Corporate Accounting Report: Funding Sources, Provisions, and Assets

VerifiedAdded on 2022/08/23

|16

|768

|15

Report

AI Summary

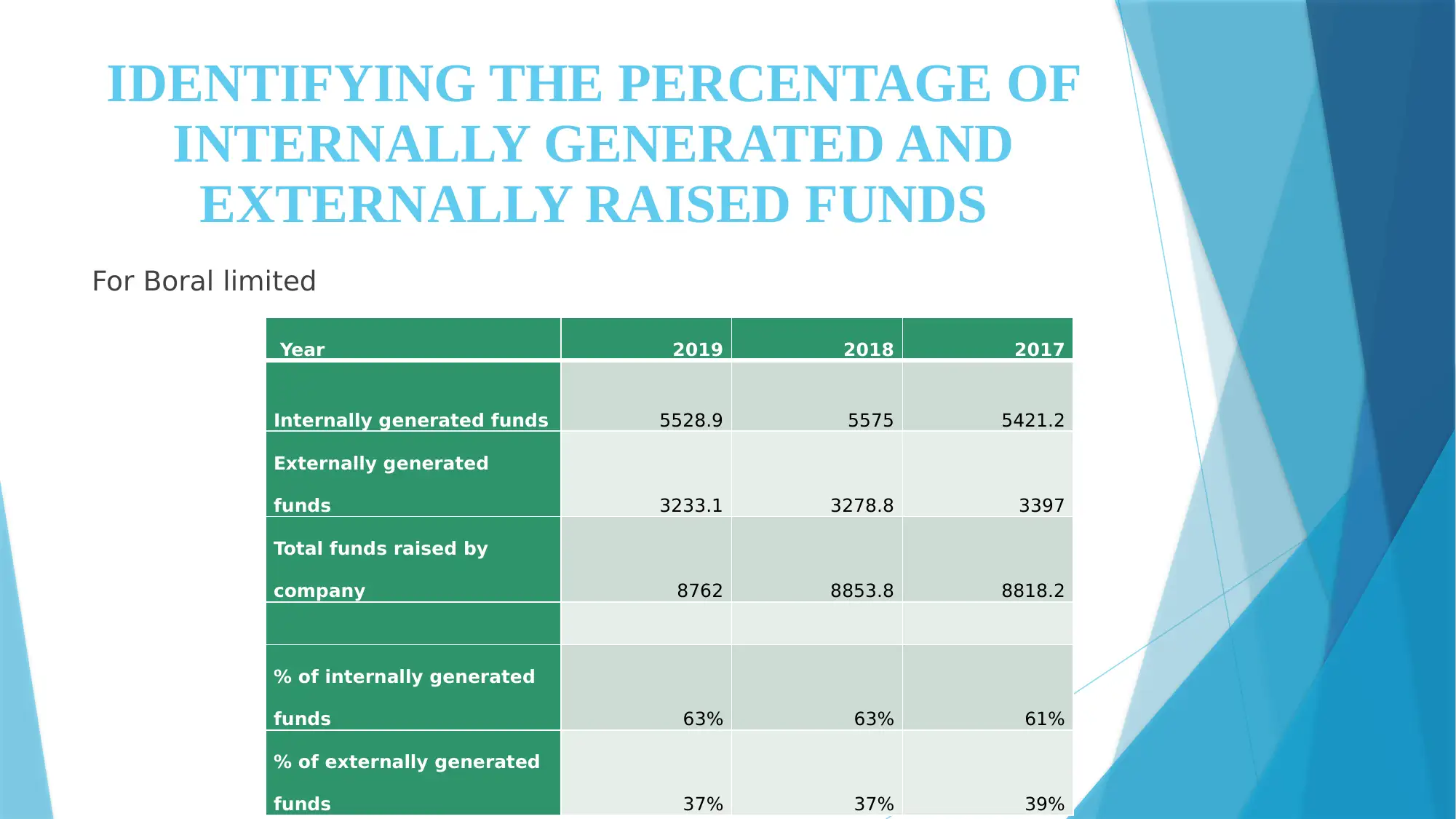

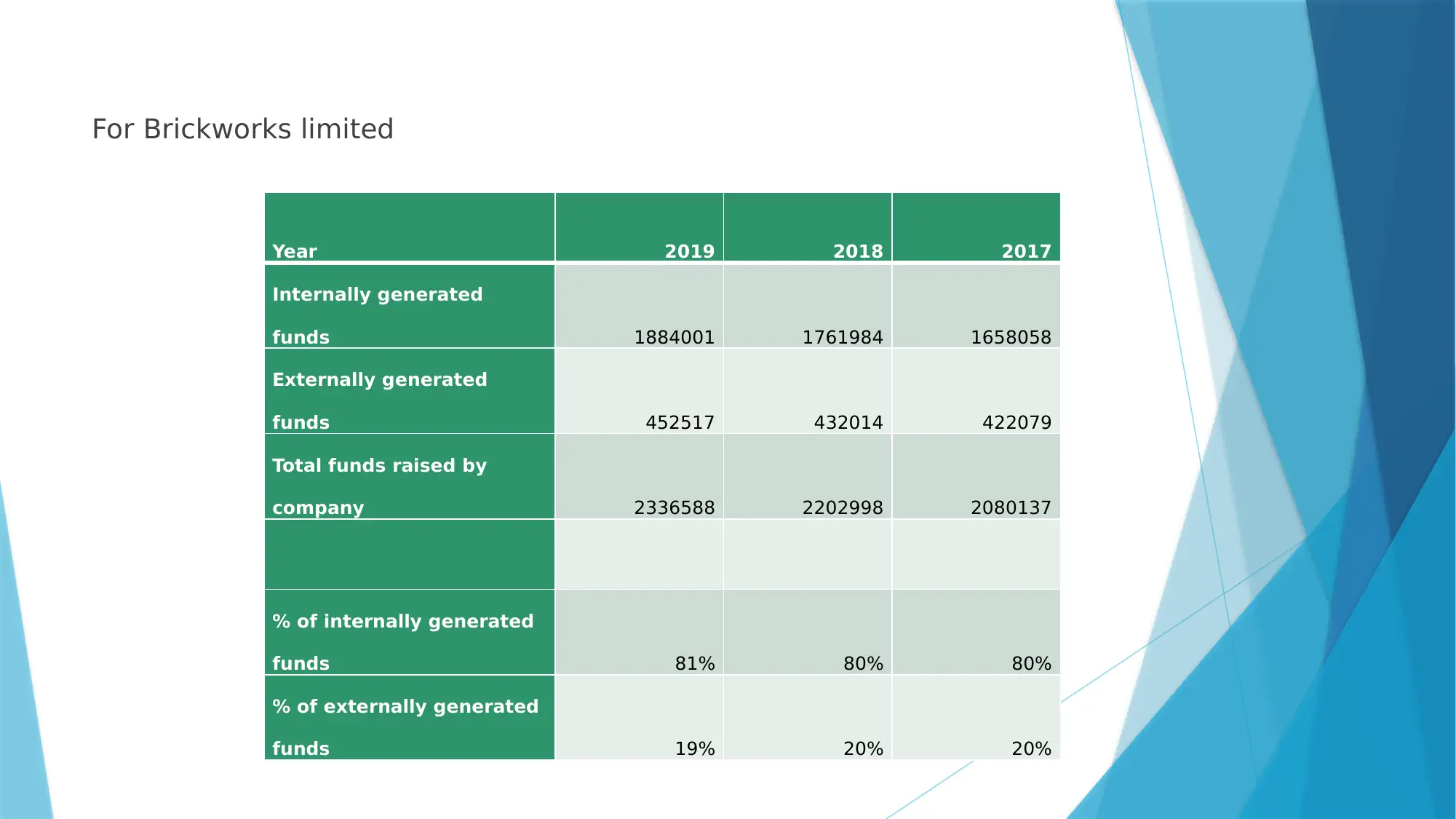

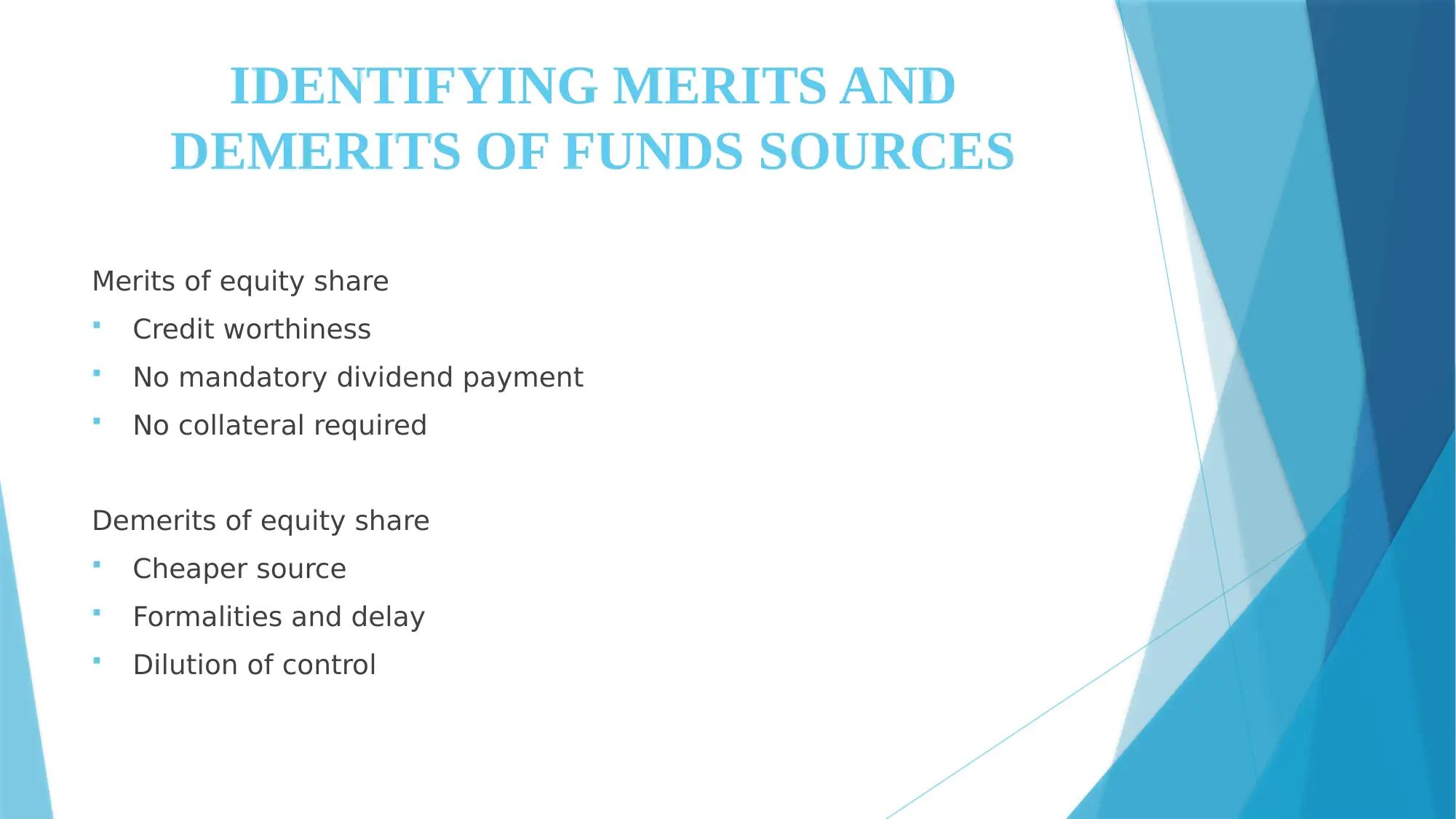

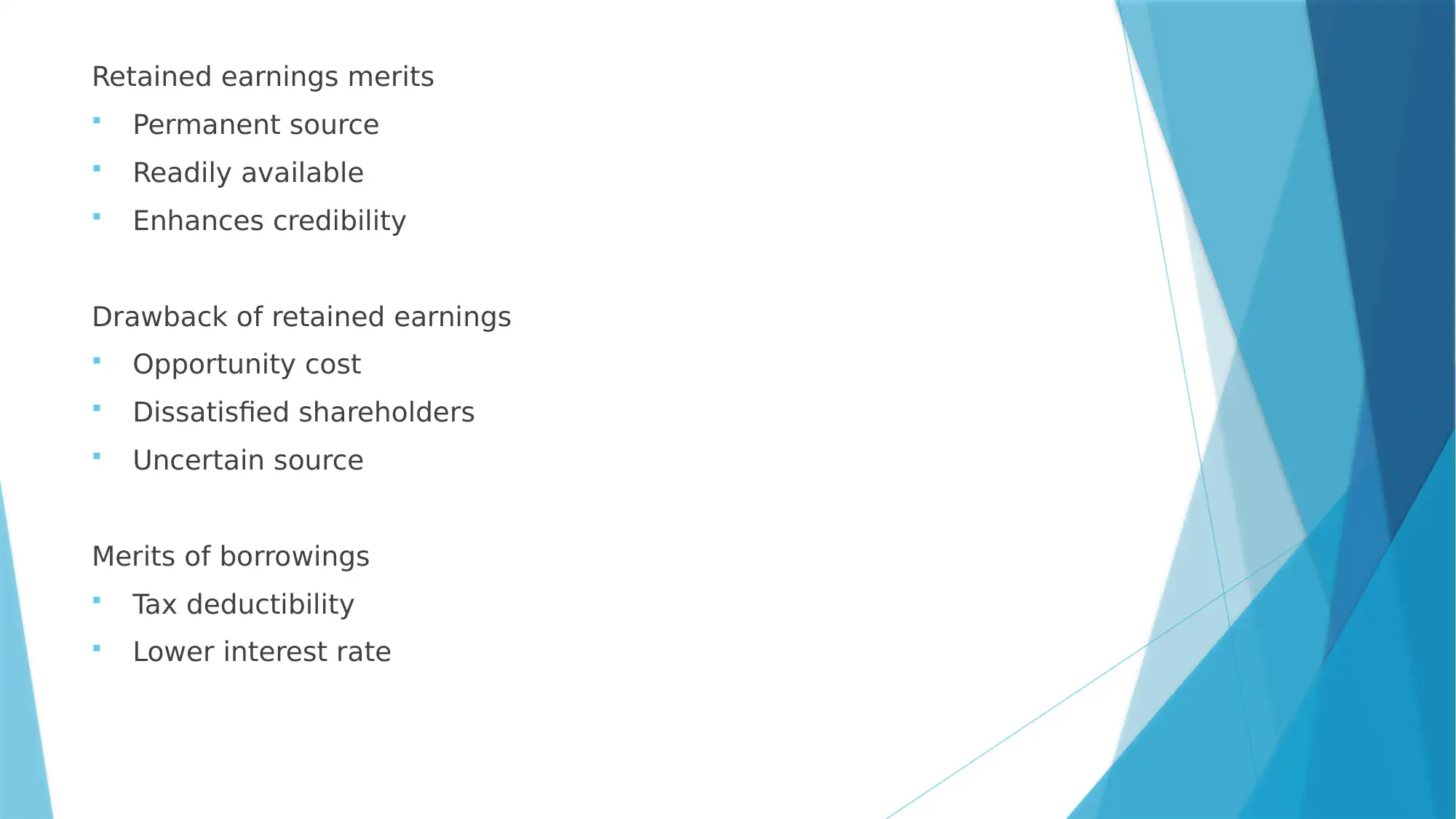

