Comprehensive Solutions: Corporate Financial Strategy Module

VerifiedAdded on 2023/06/18

|16

|2513

|241

Homework Assignment

AI Summary

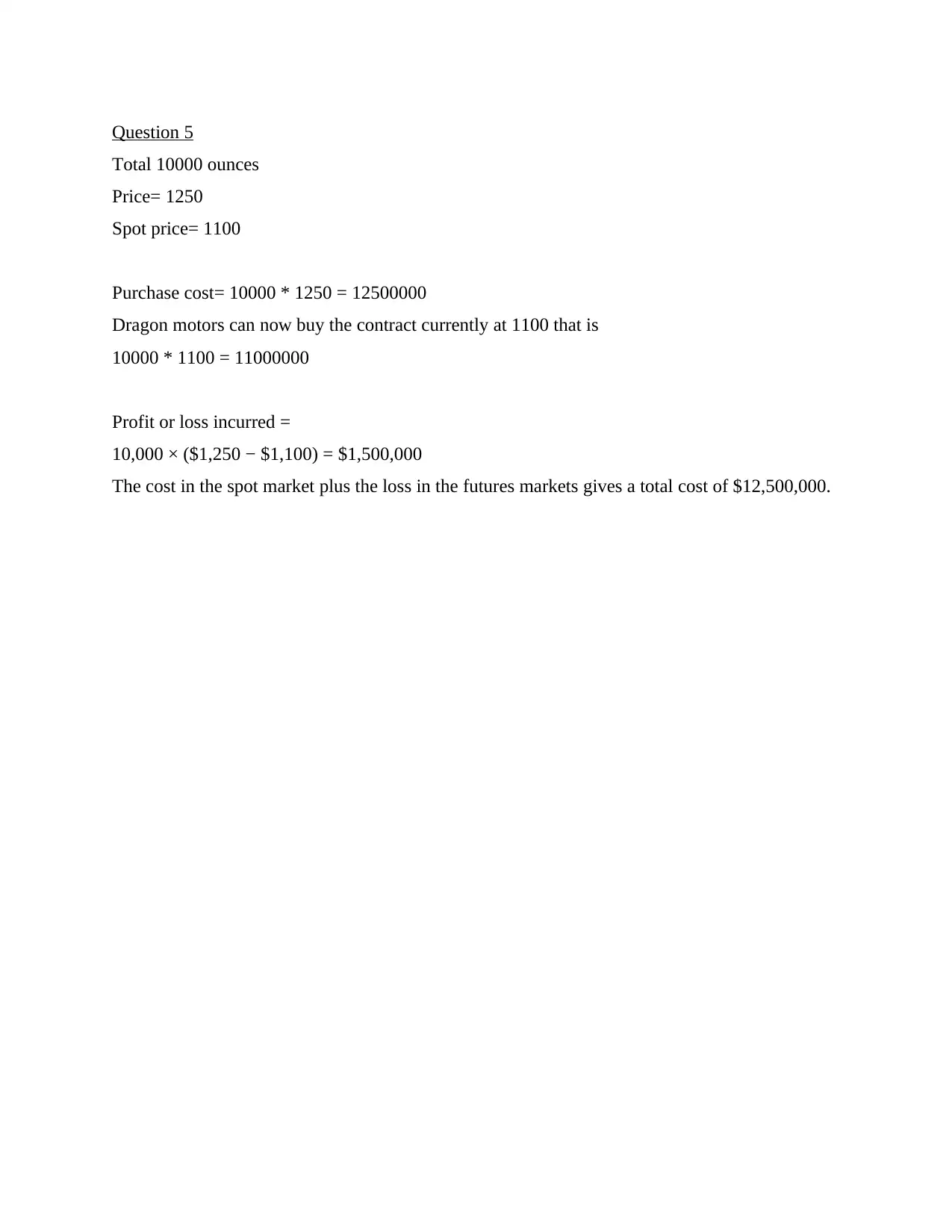

