Corporate Financial Management Report: Investment Appraisal Techniques

VerifiedAdded on 2023/01/06

|15

|4411

|69

Report

AI Summary

This report delves into the core aspects of corporate financial management. It begins by examining diversification strategies as a risk management technique, emphasizing the importance of balancing risk and return through portfolio construction. The report then moves on to company valuation, exploring various methods such as the Price/Earnings (P/E) ratio, Dividend Valuation Model, and Discounted Cash Flow (DCF) analysis, using Espirit PLC as a case study. It outlines the key drivers behind these valuation models, including earnings, dividends, cash flows, and market conditions. Finally, the report concludes with a discussion of investment appraisal techniques, evaluating their effectiveness in making sound financial decisions. The report provides a comprehensive overview of essential concepts in corporate finance, equipping readers with a strong understanding of valuation and investment strategies.

Corporate Financial

Management

1

Management

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

Part B...............................................................................................................................................3

Task 1.....................................................................................................................................3

Diversification...................................................................................................................3

Task 2.....................................................................................................................................5

Valuation of a company.....................................................................................................5

Key drivers of valuation models........................................................................................7

Task 3.....................................................................................................................................9

Investment appraisal techniques........................................................................................9

Evaluation of investment appraisal techniques................................................................11

Conclusion.....................................................................................................................................14

References......................................................................................................................................15

2

Introduction......................................................................................................................................3

Part B...............................................................................................................................................3

Task 1.....................................................................................................................................3

Diversification...................................................................................................................3

Task 2.....................................................................................................................................5

Valuation of a company.....................................................................................................5

Key drivers of valuation models........................................................................................7

Task 3.....................................................................................................................................9

Investment appraisal techniques........................................................................................9

Evaluation of investment appraisal techniques................................................................11

Conclusion.....................................................................................................................................14

References......................................................................................................................................15

2

Introduction

Every investor wants to maximise return and minimise risk. All investments include risk

factor which is compensated by return. As the saying goes, more the risk more the return. So, to

have more returns, an investor needs to take more risk (Bessler, Opfer and Wolff, 2017). Another

way to reduce risk is to diversify portfolio in different instruments having different risks and

returns. First part of this report discusses how an investor can manage both risk and return.

Valuation of a company is discussed using multiple methods in second part. In final part of report,

investment appraisal techniques are demonstrated for better understanding.

Part B

Task 1

Diversification

Diversification is a technique of risk management. An investment is bifurcated into a wide

variety of financial instruments within a portfolio to reduce risk involved to any single investment

vehicle. Another thought behind this technique is that a portfolio of multiple kinds of assets will

yield higher long-term returns while reducing risk attached to single asset i.e. the profit on

investment performing well will offset the losses on poor performance of others. For example,

bonds and stock generally perform in mutually exclusive manner. When economy weakens, stock

prices are likely to fall. To salvage market in this condition, central banks cut interest rates to

reduce cost of borrowing and stimulate market spending. This causes bond prices to increase. If

any investor is having both stocks and bonds in portfolio, the rise in valuation of bonds may help

offset the fall in valuation of stocks. This way even if the profits are not increased, at least the risk

has been reduced.

Whenever any investors decide to undertake investment in any financial instrument, not

only returns but risks form the major part of decision-making process. Risks is that chance that

actual gain from an investment will differ from the expected return (Najeeb, Bacha and Masih,

2015). Every investment involves some kind of risk and every investor has different risk appetite.

Financial risks are of two types -systematic risks and unsystematic risks. Systematic risks are also

known as market risk as these risks have macro effect. Common type of systematic risks are risks

of interest rate, inflation, liquidity in market, etc. Unsystematic risks are also known as specific

3

Every investor wants to maximise return and minimise risk. All investments include risk

factor which is compensated by return. As the saying goes, more the risk more the return. So, to

have more returns, an investor needs to take more risk (Bessler, Opfer and Wolff, 2017). Another

way to reduce risk is to diversify portfolio in different instruments having different risks and

returns. First part of this report discusses how an investor can manage both risk and return.

Valuation of a company is discussed using multiple methods in second part. In final part of report,

investment appraisal techniques are demonstrated for better understanding.

Part B

Task 1

Diversification

Diversification is a technique of risk management. An investment is bifurcated into a wide

variety of financial instruments within a portfolio to reduce risk involved to any single investment

vehicle. Another thought behind this technique is that a portfolio of multiple kinds of assets will

yield higher long-term returns while reducing risk attached to single asset i.e. the profit on

investment performing well will offset the losses on poor performance of others. For example,

bonds and stock generally perform in mutually exclusive manner. When economy weakens, stock

prices are likely to fall. To salvage market in this condition, central banks cut interest rates to

reduce cost of borrowing and stimulate market spending. This causes bond prices to increase. If

any investor is having both stocks and bonds in portfolio, the rise in valuation of bonds may help

offset the fall in valuation of stocks. This way even if the profits are not increased, at least the risk

has been reduced.

Whenever any investors decide to undertake investment in any financial instrument, not

only returns but risks form the major part of decision-making process. Risks is that chance that

actual gain from an investment will differ from the expected return (Najeeb, Bacha and Masih,

2015). Every investment involves some kind of risk and every investor has different risk appetite.

Financial risks are of two types -systematic risks and unsystematic risks. Systematic risks are also

known as market risk as these risks have macro effect. Common type of systematic risks are risks

of interest rate, inflation, liquidity in market, etc. Unsystematic risks are also known as specific

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

risk as risks of these categories affect particular industry or company. For example, change in

management, product recall, new big player in the market, etc. Systematic risks are common to all

and difficult to diverse. It is the unsystematic risk that investors aim to manage by diversifying

their portfolio.

Investors expect to be compensated for risk and time value for their money. Good method to

determine this is Capital Asset Pricing Model (CAPM). It describes relationship between expected

return from investment and systematic risk it carries (Zhao and Jin, 2018). Risk free rate in it

accounts for time value of money and risk is also duly taken care of while calculating it. Beta in it

is a measure of amount of risk the investment will add to market portfolio. Its goal is to evaluate

whether a stock is fairly valued in terms of return on being compared with risk and time value it is

carrying. Primary aim of investors in earning return or yield. Estimation of these return shall be

made beforehand by the investors before investing their money anywhere. Many financial ratios

help in such calculations. For example - earnings yield, it helps in determining relation between

earnings per share and company’s stock price per share. It is like inverse to P/E ratio. It is a good

return on investment metric. There are several ways to plan by investors to ensure that their

portfolio is diverse and their risk is minimised and losses are set off against possible profits. Some

are below mentioned:

Investors shall first identify their risk appetite in comparison to the returns they are

expecting (Michalkova and Kramarova, 2017). Then, they should spread their

portfolio among different investment instruments such as cash, stocks, bonds, mutual

funds, ETFs, gold, etc.

