Corporate Accounting Report: Sources of Funds and Asset Analysis

VerifiedAdded on 2023/01/13

|21

|3013

|46

Report

AI Summary

This report provides an in-depth analysis of corporate accounting practices, focusing on the sources of funds, liabilities, and asset management of two Australian companies: Woolworths and Telstra. The report explores the different types of funds used by these companies, including short-term and long-term debts, retained earnings, and equity capital, and examines their evolution over a three-year period. It identifies the percentage of internally and externally generated funds for each company and evaluates the merits and shortcomings of various funding sources. Furthermore, the report delves into the different types of liabilities, including interest-bearing and non-interest-bearing liabilities, and critically examines the key provisions of AASB 137 concerning provisions, contingent liabilities, and contingent assets. The study also investigates how these companies reference AASB 137 in their annual reports and categorizes the assets recorded by each company, critically evaluating the measurement basis used for each asset class. The report offers a comprehensive overview of the financial strategies and accounting practices employed by Woolworths and Telstra.

Corporate Account

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

(I) Different sources of funds used by chosen companies......................................................1

(ii) Evolution of source of funds used by company over last three years..............................1

(iii) Identify the percentage of the fund that is internally generated and the percentage of the

fund that is externally generated for each selected company.................................................2

(iv) Explain the relative merits and shortcomings of the different sources of fund used by your

selected companies.................................................................................................................3

(v) Different types of liabilities shown in the balance sheet of your selected companies?

Identify which ones of the liabilities are interest bearing and which ones are not interest is

bearing....................................................................................................................................4

(vi) Critically examine the key provisions under the AASB 137 ‘Provisions, Contingent

liabilities and Contingent assets'.............................................................................................5

(vii) Identify if your selected companies have made any reference to this particular standard

(AASB 137) in their annual reports........................................................................................6

(viii) Different categories of assets recorded by the selected companies...............................6

(ix) Critically examine the measurement basis used by the company for each class of assets

recoded by the selected companies.........................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

APPENDICS..................................................................................................................................10

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

(I) Different sources of funds used by chosen companies......................................................1

(ii) Evolution of source of funds used by company over last three years..............................1

(iii) Identify the percentage of the fund that is internally generated and the percentage of the

fund that is externally generated for each selected company.................................................2

(iv) Explain the relative merits and shortcomings of the different sources of fund used by your

selected companies.................................................................................................................3

(v) Different types of liabilities shown in the balance sheet of your selected companies?

Identify which ones of the liabilities are interest bearing and which ones are not interest is

bearing....................................................................................................................................4

(vi) Critically examine the key provisions under the AASB 137 ‘Provisions, Contingent

liabilities and Contingent assets'.............................................................................................5

(vii) Identify if your selected companies have made any reference to this particular standard

(AASB 137) in their annual reports........................................................................................6

(viii) Different categories of assets recorded by the selected companies...............................6

(ix) Critically examine the measurement basis used by the company for each class of assets

recoded by the selected companies.........................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

APPENDICS..................................................................................................................................10

INTRODUCTION

Corporate accounting is a procedure that is consecrated to the operational activities of an

organisation it is a special branch of accounting. It is dealing with the accounting that applied

into different types of organisation, supports to produce final accounts, cash flow statement and

application of financial results of an organisation. It is mainly applied by the Australian

companies (Belal, 2016). The given assignment based on the understanding about different types

of sources that utilise by business. To better understand of the report selected ASX listed

companies, Woolworths, it is an Australian chain of supermarket that dealing into grocery stores

that owned by Woolworth group. Another organisation Telstra corporation limited is Australian

telecommunication company that conduct activities into provide services of network, internet

access, markets voice and many others. In this report consist of sources of fund, different types

of sources, information as per the AASB 137.

MAIN BODY

(I) Different sources of funds used by chosen companies.

There are different types of sources of funds that helps to run organisation procedure in

smoothly manner. The Woolworth company use these sources such as:

Long term debts

Common stock

Retained earnings

Other equity

Telstra corporation limited

Bank loans

Short term debt

Government grants and subsidiaries

(ii) Evolution of source of funds used by company over last three years.

