FIN200 Corporate Finance Report: CML, SML, Minimum Variance

VerifiedAdded on 2022/08/27

|12

|2509

|17

Report

AI Summary

This report delves into key aspects of corporate finance, differentiating between the Capital Market Line (CML) and the Security Market Line (SML) and exploring their applications in investment analysis. It provides a detailed explanation of minimum variance portfolios, highlighting their role in managing risk and return. Furthermore, the report examines the Capital Asset Pricing Model (CAPM), illustrating its use in evaluating the required rate of return on investments. Through graphical representations and in-depth analysis, the report aims to equip investors with the knowledge needed to make informed decisions regarding stock valuation and portfolio management. It covers the evaluation of stocks, the impact of market imperfections, and the significance of CAPM in comparison to WACC. The report concludes by summarizing the key concepts and emphasizing the importance of these financial tools in increasing shareholder value.

Running head: CORPORATE FINANCIAL MANAGEMENT

CORPORATE FINANCIAL MANAGEMENT

Name of the Student

Name of the University

Author Note

CORPORATE FINANCIAL MANAGEMENT

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CORPORATE FINANCIAL MANAGEMENT

1. Introduction

The report that is being prepared is on the aspects of corporate finance that will

describe all the differences between the Capital Market Line (CML) and Security Market

Line (SML) and there is also a further explanation of minimum variance portfolios and

Capital Asset Pricing Model (CAPM). For the investment purpose, these tools are used by the

investors so that they can get a clear idea about the status of the stocks on which they will

invest and also help in decision making. In the first part of the report, all the points related to

the differences of the Capital Market Line (CML) and Security Market Line (SML) are

explained with the help of graphs. After that, minimum variance portfolios are explained

through which it has helps the investors at the time of investments to determine the risk and

return upon which they are investing. In the last part, the Capital Asset Pricing Model

(CAPM) is being explained with graphs that will help in the evaluation of the required rate of

return upon the investment.

2. A Graphical representation on the differences of Capital Market Line

(CML) and Security Market Line (SML)

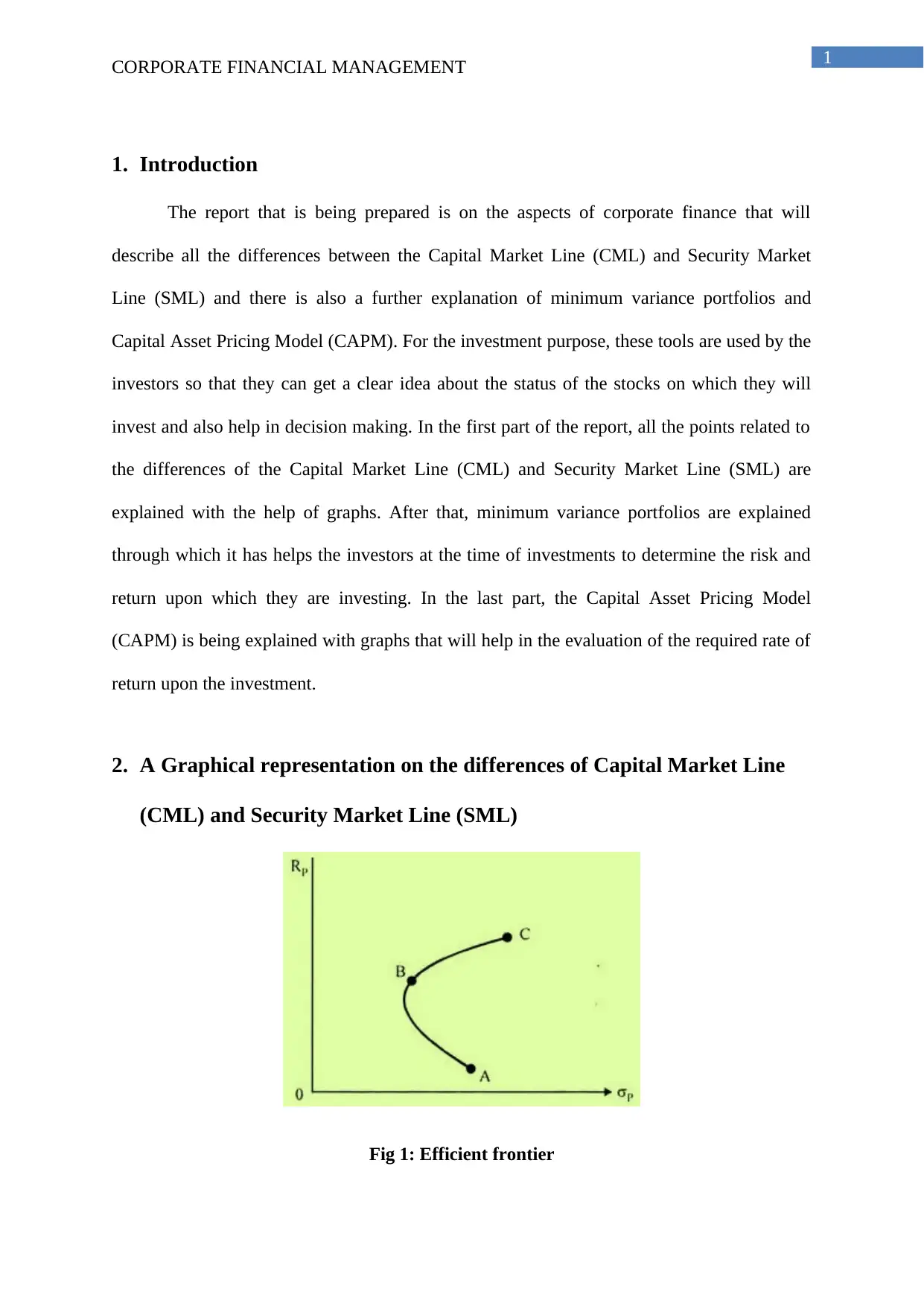

Fig 1: Efficient frontier

CORPORATE FINANCIAL MANAGEMENT

1. Introduction

The report that is being prepared is on the aspects of corporate finance that will

describe all the differences between the Capital Market Line (CML) and Security Market

Line (SML) and there is also a further explanation of minimum variance portfolios and

Capital Asset Pricing Model (CAPM). For the investment purpose, these tools are used by the

investors so that they can get a clear idea about the status of the stocks on which they will

invest and also help in decision making. In the first part of the report, all the points related to

the differences of the Capital Market Line (CML) and Security Market Line (SML) are

explained with the help of graphs. After that, minimum variance portfolios are explained

through which it has helps the investors at the time of investments to determine the risk and

return upon which they are investing. In the last part, the Capital Asset Pricing Model

(CAPM) is being explained with graphs that will help in the evaluation of the required rate of

return upon the investment.

