Corporate and Financial Accounting Report: Four Company Analysis

VerifiedAdded on 2020/10/22

|9

|2423

|123

Report

AI Summary

This report provides a comprehensive analysis of corporate accounting practices, focusing on financial reporting, corporate regulations, and the role of the International Accounting Standards Board (IASB) and the Australian Accounting Standards Board (AASB) in setting accounting standards. The report examines the functions of financial accounting and its importance in providing information for decision-making by investors and creditors. Furthermore, it includes a detailed analysis of the equity items and debt-equity ratios of four companies: Dark Horse Resources, Aeon Metals, European Lithium, and Accent Resources. The analysis covers the issued capital, reserves, and accumulated losses of each company over a four-year period, offering insights into their financial performance and stability. The report concludes with a comparative analysis of the debt-equity positions of the four companies, highlighting the implications of different financing strategies. The report uses data from 2014-2017 to provide a comparative analysis of the debt equity position of four companies. This report is a valuable resource for students and professionals seeking to understand corporate accounting principles and financial statement analysis.

CORPORATE

AND

FINANCIAL

ACCOUNTING

AND

FINANCIAL

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................4

TASK...............................................................................................................................................4

CORPORATE REGULATIONS.....................................................................................................4

Functions of Financial Accounting and Reporting.....................................................................4

TASK .............................................................................................................................................6

ACCOUNTING STANDARDS SETTING:...................................................................................6

TASK...............................................................................................................................................7

List of items of equity of four companies :.................................................................................7

Comparative analysis of debt equity position of four companies:..............................................9

CONCLUSION................................................................................................................................9

REFERENCES .............................................................................................................................10

INTRODUCTION...........................................................................................................................4

TASK...............................................................................................................................................4

CORPORATE REGULATIONS.....................................................................................................4

Functions of Financial Accounting and Reporting.....................................................................4

TASK .............................................................................................................................................6

ACCOUNTING STANDARDS SETTING:...................................................................................6

TASK...............................................................................................................................................7

List of items of equity of four companies :.................................................................................7

Comparative analysis of debt equity position of four companies:..............................................9

CONCLUSION................................................................................................................................9

REFERENCES .............................................................................................................................10

INTRODUCTION

Corporate accounting is considered as one of the specialised branch of accounting that

deals with the accounting for the companies, preparation of their final account and other

statements. In order to accomplish this particular project there are four companies which are

taken into account such as, Dark horse, Aeon, European lithium and Accent resource. A well

organise research is done on the financial accounting and reporting that is maintained by the

manager of the companies are discussed under this report. Apart from this, critical evaluation of

AASB in international accounting standard setting process is also being done properly. At last,

items those are categories into the owner’s equities of the mentioned companies are examine

accordingly (Schaltegger and Burritt, 2017).

TASK

CORPORATE REGULATIONS

Functions of Financial Accounting and Reporting

The International Accounting Standard Board (IASB) for financial reporting state that the

objective of general purpose financial reporting is to provide financial information about the

reporting entity that is useful to existing and potential investors, lenders and other creditors in

making decisions about providing resources to the entity. Those decisions involve buying, selling

or holding equity and debt instruments, and providing or settling loans and other forms of credit.

Moreover, the motivation for all accounting is to provide information, financial or otherwise, that

can assist the users of financial statements in their economic decision making.

The financial accounting is a process which is undertaken with ultimate aim of:

Identifying

Measuring

Communicating

information to the users of accounting information, in order to allow them to make informed

judgements and decisions. The information which is identified, measured and communicated is

largely financial in nature. The identification if information is undertaken in the bookkeeping

process -covered in financial accounting. Transactions are recorded in the books an records of

business entity by using double entry system of bookkeeping (Panaretou, Shackleton and

Taylor, 2013).