Woolwoth company Short term debts: The company have short term debts about $377 million in the year of

2017 but increase in 2018 and reach on &1599 million then increased about $1624

million in the year of 2019.

1

Corporate accounting is a procedure that is consecrated to the operational activities of an

organisation it is a special branch of accounting. It is dealing with the accounting that applied

into different types of organisation, supports to produce final accounts, cash flow statement and

application of financial results of an organisation. It is mainly applied by the Australian

companies (Belal, 2016). The given assignment based on the understanding about different types

of sources that utilise by business. To better understand of the report selected ASX listed

companies, Woolworths, it is an Australian chain of supermarket that dealing into grocery stores

that owned by Woolworth group. Another organisation Telstra corporation limited is Australian

telecommunication company that conduct activities into provide services of network, internet

access, markets voice and many others. In this report consist of sources of fund, different types

of sources, information as per the AASB 137.

MAIN BODY

(I) Different sources of funds used by chosen companies.

There are different types of sources of funds that helps to run organisation procedure in

smoothly manner. The Woolworth company use these sources such as:

Long term debts

Common stock

Retained earnings

Other equity

Telstra corporation limited

Bank loans

Short term debt

Government grants and subsidiaries

(ii) Evolution of source of funds used by company over last three years.

Woolwoth company Short term debts: The company have short term debts about $377 million in the year of

2017 but increase in 2018 and reach on &1599 million then increased about $1624

million in the year of 2019.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Long term debts: The company have good long term debt which is securities and bank

loans that is increasing in 2019 as compare with 2018. Such as 539 in 2018 and 647 in

2019 (Crowther, 2018) .

Retained earnings: The company have retained earning about 3968 in 2019 and 4073 in

2018.

Telstra corporation limited Short term debts: In short term debt consist of commercial paper, bank facilities that

helps to maintain liquidity. In 2018 company have $809 million, as per the year of 2018

focus on debt so it is getting that &15368 million, comprising acquiring, Long term debts: In 2019 it is analysed that company have growth in long term debt

about 4.9% that based on the net financial cost and changeable.

Retained earnings: The company have retained earning that comes from equity holders

which is 112 in 2018 and 10 in 2018.

(iii) Identify the percentage of the fund that is internally generated and the percentage of the fund

that is externally generated for each selected company

Every organisation require internal as well as external funds that are managed by both

organisation in particular percentage like:

Internally funds: These types of fund arrange by the organisation own personal level to

conduct internal operations. There are consisting of retained earning profits, start up, invest

amount securities.

Woolwoth company Loan from partners: The organisation take loan from their partner to arrange fund

because of both are known each others. It is contributed about 7% in the company. Sale of assets: To arrange funds company sale out old assets to generate income for a

business. So this part contribute about 15% in an business entity (Daniels and Morck,

2019)..

Recover from insurance: The company claim on the insurance which is already matured

and recover in same year but it contributes only 15%.

Telstra corporation limited Retained earning profits: The organisation can generated profit through commercial

paper and control on business operations in order to collect fund which is 5%.

2

loans that is increasing in 2019 as compare with 2018. Such as 539 in 2018 and 647 in

2019 (Crowther, 2018) .

Retained earnings: The company have retained earning about 3968 in 2019 and 4073 in

2018.

Telstra corporation limited Short term debts: In short term debt consist of commercial paper, bank facilities that

helps to maintain liquidity. In 2018 company have $809 million, as per the year of 2018

focus on debt so it is getting that &15368 million, comprising acquiring, Long term debts: In 2019 it is analysed that company have growth in long term debt

about 4.9% that based on the net financial cost and changeable.

Retained earnings: The company have retained earning that comes from equity holders

which is 112 in 2018 and 10 in 2018.