2. A Graphical representation on the differences of Capital Market Line

(CML) and Security Market Line (SML)

Fig 1: Efficient frontier

2

CORPORATE FINANCIAL MANAGEMENT

(Source: Heinze 2018)

The above diagram which is presented, it can be seen that the investors got two option

to invest, with they have to invest on point B or C, or they want to invest in point A and B.

The investors will get an idea in seeing this graph as they could invest in one of the securities

in-between the B and C. both the points have a similar risk level if compared then stock C

will give a much more return than the stock A. Thus, the point C is more preferable for

investment.

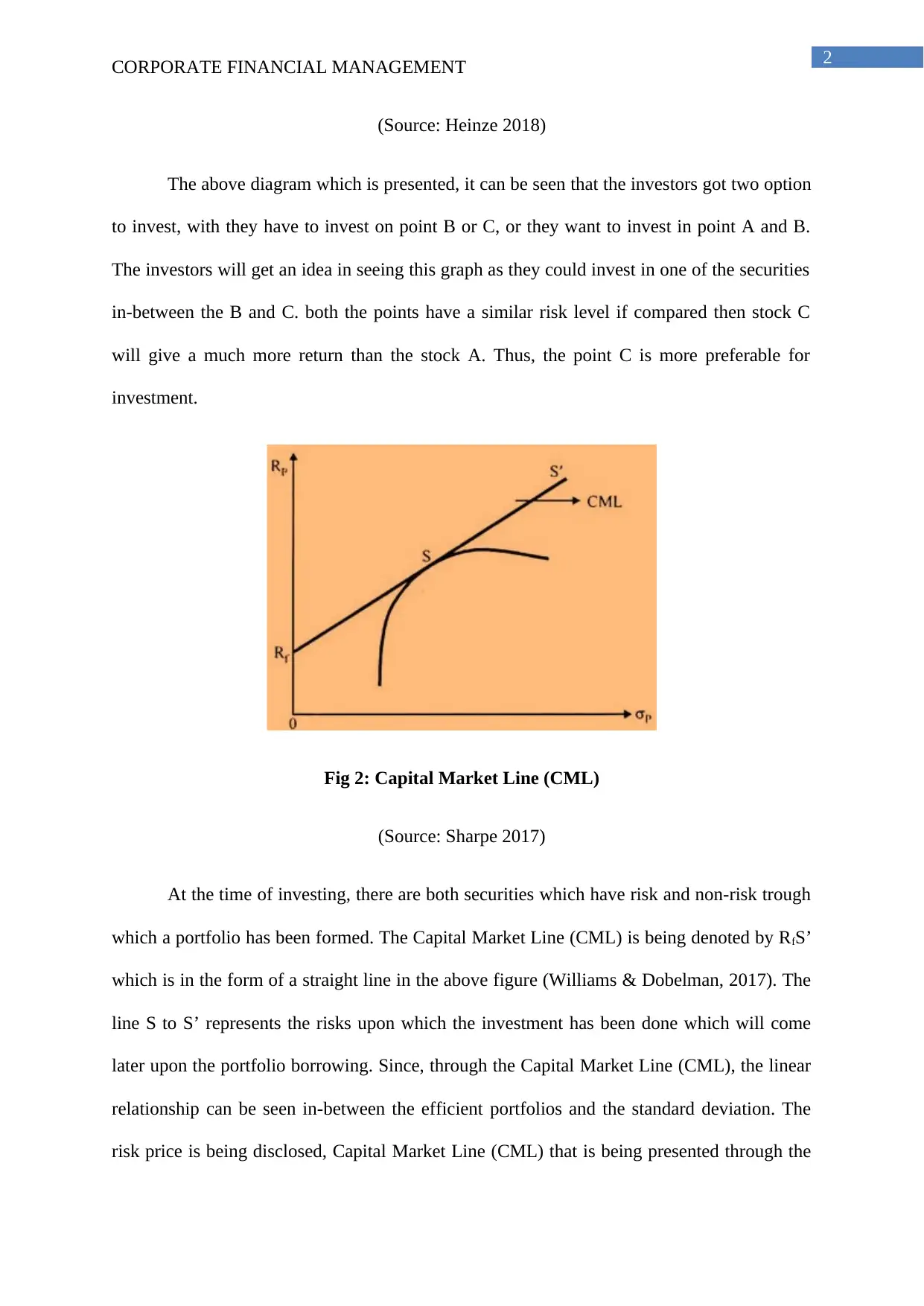

Fig 2: Capital Market Line (CML)

(Source: Sharpe 2017)

At the time of investing, there are both securities which have risk and non-risk trough

which a portfolio has been formed. The Capital Market Line (CML) is being denoted by RfS’

which is in the form of a straight line in the above figure (Williams & Dobelman, 2017). The

line S to S’ represents the risks upon which the investment has been done which will come

later upon the portfolio borrowing. Since, through the Capital Market Line (CML), the linear

relationship can be seen in-between the efficient portfolios and the standard deviation. The

risk price is being disclosed, Capital Market Line (CML) that is being presented through the

CORPORATE FINANCIAL MANAGEMENT

(Source: Heinze 2018)

The above diagram which is presented, it can be seen that the investors got two option

to invest, with they have to invest on point B or C, or they want to invest in point A and B.

The investors will get an idea in seeing this graph as they could invest in one of the securities

in-between the B and C. both the points have a similar risk level if compared then stock C

will give a much more return than the stock A. Thus, the point C is more preferable for

investment.

Fig 2: Capital Market Line (CML)

(Source: Sharpe 2017)

At the time of investing, there are both securities which have risk and non-risk trough

which a portfolio has been formed. The Capital Market Line (CML) is being denoted by RfS’

which is in the form of a straight line in the above figure (Williams & Dobelman, 2017). The

line S to S’ represents the risks upon which the investment has been done which will come

later upon the portfolio borrowing. Since, through the Capital Market Line (CML), the linear

relationship can be seen in-between the efficient portfolios and the standard deviation. The

risk price is being disclosed, Capital Market Line (CML) that is being presented through the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CORPORATE FINANCIAL MANAGEMENT

line slope and the return that is being projected above the risk-free rate which is being with

in-line with the standard deviation which is being connected with the terms of portfolio,

which is being accustomed as the market portfolio.