Within each type of investment channel also, diversification shall be followed. For

example, vary securities on the basis of the industry, market capitalisation, region,

income, value, growth, etc.

Try to identify and include securities that vary in risk factor that they off set each

other’s risks. The only thing that is to be kept in mind is that diversification is not a

one-time process. Investors shall keep regular check over performance of their

investments and adjust securities as per their goals and strategies.

4

management, product recall, new big player in the market, etc. Systematic risks are common to all

and difficult to diverse. It is the unsystematic risk that investors aim to manage by diversifying

their portfolio.

Investors expect to be compensated for risk and time value for their money. Good method to

determine this is Capital Asset Pricing Model (CAPM). It describes relationship between expected

return from investment and systematic risk it carries (Zhao and Jin, 2018). Risk free rate in it

accounts for time value of money and risk is also duly taken care of while calculating it. Beta in it

is a measure of amount of risk the investment will add to market portfolio. Its goal is to evaluate

whether a stock is fairly valued in terms of return on being compared with risk and time value it is

carrying. Primary aim of investors in earning return or yield. Estimation of these return shall be

made beforehand by the investors before investing their money anywhere. Many financial ratios

help in such calculations. For example - earnings yield, it helps in determining relation between

earnings per share and company’s stock price per share. It is like inverse to P/E ratio. It is a good

return on investment metric. There are several ways to plan by investors to ensure that their

portfolio is diverse and their risk is minimised and losses are set off against possible profits. Some

are below mentioned:

Investors shall first identify their risk appetite in comparison to the returns they are

expecting (Michalkova and Kramarova, 2017). Then, they should spread their

portfolio among different investment instruments such as cash, stocks, bonds, mutual

funds, ETFs, gold, etc.

Within each type of investment channel also, diversification shall be followed. For

example, vary securities on the basis of the industry, market capitalisation, region,

income, value, growth, etc.

Try to identify and include securities that vary in risk factor that they off set each

other’s risks. The only thing that is to be kept in mind is that diversification is not a

one-time process. Investors shall keep regular check over performance of their

investments and adjust securities as per their goals and strategies.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

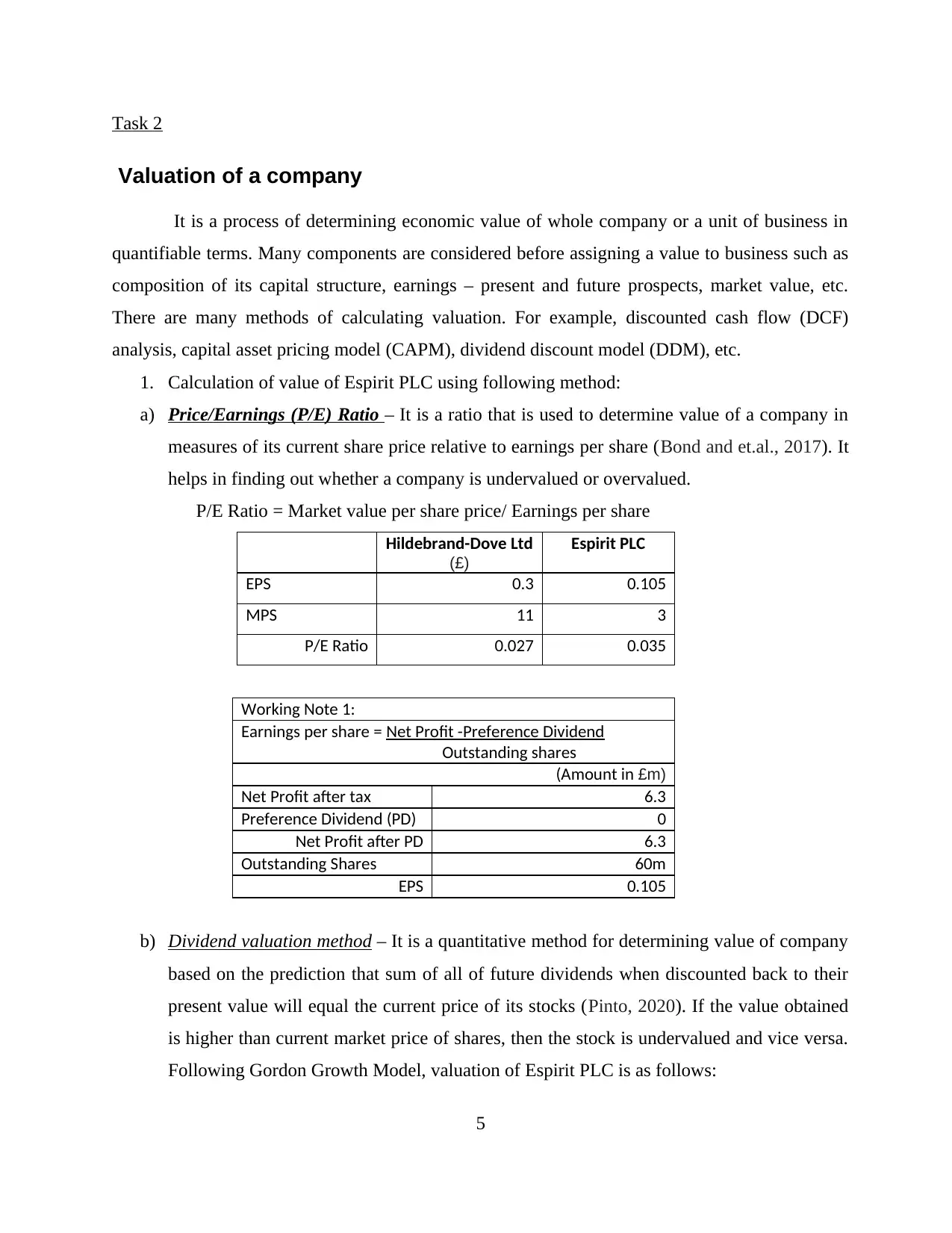

Task 2

Valuation of a company

It is a process of determining economic value of whole company or a unit of business in

quantifiable terms. Many components are considered before assigning a value to business such as

composition of its capital structure, earnings – present and future prospects, market value, etc.

