HA2032 Corporate and Financial Accounting Report: Company Analysis

VerifiedAdded on 2022/10/01

|15

|3565

|45

Report

AI Summary

This report presents a financial analysis of two Australian Stock Exchange (ASX)-listed companies in the energy sector: Whitehaven Coal Limited and Caltex Australia. The analysis focuses on their financial performance, particularly profitability, solvency, and the management of financing activities and investments. The report delves into the recording of items under owner's equity, including issued capital, treasury stock, reserves, and retained earnings, as well as the components of liabilities, both current and non-current. It compares the equity structures and liability profiles of both companies, highlighting the advantages and disadvantages of debt and equity financing. The report examines the sources of funds employed by each company, with Whitehaven Coal primarily using equity and Caltex Australia relying more on debt. The report also discusses the implications of these financial choices, including the impact on cash flow, credit ratings, and overall financial risk, providing a comprehensive overview of corporate and financial accounting practices and their strategic implications.

CORPORATE AND FINANCIAL

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Abstract

This report brings out an evaluative matter with the help of financial analysis of two huge

corporations that are listed on ASX in the energy sector of Australia. The chosen

organisations are Whiterhaven coal limited and Caltex Australia. The annual reports of both

organisations signify analyses of profitability, which indicates that Whitehaven limited has

been performing better as compared to Caltex in several aspects including solvency because

Catlex is holding 51 percent of debt in the total capital structure whereas, Whitehaven has

been holding 17 percent of total capital structure and management of financing activities and

investment.

This report brings out an evaluative matter with the help of financial analysis of two huge

corporations that are listed on ASX in the energy sector of Australia. The chosen

organisations are Whiterhaven coal limited and Caltex Australia. The annual reports of both

organisations signify analyses of profitability, which indicates that Whitehaven limited has

been performing better as compared to Caltex in several aspects including solvency because

Catlex is holding 51 percent of debt in the total capital structure whereas, Whitehaven has

been holding 17 percent of total capital structure and management of financing activities and

investment.

Contents

Abstract......................................................................................................................................1

Introduction................................................................................................................................3

Recording of items under “owner equity”.................................................................................4

Explanation of understanding of each equity section................................................................5

Items under liabilities section.....................................................................................................6

Explanation and understanding of each liability item................................................................8

Advantages and disadvantages of every source of fund, which is selected by the company....9

Conclusion................................................................................................................................11

References................................................................................................................................13

Abstract......................................................................................................................................1

Introduction................................................................................................................................3

Recording of items under “owner equity”.................................................................................4

Explanation of understanding of each equity section................................................................5

Items under liabilities section.....................................................................................................6

Explanation and understanding of each liability item................................................................8

Advantages and disadvantages of every source of fund, which is selected by the company....9

Conclusion................................................................................................................................11

References................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

This report covers elaboration of owner`s equity and its every item accomplished in the

equity section. Further, it covers items of liabilities with clear understanding of its

movements. There is a description of pros and cons of every source of fund decided to invest

in the company. For the second part, there is a critical examination of the concept of small or

large company. This implies the application of three types of organisations in terms of

compliances and the required reporting.

The purpose of the report is to foresee the listed organisations of Australian securities

exchange. While analysing the financial performance of Whitehaven coal limited and Caltex

Australia. The selection is based on same industry, which allow the performance analysis of

both companies on same grounds.

Caltex Australia is among the leading manufacturers and suppliers of several petroleum

products all-over the Australia. The organisation exports varied products to New Zealand and

Singapore. The company is operating since 1900 and it is being headquartered in Sydney.

The company is operating in two major segments such as lytton segment and supply

marketing segment. The main segment deals in selling function of the Caltex products named

as lubricant, fuels, liquefied petroleum gas, diesel oils and many more. Whereas, Lytton

undertakes refining of crude oil in order to convert thr same into the diesel oil and, many

other petroleum products.

Whitehaven involves in development of business in regards to coal mines in Australia, which

is leading Australian corporation. The organisation operating in 1999, which is supplying

coal products to several domestic units and also to the other countries at international level

such as China, Korea, Vietnam, Malaysia, Indonesia, Japan, Taiwan, and Chile (Whitehaven

Coal, 2018b). The company has its two operational segments such as underground operations

This report covers elaboration of owner`s equity and its every item accomplished in the

equity section. Further, it covers items of liabilities with clear understanding of its

movements. There is a description of pros and cons of every source of fund decided to invest

in the company. For the second part, there is a critical examination of the concept of small or

large company. This implies the application of three types of organisations in terms of

compliances and the required reporting.

The purpose of the report is to foresee the listed organisations of Australian securities

exchange. While analysing the financial performance of Whitehaven coal limited and Caltex

Australia. The selection is based on same industry, which allow the performance analysis of

both companies on same grounds.

Caltex Australia is among the leading manufacturers and suppliers of several petroleum

products all-over the Australia. The organisation exports varied products to New Zealand and

Singapore. The company is operating since 1900 and it is being headquartered in Sydney.

The company is operating in two major segments such as lytton segment and supply

marketing segment. The main segment deals in selling function of the Caltex products named

as lubricant, fuels, liquefied petroleum gas, diesel oils and many more. Whereas, Lytton

undertakes refining of crude oil in order to convert thr same into the diesel oil and, many

other petroleum products.