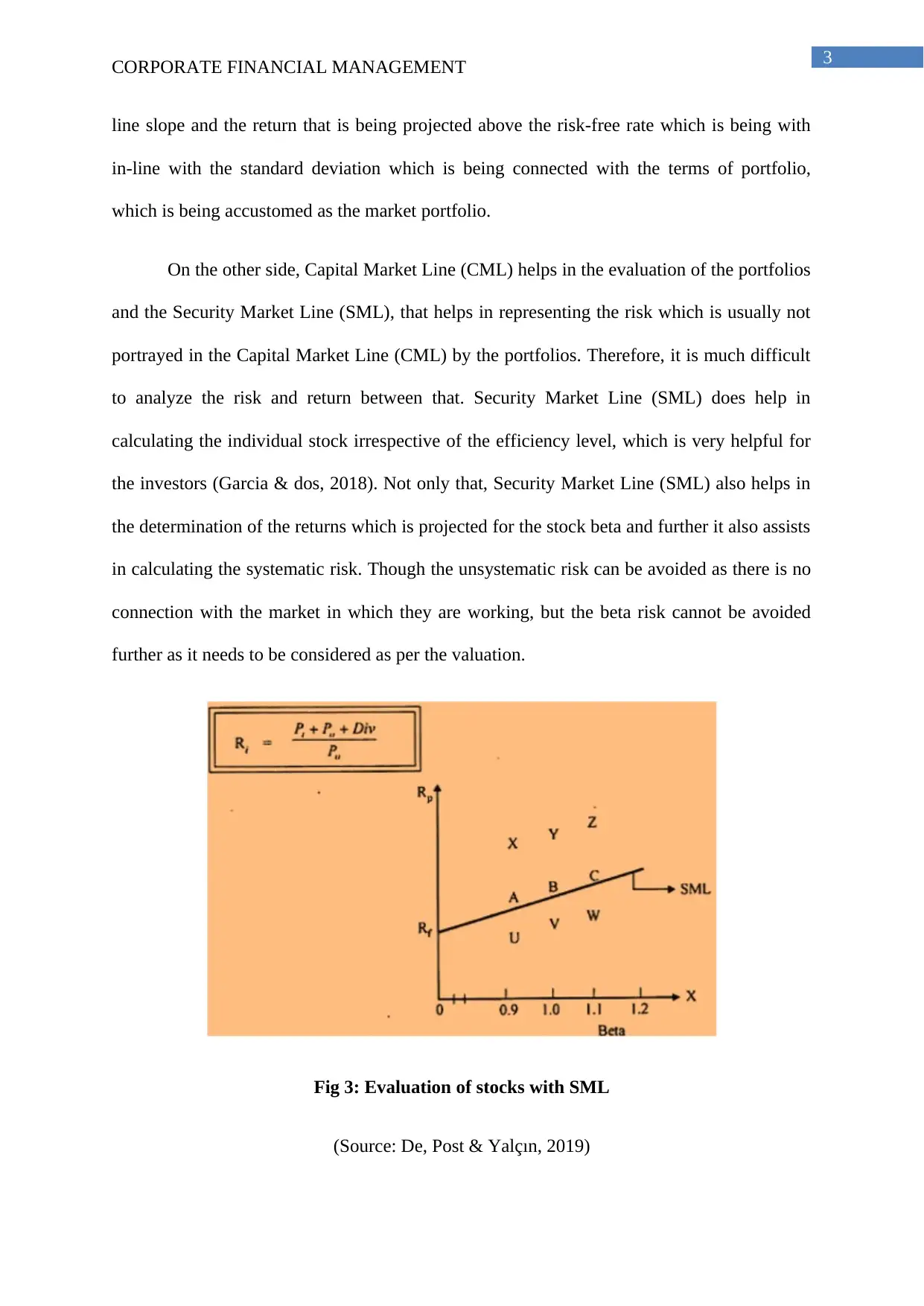

On the other side, Capital Market Line (CML) helps in the evaluation of the portfolios

and the Security Market Line (SML), that helps in representing the risk which is usually not

portrayed in the Capital Market Line (CML) by the portfolios. Therefore, it is much difficult

to analyze the risk and return between that. Security Market Line (SML) does help in

calculating the individual stock irrespective of the efficiency level, which is very helpful for

the investors (Garcia & dos, 2018). Not only that, Security Market Line (SML) also helps in

the determination of the returns which is projected for the stock beta and further it also assists

in calculating the systematic risk. Though the unsystematic risk can be avoided as there is no

connection with the market in which they are working, but the beta risk cannot be avoided

further as it needs to be considered as per the valuation.

Fig 3: Evaluation of stocks with SML

(Source: De, Post & Yalçın, 2019)

CORPORATE FINANCIAL MANAGEMENT

line slope and the return that is being projected above the risk-free rate which is being with

in-line with the standard deviation which is being connected with the terms of portfolio,

which is being accustomed as the market portfolio.

On the other side, Capital Market Line (CML) helps in the evaluation of the portfolios

and the Security Market Line (SML), that helps in representing the risk which is usually not

portrayed in the Capital Market Line (CML) by the portfolios. Therefore, it is much difficult

to analyze the risk and return between that. Security Market Line (SML) does help in

calculating the individual stock irrespective of the efficiency level, which is very helpful for

the investors (Garcia & dos, 2018). Not only that, Security Market Line (SML) also helps in

the determination of the returns which is projected for the stock beta and further it also assists

in calculating the systematic risk. Though the unsystematic risk can be avoided as there is no

connection with the market in which they are working, but the beta risk cannot be avoided

further as it needs to be considered as per the valuation.

Fig 3: Evaluation of stocks with SML

(Source: De, Post & Yalçın, 2019)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CORPORATE FINANCIAL MANAGEMENT

Through the Security Market Line (SML), the securities that are overpriced and

underpriced can be easily determined. From figure 3, that is presented above can be seen that

above the Security Market Line (SML) are the underpriced stocks which can be identified as

X, Y, and Z. U, V, and W are the three stock which can be seen that they are all overpriced as

they are below the Security Market Line (SML). Though the two class of stock has the same

level of risk, they are several dissimilarities that can be observed from there (Nguyen et al.,

2017). The overpriced stocks will not give a greater return as compared to the underpriced

stock. The formula that has been given above, can be defined as P1 as the current price, P0 as

the purchase price and dividend is denoted as the Div. On the SML there are three stocks A,

B and C which is lying, the price of the stock is accurate as they have the same level of risk

and return.

