Corporate Accounting Report: Telstra Corporation Financial Analysis

VerifiedAdded on 2021/06/15

|16

|3154

|33

Report

AI Summary

This report provides a comprehensive analysis of corporate accounting practices, using Telstra Corporation as a case study. It is divided into two parts, with the first part exploring qualitative characteristics like comparability and relevance within financial reporting, alongside environmental disclosure practices. The report highlights Telstra's sustainability efforts, including reductions in greenhouse gas emissions, digital literacy programs, and employee volunteering. The second part delves into pre-acquisition entries in consolidated financial statements, explaining their role in preventing double-counting of assets and equities, and discusses dividend treatments in different scenarios. Furthermore, it covers the treatment of goodwill under partial and full goodwill methods and the necessary adjustments when carrying amounts differ from fair values during acquisitions. The report also offers recommendations for improving the presentation of financial and sustainability information, such as the inclusion of more quantitative data and comparative information.

Running head: CORPORATE ACCOUNTING

Name of the Student

Name of the University

Author Note

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE ACCOUNTING

Executive Summary:

The relevant discussions of the study have been taken into consideration with aspects of

corporate accounting in terms of “Telstra Corporations limited”. The report has been

segregated into two parts, the first part has stated about the qualitative characteristics of

compatibility and relevance thereby disclosing the environmental reporting practices. The

second part of the study have shown the intention of pre-acquisition entries during the

depression of consolidated financial statements. The findings of the study reveal that the

overall sustainability and judgement of the company with the stakeholder is more than 71%

and it is aimed at focusing 68% reduction in greenhouse gas emissions. The sustainability

efforts have concentrated on most significant issues associated to reaching to more than

63000 people via digital literacy programs and their employees taking part in more than 8900

volunteering days in the community. Some of the other excerpts of the study have found that

the pre-acquisition entries are conducive in preventing any instance of “double counting of

assets”. The pre-acquisition entries are also conducive vital in preventing any instance of

“double counting” associated with the equities of the concerned organisation.

Executive Summary:

The relevant discussions of the study have been taken into consideration with aspects of

corporate accounting in terms of “Telstra Corporations limited”. The report has been

segregated into two parts, the first part has stated about the qualitative characteristics of

compatibility and relevance thereby disclosing the environmental reporting practices. The

second part of the study have shown the intention of pre-acquisition entries during the

depression of consolidated financial statements. The findings of the study reveal that the

overall sustainability and judgement of the company with the stakeholder is more than 71%

and it is aimed at focusing 68% reduction in greenhouse gas emissions. The sustainability

efforts have concentrated on most significant issues associated to reaching to more than

63000 people via digital literacy programs and their employees taking part in more than 8900

volunteering days in the community. Some of the other excerpts of the study have found that

the pre-acquisition entries are conducive in preventing any instance of “double counting of

assets”. The pre-acquisition entries are also conducive vital in preventing any instance of

“double counting” associated with the equities of the concerned organisation.

2CORPORATE ACCOUNTING

Table of Contents

Introduction:...............................................................................................................................3

Discussion:.................................................................................................................................3

Part A 1a:....................................................................................................................................3

Part A 1b:...................................................................................................................................5

Part A 2......................................................................................................................................7

Part A 3......................................................................................................................................8

Part B 1.......................................................................................................................................9

Part B 2.......................................................................................................................................9

Part B 3.....................................................................................................................................10

Part B 4.....................................................................................................................................10

Part B 5.....................................................................................................................................11

Conclusion:..............................................................................................................................12

References................................................................................................................................13

Table of Contents

Introduction:...............................................................................................................................3

Discussion:.................................................................................................................................3

Part A 1a:....................................................................................................................................3

Part A 1b:...................................................................................................................................5

Part A 2......................................................................................................................................7

Part A 3......................................................................................................................................8

Part B 1.......................................................................................................................................9

Part B 2.......................................................................................................................................9

Part B 3.....................................................................................................................................10

Part B 4.....................................................................................................................................10

Part B 5.....................................................................................................................................11

Conclusion:..............................................................................................................................12

References................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE ACCOUNTING

Introduction:

The analysis based on the financial statement of the company is depicted to be having

a significant role in terms of corporate accounting. It is to be discerned that financial

statements often serve as a performance statement of company. Therefore, “consolidated

balance sheet”, “comprehensive income statement”, “cash flow statement” and the “statement

showing equity changes”, cannot be overlooked. The consideration of these vital things

serves as various qualities of financial statements and the environmental aspects for making

disclosure about compliance to the top management. The present study has discussed the

various aspects of corporate accounting in terms of “Telstra Corporations limited”. The report

has been segregated into two parts, the first part has stated about the qualitative

characteristics of compatibility and relevance thereby disclosing the environmental reporting

practices. The second part of the study have shown the intention of pre-acquisition entries

during the depression of consolidated financial statements (Leung, Parker & Courtis, 2015).

Discussion:

Part A 1a:

The important aspects of the qualitative characteristics considered from the excerpts

of financial report are related to “comparability, understand ability and reliability” of the

reporting. In this segment, the principle of relevance and comparability is duly discussed with

reference to the financial statement of Telstra Corporations (Telstra.com.au, 2018).

