Holmes Institute HA2032: Corporate and Financial Accounting Report

VerifiedAdded on 2023/01/11

|11

|3336

|52

Report

AI Summary

This report provides a comprehensive analysis of BHP Billiton's financial accounting practices. It begins with an executive summary and table of contents, followed by an introduction outlining the importance of financial accounting for corporations. The report delves into the statement of cash flow, identifying items related to the balance sheet, and analyzes BHP Billiton's performance based on Earnings Per Share (EPS), including calculations for the last two years and a discussion of its usefulness as a performance indicator. The report also examines material movements in the statement of changes in equity, items recorded as non-current liabilities, and potential advantages and disadvantages of different capital sources within the company's capital structure. Furthermore, the report researches and discusses the disclosure requirements for publicly listed companies compared to non-listed companies, culminating in a conclusion and references. The analysis covers key financial aspects such as cash flow, EPS, equity changes, and non-current liabilities, providing a detailed overview of BHP Billiton's financial health and strategic decision-making.

Corporate and

Financial accounting

Financial accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Present report is based upon the analysis of financial accounting for corporations such as

BHP Billiton. This assignment summarises different concepts such as elements of cash flow,

importance of EPS, movement in elements of statement of changes in equities, discussion of

non-current liabilities etc. The company is recommended to disclose its final accounts every year

so that it can meet expectation of internal as well as external stakeholders.

Present report is based upon the analysis of financial accounting for corporations such as

BHP Billiton. This assignment summarises different concepts such as elements of cash flow,

importance of EPS, movement in elements of statement of changes in equities, discussion of

non-current liabilities etc. The company is recommended to disclose its final accounts every year

so that it can meet expectation of internal as well as external stakeholders.

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................2

Table of Contents.............................................................................................................................3

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

1. Discussion and analysis of the items of statement of cash flow and identification of the

items which are related to balance sheet......................................................................................1

2. Explanation of the company’s performance according to EPS and calculation of EPS for last

two years......................................................................................................................................2

3. Discussion of whether EPS is useful performance indicator for the company or not.............3

4. Explanation of the way in which material movement in the statement of changes in equity is

reflected and reported in the statement of cash flows..................................................................3

5. Discussion of the items which are recorded as non-current liabilities, including the related

notes and providing explanation of material movement of each item.........................................4

6. Discussion of potential advantages and disadvantages of each source of capital according to

the capital structure of the company............................................................................................5

PART B...........................................................................................................................................6

Research and discussion of the disclosure requirements for publicly listed companies in the

financial statements in comparison to other non-listed companies.............................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

EXECUTIVE SUMMARY.............................................................................................................2

Table of Contents.............................................................................................................................3

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

1. Discussion and analysis of the items of statement of cash flow and identification of the

items which are related to balance sheet......................................................................................1

2. Explanation of the company’s performance according to EPS and calculation of EPS for last

two years......................................................................................................................................2

3. Discussion of whether EPS is useful performance indicator for the company or not.............3

4. Explanation of the way in which material movement in the statement of changes in equity is

reflected and reported in the statement of cash flows..................................................................3

5. Discussion of the items which are recorded as non-current liabilities, including the related

notes and providing explanation of material movement of each item.........................................4

6. Discussion of potential advantages and disadvantages of each source of capital according to

the capital structure of the company............................................................................................5

PART B...........................................................................................................................................6

Research and discussion of the disclosure requirements for publicly listed companies in the

financial statements in comparison to other non-listed companies.............................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting can be defined as the procedure which is followed by most of the

entities for the purpose of generating final accounts so that actual performance and market

position of business could be determined. Almost all the corporations are focused with it as it

guides them to formulate effective and strategic decisions for future so that desired targets could

be achieved successfully. If an enterprise is not able to make sure that are its financial statements

are not having accurate figures then it may leave negative impact upon execution of business as

it will affect interest of stakeholders in business (Caires, 2018). Main aim of this report is to

enhance understanding of financial accounting for companies so that they can meet the long-term

business goals. For this purpose, the entity which is selected for the assignment is BHP Billiton.