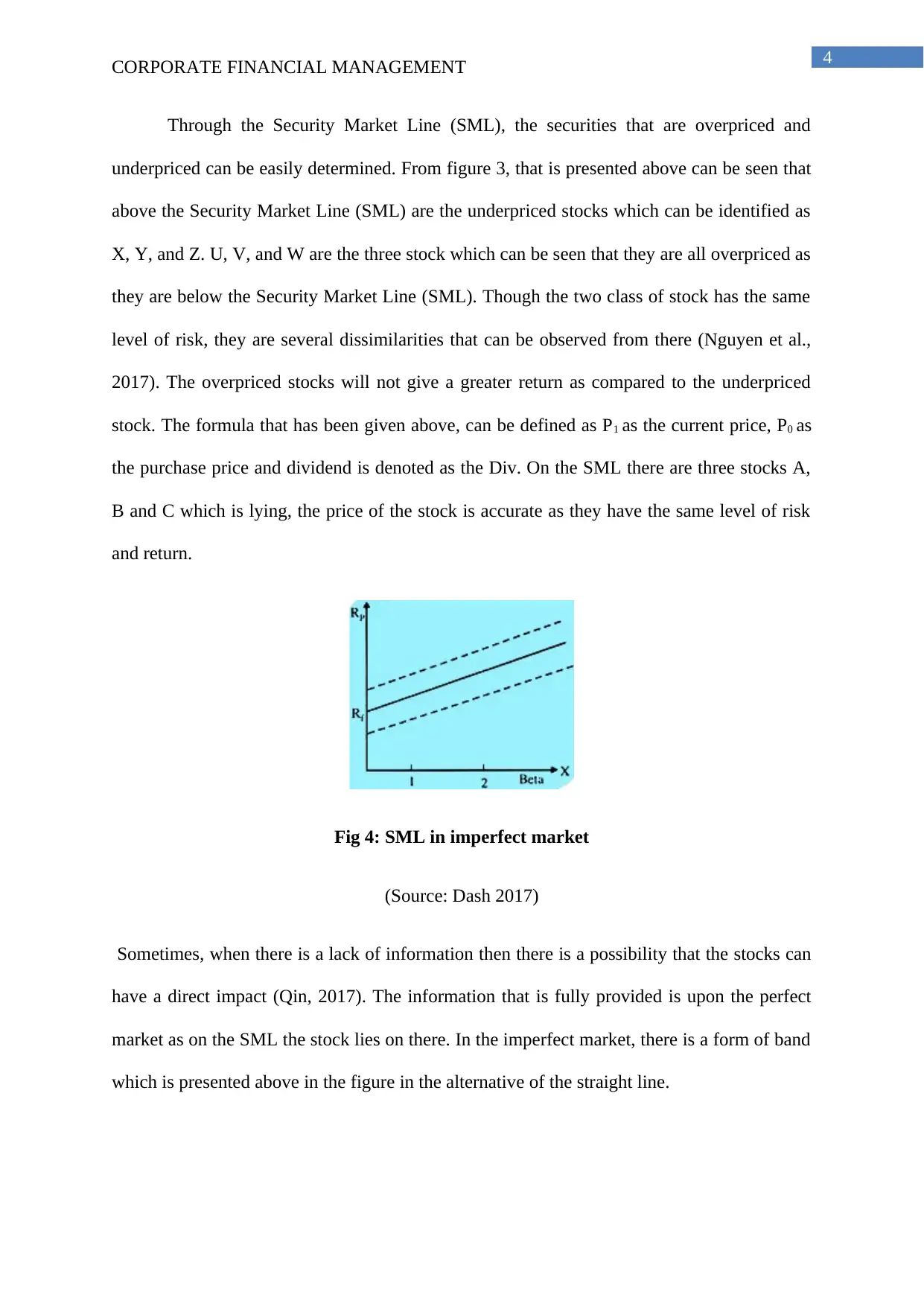

Fig 4: SML in imperfect market

(Source: Dash 2017)

Sometimes, when there is a lack of information then there is a possibility that the stocks can

have a direct impact (Qin, 2017). The information that is fully provided is upon the perfect

market as on the SML the stock lies on there. In the imperfect market, there is a form of band

which is presented above in the figure in the alternative of the straight line.

CORPORATE FINANCIAL MANAGEMENT

Through the Security Market Line (SML), the securities that are overpriced and

underpriced can be easily determined. From figure 3, that is presented above can be seen that

above the Security Market Line (SML) are the underpriced stocks which can be identified as

X, Y, and Z. U, V, and W are the three stock which can be seen that they are all overpriced as

they are below the Security Market Line (SML). Though the two class of stock has the same

level of risk, they are several dissimilarities that can be observed from there (Nguyen et al.,

2017). The overpriced stocks will not give a greater return as compared to the underpriced

stock. The formula that has been given above, can be defined as P1 as the current price, P0 as

the purchase price and dividend is denoted as the Div. On the SML there are three stocks A,

B and C which is lying, the price of the stock is accurate as they have the same level of risk

and return.

Fig 4: SML in imperfect market

(Source: Dash 2017)

Sometimes, when there is a lack of information then there is a possibility that the stocks can

have a direct impact (Qin, 2017). The information that is fully provided is upon the perfect

market as on the SML the stock lies on there. In the imperfect market, there is a form of band

which is presented above in the figure in the alternative of the straight line.