Whitehaven involves in development of business in regards to coal mines in Australia, which

is leading Australian corporation. The organisation operating in 1999, which is supplying

coal products to several domestic units and also to the other countries at international level

such as China, Korea, Vietnam, Malaysia, Indonesia, Japan, Taiwan, and Chile (Whitehaven

Coal, 2018b). The company has its two operational segments such as underground operations

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and cut operations. The organisation has six branches in North Western wales. It offers

thermal and metallurgical coal products (Whitehaven Coal, 2018b).

The major financial aspects covered in the first section include equity structure, liabilities

items, and selection of investment in terms of debt and equity for 2018 for both the

companies.

Part-A

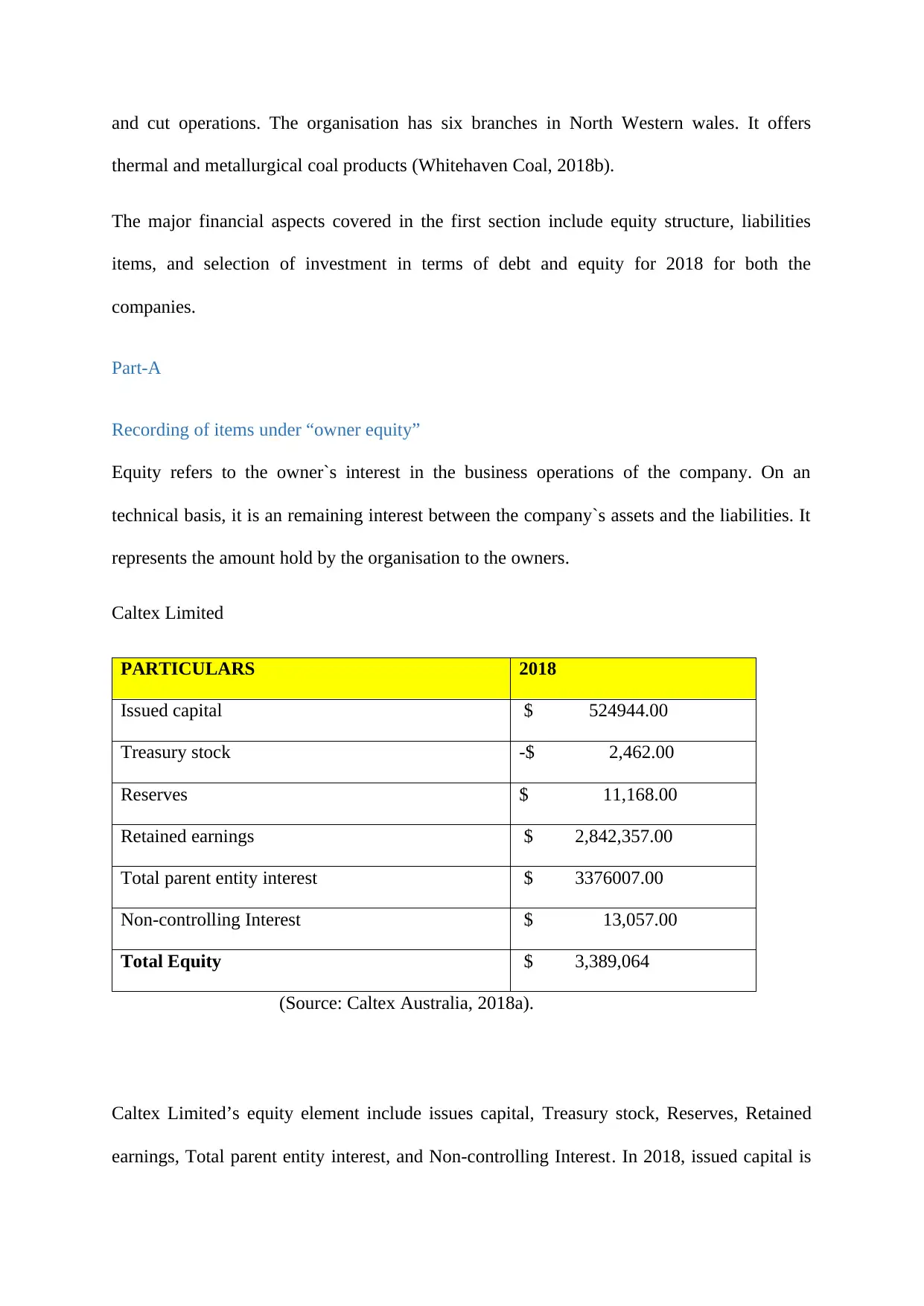

Recording of items under “owner equity”

Equity refers to the owner`s interest in the business operations of the company. On an

technical basis, it is an remaining interest between the company`s assets and the liabilities. It

represents the amount hold by the organisation to the owners.

Caltex Limited

PARTICULARS 2018

Issued capital $ 524944.00

Treasury stock -$ 2,462.00

Reserves $ 11,168.00

Retained earnings $ 2,842,357.00

Total parent entity interest $ 3376007.00

Non-controlling Interest $ 13,057.00

Total Equity $ 3,389,064

(Source: Caltex Australia, 2018a).

Caltex Limited’s equity element include issues capital, Treasury stock, Reserves, Retained

earnings, Total parent entity interest, and Non-controlling Interest. In 2018, issued capital is

thermal and metallurgical coal products (Whitehaven Coal, 2018b).