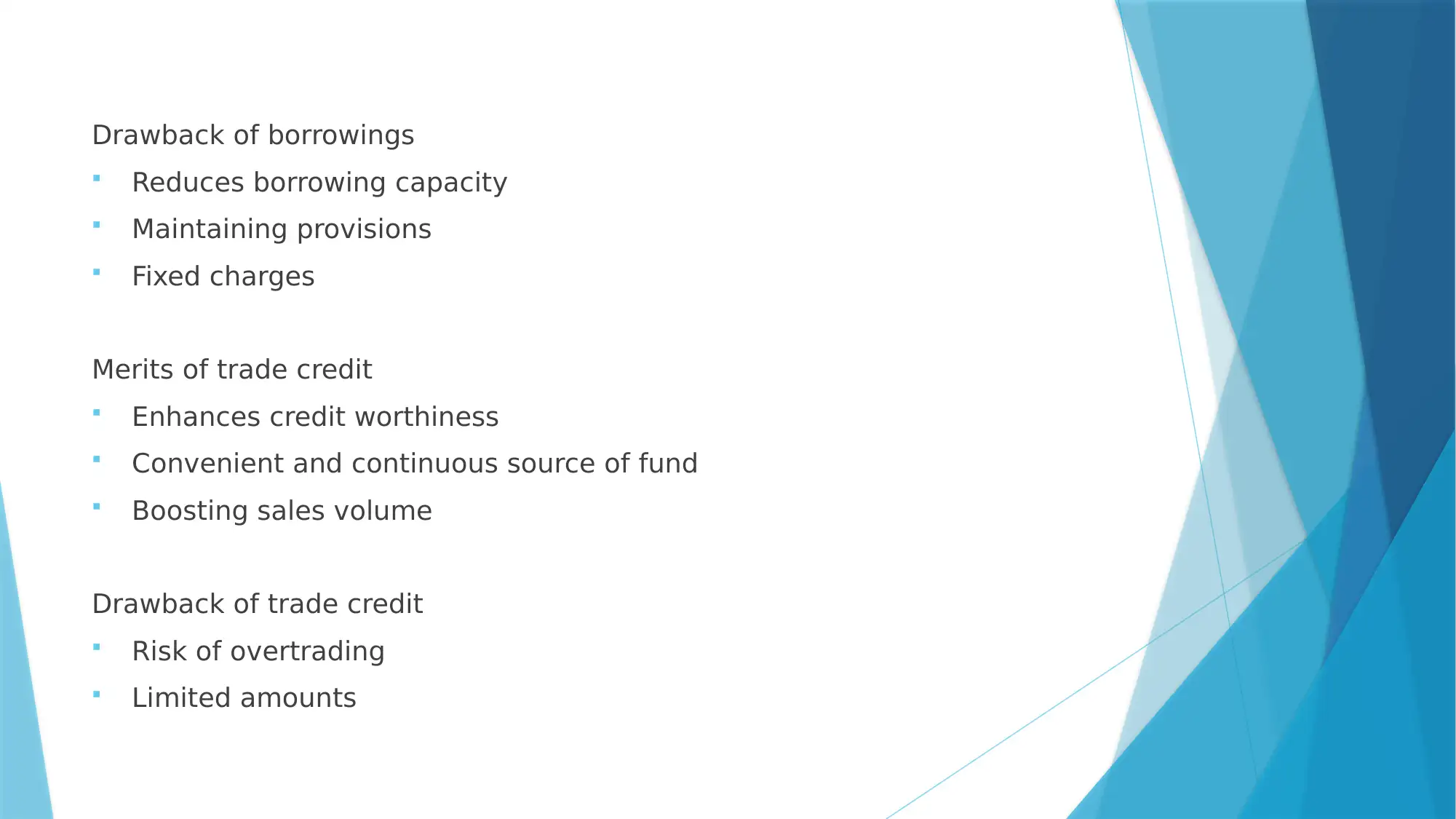

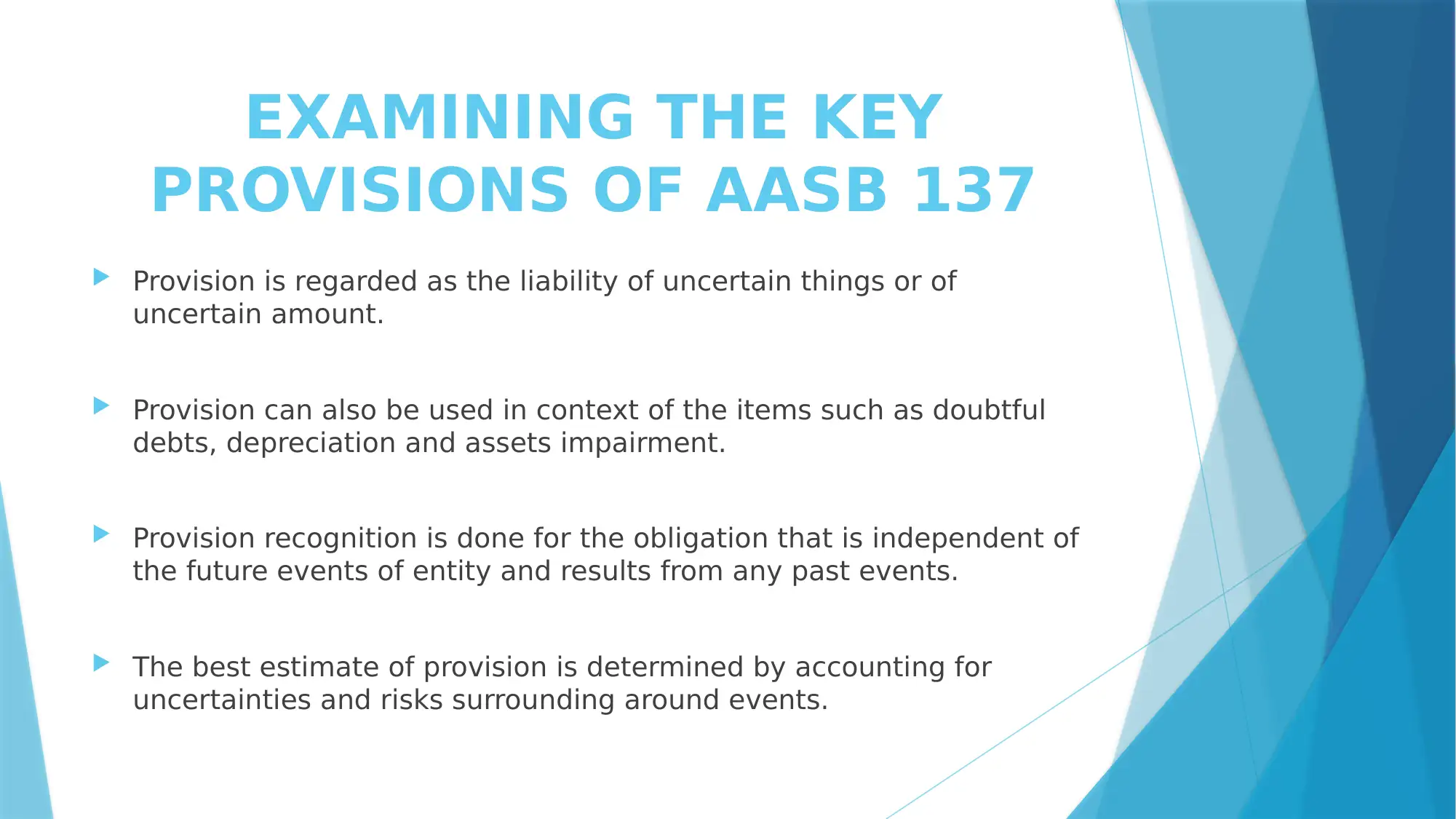

This report provides an in-depth analysis of corporate accounting practices, focusing on the funding sources utilized by organizations, with Boral Limited and Brickworks Limited serving as case studies. It identifies both internally generated funds, such as retained earnings and equity, and externally raised funds, including borrowings and trade credit. The report evaluates the merits and demerits of each funding source, considering factors like creditworthiness, dividend policies, and potential impacts on control. Furthermore, it examines the application of AASB 137, provisions, contingent liabilities, and contingent assets, analyzing the liabilities and assets reported by the chosen companies and their measurement bases. The analysis includes an assessment of the companies' compliance with AASB 137, specifically regarding the recognition and measurement of provisions. The report concludes by emphasizing the importance of maintaining an optimal balance between internal and external funding to achieve optimal financial leverage. The analysis covers the different classes of assets recorded and their measurement basis, including inventories, receivables, plant, property, equipment, and goodwill. References include key accounting standards and relevant literature on corporate finance and reporting.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.