Corporate accounting is considered as one of the specialised branch of accounting that

deals with the accounting for the companies, preparation of their final account and other

statements. In order to accomplish this particular project there are four companies which are

taken into account such as, Dark horse, Aeon, European lithium and Accent resource. A well

organise research is done on the financial accounting and reporting that is maintained by the

manager of the companies are discussed under this report. Apart from this, critical evaluation of

AASB in international accounting standard setting process is also being done properly. At last,

items those are categories into the owner’s equities of the mentioned companies are examine

accordingly (Schaltegger and Burritt, 2017).

TASK

CORPORATE REGULATIONS

Functions of Financial Accounting and Reporting

The International Accounting Standard Board (IASB) for financial reporting state that the

objective of general purpose financial reporting is to provide financial information about the

reporting entity that is useful to existing and potential investors, lenders and other creditors in

making decisions about providing resources to the entity. Those decisions involve buying, selling

or holding equity and debt instruments, and providing or settling loans and other forms of credit.

Moreover, the motivation for all accounting is to provide information, financial or otherwise, that

can assist the users of financial statements in their economic decision making.

The financial accounting is a process which is undertaken with ultimate aim of:

Identifying

Measuring

Communicating

information to the users of accounting information, in order to allow them to make informed

judgements and decisions. The information which is identified, measured and communicated is

largely financial in nature. The identification if information is undertaken in the bookkeeping

process -covered in financial accounting. Transactions are recorded in the books an records of

business entity by using double entry system of bookkeeping (Panaretou, Shackleton and

Taylor, 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial accounting focused on following areas;

Identification and recording in accounting procedures such as the preparation of control

accounts and bank reconciliation statements ensures that the information contained in the

double entry system is accurate. Items in the control accounts or bank reconciliation for

which there is inadequate information are initially recorded and subsequently corrected

by suspense account. This suspense account is a working account that must be cleared

before the financial statements are published. a suspense account should never show in

either a profit and loss statements or in balance sheet.

Measuring the financial performance of a sole trader by profit and loss account and

balance sheet.

Communicating by preparing the financial statements of a sole trader or a not for profit

organisation(Hoi, Wu and Zhang,2013) .

A new financial statement that measures the cash position of a business entity is also

examined. Therefore while financial accounting primarily focused on identifying and measuring

financial information, Advanced financial accounting focuses on the communication of this

information to users of accounting information, as the ultimate aim of the financial accounting

process is to produce financial information about an entity that is understandable, relevant,

reliable and comparable to aid the users of financial information make decisions about the

business entity. Moreover, information asymmetry between the firm or the bank and third parties,

whether these are investors, creditors, employees or the public authorities, can thus safely be

considered as one of the main culprits of financial and economic crises and, as such, lies at heart

of actors' concerns. Disclosures, whether voluntary or mandatory, would have the virtue of

reducing information asymmetries and of allowing effective control of managers, and re-

establishing good governance.

TASK

ACCOUNTING STANDARDS SETTING:

A Technical issue may be identified by the International Accounting Standards Board (IASB) or

the IFRS Interpretations Committee (IFRIC).

Australia has adopted International Financial Reporting Standards (IFRS) since 1 January 2005,

in line with a strategic direction from the Financial Reporting Council. Therefore, issues on the

Identification and recording in accounting procedures such as the preparation of control

accounts and bank reconciliation statements ensures that the information contained in the

double entry system is accurate. Items in the control accounts or bank reconciliation for

which there is inadequate information are initially recorded and subsequently corrected

by suspense account. This suspense account is a working account that must be cleared

before the financial statements are published. a suspense account should never show in

either a profit and loss statements or in balance sheet.

Measuring the financial performance of a sole trader by profit and loss account and

balance sheet.

Communicating by preparing the financial statements of a sole trader or a not for profit

organisation(Hoi, Wu and Zhang,2013) .

