King's Own Institute: Corporate Financial Management Report - FIN200

VerifiedAdded on 2022/08/23

|9

|2020

|19

Report

AI Summary

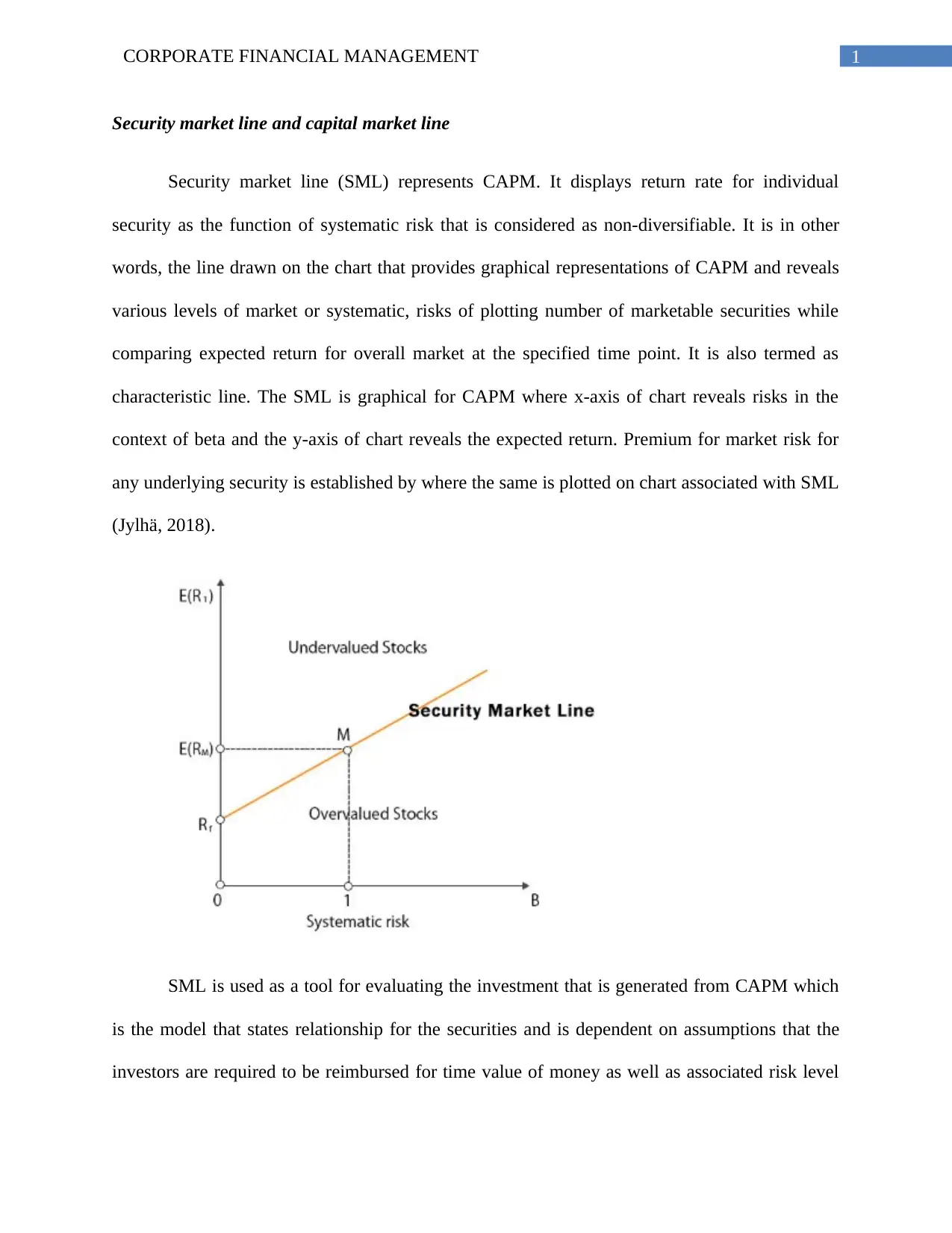

This report delves into the core concepts of Corporate Financial Management, specifically examining the Security Market Line (SML) and the Capital Market Line (CML). The report begins by defining the SML as a graphical representation of the Capital Asset Pricing Model (CAPM), illustrating the relationship between expected return and systematic risk (beta). It explains how the SML is used to evaluate investments based on their position relative to the line, indicating whether a security is undervalued or overvalued. The report then contrasts the SML with the CML, which measures risk through standard deviation and represents efficient portfolios. It highlights the differences in how risk is measured (beta vs. standard deviation) and the types of portfolios each line defines. Furthermore, the report outlines the formulas used to plot both lines and discusses their applications in investment analysis, including comparing securities and assessing their risk-return profiles. It also touches upon the limitations of using these tools in isolation and concludes by emphasizing the importance of understanding both SML and CML for effective corporate financial management. The report includes the differences between the SML and CML with the help of graphical representations.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.