(iii) Identify the percentage of the fund that is internally generated and the percentage of the fund

that is externally generated for each selected company

Every organisation require internal as well as external funds that are managed by both

organisation in particular percentage like:

Internally funds: These types of fund arrange by the organisation own personal level to

conduct internal operations. There are consisting of retained earning profits, start up, invest

amount securities.

Woolwoth company Loan from partners: The organisation take loan from their partner to arrange fund

because of both are known each others. It is contributed about 7% in the company. Sale of assets: To arrange funds company sale out old assets to generate income for a

business. So this part contribute about 15% in an business entity (Daniels and Morck,

2019)..

Recover from insurance: The company claim on the insurance which is already matured

and recover in same year but it contributes only 15%.

Telstra corporation limited Retained earning profits: The organisation can generated profit through commercial

paper and control on business operations in order to collect fund which is 5%.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interest from loan: When company have more liquidity so control of this invest amount

in other securities and get interest that help to business.

Fixed assets on hand: If organisation wants to more funds for business so easily get

through fixed assets that sale out in big amount. It is good source that contribute about

17% in business.

Externally funds: These funds are arisen from different outside sources. The monies that

are acquired from the sale of securities and bonds are external funds.

Woolwoth company Venture Capital: It is kind of financing that is supplied by business at different stages

and help in organisational procedure. It is contributed about 20% in the business.

Equity capital: There are collecting amount from public and provide dividend. These

amount use by organisation for operational activities. It is contributed about 25% in

business (De Haan and Vlahu, 2016).

Telstra corporation limited Leasing: It is based on the contract that use by business as assets and help in arrangement

of fund. It contributes about 10% in business.

Bank overdraft: It is defined as flexible facility that provide by bank to their users but

take high interest on them. So it is contributed about 125 in the business but for short

time manner.

(iv) Explain the relative merits and shortcomings of the different sources of fund used by your

selected companies

The selected firms are acquiring funds from various financing sources. Following are

limitations and benefits that are connected with each source:

Short term debt: The financing source wherein lender provides financial resources that

are repayed with interest in upcoming duration. It is generally taken by both entities for short

time only that is one year.

Benefits: Short term debt ensures availability of cash fastly so to satisfy needs for

operating capital. Moreover, it benefits both business concerns to pay interest at lower rates that

reserves their profits.

3

in other securities and get interest that help to business.

Fixed assets on hand: If organisation wants to more funds for business so easily get

through fixed assets that sale out in big amount. It is good source that contribute about

17% in business.

Externally funds: These funds are arisen from different outside sources. The monies that

are acquired from the sale of securities and bonds are external funds.

Woolwoth company Venture Capital: It is kind of financing that is supplied by business at different stages

and help in organisational procedure. It is contributed about 20% in the business.

Equity capital: There are collecting amount from public and provide dividend. These

amount use by organisation for operational activities. It is contributed about 25% in

business (De Haan and Vlahu, 2016).

Telstra corporation limited Leasing: It is based on the contract that use by business as assets and help in arrangement

of fund. It contributes about 10% in business.

Bank overdraft: It is defined as flexible facility that provide by bank to their users but

take high interest on them. So it is contributed about 125 in the business but for short

time manner.

(iv) Explain the relative merits and shortcomings of the different sources of fund used by your

selected companies

The selected firms are acquiring funds from various financing sources. Following are

limitations and benefits that are connected with each source:

Short term debt: The financing source wherein lender provides financial resources that

are repayed with interest in upcoming duration. It is generally taken by both entities for short

time only that is one year.

Benefits: Short term debt ensures availability of cash fastly so to satisfy needs for

operating capital. Moreover, it benefits both business concerns to pay interest at lower rates that

reserves their profits.

3

Limitations: Using short term debt financing source, selected entities faces borrowing

cycle risk and it is uneconomical for making payments in context to some long term projects.

High transaction cost is associated with the source that is its major limitation.

Long term debt: It is the financing source that is used for getting loans for long terms. In

this source, organisations including Woolwoth company and Telstra corporation limited takes

financial loans from banking institutions for long durations that beyond 12 months.

