CBE6382: Corporate Financial Management Report on Rio Tinto

VerifiedAdded on 2022/10/01

|22

|5335

|22

Report

AI Summary

This report provides a comprehensive financial analysis of Rio Tinto, examining its corporate financial management. It begins with an introduction to corporate finance and discusses corporate governance within Rio Tinto. The report then delves into the company's financial performance, analyzing profitability, liquidity, efficiency, and solvency ratios for the years 2017 and 2018. It evaluates the company's dividend policy, risk profile, and optimal capital structure, including a detailed discussion of the DCF model. The report further explores investment appraisal techniques, including Net Present Value (NPV), Internal Rate of Return (IRR), Payback Period, and Profitability Index. The analysis is supported by financial data and relevant literature, providing insights into Rio Tinto's financial health and strategic decisions. The report concludes with a summary of findings and recommendations.

Running Head: CORPORATE FINANCIAL MANAGEMENT

1

CORPORATE FINANCIAL MANAGEMENT

1

CORPORATE FINANCIAL MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: CORPORATE FINANCIAL MANAGEMENT

Contents

Part A..........................................................................................................................................................3

Introduction.................................................................................................................................................3

Corporate governance..................................................................................................................................4

Financial performance.................................................................................................................................4

Dividend Policy...........................................................................................................................................7

Risk Profile..................................................................................................................................................8

Optimal Capital Structure of Rio Tinto.......................................................................................................9

DCF Model................................................................................................................................................11

Part B.........................................................................................................................................................13

NPV.......................................................................................................................................................14

IRR........................................................................................................................................................15

Payback Period......................................................................................................................................16

Profitability Index..................................................................................................................................17

Conclusion.................................................................................................................................................18

References.................................................................................................................................................20

Contents

Part A..........................................................................................................................................................3

Introduction.................................................................................................................................................3

Corporate governance..................................................................................................................................4

Financial performance.................................................................................................................................4

Dividend Policy...........................................................................................................................................7

Risk Profile..................................................................................................................................................8

Optimal Capital Structure of Rio Tinto.......................................................................................................9

DCF Model................................................................................................................................................11

Part B.........................................................................................................................................................13

NPV.......................................................................................................................................................14

IRR........................................................................................................................................................15

Payback Period......................................................................................................................................16

Profitability Index..................................................................................................................................17

Conclusion.................................................................................................................................................18

References.................................................................................................................................................20

Running Head: CORPORATE FINANCIAL MANAGEMENT

Part A

Introduction

Corporate finance is an area of finance that deals with the sources of funding, capital structure,

the action that manager take to increase the value of the organization. It is required to use the

financial tool to allocate the financial resources appropriately (Fracassi, 2016). It is essential to

analyze the financial position of the company to allocate the resources in an appropriate manner.

There are different terms and policy developed in the form of standard just to manage the

financial statements of the company accurately such as income statements, profit and loss and

balance sheet. The items are recorded under the different heads as per the standards and policy so

that the financial performance of the company is easily evaluated (Dang, Li, and Yang, 2018).

However, the analysis or forecasting the financial position of the company it is necessary to

evaluate the financial ratios and the other calculations (Tricker, and Tricker, 2015). In this

report, the discussion is based on the financial analysis of the company. In this paper, Rio Tinto

has been taken into consideration to evaluate the financial performance as per the standards.

Rio Tinto is an Australian multinational company which operates the business in metals and

mining. It was founded in the year 1873 while purchasing the mine complex. The company is

growing with the method of mergers and acquisitions. It operates in six components such as

Australia and Canada (Rio Tinto, 2018a).

The report is classified in two parts such as task 1 and task 2. In task 1, the different terms and

policy of financial statements will be discussed. In task 2, investment appraisal techniques will

be discussed with the evaluation.

Part A

Introduction

Corporate finance is an area of finance that deals with the sources of funding, capital structure,

the action that manager take to increase the value of the organization. It is required to use the

financial tool to allocate the financial resources appropriately (Fracassi, 2016). It is essential to

analyze the financial position of the company to allocate the resources in an appropriate manner.

There are different terms and policy developed in the form of standard just to manage the

financial statements of the company accurately such as income statements, profit and loss and

balance sheet. The items are recorded under the different heads as per the standards and policy so

that the financial performance of the company is easily evaluated (Dang, Li, and Yang, 2018).

However, the analysis or forecasting the financial position of the company it is necessary to

evaluate the financial ratios and the other calculations (Tricker, and Tricker, 2015). In this

report, the discussion is based on the financial analysis of the company. In this paper, Rio Tinto

has been taken into consideration to evaluate the financial performance as per the standards.

Rio Tinto is an Australian multinational company which operates the business in metals and

mining. It was founded in the year 1873 while purchasing the mine complex. The company is

growing with the method of mergers and acquisitions. It operates in six components such as

Australia and Canada (Rio Tinto, 2018a).

The report is classified in two parts such as task 1 and task 2. In task 1, the different terms and

policy of financial statements will be discussed. In task 2, investment appraisal techniques will

be discussed with the evaluation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: CORPORATE FINANCIAL MANAGEMENT

Corporate governance

Corporate governance is the grouping of processes, rules or laws by which organization are

functions are operated, controlled and regulated (McCahery, Sautner, and Starks, 2016). In the

case of Rio Tinto, the board of directors develops laws, rules to control or operates the functions

of the business. It has been seen that the directors of the company are collectively responsible for

the long term success of the group. Board of Directors of the company is classified in three

positions such as chairman, executive and non-executive. The chairman of the company is Simon

Thompson, Chief executive is Jean Sesbastien Jacques, Chief Financial Officer is Jackob

Stausholm, and non-executive director is Megan Clark AC.