5

CORPORATE FINANCIAL MANAGEMENT

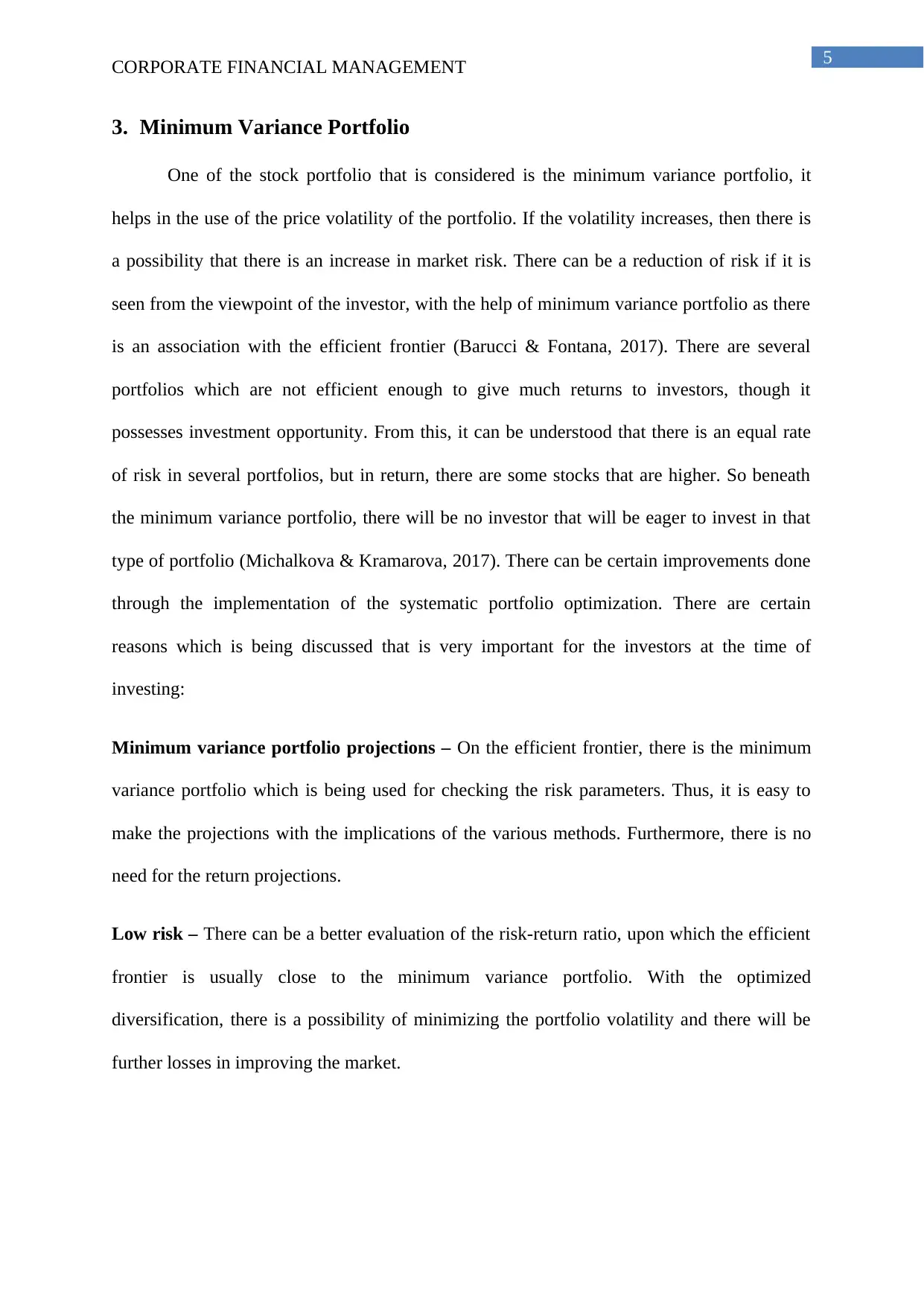

3. Minimum Variance Portfolio

One of the stock portfolio that is considered is the minimum variance portfolio, it

helps in the use of the price volatility of the portfolio. If the volatility increases, then there is

a possibility that there is an increase in market risk. There can be a reduction of risk if it is

seen from the viewpoint of the investor, with the help of minimum variance portfolio as there

is an association with the efficient frontier (Barucci & Fontana, 2017). There are several

portfolios which are not efficient enough to give much returns to investors, though it

possesses investment opportunity. From this, it can be understood that there is an equal rate

of risk in several portfolios, but in return, there are some stocks that are higher. So beneath

the minimum variance portfolio, there will be no investor that will be eager to invest in that

type of portfolio (Michalkova & Kramarova, 2017). There can be certain improvements done

through the implementation of the systematic portfolio optimization. There are certain

reasons which is being discussed that is very important for the investors at the time of

investing:

Minimum variance portfolio projections – On the efficient frontier, there is the minimum

variance portfolio which is being used for checking the risk parameters. Thus, it is easy to

make the projections with the implications of the various methods. Furthermore, there is no

need for the return projections.

Low risk – There can be a better evaluation of the risk-return ratio, upon which the efficient

frontier is usually close to the minimum variance portfolio. With the optimized

diversification, there is a possibility of minimizing the portfolio volatility and there will be

further losses in improving the market.

CORPORATE FINANCIAL MANAGEMENT

3. Minimum Variance Portfolio

One of the stock portfolio that is considered is the minimum variance portfolio, it

helps in the use of the price volatility of the portfolio. If the volatility increases, then there is

a possibility that there is an increase in market risk. There can be a reduction of risk if it is

seen from the viewpoint of the investor, with the help of minimum variance portfolio as there

is an association with the efficient frontier (Barucci & Fontana, 2017). There are several

portfolios which are not efficient enough to give much returns to investors, though it

possesses investment opportunity. From this, it can be understood that there is an equal rate

of risk in several portfolios, but in return, there are some stocks that are higher. So beneath

the minimum variance portfolio, there will be no investor that will be eager to invest in that

type of portfolio (Michalkova & Kramarova, 2017). There can be certain improvements done

through the implementation of the systematic portfolio optimization. There are certain

reasons which is being discussed that is very important for the investors at the time of

investing:

Minimum variance portfolio projections – On the efficient frontier, there is the minimum

variance portfolio which is being used for checking the risk parameters. Thus, it is easy to

make the projections with the implications of the various methods. Furthermore, there is no

need for the return projections.

