HA2032 - Financial Reporting: Regulation, AASB, and IFRS Impact

VerifiedAdded on 2023/06/07

|20

|3154

|343

Report

AI Summary

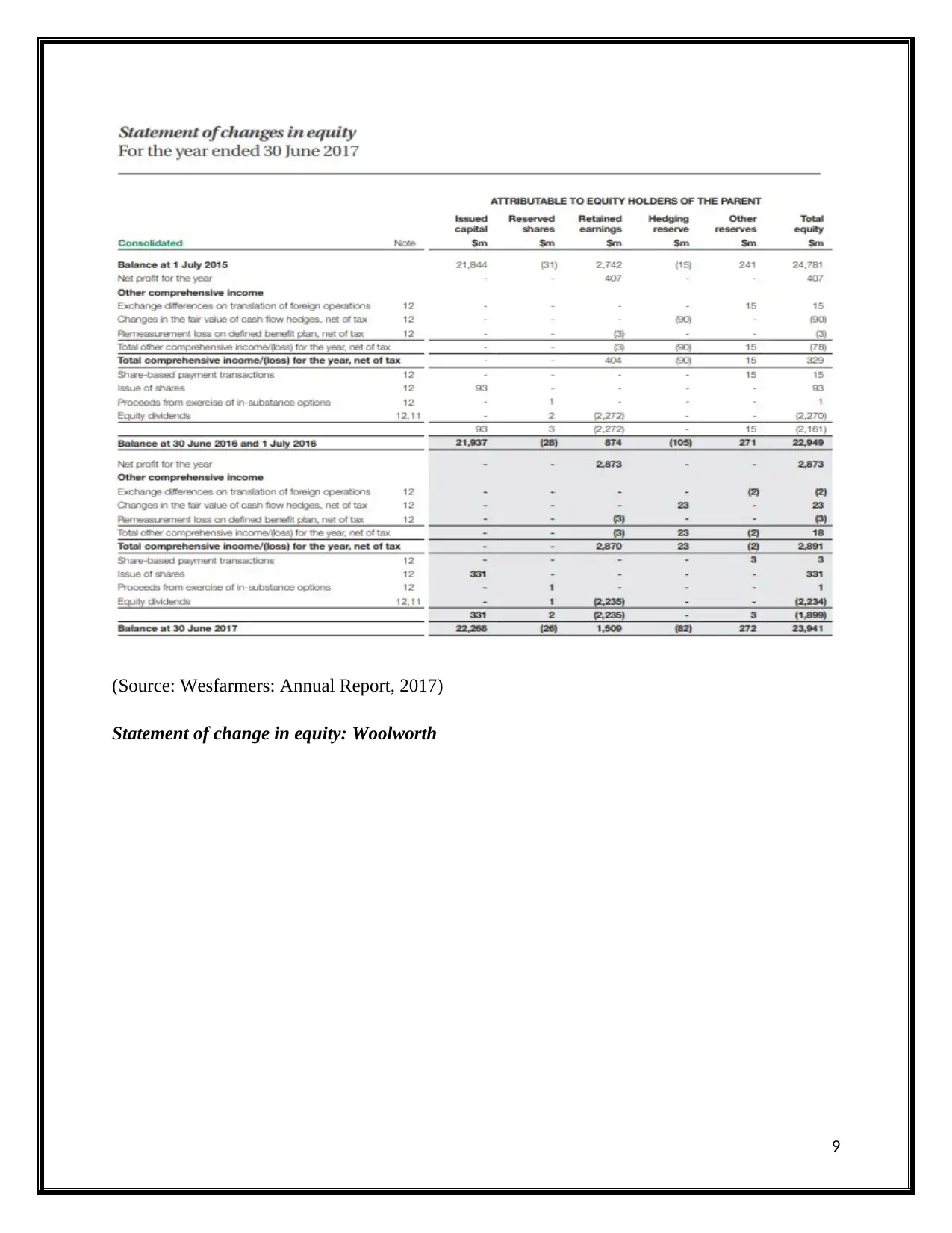

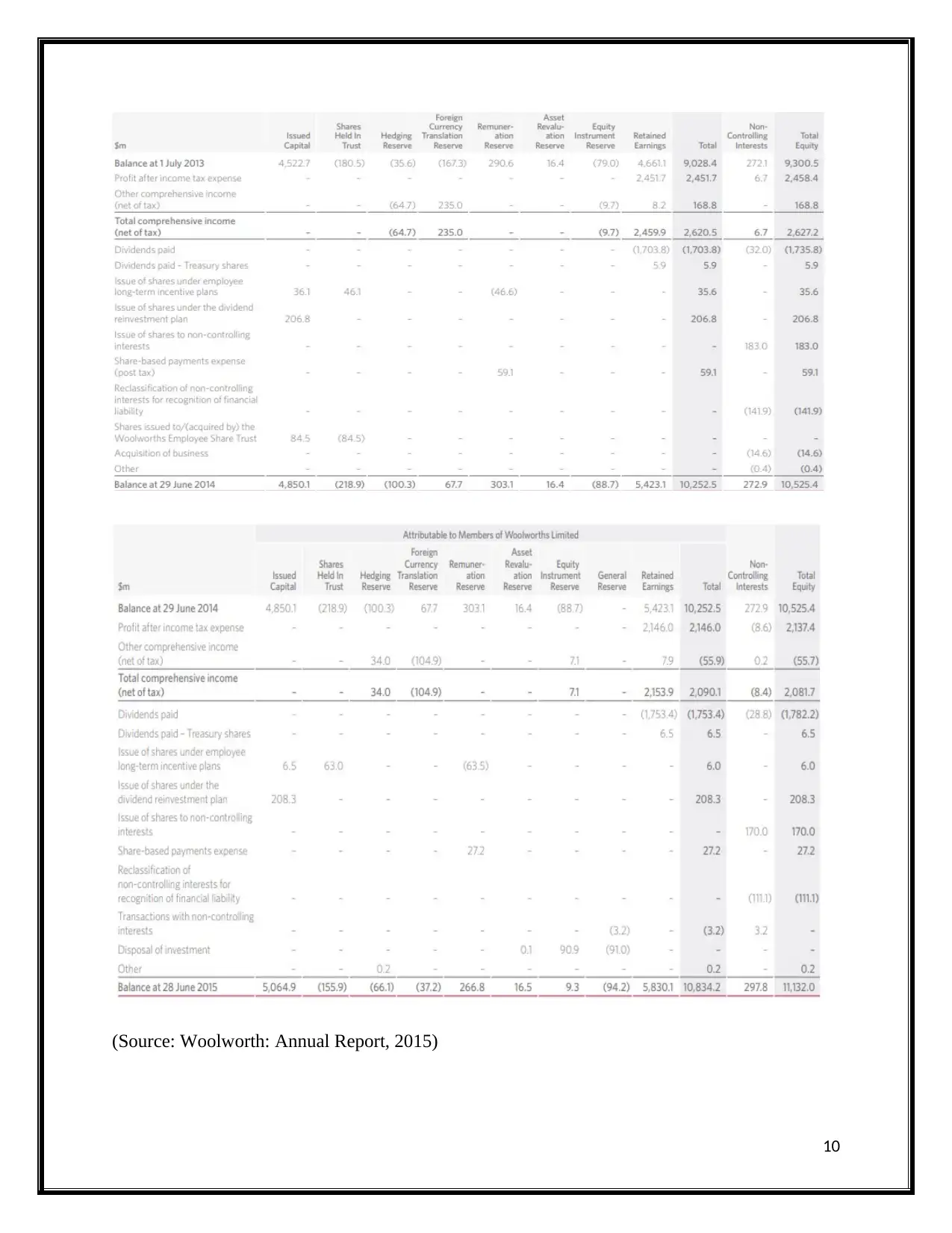

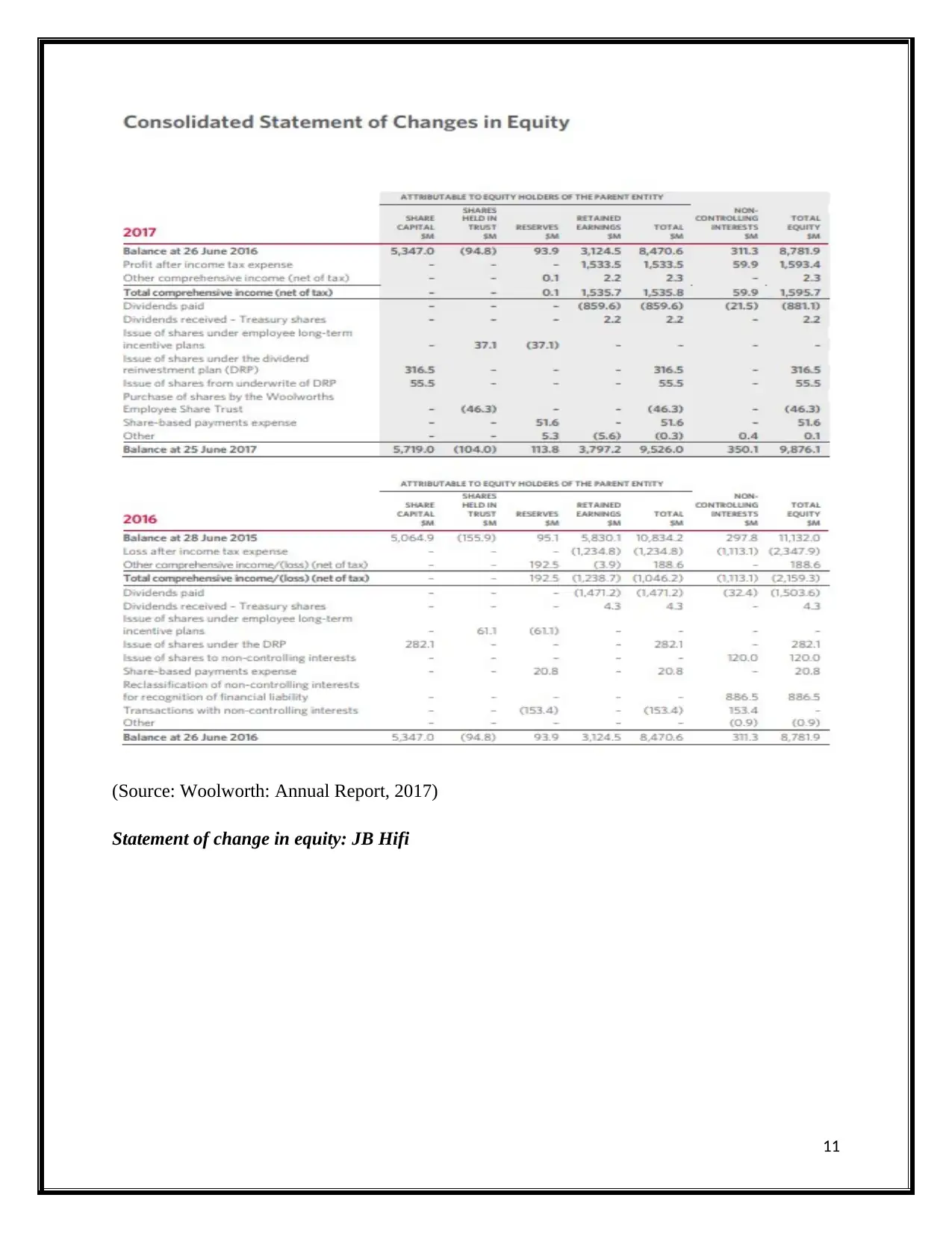

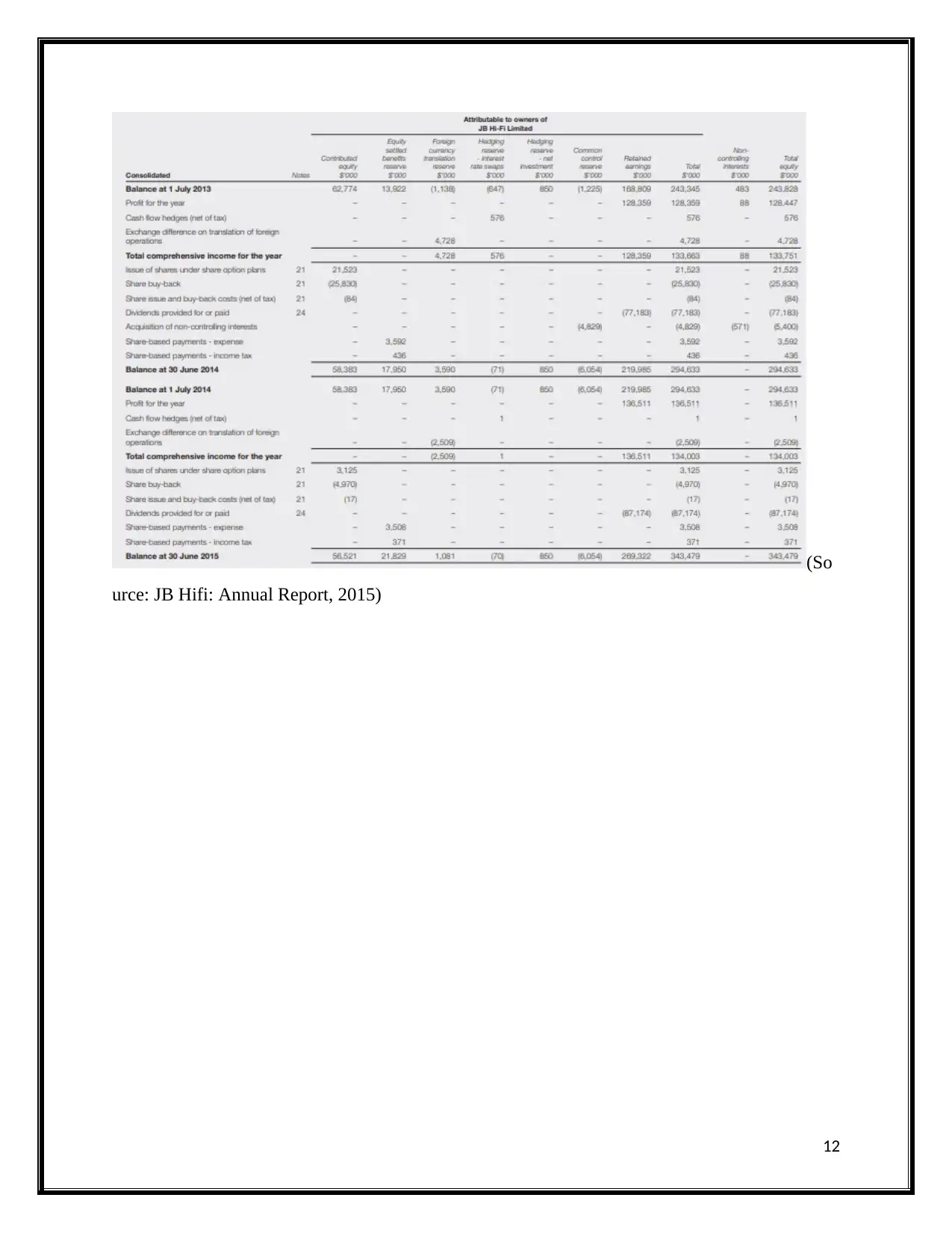

This report critically examines the regulation of financial reporting versus voluntary disclosure, highlighting the roles of accountants and policymakers. It analyzes the Australian Accounting Standards Board's (AASB) participation in global accounting standard-setting, specifically its adoption of International Financial Reporting Standards (IFRS). The report also explores why IFRS adoption isn't compulsory for IASB member countries. Furthermore, it includes a financial statement analysis of four ASX-listed retail companies—Harvey Norman, JB Hi-Fi, Woolworths, and Wesfarmers—focusing on owner's equity and changes in equity over four years. Finally, a comparative analysis of debt and equity capital across these companies is presented, providing a comprehensive overview of their financial structures. Desklib provides access to similar solved assignments and past papers.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.