There are also other committee’s such as Audit committee, chairman committee, sustainability

committee, remuneration committee (Rio Tinto, 2018b). Different committee manages the

different activities of the company such as executive committee responsible for delivering of

strategy, annual plans and commercial objectives. The role of board of directors of the company

is to develop the laws and rules to operate the business effectively. The rules and regulation are

introduced by the directors as per the financial performance of the company just to control the

functions (Tricker, and Tricker, 2015).

Financial performance

Financial Ratio

Analysis

Rio Tinto

2017 2018

Profitability Ratio

Gross Profit Margin Gross Profit 24223 23963

Net Sales 40030 61% 40522 59%

Corporate governance

Corporate governance is the grouping of processes, rules or laws by which organization are

functions are operated, controlled and regulated (McCahery, Sautner, and Starks, 2016). In the

case of Rio Tinto, the board of directors develops laws, rules to control or operates the functions

of the business. It has been seen that the directors of the company are collectively responsible for

the long term success of the group. Board of Directors of the company is classified in three

positions such as chairman, executive and non-executive. The chairman of the company is Simon

Thompson, Chief executive is Jean Sesbastien Jacques, Chief Financial Officer is Jackob

Stausholm, and non-executive director is Megan Clark AC.

There are also other committee’s such as Audit committee, chairman committee, sustainability

committee, remuneration committee (Rio Tinto, 2018b). Different committee manages the

different activities of the company such as executive committee responsible for delivering of

strategy, annual plans and commercial objectives. The role of board of directors of the company

is to develop the laws and rules to operate the business effectively. The rules and regulation are

introduced by the directors as per the financial performance of the company just to control the

functions (Tricker, and Tricker, 2015).

Financial performance

Financial Ratio

Analysis

Rio Tinto

2017 2018

Profitability Ratio

Gross Profit Margin Gross Profit 24223 23963

Net Sales 40030 61% 40522 59%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: CORPORATE FINANCIAL MANAGEMENT