It is a mining, petroleum and metal company which is listed on Australian Stock Exchange. It is

having headquarter in Melbourne, Australia and founded in year 1885. This project covers

various topics such as discussion of items of cash flow statement, calculation of EPS and

discussion of its usefulness, analysis of material movement in cash flow and other items.

Additionally, research and discussion of disclosure requirements for publicly listed companies in

the financial statements in comparison to non-listed companies are also covered in this

assignment.

PART A

1. Discussion and analysis of the items of statement of cash flow and identification of the

items which are related to balance sheet

Cash flow statement is generated by all the companies on yearly basis so that they can

analyse the liquidity and liquid strength of business. Main purpose of generating it, is to analyse

that the organisation is having sufficient funds to meet long term business goals or not. From the

cash flow statement of BHP Billiton it has been identified that total cash generation from

operations for year was 23428, total cash flow from operating activities was 17871. Apart from

this, the total capital and exploration expenses were 7123 for the same year. Net cash inflow

from investing activities for the company is 2607 and for financing activities it is 20528 in

negative. At the end of the year there was a decrement of 10477 in the cash and cash equivalents

(Annual report of BHP Billiton, 2019).

1

Financial accounting can be defined as the procedure which is followed by most of the

entities for the purpose of generating final accounts so that actual performance and market

position of business could be determined. Almost all the corporations are focused with it as it

guides them to formulate effective and strategic decisions for future so that desired targets could

be achieved successfully. If an enterprise is not able to make sure that are its financial statements

are not having accurate figures then it may leave negative impact upon execution of business as

it will affect interest of stakeholders in business (Caires, 2018). Main aim of this report is to

enhance understanding of financial accounting for companies so that they can meet the long-term

business goals. For this purpose, the entity which is selected for the assignment is BHP Billiton.

It is a mining, petroleum and metal company which is listed on Australian Stock Exchange. It is

having headquarter in Melbourne, Australia and founded in year 1885. This project covers

various topics such as discussion of items of cash flow statement, calculation of EPS and

discussion of its usefulness, analysis of material movement in cash flow and other items.

Additionally, research and discussion of disclosure requirements for publicly listed companies in

the financial statements in comparison to non-listed companies are also covered in this

assignment.

PART A

1. Discussion and analysis of the items of statement of cash flow and identification of the

items which are related to balance sheet

Cash flow statement is generated by all the companies on yearly basis so that they can

analyse the liquidity and liquid strength of business. Main purpose of generating it, is to analyse

that the organisation is having sufficient funds to meet long term business goals or not. From the

cash flow statement of BHP Billiton it has been identified that total cash generation from

operations for year was 23428, total cash flow from operating activities was 17871. Apart from

this, the total capital and exploration expenses were 7123 for the same year. Net cash inflow

from investing activities for the company is 2607 and for financing activities it is 20528 in

negative. At the end of the year there was a decrement of 10477 in the cash and cash equivalents

(Annual report of BHP Billiton, 2019).

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From the cash flow of the company it has also been identified that there are various items

which are related to balance sheet. All of them are as follows:

Purchase of property, plant and equipment: During the year 2019 the organisation

have purchased fixed assets of 6250.

Investment and funding of equity accounted investments: In year 2019 the

organisation made investment and funding in equities which is around 630 dollars.

Payment of interest-bearing liabilities: In 2019 BHP repaid some of the interest-

bearing liabilities and cost of it was 2514.

Share buyback: In 2019 BHP Billiton bought its own shares of 5220 dollars and it was

recorded in the financing activities of year 2019.

All the above described items are shows in cash flow statement of the organisation but they

are related to balance sheet of the enterprise.