A new financial statement that measures the cash position of a business entity is also

examined. Therefore while financial accounting primarily focused on identifying and measuring

financial information, Advanced financial accounting focuses on the communication of this

information to users of accounting information, as the ultimate aim of the financial accounting

process is to produce financial information about an entity that is understandable, relevant,

reliable and comparable to aid the users of financial information make decisions about the

business entity. Moreover, information asymmetry between the firm or the bank and third parties,

whether these are investors, creditors, employees or the public authorities, can thus safely be

considered as one of the main culprits of financial and economic crises and, as such, lies at heart

of actors' concerns. Disclosures, whether voluntary or mandatory, would have the virtue of

reducing information asymmetries and of allowing effective control of managers, and re-

establishing good governance.

TASK

ACCOUNTING STANDARDS SETTING:

A Technical issue may be identified by the International Accounting Standards Board (IASB) or

the IFRS Interpretations Committee (IFRIC).

Australia has adopted International Financial Reporting Standards (IFRS) since 1 January 2005,

in line with a strategic direction from the Financial Reporting Council. Therefore, issues on the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

IASB work program and the IFRIC work program are also included on the AASB work program,

although the degree of involvement by the AASB varies issue-by-issue and may be substantive

or non substantive.

A technical issue may also be identified by the International Public Sector Accounting Standards

Board (IPSASB). The AASB closely monitors the IPSASB work program and undertakes work

on selected topics, based on their significance to public sector financial reporting in Australia.

Therefore, issues on the IASB work program and the IFRIC work program are also included on

the AASB work program, although the degree of involvement by the AASB varies issue-by-issue

and may be substantive or non-substantive (Hoi, 2013).

The IFRS Foundation was established on 1 march 2010 and at the time of writing is comprised

of 21 trustees. The trustees are appointed by Monitoring Board and report to Monitoring board.

Some activities of IFRS Foundation are as follows;

Appointing members of the IASB, the IFRS Advisory council and the IFRS interpretation

committee.

Overseeing the work of the IASB, in the terms of structure, strategy and effectiveness.

Consideration of, but not determination of the IASB's agenda.

Establishing and amending the operations procedures, consultative arrangements and due

process for the three organisations (the IASB, the IFRS Advisory council and the IFRS

interpretations committee).

Establishing and maintaining financing arrangements.

The mission of the AASB is to develop and maintain high quality financial reporting standards

for all sectors of Australian economy and to contribute to the development of global finance

reporting. the major standard-setting objectives of the AASB are to:

issue Australian versions of international Accounting standards boards documents.

Produce standards that treat like transactions consistently.

3. Significantly influence the development of international financial reporting standards .

4. Identify areas requiring fundamental review and introduce standards to cover those

areas and promote globally consistent application and interpretation of accounting standards

(Aebi, Sabato and Schmid, 2012).

although the degree of involvement by the AASB varies issue-by-issue and may be substantive

or non substantive.

A technical issue may also be identified by the International Public Sector Accounting Standards

Board (IPSASB). The AASB closely monitors the IPSASB work program and undertakes work

on selected topics, based on their significance to public sector financial reporting in Australia.

Therefore, issues on the IASB work program and the IFRIC work program are also included on

the AASB work program, although the degree of involvement by the AASB varies issue-by-issue

and may be substantive or non-substantive (Hoi, 2013).

The IFRS Foundation was established on 1 march 2010 and at the time of writing is comprised

of 21 trustees. The trustees are appointed by Monitoring Board and report to Monitoring board.

Some activities of IFRS Foundation are as follows;

Appointing members of the IASB, the IFRS Advisory council and the IFRS interpretation

committee.

Overseeing the work of the IASB, in the terms of structure, strategy and effectiveness.

Consideration of, but not determination of the IASB's agenda.

Establishing and amending the operations procedures, consultative arrangements and due

process for the three organisations (the IASB, the IFRS Advisory council and the IFRS

interpretations committee).

Establishing and maintaining financing arrangements.

The mission of the AASB is to develop and maintain high quality financial reporting standards

for all sectors of Australian economy and to contribute to the development of global finance

reporting. the major standard-setting objectives of the AASB are to:

issue Australian versions of international Accounting standards boards documents.

Produce standards that treat like transactions consistently.