There are many methods of calculating valuation. For example, discounted cash flow (DCF)

analysis, capital asset pricing model (CAPM), dividend discount model (DDM), etc.

1. Calculation of value of Espirit PLC using following method:

a) Price/Earnings (P/E) Ratio – It is a ratio that is used to determine value of a company in

measures of its current share price relative to earnings per share (Bond and et.al., 2017). It

helps in finding out whether a company is undervalued or overvalued.

P/E Ratio = Market value per share price/ Earnings per share

Hildebrand-Dove Ltd

(£)

Espirit PLC

EPS 0.3 0.105

MPS 11 3

P/E Ratio 0.027 0.035

Working Note 1:

Earnings per share = Net Profit -Preference Dividend

Outstanding shares

(Amount in £m)

Net Profit after tax 6.3

Preference Dividend (PD) 0

Net Profit after PD 6.3

Outstanding Shares 60m

EPS 0.105

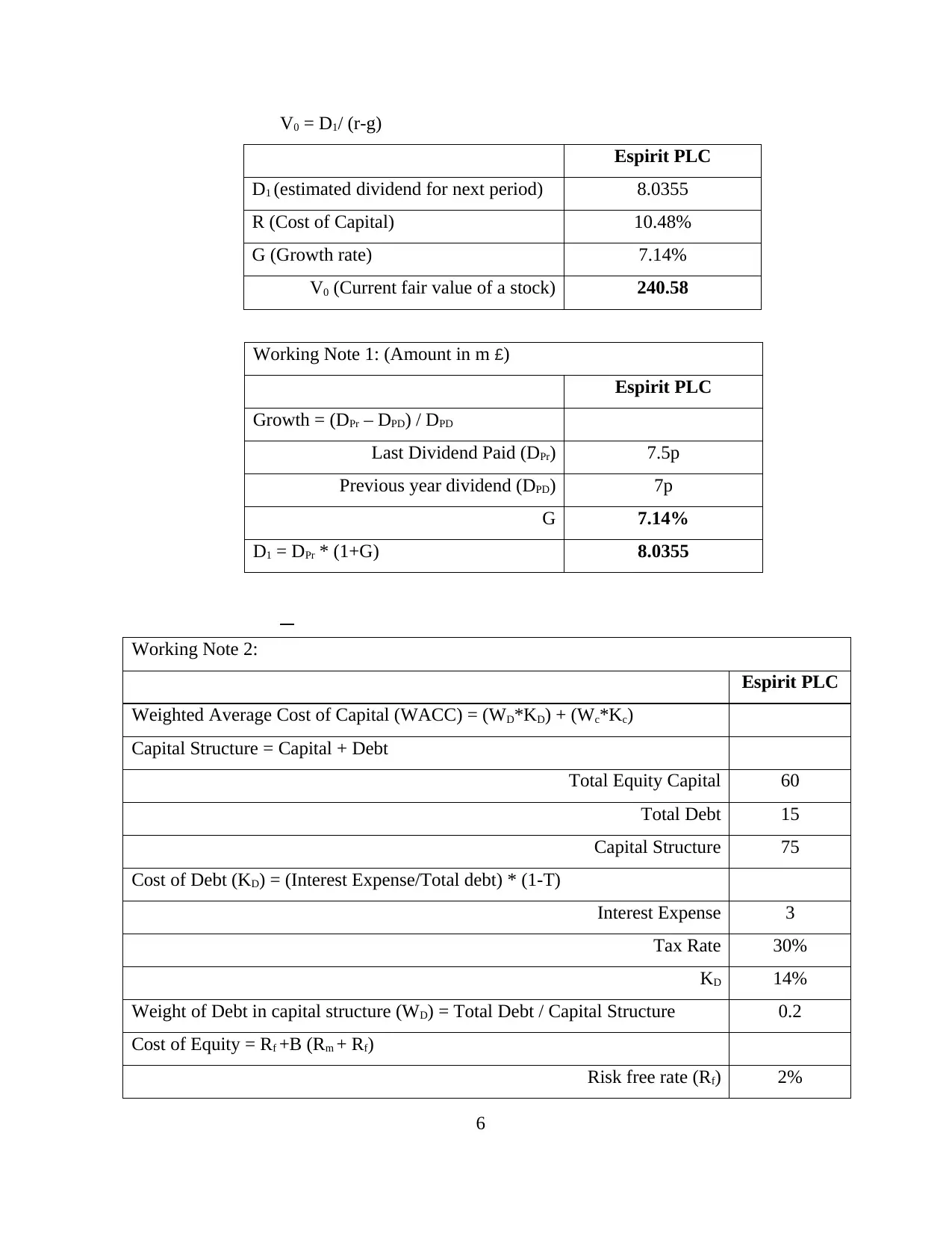

b) Dividend valuation method – It is a quantitative method for determining value of company

based on the prediction that sum of all of future dividends when discounted back to their

present value will equal the current price of its stocks (Pinto, 2020). If the value obtained

is higher than current market price of shares, then the stock is undervalued and vice versa.

Following Gordon Growth Model, valuation of Espirit PLC is as follows:

5

Valuation of a company

It is a process of determining economic value of whole company or a unit of business in

quantifiable terms. Many components are considered before assigning a value to business such as

composition of its capital structure, earnings – present and future prospects, market value, etc.

There are many methods of calculating valuation. For example, discounted cash flow (DCF)

analysis, capital asset pricing model (CAPM), dividend discount model (DDM), etc.

1. Calculation of value of Espirit PLC using following method:

a) Price/Earnings (P/E) Ratio – It is a ratio that is used to determine value of a company in

measures of its current share price relative to earnings per share (Bond and et.al., 2017). It

helps in finding out whether a company is undervalued or overvalued.

P/E Ratio = Market value per share price/ Earnings per share

Hildebrand-Dove Ltd

(£)

Espirit PLC

EPS 0.3 0.105

MPS 11 3

P/E Ratio 0.027 0.035

Working Note 1:

Earnings per share = Net Profit -Preference Dividend

Outstanding shares

(Amount in £m)

Net Profit after tax 6.3

Preference Dividend (PD) 0

Net Profit after PD 6.3

Outstanding Shares 60m

EPS 0.105

b) Dividend valuation method – It is a quantitative method for determining value of company

based on the prediction that sum of all of future dividends when discounted back to their

present value will equal the current price of its stocks (Pinto, 2020). If the value obtained

is higher than current market price of shares, then the stock is undervalued and vice versa.

