Corporate and Financial Reporting: Analysis of Business Acquisitions

VerifiedAdded on 2022/10/19

|11

|3189

|198

Report

AI Summary

This report delves into the complexities of corporate and financial reporting, specifically focusing on business acquisitions and consolidations. It examines the accounting treatments involved in acquisitions, including the selection between consolidated and equity methods, with detailed examples of journal entries. The report explores intragroup transactions, emphasizing the treatment of unrealized profits and the necessary adjustments to ensure accurate financial reporting. Furthermore, it addresses the impact of disclosures related to non-controlling interests in consolidated financial statements, providing insights into the presentation and compliance requirements. The analysis covers key aspects such as the recognition and measurement of unrealized revenue, intercompany transactions, and the disclosure requirements for parent companies when preparing consolidated financial statements, making it a comprehensive resource for understanding financial reporting in the context of business acquisitions.

Running head: CORPORATE AND FINANCIAL REPORTING

Corporate and Financial Reporting

Name of the Student:

Name of the University:

Author’s Note

Corporate and Financial Reporting

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CORPORATE AND FINANCIAL REPORTING

Executive Summary

The main objective behind this assessment is to analyse the accounting treatments

which takes place when a business acquires another business. The discussion below

shows the presentation and compliance requirements which is necessary for preparing

the consolidated financial statement of the business. The assessment would also be

dealing with the treatment of unrealised profits and how the same are represented in the

annual reports of the business. The assessment mentions the recognition and

measurement criteria of unrealise revenue. The assessment would also be dealing with

intragroup transactions and also with disclosure requirements which the parent

company must adhere to while preparing the consolidated financial statements.

CORPORATE AND FINANCIAL REPORTING

Executive Summary

The main objective behind this assessment is to analyse the accounting treatments

which takes place when a business acquires another business. The discussion below

shows the presentation and compliance requirements which is necessary for preparing

the consolidated financial statement of the business. The assessment would also be

dealing with the treatment of unrealised profits and how the same are represented in the

annual reports of the business. The assessment mentions the recognition and

measurement criteria of unrealise revenue. The assessment would also be dealing with

intragroup transactions and also with disclosure requirements which the parent

company must adhere to while preparing the consolidated financial statements.

2

CORPORATE AND FINANCIAL REPORTING

Table of Contents

Introduction........................................................................................................................3

Consolidated and Equity Method of Accounting................................................................3

Intragroup Transactions.....................................................................................................5

Impact of Disclosures of Non-controlling Interest in Consolidated Financial Statement. .7

Conclusion.........................................................................................................................8

Reference..........................................................................................................................9

CORPORATE AND FINANCIAL REPORTING

Table of Contents

Introduction........................................................................................................................3

Consolidated and Equity Method of Accounting................................................................3

Intragroup Transactions.....................................................................................................5

Impact of Disclosures of Non-controlling Interest in Consolidated Financial Statement. .7

Conclusion.........................................................................................................................8

Reference..........................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CORPORATE AND FINANCIAL REPORTING

Introduction

The main purpose of the assessment is to conduct a detailed analysis on the

topic of acquisition and takeovers in which major businesses are engaged in modern

era. The assessment considers the various accounting treatments and disclosures

which are required to be portrayed in the annual report when a business acquisition

takes place. The assessment represents the case of acquisition which was undertaken

by JKY ltd of the business of FAB ltd. The assessment would be subdivided into three

parts. The first part would deal with different methods which are available in particular

the consolidation accounting and equity accounting along with proper examples relating

to the same (Robinson et al. 2015). The second part would deal with intragroup

transactions which forms an important part of consolidation would be shown with proper

examples representing the same. The last part would be dealing with disclosures which

a business need to show for treatment of non-controlling interest in the consolidated

financial statements which is prepared by the business.

Consolidated and Equity Method of Accounting

In case of Business takeover or merger, one of the key consideration which the

management of the acquirer company needs to select appropriate acquisition strategy

which is to be followed by the business. In the case provided, the management of JKY

ltd needs to select an appropriate strategy for acquiring the business of FAB ltd. The

options which are available to the management is either consolidated accounting

method or equity accounting method for the purpose of reporting the same in the

financial reports which is prepared by the business (Müller 2014). The method which is

to be selected would be determined from the way financial reports demonstrate the

partnership. It is a known fact that the difference which is present is in the methodology

which is followed by respective businesses.