Low risk – There can be a better evaluation of the risk-return ratio, upon which the efficient

frontier is usually close to the minimum variance portfolio. With the optimized

diversification, there is a possibility of minimizing the portfolio volatility and there will be

further losses in improving the market.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CORPORATE FINANCIAL MANAGEMENT

Figure 5: Minimum variance portfolio

(Source: Bodnar, Parolya and Schmid 2018)

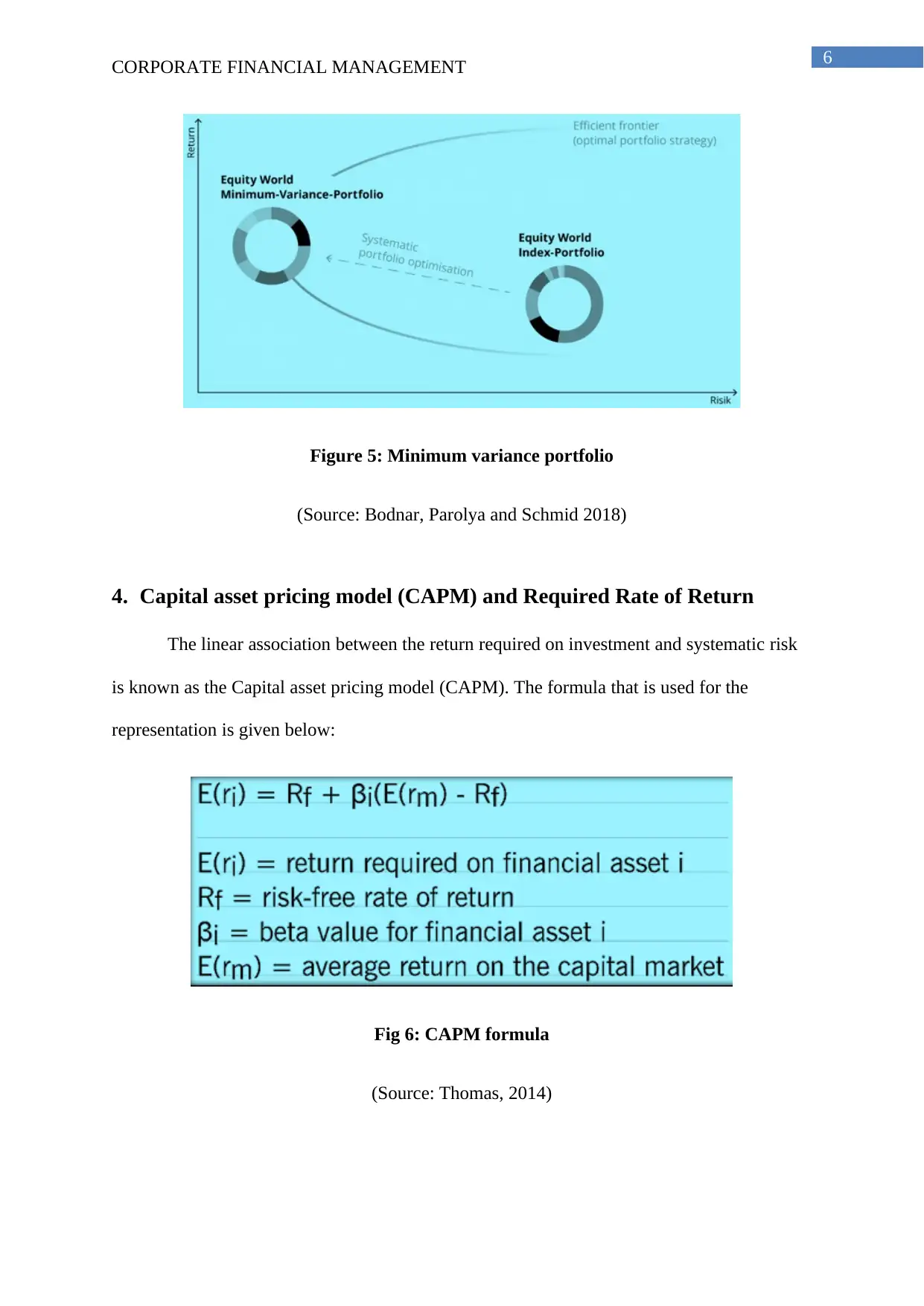

4. Capital asset pricing model (CAPM) and Required Rate of Return

The linear association between the return required on investment and systematic risk

is known as the Capital asset pricing model (CAPM). The formula that is used for the

representation is given below:

Fig 6: CAPM formula

(Source: Thomas, 2014)

CORPORATE FINANCIAL MANAGEMENT

Figure 5: Minimum variance portfolio

(Source: Bodnar, Parolya and Schmid 2018)

4. Capital asset pricing model (CAPM) and Required Rate of Return

The linear association between the return required on investment and systematic risk

is known as the Capital asset pricing model (CAPM). The formula that is used for the

representation is given below:

Fig 6: CAPM formula

(Source: Thomas, 2014)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE FINANCIAL MANAGEMENT

The investor uses the Capital asset pricing model (CAPM) so that it helps in the

determination of the projected investment returns (Patrick and French 2016). At the time of

calculating the Weighted Average Cost of Capital (WACC), Capital asset pricing model

plays a major role. Through WACC, it is used at a discounted rate which helps in the

investment appraisals, some of the assumptions are described below:

There should be similarities in-between the activities of the business related to the project

and of the organization that has invested.

The financing strategy that has used in the project and capital structure that has

implemented should have resemblances.

The funds that is existed of the organization has to maintain the same rate of return after

the project has been granted.

The project upon which the investment has to be done should not be more than the firm

that is doing the investment.

There can be a possibility of change in the discount rate through various assumptions

if both the risk i.e. financial and business of the current organization is not being changed. At

the time of any dissimilarities, there can be use of the Capital asset pricing model (CAPM),

for the particular project that will work as the rate of discount (Magni & Martin, 2018). Thus,

it can be said that the CAPM will help in assisting the bigger investments compared to the

Weighted Average Cost of Capital (WACC) which is further illustrated with the graphical

representation:

CORPORATE FINANCIAL MANAGEMENT

The investor uses the Capital asset pricing model (CAPM) so that it helps in the

determination of the projected investment returns (Patrick and French 2016). At the time of

calculating the Weighted Average Cost of Capital (WACC), Capital asset pricing model

plays a major role. Through WACC, it is used at a discounted rate which helps in the

investment appraisals, some of the assumptions are described below:

There should be similarities in-between the activities of the business related to the project

and of the organization that has invested.

The financing strategy that has used in the project and capital structure that has

implemented should have resemblances.

The funds that is existed of the organization has to maintain the same rate of return after

the project has been granted.

The project upon which the investment has to be done should not be more than the firm

that is doing the investment.

