Raising Funds and Liabilities: Corporate Accounting Assignment

VerifiedAdded on 2022/08/24

|17

|4044

|17

Homework Assignment

AI Summary

This assignment delves into corporate accounting, specifically examining the sources of funds utilized by companies for financing their operations and managing liabilities. The analysis centers on two companies listed on the Australian Stock Exchange (ASX) within the food, beverage, and tobacco sector: Australia Vintage Limited and Beston Global Foods Limited. The assignment explores the different funding sources employed by these companies, including debt, equity, and reserves, and evaluates the evolution of these sources over three financial years. It also assesses the merits and shortcomings of each funding method, such as equity financing, retained earnings, and borrowings. Furthermore, the assignment summarizes the key principles of AASB 137, concerning provisions, contingent liabilities, and contingent assets, and identifies how these companies apply the standard. Finally, the assignment identifies different categories of assets recorded by the selected companies and examines the measurement basis used by the company for each class of assets.

Running head: CORPORATE ACCOUNTING

Corporate accounting

Name of the Student

Name of the University

Author Note

Corporate accounting

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE ACCOUNTING

Abstract:

The paper elucidates an understanding of the several sources of funds used by the company

for financing their business. In this regard, two companies from the Food, beverage, tobacco

and listed on the ASX (Australian stock exchange) has been selected for identifying the

different source of funds. Discussion also incorporates the merits and shortcomings of

various sources of funds used by the company. In addition to this, the key concepts of the

standard AASSB 137 “Provision, contingent liabilities and contingent assets” have been

summarized and the companies make conclusions regarding the adoption of this standard.

Abstract:

The paper elucidates an understanding of the several sources of funds used by the company

for financing their business. In this regard, two companies from the Food, beverage, tobacco

and listed on the ASX (Australian stock exchange) has been selected for identifying the

different source of funds. Discussion also incorporates the merits and shortcomings of

various sources of funds used by the company. In addition to this, the key concepts of the

standard AASSB 137 “Provision, contingent liabilities and contingent assets” have been

summarized and the companies make conclusions regarding the adoption of this standard.

CORPORATE ACCOUNTING

Table of Contents

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................2

Answer to question i).................................................................................................................2

Answer to question ii)................................................................................................................2

Answer to question iii)...............................................................................................................2

Answer to question iv)...............................................................................................................2

Answer to question v)................................................................................................................2

Answer to question vi)...............................................................................................................2

Answer to question vii)..............................................................................................................2

Answer to question viii).............................................................................................................2

Answer to question ix)...............................................................................................................2

Conclusion:................................................................................................................................2

Table of Contents

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................2

Answer to question i).................................................................................................................2

Answer to question ii)................................................................................................................2

Answer to question iii)...............................................................................................................2

Answer to question iv)...............................................................................................................2

Answer to question v)................................................................................................................2

Answer to question vi)...............................................................................................................2

Answer to question vii)..............................................................................................................2

Answer to question viii).............................................................................................................2

Answer to question ix)...............................................................................................................2

Conclusion:................................................................................................................................2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE ACCOUNTING

Introduction:

The paper discusses about the different sources of funds that is used by the companies

to raise funds and the relative merits of the different funds used by the companies are

demonstrated. The use of the standard ASSB 137 provisions, contingent liabilities and

contingent assets by the companies are identified and the key concepts have been evaluated.

For this purpose, two companies listed on AXS operating in food, beverage and tobacco

sector has been chosen that is Australia Vintage limited and Beston Global food limited.

Various sources of funds used by these companies are analysed for the evolution of the funds

used. The shortcomings and merits of the different sources of the funds used by the

companies have been analysed. Australian vintage limited is the leading wine company of

Australia that has a fully integrated model of doing business and the capabilities extended to

wine and boutique. Beston Global limited on other hand serves the global market by

providing verifiably and natural beverages and safe food enabling consumers to make healthy

choices.

Discussion:

Answer to question i)

From the financial report of Australian Vintage limited, it has observed that the

company is using a mixed funding. Such funding comprises of debt, issued capital and

reserves. Financial report of Beston Global food limited reveals that the company uses

various sources of funds such as equity, contributed equity and reserves. On other hand,

Beston is also dependent upon other funding source such as borrowings and employee benefit

Introduction:

The paper discusses about the different sources of funds that is used by the companies

to raise funds and the relative merits of the different funds used by the companies are

demonstrated. The use of the standard ASSB 137 provisions, contingent liabilities and

contingent assets by the companies are identified and the key concepts have been evaluated.