Following Gordon Growth Model, valuation of Espirit PLC is as follows:

5

V0 = D1/ (r-g)

Espirit PLC

D1 (estimated dividend for next period) 8.0355

R (Cost of Capital) 10.48%

G (Growth rate) 7.14%

V0 (Current fair value of a stock) 240.58

Working Note 1: (Amount in m £)

Espirit PLC

Growth = (DPr – DPD) / DPD

Last Dividend Paid (DPr) 7.5p

Previous year dividend (DPD) 7p

G 7.14%

D1 = DPr * (1+G) 8.0355

Working Note 2:

Espirit PLC

Weighted Average Cost of Capital (WACC) = (WD*KD) + (Wc*Kc)

Capital Structure = Capital + Debt

Total Equity Capital 60

Total Debt 15

Capital Structure 75

Cost of Debt (KD) = (Interest Expense/Total debt) * (1-T)

Interest Expense 3

Tax Rate 30%

KD 14%

Weight of Debt in capital structure (WD) = Total Debt / Capital Structure 0.2

Cost of Equity = Rf +B (Rm + Rf)

Risk free rate (Rf) 2%

6

Espirit PLC

D1 (estimated dividend for next period) 8.0355

R (Cost of Capital) 10.48%

G (Growth rate) 7.14%

V0 (Current fair value of a stock) 240.58

Working Note 1: (Amount in m £)

Espirit PLC

Growth = (DPr – DPD) / DPD

Last Dividend Paid (DPr) 7.5p

Previous year dividend (DPD) 7p

G 7.14%

D1 = DPr * (1+G) 8.0355

Working Note 2:

Espirit PLC

Weighted Average Cost of Capital (WACC) = (WD*KD) + (Wc*Kc)

Capital Structure = Capital + Debt

Total Equity Capital 60

Total Debt 15

Capital Structure 75

Cost of Debt (KD) = (Interest Expense/Total debt) * (1-T)

Interest Expense 3

Tax Rate 30%

KD 14%

Weight of Debt in capital structure (WD) = Total Debt / Capital Structure 0.2

Cost of Equity = Rf +B (Rm + Rf)

Risk free rate (Rf) 2%

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

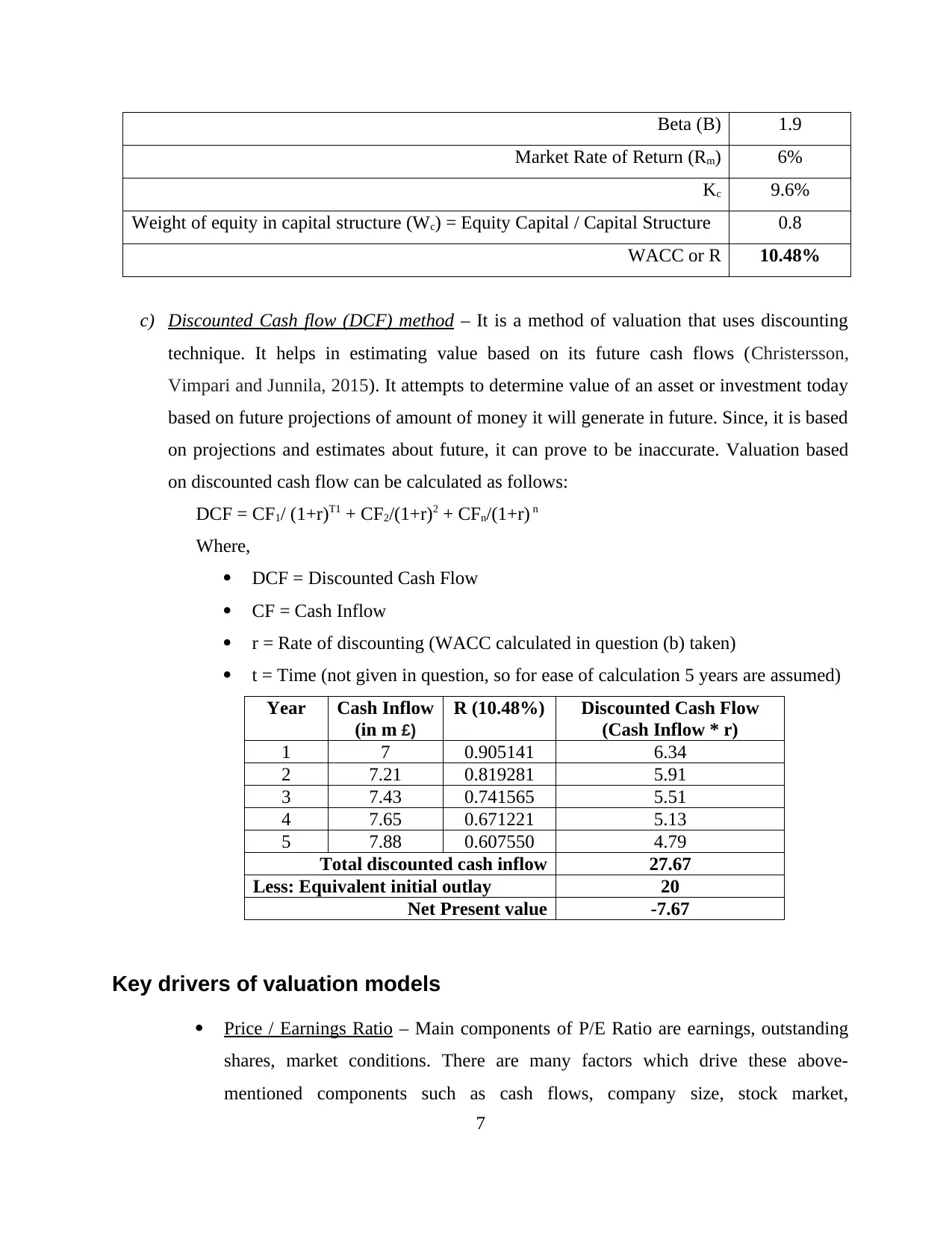

Beta (B) 1.9

Market Rate of Return (Rm) 6%

Kc 9.6%

Weight of equity in capital structure (Wc) = Equity Capital / Capital Structure 0.8