Benefits: Long term debt provides benefits to selected companies through giving

immediate access of money. It also provide advantage related to financial leveraging to entities.

Limitations: The process for repayments of long term debts usually consumes more time

and it is paid with principal and interest amount (Drutman, 2015).

(v) Different types of liabilities shown in the balance sheet of your selected companies? Identify

which ones of the liabilities are interest bearing and which ones are not interest is bearing.

Woolwoth company

Liabilities Types

...Short term debts Interest bearing

...Accounts payable

...Deferred income tax

...Other current liabilities

...Long term debts Interest bearing

...Deferred tax liabilities

…Other long term liabilities

Telstra corporation limited

Liabilities Types

….Short term debts Interest bearing

….Accounts payable

….Deferred income tax

4

cycle risk and it is uneconomical for making payments in context to some long term projects.

High transaction cost is associated with the source that is its major limitation.

Long term debt: It is the financing source that is used for getting loans for long terms. In

this source, organisations including Woolwoth company and Telstra corporation limited takes

financial loans from banking institutions for long durations that beyond 12 months.

Benefits: Long term debt provides benefits to selected companies through giving

immediate access of money. It also provide advantage related to financial leveraging to entities.

Limitations: The process for repayments of long term debts usually consumes more time

and it is paid with principal and interest amount (Drutman, 2015).

(v) Different types of liabilities shown in the balance sheet of your selected companies? Identify

which ones of the liabilities are interest bearing and which ones are not interest is bearing.

Woolwoth company

Liabilities Types

...Short term debts Interest bearing

...Accounts payable

...Deferred income tax

...Other current liabilities

...Long term debts Interest bearing

...Deferred tax liabilities

…Other long term liabilities

Telstra corporation limited

Liabilities Types

….Short term debts Interest bearing

….Accounts payable

….Deferred income tax

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

….Other current liabilities

….Long term debts Interest bearing

….Deferred tax liabilities

….Other long term liabilities

(vi) Critically examine the key provisions under the AASB 137 ‘Provisions, Contingent

liabilities and Contingent assets'

AASB 137 is mentioned to the standard that companies apply for contingent assets that

are essential asset which are acquired through past operations. It develops as well as maintains

standards concerned to financial reporting which are applied by organisations working in both

sectors that are private and public.

Provisions: Provisions are mainly different from liabilities as some uncertainty is

associated with amount addition to timings. In accordingly, entities are required to settle all

disbursement. In wider sense, it includes:

Accounts payable which is an liability that companies uses for merchandise and services

that are supplied or gained. Moreover, there comprises invoices as well as are agreed by

suppliers (Hamdani and Ruffing, 2015) ..

The next are accruals which are also liabilities which are paid by institutions for receiving

or supplying products or services which are not paid yet. In various cases, these are less

against provisions because of uncertainties which have arisen.

Relationship among contingent liabilities along with provisions: Generally, all types of

provisions are uncertain because of uncertainties related to time and amount. With standard term,

contingent are used in place of liabilities or assets which are not identifies because of confirmed

presence and huge uncontrollable activities.

Contingent liabilities: Liabilities which might incurred by business concerns depending

on results of uncertain upcoming event are contingent liabilities. The liabilities such as product

warranties, pending investigations as well as potential lawsuits are part of contingent liabilities

that might arise at Woolworth company and Telstra corporation.

Contingent assets: The possible assets whose occurrence depends on upcoming events

that are not in company control are contingent assets. These assets are not recorded in

5

….Long term debts Interest bearing

….Deferred tax liabilities

….Other long term liabilities

(vi) Critically examine the key provisions under the AASB 137 ‘Provisions, Contingent

liabilities and Contingent assets'

AASB 137 is mentioned to the standard that companies apply for contingent assets that

are essential asset which are acquired through past operations. It develops as well as maintains

standards concerned to financial reporting which are applied by organisations working in both

sectors that are private and public.