For this purpose, two companies listed on AXS operating in food, beverage and tobacco

sector has been chosen that is Australia Vintage limited and Beston Global food limited.

Various sources of funds used by these companies are analysed for the evolution of the funds

used. The shortcomings and merits of the different sources of the funds used by the

companies have been analysed. Australian vintage limited is the leading wine company of

Australia that has a fully integrated model of doing business and the capabilities extended to

wine and boutique. Beston Global limited on other hand serves the global market by

providing verifiably and natural beverages and safe food enabling consumers to make healthy

choices.

Discussion:

Answer to question i)

From the financial report of Australian Vintage limited, it has observed that the

company is using a mixed funding. Such funding comprises of debt, issued capital and

reserves. Financial report of Beston Global food limited reveals that the company uses

various sources of funds such as equity, contributed equity and reserves. On other hand,

Beston is also dependent upon other funding source such as borrowings and employee benefit

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE ACCOUNTING

obligation. In addition to this, there is a provision of funding via changing interest on loan

balances and convertible notes. Working capital of the company is increased by using a range

of options to fund the project.

Answer to question ii)

In this section, the evolution of different sources of funds used by the company over

the last three financial year has been analysed. Any changes in the source of funding has also

been analysed. The long-term borrowing of Australian Vintage limited has decreased in

financial year 2019 to $ 79965 from $ 84880 in year 2017. On other hand, total amount of

issued capital as a way of raising funds has increased from $ 463009 in year 2017 to $

463961 in year 2018 and stood at $ 465490 in year 2019. Reserves of Vintage has increased

continuously from $ 1829 in year 2017 to $ 1989 in year 2018 and further to $ 2443 in year

2019. This implies that the company has increased the use of issued capital and reserves for

funding and other hand has reduced its dependency on borrowing (Australianvintage.com.au

2020).

Now, looking at the financial report of Beston Global Foods Company limited, it is

observed that the company has not borrowed for the last two years and the value of

borrowing is at zero. It is in the financial year 2019 that the funds have been issued by issuing

debentures or taking debt. Total amount of borrowings is recorded at $ 35807 in the financial

year 2019. In addition to this, employee benefits obligations are also a source of funding, the

value has increased year on year from $ 25 in 2017 to $ 70 in 2018, and this further increased

to $ 179 in year 2019 respectively. On other hand, other source of funding used by Beston

Global food is contributed equity and other reserves. Total amount of issued equity capital

has remained at $ 147535 for the last three financial years. However, the amount of reserves

used by the company in funding has reduced from 482 in year 2017 to 9135 in year 2019.

obligation. In addition to this, there is a provision of funding via changing interest on loan

balances and convertible notes. Working capital of the company is increased by using a range

of options to fund the project.

Answer to question ii)

In this section, the evolution of different sources of funds used by the company over

the last three financial year has been analysed. Any changes in the source of funding has also

been analysed. The long-term borrowing of Australian Vintage limited has decreased in

financial year 2019 to $ 79965 from $ 84880 in year 2017. On other hand, total amount of

issued capital as a way of raising funds has increased from $ 463009 in year 2017 to $

463961 in year 2018 and stood at $ 465490 in year 2019. Reserves of Vintage has increased

continuously from $ 1829 in year 2017 to $ 1989 in year 2018 and further to $ 2443 in year

2019. This implies that the company has increased the use of issued capital and reserves for

funding and other hand has reduced its dependency on borrowing (Australianvintage.com.au

2020).

Now, looking at the financial report of Beston Global Foods Company limited, it is

observed that the company has not borrowed for the last two years and the value of

borrowing is at zero. It is in the financial year 2019 that the funds have been issued by issuing

debentures or taking debt. Total amount of borrowings is recorded at $ 35807 in the financial

year 2019. In addition to this, employee benefits obligations are also a source of funding, the

value has increased year on year from $ 25 in 2017 to $ 70 in 2018, and this further increased

to $ 179 in year 2019 respectively. On other hand, other source of funding used by Beston

Global food is contributed equity and other reserves. Total amount of issued equity capital

has remained at $ 147535 for the last three financial years. However, the amount of reserves

used by the company in funding has reduced from 482 in year 2017 to 9135 in year 2019.

