Corporate and Financial Accounting Report: International Standards

VerifiedAdded on 2023/06/04

|13

|3039

|111

Report

AI Summary

This report provides an overview of corporate and financial accounting from an international perspective. It begins by discussing the importance of financial reporting regulation and the role of voluntary disclosure. The report then explores accounting standard setting, focusing on the role of the AASB in the global standard-setting process and the reasons why IFRS is not compulsory for all IASB member countries. Finally, the report analyzes the owner's equity and debt-to-equity positions of four companies listed on the ASX: ANZ Bank, Bank of Queensland, Commonwealth Bank, and ASX Limited, providing insights into their capital structures and financial leverage over a four-year period. The analysis includes the debt-to-equity ratios of the selected companies and their implications for financial health and investment strategies.

Running head: CORPORATE AND FINANCIAL ACCOUNTING

Corporate and Financial Accounting

Name of the Student

Name of the University

Author Note

Corporate and Financial Accounting

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2CORPORATE AND FINANCIAL ACCOUNTING

Executive Summary

The main aim of this report is to provide a brief account of the accounting standard, corporate

regulation and the owners equity from the world perspective. As per reports, it is found that

the managers may not be willing to share the financial information that is relevant to all users

of the financial statements. This is the main reason why regulation and financial reporting is

necessary while preparing financial statements. It is well documented that all nations have

their own accounting standards. The organisations like IASB have made attempts to develop

a single standard that should be acceptable to most countries.

Executive Summary

The main aim of this report is to provide a brief account of the accounting standard, corporate

regulation and the owners equity from the world perspective. As per reports, it is found that

the managers may not be willing to share the financial information that is relevant to all users

of the financial statements. This is the main reason why regulation and financial reporting is

necessary while preparing financial statements. It is well documented that all nations have

their own accounting standards. The organisations like IASB have made attempts to develop

a single standard that should be acceptable to most countries.

3CORPORATE AND FINANCIAL ACCOUNTING

Table of Contents

Introduction................................................................................................................................4

Corporate regulation...................................................................................................................4

Answer to question I..............................................................................................................4

Accounting standard setting.......................................................................................................5

Answer to Question II............................................................................................................5

Owner’s equity...........................................................................................................................7

Answer to question III............................................................................................................7

Answer to Question IV...........................................................................................................8

Conclusion................................................................................................................................10

References................................................................................................................................11

Table of Contents

Introduction................................................................................................................................4

Corporate regulation...................................................................................................................4

Answer to question I..............................................................................................................4

Accounting standard setting.......................................................................................................5

Answer to Question II............................................................................................................5

Owner’s equity...........................................................................................................................7

Answer to question III............................................................................................................7

Answer to Question IV...........................................................................................................8

Conclusion................................................................................................................................10

References................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4CORPORATE AND FINANCIAL ACCOUNTING

Introduction

This report is made with an intention of providing a brief account of the owners

equity, corporate regulation and accounting standard from the international perspective. The

first section would provide a brief account of the importance and necessity of regulation in

financial accounting . It also provides a brief account of the voluntary disclosure of financial

accounting information. In the second section of the report it would emphasise on the role of

AASB and its helpfulness in setting the international standard setting process which is called

the IFRS. It would also discuss the reasons why IFRS is not compulsory for the member

nations of IASB to follow. Finally the report would shed some light on selecting four

companies from the companies that are listed in ASX and an evaluation would be made in

relation their owner’s equity position as well as the equity debt position of these companies.

Corporate regulation

Answer to question I

Favourable points for regulation of financial accounting and reporting

There exists a basic need so that it can regulate financial reporting due to numerous

reasons. First of all if the information is not regulated, the information published by the

business organisation might be selective. It could be manipulated by the individuals

accountable to reveal the same information to the public. Hence the organisations need to

fulfil various requirements for aligning the public interest of both current and potential

investors. The regulation authorities formulated the criteria for assuring information quality at

minimal or zero cost . It helps in shielding the public from hidden, fraudulent and misleading

disclosures(Leuz and Wysocki 2016 ) Secondly there is an increasing demand for actual and

true accounting information for prospective investors. When business entities make

investments, it becomes necessary for the regulating authorities to intervene . They intervene

Introduction

This report is made with an intention of providing a brief account of the owners

equity, corporate regulation and accounting standard from the international perspective. The

first section would provide a brief account of the importance and necessity of regulation in

financial accounting . It also provides a brief account of the voluntary disclosure of financial

accounting information. In the second section of the report it would emphasise on the role of

AASB and its helpfulness in setting the international standard setting process which is called

the IFRS. It would also discuss the reasons why IFRS is not compulsory for the member

nations of IASB to follow. Finally the report would shed some light on selecting four

companies from the companies that are listed in ASX and an evaluation would be made in

relation their owner’s equity position as well as the equity debt position of these companies.