Provisions: Provisions are mainly different from liabilities as some uncertainty is

associated with amount addition to timings. In accordingly, entities are required to settle all

disbursement. In wider sense, it includes:

Accounts payable which is an liability that companies uses for merchandise and services

that are supplied or gained. Moreover, there comprises invoices as well as are agreed by

suppliers (Hamdani and Ruffing, 2015) ..

The next are accruals which are also liabilities which are paid by institutions for receiving

or supplying products or services which are not paid yet. In various cases, these are less

against provisions because of uncertainties which have arisen.

Relationship among contingent liabilities along with provisions: Generally, all types of

provisions are uncertain because of uncertainties related to time and amount. With standard term,

contingent are used in place of liabilities or assets which are not identifies because of confirmed

presence and huge uncontrollable activities.

Contingent liabilities: Liabilities which might incurred by business concerns depending

on results of uncertain upcoming event are contingent liabilities. The liabilities such as product

warranties, pending investigations as well as potential lawsuits are part of contingent liabilities

that might arise at Woolworth company and Telstra corporation.

Contingent assets: The possible assets whose occurrence depends on upcoming events

that are not in company control are contingent assets. These assets are not recorded in

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

organisational balance sheet. There are certain conditions that are to be meet for contingent

assets and are only recorded when realization of flows of cash is connected with relative

certainty.

(vii) Identify if your selected companies have made any reference to this particular standard

(AASB 137) in their annual reports

AASB 137 standrd related with the provisions, contingent liabilities and contingent

assets. The main purpose of this standard is to assure about the identification and measurement

depends are implemented systematically for provision, contingent liabilities & assets to effective

applicant to understand the nature, timing as well as amounts of firm. This standard must apply

by both organisation in order to come out from circumstances that origin any time in business.

With the help of this standard company prepare provision for different types of risk that

categorise in financial and non financial manner. As per the contingent liabilities are using by

both organisation to analysis the outflow of resources to achieve economical advantages. It is

obliged with various portion that expected to meet with other parties. This standard mainly

related with the contingency assets, liabilities and provisions (Hamilton and Micklethwait,

2016).

These assets are supporting for the disclose all inflow that conduct by business in

particular year. These are helping to improvements in financ9ial statements and analysis accurate

position of business effectively. The contingency liabilities has been categorised into two manner

such as:

Possible obligation

Present obligation

(viii) Different categories of assets recorded by the selected companies.

Every business activities based on the different types of assets that supports to business

generate profitability and increase productivity. There are discussed various types assets that

classified into headings like current, non current, fixed.

Woolwoth company

Intangible assets Goodwill

Copyright

Fixed assets Furniture & fixture

6

assets and are only recorded when realization of flows of cash is connected with relative

certainty.

(vii) Identify if your selected companies have made any reference to this particular standard

(AASB 137) in their annual reports

AASB 137 standrd related with the provisions, contingent liabilities and contingent

assets. The main purpose of this standard is to assure about the identification and measurement

depends are implemented systematically for provision, contingent liabilities & assets to effective

applicant to understand the nature, timing as well as amounts of firm. This standard must apply

by both organisation in order to come out from circumstances that origin any time in business.

With the help of this standard company prepare provision for different types of risk that

categorise in financial and non financial manner. As per the contingent liabilities are using by

both organisation to analysis the outflow of resources to achieve economical advantages. It is

obliged with various portion that expected to meet with other parties. This standard mainly

related with the contingency assets, liabilities and provisions (Hamilton and Micklethwait,

2016).

These assets are supporting for the disclose all inflow that conduct by business in

particular year. These are helping to improvements in financ9ial statements and analysis accurate

position of business effectively. The contingency liabilities has been categorised into two manner

such as:

Possible obligation

Present obligation

(viii) Different categories of assets recorded by the selected companies.

Every business activities based on the different types of assets that supports to business

generate profitability and increase productivity. There are discussed various types assets that

classified into headings like current, non current, fixed.