WACC or R 10.48%

c) Discounted Cash flow (DCF) method – It is a method of valuation that uses discounting

technique. It helps in estimating value based on its future cash flows (Christersson,

Vimpari and Junnila, 2015). It attempts to determine value of an asset or investment today

based on future projections of amount of money it will generate in future. Since, it is based

on projections and estimates about future, it can prove to be inaccurate. Valuation based

on discounted cash flow can be calculated as follows:

DCF = CF1/ (1+r)T1 + CF2/(1+r)2 + CFn/(1+r) n

Where,

DCF = Discounted Cash Flow

CF = Cash Inflow

r = Rate of discounting (WACC calculated in question (b) taken)

t = Time (not given in question, so for ease of calculation 5 years are assumed)

Year Cash Inflow

(in m £)

R (10.48%) Discounted Cash Flow

(Cash Inflow * r)

1 7 0.905141 6.34

2 7.21 0.819281 5.91

3 7.43 0.741565 5.51

4 7.65 0.671221 5.13

5 7.88 0.607550 4.79

Total discounted cash inflow 27.67

Less: Equivalent initial outlay 20

Net Present value -7.67

Key drivers of valuation models

Price / Earnings Ratio – Main components of P/E Ratio are earnings, outstanding

shares, market conditions. There are many factors which drive these above-

mentioned components such as cash flows, company size, stock market,

7

Market Rate of Return (Rm) 6%

Kc 9.6%

Weight of equity in capital structure (Wc) = Equity Capital / Capital Structure 0.8

WACC or R 10.48%

c) Discounted Cash flow (DCF) method – It is a method of valuation that uses discounting

technique. It helps in estimating value based on its future cash flows (Christersson,

Vimpari and Junnila, 2015). It attempts to determine value of an asset or investment today

based on future projections of amount of money it will generate in future. Since, it is based

on projections and estimates about future, it can prove to be inaccurate. Valuation based

on discounted cash flow can be calculated as follows:

DCF = CF1/ (1+r)T1 + CF2/(1+r)2 + CFn/(1+r) n

Where,

DCF = Discounted Cash Flow

CF = Cash Inflow

r = Rate of discounting (WACC calculated in question (b) taken)

t = Time (not given in question, so for ease of calculation 5 years are assumed)

Year Cash Inflow

(in m £)

R (10.48%) Discounted Cash Flow

(Cash Inflow * r)

1 7 0.905141 6.34

2 7.21 0.819281 5.91

3 7.43 0.741565 5.51

4 7.65 0.671221 5.13

5 7.88 0.607550 4.79

Total discounted cash inflow 27.67

Less: Equivalent initial outlay 20

Net Present value -7.67

Key drivers of valuation models

Price / Earnings Ratio – Main components of P/E Ratio are earnings, outstanding

shares, market conditions. There are many factors which drive these above-

mentioned components such as cash flows, company size, stock market,

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

government regulations, operating history, growth rate, return on equity, sectorial

leadership, sustainability of earnings, etc.

Finance managers shall check combination of cost control and increase in sales as

drivers for higher earnings. They shall also explore possibilities of venturing in

new products and new markets. They shall also keep a close watch on performance

of stock market. Stock market is volatile and react strongly to every significant

change be it reporting of unexpected profit/loss by management or some potential

opportunity/threat in company’s way (Aprilia, 2015). Companies that are market

leaders or have a reputation of developing innovative productivity solutions enjoy

higher P/E Ratios in market and investors are ready to premium prices for the

shares of such companies. General economic conditions such as interest rates,

operating costs, unemployment rate, etc. of the place where business operates shall

also be in mind of finance managers. It lays effect not only on earnings but on

market price of shares as well.

Dividend Valuation method – Main components of this model are dividend, growth

rate with which dividend grows and cost of capital to the company. These

components are driven by factors such as regular cash flows, retention policy,

dividend expectations of shareholders, dividend distribution policy, time value of

money, cost of equity and debt to the company, risk factor, etc.

While calculating valuation of a company or project, finance managers shall keep

in mind that there are three key inputs in this model namely dividend per share

(DPS), growth rate in DPS and the desired rate of return. Managers should keep a

watch over cash flows and ensure their consistency. Capital structure of finance is

internal decision of management so to ensure least cost to company, managers shall

explore all possible options of investments before choosing one. Shareholders

expect a steady growth rate in dividend pay-out by company which shall be in

coherence with company’s distribution and retention policy. Balancing between

two is responsibility of managers. Time value of money is assumed on the basis of

historical data and future estimates but future is uncertain. So, provision shall be

made according to risk involved.

8

leadership, sustainability of earnings, etc.

Finance managers shall check combination of cost control and increase in sales as

drivers for higher earnings. They shall also explore possibilities of venturing in

new products and new markets. They shall also keep a close watch on performance

of stock market. Stock market is volatile and react strongly to every significant

change be it reporting of unexpected profit/loss by management or some potential

opportunity/threat in company’s way (Aprilia, 2015). Companies that are market

leaders or have a reputation of developing innovative productivity solutions enjoy

higher P/E Ratios in market and investors are ready to premium prices for the

shares of such companies. General economic conditions such as interest rates,

operating costs, unemployment rate, etc. of the place where business operates shall

also be in mind of finance managers. It lays effect not only on earnings but on

market price of shares as well.

Dividend Valuation method – Main components of this model are dividend, growth

rate with which dividend grows and cost of capital to the company. These

components are driven by factors such as regular cash flows, retention policy,

dividend expectations of shareholders, dividend distribution policy, time value of

money, cost of equity and debt to the company, risk factor, etc.

While calculating valuation of a company or project, finance managers shall keep

in mind that there are three key inputs in this model namely dividend per share

(DPS), growth rate in DPS and the desired rate of return. Managers should keep a

watch over cash flows and ensure their consistency. Capital structure of finance is

internal decision of management so to ensure least cost to company, managers shall

explore all possible options of investments before choosing one. Shareholders

expect a steady growth rate in dividend pay-out by company which shall be in

coherence with company’s distribution and retention policy. Balancing between

two is responsibility of managers. Time value of money is assumed on the basis of

historical data and future estimates but future is uncertain. So, provision shall be

made according to risk involved.