Consolidation method of accounting:

The consolidated method of accounting is a process of accounting which

effectively measures the assets and liabilities of the subsidiary business and the same

is shown in a combined manner in the balance sheet of the acquirer company. The

consolidated method of accounting effectively organizes the assets and liabilities of the

subsidiary company and record the same in the financial statement of its own. The

provisions which are stated under Paragraph B86 of AASB 10”, show that the items

which are mainly equity, assets, liabilities, cash flows, income and expenses of the

acquirer company for the purpose of reporting and the same is combined with the

values which are shown in the balance sheet of the subsidiary company. The method

also offsets any investments values which might be there between the parent company

and the subsidiary company. In addition to this, intercompany transactions are not

considered while preparing the consolidated financial statements of the business. This

is done so that there is no double counting situation thereby ensuring that the

consolidated financial statement which is prepared is showing accurate view of the

financial information of both the companies.

CORPORATE AND FINANCIAL REPORTING

Introduction

The main purpose of the assessment is to conduct a detailed analysis on the

topic of acquisition and takeovers in which major businesses are engaged in modern

era. The assessment considers the various accounting treatments and disclosures

which are required to be portrayed in the annual report when a business acquisition

takes place. The assessment represents the case of acquisition which was undertaken

by JKY ltd of the business of FAB ltd. The assessment would be subdivided into three

parts. The first part would deal with different methods which are available in particular

the consolidation accounting and equity accounting along with proper examples relating

to the same (Robinson et al. 2015). The second part would deal with intragroup

transactions which forms an important part of consolidation would be shown with proper

examples representing the same. The last part would be dealing with disclosures which

a business need to show for treatment of non-controlling interest in the consolidated

financial statements which is prepared by the business.

Consolidated and Equity Method of Accounting

In case of Business takeover or merger, one of the key consideration which the

management of the acquirer company needs to select appropriate acquisition strategy

which is to be followed by the business. In the case provided, the management of JKY

ltd needs to select an appropriate strategy for acquiring the business of FAB ltd. The

options which are available to the management is either consolidated accounting

method or equity accounting method for the purpose of reporting the same in the

financial reports which is prepared by the business (Müller 2014). The method which is

to be selected would be determined from the way financial reports demonstrate the

partnership. It is a known fact that the difference which is present is in the methodology

which is followed by respective businesses.

Consolidation method of accounting:

The consolidated method of accounting is a process of accounting which

effectively measures the assets and liabilities of the subsidiary business and the same

is shown in a combined manner in the balance sheet of the acquirer company. The

consolidated method of accounting effectively organizes the assets and liabilities of the

subsidiary company and record the same in the financial statement of its own. The

provisions which are stated under Paragraph B86 of AASB 10”, show that the items

which are mainly equity, assets, liabilities, cash flows, income and expenses of the

acquirer company for the purpose of reporting and the same is combined with the

values which are shown in the balance sheet of the subsidiary company. The method

also offsets any investments values which might be there between the parent company

and the subsidiary company. In addition to this, intercompany transactions are not

considered while preparing the consolidated financial statements of the business. This

is done so that there is no double counting situation thereby ensuring that the

consolidated financial statement which is prepared is showing accurate view of the

financial information of both the companies.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CORPORATE AND FINANCIAL REPORTING

The provisions of “Paragraph B88 of AASB 10” covers the measurement criteria which

is to be followed for different items which are presented in the financial statements of

the business. The income and expenses of the subsidiary is based on the amount which

is received for the assets and liabilities realised at the date of acquisition of the

business. The provisions of “Paragraph 32 of AASB 3” provides an explanation relating

to goodwill recognition of the business (Aasb.gov.au. 2019). The criteria which is to be

followed are based on the higher of the two figure which is shown below:

a. The aggregate of the two:

The transfer of consideration estimated s per the guidelines of AASB 3 which

requires fair value at the acquisition date.

The value of the non-controlling interest of the subsidiary as per the requirements

of the standard

In case of business combination established in stages, the fair value of the equity

interest held in past in the subsidiary by the parent company at the fair value of

the acquisition date

b. The assets and the liabilities at their net figures which are estimated complying to

the requirements of the standard.