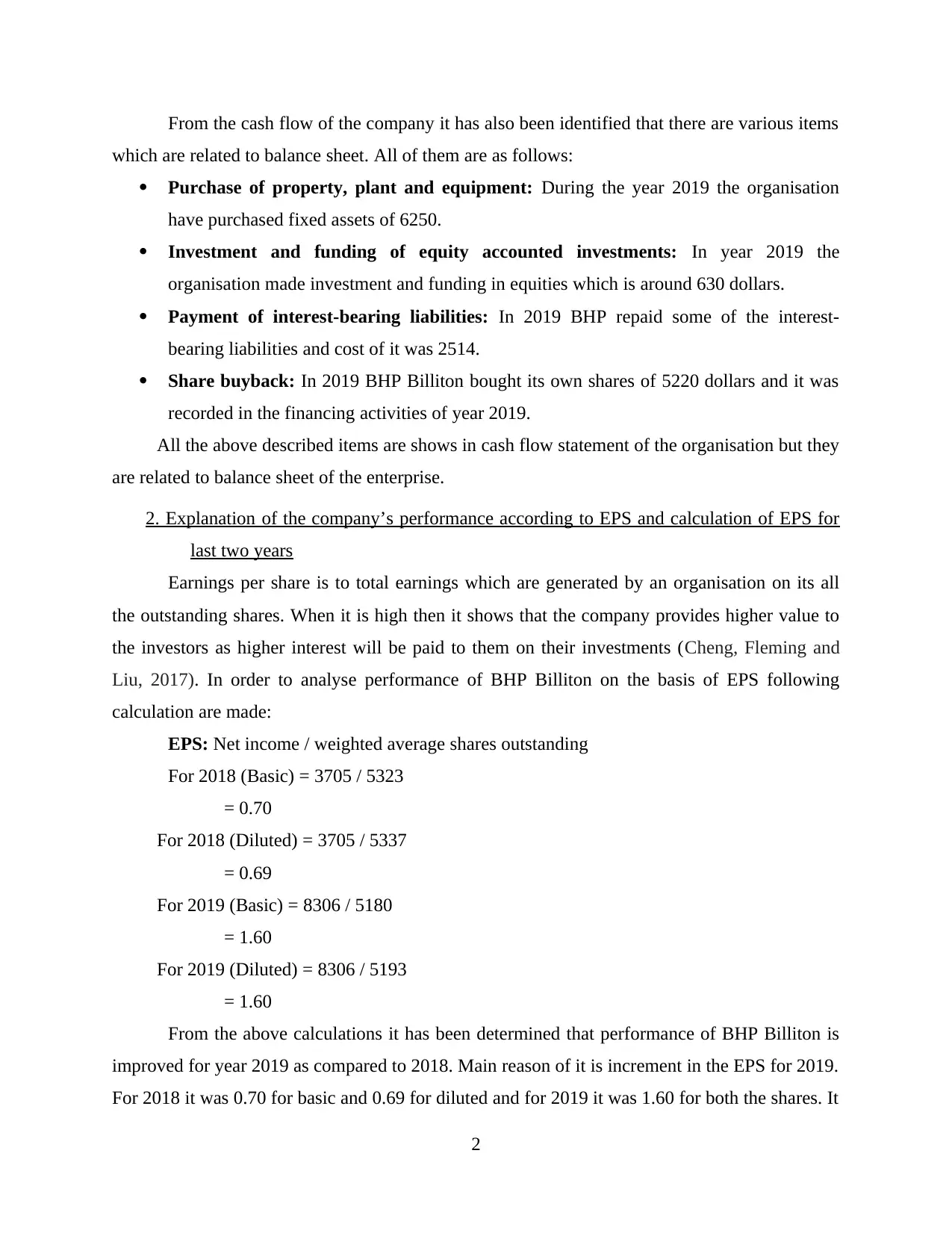

2. Explanation of the company’s performance according to EPS and calculation of EPS for

last two years

Earnings per share is to total earnings which are generated by an organisation on its all

the outstanding shares. When it is high then it shows that the company provides higher value to

the investors as higher interest will be paid to them on their investments (Cheng, Fleming and

Liu, 2017). In order to analyse performance of BHP Billiton on the basis of EPS following

calculation are made:

EPS: Net income / weighted average shares outstanding

For 2018 (Basic) = 3705 / 5323

= 0.70

For 2018 (Diluted) = 3705 / 5337

= 0.69

For 2019 (Basic) = 8306 / 5180

= 1.60

For 2019 (Diluted) = 8306 / 5193

= 1.60

From the above calculations it has been determined that performance of BHP Billiton is

improved for year 2019 as compared to 2018. Main reason of it is increment in the EPS for 2019.

For 2018 it was 0.70 for basic and 0.69 for diluted and for 2019 it was 1.60 for both the shares. It

2

which are related to balance sheet. All of them are as follows:

Purchase of property, plant and equipment: During the year 2019 the organisation

have purchased fixed assets of 6250.