Relevance: The important aspect of relevance of in the financial report states that the various

types of qualitative data should be relevant to the information which is being investigated by

the stakeholders. As the statements have a critical role in the economic decision-making, the

results of this information must be considered with utmost care. Henceforth, the omission of

such information can lead to detrimental repercussions. The total amount of dividend

Introduction:

The analysis based on the financial statement of the company is depicted to be having

a significant role in terms of corporate accounting. It is to be discerned that financial

statements often serve as a performance statement of company. Therefore, “consolidated

balance sheet”, “comprehensive income statement”, “cash flow statement” and the “statement

showing equity changes”, cannot be overlooked. The consideration of these vital things

serves as various qualities of financial statements and the environmental aspects for making

disclosure about compliance to the top management. The present study has discussed the

various aspects of corporate accounting in terms of “Telstra Corporations limited”. The report

has been segregated into two parts, the first part has stated about the qualitative

characteristics of compatibility and relevance thereby disclosing the environmental reporting

practices. The second part of the study have shown the intention of pre-acquisition entries

during the depression of consolidated financial statements (Leung, Parker & Courtis, 2015).

Discussion:

Part A 1a:

The important aspects of the qualitative characteristics considered from the excerpts

of financial report are related to “comparability, understand ability and reliability” of the

reporting. In this segment, the principle of relevance and comparability is duly discussed with

reference to the financial statement of Telstra Corporations (Telstra.com.au, 2018).

Relevance: The important aspect of relevance of in the financial report states that the various

types of qualitative data should be relevant to the information which is being investigated by

the stakeholders. As the statements have a critical role in the economic decision-making, the

results of this information must be considered with utmost care. Henceforth, the omission of

such information can lead to detrimental repercussions. The total amount of dividend