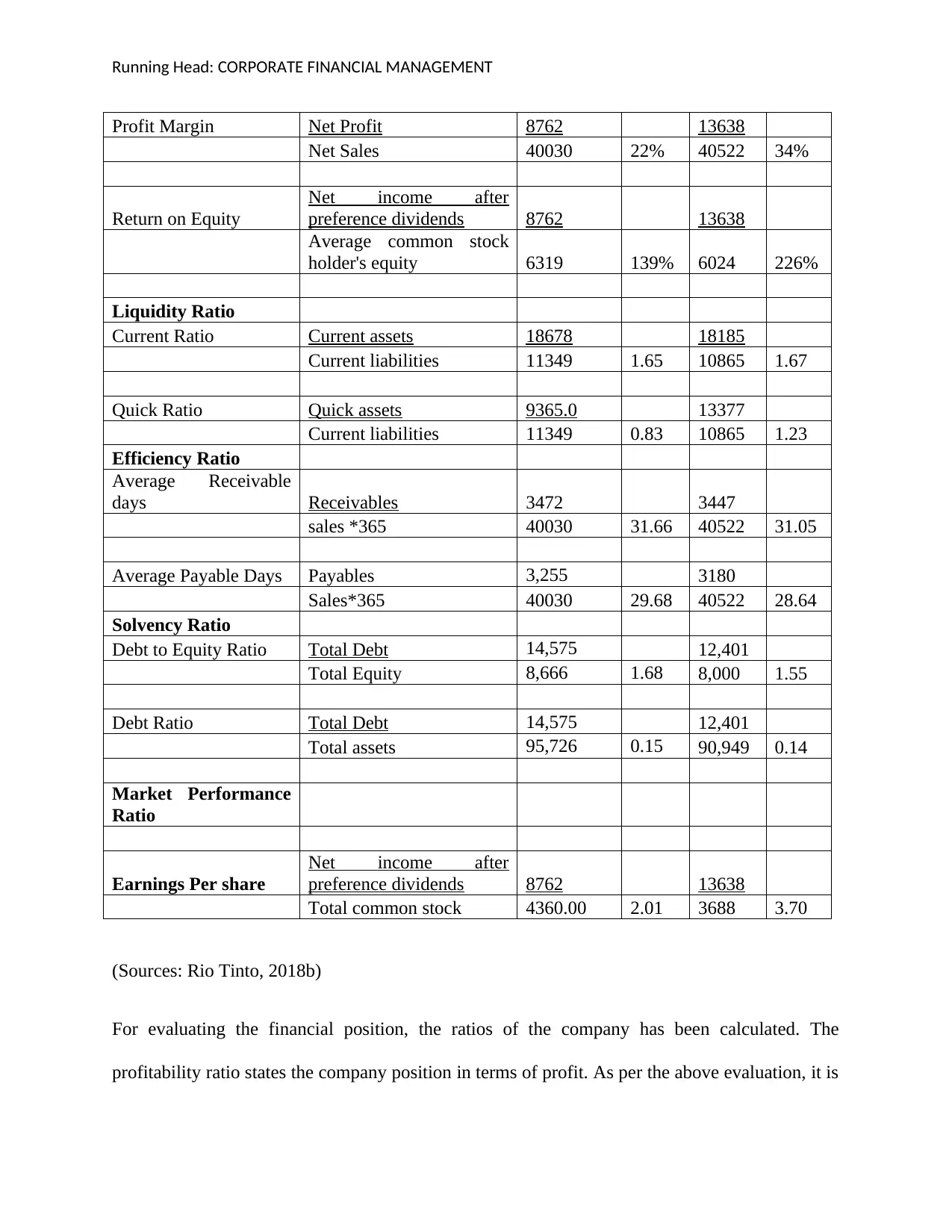

Profit Margin Net Profit 8762 13638

Net Sales 40030 22% 40522 34%

Return on Equity

Net income after

preference dividends 8762 13638

Average common stock

holder's equity 6319 139% 6024 226%

Liquidity Ratio

Current Ratio Current assets 18678 18185

Current liabilities 11349 1.65 10865 1.67

Quick Ratio Quick assets 9365.0 13377

Current liabilities 11349 0.83 10865 1.23

Efficiency Ratio

Average Receivable

days Receivables 3472 3447

sales *365 40030 31.66 40522 31.05

Average Payable Days Payables 3,255 3180

Sales*365 40030 29.68 40522 28.64

Solvency Ratio

Debt to Equity Ratio Total Debt 14,575 12,401

Total Equity 8,666 1.68 8,000 1.55

Debt Ratio Total Debt 14,575 12,401

Total assets 95,726 0.15 90,949 0.14

Market Performance

Ratio

Earnings Per share

Net income after

preference dividends 8762 13638

Total common stock 4360.00 2.01 3688 3.70

(Sources: Rio Tinto, 2018b)

For evaluating the financial position, the ratios of the company has been calculated. The

profitability ratio states the company position in terms of profit. As per the above evaluation, it is

Profit Margin Net Profit 8762 13638

Net Sales 40030 22% 40522 34%

Return on Equity

Net income after

preference dividends 8762 13638

Average common stock

holder's equity 6319 139% 6024 226%

Liquidity Ratio

Current Ratio Current assets 18678 18185

Current liabilities 11349 1.65 10865 1.67

Quick Ratio Quick assets 9365.0 13377

Current liabilities 11349 0.83 10865 1.23

Efficiency Ratio

Average Receivable

days Receivables 3472 3447

sales *365 40030 31.66 40522 31.05

Average Payable Days Payables 3,255 3180

Sales*365 40030 29.68 40522 28.64

Solvency Ratio

Debt to Equity Ratio Total Debt 14,575 12,401

Total Equity 8,666 1.68 8,000 1.55

Debt Ratio Total Debt 14,575 12,401

Total assets 95,726 0.15 90,949 0.14

Market Performance

Ratio

Earnings Per share

Net income after

preference dividends 8762 13638

Total common stock 4360.00 2.01 3688 3.70

(Sources: Rio Tinto, 2018b)

For evaluating the financial position, the ratios of the company has been calculated. The

profitability ratio states the company position in terms of profit. As per the above evaluation, it is

Running Head: CORPORATE FINANCIAL MANAGEMENT

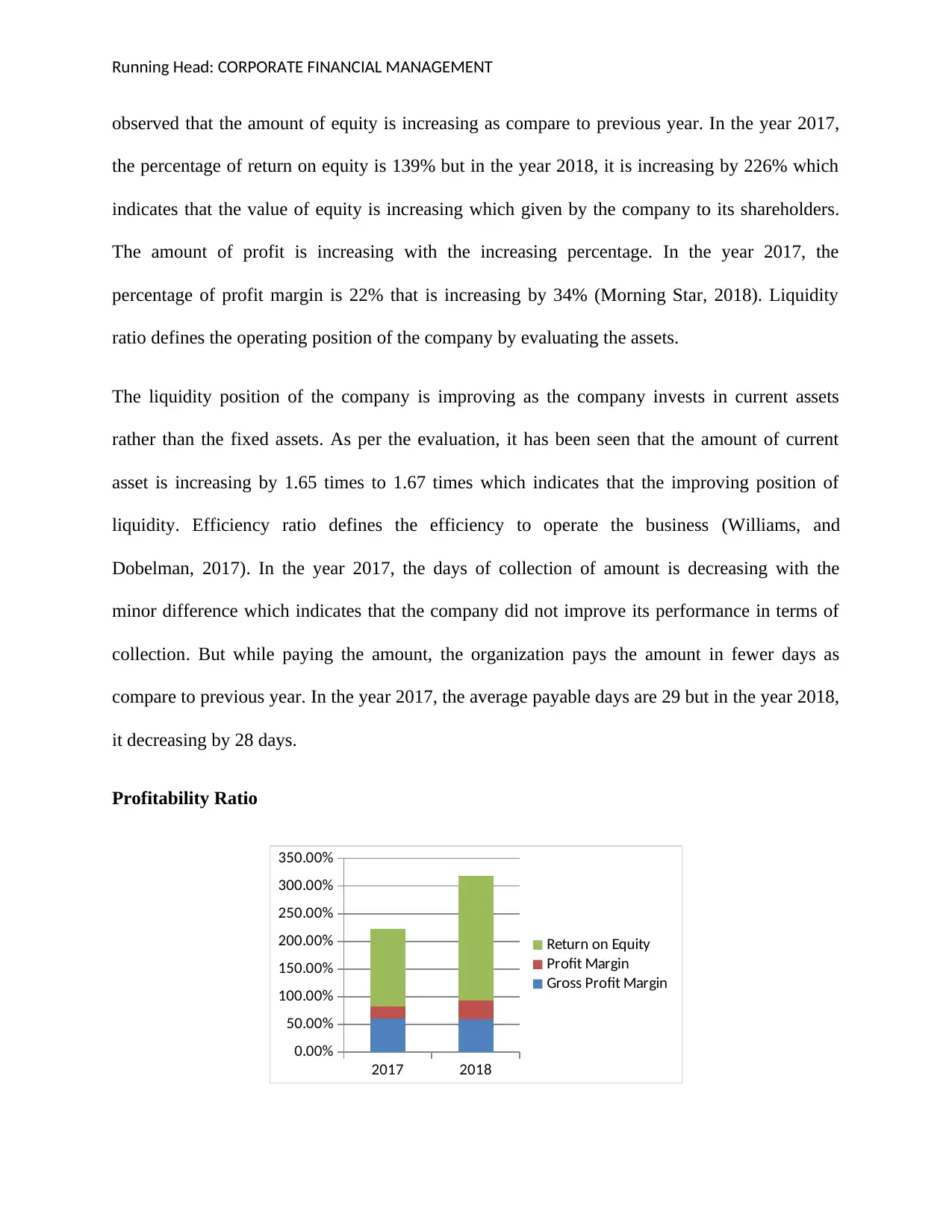

observed that the amount of equity is increasing as compare to previous year. In the year 2017,

the percentage of return on equity is 139% but in the year 2018, it is increasing by 226% which

indicates that the value of equity is increasing which given by the company to its shareholders.

