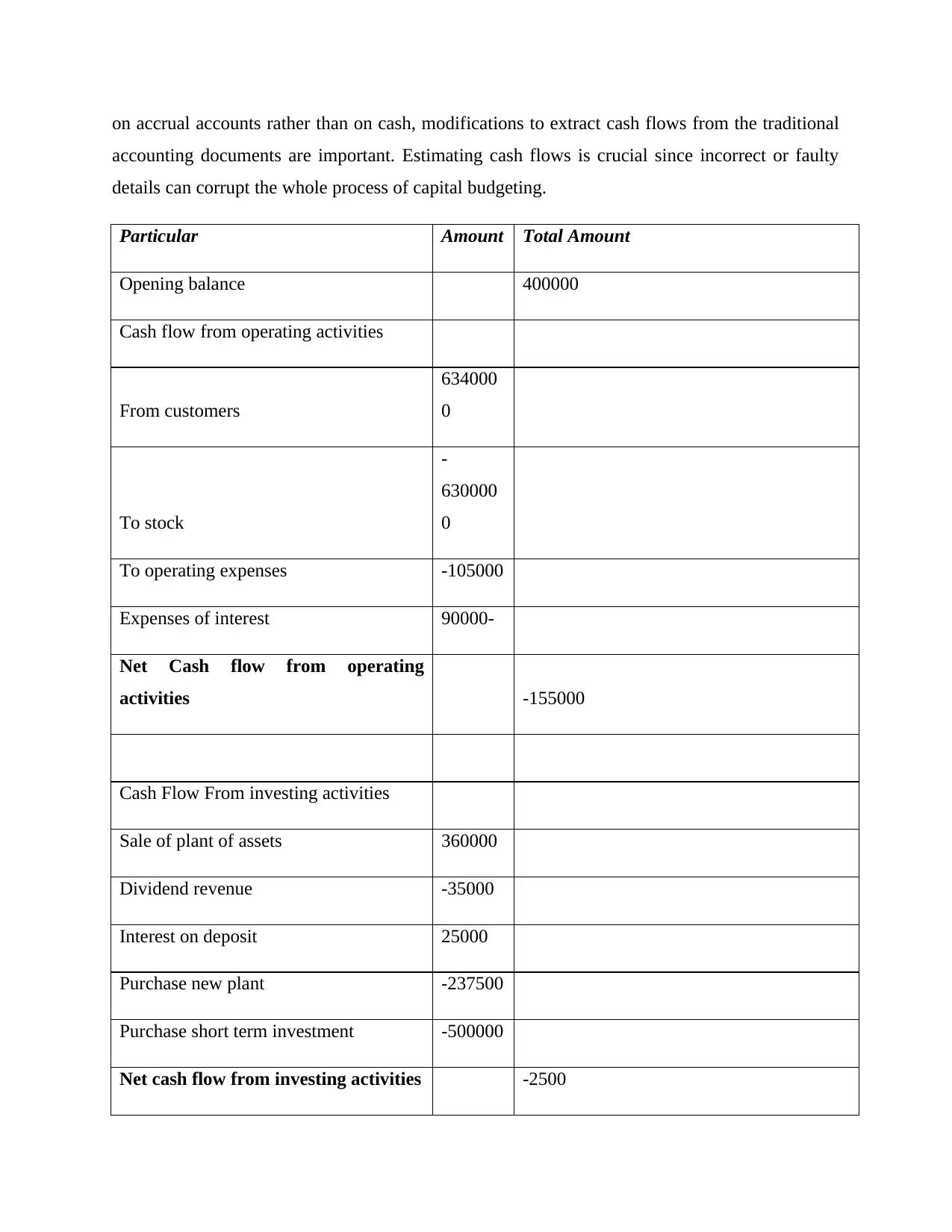

Particular Amount Total Amount

Opening balance 400000

Cash flow from operating activities

From customers

634000

0

To stock

-

630000

0

To operating expenses -105000

Expenses of interest 90000-

Net Cash flow from operating

activities -155000

Cash Flow From investing activities

Sale of plant of assets 360000

Dividend revenue -35000

Interest on deposit 25000

Purchase new plant -237500

Purchase short term investment -500000

Net cash flow from investing activities -2500

accounting documents are important. Estimating cash flows is crucial since incorrect or faulty

details can corrupt the whole process of capital budgeting.