Examples

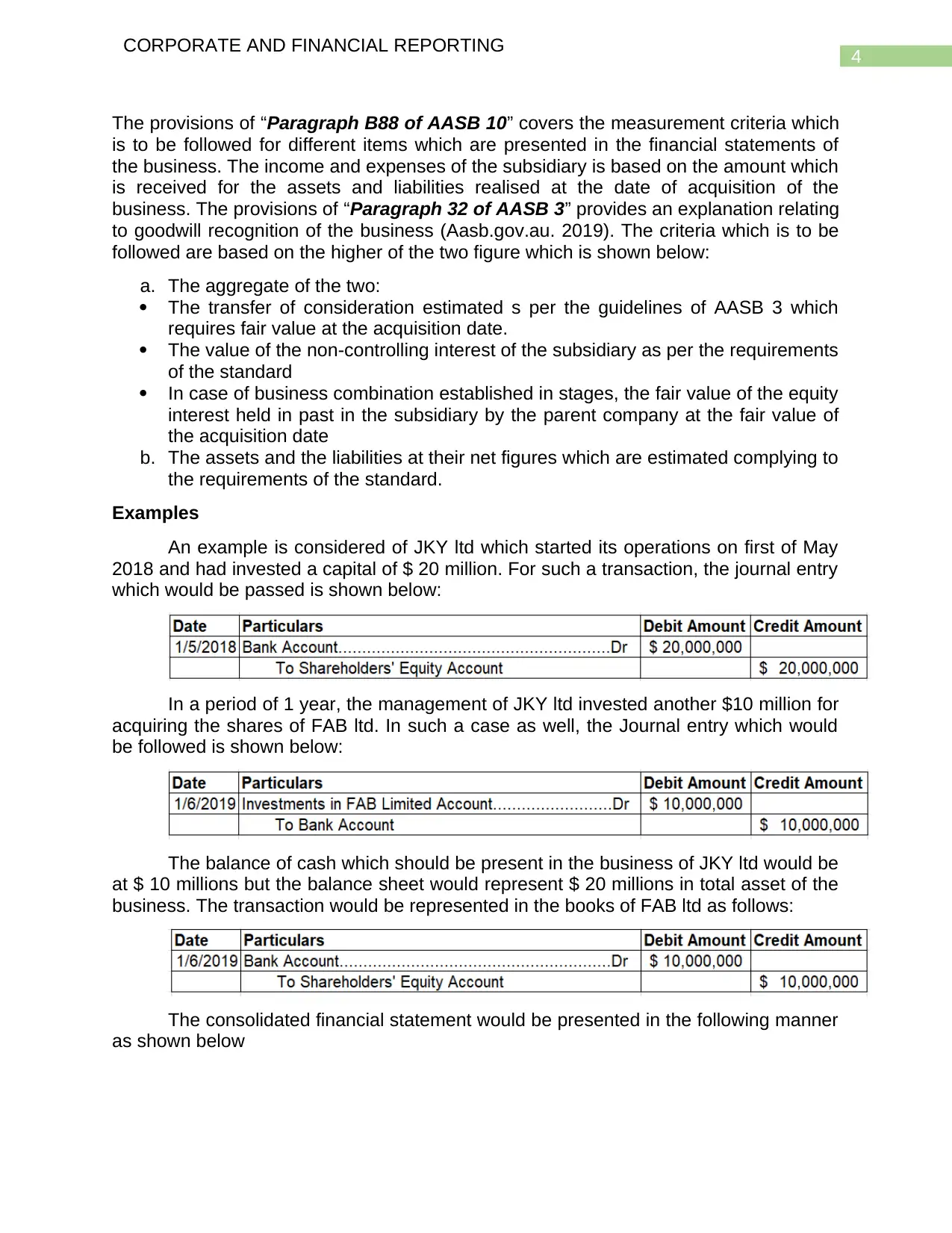

An example is considered of JKY ltd which started its operations on first of May

2018 and had invested a capital of $ 20 million. For such a transaction, the journal entry

which would be passed is shown below:

In a period of 1 year, the management of JKY ltd invested another $10 million for

acquiring the shares of FAB ltd. In such a case as well, the Journal entry which would

be followed is shown below:

The balance of cash which should be present in the business of JKY ltd would be

at $ 10 millions but the balance sheet would represent $ 20 millions in total asset of the

business. The transaction would be represented in the books of FAB ltd as follows:

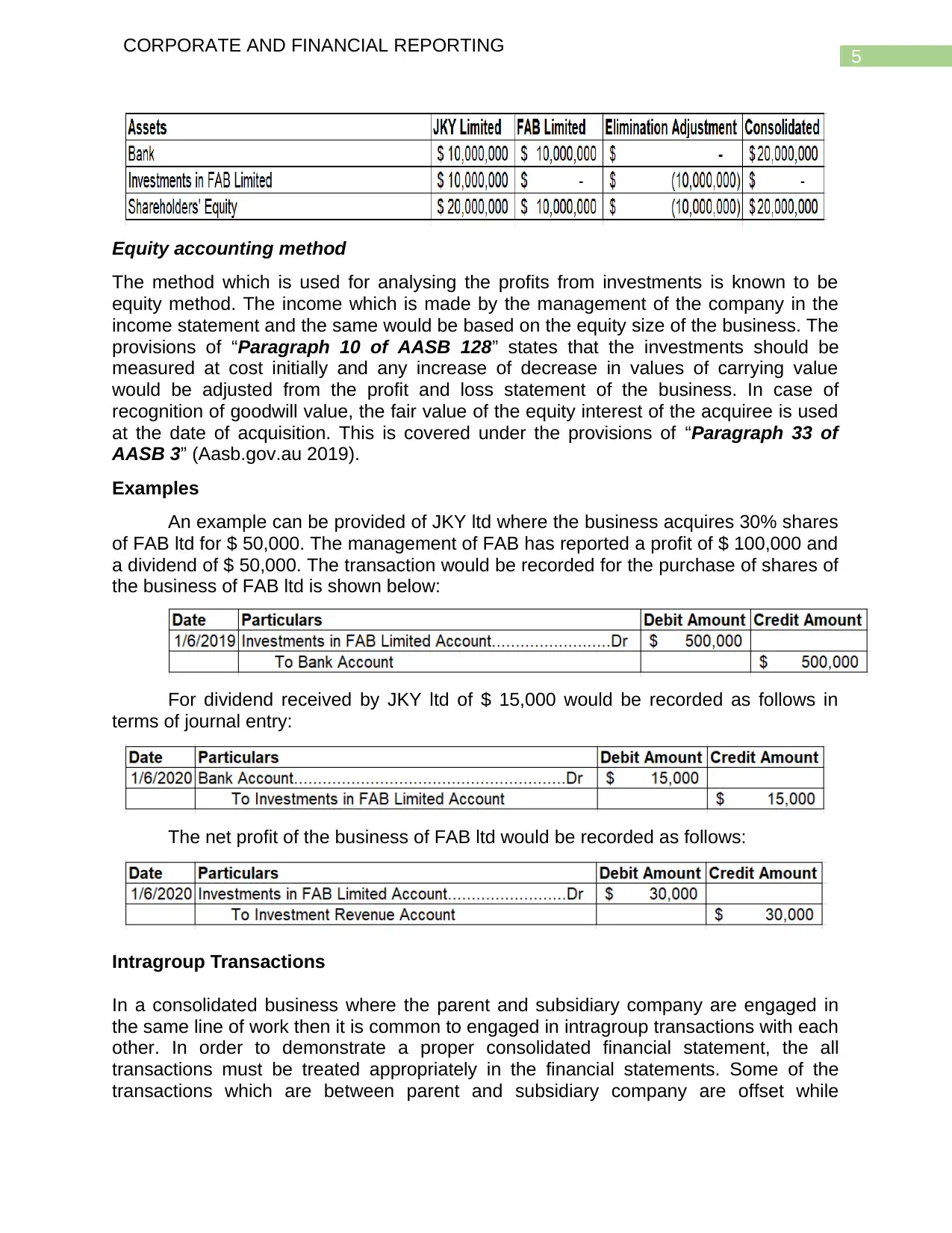

The consolidated financial statement would be presented in the following manner

as shown below

CORPORATE AND FINANCIAL REPORTING

The provisions of “Paragraph B88 of AASB 10” covers the measurement criteria which

is to be followed for different items which are presented in the financial statements of

the business. The income and expenses of the subsidiary is based on the amount which

is received for the assets and liabilities realised at the date of acquisition of the

business. The provisions of “Paragraph 32 of AASB 3” provides an explanation relating

to goodwill recognition of the business (Aasb.gov.au. 2019). The criteria which is to be

followed are based on the higher of the two figure which is shown below:

a. The aggregate of the two:

The transfer of consideration estimated s per the guidelines of AASB 3 which

requires fair value at the acquisition date.

The value of the non-controlling interest of the subsidiary as per the requirements

of the standard

In case of business combination established in stages, the fair value of the equity

interest held in past in the subsidiary by the parent company at the fair value of

the acquisition date

b. The assets and the liabilities at their net figures which are estimated complying to

the requirements of the standard.

Examples

An example is considered of JKY ltd which started its operations on first of May

2018 and had invested a capital of $ 20 million. For such a transaction, the journal entry

which would be passed is shown below:

In a period of 1 year, the management of JKY ltd invested another $10 million for

acquiring the shares of FAB ltd. In such a case as well, the Journal entry which would

be followed is shown below:

The balance of cash which should be present in the business of JKY ltd would be

at $ 10 millions but the balance sheet would represent $ 20 millions in total asset of the

business. The transaction would be represented in the books of FAB ltd as follows:

The consolidated financial statement would be presented in the following manner

as shown below

5

CORPORATE AND FINANCIAL REPORTING

Equity accounting method

The method which is used for analysing the profits from investments is known to be

equity method. The income which is made by the management of the company in the

income statement and the same would be based on the equity size of the business. The

provisions of “Paragraph 10 of AASB 128” states that the investments should be

measured at cost initially and any increase of decrease in values of carrying value

would be adjusted from the profit and loss statement of the business. In case of

recognition of goodwill value, the fair value of the equity interest of the acquiree is used

at the date of acquisition. This is covered under the provisions of “Paragraph 33 of

AASB 3” (Aasb.gov.au 2019).