CORPORATE ACCOUNTING

This fall in value implies that the company is not left with reserves to investment in the

business as directors in the form of dividend have kept a larger proportion of profits. It is

inferred from the analysis that the company has not changed any source of fund or added any

other source for funding its business other than borrowing. No additional funds has been

raised by issuing equity as evident from unchanged value of contributed equity

(bestonglobalfoods.com.au 2020).

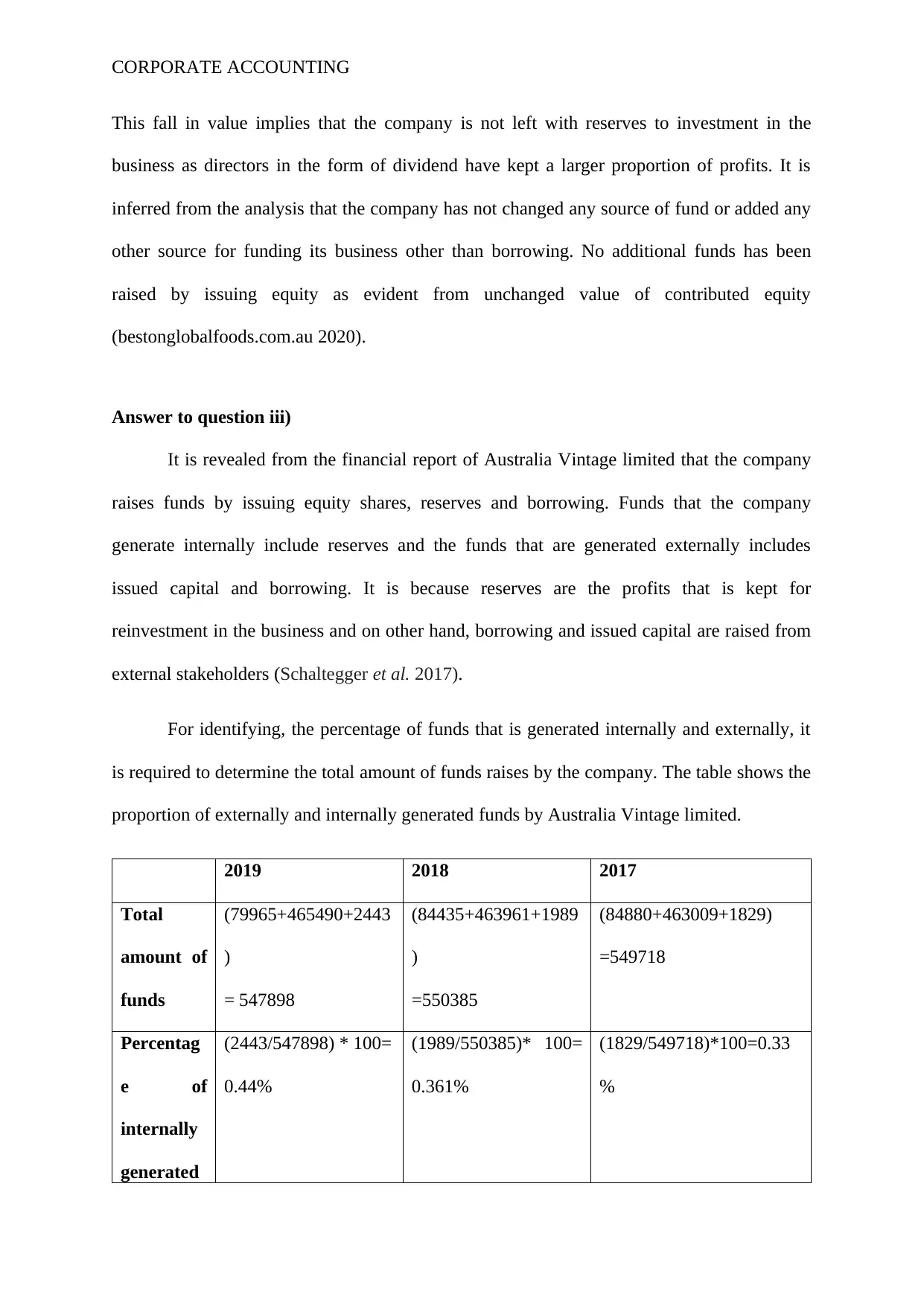

Answer to question iii)

It is revealed from the financial report of Australia Vintage limited that the company

raises funds by issuing equity shares, reserves and borrowing. Funds that the company

generate internally include reserves and the funds that are generated externally includes

issued capital and borrowing. It is because reserves are the profits that is kept for

reinvestment in the business and on other hand, borrowing and issued capital are raised from

external stakeholders (Schaltegger et al. 2017).