Corporate regulation

Answer to question I

Favourable points for regulation of financial accounting and reporting

There exists a basic need so that it can regulate financial reporting due to numerous

reasons. First of all if the information is not regulated, the information published by the

business organisation might be selective. It could be manipulated by the individuals

accountable to reveal the same information to the public. Hence the organisations need to

fulfil various requirements for aligning the public interest of both current and potential

investors. The regulation authorities formulated the criteria for assuring information quality at

minimal or zero cost . It helps in shielding the public from hidden, fraudulent and misleading

disclosures(Leuz and Wysocki 2016 ) Secondly there is an increasing demand for actual and

true accounting information for prospective investors. When business entities make

investments, it becomes necessary for the regulating authorities to intervene . They intervene

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5CORPORATE AND FINANCIAL ACCOUNTING

to make sure that the formats f accounting and reporting fulfil the investors needs by

answering their questions.

When an organisation finds that its shares are listed in a stock exchange . It wold be

appropriate for the organisation to publish such information in standardised formats. This

would help in evaluating whether both shareholders and investors have equal knowledge of

information or not(Goodhart, et al. 2013). Hence from the overall discussion it can be said

that the necessity of regulation is increasing the standard of the profession.

Favourable points for voluntary disclosure of financial reporting and accounting

When managers are given the chance of disclosing voluntary financial information ,

they would conduct the work in a fair and responsible manner . Managers have knowledge

about internal activities of the organisations. Hence they have knowledge about actual

financial conditions as well. This would help them in providing a certain non standardised

financial information to the market. When such information is revealed by managers of

companies , the share price of these companies would increase n a substantial manner .

Businesses outside would also be ensured about the financial conditions(Beatty and Liao

2014)

The managers may be unwilling to disclose the internal financial information to all

users of the financial statements. They might distort such information to the investors for

maximising their profits because they fear that they could lose their job. As per the demand

of the regulators, the information should not be made more public. Hence regulation on

financial information and reporting is preferred over voluntary disclosure of financial

information. This is done in order to avoid manipulation and frauds in the financial reports.

to make sure that the formats f accounting and reporting fulfil the investors needs by

answering their questions.

When an organisation finds that its shares are listed in a stock exchange . It wold be

appropriate for the organisation to publish such information in standardised formats. This

would help in evaluating whether both shareholders and investors have equal knowledge of

information or not(Goodhart, et al. 2013). Hence from the overall discussion it can be said

that the necessity of regulation is increasing the standard of the profession.

Favourable points for voluntary disclosure of financial reporting and accounting

When managers are given the chance of disclosing voluntary financial information ,

they would conduct the work in a fair and responsible manner . Managers have knowledge

about internal activities of the organisations. Hence they have knowledge about actual

financial conditions as well. This would help them in providing a certain non standardised

financial information to the market. When such information is revealed by managers of

companies , the share price of these companies would increase n a substantial manner .

Businesses outside would also be ensured about the financial conditions(Beatty and Liao

2014)

The managers may be unwilling to disclose the internal financial information to all

users of the financial statements. They might distort such information to the investors for

maximising their profits because they fear that they could lose their job. As per the demand

of the regulators, the information should not be made more public. Hence regulation on

financial information and reporting is preferred over voluntary disclosure of financial

information. This is done in order to avoid manipulation and frauds in the financial reports.

6CORPORATE AND FINANCIAL ACCOUNTING

Accounting standard setting

Answer to Question II

The process through which AASB participates in the global standard setting process

The AASB has the vision of magnifying its reputation in the form of a leading national

state setter for gaining recognition in international excellence setting. This would be made

sure by maintaining greater quality standards of financial reporting for all Australian

economic sectors by contributing enough talent and leadership(Al-Janadi, Rahman and Omar

2013). AASB takes part in the setting process as follows:

The standard amendments as well as accounting standards made by IASB are in line

with the legislative drafting protocols of Australia

The accounting compilations or standards are file on “ Federal registration Legislative

instruments” and are disclosed on the website of AASB.

The adequate responses are made to all the important drafts of IASB and

IPSASB(Allegrini and Greco 2013).

Reason as to why IFRS is not compulsory for the member countries of IASB

The IASB is a private and independent group. It formulates and approves IFRS. This

group functions under the direct supervision of the IFRS foundation. It is involved in

overseeing the operations conducted by IASB. The IASB was established way back in 1901

to replace the” International Accounting Standards Committee” . Currently, the IASB has

fourteen member nations and in accordance with the constitution of the IFRS foundation.