The major financial aspects covered in the first section include equity structure, liabilities

items, and selection of investment in terms of debt and equity for 2018 for both the

companies.

Part-A

Recording of items under “owner equity”

Equity refers to the owner`s interest in the business operations of the company. On an

technical basis, it is an remaining interest between the company`s assets and the liabilities. It

represents the amount hold by the organisation to the owners.

Caltex Limited

PARTICULARS 2018

Issued capital $ 524944.00

Treasury stock -$ 2,462.00

Reserves $ 11,168.00

Retained earnings $ 2,842,357.00

Total parent entity interest $ 3376007.00

Non-controlling Interest $ 13,057.00

Total Equity $ 3,389,064

(Source: Caltex Australia, 2018a).

Caltex Limited’s equity element include issues capital, Treasury stock, Reserves, Retained

earnings, Total parent entity interest, and Non-controlling Interest. In 2018, issued capital is

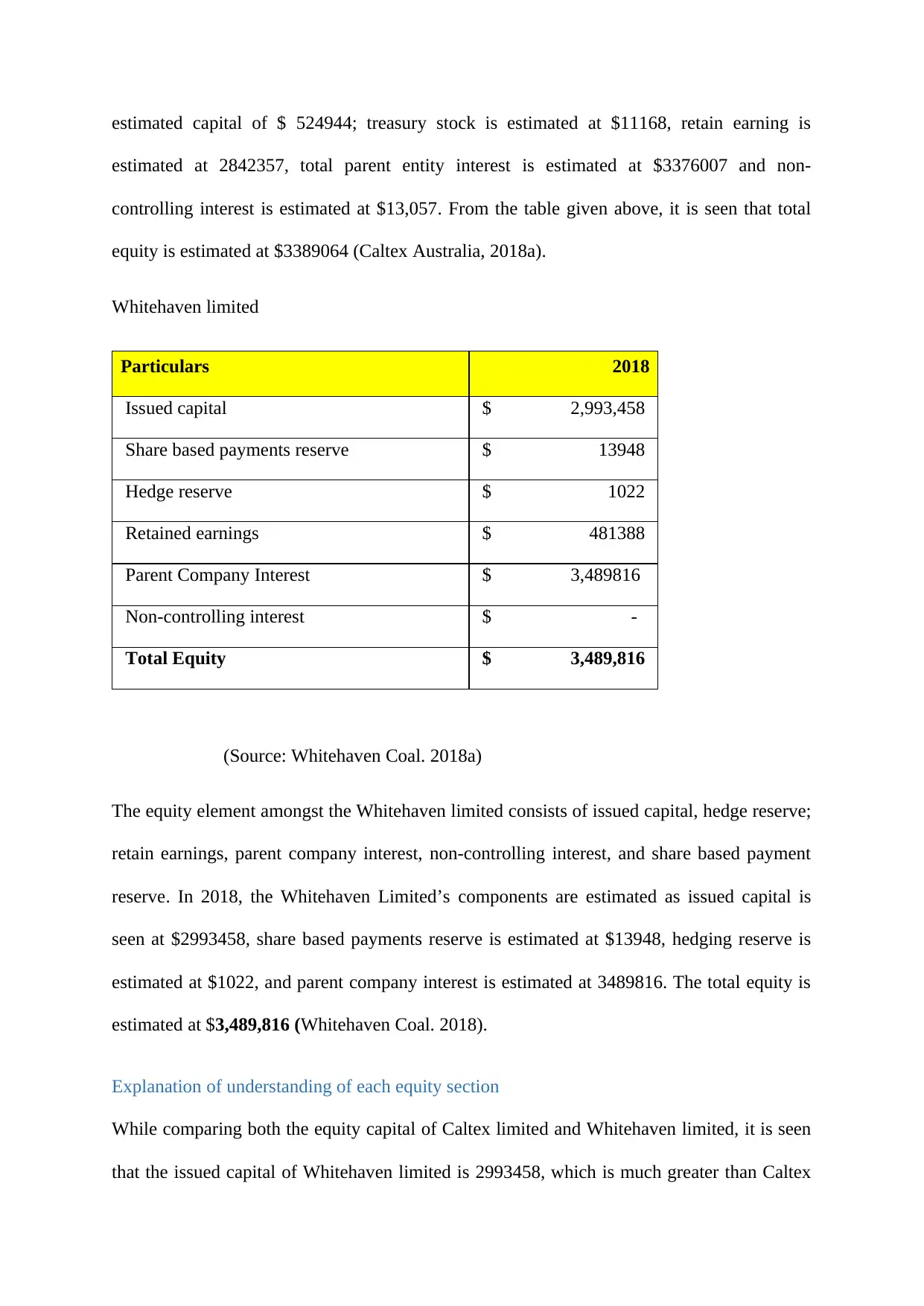

estimated capital of $ 524944; treasury stock is estimated at $11168, retain earning is

estimated at 2842357, total parent entity interest is estimated at $3376007 and non-

controlling interest is estimated at $13,057. From the table given above, it is seen that total

equity is estimated at $3389064 (Caltex Australia, 2018a).