Examples

An example can be provided of JKY ltd where the business acquires 30% shares

of FAB ltd for $ 50,000. The management of FAB has reported a profit of $ 100,000 and

a dividend of $ 50,000. The transaction would be recorded for the purchase of shares of

the business of FAB ltd is shown below:

For dividend received by JKY ltd of $ 15,000 would be recorded as follows in

terms of journal entry:

The net profit of the business of FAB ltd would be recorded as follows:

Intragroup Transactions

In a consolidated business where the parent and subsidiary company are engaged in

the same line of work then it is common to engaged in intragroup transactions with each

other. In order to demonstrate a proper consolidated financial statement, the all

transactions must be treated appropriately in the financial statements. Some of the

transactions which are between parent and subsidiary company are offset while

CORPORATE AND FINANCIAL REPORTING

Equity accounting method

The method which is used for analysing the profits from investments is known to be

equity method. The income which is made by the management of the company in the

income statement and the same would be based on the equity size of the business. The

provisions of “Paragraph 10 of AASB 128” states that the investments should be

measured at cost initially and any increase of decrease in values of carrying value

would be adjusted from the profit and loss statement of the business. In case of

recognition of goodwill value, the fair value of the equity interest of the acquiree is used

at the date of acquisition. This is covered under the provisions of “Paragraph 33 of

AASB 3” (Aasb.gov.au 2019).

Examples

An example can be provided of JKY ltd where the business acquires 30% shares

of FAB ltd for $ 50,000. The management of FAB has reported a profit of $ 100,000 and

a dividend of $ 50,000. The transaction would be recorded for the purchase of shares of

the business of FAB ltd is shown below:

For dividend received by JKY ltd of $ 15,000 would be recorded as follows in

terms of journal entry:

The net profit of the business of FAB ltd would be recorded as follows:

Intragroup Transactions

In a consolidated business where the parent and subsidiary company are engaged in

the same line of work then it is common to engaged in intragroup transactions with each

other. In order to demonstrate a proper consolidated financial statement, the all

transactions must be treated appropriately in the financial statements. Some of the

transactions which are between parent and subsidiary company are offset while

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CORPORATE AND FINANCIAL REPORTING

preparing the consolidated financial statement of the business. The provisions of,

“Paragraph 29 of AASB 127” covers intragroup transaction and the section states that

income and expenses between parent and subsidiary company needs to be cancelled

out while reporting the same in the annual reports (Aasb.gov.au. 2019). Some examples

of intragroup transactions are listed below:

Payment of Management fee to a member of the group

Dividend payments to members of the group

Intra-group inventory sale

Intra-group non-current asset sale

Intra-group loans

The adjustments which are made in the consolidated financial statements should

be in a manner that actual accounting entries are reversed so that the same cancels out

the transactions which are provided in the consolidated annual report of the business.

The case which is shown represent a purchase agreement which was

established between JKY Ltd and one of its subsidiaries which was partially owned. The

purchase was made for inventory. Th revenue can only be recognised in case of

inventory when the same is actually sold to an external party by the subsidiary

business. This results in generation of unrealised profits which must not be shown in the

consolidated books of accounts (Cîrstea 2014). The case shows that unrealised profits

are created when sales is made within the group and actual sale is not made to an

external party. The provisions of “Paragraph 25 of AASB 127” states that in case of

intragroup transaction unrealised profits would be shown in the balance sheet under the

head of non-current assets while at the same time inventory value is eliminated

(Aasb.gov.au. 2019).

The case which provided in the assessment shows that JKY ltd has purchased

inventory from a partially owned subsidiary. The sale which is made can be assumed to

be carrying some element of profit. When JKY ltd sells the inventory to final customer

then the profits can be established and the unrealised profits can then be settled. Until

then the management of partially owned subsidiary should record the same as

unrealised profits in the financial statements. For the purpose of clarity, lets assume that

JKY ltd purchased the inventory at a price of $ 14,000 and the mark up which was set

by the partially owned subsidiary was 40%. Thus, the profit from the sale of inventory

can be estimated to be $ 4,000 (14,000*40/140). Therefore, from the point of view of

business, the profits are overstated and appropriate adjustments would be necessary to

cancel out the unrealised profits of the business. The journal entry which would be

passed for making the adjustment of $ 4,000is shown below:

Consolidated Profit Account......................................Dr $4,000

To Consolidated Inventory Account $4,000

The above journal entry would make the appropriate changes in the consolidated

financial statements and eradicate the unrealised profits. The profits which are which

are to be shown in the non-controlling interest of the business would be treated

differently. One of the approach is that the non-controlling interest would be assigned a