IASB has full accountability for all technical aspects of the foundation(Brüggemann, Hitz

and Sellhorn 2013). These include complete discretion to pursue its technical goal , which is

subject to needs with the public and the trustees. It takes into account the issuance and

Accounting standard setting

Answer to Question II

The process through which AASB participates in the global standard setting process

The AASB has the vision of magnifying its reputation in the form of a leading national

state setter for gaining recognition in international excellence setting. This would be made

sure by maintaining greater quality standards of financial reporting for all Australian

economic sectors by contributing enough talent and leadership(Al-Janadi, Rahman and Omar

2013). AASB takes part in the setting process as follows:

The standard amendments as well as accounting standards made by IASB are in line

with the legislative drafting protocols of Australia

The accounting compilations or standards are file on “ Federal registration Legislative

instruments” and are disclosed on the website of AASB.

The adequate responses are made to all the important drafts of IASB and

IPSASB(Allegrini and Greco 2013).

Reason as to why IFRS is not compulsory for the member countries of IASB

The IASB is a private and independent group. It formulates and approves IFRS. This

group functions under the direct supervision of the IFRS foundation. It is involved in

overseeing the operations conducted by IASB. The IASB was established way back in 1901

to replace the” International Accounting Standards Committee” . Currently, the IASB has

fourteen member nations and in accordance with the constitution of the IFRS foundation.

IASB has full accountability for all technical aspects of the foundation(Brüggemann, Hitz

and Sellhorn 2013). These include complete discretion to pursue its technical goal , which is

subject to needs with the public and the trustees. It takes into account the issuance and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7CORPORATE AND FINANCIAL ACCOUNTING

formulation of IFRS as well as exposure drafts following the due procedure that is mentioned

in the constitution. Finally, it considers the issuance and approval of interpretations. This is

developed from the end of the committee of IFRS interpretation.

All nations have their respective accounting standards. This helps in bringing

comparability and standardisation . The IASB have made attempts to develop a single

acceptable standard that is acceptable for most countries. Inspite of such attempts , it is not

compulsory for the nations to converge into IFRS. This is because the IFRS have their own

groups of accounting standard(Brochet, Jagolinzer and Riedl 2013) . Hence the IFRS

convergence is not occurring in phases.

Owner’s equity

The four organisations that are selected for this section include ANZ bank , Bank of

Queensland , Commonwealth Bank and ASX limited.

Answer to question III

In the statement of financial position of an entity, the three significant items are

apparent and the equity capital is one of them. According to this statement, the main items of

equity include share capital, reserves and retained earnings. The issued capital is part of the

equity capital of the business organisations. From the annual report of ANZ bank , the issued

capital of the company has risen from $ 28, 765 million to $ 29,088 million between the

years 2014 to 2015. It has remained constant in both years 2016 to 2107. The issued capital

of the Commonwealth bank has fallen from 36,218 $ million to 34217 $ million in the yaers

2014 to 2015 but has risen to $36817 to 37920 $ million in the years 2016 to 2017. For bank

of Queensland , the issued capital has risen from $4213 million to $4516 million in the years

between 2014 and 2015. It also reduced in the years 2016 and 2017. They were reported at

$4266 million and $ 4210 million in the years 2016 and 2017. The issued capital of ASX

formulation of IFRS as well as exposure drafts following the due procedure that is mentioned

in the constitution. Finally, it considers the issuance and approval of interpretations. This is

developed from the end of the committee of IFRS interpretation.

All nations have their respective accounting standards. This helps in bringing

comparability and standardisation . The IASB have made attempts to develop a single

acceptable standard that is acceptable for most countries. Inspite of such attempts , it is not

compulsory for the nations to converge into IFRS. This is because the IFRS have their own

groups of accounting standard(Brochet, Jagolinzer and Riedl 2013) . Hence the IFRS

convergence is not occurring in phases.

Owner’s equity

The four organisations that are selected for this section include ANZ bank , Bank of

Queensland , Commonwealth Bank and ASX limited.

Answer to question III

In the statement of financial position of an entity, the three significant items are

apparent and the equity capital is one of them. According to this statement, the main items of

equity include share capital, reserves and retained earnings. The issued capital is part of the

equity capital of the business organisations. From the annual report of ANZ bank , the issued

capital of the company has risen from $ 28, 765 million to $ 29,088 million between the

years 2014 to 2015. It has remained constant in both years 2016 to 2107. The issued capital

of the Commonwealth bank has fallen from 36,218 $ million to 34217 $ million in the yaers

2014 to 2015 but has risen to $36817 to 37920 $ million in the years 2016 to 2017. For bank

of Queensland , the issued capital has risen from $4213 million to $4516 million in the years

between 2014 and 2015. It also reduced in the years 2016 and 2017. They were reported at

$4266 million and $ 4210 million in the years 2016 and 2017. The issued capital of ASX

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8CORPORATE AND FINANCIAL ACCOUNTING

limited has risen from $ 2907 million to $ 3013 million between 2014 and 2015. It again

decreased to $ 2971 million to $ 3027 million in the years 2016 to 2017.

