Corporate Governance: Strategies, Accounting, and Failures Analysis

VerifiedAdded on 2022/08/23

|12

|2481

|20

Report

AI Summary

This report provides an in-depth analysis of corporate governance, focusing on the practices and strategies of BHP Group and Rio Tinto. It examines key indicators like director numbers, executive shareholdings, and CEO statements, comparing their approaches to corporate governance. The report then delves into the critical role of corporate governance in accounting, highlighting how accounting practices support business decisions, ensure transparency, and provide financial information to stakeholders. It further discusses the responsibilities of accountants in maintaining accountability and transparency within organizations. The report also explores the impact of regulatory bodies like ASIC and the reasons behind corporate governance failures, such as leadership experience and confusion about the role of good governance. Finally, it concludes by emphasizing the interconnectedness of accounting and corporate governance, underscoring how good governance builds customer trust and reduces capital costs, while accounting provides a clear picture of organizational activities and sets the standards for governance processes.

Running Head: Corporate Governance

Corporate Governance

Name of the Student

Name of the University

Author Note

Corporate Governance

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Corporate Governance

Table of Contents

Part A.........................................................................................................................................2

Part B..........................................................................................................................................4

Corporate Governance

Table of Contents

Part A.........................................................................................................................................2

Part B..........................................................................................................................................4

2

Corporate Governance

Part A

1. The two companies which have been selected are BHP Group and Rio Tinto and their

strategies, policies and practices of corporate governance are discussed below-

BHP Group-

According to BHP Group, they believe in high quality governance support for the

creation of long term value as good governance leads to good business. The approach of

BHP is to adopt the standards of governance in Australia, the United States and the

United Kingdom. The Financial Reporting Council has released the UK Corporate

Governance Code and the Guidance on the Effectiveness of Board of 2018 in July 2018.

It helps to describe the importance of demonstrating the corporate governance structure

through reporting and how it helps to achieve wider objectives by contributing in the

long-term sustainable success (Bhp.com, 2020).

Rio Tinto-

According to Rio Tinto, they produce those materials which are important for human

progress. This purpose requires them to work in remote and sensitive locations which are

owned by indigenous people. The values of Rio Tinto put emphasise on delivering

products with long lasting benefits for the owners of the company as well as for the

community in which they operate. The group has launched its first integrated sustainable

strategy in 2018. According to this strategy, the group has committed to adopt high

standards, aiming beyond the legal requirements and issuing of materials for the business

and the stakeholders. At the same time, they lead to innovate few key areas which will

strengthen their contribution in the society and sharpen their competitive advantage

(Riotinto.com, 2020).

Corporate Governance

Part A

1. The two companies which have been selected are BHP Group and Rio Tinto and their

strategies, policies and practices of corporate governance are discussed below-

BHP Group-

According to BHP Group, they believe in high quality governance support for the

creation of long term value as good governance leads to good business. The approach of

BHP is to adopt the standards of governance in Australia, the United States and the

United Kingdom. The Financial Reporting Council has released the UK Corporate

Governance Code and the Guidance on the Effectiveness of Board of 2018 in July 2018.

It helps to describe the importance of demonstrating the corporate governance structure

through reporting and how it helps to achieve wider objectives by contributing in the

long-term sustainable success (Bhp.com, 2020).

Rio Tinto-

According to Rio Tinto, they produce those materials which are important for human

progress. This purpose requires them to work in remote and sensitive locations which are

owned by indigenous people. The values of Rio Tinto put emphasise on delivering

products with long lasting benefits for the owners of the company as well as for the

community in which they operate. The group has launched its first integrated sustainable

strategy in 2018. According to this strategy, the group has committed to adopt high

standards, aiming beyond the legal requirements and issuing of materials for the business

and the stakeholders. At the same time, they lead to innovate few key areas which will

strengthen their contribution in the society and sharpen their competitive advantage

(Riotinto.com, 2020).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Corporate Governance

2. Computation of the following indicators of corporate governance collected from the

annual reports of BHP Group and Rio Tinto-

Particulars BHP Group Rio Tinto

a. Total number of

directors

15 directors 8 directors

b. Percentage of non-

executive directors

46.66 % 100 %

c. Percentage of

independent

directors

66.66 % 100 %

d. Chief Executive

Officer

Andrew Mackenzie Jean- Sebastian Jacques

Summary of CEO’s

statement

According to him, BHP is

successful when the people

start their day with a

purpose and ends with

accomplishment and they

have an inclusive and

cultured team with good

relationships between the

suppliers, customers and

communities.

According to the CEO,

Rio Tinto has a global

tailing standard since 2015

and the financial year

2018 has been another

solid year fir them as they

have declared $13.5

billion cash returns to the

shareholder. It has been

highest in the history of

Rio Tinto

e. Percentage of shares

hold by executive

2.60 % 11.8 (multiple base fee)

Corporate Governance

2. Computation of the following indicators of corporate governance collected from the

annual reports of BHP Group and Rio Tinto-

Particulars BHP Group Rio Tinto

a. Total number of

directors

15 directors 8 directors

b. Percentage of non-

executive directors

46.66 % 100 %

c. Percentage of

independent

directors

66.66 % 100 %

d. Chief Executive

Officer

Andrew Mackenzie Jean- Sebastian Jacques

Summary of CEO’s

statement

According to him, BHP is

successful when the people

start their day with a

purpose and ends with

accomplishment and they

have an inclusive and

cultured team with good

relationships between the

suppliers, customers and

communities.