Investment and funding of equity accounted investments: In year 2019 the

organisation made investment and funding in equities which is around 630 dollars.

Payment of interest-bearing liabilities: In 2019 BHP repaid some of the interest-

bearing liabilities and cost of it was 2514.

Share buyback: In 2019 BHP Billiton bought its own shares of 5220 dollars and it was

recorded in the financing activities of year 2019.

All the above described items are shows in cash flow statement of the organisation but they

are related to balance sheet of the enterprise.

2. Explanation of the company’s performance according to EPS and calculation of EPS for

last two years

Earnings per share is to total earnings which are generated by an organisation on its all

the outstanding shares. When it is high then it shows that the company provides higher value to

the investors as higher interest will be paid to them on their investments (Cheng, Fleming and

Liu, 2017). In order to analyse performance of BHP Billiton on the basis of EPS following

calculation are made:

EPS: Net income / weighted average shares outstanding

For 2018 (Basic) = 3705 / 5323

= 0.70

For 2018 (Diluted) = 3705 / 5337

= 0.69

For 2019 (Basic) = 8306 / 5180

= 1.60

For 2019 (Diluted) = 8306 / 5193

= 1.60

From the above calculations it has been determined that performance of BHP Billiton is

improved for year 2019 as compared to 2018. Main reason of it is increment in the EPS for 2019.

For 2018 it was 0.70 for basic and 0.69 for diluted and for 2019 it was 1.60 for both the shares. It

2

shows that in 2019 the organisation will provide more value to the investors and they will get

higher returns on their investment as the profit for the year are very high. As the EPS for BHP is

increased for 2019 so it shows that company is a good condition and able to meet expectations of

all the stakeholders whether they are investors or shareholders (Chittenden, 2018).

3. Discussion of whether EPS is useful performance indicator for the company or not

Earnings per share can be defined as the monetary value of the earnings on all the

outstanding shares of the common stock of organisation. With the help of it, all the investors can

determine the company will be able to provide them higher returns for the investment or not. If it

is increased in current year as compared to the last year then it shows that higher returns will be

offered to investors as the profit of the enterprise are enhanced. On the other hand, if the EPS is

following the declining trend then potential investors will not show interest in the business

because there is huge risk for them because in this situation the entity may become insolvent. For

all the companies such as BHP Billiton it is very useful performance indicator as it helps to

analyse that the company is able to provide more value to the investors or not. It can also guide

the top-level executives of organisations to analyse that their business is progressive or not. It is

one of the main performance indicators which are used by enterprises to analyse performance of

business and formulate effective decisions for future. As it helps the managers to provide more

value to the investors so it is definitely a useful indicator for BHP Billiton (Guo, 2018).

4. Explanation of the way in which material movement in the statement of changes in equity

is reflected and reported in the statement of cash flows

From the statement of changes in equity of BHP Billiton it has been determined that

various changes have taken pace during year 2019. At the beginning of the year the enterprise

was having total equities of 60670 and the impact of adopting IFRS was (7), so the total opening

balance of it as on 1 July 2018 was 60663. At the end of the year the total equities for the

organisation were 51824 which shows that various changes are being made by the company in

the equities. Total comprehensive income for the year according to changes in equity statement

was 9160. Purchase of shares for the year was 188, accrued employee entitlement for the year

was 138 and dividends for the year were around 12507. The value of buyback shares according

to the statement is 5274 and divestment of subsidiaries is showing a negative balance of 168.

There are various changes are reflected in the cash flow statement. The shares purchased

by the enterprise by ESOP Trusts were shown as other financing activities. In Cash flow

3

higher returns on their investment as the profit for the year are very high. As the EPS for BHP is

increased for 2019 so it shows that company is a good condition and able to meet expectations of

all the stakeholders whether they are investors or shareholders (Chittenden, 2018).