The next item of equity that is included in this report is retained earnings. This

amount reflects the additional earnings of an organisation that is available to an organisation

after paying out dividends to its shareholders (Sytnik 2014). The retained earnings of the

company ANZ bank has been found to be in decline for the years . The same would be

witnessed for the companies for bank of Queensland and ASX limited. The retained earnings

for the company Commonwealth bank has been found to show an increasing trend over the

years. Therefore from this it can be interpreted that the company Commonwealth Bank

accumulates more equity than all the three companies , since its net assets base is the most

among the four organisations in the banking sector of Australia(Babalola and Abiola 2013).

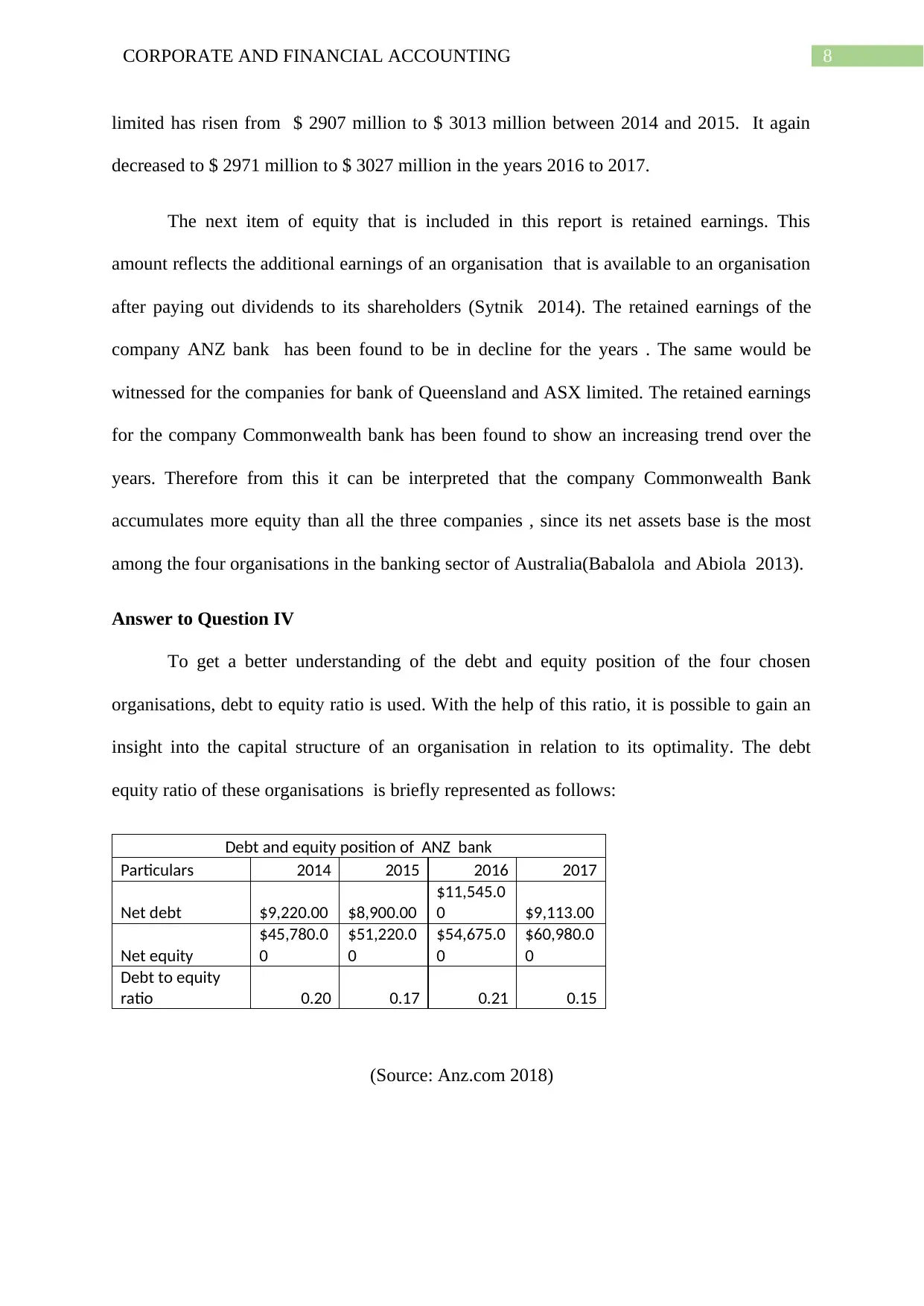

Answer to Question IV

To get a better understanding of the debt and equity position of the four chosen

organisations, debt to equity ratio is used. With the help of this ratio, it is possible to gain an

insight into the capital structure of an organisation in relation to its optimality. The debt

equity ratio of these organisations is briefly represented as follows:

Debt and equity position of ANZ bank

Particulars 2014 2015 2016 2017

Net debt $9,220.00 $8,900.00

$11,545.0

0 $9,113.00

Net equity

$45,780.0

0

$51,220.0

0

$54,675.0

0

$60,980.0

0

Debt to equity

ratio 0.20 0.17 0.21 0.15

(Source: Anz.com 2018)

limited has risen from $ 2907 million to $ 3013 million between 2014 and 2015. It again

decreased to $ 2971 million to $ 3027 million in the years 2016 to 2017.