CORPORATE AND FINANCIAL REPORTING

preparing the consolidated financial statement of the business. The provisions of,

“Paragraph 29 of AASB 127” covers intragroup transaction and the section states that

income and expenses between parent and subsidiary company needs to be cancelled

out while reporting the same in the annual reports (Aasb.gov.au. 2019). Some examples

of intragroup transactions are listed below:

Payment of Management fee to a member of the group

Dividend payments to members of the group

Intra-group inventory sale

Intra-group non-current asset sale

Intra-group loans

The adjustments which are made in the consolidated financial statements should

be in a manner that actual accounting entries are reversed so that the same cancels out

the transactions which are provided in the consolidated annual report of the business.

The case which is shown represent a purchase agreement which was

established between JKY Ltd and one of its subsidiaries which was partially owned. The

purchase was made for inventory. Th revenue can only be recognised in case of

inventory when the same is actually sold to an external party by the subsidiary

business. This results in generation of unrealised profits which must not be shown in the

consolidated books of accounts (Cîrstea 2014). The case shows that unrealised profits

are created when sales is made within the group and actual sale is not made to an

external party. The provisions of “Paragraph 25 of AASB 127” states that in case of

intragroup transaction unrealised profits would be shown in the balance sheet under the

head of non-current assets while at the same time inventory value is eliminated

(Aasb.gov.au. 2019).

The case which provided in the assessment shows that JKY ltd has purchased

inventory from a partially owned subsidiary. The sale which is made can be assumed to

be carrying some element of profit. When JKY ltd sells the inventory to final customer

then the profits can be established and the unrealised profits can then be settled. Until

then the management of partially owned subsidiary should record the same as

unrealised profits in the financial statements. For the purpose of clarity, lets assume that

JKY ltd purchased the inventory at a price of $ 14,000 and the mark up which was set

by the partially owned subsidiary was 40%. Thus, the profit from the sale of inventory

can be estimated to be $ 4,000 (14,000*40/140). Therefore, from the point of view of

business, the profits are overstated and appropriate adjustments would be necessary to

cancel out the unrealised profits of the business. The journal entry which would be

passed for making the adjustment of $ 4,000is shown below:

Consolidated Profit Account......................................Dr $4,000

To Consolidated Inventory Account $4,000

The above journal entry would make the appropriate changes in the consolidated

financial statements and eradicate the unrealised profits. The profits which are which

are to be shown in the non-controlling interest of the business would be treated

differently. One of the approach is that the non-controlling interest would be assigned a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE AND FINANCIAL REPORTING

proportionate share of unrealised profits. In this way, the entire profits in the selling

entity is eliminated. The second alternative approach is that no portion of unrealised

profits would be shown in the non-controlling interests and the figure of non-controlling

interest depicts entitlement of share capital and reserves associated with the subsidiary.

An assumption can be made that JKY LTD has 80% interest in D ltd and 75%

interest in E ltd. D ltd made sales of good to E ltd for $ 100,000. The original cost of

product was $ 70,000 and the same product was sold by E ltd. The sales were made for

half of the products. When the parent company i.e. JKY ltd prepares the consolidated

financial statements, unrealised profits needs to be eradicated so that proper valuation

of the inventory is shown. The transfer of profit from D Limited to E Limited is made at

$50,000 and the group cost would be $35,000. Therefore, the intra-group profit to be

removed from inventories is $15,000. Here, the application of the first method would

reveal the non-controlling interest of the business to be 20% and the same would be $

3,000 ($ 15,000*20%).

Impact of Disclosures of Non-controlling Interest in Consolidated Financial

Statement

The provisions of “Paragraph 27 of AASB 127” clearly shows that separate

consolidated financial statement shows separate presentation of the non-controlling

interest from the equity of the parent company which is presented in the balance sheet

of the business. The non-controlling interest can be referred to as a part of the equity of

the business of subsidiary company and the same is attributed to the parent company at

the time of consolidation of the business. The standard which is stated above has made

reporting requirements for non-controlling interest much easier. The adjustments which

are made due to incorporation of non-controlling interest are shown in the equity

balances of the parent company. The changes need to be reconciled in the

consolidated financial statements as per the provisions which is stated under

“Paragraph 106 (a) of AASB 101” (Aasb.gov.au 2019). The non-controlling interest

amount need to be identified appropriately. In addition to this, separate presentation of

the non-controlling interest would also ensure that proper explanation is provided to the

shareholders of the business who have a claim on the net assets of the business

(Hoyle, Schaefer and Doupnik 2015). In addition to this, the provisions which are stated

in AASB 101 also requires full and faithful disclosure of the financial information in the

consolidated statements.