3. Discussion of whether EPS is useful performance indicator for the company or not

Earnings per share can be defined as the monetary value of the earnings on all the

outstanding shares of the common stock of organisation. With the help of it, all the investors can

determine the company will be able to provide them higher returns for the investment or not. If it

is increased in current year as compared to the last year then it shows that higher returns will be

offered to investors as the profit of the enterprise are enhanced. On the other hand, if the EPS is

following the declining trend then potential investors will not show interest in the business

because there is huge risk for them because in this situation the entity may become insolvent. For

all the companies such as BHP Billiton it is very useful performance indicator as it helps to

analyse that the company is able to provide more value to the investors or not. It can also guide

the top-level executives of organisations to analyse that their business is progressive or not. It is

one of the main performance indicators which are used by enterprises to analyse performance of

business and formulate effective decisions for future. As it helps the managers to provide more

value to the investors so it is definitely a useful indicator for BHP Billiton (Guo, 2018).

4. Explanation of the way in which material movement in the statement of changes in equity

is reflected and reported in the statement of cash flows

From the statement of changes in equity of BHP Billiton it has been determined that

various changes have taken pace during year 2019. At the beginning of the year the enterprise

was having total equities of 60670 and the impact of adopting IFRS was (7), so the total opening

balance of it as on 1 July 2018 was 60663. At the end of the year the total equities for the

organisation were 51824 which shows that various changes are being made by the company in

the equities. Total comprehensive income for the year according to changes in equity statement

was 9160. Purchase of shares for the year was 188, accrued employee entitlement for the year

was 138 and dividends for the year were around 12507. The value of buyback shares according

to the statement is 5274 and divestment of subsidiaries is showing a negative balance of 168.

There are various changes are reflected in the cash flow statement. The shares purchased

by the enterprise by ESOP Trusts were shown as other financing activities. In Cash flow

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

statement the value of buy-back shares is 5220 but in statement of changes in equities it is

showing 5274. Apart from this total dividend paid which is reflected in the cash flow is 12593

(11395+1198) and in statement of equity it is showing 12507. Some of the values are changed

while reflecting in cash flow statement (Hubbard and Moore, 2017).

5. Discussion of the items which are recorded as non-current liabilities, including the related

notes and providing explanation of material movement of each item

Non-current liabilities are such obligation which are having more than one-year time

period to pay. From the balance sheet of BHP Billiton it has been analysed that different items

are shows as non-current liabilities. These are trade and other payables which were 3 for 2018

and increased up to 5 for 2019. From the note 9 it has been determined that total payables were

around 6722 and 5980 for 2019 and 2018 respectively and 6717 and 5977 were having current

nature so the balance is considered as non-current payables (Paynter, Halabi and Tuck, 2019).

Another item in the non-current liabilities of BHP is interest bearing liabilities. For 2018

it was 24069 and in 2019 it was decreased upon to 23167. From the note 19 which is related to it,

it has been determined that interest bearing liabilities include, bank loan, notes and debentures,

finance leases and other liabilities.

Other financial liabilities are also reflected in the balance sheet under non-current

liabilities of BHP Billiton. The value of it for 2018 was 1093 and for 2019 it was 896. In order to

understand the changes of it note 21 is generated which is mainly related to financial risk

management. As the financial liabilities may result in risks for business so all the adjustments of

them are made under this note. Non-current tax payable is also shown in the liabilities and the

values of it for 2018 and 2019 were 137 and 187 respectively. No notes are generated in context

to this element of the final accounts.

Deferred tax liabilities are also related to non-current liabilities of the company for 2018

it was 3472 and in 2019 the value of it was decreased up to 3234. From the note 13 it has been

analysed that the value of the tax covers number of various elements which are depreciation,

resource rent tax, deferred charges, investments that include foreign tax credits and other

liabilities. Some of the elements were deducted from the cost of all of them which are employee

benefit, closure and rehabilitation, other provisions, deferred income, foreign exchange gains etc.

Deferred incomes are also part of non-current liabilities and the total value of it for 2018

is 337 which is decreased up to 281 for 2019. There is no specific note generated for this element

4

showing 5274. Apart from this total dividend paid which is reflected in the cash flow is 12593

(11395+1198) and in statement of equity it is showing 12507. Some of the values are changed

while reflecting in cash flow statement (Hubbard and Moore, 2017).