Whitehaven limited

Particulars 2018

Issued capital $ 2,993,458

Share based payments reserve $ 13948

Hedge reserve $ 1022

Retained earnings $ 481388

Parent Company Interest $ 3,489816

Non-controlling interest $ -

Total Equity $ 3,489,816

(Source: Whitehaven Coal. 2018a)

The equity element amongst the Whitehaven limited consists of issued capital, hedge reserve;

retain earnings, parent company interest, non-controlling interest, and share based payment

reserve. In 2018, the Whitehaven Limited’s components are estimated as issued capital is

seen at $2993458, share based payments reserve is estimated at $13948, hedging reserve is

estimated at $1022, and parent company interest is estimated at 3489816. The total equity is

estimated at $3,489,816 (Whitehaven Coal. 2018).

Explanation of understanding of each equity section

While comparing both the equity capital of Caltex limited and Whitehaven limited, it is seen

that the issued capital of Whitehaven limited is 2993458, which is much greater than Caltex

estimated at 2842357, total parent entity interest is estimated at $3376007 and non-

controlling interest is estimated at $13,057. From the table given above, it is seen that total

equity is estimated at $3389064 (Caltex Australia, 2018a).

Whitehaven limited

Particulars 2018

Issued capital $ 2,993,458

Share based payments reserve $ 13948

Hedge reserve $ 1022

Retained earnings $ 481388

Parent Company Interest $ 3,489816

Non-controlling interest $ -

Total Equity $ 3,489,816

(Source: Whitehaven Coal. 2018a)

The equity element amongst the Whitehaven limited consists of issued capital, hedge reserve;

retain earnings, parent company interest, non-controlling interest, and share based payment

reserve. In 2018, the Whitehaven Limited’s components are estimated as issued capital is

seen at $2993458, share based payments reserve is estimated at $13948, hedging reserve is

estimated at $1022, and parent company interest is estimated at 3489816. The total equity is

estimated at $3,489,816 (Whitehaven Coal. 2018).

Explanation of understanding of each equity section

While comparing both the equity capital of Caltex limited and Whitehaven limited, it is seen

that the issued capital of Whitehaven limited is 2993458, which is much greater than Caltex

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

limited that is near to 524944. The company has announced buy back of equity shares so that

it can manage its capital. Issued capital of Whitehaven has not changed much while

comparing to its previous years in regards to the capital structure (Caltex Australia, 2018b).

Treasury stock is the amount of bought shares as backed by the organisation and it is

reflected as negative amount in the financial statements as it will reflect deduction in share

capital of the reporting on the account of share buyback. There can be change in treasury

stock account that takes place just because of Caltex`s decision of buying back of the shares

from the market (Caltex Australia, 2018b).

Items under liabilities section

The liability section categorises it in two parts named as current and non-current liabilities.

Current liabilities are understood as liabilities of business, which will be settled in cash in the

fiscal year with the operating cycle of the firm (Caltex Australia, 2018b). Amounts that has

been listed in the balance sheet as the unpaid account, which is related to issuance of account

payable representing payables representing the purchase of goods from vendors of the

organisation. Whereas, non-current liabilities are the long-term liabilities that are financial

obligation of the organisation, which will come due in a year or more than a year. While

analysing the current and non-current liabilities of both the organisation, it is seen that both

the organisations maintain an almost same items under current and non-current liabilities

(Morton, Schlackow, Mihaylova, Staplin, Gray, and Cass, 2015).

Caltex limited

Particulars 2018

Interest bearing loans and borrowings $ 810914

Payable $ 41686

Provisions $ 252098

it can manage its capital. Issued capital of Whitehaven has not changed much while

comparing to its previous years in regards to the capital structure (Caltex Australia, 2018b).

Treasury stock is the amount of bought shares as backed by the organisation and it is

reflected as negative amount in the financial statements as it will reflect deduction in share

capital of the reporting on the account of share buyback. There can be change in treasury

stock account that takes place just because of Caltex`s decision of buying back of the shares

from the market (Caltex Australia, 2018b).

Items under liabilities section

The liability section categorises it in two parts named as current and non-current liabilities.

Current liabilities are understood as liabilities of business, which will be settled in cash in the

fiscal year with the operating cycle of the firm (Caltex Australia, 2018b). Amounts that has

been listed in the balance sheet as the unpaid account, which is related to issuance of account

payable representing payables representing the purchase of goods from vendors of the

organisation. Whereas, non-current liabilities are the long-term liabilities that are financial

obligation of the organisation, which will come due in a year or more than a year. While

analysing the current and non-current liabilities of both the organisation, it is seen that both

the organisations maintain an almost same items under current and non-current liabilities

(Morton, Schlackow, Mihaylova, Staplin, Gray, and Cass, 2015).