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE ACCOUNTING

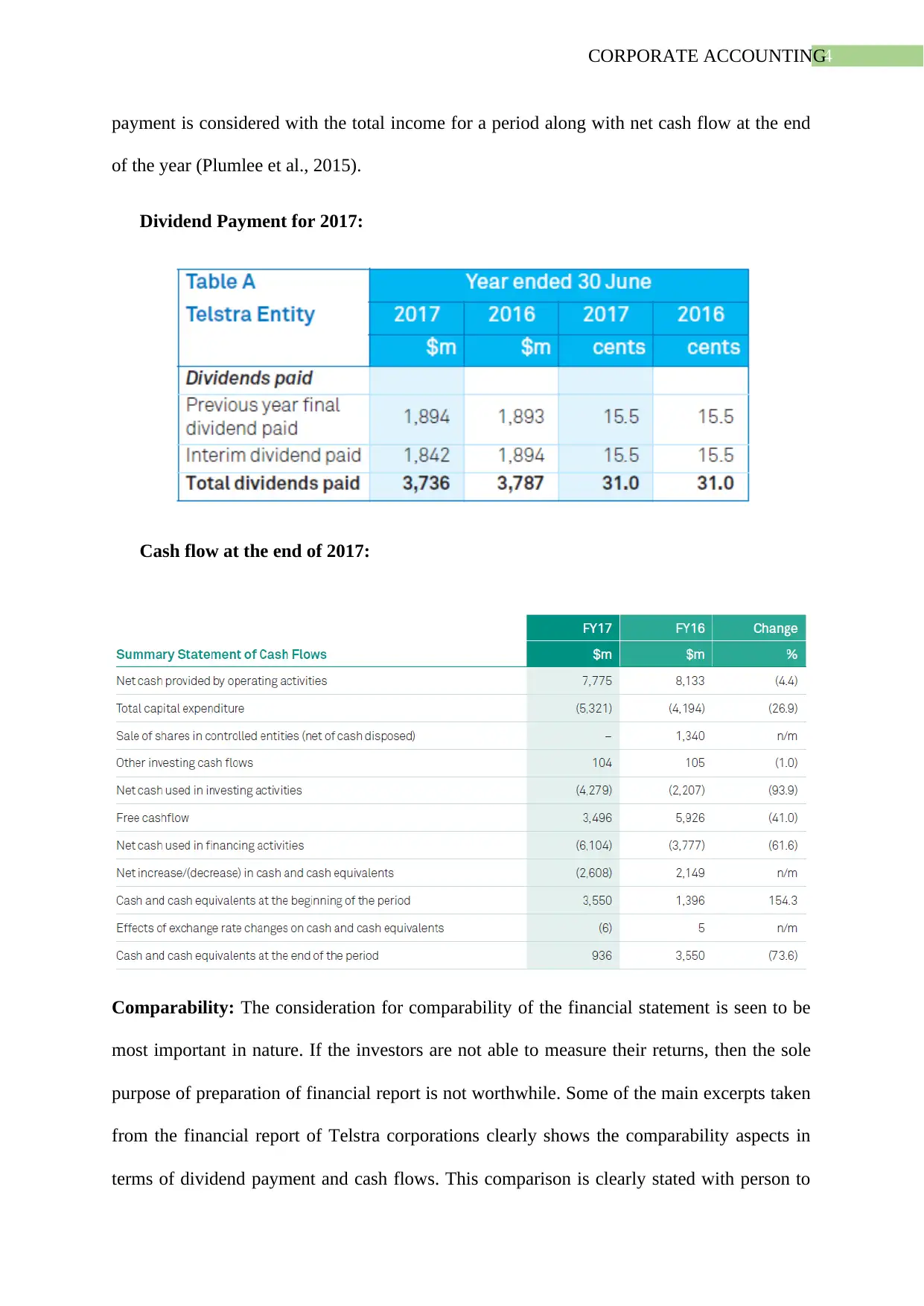

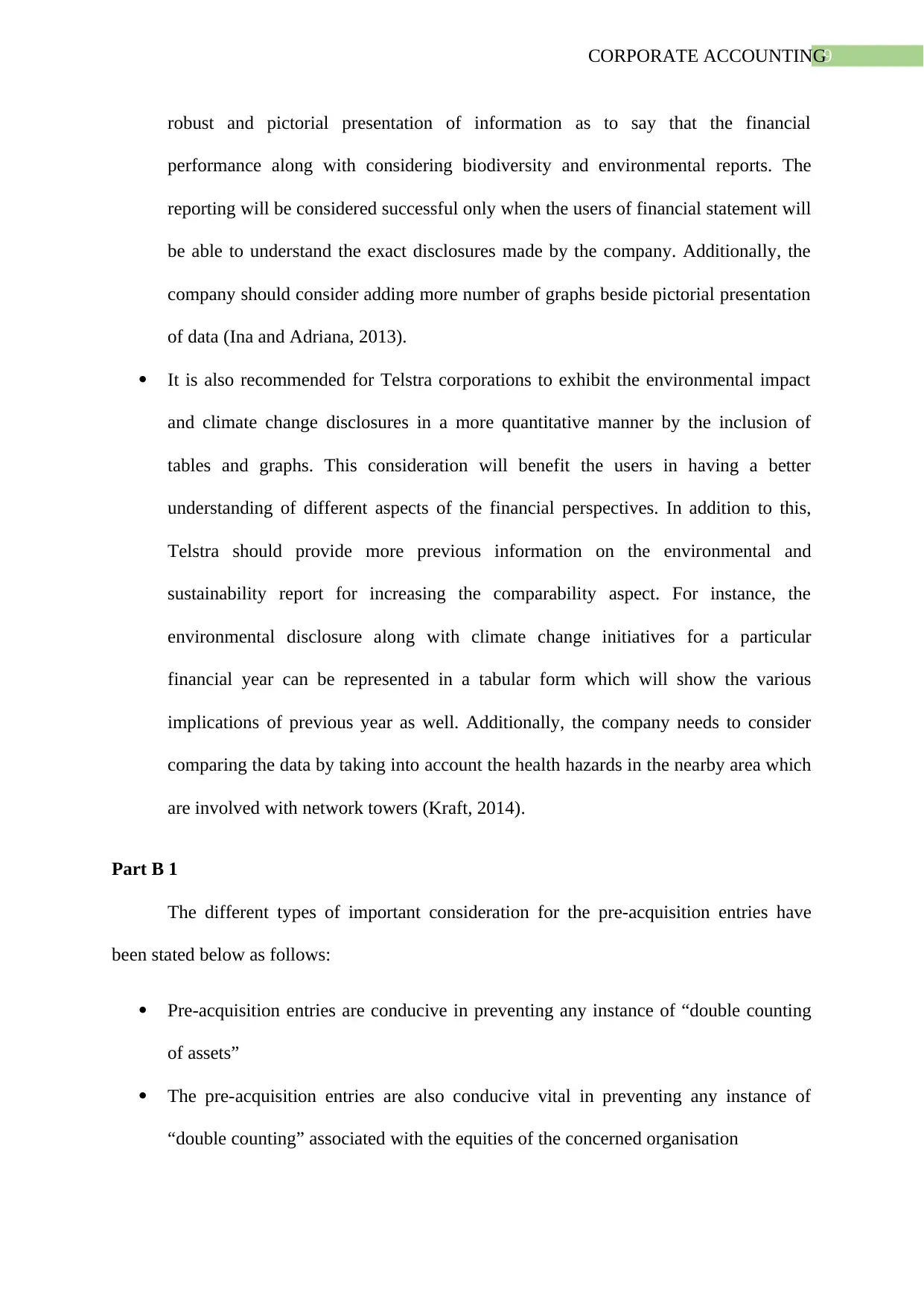

payment is considered with the total income for a period along with net cash flow at the end

of the year (Plumlee et al., 2015).

Dividend Payment for 2017:

Cash flow at the end of 2017:

Comparability: The consideration for comparability of the financial statement is seen to be

most important in nature. If the investors are not able to measure their returns, then the sole

purpose of preparation of financial report is not worthwhile. Some of the main excerpts taken

from the financial report of Telstra corporations clearly shows the comparability aspects in

terms of dividend payment and cash flows. This comparison is clearly stated with person to

payment is considered with the total income for a period along with net cash flow at the end

of the year (Plumlee et al., 2015).