The next item of equity that is included in this report is retained earnings. This

amount reflects the additional earnings of an organisation that is available to an organisation

after paying out dividends to its shareholders (Sytnik 2014). The retained earnings of the

company ANZ bank has been found to be in decline for the years . The same would be

witnessed for the companies for bank of Queensland and ASX limited. The retained earnings

for the company Commonwealth bank has been found to show an increasing trend over the

years. Therefore from this it can be interpreted that the company Commonwealth Bank

accumulates more equity than all the three companies , since its net assets base is the most

among the four organisations in the banking sector of Australia(Babalola and Abiola 2013).

Answer to Question IV

To get a better understanding of the debt and equity position of the four chosen

organisations, debt to equity ratio is used. With the help of this ratio, it is possible to gain an

insight into the capital structure of an organisation in relation to its optimality. The debt

equity ratio of these organisations is briefly represented as follows:

Debt and equity position of ANZ bank

Particulars 2014 2015 2016 2017

Net debt $9,220.00 $8,900.00

$11,545.0

0 $9,113.00

Net equity

$45,780.0

0

$51,220.0

0

$54,675.0

0

$60,980.0

0

Debt to equity

ratio 0.20 0.17 0.21 0.15

(Source: Anz.com 2018)

9CORPORATE AND FINANCIAL ACCOUNTING

As per the above table, a decrease in debt to equity ratio could be observed from 2014

to 2015, followed by an increase in the year 2016 and with an increase in 2017. A ratio with

0.5 or lower is considered to be the optimal situation for capital structure. In this case the

ratio is less than 0.5 for all the years. This implies that the financial leverage of ANZ Bank

has not been that high because it shows that it has shifted its focus on raising more funds

through issue of equity shares in the market.