3. Significantly influence the development of international financial reporting standards .

4. Identify areas requiring fundamental review and introduce standards to cover those

areas and promote globally consistent application and interpretation of accounting standards

(Aebi, Sabato and Schmid, 2012).

TASK

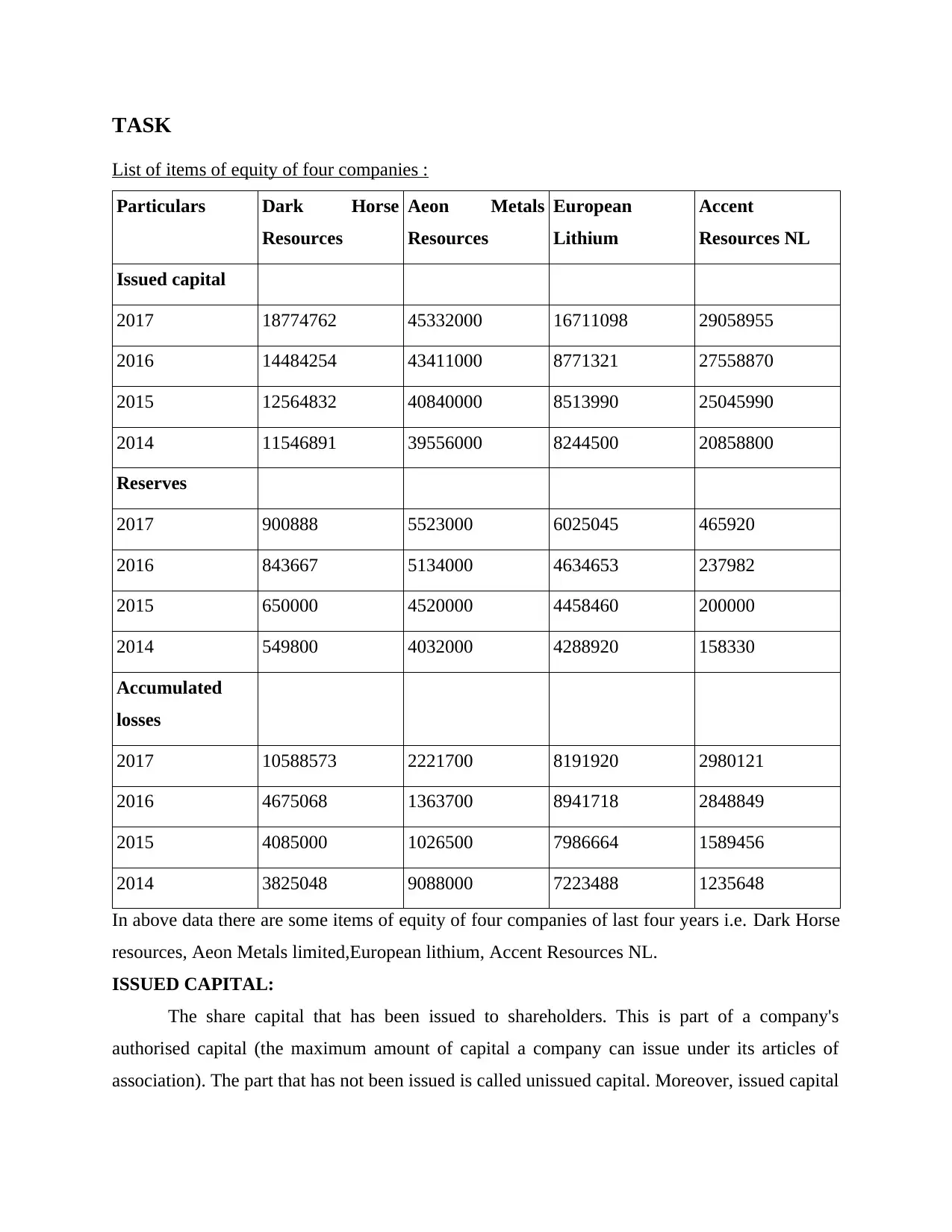

List of items of equity of four companies :