Caltex limited

Particulars 2018

Interest bearing loans and borrowings $ 810914

Payable $ 41686

Provisions $ 252098

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

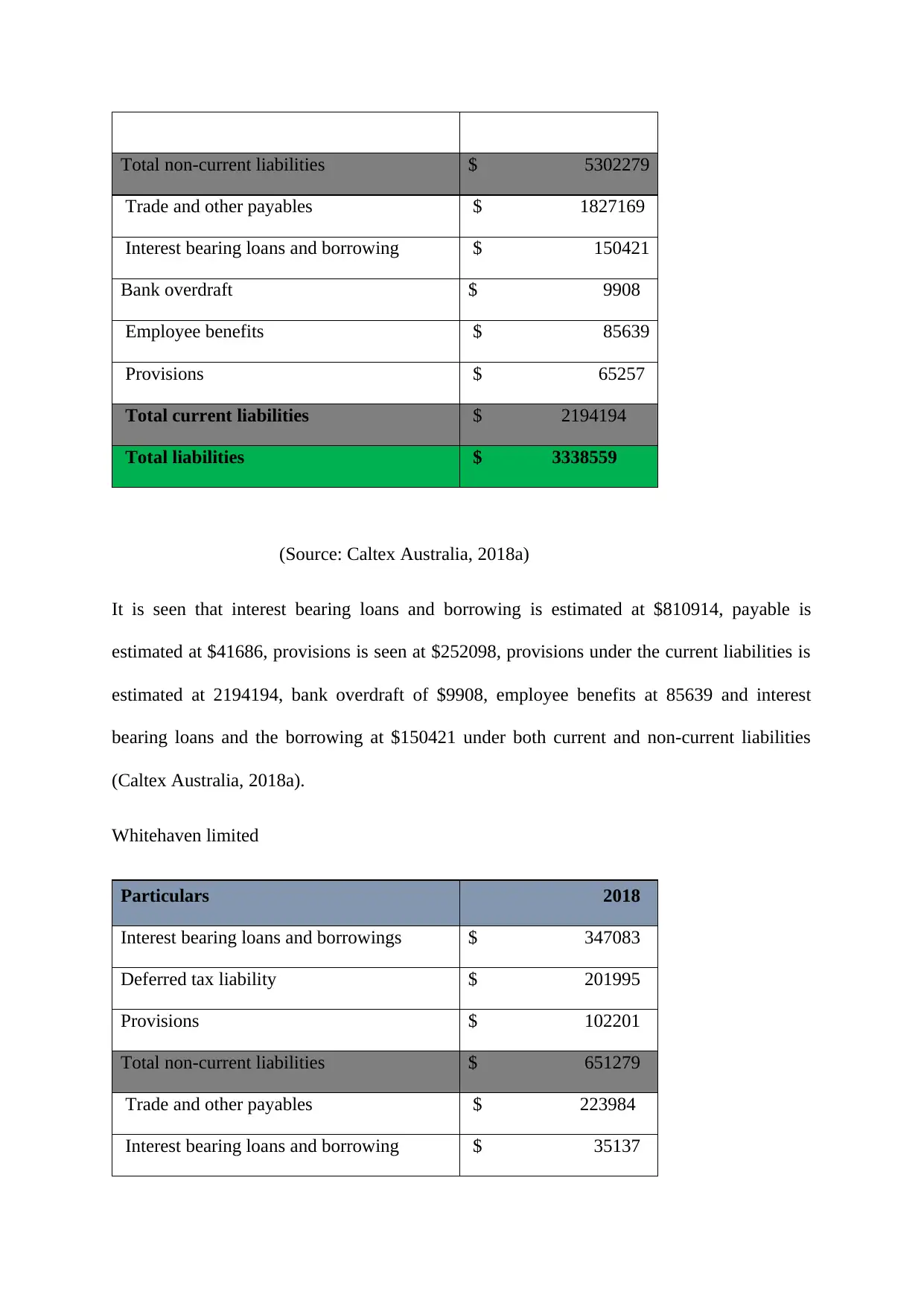

Total non-current liabilities $ 5302279

Trade and other payables $ 1827169

Interest bearing loans and borrowing $ 150421

Bank overdraft $ 9908

Employee benefits $ 85639

Provisions $ 65257

Total current liabilities $ 2194194

Total liabilities $ 3338559

(Source: Caltex Australia, 2018a)

It is seen that interest bearing loans and borrowing is estimated at $810914, payable is

estimated at $41686, provisions is seen at $252098, provisions under the current liabilities is

estimated at 2194194, bank overdraft of $9908, employee benefits at 85639 and interest

bearing loans and the borrowing at $150421 under both current and non-current liabilities

(Caltex Australia, 2018a).