8

Discounted cash flow method – This method is entirely based on estimates about

future. Thus, it is only as accurate as the assumptions are. All forecasts are based

on key value drivers like free cashflow projections, cost of capital which serves as

discounting factor, growth rate of terminal value, length of forecast period, etc.

Cash flows have strongest influence and can be said as decisive aspect for this

method. So naturally maintaining consistent cash flows shall be focus of finance

managers. They shall always undertake activities to increase sales, decrease cost,

payment modalities, conditions for debtors, etc. to ensure that value of business

always stays positive. Cost of capital is used as discounting factor and hence,

efforts to optimise capital structure and cost of debt and equity shall always be in

the plan of finance department. Growth rate in the terminal value reflects growth of

cashflows at the end of forecasted period (Goedhart, Koller and Wessels, 2015).

So, efforts shall be made to optimise it. Other than cash flow and discount rate,

another major affecting factor is length of the forecast period. Extending or

shortening time period can have substantial impact on the value and results for the

company. So, it should be considered to use period as per the requirement of the

company.

Task 3

Investment appraisal techniques

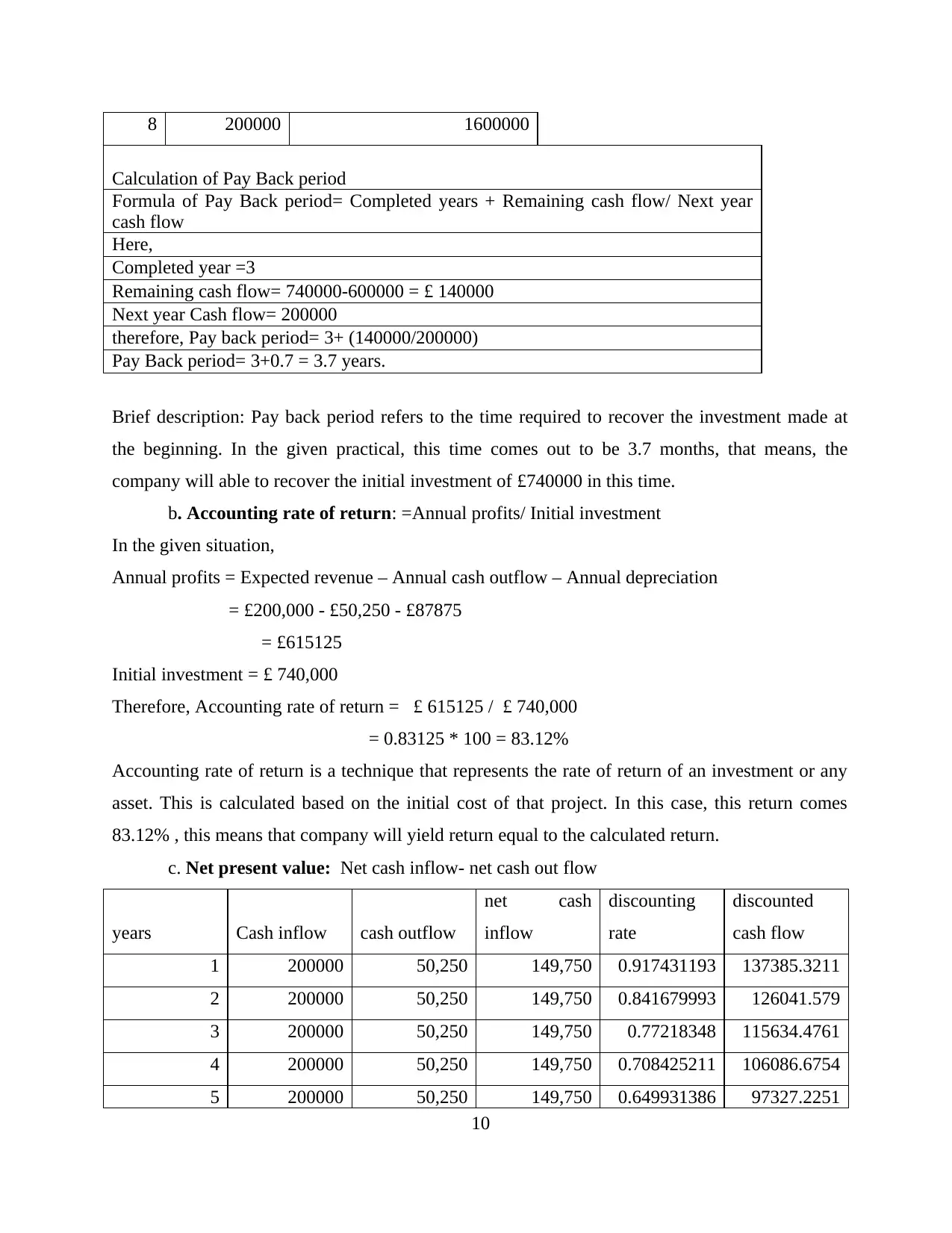

a. The Pay Back period:

Pay back period

Years Cash inflow Cumulative cash inflow

1 200000 200000

2 200000 400000

3 200000 600000

4 200000 800000

5 200000 1000000

6 200000 1200000

7 200000 1400000

9

future. Thus, it is only as accurate as the assumptions are. All forecasts are based

on key value drivers like free cashflow projections, cost of capital which serves as

discounting factor, growth rate of terminal value, length of forecast period, etc.

Cash flows have strongest influence and can be said as decisive aspect for this

method. So naturally maintaining consistent cash flows shall be focus of finance

managers. They shall always undertake activities to increase sales, decrease cost,

payment modalities, conditions for debtors, etc. to ensure that value of business

always stays positive. Cost of capital is used as discounting factor and hence,

efforts to optimise capital structure and cost of debt and equity shall always be in

the plan of finance department. Growth rate in the terminal value reflects growth of

cashflows at the end of forecasted period (Goedhart, Koller and Wessels, 2015).

So, efforts shall be made to optimise it. Other than cash flow and discount rate,

another major affecting factor is length of the forecast period. Extending or

shortening time period can have substantial impact on the value and results for the

company. So, it should be considered to use period as per the requirement of the

company.