There can be a possibility of change in the discount rate through various assumptions

if both the risk i.e. financial and business of the current organization is not being changed. At

the time of any dissimilarities, there can be use of the Capital asset pricing model (CAPM),

for the particular project that will work as the rate of discount (Magni & Martin, 2018). Thus,

it can be said that the CAPM will help in assisting the bigger investments compared to the

Weighted Average Cost of Capital (WACC) which is further illustrated with the graphical

representation:

8

CORPORATE FINANCIAL MANAGEMENT

.

Fig 7: WACC versus CAPM

(Source: Fernandez, 2019)

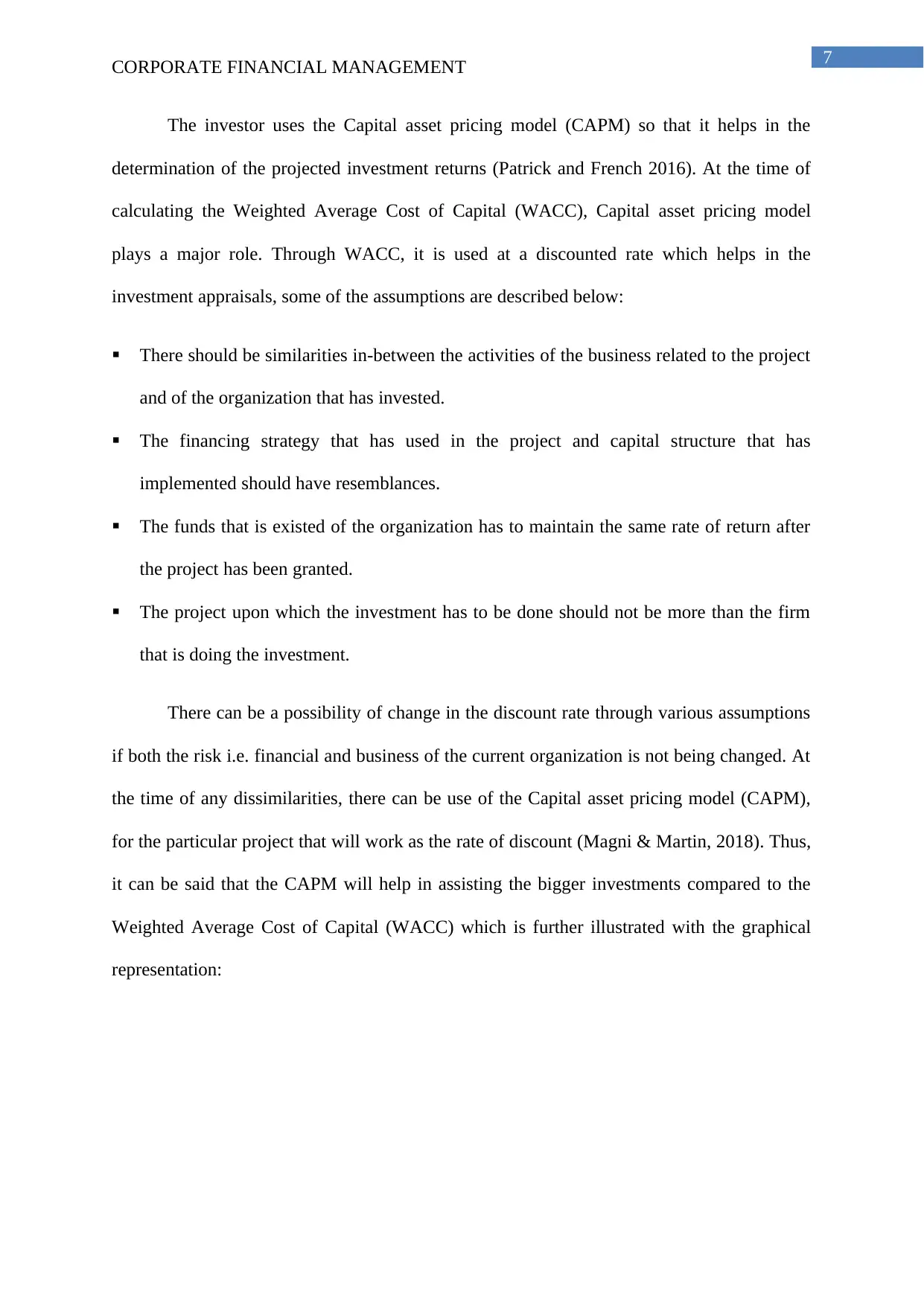

Upon the diagram that has been presented above, it can be observed that Project A

cannot be accepted and if the discounted rate is being taken of the WACC, then it can be

considered that the IRR has to be lower than the WACC. The decision that is usually not

deemed is usually correct at the time of making the investment decisions. The main reason

which is usually behind is that the IRR of the project A is being placed over the SML, so it is

usual that it should be accepted at the time when the discount rate of the CAPM is being

utilized (Sneps, 2017). Thus, it can be easily stated that project A can give more return for

compensating the level of systematic risk and the shareholders' value will increase if it is

further accepted. But on the flip side, the approach of the WACC proposes the acceptance of

Project B. Thus, it cannot be considered a correct decision as the discount rate of CAPM will

reject the project that is being undertaken. The main reason is that the Internal Rate of Return

(IRR) does not have the sufficient compensation for the level of systematic risk.

CORPORATE FINANCIAL MANAGEMENT

.

Fig 7: WACC versus CAPM

(Source: Fernandez, 2019)

Upon the diagram that has been presented above, it can be observed that Project A

cannot be accepted and if the discounted rate is being taken of the WACC, then it can be

considered that the IRR has to be lower than the WACC. The decision that is usually not

deemed is usually correct at the time of making the investment decisions. The main reason

which is usually behind is that the IRR of the project A is being placed over the SML, so it is

usual that it should be accepted at the time when the discount rate of the CAPM is being

utilized (Sneps, 2017). Thus, it can be easily stated that project A can give more return for

compensating the level of systematic risk and the shareholders' value will increase if it is

further accepted. But on the flip side, the approach of the WACC proposes the acceptance of

Project B. Thus, it cannot be considered a correct decision as the discount rate of CAPM will

reject the project that is being undertaken. The main reason is that the Internal Rate of Return

(IRR) does not have the sufficient compensation for the level of systematic risk.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CORPORATE FINANCIAL MANAGEMENT

5. Conclusion

From the above analysis, it can be stated that there are different levels of

measurement upon which the SML, minimum variance portfolios and CML can be

represented. The investors would like to invest upon the portfolios which is beneath the

minimum variance portfolios. With the implication of the optimization of systematic

portfolio, there can be further improvement done. Moreover, it can be stated that the

shareholders’ value can be increased upon the utilization of the Capital asset pricing model.