Equity transactions could be assessed as a variation in ownership interest of

parent firm in a subsidiary, which does not take place when the parent firm loses control

over the subsidiary. If there is a change in the proportion of equity that is held by non-

controlling interest than the proportion changes altogether and necessary adjustments

need to be made in the carrying values of controlling and non-controlling interest of a

business (Palea 2013). The non-controlling interest along with fair value of

consideration is also recognised for the subsidiary business and the same is attributable

to the parent company which is engaged in consolidation.

Changes needed to ensure the accurate representation of the consolidated

financial statements:

CORPORATE AND FINANCIAL REPORTING

proportionate share of unrealised profits. In this way, the entire profits in the selling

entity is eliminated. The second alternative approach is that no portion of unrealised

profits would be shown in the non-controlling interests and the figure of non-controlling

interest depicts entitlement of share capital and reserves associated with the subsidiary.

An assumption can be made that JKY LTD has 80% interest in D ltd and 75%

interest in E ltd. D ltd made sales of good to E ltd for $ 100,000. The original cost of

product was $ 70,000 and the same product was sold by E ltd. The sales were made for

half of the products. When the parent company i.e. JKY ltd prepares the consolidated

financial statements, unrealised profits needs to be eradicated so that proper valuation

of the inventory is shown. The transfer of profit from D Limited to E Limited is made at

$50,000 and the group cost would be $35,000. Therefore, the intra-group profit to be

removed from inventories is $15,000. Here, the application of the first method would

reveal the non-controlling interest of the business to be 20% and the same would be $

3,000 ($ 15,000*20%).

Impact of Disclosures of Non-controlling Interest in Consolidated Financial

Statement

The provisions of “Paragraph 27 of AASB 127” clearly shows that separate

consolidated financial statement shows separate presentation of the non-controlling

interest from the equity of the parent company which is presented in the balance sheet

of the business. The non-controlling interest can be referred to as a part of the equity of

the business of subsidiary company and the same is attributed to the parent company at

the time of consolidation of the business. The standard which is stated above has made

reporting requirements for non-controlling interest much easier. The adjustments which

are made due to incorporation of non-controlling interest are shown in the equity

balances of the parent company. The changes need to be reconciled in the

consolidated financial statements as per the provisions which is stated under

“Paragraph 106 (a) of AASB 101” (Aasb.gov.au 2019). The non-controlling interest

amount need to be identified appropriately. In addition to this, separate presentation of

the non-controlling interest would also ensure that proper explanation is provided to the

shareholders of the business who have a claim on the net assets of the business

(Hoyle, Schaefer and Doupnik 2015). In addition to this, the provisions which are stated

in AASB 101 also requires full and faithful disclosure of the financial information in the

consolidated statements.

Equity transactions could be assessed as a variation in ownership interest of

parent firm in a subsidiary, which does not take place when the parent firm loses control

over the subsidiary. If there is a change in the proportion of equity that is held by non-

controlling interest than the proportion changes altogether and necessary adjustments

need to be made in the carrying values of controlling and non-controlling interest of a

business (Palea 2013). The non-controlling interest along with fair value of

consideration is also recognised for the subsidiary business and the same is attributable

to the parent company which is engaged in consolidation.

Changes needed to ensure the accurate representation of the consolidated

financial statements:

8

CORPORATE AND FINANCIAL REPORTING

The representation of the financial statement would be depending on the

provisions which are stated under AASB 101. The adjustments which are required to be

made for appropriate presentation of the financial statements would concentrate on

main account treatments. The investments which is made by parent company in the

subsidiary needs to be adjusted or offset and part of equity of the subsidiary needs to

be eliminated. In addition to this, if there are any unrealised profits, then the same also

needs to be eliminated. Any impairment losses for the assets which are to be realised

need to be identified as intragroup losses. While all income and expense need to be

settled between the parent and subsidiary company. There is also a requirement of

keeping the accounting policies of the business same between the parent and

subsidiary company. The treatment of non-controlling interest needs to be properly

done by the business and the same needs to be shown in comprehensive income

statement prepared by the business. In addition, any profit or loss in relation to

subsidiary’s outstanding cumulative preference shares needs to be calculated.

Effects of the required changes on the disclosure requirements

The provisions of “Paragraph 10 of AASB 127”, when a parent company

prepares a consolidated financial statement then it need to account for investments

made in joint ventures which may be at cost or as per AASB 9. Therefore, there exist a

relaxation in accounting policies. However, proper disclosures still need to be presented

in the annual report. The consolidated financial statements have to be developed in

such a manner that the same discloses the nature and degree of any important

limitations arising from the need of regulations on the ability of the subsidiary in

transferring to the parent either through repayment of loans, advances and dividends in

cash.