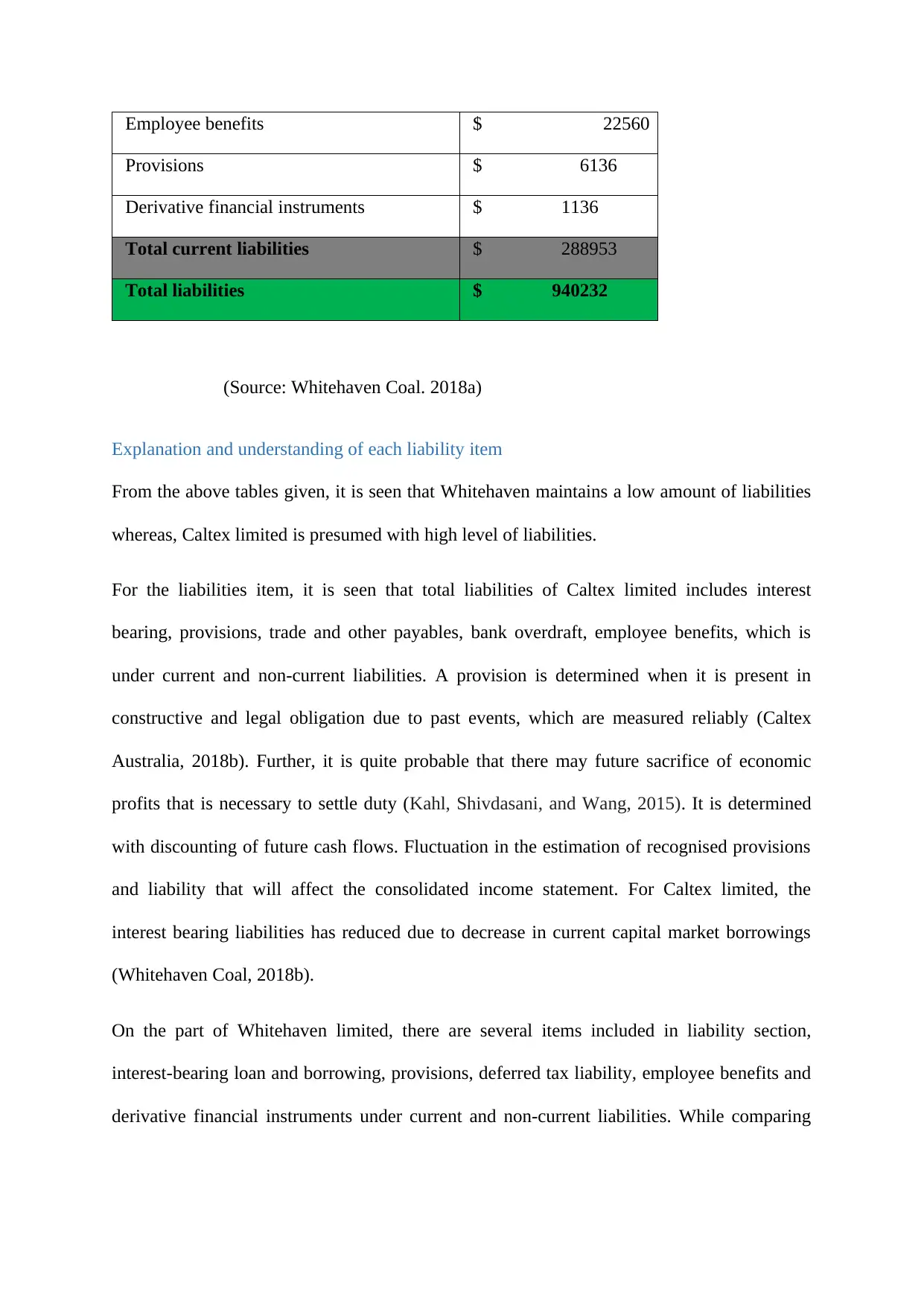

Whitehaven limited

Particulars 2018

Interest bearing loans and borrowings $ 347083

Deferred tax liability $ 201995

Provisions $ 102201

Total non-current liabilities $ 651279

Trade and other payables $ 223984

Interest bearing loans and borrowing $ 35137

Trade and other payables $ 1827169

Interest bearing loans and borrowing $ 150421

Bank overdraft $ 9908

Employee benefits $ 85639

Provisions $ 65257

Total current liabilities $ 2194194

Total liabilities $ 3338559

(Source: Caltex Australia, 2018a)

It is seen that interest bearing loans and borrowing is estimated at $810914, payable is

estimated at $41686, provisions is seen at $252098, provisions under the current liabilities is

estimated at 2194194, bank overdraft of $9908, employee benefits at 85639 and interest

bearing loans and the borrowing at $150421 under both current and non-current liabilities

(Caltex Australia, 2018a).

Whitehaven limited

Particulars 2018

Interest bearing loans and borrowings $ 347083

Deferred tax liability $ 201995

Provisions $ 102201

Total non-current liabilities $ 651279

Trade and other payables $ 223984

Interest bearing loans and borrowing $ 35137

Employee benefits $ 22560

Provisions $ 6136

Derivative financial instruments $ 1136

Total current liabilities $ 288953

Total liabilities $ 940232

(Source: Whitehaven Coal. 2018a)

Explanation and understanding of each liability item

From the above tables given, it is seen that Whitehaven maintains a low amount of liabilities

whereas, Caltex limited is presumed with high level of liabilities.

For the liabilities item, it is seen that total liabilities of Caltex limited includes interest

bearing, provisions, trade and other payables, bank overdraft, employee benefits, which is

under current and non-current liabilities. A provision is determined when it is present in

constructive and legal obligation due to past events, which are measured reliably (Caltex

Australia, 2018b). Further, it is quite probable that there may future sacrifice of economic

profits that is necessary to settle duty (Kahl, Shivdasani, and Wang, 2015). It is determined

with discounting of future cash flows. Fluctuation in the estimation of recognised provisions

and liability that will affect the consolidated income statement. For Caltex limited, the

interest bearing liabilities has reduced due to decrease in current capital market borrowings

(Whitehaven Coal, 2018b).

On the part of Whitehaven limited, there are several items included in liability section,

interest-bearing loan and borrowing, provisions, deferred tax liability, employee benefits and

derivative financial instruments under current and non-current liabilities. While comparing

Provisions $ 6136

Derivative financial instruments $ 1136

Total current liabilities $ 288953

Total liabilities $ 940232

(Source: Whitehaven Coal. 2018a)

Explanation and understanding of each liability item

From the above tables given, it is seen that Whitehaven maintains a low amount of liabilities

whereas, Caltex limited is presumed with high level of liabilities.