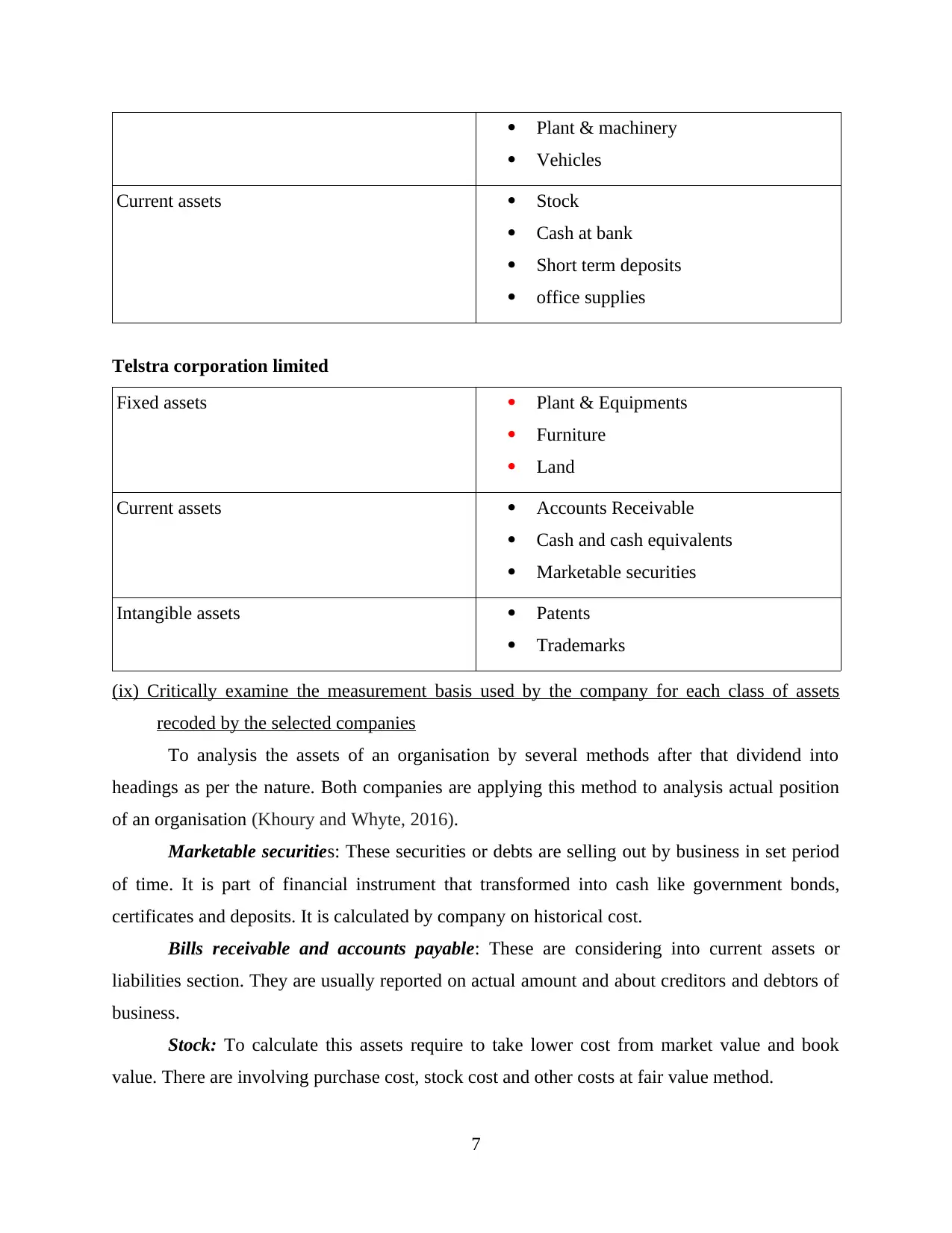

Woolwoth company

Intangible assets Goodwill

Copyright

Fixed assets Furniture & fixture

6

Plant & machinery

Vehicles

Current assets Stock

Cash at bank

Short term deposits

office supplies

Telstra corporation limited

Fixed assets Plant & Equipments

Furniture

Land

Current assets Accounts Receivable

Cash and cash equivalents

Marketable securities

Intangible assets Patents

Trademarks

(ix) Critically examine the measurement basis used by the company for each class of assets

recoded by the selected companies

To analysis the assets of an organisation by several methods after that dividend into

headings as per the nature. Both companies are applying this method to analysis actual position

of an organisation (Khoury and Whyte, 2016).