5. Discussion of the items which are recorded as non-current liabilities, including the related

notes and providing explanation of material movement of each item

Non-current liabilities are such obligation which are having more than one-year time

period to pay. From the balance sheet of BHP Billiton it has been analysed that different items

are shows as non-current liabilities. These are trade and other payables which were 3 for 2018

and increased up to 5 for 2019. From the note 9 it has been determined that total payables were

around 6722 and 5980 for 2019 and 2018 respectively and 6717 and 5977 were having current

nature so the balance is considered as non-current payables (Paynter, Halabi and Tuck, 2019).

Another item in the non-current liabilities of BHP is interest bearing liabilities. For 2018

it was 24069 and in 2019 it was decreased upon to 23167. From the note 19 which is related to it,

it has been determined that interest bearing liabilities include, bank loan, notes and debentures,

finance leases and other liabilities.

Other financial liabilities are also reflected in the balance sheet under non-current

liabilities of BHP Billiton. The value of it for 2018 was 1093 and for 2019 it was 896. In order to

understand the changes of it note 21 is generated which is mainly related to financial risk

management. As the financial liabilities may result in risks for business so all the adjustments of

them are made under this note. Non-current tax payable is also shown in the liabilities and the

values of it for 2018 and 2019 were 137 and 187 respectively. No notes are generated in context

to this element of the final accounts.

Deferred tax liabilities are also related to non-current liabilities of the company for 2018

it was 3472 and in 2019 the value of it was decreased up to 3234. From the note 13 it has been

analysed that the value of the tax covers number of various elements which are depreciation,

resource rent tax, deferred charges, investments that include foreign tax credits and other

liabilities. Some of the elements were deducted from the cost of all of them which are employee

benefit, closure and rehabilitation, other provisions, deferred income, foreign exchange gains etc.

Deferred incomes are also part of non-current liabilities and the total value of it for 2018

is 337 which is decreased up to 281 for 2019. There is no specific note generated for this element

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of liabilities. The last non-current liability is provision and the value of it is increased up to 8928

in 2019. In 2018 its value was 8223. There are several notes are generated for this element which

are 4, 14, 18 and 24. From these notes, it has been determined that organisation create provision

for dealing with uncertainties in future (Paynter, Halabi and Tuck, 2019).

6. Discussion of potential advantages and disadvantages of each source of capital according

to the capital structure of the company

From the annual report of BHP Billiton it has been analysed that the capital structure of

the company is having various source of capital. All of them are as follows:

Share capital: Total share capital of the organisation for year 2019 is around 2168. It is

the combination of shares in BHP Group Limited and BHP Group Plc. It is the total funding of

shareholders which is used by the company to perform all the operations properly. The main

advantage of it for the organisation is that the management does not have to be worried about

the interest which is required to be paid on debts. Disadvantages of share capital are dividend

uncertainty, high level of risk, fluctuation in market price etc.

Reserves: Balance sheet of BHP Billiton is showing reserves of 2285 for 2019 and these

are kept by the organisations to deal with negative events that may take place in future. The main

advantage of it is that if the company is not able to generate good profits in a year then the

reserved amount could be used to meet all the monetary requirements (Shao, 2017).

Disadvantage of reserve is that, preparation of them may lead the organisation towards changes

in the supply of monetary resources.

Retained earnings: These are the funds which are retained by the organisation by

ignoring the dividends of shareholders. For 2019 total retained earnings were around 42819.

Advantage of it for a business is that it could be used to fund the future operations if the entity is

not having proper investments. Disadvantage of it for a business is lower engagement of

shareholders in business because the amount of it is the dividend of them for which they

provided funds to the organisation.

5

in 2019. In 2018 its value was 8223. There are several notes are generated for this element which

are 4, 14, 18 and 24. From these notes, it has been determined that organisation create provision

for dealing with uncertainties in future (Paynter, Halabi and Tuck, 2019).

6. Discussion of potential advantages and disadvantages of each source of capital according

to the capital structure of the company

From the annual report of BHP Billiton it has been analysed that the capital structure of

the company is having various source of capital. All of them are as follows:

Share capital: Total share capital of the organisation for year 2019 is around 2168. It is

the combination of shares in BHP Group Limited and BHP Group Plc. It is the total funding of

shareholders which is used by the company to perform all the operations properly. The main

advantage of it for the organisation is that the management does not have to be worried about

the interest which is required to be paid on debts. Disadvantages of share capital are dividend

uncertainty, high level of risk, fluctuation in market price etc.