Particulars Dark Horse

Resources

Aeon Metals

Resources

European

Lithium

Accent

Resources NL

Issued capital

2017 18774762 45332000 16711098 29058955

2016 14484254 43411000 8771321 27558870

2015 12564832 40840000 8513990 25045990

2014 11546891 39556000 8244500 20858800

Reserves

2017 900888 5523000 6025045 465920

2016 843667 5134000 4634653 237982

2015 650000 4520000 4458460 200000

2014 549800 4032000 4288920 158330

Accumulated

losses

2017 10588573 2221700 8191920 2980121

2016 4675068 1363700 8941718 2848849

2015 4085000 1026500 7986664 1589456

2014 3825048 9088000 7223488 1235648

In above data there are some items of equity of four companies of last four years i.e. Dark Horse

resources, Aeon Metals limited,European lithium, Accent Resources NL.

ISSUED CAPITAL:

The share capital that has been issued to shareholders. This is part of a company's

authorised capital (the maximum amount of capital a company can issue under its articles of

association). The part that has not been issued is called unissued capital. Moreover, issued capital

List of items of equity of four companies :

Particulars Dark Horse

Resources

Aeon Metals

Resources

European

Lithium

Accent

Resources NL

Issued capital

2017 18774762 45332000 16711098 29058955

2016 14484254 43411000 8771321 27558870

2015 12564832 40840000 8513990 25045990

2014 11546891 39556000 8244500 20858800

Reserves

2017 900888 5523000 6025045 465920

2016 843667 5134000 4634653 237982

2015 650000 4520000 4458460 200000

2014 549800 4032000 4288920 158330

Accumulated

losses

2017 10588573 2221700 8191920 2980121

2016 4675068 1363700 8941718 2848849

2015 4085000 1026500 7986664 1589456

2014 3825048 9088000 7223488 1235648

In above data there are some items of equity of four companies of last four years i.e. Dark Horse

resources, Aeon Metals limited,European lithium, Accent Resources NL.

ISSUED CAPITAL:

The share capital that has been issued to shareholders. This is part of a company's

authorised capital (the maximum amount of capital a company can issue under its articles of

association). The part that has not been issued is called unissued capital. Moreover, issued capital

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of Dark Horse Resources increases year after year, but issued capital of Aeon Metals Limited is

stable since last year (Aldaya and et. al., 2012).

Reasons behind increments in issued capitals of all companies may be, companies wants to

reduce its debts, or company plans to invest in new projects, or may be due to excess of retained

earnings that's why company decided to issue new shares to existing shareholders and utilise the

retained earnings. An increase in the total of capital stock showing on a company's balance sheet

is bad for investors, because it represents the issuance of additional stock shares, which dilute the

ownership value of investors' existing shares. However, the increase in capital stock may, in the

long run, benefit investors in the form of increased return on equity through capital gains, an

increase in dividend payouts or both.

RESERVES:

Liquid assets held by a bank, company or government in order to meet expected future

payments and/or emergency needs. In the case of a bank, its reserves are cash and other liquid

deposits held either in its vaults or with the central bank. In the case of a company, reserves are

normally built up from retained earnings (i.e. profits not distributed as dividends to

shareholders). In the case of a government, its official reserves comprise foreign currency

(foreign exchange reserves) as well as gold and IMF special drawing rights (Mahoney, and et.

al., 2013).

In above comparative statement, reserves increases year after year, reserves depend on

funds availability and shows liquidity performance of company as shown above, both companies

have reserves normally built up from retained earnings and extra profits .

ACCUMULATED LOSSES:

The retained earnings of a corporation are the accumulated net income of the corporation that is

retained by the corporation at a particular point of time, such as at the end of the reporting

period. At the end of that period, the net income (or net loss) at that point is transferred from the

Profit and Loss Account to the retained earnings account. If the balance of the retained earnings

account is negative it may be called accumulated losses, retained losses or accumulated deficit.