For identifying, the percentage of funds that is generated internally and externally, it

is required to determine the total amount of funds raises by the company. The table shows the

proportion of externally and internally generated funds by Australia Vintage limited.

2019 2018 2017

Total

amount of

funds

(79965+465490+2443

)

= 547898

(84435+463961+1989

)

=550385

(84880+463009+1829)

=549718

Percentag

e of

internally

generated

(2443/547898) * 100=

0.44%

(1989/550385)* 100=

0.361%

(1829/549718)*100=0.33

%

This fall in value implies that the company is not left with reserves to investment in the

business as directors in the form of dividend have kept a larger proportion of profits. It is

inferred from the analysis that the company has not changed any source of fund or added any

other source for funding its business other than borrowing. No additional funds has been

raised by issuing equity as evident from unchanged value of contributed equity

(bestonglobalfoods.com.au 2020).

Answer to question iii)

It is revealed from the financial report of Australia Vintage limited that the company

raises funds by issuing equity shares, reserves and borrowing. Funds that the company

generate internally include reserves and the funds that are generated externally includes

issued capital and borrowing. It is because reserves are the profits that is kept for

reinvestment in the business and on other hand, borrowing and issued capital are raised from

external stakeholders (Schaltegger et al. 2017).

For identifying, the percentage of funds that is generated internally and externally, it

is required to determine the total amount of funds raises by the company. The table shows the

proportion of externally and internally generated funds by Australia Vintage limited.

2019 2018 2017

Total

amount of

funds

(79965+465490+2443

)

= 547898

(84435+463961+1989

)

=550385

(84880+463009+1829)