CORPORATE FINANCIAL MANAGEMENT

5. Conclusion

From the above analysis, it can be stated that there are different levels of

measurement upon which the SML, minimum variance portfolios and CML can be

represented. The investors would like to invest upon the portfolios which is beneath the

minimum variance portfolios. With the implication of the optimization of systematic

portfolio, there can be further improvement done. Moreover, it can be stated that the

shareholders’ value can be increased upon the utilization of the Capital asset pricing model.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CORPORATE FINANCIAL MANAGEMENT

References

Barucci, E. and Fontana, C., 2017. Factor Asset Pricing Models: CAPM and APT.

In Financial Markets Theory (pp. 201-253). Springer, London.

Bodnar, T., Parolya, N. and Schmid, W., 2018. Estimation of the global minimum

variance portfolio in high dimensions. European Journal of Operational

Research, 266(1), pp.371-390.

Dash, M., 2017. “Reverse-Engineering” the Market Portfolio. Journal of Applied

Management and Investments, 6(3), pp.151-156.

De Giorgi, E.G., Post, T. and Yalçın, A., 2019. A concave security market line. Journal of

Banking & Finance, 106, pp.65-81.

Fernandez, P., 2019. WACC and CAPM according to Utilities Regulators: Confusions,

Errors, and Inconsistencies. Errors and Inconsistencies (February 1, 2019).

Garcia, M.T.M. and dos Santos Borrego, D.A.B., 2018. Calculating the Efficient Frontier

for the Portuguese Stock Market. International Advances in Economic Research, 24(4),

pp.339-349.

Heinze, T., Provinzial Rheinland Versicherung AG, 2018. Portfolio optimization using

the diversified efficient frontier. U.S. Patent Application 15/431,199.

Magni, C.A. and Martin, J.D., 2018. Defining a Reliable Multi-Period Project Rate of

Return. An Alternative to IRR. An Alternative to IRR.(September 23, 2018).

CORPORATE FINANCIAL MANAGEMENT

References

Barucci, E. and Fontana, C., 2017. Factor Asset Pricing Models: CAPM and APT.

In Financial Markets Theory (pp. 201-253). Springer, London.

Bodnar, T., Parolya, N. and Schmid, W., 2018. Estimation of the global minimum

variance portfolio in high dimensions. European Journal of Operational

Research, 266(1), pp.371-390.

Dash, M., 2017. “Reverse-Engineering” the Market Portfolio. Journal of Applied

Management and Investments, 6(3), pp.151-156.

De Giorgi, E.G., Post, T. and Yalçın, A., 2019. A concave security market line. Journal of

Banking & Finance, 106, pp.65-81.

Fernandez, P., 2019. WACC and CAPM according to Utilities Regulators: Confusions,

Errors, and Inconsistencies. Errors and Inconsistencies (February 1, 2019).

Garcia, M.T.M. and dos Santos Borrego, D.A.B., 2018. Calculating the Efficient Frontier

for the Portuguese Stock Market. International Advances in Economic Research, 24(4),

pp.339-349.

Heinze, T., Provinzial Rheinland Versicherung AG, 2018. Portfolio optimization using

the diversified efficient frontier. U.S. Patent Application 15/431,199.

Magni, C.A. and Martin, J.D., 2018. Defining a Reliable Multi-Period Project Rate of

Return. An Alternative to IRR. An Alternative to IRR.(September 23, 2018).

11

CORPORATE FINANCIAL MANAGEMENT

Michalkova, L. and Kramarova, K., 2017. CAPM Model, Beta and Relationship with

Credit Rating. In Advances in Applied Economic Research (pp. 645-652). Springer,

Cham.

Nguyen, T., Stalin, O., Diagne, A., Aukea, L., Rootzen, P.H. and Herbertsson, A., 2017.

The Capital asset pricing model and the Arbitrage pricing theory. Gothenburg University,

(May 15, 2017).

Patrick, M. and French, N., 2016. The internal rate of return (IRR): projections,

benchmarks and pitfalls. Journal of Property Investment & Finance, 34(6), pp.664-669.

Qin, J., 2017. Regret-CAPM: A Model of Regret and Asset Pricing. Journal of

Behavioral Economics and Finance, 10(Special_issue), pp.S1-S4.

Sharpe, W., 2017. Capital Market Theory, Efficiency, and Imperfections. Quantitative

Financial Analytics: The Path to Investment Profits, p.445.

Sneps-Sneppe, M., 2017. On the internal rate of return of IRR and the priority of

investments. International Journal of Open Information Technologies, 5(9), pp.39-44.

Williams, E.E. and Dobelman, J.A., 2017. Capital Market Theory, Efficiency, and

Imperfections. World Scientific Book Chapters, pp.445-510.

CORPORATE FINANCIAL MANAGEMENT

Michalkova, L. and Kramarova, K., 2017. CAPM Model, Beta and Relationship with

Credit Rating. In Advances in Applied Economic Research (pp. 645-652). Springer,

Cham.

Nguyen, T., Stalin, O., Diagne, A., Aukea, L., Rootzen, P.H. and Herbertsson, A., 2017.

The Capital asset pricing model and the Arbitrage pricing theory. Gothenburg University,

(May 15, 2017).

Patrick, M. and French, N., 2016. The internal rate of return (IRR): projections,

benchmarks and pitfalls. Journal of Property Investment & Finance, 34(6), pp.664-669.

Qin, J., 2017. Regret-CAPM: A Model of Regret and Asset Pricing. Journal of

Behavioral Economics and Finance, 10(Special_issue), pp.S1-S4.

Sharpe, W., 2017. Capital Market Theory, Efficiency, and Imperfections. Quantitative

Financial Analytics: The Path to Investment Profits, p.445.

Sneps-Sneppe, M., 2017. On the internal rate of return of IRR and the priority of

investments. International Journal of Open Information Technologies, 5(9), pp.39-44.

Williams, E.E. and Dobelman, J.A., 2017. Capital Market Theory, Efficiency, and

Imperfections. World Scientific Book Chapters, pp.445-510.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.