Any part of a credit balance in the account can be capitalised, by the issue of bonus shares, and

the balance is available for distribution of dividends to shareholders, and the residue is carried

forward into the next period. Dividends can only be paid out of the positive balance of the

retained earnings account at the time that payment is to be made (Bhasin, 2015).

stable since last year (Aldaya and et. al., 2012).

Reasons behind increments in issued capitals of all companies may be, companies wants to

reduce its debts, or company plans to invest in new projects, or may be due to excess of retained

earnings that's why company decided to issue new shares to existing shareholders and utilise the

retained earnings. An increase in the total of capital stock showing on a company's balance sheet

is bad for investors, because it represents the issuance of additional stock shares, which dilute the

ownership value of investors' existing shares. However, the increase in capital stock may, in the

long run, benefit investors in the form of increased return on equity through capital gains, an

increase in dividend payouts or both.

RESERVES:

Liquid assets held by a bank, company or government in order to meet expected future

payments and/or emergency needs. In the case of a bank, its reserves are cash and other liquid

deposits held either in its vaults or with the central bank. In the case of a company, reserves are

normally built up from retained earnings (i.e. profits not distributed as dividends to

shareholders). In the case of a government, its official reserves comprise foreign currency

(foreign exchange reserves) as well as gold and IMF special drawing rights (Mahoney, and et.

al., 2013).

In above comparative statement, reserves increases year after year, reserves depend on

funds availability and shows liquidity performance of company as shown above, both companies

have reserves normally built up from retained earnings and extra profits .

ACCUMULATED LOSSES:

The retained earnings of a corporation are the accumulated net income of the corporation that is

retained by the corporation at a particular point of time, such as at the end of the reporting

period. At the end of that period, the net income (or net loss) at that point is transferred from the

Profit and Loss Account to the retained earnings account. If the balance of the retained earnings

account is negative it may be called accumulated losses, retained losses or accumulated deficit.

Any part of a credit balance in the account can be capitalised, by the issue of bonus shares, and

the balance is available for distribution of dividends to shareholders, and the residue is carried

forward into the next period. Dividends can only be paid out of the positive balance of the

retained earnings account at the time that payment is to be made (Bhasin, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