Marketable securities: These securities or debts are selling out by business in set period

of time. It is part of financial instrument that transformed into cash like government bonds,

certificates and deposits. It is calculated by company on historical cost.

Bills receivable and accounts payable: These are considering into current assets or

liabilities section. They are usually reported on actual amount and about creditors and debtors of

business.

Stock: To calculate this assets require to take lower cost from market value and book

value. There are involving purchase cost, stock cost and other costs at fair value method.

7

Vehicles

Current assets Stock

Cash at bank

Short term deposits

office supplies

Telstra corporation limited

Fixed assets Plant & Equipments

Furniture

Land

Current assets Accounts Receivable

Cash and cash equivalents

Marketable securities

Intangible assets Patents

Trademarks

(ix) Critically examine the measurement basis used by the company for each class of assets

recoded by the selected companies

To analysis the assets of an organisation by several methods after that dividend into

headings as per the nature. Both companies are applying this method to analysis actual position

of an organisation (Khoury and Whyte, 2016).

Marketable securities: These securities or debts are selling out by business in set period

of time. It is part of financial instrument that transformed into cash like government bonds,

certificates and deposits. It is calculated by company on historical cost.

Bills receivable and accounts payable: These are considering into current assets or

liabilities section. They are usually reported on actual amount and about creditors and debtors of

business.

Stock: To calculate this assets require to take lower cost from market value and book

value. There are involving purchase cost, stock cost and other costs at fair value method.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cash & cash equivalents: It is part of the current assets that remain less than one year

and for this apply cash glow method where categorised in three manner. This method help to

analysis cash inflow and out flow.

Intangible assets: In this types of assets have not physical existence only have imagery

existence. These are measured on the basis of revaluation or business model. Such as, Goodwill,

trademark etc.

Fixed assets: To life line of fixed assets require to apply depreciation method as per the

systematic procedure. The company applied it in two manner such as straight line and double

line method.

Current assets: These types of assets are maintain liquidity ion business and require to

utilise in less than one year like stock, bills receivables, cash etc. It is analysed on cost model and

also on revaluation model (Rönnegard, 2015).

CONCLUSION

As per the discussion it is concluded that this type of accounting apply in the business to

assure about the financial activities which is linked with the laws and legislation qualify by

oversight bodies. Corporate accountants generally use it to make effective & strategic decision

for an organisation. This accounting apply by the both organisation to prepare financial

statements in effective manner. Companies following AASB 137 to analysis about provisions

and contingent assets & liabilities.

8

and for this apply cash glow method where categorised in three manner. This method help to

analysis cash inflow and out flow.

Intangible assets: In this types of assets have not physical existence only have imagery

existence. These are measured on the basis of revaluation or business model. Such as, Goodwill,

trademark etc.

Fixed assets: To life line of fixed assets require to apply depreciation method as per the

systematic procedure. The company applied it in two manner such as straight line and double

line method.

Current assets: These types of assets are maintain liquidity ion business and require to

utilise in less than one year like stock, bills receivables, cash etc. It is analysed on cost model and

also on revaluation model (Rönnegard, 2015).

CONCLUSION

As per the discussion it is concluded that this type of accounting apply in the business to

assure about the financial activities which is linked with the laws and legislation qualify by

oversight bodies. Corporate accountants generally use it to make effective & strategic decision

for an organisation. This accounting apply by the both organisation to prepare financial

statements in effective manner. Companies following AASB 137 to analysis about provisions

and contingent assets & liabilities.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Belal, A. R., 2016. Corporate social responsibility reporting in developing countries: The case

of Bangladesh. Routledge.