Reserves: Balance sheet of BHP Billiton is showing reserves of 2285 for 2019 and these

are kept by the organisations to deal with negative events that may take place in future. The main

advantage of it is that if the company is not able to generate good profits in a year then the

reserved amount could be used to meet all the monetary requirements (Shao, 2017).

Disadvantage of reserve is that, preparation of them may lead the organisation towards changes

in the supply of monetary resources.

Retained earnings: These are the funds which are retained by the organisation by

ignoring the dividends of shareholders. For 2019 total retained earnings were around 42819.

Advantage of it for a business is that it could be used to fund the future operations if the entity is

not having proper investments. Disadvantage of it for a business is lower engagement of

shareholders in business because the amount of it is the dividend of them for which they

provided funds to the organisation.

5

PART B

Research and discussion of the disclosure requirements for publicly listed companies in the

financial statements in comparison to other non-listed companies

According to SEC all the public listed companies are required to issue two different

disclosure related annual report. On of them is for SEC and another one of the shareholders. If

the company is not listed then there is no compulsion of releasing the disclosure reports as it

does not have to comply with the regulations of SEC (Stadler and Nobes, 2018).

The guidelines which are set by SEC for all the companies states that all the records that

will be presented in the disclosure report should be updated and have detailed as well as accurate

information. For listed companies it is compulsory as public invests their monetary resources in

businesses and they have right to analyse the performance of the entity in which they have

invested their money. If SEC finds any type of mistake in the report then legal action could be

taken against the business because it will be treated as legal offence. If the company is not listed

then it is not having any type of compulsion to disclose its annual report or any other type of

records as public is not investing money in it.

If an entity which is publicly listed is sharing its disclosure report with public,

shreaholders as well as SEC then it may acquire different types of benefits. Some of the are listed

below:

When the company will disclose its reports for public then it may result in attraction of

new investors who will analyse the annual report and evaluate the interest rate which

could be acquired by them in future.

By disclosing report, the entities will be able to facilitate the external users to make

effective decisions such as providing credit, supplying goods etc.

When the records will be disclosed to shareholders then it will help the entity to retain

their interest in business as they will get satisfied with the performance if accurate results

will be shown to them (Trotman and Carson, 2018).

If accurate reports will be disclosed to SEC then it can also benefit a business to establish

positive market image and ignore the legal actions.

6

Research and discussion of the disclosure requirements for publicly listed companies in the

financial statements in comparison to other non-listed companies

According to SEC all the public listed companies are required to issue two different

disclosure related annual report. On of them is for SEC and another one of the shareholders. If

the company is not listed then there is no compulsion of releasing the disclosure reports as it

does not have to comply with the regulations of SEC (Stadler and Nobes, 2018).

The guidelines which are set by SEC for all the companies states that all the records that

will be presented in the disclosure report should be updated and have detailed as well as accurate

information. For listed companies it is compulsory as public invests their monetary resources in

businesses and they have right to analyse the performance of the entity in which they have

invested their money. If SEC finds any type of mistake in the report then legal action could be

taken against the business because it will be treated as legal offence. If the company is not listed

then it is not having any type of compulsion to disclose its annual report or any other type of

records as public is not investing money in it.

If an entity which is publicly listed is sharing its disclosure report with public,

shreaholders as well as SEC then it may acquire different types of benefits. Some of the are listed

below:

When the company will disclose its reports for public then it may result in attraction of

new investors who will analyse the annual report and evaluate the interest rate which

could be acquired by them in future.

By disclosing report, the entities will be able to facilitate the external users to make

effective decisions such as providing credit, supplying goods etc.

When the records will be disclosed to shareholders then it will help the entity to retain

their interest in business as they will get satisfied with the performance if accurate results

will be shown to them (Trotman and Carson, 2018).

If accurate reports will be disclosed to SEC then it can also benefit a business to establish

positive market image and ignore the legal actions.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONCLUSION

From the above project report it has been concluded that financial accounting is a process

which is required to be followed by all the companies to create financial statements. There are

various types of items which are reflected in cash flow and related to balance sheet. These are

purchase of asset, repayment of loans etc. EPS is one of the main performance indicators which

can help to analyse performance of business. For all the public listed companies it is compulsory

to disclose the reports so that future activities could be performed properly.