For the liabilities item, it is seen that total liabilities of Caltex limited includes interest

bearing, provisions, trade and other payables, bank overdraft, employee benefits, which is

under current and non-current liabilities. A provision is determined when it is present in

constructive and legal obligation due to past events, which are measured reliably (Caltex

Australia, 2018b). Further, it is quite probable that there may future sacrifice of economic

profits that is necessary to settle duty (Kahl, Shivdasani, and Wang, 2015). It is determined

with discounting of future cash flows. Fluctuation in the estimation of recognised provisions

and liability that will affect the consolidated income statement. For Caltex limited, the

interest bearing liabilities has reduced due to decrease in current capital market borrowings

(Whitehaven Coal, 2018b).

On the part of Whitehaven limited, there are several items included in liability section,

interest-bearing loan and borrowing, provisions, deferred tax liability, employee benefits and

derivative financial instruments under current and non-current liabilities. While comparing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

both of the items of these two companies, it is seen that Whiteman incurred less liabilities as

compared to Caltex limited (Whitehaven Coal. 2018a).

Advantages and disadvantages of every source of fund, which is selected by the company

In order to expand the business level, the company can rely on sources of investment and

funds such as letter of credit, euro issue, venture funding, equity, retain earning, capital loans,

and debt (Chiu, Wang, and Peña, 2017). Except equity and debt, all the above mentioned

source of funds are short term borrowings. Source of funds have been classified on the basis

of period, source, ownership, generation, and control (Chiu, Wang, and Peña, 2017). The two

major source of funds for Caltex limited and Whitehaven limited are debt and equity.

Whitehaven employs more of equity for the source of funds whereas it employs debt of

$651279 (Chiu, Wang, and Peña, 2017). The company majorly rely on equity rather than

debt. The company might have considered some of the disadvantages of debt-

One of the major disadvantage of debt is related to when the organisations are obliged to pay

back the amount that is being borrowed with the interest amount according to the time

(Alomari, Power, and Tantisantiwong, 2018). Organisation often suffer cash flow issues,

which are difficult to pay within the time. Many a times, severe penalties are imposed on

companies that fail to pay the debt in a decided time (Chiu, Wang, and Peña, 2017).

Some of the advantages of debt and financing are-

The main advantage is the issuing bonds with borrowing money from the lenders, which

enables it to maintain the ownership completely. This benefit of ownership maintaining lead

to complete control over the main decisions accomplished on the behalf of the organisation.

Management has its own ability to select its board members (Wu, 2019).

Another disadvantage of the debt financing is related to when organisations receive deduction

in taxes for interest paid for debt. Internal revenue undertakes the interest paid as a business

compared to Caltex limited (Whitehaven Coal. 2018a).

Advantages and disadvantages of every source of fund, which is selected by the company

In order to expand the business level, the company can rely on sources of investment and

funds such as letter of credit, euro issue, venture funding, equity, retain earning, capital loans,

and debt (Chiu, Wang, and Peña, 2017). Except equity and debt, all the above mentioned

source of funds are short term borrowings. Source of funds have been classified on the basis

of period, source, ownership, generation, and control (Chiu, Wang, and Peña, 2017). The two

major source of funds for Caltex limited and Whitehaven limited are debt and equity.

Whitehaven employs more of equity for the source of funds whereas it employs debt of

$651279 (Chiu, Wang, and Peña, 2017). The company majorly rely on equity rather than

debt. The company might have considered some of the disadvantages of debt-

One of the major disadvantage of debt is related to when the organisations are obliged to pay

back the amount that is being borrowed with the interest amount according to the time

(Alomari, Power, and Tantisantiwong, 2018). Organisation often suffer cash flow issues,

which are difficult to pay within the time. Many a times, severe penalties are imposed on

companies that fail to pay the debt in a decided time (Chiu, Wang, and Peña, 2017).

Some of the advantages of debt and financing are-

The main advantage is the issuing bonds with borrowing money from the lenders, which

enables it to maintain the ownership completely. This benefit of ownership maintaining lead

to complete control over the main decisions accomplished on the behalf of the organisation.

Management has its own ability to select its board members (Wu, 2019).

Another disadvantage of the debt financing is related to when organisations receive deduction

in taxes for interest paid for debt. Internal revenue undertakes the interest paid as a business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

expense, which permit the businesses to subtract the payment from the income they earn from

corporates and business operation (Wu, 2019). Organisation can use debt financing in order

to raise the capital that are more flexible as compared to using equity financing as they are

obliged to investors and lenders for the repayment period (Wu, 2019).

Another disadvantage of the debt financing can be where organisations are responsible to pay

the main and principal amount along with the interest. Debt financing affects the credit rating

of the organisation (Wu, 2019). The company, which has greater level of debt employed in its

operation than equity financing, will be affected and it will have to suffer in its profits and

increasing risk (Wu, 2019). Another negative point can be debt financing affecting credit

rating of the organisation. A company can only maintain a significant amount of risk in

relation to equity financing. An organisation with low credit rating will have to rely on

issuing of bonds that will have to pay high interest rate while attracting investors (Wu, 2019).

Organisation will have to pay high rate of interest that will further lead to paying more

interest as cash flow issues can be there in future. Organisations often seek debt financing

that lead to deal with meeting the lender`s cash in hand (Groh, 2017). Some other

organisations can pull up the collateral to seen the quality for financing that keep the assets at

risk if the organisation is not able to pay its debt again (Khmel, and Zhao, 2016).