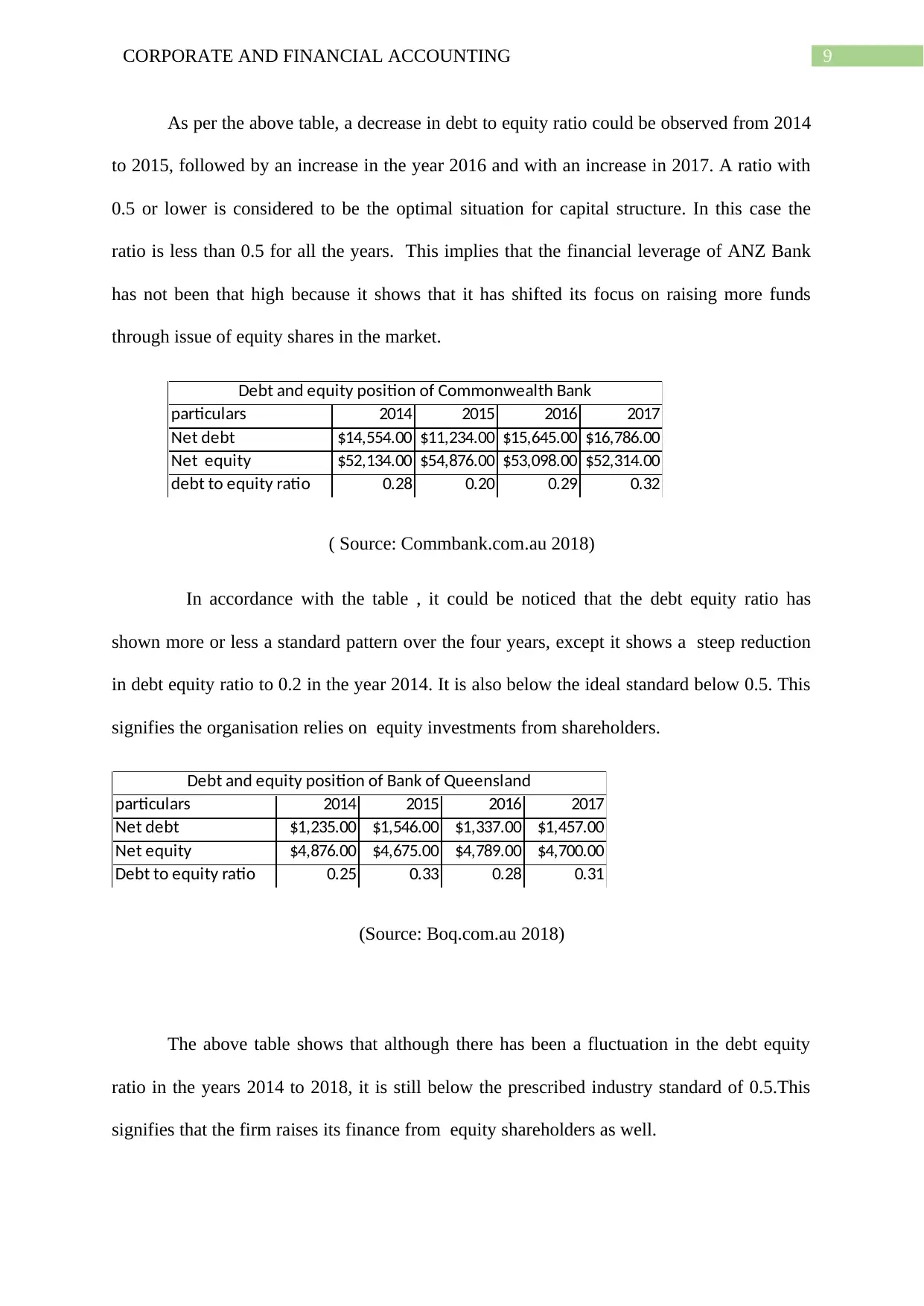

particulars 2014 2015 2016 2017

Net debt $14,554.00 $11,234.00 $15,645.00 $16,786.00

Net equity $52,134.00 $54,876.00 $53,098.00 $52,314.00

debt to equity ratio 0.28 0.20 0.29 0.32

Debt and equity position of Commonwealth Bank

( Source: Commbank.com.au 2018)

In accordance with the table , it could be noticed that the debt equity ratio has

shown more or less a standard pattern over the four years, except it shows a steep reduction

in debt equity ratio to 0.2 in the year 2014. It is also below the ideal standard below 0.5. This

signifies the organisation relies on equity investments from shareholders.

particulars 2014 2015 2016 2017

Net debt $1,235.00 $1,546.00 $1,337.00 $1,457.00

Net equity $4,876.00 $4,675.00 $4,789.00 $4,700.00

Debt to equity ratio 0.25 0.33 0.28 0.31

Debt and equity position of Bank of Queensland

(Source: Boq.com.au 2018)

The above table shows that although there has been a fluctuation in the debt equity

ratio in the years 2014 to 2018, it is still below the prescribed industry standard of 0.5.This

signifies that the firm raises its finance from equity shareholders as well.

As per the above table, a decrease in debt to equity ratio could be observed from 2014

to 2015, followed by an increase in the year 2016 and with an increase in 2017. A ratio with

0.5 or lower is considered to be the optimal situation for capital structure. In this case the

ratio is less than 0.5 for all the years. This implies that the financial leverage of ANZ Bank

has not been that high because it shows that it has shifted its focus on raising more funds

through issue of equity shares in the market.

particulars 2014 2015 2016 2017

Net debt $14,554.00 $11,234.00 $15,645.00 $16,786.00

Net equity $52,134.00 $54,876.00 $53,098.00 $52,314.00

debt to equity ratio 0.28 0.20 0.29 0.32

Debt and equity position of Commonwealth Bank

( Source: Commbank.com.au 2018)

In accordance with the table , it could be noticed that the debt equity ratio has

shown more or less a standard pattern over the four years, except it shows a steep reduction

in debt equity ratio to 0.2 in the year 2014. It is also below the ideal standard below 0.5. This

signifies the organisation relies on equity investments from shareholders.

particulars 2014 2015 2016 2017

Net debt $1,235.00 $1,546.00 $1,337.00 $1,457.00

Net equity $4,876.00 $4,675.00 $4,789.00 $4,700.00

Debt to equity ratio 0.25 0.33 0.28 0.31

Debt and equity position of Bank of Queensland

(Source: Boq.com.au 2018)

The above table shows that although there has been a fluctuation in the debt equity

ratio in the years 2014 to 2018, it is still below the prescribed industry standard of 0.5.This

signifies that the firm raises its finance from equity shareholders as well.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10CORPORATE AND FINANCIAL ACCOUNTING