7

From the above project report it has been concluded that financial accounting is a process

which is required to be followed by all the companies to create financial statements. There are

various types of items which are reflected in cash flow and related to balance sheet. These are

purchase of asset, repayment of loans etc. EPS is one of the main performance indicators which

can help to analyse performance of business. For all the public listed companies it is compulsory

to disclose the reports so that future activities could be performed properly.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Caires, P. F. H., 2018. Equity research: BHP Billiton Ltd (Doctoral dissertation, Instituto

Superior de Economia e Gestão).

Cheng, Z., Fleming, G. and Liu, Z., 2017. Financial constraints and investment thirst in Chinese

reverse merger companies. Accounting & Finance. 57(5). pp.1315-1347.

Chittenden, R., 2018. An investigation into the ability of non-IFRS earnings measures' to predict

future operating cash flows for a sample of South African JSE listed

companies (Doctoral dissertation, University of Cape Town).

Guo, Q., 2018. Rhetoric in financial reporting: evaluation of ISA 720.

Hubbard, T. N. and Moore, M. J., 2017. Bhp billiton: Mining potash. Kellogg School of

Management Cases.

Paynter, M., Halabi, A. and Tuck, J., 2019. Storytelling and Corporate Social Responsibility

Reporting: A Review of BHP 1992–2017. In The Components of Sustainable

Development (pp. 205-230). Springer, Singapore.

Paynter, M., Halabi, A. and Tuck, J., 2019. Storytelling and Corporate Social Responsibility

Reporting: A Review. The Components of Sustainable Development: Engagement and

Partnership, p.205.

Shao, Y., 2017. Accounting for the Right to Water: The Great Artesian Basin and Olympic Dam

Mine.

Stadler, C. and Nobes, C. W., 2018. Accounting for government grants: Standard-setting and

accounting choice. Journal of Accounting and Public Policy. 37(2). pp.113-129.

Trotman, K. and Carson, E., 2018. Financial accounting: an integrated approach. Cengage AU.

Online

Annual report of BHP Billiton. 2019. [Online]. Available through:

<https://www.bhp.com/-/media/documents/investors/annual-reports/2019/

bhpannualreport2019.pdf>

8

Books and Journals:

Caires, P. F. H., 2018. Equity research: BHP Billiton Ltd (Doctoral dissertation, Instituto

Superior de Economia e Gestão).

Cheng, Z., Fleming, G. and Liu, Z., 2017. Financial constraints and investment thirst in Chinese

reverse merger companies. Accounting & Finance. 57(5). pp.1315-1347.

Chittenden, R., 2018. An investigation into the ability of non-IFRS earnings measures' to predict

future operating cash flows for a sample of South African JSE listed

companies (Doctoral dissertation, University of Cape Town).

Guo, Q., 2018. Rhetoric in financial reporting: evaluation of ISA 720.

Hubbard, T. N. and Moore, M. J., 2017. Bhp billiton: Mining potash. Kellogg School of

Management Cases.

Paynter, M., Halabi, A. and Tuck, J., 2019. Storytelling and Corporate Social Responsibility

Reporting: A Review of BHP 1992–2017. In The Components of Sustainable

Development (pp. 205-230). Springer, Singapore.

Paynter, M., Halabi, A. and Tuck, J., 2019. Storytelling and Corporate Social Responsibility

Reporting: A Review. The Components of Sustainable Development: Engagement and

Partnership, p.205.

Shao, Y., 2017. Accounting for the Right to Water: The Great Artesian Basin and Olympic Dam

Mine.

Stadler, C. and Nobes, C. W., 2018. Accounting for government grants: Standard-setting and

accounting choice. Journal of Accounting and Public Policy. 37(2). pp.113-129.

Trotman, K. and Carson, E., 2018. Financial accounting: an integrated approach. Cengage AU.

Online

Annual report of BHP Billiton. 2019. [Online]. Available through:

<https://www.bhp.com/-/media/documents/investors/annual-reports/2019/

bhpannualreport2019.pdf>

8

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.