Dividend Payment for 2017:

Cash flow at the end of 2017:

Comparability: The consideration for comparability of the financial statement is seen to be

most important in nature. If the investors are not able to measure their returns, then the sole

purpose of preparation of financial report is not worthwhile. Some of the main excerpts taken

from the financial report of Telstra corporations clearly shows the comparability aspects in

terms of dividend payment and cash flows. This comparison is clearly stated with person to

5CORPORATE ACCOUNTING

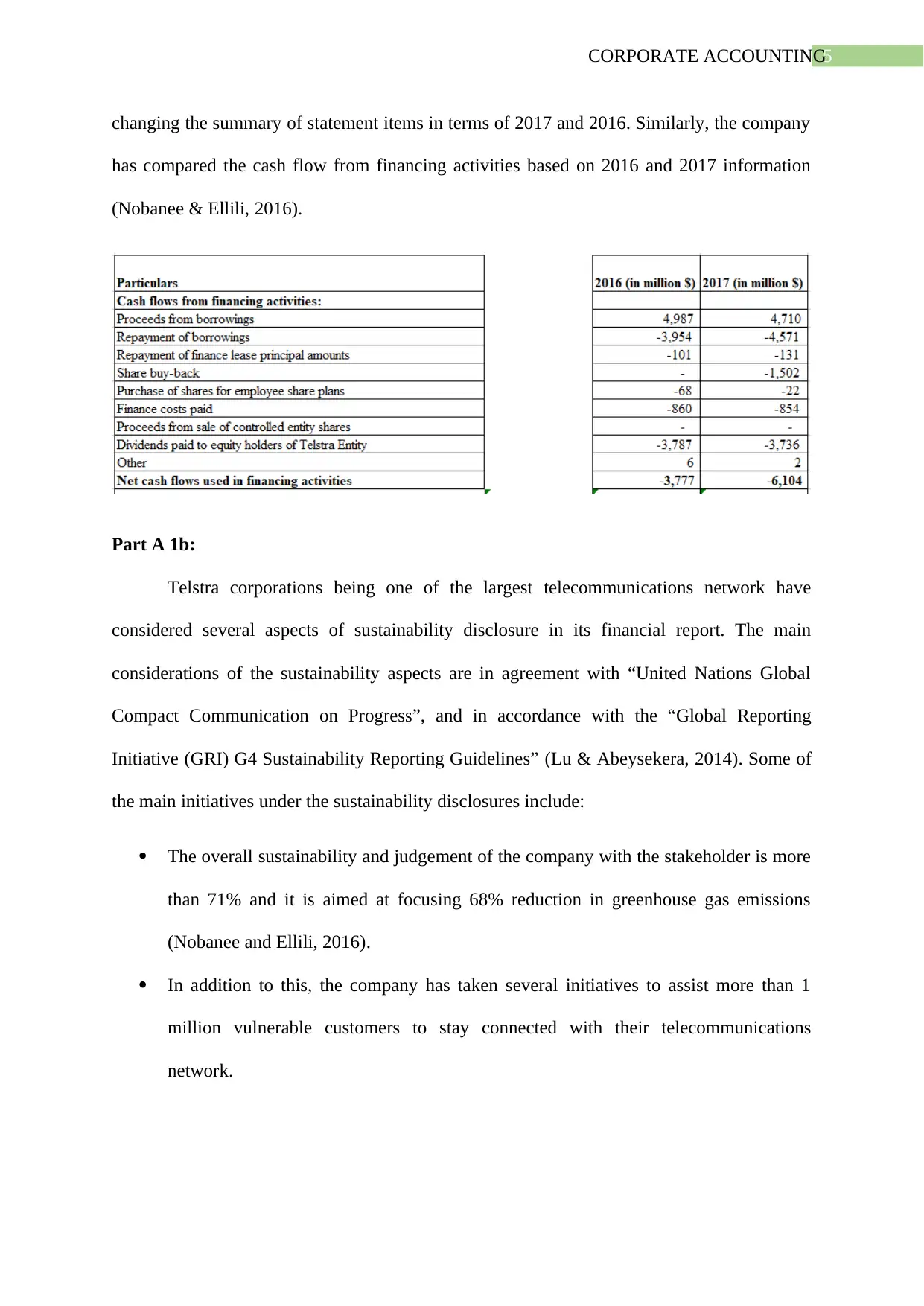

changing the summary of statement items in terms of 2017 and 2016. Similarly, the company

has compared the cash flow from financing activities based on 2016 and 2017 information

(Nobanee & Ellili, 2016).

Part A 1b:

Telstra corporations being one of the largest telecommunications network have

considered several aspects of sustainability disclosure in its financial report. The main

considerations of the sustainability aspects are in agreement with “United Nations Global

Compact Communication on Progress”, and in accordance with the “Global Reporting

Initiative (GRI) G4 Sustainability Reporting Guidelines” (Lu & Abeysekera, 2014). Some of

the main initiatives under the sustainability disclosures include:

The overall sustainability and judgement of the company with the stakeholder is more

than 71% and it is aimed at focusing 68% reduction in greenhouse gas emissions

(Nobanee and Ellili, 2016).