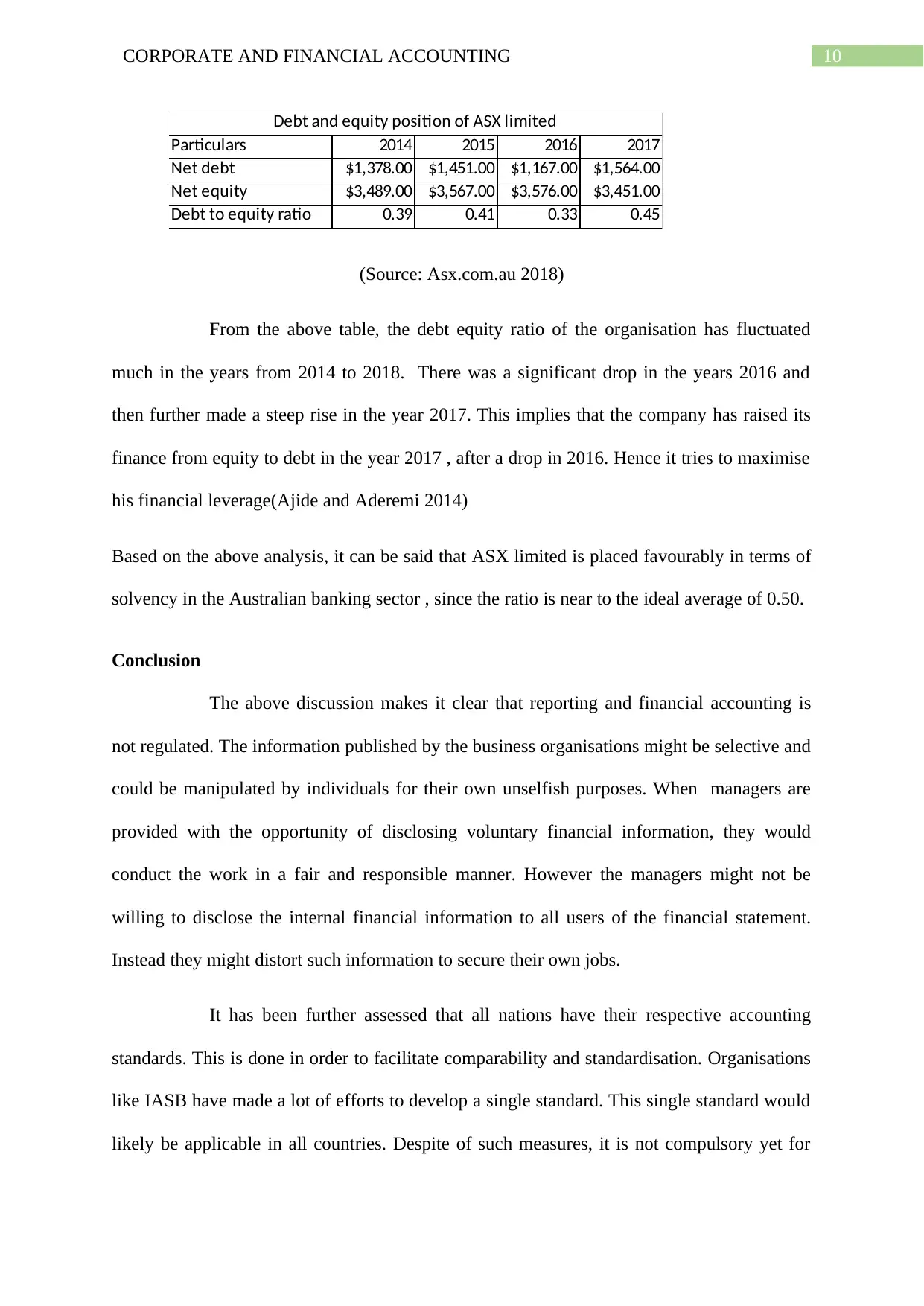

Particulars 2014 2015 2016 2017

Net debt $1,378.00 $1,451.00 $1,167.00 $1,564.00

Net equity $3,489.00 $3,567.00 $3,576.00 $3,451.00

Debt to equity ratio 0.39 0.41 0.33 0.45

Debt and equity position of ASX limited

(Source: Asx.com.au 2018)

From the above table, the debt equity ratio of the organisation has fluctuated

much in the years from 2014 to 2018. There was a significant drop in the years 2016 and

then further made a steep rise in the year 2017. This implies that the company has raised its

finance from equity to debt in the year 2017 , after a drop in 2016. Hence it tries to maximise

his financial leverage(Ajide and Aderemi 2014)

Based on the above analysis, it can be said that ASX limited is placed favourably in terms of

solvency in the Australian banking sector , since the ratio is near to the ideal average of 0.50.

Conclusion

The above discussion makes it clear that reporting and financial accounting is

not regulated. The information published by the business organisations might be selective and

could be manipulated by individuals for their own unselfish purposes. When managers are

provided with the opportunity of disclosing voluntary financial information, they would

conduct the work in a fair and responsible manner. However the managers might not be

willing to disclose the internal financial information to all users of the financial statement.

Instead they might distort such information to secure their own jobs.

It has been further assessed that all nations have their respective accounting

standards. This is done in order to facilitate comparability and standardisation. Organisations

like IASB have made a lot of efforts to develop a single standard. This single standard would

likely be applicable in all countries. Despite of such measures, it is not compulsory yet for

Particulars 2014 2015 2016 2017

Net debt $1,378.00 $1,451.00 $1,167.00 $1,564.00

Net equity $3,489.00 $3,567.00 $3,576.00 $3,451.00

Debt to equity ratio 0.39 0.41 0.33 0.45

Debt and equity position of ASX limited

(Source: Asx.com.au 2018)

From the above table, the debt equity ratio of the organisation has fluctuated

much in the years from 2014 to 2018. There was a significant drop in the years 2016 and

then further made a steep rise in the year 2017. This implies that the company has raised its

finance from equity to debt in the year 2017 , after a drop in 2016. Hence it tries to maximise

his financial leverage(Ajide and Aderemi 2014)

Based on the above analysis, it can be said that ASX limited is placed favourably in terms of

solvency in the Australian banking sector , since the ratio is near to the ideal average of 0.50.