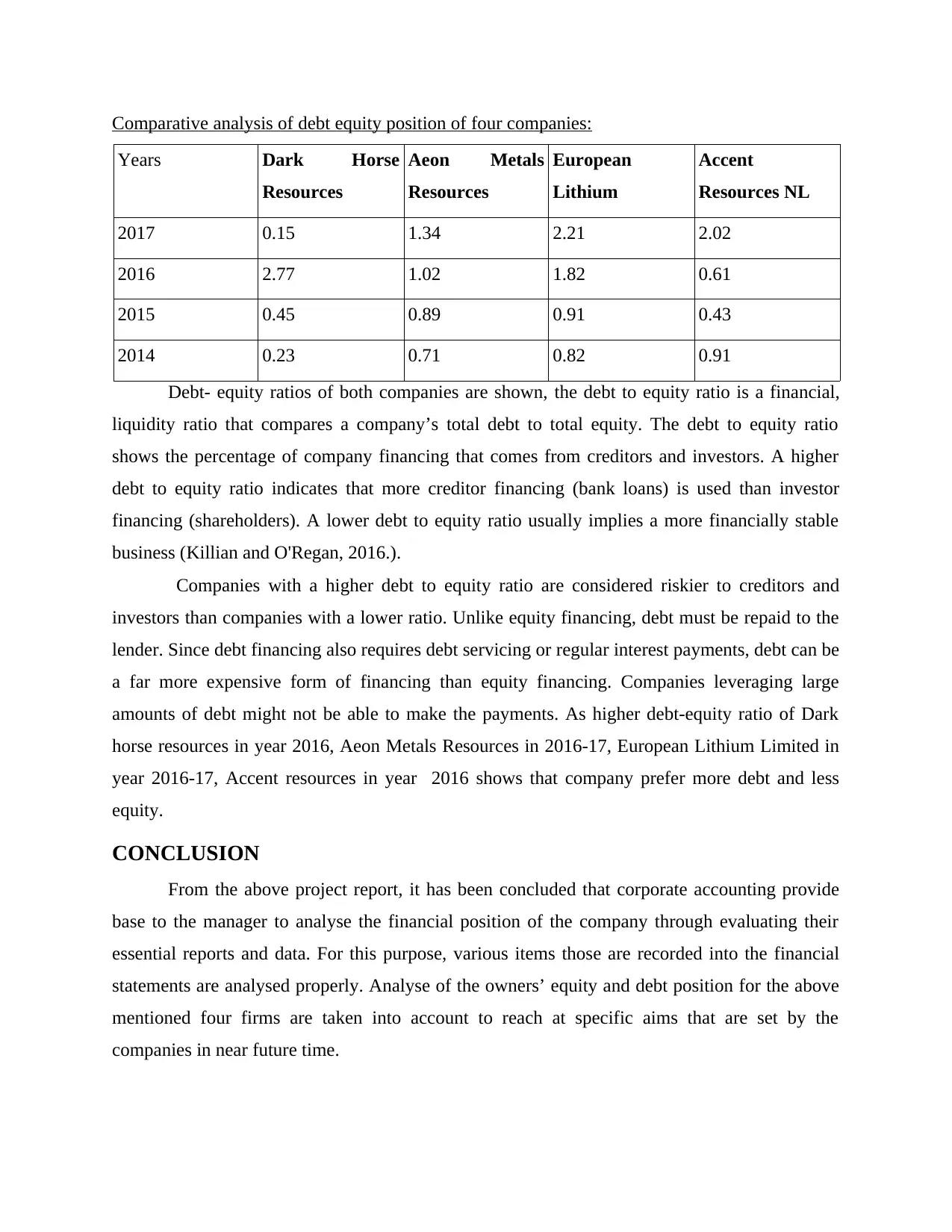

Comparative analysis of debt equity position of four companies:

Years Dark Horse

Resources

Aeon Metals

Resources

European

Lithium

Accent

Resources NL

2017 0.15 1.34 2.21 2.02

2016 2.77 1.02 1.82 0.61

2015 0.45 0.89 0.91 0.43

2014 0.23 0.71 0.82 0.91

Debt- equity ratios of both companies are shown, the debt to equity ratio is a financial,

liquidity ratio that compares a company’s total debt to total equity. The debt to equity ratio

shows the percentage of company financing that comes from creditors and investors. A higher

debt to equity ratio indicates that more creditor financing (bank loans) is used than investor

financing (shareholders). A lower debt to equity ratio usually implies a more financially stable

business (Killian and O'Regan, 2016.).

Companies with a higher debt to equity ratio are considered riskier to creditors and

investors than companies with a lower ratio. Unlike equity financing, debt must be repaid to the

lender. Since debt financing also requires debt servicing or regular interest payments, debt can be

a far more expensive form of financing than equity financing. Companies leveraging large

amounts of debt might not be able to make the payments. As higher debt-equity ratio of Dark

horse resources in year 2016, Aeon Metals Resources in 2016-17, European Lithium Limited in

year 2016-17, Accent resources in year 2016 shows that company prefer more debt and less

equity.

CONCLUSION

From the above project report, it has been concluded that corporate accounting provide

base to the manager to analyse the financial position of the company through evaluating their

essential reports and data. For this purpose, various items those are recorded into the financial

statements are analysed properly. Analyse of the owners’ equity and debt position for the above

mentioned four firms are taken into account to reach at specific aims that are set by the

companies in near future time.