Advantage of the debt financing

The organisation and the owner must have the accepted level of credit rating in order to

qualify. The interest and principal payment that are stated in advance as it is easier to work on

these company`s cash flow (Khmel, and Zhao, 2016). Opting loan can be temporary and this

relation of paying ends when it is repaid. A lender does not have any saying in how the

owners will run the business (Groh, 2017). Loan interest is deductible and on the other hand,

dividend is paid to the shareholders is not tax deductible. Principal and the interest payment

corporates and business operation (Wu, 2019). Organisation can use debt financing in order

to raise the capital that are more flexible as compared to using equity financing as they are

obliged to investors and lenders for the repayment period (Wu, 2019).

Another disadvantage of the debt financing can be where organisations are responsible to pay

the main and principal amount along with the interest. Debt financing affects the credit rating

of the organisation (Wu, 2019). The company, which has greater level of debt employed in its

operation than equity financing, will be affected and it will have to suffer in its profits and

increasing risk (Wu, 2019). Another negative point can be debt financing affecting credit

rating of the organisation. A company can only maintain a significant amount of risk in

relation to equity financing. An organisation with low credit rating will have to rely on

issuing of bonds that will have to pay high interest rate while attracting investors (Wu, 2019).

Organisation will have to pay high rate of interest that will further lead to paying more

interest as cash flow issues can be there in future. Organisations often seek debt financing

that lead to deal with meeting the lender`s cash in hand (Groh, 2017). Some other

organisations can pull up the collateral to seen the quality for financing that keep the assets at

risk if the organisation is not able to pay its debt again (Khmel, and Zhao, 2016).

Advantage of the debt financing

The organisation and the owner must have the accepted level of credit rating in order to

qualify. The interest and principal payment that are stated in advance as it is easier to work on

these company`s cash flow (Khmel, and Zhao, 2016). Opting loan can be temporary and this

relation of paying ends when it is repaid. A lender does not have any saying in how the

owners will run the business (Groh, 2017). Loan interest is deductible and on the other hand,

dividend is paid to the shareholders is not tax deductible. Principal and the interest payment

has been stated in advance where it is easier to work on the company`s flows. Loan can be

short term, medium term or long term (Caballero, Teruel, and Solano, 2016).

Advantages of equity

Low level of risk- A company will possess less risk as it does not have any fixed monthly

expense or loan payment to make. This can be helpful to the start-up organisation, which may

not have positive cash flows (Bandopadhyay, and Roy, 2016).

No credit risk- Equity financing is not only the piece of financing the fund for growth. Even

when the debt is offered then the interest rate can be relatively high. Debt loan repayments

can take out the organisation`s cash flow leading to reduce the money that is needed to

finance the growth prospects (Bandopadhyay, and Roy, 2016). Equity investors can not

expect receiving immediate return for their investment. This is the long-term view and facing

the possibility of losing the money when the organisation fails. There are some disadvantages

of equity such as its cost, loss of control, and potential for the conflicting situations. The

investors expect high dividend to receive as a return on the money as business owners will be

willing to share company`s profit with their equity partners (Bandopadhyay, and Roy, 2016).

The amount of paid to the partners can be higher than the interest rate on the debt financing.

It is important to note that every partner of business have different voicing decision regarding

the business and its related big decisions. There is always a conflict between the different

visions of the organisation and its disagreement in regards to the management styles. Finally,

an owner is willing to deal with the differences of the opinions (Allen, Qian, and Xie, 2019).

Part-B

A single person who is responsible for all the rewards and losses runs a sole proprietor

business. It is necessary to comply with rules if particular city, country or place and register

with the legal tiny home based sole proprietorship and also pay atleast minimum tax as per its

short term, medium term or long term (Caballero, Teruel, and Solano, 2016).

Advantages of equity

Low level of risk- A company will possess less risk as it does not have any fixed monthly

expense or loan payment to make. This can be helpful to the start-up organisation, which may

not have positive cash flows (Bandopadhyay, and Roy, 2016).

No credit risk- Equity financing is not only the piece of financing the fund for growth. Even

when the debt is offered then the interest rate can be relatively high. Debt loan repayments

can take out the organisation`s cash flow leading to reduce the money that is needed to

finance the growth prospects (Bandopadhyay, and Roy, 2016). Equity investors can not

expect receiving immediate return for their investment. This is the long-term view and facing

the possibility of losing the money when the organisation fails. There are some disadvantages

of equity such as its cost, loss of control, and potential for the conflicting situations. The

investors expect high dividend to receive as a return on the money as business owners will be

willing to share company`s profit with their equity partners (Bandopadhyay, and Roy, 2016).

The amount of paid to the partners can be higher than the interest rate on the debt financing.

It is important to note that every partner of business have different voicing decision regarding

the business and its related big decisions. There is always a conflict between the different

visions of the organisation and its disagreement in regards to the management styles. Finally,

an owner is willing to deal with the differences of the opinions (Allen, Qian, and Xie, 2019).

Part-B

A single person who is responsible for all the rewards and losses runs a sole proprietor

business. It is necessary to comply with rules if particular city, country or place and register

with the legal tiny home based sole proprietorship and also pay atleast minimum tax as per its

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.