=549718

Percentag

e of

internally

generated

(2443/547898) * 100=

0.44%

(1989/550385)* 100=

0.361%

(1829/549718)*100=0.33

%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE ACCOUNTING

funds

Percentag

e of

externally

generated

funds

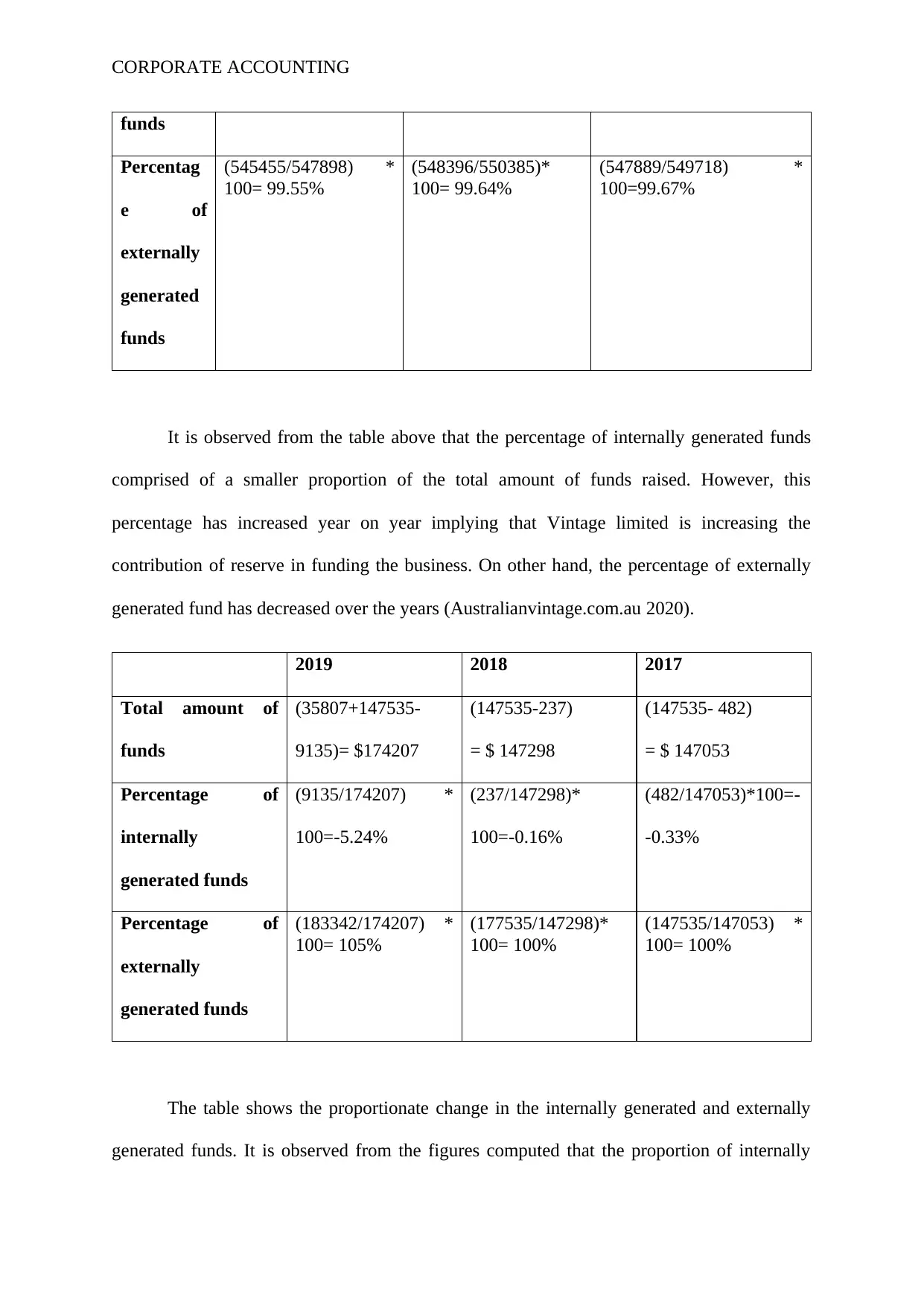

(545455/547898) *

100= 99.55%

(548396/550385)*

100= 99.64%

(547889/549718) *

100=99.67%

It is observed from the table above that the percentage of internally generated funds

comprised of a smaller proportion of the total amount of funds raised. However, this

percentage has increased year on year implying that Vintage limited is increasing the

contribution of reserve in funding the business. On other hand, the percentage of externally

generated fund has decreased over the years (Australianvintage.com.au 2020).

2019 2018 2017

Total amount of

funds

(35807+147535-

9135)= $174207

(147535-237)

= $ 147298

(147535- 482)

= $ 147053

Percentage of

internally

generated funds

(9135/174207) *

100=-5.24%

(237/147298)*

100=-0.16%

(482/147053)*100=-

-0.33%

Percentage of

externally

generated funds

(183342/174207) *

100= 105%

(177535/147298)*

100= 100%

(147535/147053) *

100= 100%

The table shows the proportionate change in the internally generated and externally

generated funds. It is observed from the figures computed that the proportion of internally

funds

Percentag

e of

externally

generated

funds

(545455/547898) *

100= 99.55%

(548396/550385)*

100= 99.64%

(547889/549718) *

100=99.67%

It is observed from the table above that the percentage of internally generated funds

comprised of a smaller proportion of the total amount of funds raised. However, this

percentage has increased year on year implying that Vintage limited is increasing the

contribution of reserve in funding the business. On other hand, the percentage of externally

generated fund has decreased over the years (Australianvintage.com.au 2020).

2019 2018 2017

Total amount of

funds

(35807+147535-

9135)= $174207

(147535-237)

= $ 147298

(147535- 482)

= $ 147053

Percentage of

internally

generated funds

(9135/174207) *

100=-5.24%

(237/147298)*

100=-0.16%

(482/147053)*100=-

-0.33%

Percentage of

externally

generated funds

(183342/174207) *

100= 105%

(177535/147298)*

100= 100%

(147535/147053) *

100= 100%

The table shows the proportionate change in the internally generated and externally

generated funds. It is observed from the figures computed that the proportion of internally

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE ACCOUNTING

generated funds in the total funds has decreased as indicated from falling figure of reserves.