In addition to this, the company has taken several initiatives to assist more than 1

million vulnerable customers to stay connected with their telecommunications

network.

changing the summary of statement items in terms of 2017 and 2016. Similarly, the company

has compared the cash flow from financing activities based on 2016 and 2017 information

(Nobanee & Ellili, 2016).

Part A 1b:

Telstra corporations being one of the largest telecommunications network have

considered several aspects of sustainability disclosure in its financial report. The main

considerations of the sustainability aspects are in agreement with “United Nations Global

Compact Communication on Progress”, and in accordance with the “Global Reporting

Initiative (GRI) G4 Sustainability Reporting Guidelines” (Lu & Abeysekera, 2014). Some of

the main initiatives under the sustainability disclosures include:

The overall sustainability and judgement of the company with the stakeholder is more

than 71% and it is aimed at focusing 68% reduction in greenhouse gas emissions

(Nobanee and Ellili, 2016).

In addition to this, the company has taken several initiatives to assist more than 1

million vulnerable customers to stay connected with their telecommunications

network.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE ACCOUNTING

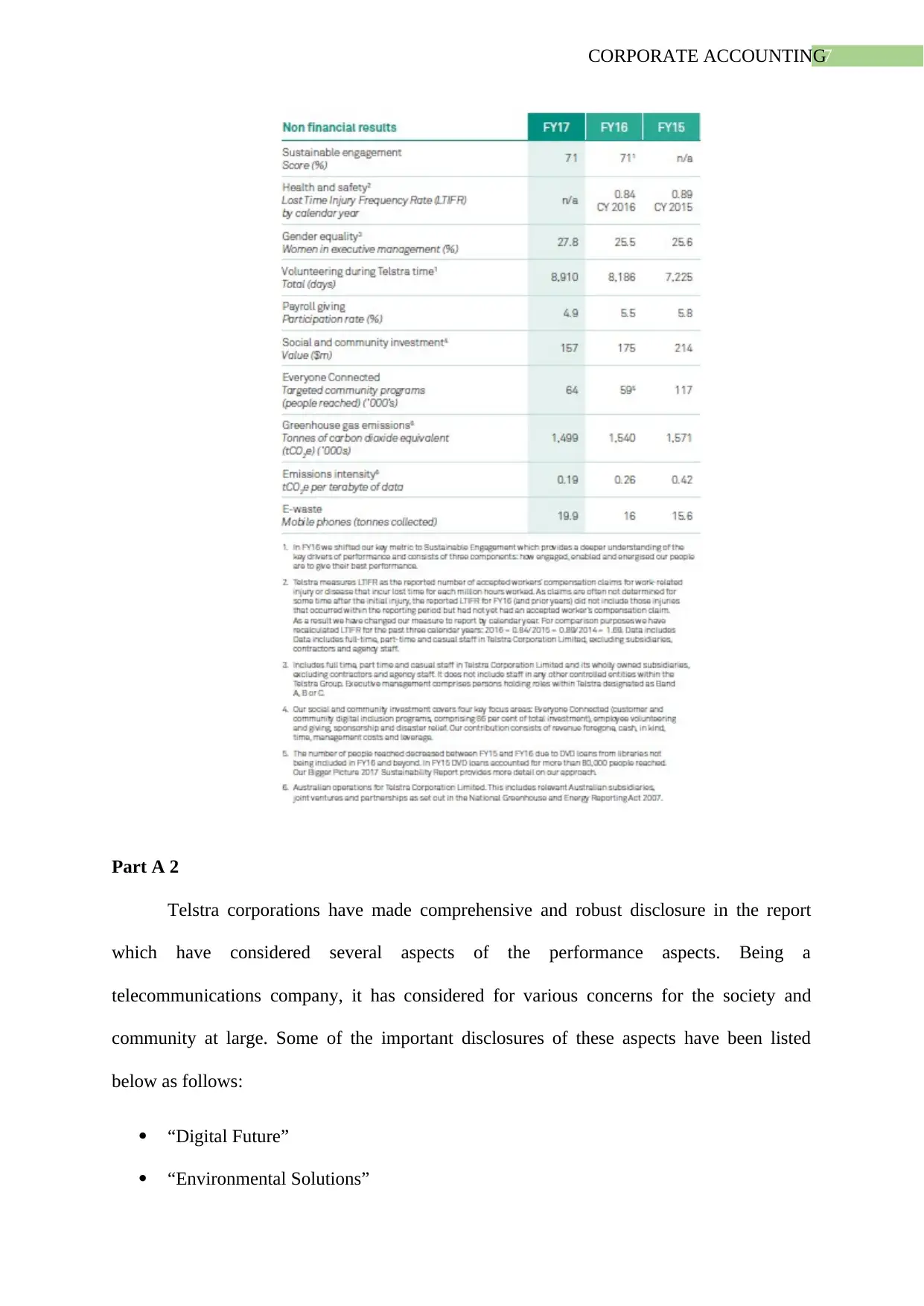

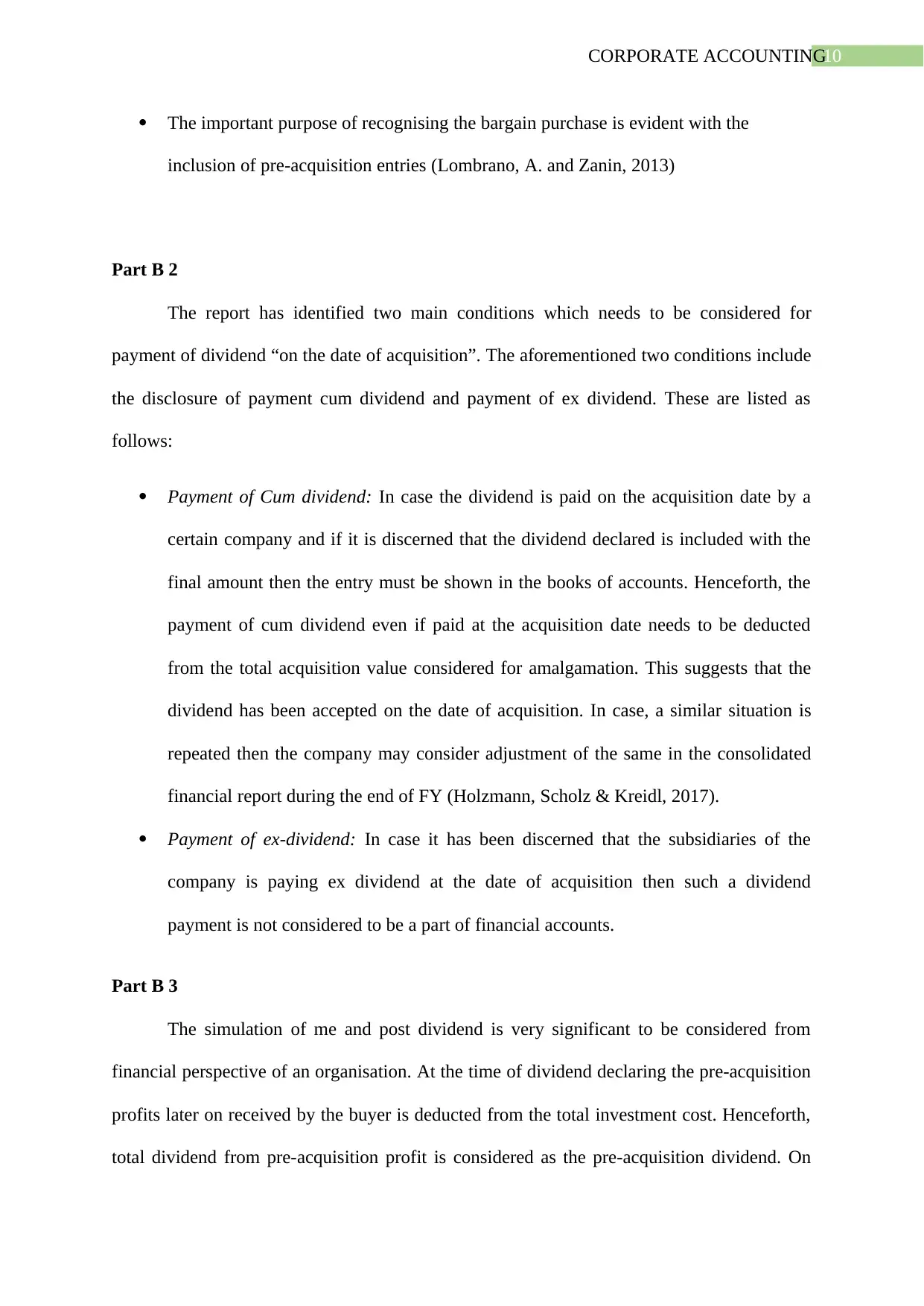

The sustainability efforts have concentrated on most significant issues associated to

reaching to more than 63000 people via digital literacy programs and their employees

taking part in more than 8900 volunteering days in the community.

Some of the core sustainability approach of the report have been considered with

Digital futures, environmental solutions, consideration for climate change and energy

and utilising resources efficiently thereby minimising environmental footprints in the

value chain (Ben-Amar, Chang & McIlkenny, 2017)

The non-financial disclosure about sustainability engagement is depicted below as

follows:

The sustainability efforts have concentrated on most significant issues associated to

reaching to more than 63000 people via digital literacy programs and their employees

taking part in more than 8900 volunteering days in the community.