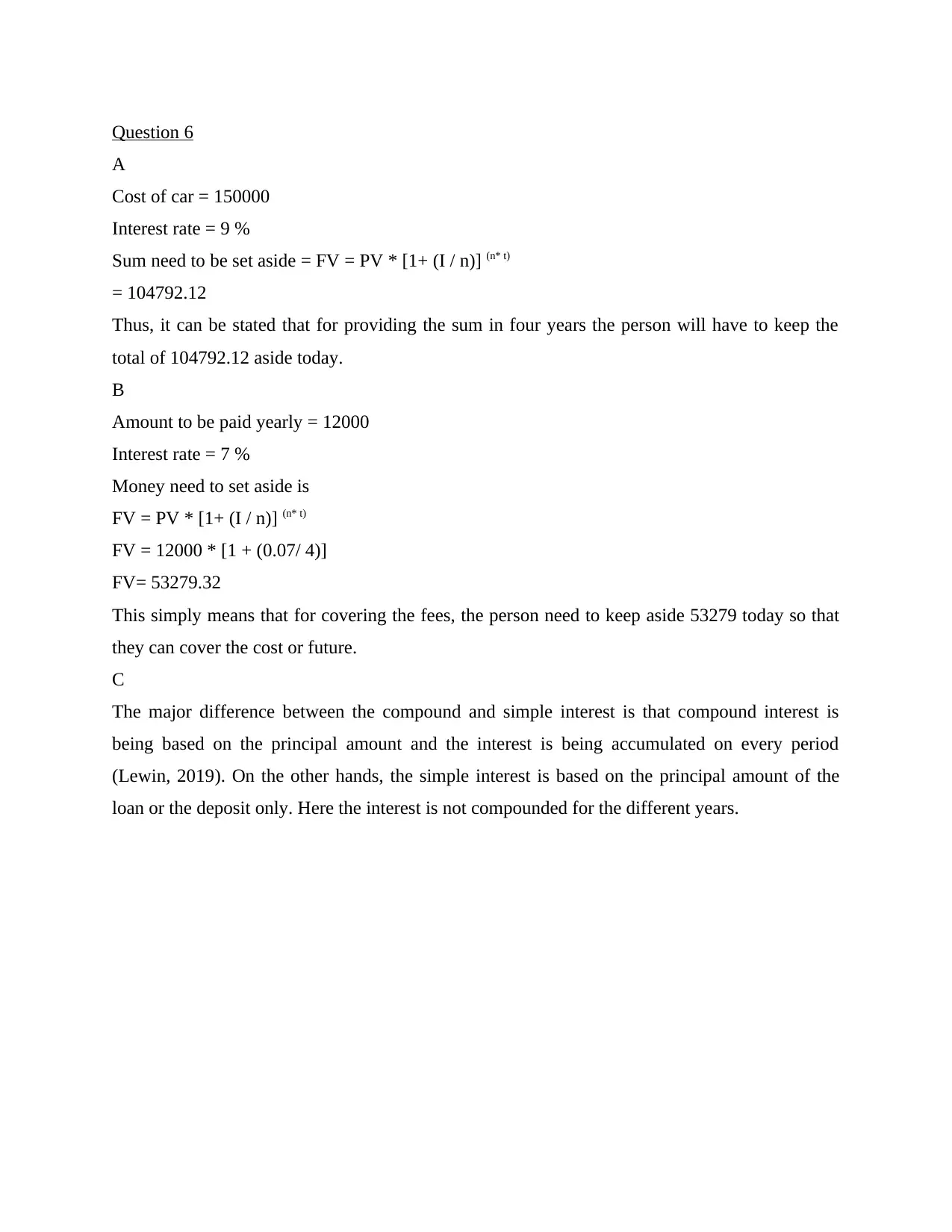

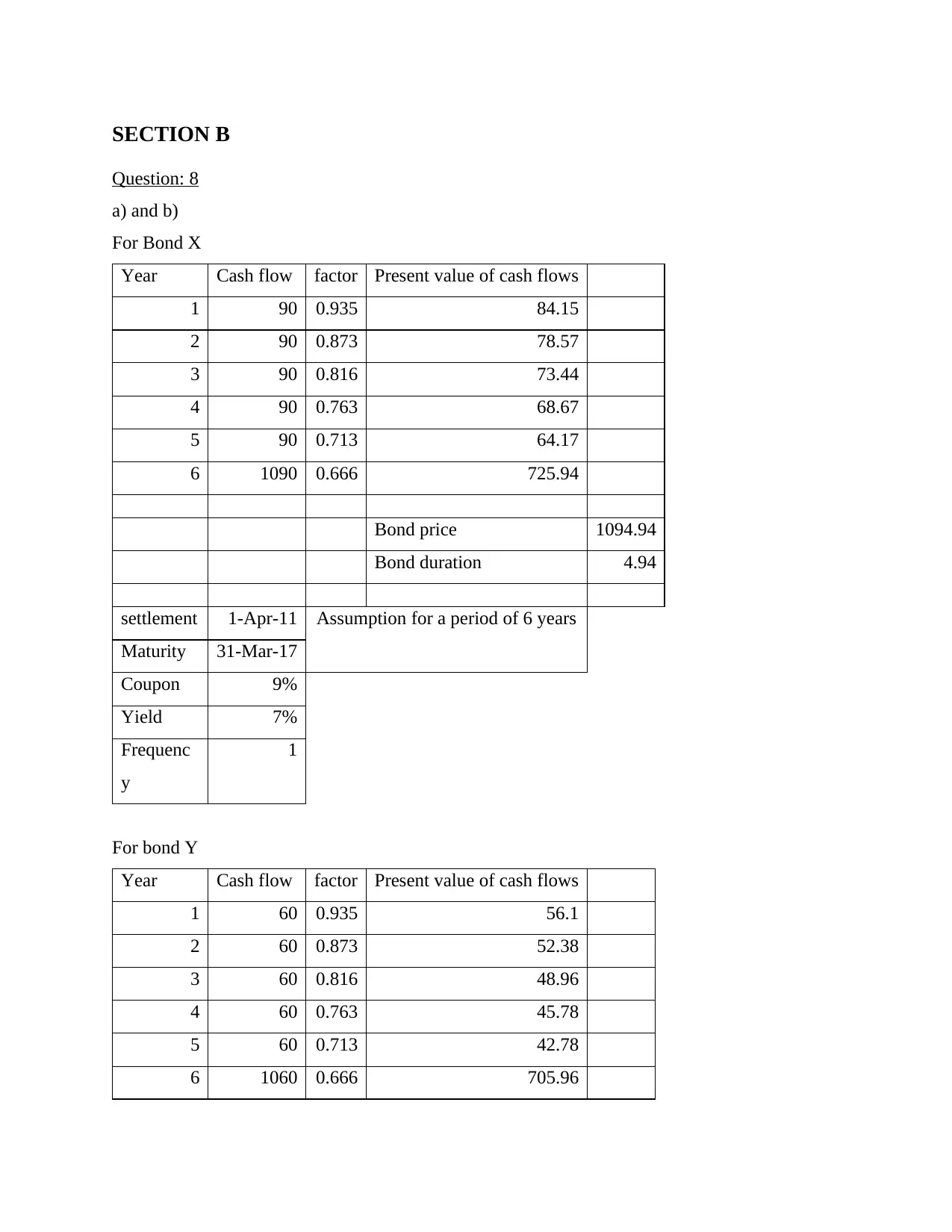

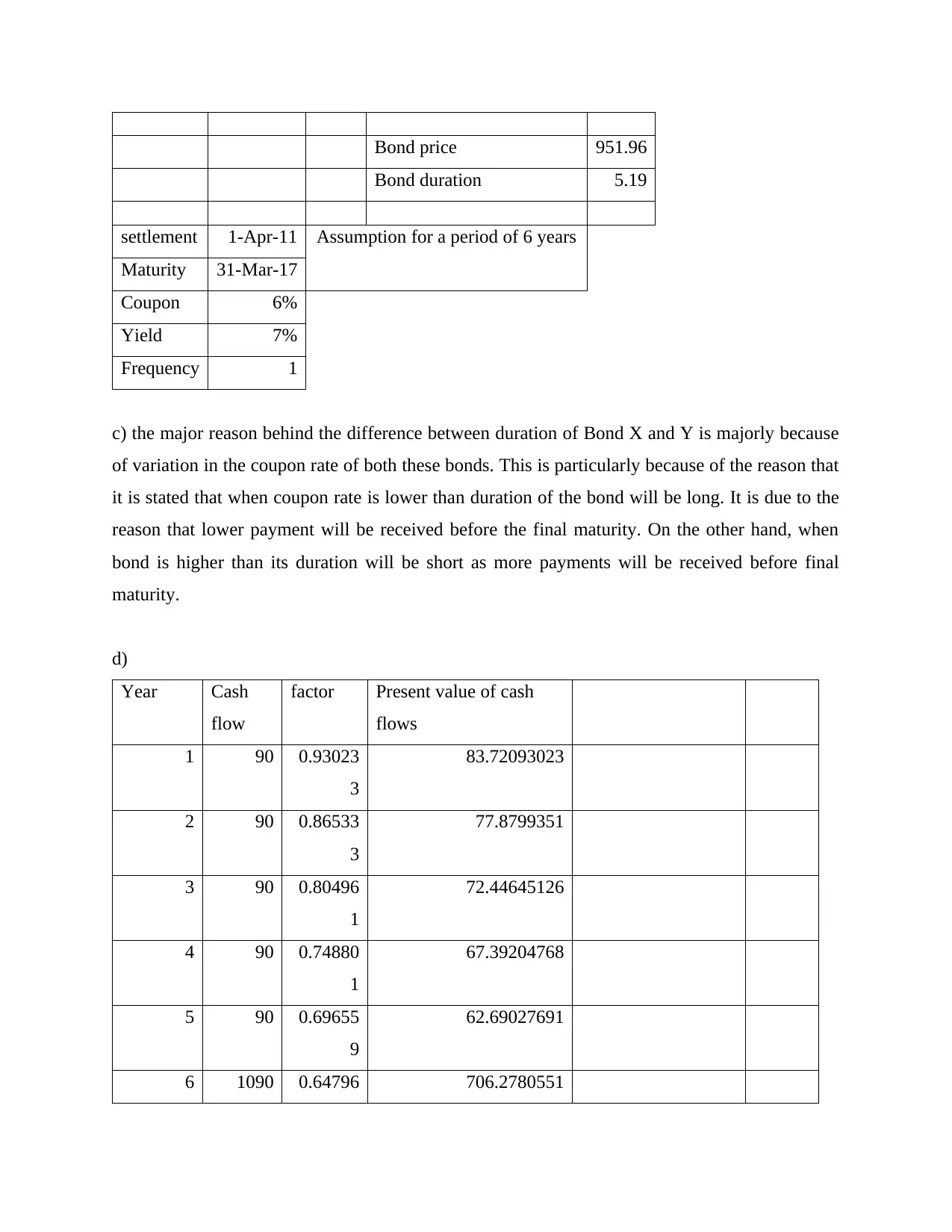

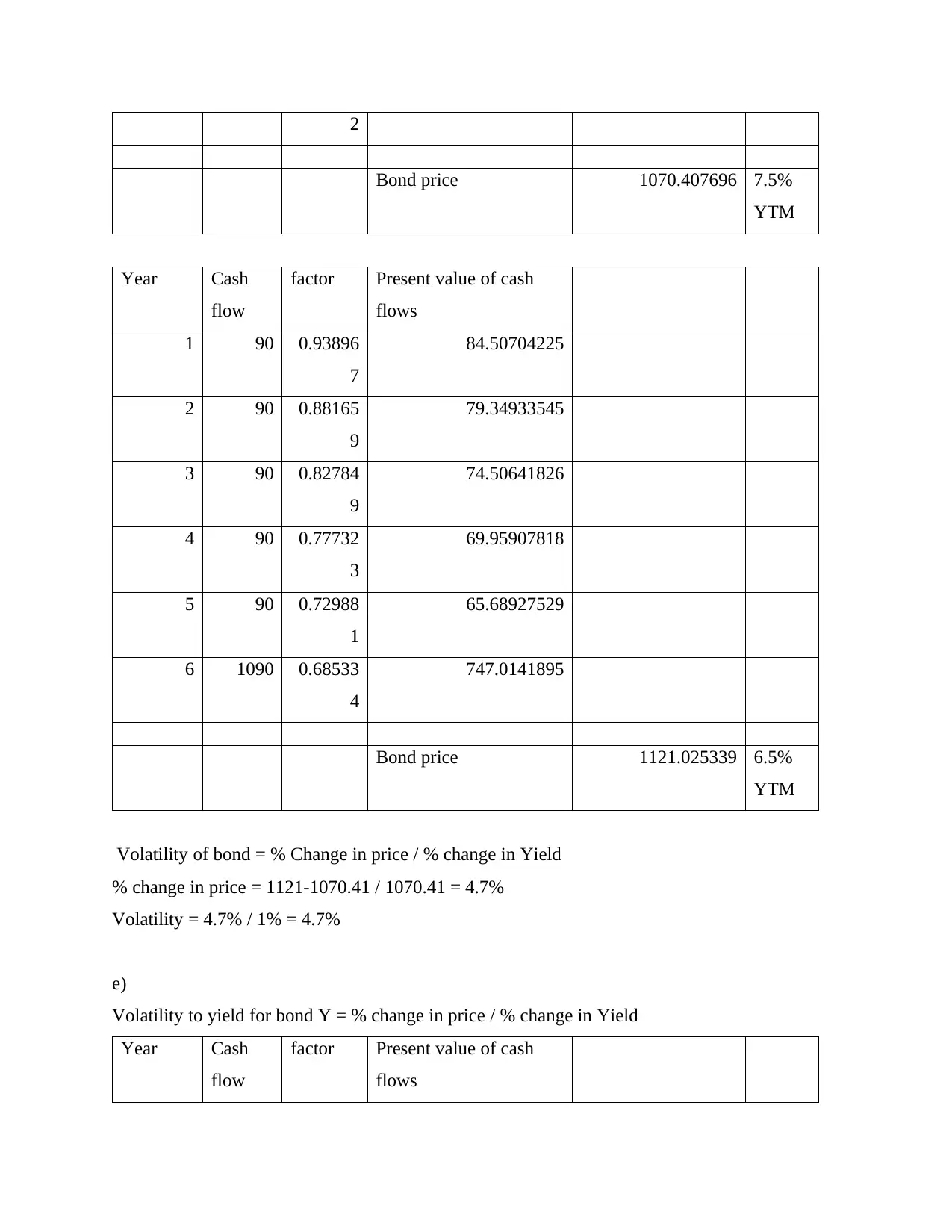

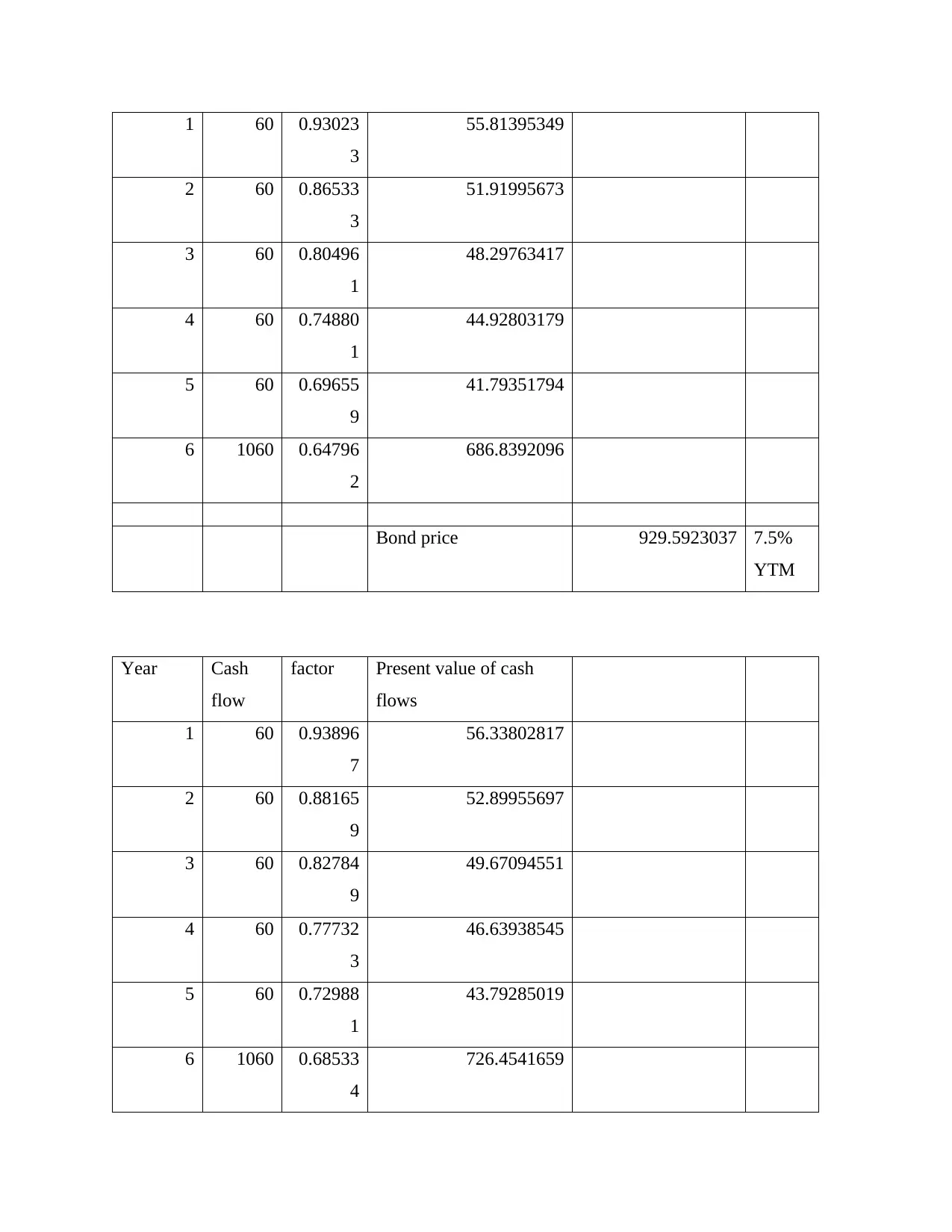