Years Dark Horse

Resources

Aeon Metals

Resources

European

Lithium

Accent

Resources NL

2017 0.15 1.34 2.21 2.02

2016 2.77 1.02 1.82 0.61

2015 0.45 0.89 0.91 0.43

2014 0.23 0.71 0.82 0.91

Debt- equity ratios of both companies are shown, the debt to equity ratio is a financial,

liquidity ratio that compares a company’s total debt to total equity. The debt to equity ratio

shows the percentage of company financing that comes from creditors and investors. A higher

debt to equity ratio indicates that more creditor financing (bank loans) is used than investor

financing (shareholders). A lower debt to equity ratio usually implies a more financially stable

business (Killian and O'Regan, 2016.).

Companies with a higher debt to equity ratio are considered riskier to creditors and

investors than companies with a lower ratio. Unlike equity financing, debt must be repaid to the

lender. Since debt financing also requires debt servicing or regular interest payments, debt can be

a far more expensive form of financing than equity financing. Companies leveraging large

amounts of debt might not be able to make the payments. As higher debt-equity ratio of Dark

horse resources in year 2016, Aeon Metals Resources in 2016-17, European Lithium Limited in

year 2016-17, Accent resources in year 2016 shows that company prefer more debt and less

equity.

CONCLUSION

From the above project report, it has been concluded that corporate accounting provide

base to the manager to analyse the financial position of the company through evaluating their

essential reports and data. For this purpose, various items those are recorded into the financial

statements are analysed properly. Analyse of the owners’ equity and debt position for the above

mentioned four firms are taken into account to reach at specific aims that are set by the

companies in near future time.

REFERENCES

Books and Journals:

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues, concepts

and practice. Routledge.

Panaretou, A., Shackleton, M. B. and Taylor, P.A., 2013. Corporate risk management and hedge

accounting. Contemporary accounting research. 30(1). pp.116-139.

Hoi, C. K., Wu, Q. and Zhang, H., 2013. Is corporate social responsibility (CSR) associated with

tax avoidance? Evidence from irresponsible CSR activities. The Accounting Review.

88(6). pp.2025-2059.

Aebi, V., Sabato, G. and Schmid, M., 2012. Risk management, corporate governance, and bank

performance in the financial crisis. Journal of Banking & Finance. 36(12). pp.3213-3226.

Aldaya, M. M. and et. al., 2012. The water footprint assessment manual: Setting the global

standard. Routledge.

Mahoney, L. S. and et. al., 2013. A research note on standalone corporate social responsibility

reports: Signaling or greenwashing? Critical perspectives on Accounting. 24(4-5).

pp.350-359.

Bhasin, M. L., 2015. Creative accounting practices in the Indian corporate sector: An empirical

study.

Killian, S. and O'Regan, P., 2016. Social accounting and the co-creation of corporate legitimacy.

Accounting, Organizations and Society. 50. pp.1-12.

Books and Journals:

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues, concepts

and practice. Routledge.

Panaretou, A., Shackleton, M. B. and Taylor, P.A., 2013. Corporate risk management and hedge

accounting. Contemporary accounting research. 30(1). pp.116-139.

Hoi, C. K., Wu, Q. and Zhang, H., 2013. Is corporate social responsibility (CSR) associated with

tax avoidance? Evidence from irresponsible CSR activities. The Accounting Review.

88(6). pp.2025-2059.

Aebi, V., Sabato, G. and Schmid, M., 2012. Risk management, corporate governance, and bank

performance in the financial crisis. Journal of Banking & Finance. 36(12). pp.3213-3226.

Aldaya, M. M. and et. al., 2012. The water footprint assessment manual: Setting the global

standard. Routledge.

Mahoney, L. S. and et. al., 2013. A research note on standalone corporate social responsibility

reports: Signaling or greenwashing? Critical perspectives on Accounting. 24(4-5).

pp.350-359.

Bhasin, M. L., 2015. Creative accounting practices in the Indian corporate sector: An empirical

study.

Killian, S. and O'Regan, P., 2016. Social accounting and the co-creation of corporate legitimacy.

Accounting, Organizations and Society. 50. pp.1-12.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.