Some of the core sustainability approach of the report have been considered with

Digital futures, environmental solutions, consideration for climate change and energy

and utilising resources efficiently thereby minimising environmental footprints in the

value chain (Ben-Amar, Chang & McIlkenny, 2017)

The non-financial disclosure about sustainability engagement is depicted below as

follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

Part A 2

Telstra corporations have made comprehensive and robust disclosure in the report

which have considered several aspects of the performance aspects. Being a

telecommunications company, it has considered for various concerns for the society and

community at large. Some of the important disclosures of these aspects have been listed

below as follows:

“Digital Future”

“Environmental Solutions”

Part A 2

Telstra corporations have made comprehensive and robust disclosure in the report

which have considered several aspects of the performance aspects. Being a

telecommunications company, it has considered for various concerns for the society and

community at large. Some of the important disclosures of these aspects have been listed

below as follows:

“Digital Future”

“Environmental Solutions”

8CORPORATE ACCOUNTING

“Responsible Business”

“Ethics and Governance”

“Culture and Capabilities”

“Environmental and Resource Efficiency”

“Networks”

“Tech for Good”

“Everyone Connected initiative”

It is to be discerned that the company has provided sufficient disclosures about each

of the relevant topics as mentioned in the above excerpt. Whether it is information regarding

climate change or considering the needs of culture and capabilities the company has produced

significant amount of disclosure in the major environmental segments. Additionally, the

efficiency in the disclosure of efforts associated with climate change and energy have been

clearly stated with mitigating the climate change impacts and helping the stakeholders and

communities to achieve the same. Some of the various initiatives for maintaining ethics and

governance has been duly depicted with the consideration of transparency in doing business.

The culture and Ability concept is taken into consideration with creating a world-class

workplace for the people (Diouf & Boiral, 2017).

Part A 3

Based on the financial statement of the company, the management has adhered to the

following disclosures in the annual report as per:

Telstra corporations is particularly ensured that the disclosure of the annual

statements is accurate, user-friendly and consists of adequate representation

encompassing all the vital criteria’s. This is essential for the company to consider a

“Responsible Business”

“Ethics and Governance”

“Culture and Capabilities”

“Environmental and Resource Efficiency”

“Networks”

“Tech for Good”

“Everyone Connected initiative”

It is to be discerned that the company has provided sufficient disclosures about each

of the relevant topics as mentioned in the above excerpt. Whether it is information regarding

climate change or considering the needs of culture and capabilities the company has produced

significant amount of disclosure in the major environmental segments. Additionally, the

efficiency in the disclosure of efforts associated with climate change and energy have been

clearly stated with mitigating the climate change impacts and helping the stakeholders and

communities to achieve the same. Some of the various initiatives for maintaining ethics and

governance has been duly depicted with the consideration of transparency in doing business.

The culture and Ability concept is taken into consideration with creating a world-class

workplace for the people (Diouf & Boiral, 2017).

Part A 3

Based on the financial statement of the company, the management has adhered to the

following disclosures in the annual report as per:

Telstra corporations is particularly ensured that the disclosure of the annual

statements is accurate, user-friendly and consists of adequate representation

encompassing all the vital criteria’s. This is essential for the company to consider a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE ACCOUNTING

robust and pictorial presentation of information as to say that the financial

performance along with considering biodiversity and environmental reports. The

reporting will be considered successful only when the users of financial statement will

be able to understand the exact disclosures made by the company. Additionally, the

company should consider adding more number of graphs beside pictorial presentation

of data (Ina and Adriana, 2013).

It is also recommended for Telstra corporations to exhibit the environmental impact

and climate change disclosures in a more quantitative manner by the inclusion of

tables and graphs. This consideration will benefit the users in having a better

understanding of different aspects of the financial perspectives. In addition to this,

Telstra should provide more previous information on the environmental and

sustainability report for increasing the comparability aspect. For instance, the

environmental disclosure along with climate change initiatives for a particular

financial year can be represented in a tabular form which will show the various

implications of previous year as well. Additionally, the company needs to consider

comparing the data by taking into account the health hazards in the nearby area which

are involved with network towers (Kraft, 2014).

Part B 1

The different types of important consideration for the pre-acquisition entries have

been stated below as follows:

Pre-acquisition entries are conducive in preventing any instance of “double counting

of assets”

The pre-acquisition entries are also conducive vital in preventing any instance of

“double counting” associated with the equities of the concerned organisation

robust and pictorial presentation of information as to say that the financial

performance along with considering biodiversity and environmental reports. The

reporting will be considered successful only when the users of financial statement will

be able to understand the exact disclosures made by the company. Additionally, the

company should consider adding more number of graphs beside pictorial presentation

of data (Ina and Adriana, 2013).

It is also recommended for Telstra corporations to exhibit the environmental impact

and climate change disclosures in a more quantitative manner by the inclusion of

tables and graphs. This consideration will benefit the users in having a better

understanding of different aspects of the financial perspectives. In addition to this,

Telstra should provide more previous information on the environmental and

sustainability report for increasing the comparability aspect. For instance, the

environmental disclosure along with climate change initiatives for a particular

financial year can be represented in a tabular form which will show the various

implications of previous year as well. Additionally, the company needs to consider

comparing the data by taking into account the health hazards in the nearby area which

are involved with network towers (Kraft, 2014).