Crowther, D., 2018. A Social Critique of Corporate Reporting: A Semiotic Analysis of Corporate

Financial and Environmental Reporting: A Semiotic Analysis of Corporate Financial

and Environmental Reporting. Routledge.

Daniels, R. J. and Morck, R., 2019. Corporate Decision Making in Canada. Routledge.

De Haan, J. and Vlahu, R., 2016. Corporate governance of banks: A survey. Journal of

Economic Surveys. 30(2). pp.228-277.

Drutman, L., 2015. The business of America is lobbying: How corporations became politicized

and politics became more corporate. Oxford University Press.

Hamdani, K. and Ruffing, L., 2015. United Nations Centre on Transnational Corporations:

corporate conduct and the public interest. Routledge.

Hamilton, S. and Micklethwait, A., 2016. Greed and corporate failure: The lessons from recent

disasters. Springer.

Khoury, S. and Whyte, D., 2016. Corporate human rights violations: Global prospects for legal

action. Routledge.

Rönnegard, D., 2015. The fallacy of corporate moral agency(Vol. 44). Dordrecht: Springer.

Stoll, M. L., 2015. Corporate political speech and moral obligation. Journal of Business

Ethics, 132(3), pp.553-563.

Tombs, S. and Whyte, D., 2015. The corporate criminal: Why corporations must be abolished.

Routledge.

Tricker, R. B. and Tricker, R. I., 2015. Corporate governance: Principles, policies, and

practices. Oxford University Press.

Tung, F. and Roe, M. J., 2016. Bankruptcy and Corporate Reorganization, Legal and Financial

Materials. Foundation Press.

Welford, R., 2016. Corporate environmental management 1: Systems and strategies. Routledge.

Wells, H. ed., 2018. Research handbook on the history of corporate and company law. Edward

Elgar Publishing.

9

Books and Journals

Belal, A. R., 2016. Corporate social responsibility reporting in developing countries: The case

of Bangladesh. Routledge.

Crowther, D., 2018. A Social Critique of Corporate Reporting: A Semiotic Analysis of Corporate

Financial and Environmental Reporting: A Semiotic Analysis of Corporate Financial

and Environmental Reporting. Routledge.

Daniels, R. J. and Morck, R., 2019. Corporate Decision Making in Canada. Routledge.

De Haan, J. and Vlahu, R., 2016. Corporate governance of banks: A survey. Journal of

Economic Surveys. 30(2). pp.228-277.

Drutman, L., 2015. The business of America is lobbying: How corporations became politicized

and politics became more corporate. Oxford University Press.

Hamdani, K. and Ruffing, L., 2015. United Nations Centre on Transnational Corporations:

corporate conduct and the public interest. Routledge.

Hamilton, S. and Micklethwait, A., 2016. Greed and corporate failure: The lessons from recent

disasters. Springer.

Khoury, S. and Whyte, D., 2016. Corporate human rights violations: Global prospects for legal

action. Routledge.

Rönnegard, D., 2015. The fallacy of corporate moral agency(Vol. 44). Dordrecht: Springer.

Stoll, M. L., 2015. Corporate political speech and moral obligation. Journal of Business

Ethics, 132(3), pp.553-563.

Tombs, S. and Whyte, D., 2015. The corporate criminal: Why corporations must be abolished.

Routledge.

Tricker, R. B. and Tricker, R. I., 2015. Corporate governance: Principles, policies, and

practices. Oxford University Press.

Tung, F. and Roe, M. J., 2016. Bankruptcy and Corporate Reorganization, Legal and Financial

Materials. Foundation Press.

Welford, R., 2016. Corporate environmental management 1: Systems and strategies. Routledge.

Wells, H. ed., 2018. Research handbook on the history of corporate and company law. Edward

Elgar Publishing.

9

APPENDICS

Telstra corporation limited

10

Telstra corporation limited

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.