Particular Amount Total Amount

Opening balance 400000

Cash flow from operating activities

From customers

634000

0

To stock

-

630000

0

To operating expenses -105000

Expenses of interest 90000-

Net Cash flow from operating

activities -155000

Cash Flow From investing activities

Sale of plant of assets 360000

Dividend revenue -35000

Interest on deposit 25000

Purchase new plant -237500

Purchase short term investment -500000

Net cash flow from investing activities -2500

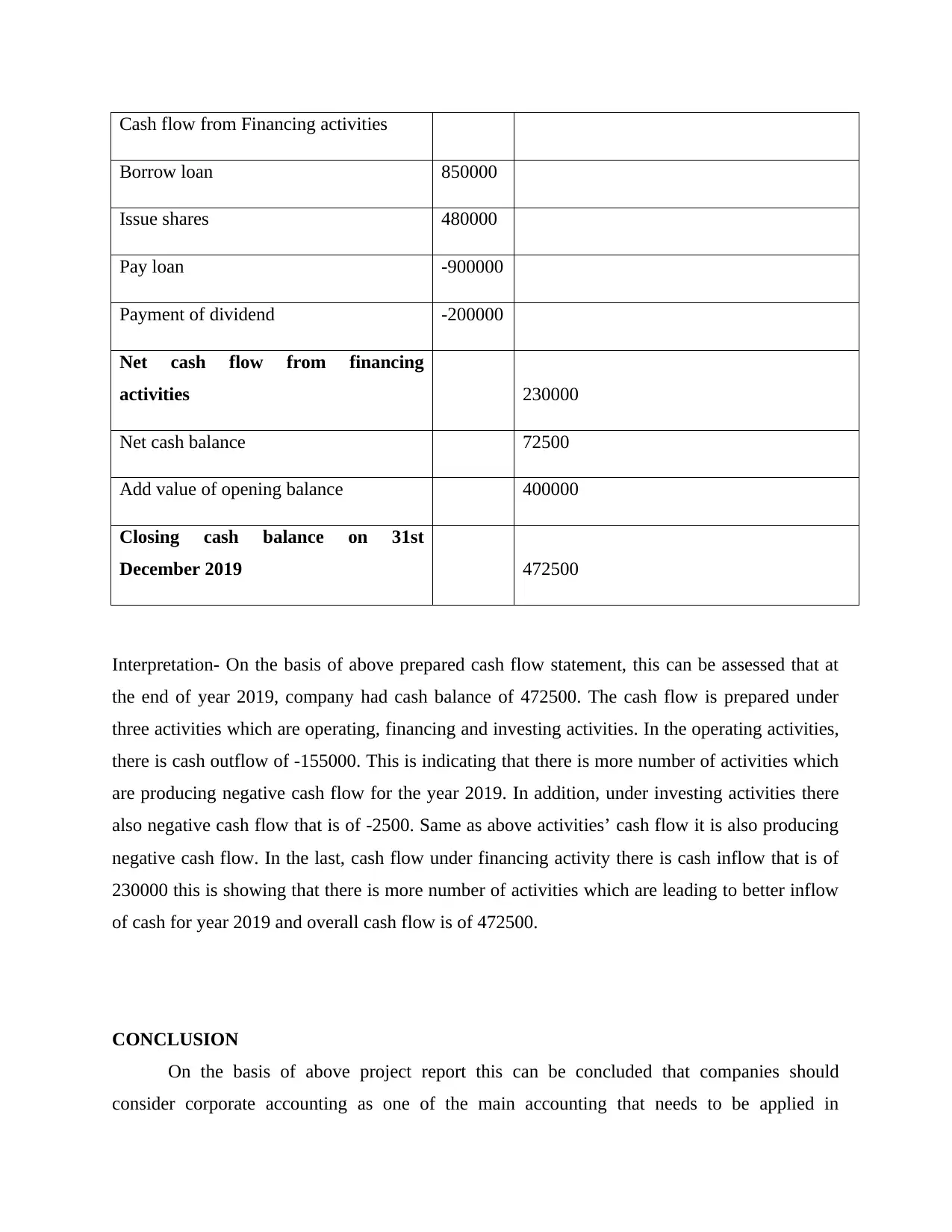

Cash flow from Financing activities

Borrow loan 850000

Issue shares 480000

Pay loan -900000

Payment of dividend -200000

Net cash flow from financing

activities 230000

Net cash balance 72500

Add value of opening balance 400000

Closing cash balance on 31st

December 2019 472500

Interpretation- On the basis of above prepared cash flow statement, this can be assessed that at

the end of year 2019, company had cash balance of 472500. The cash flow is prepared under

three activities which are operating, financing and investing activities. In the operating activities,

there is cash outflow of -155000. This is indicating that there is more number of activities which

are producing negative cash flow for the year 2019. In addition, under investing activities there

also negative cash flow that is of -2500. Same as above activities’ cash flow it is also producing

negative cash flow. In the last, cash flow under financing activity there is cash inflow that is of

230000 this is showing that there is more number of activities which are leading to better inflow

of cash for year 2019 and overall cash flow is of 472500.

CONCLUSION

On the basis of above project report this can be concluded that companies should

consider corporate accounting as one of the main accounting that needs to be applied in

Borrow loan 850000

Issue shares 480000

Pay loan -900000

Payment of dividend -200000

Net cash flow from financing

activities 230000

Net cash balance 72500

Add value of opening balance 400000

Closing cash balance on 31st

December 2019 472500

Interpretation- On the basis of above prepared cash flow statement, this can be assessed that at

the end of year 2019, company had cash balance of 472500. The cash flow is prepared under

three activities which are operating, financing and investing activities. In the operating activities,

there is cash outflow of -155000. This is indicating that there is more number of activities which

are producing negative cash flow for the year 2019. In addition, under investing activities there

also negative cash flow that is of -2500. Same as above activities’ cash flow it is also producing

negative cash flow. In the last, cash flow under financing activity there is cash inflow that is of

230000 this is showing that there is more number of activities which are leading to better inflow

of cash for year 2019 and overall cash flow is of 472500.

CONCLUSION

On the basis of above project report this can be concluded that companies should

consider corporate accounting as one of the main accounting that needs to be applied in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.