It is also required for the parent company to disclose the proportion of holdings

that the company has in the subsidiary company. If the parent company does not hold

50% or more of the voting rights than the same must also be disclosed in the

consolidated financial statements.

Conclusion

The above discussion effectively shows the difference in treatments under

consolidation method and equity method and also shows relevance of the accounting

standards in providing appropriate treatment relating to the same. In addition to this, the

treatment of non-controlling interest in a consolidated financial statement would be

analysed so that appropriate treatment and disclosures are provided in the consolidated

financial statements of the business. Moreover, the disclosure requirements for entire

consolidation is discussed above along with situation where unrealised profits arises in

case of intragroup transactions.

CORPORATE AND FINANCIAL REPORTING

The representation of the financial statement would be depending on the

provisions which are stated under AASB 101. The adjustments which are required to be

made for appropriate presentation of the financial statements would concentrate on

main account treatments. The investments which is made by parent company in the

subsidiary needs to be adjusted or offset and part of equity of the subsidiary needs to

be eliminated. In addition to this, if there are any unrealised profits, then the same also

needs to be eliminated. Any impairment losses for the assets which are to be realised

need to be identified as intragroup losses. While all income and expense need to be

settled between the parent and subsidiary company. There is also a requirement of

keeping the accounting policies of the business same between the parent and

subsidiary company. The treatment of non-controlling interest needs to be properly

done by the business and the same needs to be shown in comprehensive income

statement prepared by the business. In addition, any profit or loss in relation to

subsidiary’s outstanding cumulative preference shares needs to be calculated.

Effects of the required changes on the disclosure requirements

The provisions of “Paragraph 10 of AASB 127”, when a parent company

prepares a consolidated financial statement then it need to account for investments

made in joint ventures which may be at cost or as per AASB 9. Therefore, there exist a

relaxation in accounting policies. However, proper disclosures still need to be presented

in the annual report. The consolidated financial statements have to be developed in

such a manner that the same discloses the nature and degree of any important

limitations arising from the need of regulations on the ability of the subsidiary in

transferring to the parent either through repayment of loans, advances and dividends in

cash.

It is also required for the parent company to disclose the proportion of holdings

that the company has in the subsidiary company. If the parent company does not hold

50% or more of the voting rights than the same must also be disclosed in the

consolidated financial statements.

Conclusion

The above discussion effectively shows the difference in treatments under

consolidation method and equity method and also shows relevance of the accounting

standards in providing appropriate treatment relating to the same. In addition to this, the

treatment of non-controlling interest in a consolidated financial statement would be

analysed so that appropriate treatment and disclosures are provided in the consolidated

financial statements of the business. Moreover, the disclosure requirements for entire

consolidation is discussed above along with situation where unrealised profits arises in

case of intragroup transactions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CORPORATE AND FINANCIAL REPORTING

Reference

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15.pdf [Accessed 3 May

2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB128_08-11.pdf [Accessed 3

May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB10_08-11.pdf [Accessed 3 May

2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB127_08-11_COMPjan15_07-

15.pdf [Accessed 3 May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf [Accessed 3

May 2019].

Cîrstea, A., 2014. The need for public sector consolidated financial

statements. Procedia Economics and Finance, 15, pp.1289-1296.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

Müller, V.O., 2014. The impact of IFRS adoption on the quality of consolidated financial

reporting. Procedia-Social and Behavioral Sciences, 109, pp.976-982.

Palea, V., 2013. IAS/IFRS and financial reporting quality: Lessons from the European

experience. China Journal of Accounting Research, 6(4), pp.247-263.

Robinson, T.R., Henry, E., Pirie, W.L. and Broihahn, M.A., 2015. International financial

statement analysis. John Wiley & Sons.

CORPORATE AND FINANCIAL REPORTING

Reference

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15.pdf [Accessed 3 May

2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB128_08-11.pdf [Accessed 3

May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB10_08-11.pdf [Accessed 3 May

2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB127_08-11_COMPjan15_07-

15.pdf [Accessed 3 May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf [Accessed 3

May 2019].

Cîrstea, A., 2014. The need for public sector consolidated financial

statements. Procedia Economics and Finance, 15, pp.1289-1296.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

Müller, V.O., 2014. The impact of IFRS adoption on the quality of consolidated financial

reporting. Procedia-Social and Behavioral Sciences, 109, pp.976-982.

Palea, V., 2013. IAS/IFRS and financial reporting quality: Lessons from the European

experience. China Journal of Accounting Research, 6(4), pp.247-263.

Robinson, T.R., Henry, E., Pirie, W.L. and Broihahn, M.A., 2015. International financial

statement analysis. John Wiley & Sons.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CORPORATE AND FINANCIAL REPORTING

CORPORATE AND FINANCIAL REPORTING

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.