Now, observing the figure of percentage of externally generated funds, it is viewed that the

proportion of externally generated funds has increased over the years from 100% to 105% in

year 2019 (bestonglobalfoods.com.au 2020). From the computed figures, it is inferred that the

proportion of externally generated funds comprising of issued capital and borrowings has

increased in the recent years. This implies that the proportion of the funds generated from the

owner’s fund and borrowings has increased (Lee and Kim 2017).

Answer to question iv)

Different sources of funds raised by the chosen company in the analysis is Equity

capital, reserves and borrowings.

Advantages of equity finance:

Unlike loan or debentures, equity capital do not entitle the business to make regular

payments to the investors investing money into the business. Business is able to add

value and share the risk at the same time by issuing equity to the investors. Investment

is only realized when the business earns and return is generated from the profits in the

form of dividends (Hoggett et al. 2018).

With the growth in business, investors are also willing to contribute by following up

the funding. Hence, business can rely on equity financing for further development and

growth of the business.

Several valuable skills, contacts and experience is brought by the venture capitalists

and businesses investors and thereby assign the company in formulating strategy and

making decisions.

Shortcomings of equity finance:

generated funds in the total funds has decreased as indicated from falling figure of reserves.

Now, observing the figure of percentage of externally generated funds, it is viewed that the

proportion of externally generated funds has increased over the years from 100% to 105% in

year 2019 (bestonglobalfoods.com.au 2020). From the computed figures, it is inferred that the

proportion of externally generated funds comprising of issued capital and borrowings has

increased in the recent years. This implies that the proportion of the funds generated from the

owner’s fund and borrowings has increased (Lee and Kim 2017).

Answer to question iv)

Different sources of funds raised by the chosen company in the analysis is Equity

capital, reserves and borrowings.

Advantages of equity finance:

Unlike loan or debentures, equity capital do not entitle the business to make regular

payments to the investors investing money into the business. Business is able to add

value and share the risk at the same time by issuing equity to the investors. Investment

is only realized when the business earns and return is generated from the profits in the

form of dividends (Hoggett et al. 2018).

With the growth in business, investors are also willing to contribute by following up

the funding. Hence, business can rely on equity financing for further development and

growth of the business.

Several valuable skills, contacts and experience is brought by the venture capitalists

and businesses investors and thereby assign the company in formulating strategy and

making decisions.

Shortcomings of equity finance:

CORPORATE ACCOUNTING

In event of the company making significant investment in equity, there exist the risk

of loss control as some of the ownership and the equity capital owners retain

authority. The opportunity of the business to earn more profit would be lost due to the

impact of counter effect of sharing the risks (Hellman et al. 2018).

While raising funds, business would be required to comply with various regulatory

and legal issues and this sometimes make it difficult for business in carrying out its

investment seamlessly.

Advantages of reserves:

One of the main benefits of reserve is that the business would be provided with

readily available funds and there is not any requirement of raising any additional

funds from investors if the business has enough reserves.

The cost of raising additional funds is reduced and the loss in event of under-pricing

is also eliminated due to the retailed earnings or reserves.

It is also not required by the business to perform any formalities or comply with some

laws and regulation and any dilution or change in the control of ownership is avoided

when using reserves. In addition to this, retained earnings do not hold any negative

connotations as the issue of equity is viewed as doubtful.

Shortcomings of reserves:

The requirement of business to raise funds might not be fulfilled by the availability of

amount of reserve, as the amounts of funds raised through retailed earning is limited.

The complete benefits of the actual earnings generated by the company cannot be

enjoyed by the shareholders, which might adversely influence the market value of

shares and dissatisfy the existing shareholders.

In event of the company making significant investment in equity, there exist the risk

of loss control as some of the ownership and the equity capital owners retain

authority. The opportunity of the business to earn more profit would be lost due to the

impact of counter effect of sharing the risks (Hellman et al. 2018).

While raising funds, business would be required to comply with various regulatory

and legal issues and this sometimes make it difficult for business in carrying out its

investment seamlessly.

Advantages of reserves:

One of the main benefits of reserve is that the business would be provided with

readily available funds and there is not any requirement of raising any additional

funds from investors if the business has enough reserves.

The cost of raising additional funds is reduced and the loss in event of under-pricing

is also eliminated due to the retailed earnings or reserves.

It is also not required by the business to perform any formalities or comply with some

laws and regulation and any dilution or change in the control of ownership is avoided

when using reserves. In addition to this, retained earnings do not hold any negative

connotations as the issue of equity is viewed as doubtful.