Conclusion

The above discussion makes it clear that reporting and financial accounting is

not regulated. The information published by the business organisations might be selective and

could be manipulated by individuals for their own unselfish purposes. When managers are

provided with the opportunity of disclosing voluntary financial information, they would

conduct the work in a fair and responsible manner. However the managers might not be

willing to disclose the internal financial information to all users of the financial statement.

Instead they might distort such information to secure their own jobs.

It has been further assessed that all nations have their respective accounting

standards. This is done in order to facilitate comparability and standardisation. Organisations

like IASB have made a lot of efforts to develop a single standard. This single standard would

likely be applicable in all countries. Despite of such measures, it is not compulsory yet for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11CORPORATE AND FINANCIAL ACCOUNTING

member nations to converge their own accounting standards with that of IFRS. Finally it is

found that ASX limited is placed in a better position in the Australian banking sector in terms

of its debt and equity.

member nations to converge their own accounting standards with that of IFRS. Finally it is

found that ASX limited is placed in a better position in the Australian banking sector in terms

of its debt and equity.

12CORPORATE AND FINANCIAL ACCOUNTING

References:

Ajide, F.M. and Aderemi, A.A., 2014. The effects of corporate social responsibility activity

disclosure on corporate profitability: Empirical evidence from Nigerian commercial banks.

IOSR Journal of Economics and Finance (IOSRJEF), 2(6), pp.17-25.

Al-Janadi, Y., Rahman, R.A. and Omar, N.H., 2013. Corporate governance mechanisms and

voluntary disclosure in Saudi Arabia. Research Journal of Finance and Accounting, 4(4).

Allegrini, M. and Greco, G., 2013. Corporate boards, audit committees and voluntary

disclosure: Evidence from Italian listed companies. Journal of Management & Governance,

17(1), pp.187-216.

Anz.com. 2018. Annual Report / Annual Review | ANZ Shareholder Centre. [online]

Available at: http://shareholder.anz.com/annual-report-annual-review [Accessed 25 Sep.

2018].

Asx.com.au. 2018. Shareholder report. [online] Available at:

https://www.asx.com.au/about/asx-shareholder-reports.html [Accessed 25 Sep. 2018].

Babalola, Y.A. and Abiola, F.R., 2013. Financial ratio analysis of firms: A tool for decision

making. International journal of management sciences, 1(4), pp.132-137.

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics, 58(2-3), pp.339-383.

Boq.com.au. 2018. Annual Reports | Bank of Queensland. [online] Available at:

https://www.boq.com.au/Shareholder-centre/financial-information/Annual-Report [Accessed

25 Sep. 2018].

Brochet, F., Jagolinzer, A.D. and Riedl, E.J., 2013. Mandatory IFRS adoption and financial

statement comparability. Contemporary Accounting Research, 30(4), pp.1373-1400.

References:

Ajide, F.M. and Aderemi, A.A., 2014. The effects of corporate social responsibility activity

disclosure on corporate profitability: Empirical evidence from Nigerian commercial banks.

IOSR Journal of Economics and Finance (IOSRJEF), 2(6), pp.17-25.

Al-Janadi, Y., Rahman, R.A. and Omar, N.H., 2013. Corporate governance mechanisms and

voluntary disclosure in Saudi Arabia. Research Journal of Finance and Accounting, 4(4).

Allegrini, M. and Greco, G., 2013. Corporate boards, audit committees and voluntary

disclosure: Evidence from Italian listed companies. Journal of Management & Governance,

17(1), pp.187-216.

Anz.com. 2018. Annual Report / Annual Review | ANZ Shareholder Centre. [online]

Available at: http://shareholder.anz.com/annual-report-annual-review [Accessed 25 Sep.

2018].

Asx.com.au. 2018. Shareholder report. [online] Available at:

https://www.asx.com.au/about/asx-shareholder-reports.html [Accessed 25 Sep. 2018].

Babalola, Y.A. and Abiola, F.R., 2013. Financial ratio analysis of firms: A tool for decision

making. International journal of management sciences, 1(4), pp.132-137.

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics, 58(2-3), pp.339-383.

Boq.com.au. 2018. Annual Reports | Bank of Queensland. [online] Available at:

https://www.boq.com.au/Shareholder-centre/financial-information/Annual-Report [Accessed

25 Sep. 2018].

Brochet, F., Jagolinzer, A.D. and Riedl, E.J., 2013. Mandatory IFRS adoption and financial

statement comparability. Contemporary Accounting Research, 30(4), pp.1373-1400.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.