The amount of profit is increasing with the increasing percentage. In the year 2017, the

percentage of profit margin is 22% that is increasing by 34% (Morning Star, 2018). Liquidity

ratio defines the operating position of the company by evaluating the assets.

The liquidity position of the company is improving as the company invests in current assets

rather than the fixed assets. As per the evaluation, it has been seen that the amount of current

asset is increasing by 1.65 times to 1.67 times which indicates that the improving position of

liquidity. Efficiency ratio defines the efficiency to operate the business (Williams, and

Dobelman, 2017). In the year 2017, the days of collection of amount is decreasing with the

minor difference which indicates that the company did not improve its performance in terms of

collection. But while paying the amount, the organization pays the amount in fewer days as

compare to previous year. In the year 2017, the average payable days are 29 but in the year 2018,

it decreasing by 28 days.

Profitability Ratio

2017 2018

0.00%

50.00%

100.00%

150.00%

200.00%

250.00%

300.00%

350.00%

Return on Equity

Profit Margin

Gross Profit Margin

observed that the amount of equity is increasing as compare to previous year. In the year 2017,

the percentage of return on equity is 139% but in the year 2018, it is increasing by 226% which

indicates that the value of equity is increasing which given by the company to its shareholders.

The amount of profit is increasing with the increasing percentage. In the year 2017, the

percentage of profit margin is 22% that is increasing by 34% (Morning Star, 2018). Liquidity

ratio defines the operating position of the company by evaluating the assets.

The liquidity position of the company is improving as the company invests in current assets

rather than the fixed assets. As per the evaluation, it has been seen that the amount of current

asset is increasing by 1.65 times to 1.67 times which indicates that the improving position of

liquidity. Efficiency ratio defines the efficiency to operate the business (Williams, and

Dobelman, 2017). In the year 2017, the days of collection of amount is decreasing with the

minor difference which indicates that the company did not improve its performance in terms of

collection. But while paying the amount, the organization pays the amount in fewer days as

compare to previous year. In the year 2017, the average payable days are 29 but in the year 2018,

it decreasing by 28 days.

Profitability Ratio

2017 2018

0.00%

50.00%

100.00%

150.00%

200.00%

250.00%

300.00%

350.00%

Return on Equity

Profit Margin

Gross Profit Margin

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: CORPORATE FINANCIAL MANAGEMENT

The solvency ratio defines that the stability of the company (Robinson, Henry, Pirie, and

Broihahn, 2015). As per the evaluation of solvency ratio of the company, it is observed that the

amount of debts is decreasing which reflects positive sign to operate smoothly in the market. In

the previous year 2017, the debt ratio is 0.15 which is decreasing with the ratio 0.14 (Rio Tinto,

2018b). The debt ratio of the company indicates that it can survive for long time in the market as

it borrows the fewer amounts on credit which is a positive situation.

Dividend Policy

Dividend Policy is the financial policy which is used to evaluate the amount of dividend by the

company to its shareholders. Under this policy, the frequency is also evaluated with which the

dividend is paid by the company (CFI, 2018). Rio Tinto declared a surprise $1bn special

dividend after writing its best half years profit. The miner declared a half year dividend of 151

cents per share and also a special dividend of 61 cents per share, equivalent to $3.5bn and a

record half year payout. While the company operates Oyu Tologi, it does not have a direct

holding of shares.

The company has 50.8 percent controlling stake and 34 per cent by Mongolian government. The

number of share of the company has been arises with the 27 percent this year but it is also fell

with 2.8 percent to £45.68 (Hume, 2019). It indicates that the paid amount of dividend is also

decreasing due to which the company will face the issues of financial crises. It has been

evaluated that the decreasing dividend paid indicates the less investment just because of low

capital. It requires the large amount of capital that is why; it has to borrow the amount on debt

(Baker, and Weigand, 2015).

The solvency ratio defines that the stability of the company (Robinson, Henry, Pirie, and

Broihahn, 2015). As per the evaluation of solvency ratio of the company, it is observed that the

amount of debts is decreasing which reflects positive sign to operate smoothly in the market. In

the previous year 2017, the debt ratio is 0.15 which is decreasing with the ratio 0.14 (Rio Tinto,

2018b). The debt ratio of the company indicates that it can survive for long time in the market as

it borrows the fewer amounts on credit which is a positive situation.

Dividend Policy

Dividend Policy is the financial policy which is used to evaluate the amount of dividend by the

company to its shareholders. Under this policy, the frequency is also evaluated with which the

dividend is paid by the company (CFI, 2018). Rio Tinto declared a surprise $1bn special

dividend after writing its best half years profit. The miner declared a half year dividend of 151

cents per share and also a special dividend of 61 cents per share, equivalent to $3.5bn and a

record half year payout. While the company operates Oyu Tologi, it does not have a direct

holding of shares.