Shortcomings of reserves:

The requirement of business to raise funds might not be fulfilled by the availability of

amount of reserve, as the amounts of funds raised through retailed earning is limited.

The complete benefits of the actual earnings generated by the company cannot be

enjoyed by the shareholders, which might adversely influence the market value of

shares and dissatisfy the existing shareholders.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE ACCOUNTING

For the company with conservative dividend policy, there also exist a risk of over

capitalization due to the huge accumulation of the reserves.

The retained earnings have considerably higher opportunity cost and the companies

which do not vale such costs might end up investing in any project generating

negative return.

Advantages of borrowings:

Borrowing or issuing debenture is considered economical because the amount can be

borrowed at lower interest rate and thereby making it the cheaper method of raising

funds.

Management and the debenture holders are apart that is there is no involvement and

non-interference of the mender into the decision-making and other issues of the

company. Compared to issuing shares, price of debentures or borrowing money is

stable because the price movement of debentures is impacted insignificantly due to

change in monetary conditions.

The procedures and method of raising funds through borrowing or issuing debentures

is easier than raising funds by way of equity capital or issuing shares.

Shortcomings of borrowings:

Company faces the burden of making payment of interest as the interest to be paid on

debts issued is considered to be cumulative. Regardless of the profits generated by the

company during the financial year, it is required to make payment of interest. Such

interest payment becomes a burden for the company during the period of depression

when enough profits is not generated (Gheta 2017).

For the company with conservative dividend policy, there also exist a risk of over

capitalization due to the huge accumulation of the reserves.

The retained earnings have considerably higher opportunity cost and the companies

which do not vale such costs might end up investing in any project generating

negative return.

Advantages of borrowings:

Borrowing or issuing debenture is considered economical because the amount can be

borrowed at lower interest rate and thereby making it the cheaper method of raising

funds.

Management and the debenture holders are apart that is there is no involvement and

non-interference of the mender into the decision-making and other issues of the

company. Compared to issuing shares, price of debentures or borrowing money is

stable because the price movement of debentures is impacted insignificantly due to

change in monetary conditions.

The procedures and method of raising funds through borrowing or issuing debentures

is easier than raising funds by way of equity capital or issuing shares.

Shortcomings of borrowings:

Company faces the burden of making payment of interest as the interest to be paid on

debts issued is considered to be cumulative. Regardless of the profits generated by the

company during the financial year, it is required to make payment of interest. Such

interest payment becomes a burden for the company during the period of depression

when enough profits is not generated (Gheta 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE ACCOUNTING

The credit worthiness of the company is limited or constrained due to borrowing

money or issuing debentures. This is so because it is required by the company in most

of the cases to mortgage their assets to the debenture holders as a security. In such

scenario, the credibility of the company reduces and it might become difficult to

source additional funds (Dudar and Voget 2016).

Answer to question v)

Liabilities of the company are segregated into current liabilities and non-current

liabilities. Different types of non-current liabilities disclosed by Australia Vintage limited in

their statement of financial position are borrowings, financial liabilities and provisions and

current liabilities comprised of provisions, income received in advance, trade and other

payables, borrowings and other financial liabilities. It is observed that the value of non-

current liabilities is higher that the values of current liabilities for the three consecutive

financial year. Total mount of borrowings of Vintage limited is higher of all the other items

of liabilities followed by trade and other payables (Australianvintage.com.au 2020).

For Beston Global Food limited, it is observed that the liabilities comprise of both

current and non-current liabilities. The items reported under current liabilities include

borrowings, trade and other payable, employee benefit obligations and current tax liabilities.

Noncurrent liabilities on other hand comprised of deferred tax liabilities, borrowings,

employee benefits obligation and deferred tax liabilities. It is observed that in year 2018 and

2017, total amount of non-current liabilities was considerably lower that the current liabilities

reported in the financial year 2019. However, the amount of non-current liabilities increased

and this increment is attributable to the increase in total borrowing amount

(bestonglobalfoods.com.au 2020). ‘

The credit worthiness of the company is limited or constrained due to borrowing

money or issuing debentures. This is so because it is required by the company in most

of the cases to mortgage their assets to the debenture holders as a security. In such

scenario, the credibility of the company reduces and it might become difficult to

source additional funds (Dudar and Voget 2016).