Part B 1

The different types of important consideration for the pre-acquisition entries have

been stated below as follows:

Pre-acquisition entries are conducive in preventing any instance of “double counting

of assets”

The pre-acquisition entries are also conducive vital in preventing any instance of

“double counting” associated with the equities of the concerned organisation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE ACCOUNTING

The important purpose of recognising the bargain purchase is evident with the

inclusion of pre-acquisition entries (Lombrano, A. and Zanin, 2013)

Part B 2

The report has identified two main conditions which needs to be considered for

payment of dividend “on the date of acquisition”. The aforementioned two conditions include

the disclosure of payment cum dividend and payment of ex dividend. These are listed as

follows:

Payment of Cum dividend: In case the dividend is paid on the acquisition date by a

certain company and if it is discerned that the dividend declared is included with the

final amount then the entry must be shown in the books of accounts. Henceforth, the

payment of cum dividend even if paid at the acquisition date needs to be deducted

from the total acquisition value considered for amalgamation. This suggests that the

dividend has been accepted on the date of acquisition. In case, a similar situation is

repeated then the company may consider adjustment of the same in the consolidated

financial report during the end of FY (Holzmann, Scholz & Kreidl, 2017).

Payment of ex-dividend: In case it has been discerned that the subsidiaries of the

company is paying ex dividend at the date of acquisition then such a dividend

payment is not considered to be a part of financial accounts.

Part B 3

The simulation of me and post dividend is very significant to be considered from

financial perspective of an organisation. At the time of dividend declaring the pre-acquisition

profits later on received by the buyer is deducted from the total investment cost. Henceforth,

total dividend from pre-acquisition profit is considered as the pre-acquisition dividend. On

The important purpose of recognising the bargain purchase is evident with the

inclusion of pre-acquisition entries (Lombrano, A. and Zanin, 2013)

Part B 2

The report has identified two main conditions which needs to be considered for

payment of dividend “on the date of acquisition”. The aforementioned two conditions include

the disclosure of payment cum dividend and payment of ex dividend. These are listed as

follows:

Payment of Cum dividend: In case the dividend is paid on the acquisition date by a

certain company and if it is discerned that the dividend declared is included with the

final amount then the entry must be shown in the books of accounts. Henceforth, the

payment of cum dividend even if paid at the acquisition date needs to be deducted

from the total acquisition value considered for amalgamation. This suggests that the

dividend has been accepted on the date of acquisition. In case, a similar situation is

repeated then the company may consider adjustment of the same in the consolidated

financial report during the end of FY (Holzmann, Scholz & Kreidl, 2017).

Payment of ex-dividend: In case it has been discerned that the subsidiaries of the

company is paying ex dividend at the date of acquisition then such a dividend

payment is not considered to be a part of financial accounts.

Part B 3

The simulation of me and post dividend is very significant to be considered from

financial perspective of an organisation. At the time of dividend declaring the pre-acquisition

profits later on received by the buyer is deducted from the total investment cost. Henceforth,

total dividend from pre-acquisition profit is considered as the pre-acquisition dividend. On

11CORPORATE ACCOUNTING

the other hand, post acquisition dividend is credited to the PL account of the company.

Similarly, the dividend received from post-acquisition are termed as post acquisition dividend

(Tauseef and Nishat, 2015).

Part B 4

During the acquisition process, the identifiable net assets are considered for monetary

consideration pertaining to the subsidiary company which has been acquired. Moreover, the

resultant goodwill amount will be duly shown in the books of accounts of subsidiary

organisation, which will not be able to qualify for an identifiable asset of the company. On

the other hand, in the books of account of subsidiary company, the goodwill will not be taken

into account (Chan, Song and Fan, 2016).

In the aforementioned situation, the two methods of computing the goodwill will be

based on “partial goodwill method” and the “full goodwill method”. Additionally, there needs

to be a separate treatment for goodwill which is received from subsidiary company which is

obtained at the date of acquisition taking place. In the partial goodwill method, only that

goodwill which is received from the transaction is recorded, which is received from the

transaction. However, in the full goodwill method, the company considers the goodwill

received from subsidiary as well as on from the transactions. Additionally, the company

depicts the differences between the two which eventually results in goodwill for the parent

company.

Part B 5

In case in the date the parent acquires controlling interest in a subsidiary the carrying

amount are not equal to the fair value then there needs to be specific adjustment made as per

certain process.

the other hand, post acquisition dividend is credited to the PL account of the company.

Similarly, the dividend received from post-acquisition are termed as post acquisition dividend

(Tauseef and Nishat, 2015).

Part B 4

During the acquisition process, the identifiable net assets are considered for monetary

consideration pertaining to the subsidiary company which has been acquired. Moreover, the

resultant goodwill amount will be duly shown in the books of accounts of subsidiary

organisation, which will not be able to qualify for an identifiable asset of the company. On

the other hand, in the books of account of subsidiary company, the goodwill will not be taken

into account (Chan, Song and Fan, 2016).

In the aforementioned situation, the two methods of computing the goodwill will be

based on “partial goodwill method” and the “full goodwill method”. Additionally, there needs

to be a separate treatment for goodwill which is received from subsidiary company which is

obtained at the date of acquisition taking place. In the partial goodwill method, only that

goodwill which is received from the transaction is recorded, which is received from the

transaction. However, in the full goodwill method, the company considers the goodwill

received from subsidiary as well as on from the transactions. Additionally, the company

depicts the differences between the two which eventually results in goodwill for the parent

company.

Part B 5

In case in the date the parent acquires controlling interest in a subsidiary the carrying

amount are not equal to the fair value then there needs to be specific adjustment made as per

certain process.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.