The company has 50.8 percent controlling stake and 34 per cent by Mongolian government. The

number of share of the company has been arises with the 27 percent this year but it is also fell

with 2.8 percent to £45.68 (Hume, 2019). It indicates that the paid amount of dividend is also

decreasing due to which the company will face the issues of financial crises. It has been

evaluated that the decreasing dividend paid indicates the less investment just because of low

capital. It requires the large amount of capital that is why; it has to borrow the amount on debt

(Baker, and Weigand, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: CORPORATE FINANCIAL MANAGEMENT

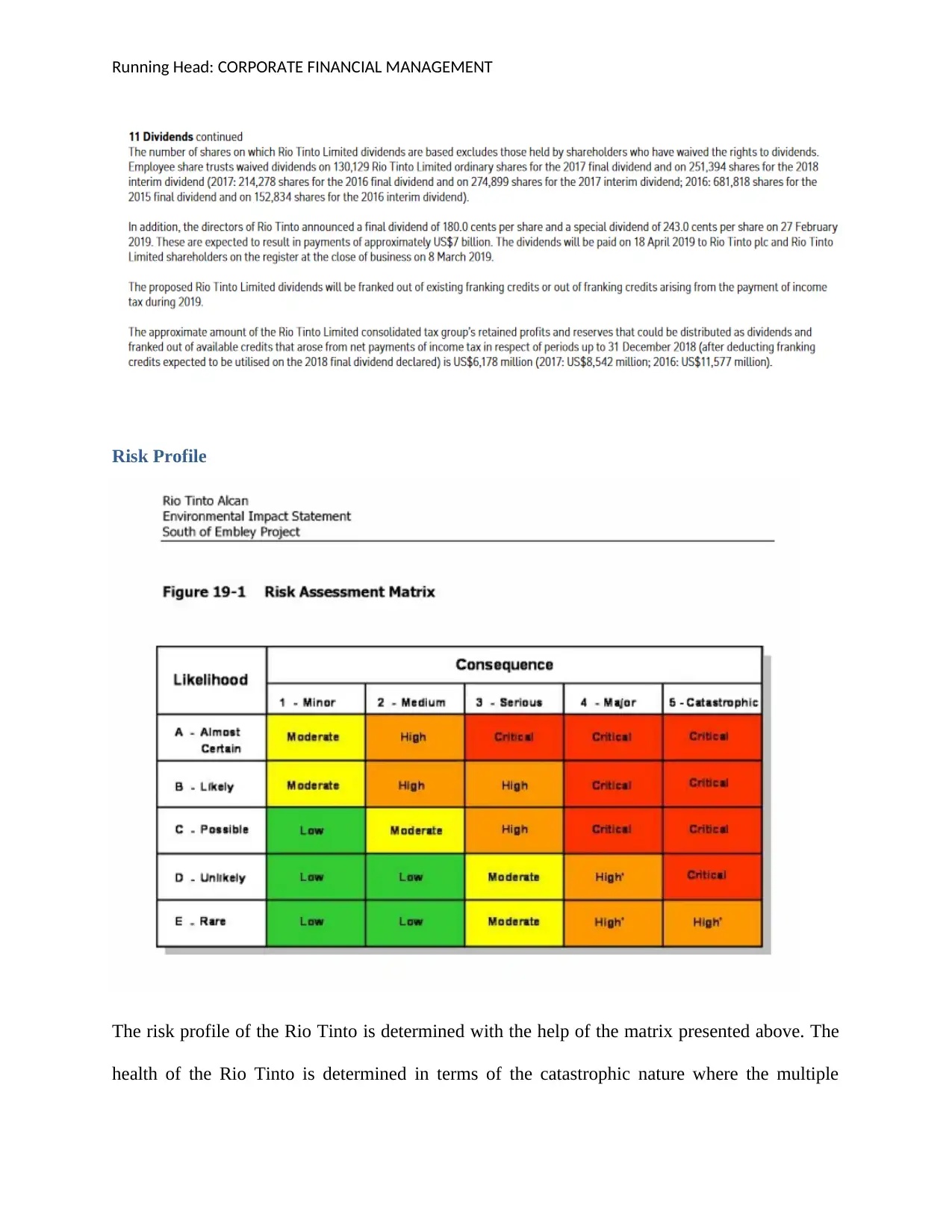

Risk Profile

The risk profile of the Rio Tinto is determined with the help of the matrix presented above. The

health of the Rio Tinto is determined in terms of the catastrophic nature where the multiple

Risk Profile

The risk profile of the Rio Tinto is determined with the help of the matrix presented above. The

health of the Rio Tinto is determined in terms of the catastrophic nature where the multiple

Running Head: CORPORATE FINANCIAL MANAGEMENT

fatalities or serious problems are taken into consideration. The safety of the company is also

measured on site which is related to the risk possessed in the environment and the risks which

are possessed outside the environment (Rio Tinto, 2019). The risk management in the year 2018

remained unsettled with the rising tension of increased volatility of the market. The increased

pressure from the market tends to be continuous and the company has focused on delivering the

operational efficiency in the business operations (Ortas, Gallego‐Alvarez and Álvarez Etxeberria,

2015). The continuous macroeconomic and the geopolitical uncertainty is one of the crucial risks

that have been face by Rio Tinto. The short term risks like the increase in the rate of exchange

have created a tension on the trade platform. Climate change represents perhaps the greatest

long-term threat to our business, but also brings opportunities. There are several other risks

which are possessed by the company such as – physical, regulatory and market. A low-carbon

economy may lead to structural shifts such as a step-change in recycling, but it will also fuel

higher demand for commodities like copper and raw materials for the batteries (Rio Tinto, 2019).

Optimal Capital Structure of Rio Tinto

The capital structure of Rio Tinto is an amalgamation of the debt as well as equity. The

amalgamation of the debt and the equity can be understood with the help of the debt and the

equity ratio. The purpose if the capital structure is how a firm finances its operations and the

growth with the help of the different sources of the funds. The debt comes in the form of bonds,

issues, and long term notes payable whereas the equity is in the form of the common stock,

preferred stock, and retained earnings (Cornell and Gokhale, 2016).