Task 3

Investment appraisal techniques

a. The Pay Back period:

Pay back period

Years Cash inflow Cumulative cash inflow

1 200000 200000

2 200000 400000

3 200000 600000

4 200000 800000

5 200000 1000000

6 200000 1200000

7 200000 1400000

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

8 200000 1600000

Calculation of Pay Back period

Formula of Pay Back period= Completed years + Remaining cash flow/ Next year

cash flow

Here,

Completed year =3

Remaining cash flow= 740000-600000 = £ 140000

Next year Cash flow= 200000

therefore, Pay back period= 3+ (140000/200000)

Pay Back period= 3+0.7 = 3.7 years.

Brief description: Pay back period refers to the time required to recover the investment made at

the beginning. In the given practical, this time comes out to be 3.7 months, that means, the

company will able to recover the initial investment of £740000 in this time.

b. Accounting rate of return: =Annual profits/ Initial investment

In the given situation,

Annual profits = Expected revenue – Annual cash outflow – Annual depreciation

= £200,000 - £50,250 - £87875

= £615125

Initial investment = £ 740,000

Therefore, Accounting rate of return = £ 615125 / £ 740,000

= 0.83125 * 100 = 83.12%

Accounting rate of return is a technique that represents the rate of return of an investment or any

asset. This is calculated based on the initial cost of that project. In this case, this return comes

83.12% , this means that company will yield return equal to the calculated return.

c. Net present value: Net cash inflow- net cash out flow

years Cash inflow cash outflow

net cash

inflow

discounting

rate

discounted

cash flow

1 200000 50,250 149,750 0.917431193 137385.3211

2 200000 50,250 149,750 0.841679993 126041.579

3 200000 50,250 149,750 0.77218348 115634.4761

4 200000 50,250 149,750 0.708425211 106086.6754

5 200000 50,250 149,750 0.649931386 97327.2251

10

Calculation of Pay Back period

Formula of Pay Back period= Completed years + Remaining cash flow/ Next year

cash flow

Here,

Completed year =3

Remaining cash flow= 740000-600000 = £ 140000

Next year Cash flow= 200000

therefore, Pay back period= 3+ (140000/200000)

Pay Back period= 3+0.7 = 3.7 years.

Brief description: Pay back period refers to the time required to recover the investment made at

the beginning. In the given practical, this time comes out to be 3.7 months, that means, the

company will able to recover the initial investment of £740000 in this time.

b. Accounting rate of return: =Annual profits/ Initial investment

In the given situation,

Annual profits = Expected revenue – Annual cash outflow – Annual depreciation

= £200,000 - £50,250 - £87875

= £615125

Initial investment = £ 740,000

Therefore, Accounting rate of return = £ 615125 / £ 740,000

= 0.83125 * 100 = 83.12%

Accounting rate of return is a technique that represents the rate of return of an investment or any

asset. This is calculated based on the initial cost of that project. In this case, this return comes

83.12% , this means that company will yield return equal to the calculated return.