Answer to question v)

Liabilities of the company are segregated into current liabilities and non-current

liabilities. Different types of non-current liabilities disclosed by Australia Vintage limited in

their statement of financial position are borrowings, financial liabilities and provisions and

current liabilities comprised of provisions, income received in advance, trade and other

payables, borrowings and other financial liabilities. It is observed that the value of non-

current liabilities is higher that the values of current liabilities for the three consecutive

financial year. Total mount of borrowings of Vintage limited is higher of all the other items

of liabilities followed by trade and other payables (Australianvintage.com.au 2020).

For Beston Global Food limited, it is observed that the liabilities comprise of both

current and non-current liabilities. The items reported under current liabilities include

borrowings, trade and other payable, employee benefit obligations and current tax liabilities.

Noncurrent liabilities on other hand comprised of deferred tax liabilities, borrowings,

employee benefits obligation and deferred tax liabilities. It is observed that in year 2018 and

2017, total amount of non-current liabilities was considerably lower that the current liabilities

reported in the financial year 2019. However, the amount of non-current liabilities increased

and this increment is attributable to the increase in total borrowing amount

(bestonglobalfoods.com.au 2020). ‘

CORPORATE ACCOUNTING

The interest bearing liabilities for both the companies is borrowings as the company is

required to make regular payment of interest to the debenture holder or the banks from which

the money has been borrowed. In this regard, it is important for the company to compute the

cost of debt or cost of financing the projects using debt. It is so because payment of interest

has to be made either quarterly or annually. No other items other than borrowing shown in

the balance sheet of the companies bear interest. These items include other financial

liabilities, trade and other payables, income received in advance, provisions, deferred tax

liabilities, current tax liabilities and employee benefits obligations (Fargher et al. 2019).

Answer to question vi)

Standard AASB 137 is applicable for all the entities that accounts for transactions and

the provision as per this standard is defined as the liabilities pertaining to uncertain amount or

timing. Provision in some countries is also used in the context of asset impairment,

depreciation and doubtful debts. The restructuring provisions is addressed in this standard

and this also helps in creating distinction between of accruals and trade payables from

provisions. It is so because there exist uncertainty in the amount and timing of the future

expenditure in the settlement. Reporting of provisions as per the standard is done separately

(Aasb.gov.au 2020). Due to the uncertainty in the amount and timing, provisions are

considered contingent.

Recognition of provisions is done as liabilities as there exist the probability that the

settlement of the obligations would require the resource outflow that embodies economic

benefits. This is the reason the provisions according to the definition of the standard is also

known and recognized as liabilities. As per the standard, recognitions of the provisions

should be done when the impact of any past event creates a present obligation for the entity.

The obligation amount can be measured reliably using the appropriate estimate and the

The interest bearing liabilities for both the companies is borrowings as the company is

required to make regular payment of interest to the debenture holder or the banks from which

the money has been borrowed. In this regard, it is important for the company to compute the

cost of debt or cost of financing the projects using debt. It is so because payment of interest

has to be made either quarterly or annually. No other items other than borrowing shown in

the balance sheet of the companies bear interest. These items include other financial

liabilities, trade and other payables, income received in advance, provisions, deferred tax

liabilities, current tax liabilities and employee benefits obligations (Fargher et al. 2019).

Answer to question vi)

Standard AASB 137 is applicable for all the entities that accounts for transactions and

the provision as per this standard is defined as the liabilities pertaining to uncertain amount or

timing. Provision in some countries is also used in the context of asset impairment,

depreciation and doubtful debts. The restructuring provisions is addressed in this standard

and this also helps in creating distinction between of accruals and trade payables from

provisions. It is so because there exist uncertainty in the amount and timing of the future

expenditure in the settlement. Reporting of provisions as per the standard is done separately

(Aasb.gov.au 2020). Due to the uncertainty in the amount and timing, provisions are

considered contingent.

Recognition of provisions is done as liabilities as there exist the probability that the

settlement of the obligations would require the resource outflow that embodies economic

benefits. This is the reason the provisions according to the definition of the standard is also

known and recognized as liabilities. As per the standard, recognitions of the provisions

should be done when the impact of any past event creates a present obligation for the entity.

The obligation amount can be measured reliably using the appropriate estimate and the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.