Debt is one of the ways to raise the capital of the business and the major reason behind the issue

of the debt is to gain the tax advantage of the business. Since the interest payments are

fatalities or serious problems are taken into consideration. The safety of the company is also

measured on site which is related to the risk possessed in the environment and the risks which

are possessed outside the environment (Rio Tinto, 2019). The risk management in the year 2018

remained unsettled with the rising tension of increased volatility of the market. The increased

pressure from the market tends to be continuous and the company has focused on delivering the

operational efficiency in the business operations (Ortas, Gallego‐Alvarez and Álvarez Etxeberria,

2015). The continuous macroeconomic and the geopolitical uncertainty is one of the crucial risks

that have been face by Rio Tinto. The short term risks like the increase in the rate of exchange

have created a tension on the trade platform. Climate change represents perhaps the greatest

long-term threat to our business, but also brings opportunities. There are several other risks

which are possessed by the company such as – physical, regulatory and market. A low-carbon

economy may lead to structural shifts such as a step-change in recycling, but it will also fuel

higher demand for commodities like copper and raw materials for the batteries (Rio Tinto, 2019).

Optimal Capital Structure of Rio Tinto

The capital structure of Rio Tinto is an amalgamation of the debt as well as equity. The

amalgamation of the debt and the equity can be understood with the help of the debt and the

equity ratio. The purpose if the capital structure is how a firm finances its operations and the

growth with the help of the different sources of the funds. The debt comes in the form of bonds,

issues, and long term notes payable whereas the equity is in the form of the common stock,

preferred stock, and retained earnings (Cornell and Gokhale, 2016).

Debt is one of the ways to raise the capital of the business and the major reason behind the issue

of the debt is to gain the tax advantage of the business. Since the interest payments are

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: CORPORATE FINANCIAL MANAGEMENT

deductible, debt always allows the company to retain the ownership whereas the Equity on the

other hand is more expensive when the interest rates are so low. However, unlike the debt the

equity is not paid back if the earnings are declined (Reid, 2018).

Optimal capital structure is a metric that the organizations use to determine the best mix of debt

and equity financing for the purpose of the operations of the business. The optimal capital

structure helps in the reduction of the cost of the capital, in order to keep the firm less dependent

on creditors and is able to finance the assets with the help of the equity as well (Burtonshaw-

Gunn, 2017).

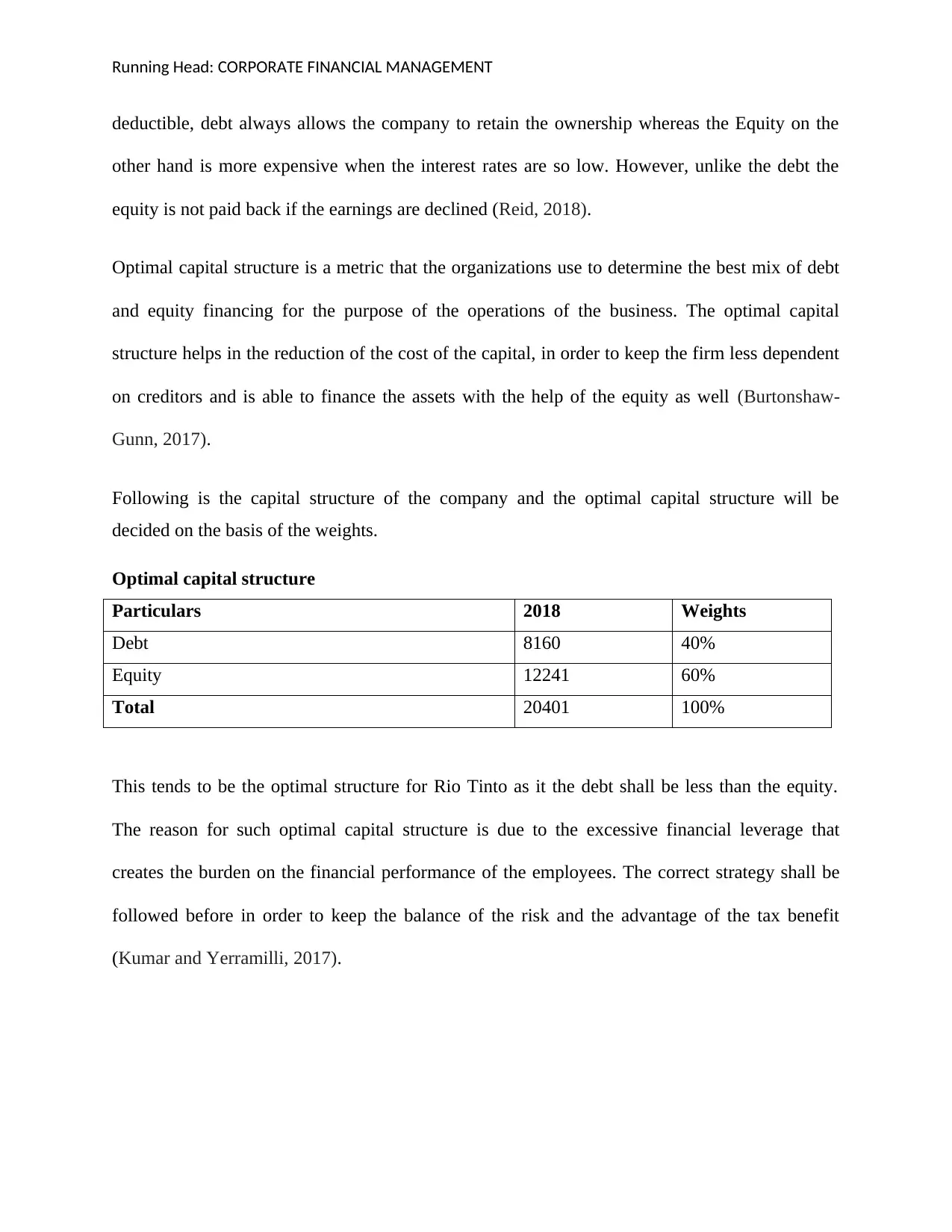

Following is the capital structure of the company and the optimal capital structure will be

decided on the basis of the weights.