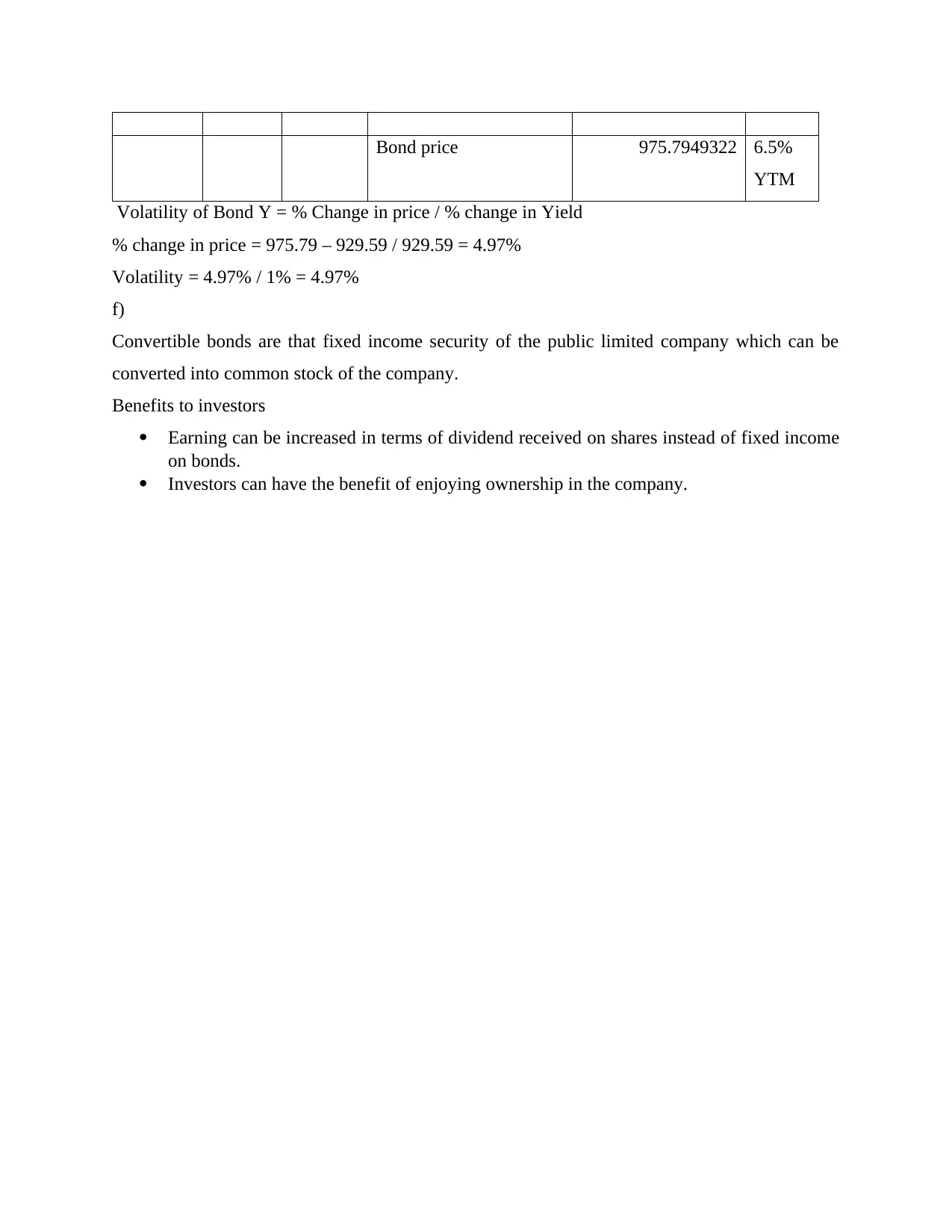

This assignment provides comprehensive solutions to a range of questions related to Corporate Financial Strategy. Topics covered include share valuation using dividend discount models, the law of one price, debt valuation, merger analysis, futures contract calculations, time value of money problems, and bond valuation with duration and volatility analysis. The solutions also address the Efficient Market Hypothesis (EMH) and its implications for investment strategies, including discussions on its weak, semi-strong, and strong forms, along with criticisms and real-world examples. The document offers detailed calculations and explanations for each question, making it a valuable resource for understanding key concepts in corporate finance. Desklib provides this and many other solved assignments and past papers.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.