c. Net present value: Net cash inflow- net cash out flow

years Cash inflow cash outflow

net cash

inflow

discounting

rate

discounted

cash flow

1 200000 50,250 149,750 0.917431193 137385.3211

2 200000 50,250 149,750 0.841679993 126041.579

3 200000 50,250 149,750 0.77218348 115634.4761

4 200000 50,250 149,750 0.708425211 106086.6754

5 200000 50,250 149,750 0.649931386 97327.2251

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

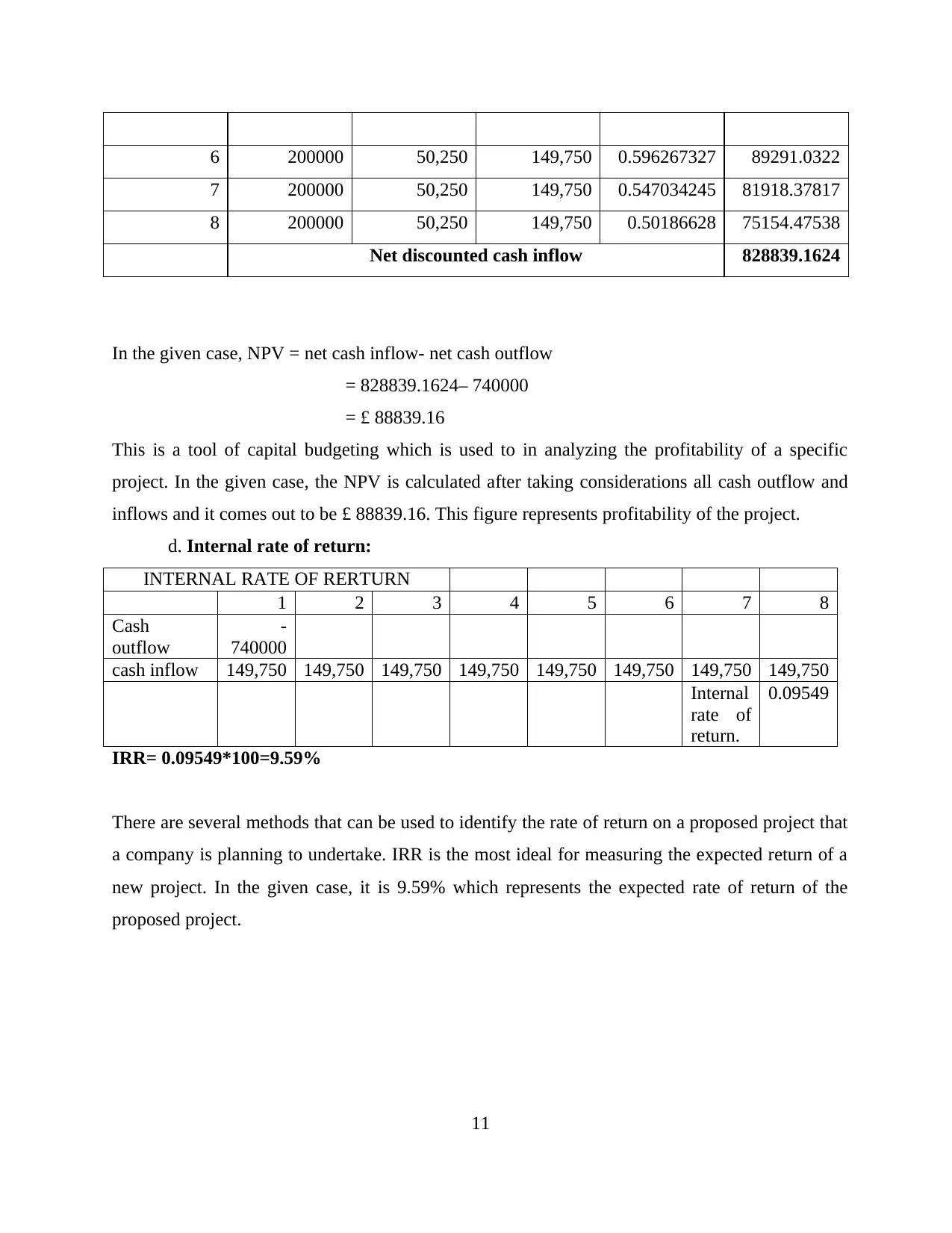

6 200000 50,250 149,750 0.596267327 89291.0322

7 200000 50,250 149,750 0.547034245 81918.37817

8 200000 50,250 149,750 0.50186628 75154.47538

Net discounted cash inflow 828839.1624

In the given case, NPV = net cash inflow- net cash outflow

= 828839.1624– 740000

= £ 88839.16

This is a tool of capital budgeting which is used to in analyzing the profitability of a specific

project. In the given case, the NPV is calculated after taking considerations all cash outflow and

inflows and it comes out to be £ 88839.16. This figure represents profitability of the project.

d. Internal rate of return:

INTERNAL RATE OF RERTURN

1 2 3 4 5 6 7 8

Cash

outflow

-

740000

cash inflow 149,750 149,750 149,750 149,750 149,750 149,750 149,750 149,750

Internal

rate of

return.

0.09549

IRR= 0.09549*100=9.59%

There are several methods that can be used to identify the rate of return on a proposed project that

a company is planning to undertake. IRR is the most ideal for measuring the expected return of a

new project. In the given case, it is 9.59% which represents the expected rate of return of the

proposed project.

11

7 200000 50,250 149,750 0.547034245 81918.37817

8 200000 50,250 149,750 0.50186628 75154.47538

Net discounted cash inflow 828839.1624

In the given case, NPV = net cash inflow- net cash outflow

= 828839.1624– 740000

= £ 88839.16

This is a tool of capital budgeting which is used to in analyzing the profitability of a specific

project. In the given case, the NPV is calculated after taking considerations all cash outflow and

inflows and it comes out to be £ 88839.16. This figure represents profitability of the project.

d. Internal rate of return:

INTERNAL RATE OF RERTURN

1 2 3 4 5 6 7 8

Cash

outflow

-

740000

cash inflow 149,750 149,750 149,750 149,750 149,750 149,750 149,750 149,750

Internal

rate of

return.

0.09549

IRR= 0.09549*100=9.59%

There are several methods that can be used to identify the rate of return on a proposed project that

a company is planning to undertake. IRR is the most ideal for measuring the expected return of a

new project. In the given case, it is 9.59% which represents the expected rate of return of the

proposed project.

11

Evaluation of investment appraisal techniques

There are various techniques of analyzing economic feasibility of proposed project that a

company is planning to acquire. Every technique has certain pros and cons, which are discussed as

below:

1. Pay Back period: It is the simplest method of measuring profitability of a project. It basically

calculates the time period for in which the initial investment will be recovered. It has certain pros

and cons as well which are enumerated below:

Advantages of Pay Back period: It is the simplest method that measures economic

feasibility of a project. It is an easy way to calculate pay-back period of different options available

with the company. Pay-back period also has many drawbacks.

Disadvantages of Pay Back period: The most significant limitation of this method is that it

does not consider time value of money. That means it weighs the value of I unit of money at

present time as well in later period of time (for say, after 5 years). Due to this limitation it lacks to

feature of clearness of profitability of a project. This analysis tool only considers the flows until

the initial investment is not recovered, and ignores, the inflows that occur after that period. It is

essential to consider every penny of inflows to measure the actual profitability of project.

Sometimes a project have lower returns in beginning of time period but have significant high

returns at the later time period. This unevenness of cash inflows may result into high pay-back

period which represents lower profitability of project, which is actually not true.

2. Accounting rate of return: It is capital budgeting metric that is a useful tool if the purpose of

calculation is investment profitability (Arjunan, 2019). ARR is basically the tool of comparing

different projects, to calculate expected return of each project. This tool help is providing

assistance to managers in taking decision about an investment or acquisition.

Advantages of Accounting rate of return: it is very easy to compute and also simple to

understand. It also take total profits that will occur over total economic life of project into

consideration. It actually considers the concept of net earnings, which means, the concept of profit

that arises after deducting tax and depreciation. This is a vital factor is measuring the profitability

of proposed investment or project. This method gives a clear view about the profitability of

project. This tool is very useful in measuring current performance of firm.

12

There are various techniques of analyzing economic feasibility of proposed project that a

company is planning to acquire. Every technique has certain pros and cons, which are discussed as

below:

1. Pay Back period: It is the simplest method of measuring profitability of a project. It basically

calculates the time period for in which the initial investment will be recovered. It has certain pros

and cons as well which are enumerated below:

Advantages of Pay Back period: It is the simplest method that measures economic

feasibility of a project. It is an easy way to calculate pay-back period of different options available

with the company. Pay-back period also has many drawbacks.

Disadvantages of Pay Back period: The most significant limitation of this method is that it

does not consider time value of money. That means it weighs the value of I unit of money at

present time as well in later period of time (for say, after 5 years). Due to this limitation it lacks to

feature of clearness of profitability of a project. This analysis tool only considers the flows until

the initial investment is not recovered, and ignores, the inflows that occur after that period. It is

essential to consider every penny of inflows to measure the actual profitability of project.

Sometimes a project have lower returns in beginning of time period but have significant high

returns at the later time period. This unevenness of cash inflows may result into high pay-back

period which represents lower profitability of project, which is actually not true.

2. Accounting rate of return: It is capital budgeting metric that is a useful tool if the purpose of

calculation is investment profitability (Arjunan, 2019). ARR is basically the tool of comparing

different projects, to calculate expected return of each project. This tool help is providing

assistance to managers in taking decision about an investment or acquisition.

Advantages of Accounting rate of return: it is very easy to compute and also simple to

understand. It also take total profits that will occur over total economic life of project into

consideration. It actually considers the concept of net earnings, which means, the concept of profit

that arises after deducting tax and depreciation. This is a vital factor is measuring the profitability

of proposed investment or project. This method gives a clear view about the profitability of

project. This tool is very useful in measuring current performance of firm.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.