Optimal capital structure

Particulars 2018 Weights

Debt 8160 40%

Equity 12241 60%

Total 20401 100%

This tends to be the optimal structure for Rio Tinto as it the debt shall be less than the equity.

The reason for such optimal capital structure is due to the excessive financial leverage that

creates the burden on the financial performance of the employees. The correct strategy shall be

followed before in order to keep the balance of the risk and the advantage of the tax benefit

(Kumar and Yerramilli, 2017).

deductible, debt always allows the company to retain the ownership whereas the Equity on the

other hand is more expensive when the interest rates are so low. However, unlike the debt the

equity is not paid back if the earnings are declined (Reid, 2018).

Optimal capital structure is a metric that the organizations use to determine the best mix of debt

and equity financing for the purpose of the operations of the business. The optimal capital

structure helps in the reduction of the cost of the capital, in order to keep the firm less dependent

on creditors and is able to finance the assets with the help of the equity as well (Burtonshaw-

Gunn, 2017).

Following is the capital structure of the company and the optimal capital structure will be

decided on the basis of the weights.

Optimal capital structure

Particulars 2018 Weights

Debt 8160 40%

Equity 12241 60%

Total 20401 100%

This tends to be the optimal structure for Rio Tinto as it the debt shall be less than the equity.

The reason for such optimal capital structure is due to the excessive financial leverage that

creates the burden on the financial performance of the employees. The correct strategy shall be

followed before in order to keep the balance of the risk and the advantage of the tax benefit

(Kumar and Yerramilli, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: CORPORATE FINANCIAL MANAGEMENT

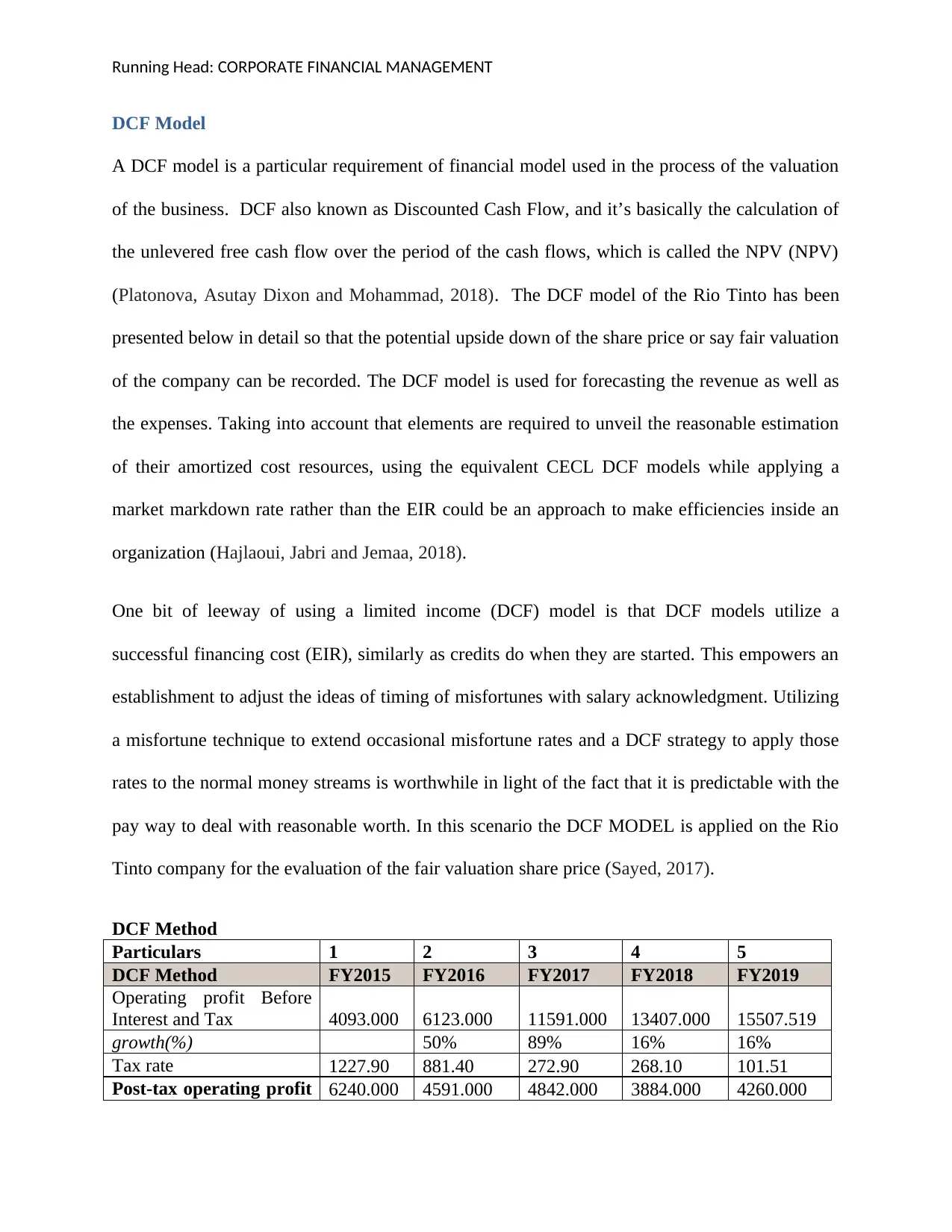

DCF Model

A DCF model is a particular requirement of financial model used in the process of the valuation

of the business. DCF also known as Discounted Cash Flow, and it’s basically the calculation of

the unlevered free cash flow over the period of the cash flows, which is called the NPV (NPV)

(Platonova, Asutay Dixon and Mohammad, 2018). The DCF model of the Rio Tinto has been

presented below in detail so that the potential upside down of the share price or say fair valuation

of the company can be recorded. The DCF model is used for forecasting the revenue as well as

the expenses. Taking into account that elements are required to unveil the reasonable estimation

of their amortized cost resources, using the equivalent CECL DCF models while applying a

market markdown rate rather than the EIR could be an approach to make efficiencies inside an

organization (Hajlaoui, Jabri and Jemaa, 2018).

One bit of leeway of using a limited income (DCF) model is that DCF models utilize a

successful financing cost (EIR), similarly as credits do when they are started. This empowers an

establishment to adjust the ideas of timing of misfortunes with salary acknowledgment. Utilizing

a misfortune technique to extend occasional misfortune rates and a DCF strategy to apply those

rates to the normal money streams is worthwhile in light of the fact that it is predictable with the

pay way to deal with reasonable worth. In this scenario the DCF MODEL is applied on the Rio

Tinto company for the evaluation of the fair valuation share price (Sayed, 2017).

DCF Method

Particulars 1 2 3 4 5

DCF Method FY2015 FY2016 FY2017 FY2018 FY2019

Operating profit Before

Interest and Tax 4093.000 6123.000 11591.000 13407.000 15507.519

growth(%) 50% 89% 16% 16%

Tax rate 1227.90 881.40 272.90 268.10 101.51

Post-tax operating profit 6240.000 4591.000 4842.000 3884.000 4260.000

DCF Model

A DCF model is a particular requirement of financial model used in the process of the valuation

of the business. DCF also known as Discounted Cash Flow, and it’s basically the calculation of

the unlevered free cash flow over the period of the cash flows, which is called the NPV (NPV)

(Platonova, Asutay Dixon and Mohammad, 2018). The DCF model of the Rio Tinto has been

presented below in detail so that the potential upside down of the share price or say fair valuation

of the company can be recorded. The DCF model is used for forecasting the revenue as well as

the expenses. Taking into account that elements are required to unveil the reasonable estimation

of their amortized cost resources, using the equivalent CECL DCF models while applying a

market markdown rate rather than the EIR could be an approach to make efficiencies inside an

organization (Hajlaoui, Jabri and Jemaa, 2018).

One bit of leeway of using a limited income (DCF) model is that DCF models utilize a

successful financing cost (EIR), similarly as credits do when they are started. This empowers an

establishment to adjust the ideas of timing of misfortunes with salary acknowledgment. Utilizing

a misfortune technique to extend occasional misfortune rates and a DCF strategy to apply those

rates to the normal money streams is worthwhile in light of the fact that it is predictable with the

pay way to deal with reasonable worth. In this scenario the DCF MODEL is applied on the Rio

Tinto company for the evaluation of the fair valuation share price (Sayed, 2017).

DCF Method

Particulars 1 2 3 4 5

DCF Method FY2015 FY2016 FY2017 FY2018 FY2019

Operating profit Before

Interest and Tax 4093.000 6123.000 11591.000 13407.000 15507.519

growth(%) 50% 89% 16% 16%

Tax rate 1227.90 881.40 272.90 268.10 101.51

Post-tax operating profit 6240.000 4591.000 4842.000 3884.000 4260.000

Running Head: CORPORATE FINANCIAL MANAGEMENT

(NOPAT)

Add: Depreciation &

amortization 2,005 2,086 2,126 2,122 2,136

Less: Change in working

capital

1,9

30.00 502.00 570.00 955.00

1,0

72.00

Less: Capex 4,6

85.00

3,0

12.00

4,4

82.00

5,4

30.00

5,2

60.00

Free Cash Flow to Firm 1

4,860 10,191 12,020 12,391 12,728

FCF growth (0.31) 0.18 0.03 0.03

Discount factor 0.953 0.908 0.865 0.825 0.786

PV of Free Cash Flows 14,16

0.44

9,2

54.24

10,4

02.13

10,2

18.19

10,0

02.07

Sum of present values of

FCFs

54,03

7.06

Free cash flow (t+1) 13109.5

Terminal value 3%

Present value of

terminal value 676538

Enterprise Value 730,57

4.73

Less:

Net debt 124010

Minorities

Equity value 854,58

4.73

Fair value per share

(OMR) 49.71

Upside/Downside 2%

48.63

(NOPAT)

Add: Depreciation &

amortization 2,005 2,086 2,126 2,122 2,136

Less: Change in working

capital

1,9

30.00 502.00 570.00 955.00

1,0

72.00

Less: Capex 4,6

85.00

3,0

12.00

4,4

82.00

5,4

30.00

5,2

60.00

Free Cash Flow to Firm 1

4,860 10,191 12,020 12,391 12,728

FCF growth (0.31) 0.18 0.03 0.03

Discount factor 0.953 0.908 0.865 0.825 0.786

PV of Free Cash Flows 14,16

0.44

9,2

54.24

10,4

02.13

10,2

18.19

10,0

02.07

Sum of present values of

FCFs

54,03

7.06

Free cash flow (t+1) 13109.5

Terminal value 3%

Present value of

terminal value 676538

Enterprise Value 730,57

4.73

Less:

Net debt 124010

Minorities

Equity value 854,58

4.73

Fair value per share

(OMR) 49.71

Upside/Downside 2%

48.63

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.