According to the CEO,

Rio Tinto has a global

tailing standard since 2015

and the financial year

2018 has been another

solid year fir them as they

have declared $13.5

billion cash returns to the

shareholder. It has been

highest in the history of

Rio Tinto

e. Percentage of shares

hold by executive

2.60 % 11.8 (multiple base fee)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Corporate Governance

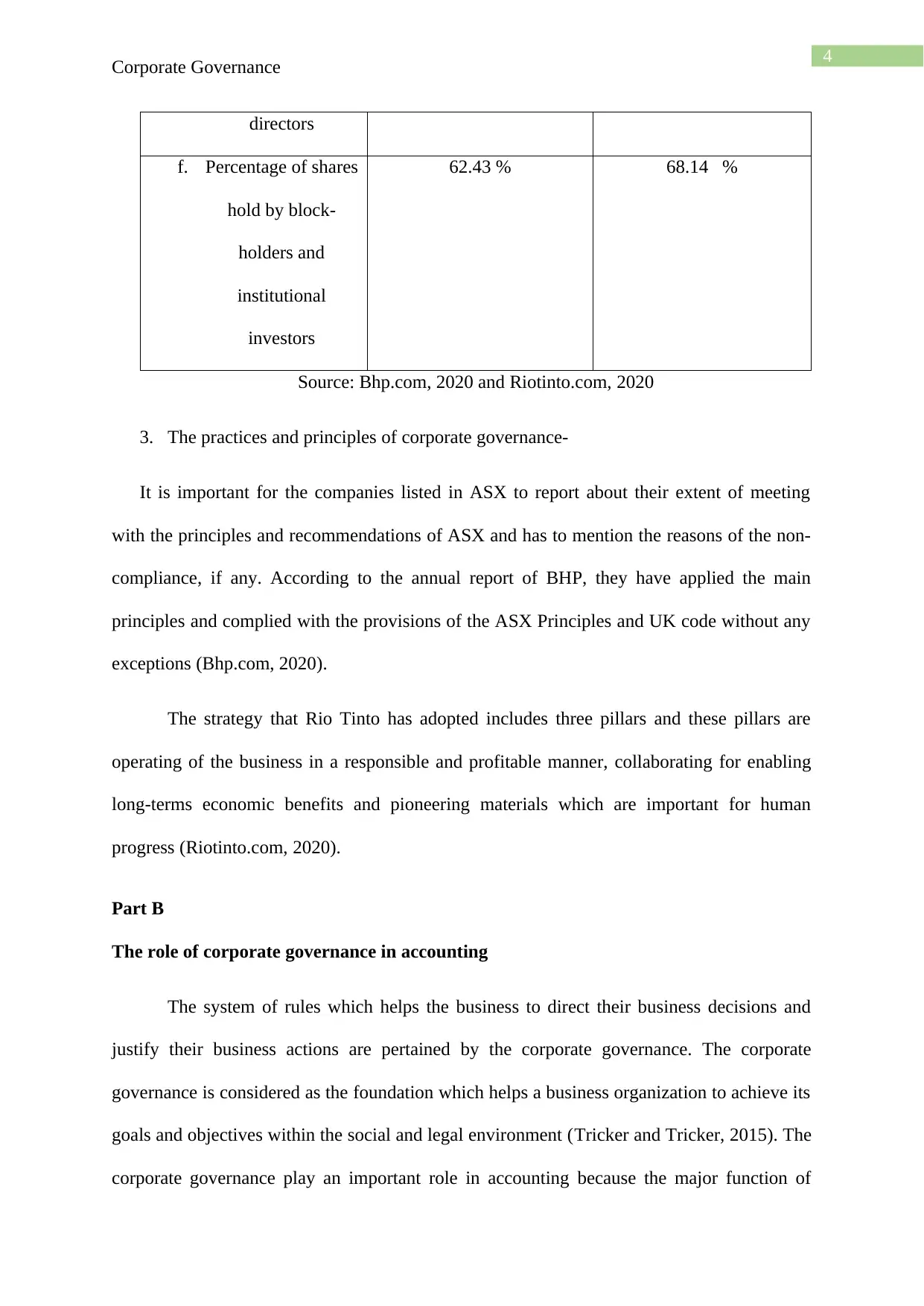

directors

f. Percentage of shares

hold by block-

holders and

institutional

investors

62.43 % 68.14 %

Source: Bhp.com, 2020 and Riotinto.com, 2020

3. The practices and principles of corporate governance-

It is important for the companies listed in ASX to report about their extent of meeting

with the principles and recommendations of ASX and has to mention the reasons of the non-

compliance, if any. According to the annual report of BHP, they have applied the main

principles and complied with the provisions of the ASX Principles and UK code without any

exceptions (Bhp.com, 2020).

The strategy that Rio Tinto has adopted includes three pillars and these pillars are

operating of the business in a responsible and profitable manner, collaborating for enabling

long-terms economic benefits and pioneering materials which are important for human

progress (Riotinto.com, 2020).

Part B

The role of corporate governance in accounting

The system of rules which helps the business to direct their business decisions and

justify their business actions are pertained by the corporate governance. The corporate

governance is considered as the foundation which helps a business organization to achieve its

goals and objectives within the social and legal environment (Tricker and Tricker, 2015). The

corporate governance play an important role in accounting because the major function of

Corporate Governance

directors

f. Percentage of shares

hold by block-

holders and

institutional

investors

62.43 % 68.14 %

Source: Bhp.com, 2020 and Riotinto.com, 2020

3. The practices and principles of corporate governance-

It is important for the companies listed in ASX to report about their extent of meeting

with the principles and recommendations of ASX and has to mention the reasons of the non-

compliance, if any. According to the annual report of BHP, they have applied the main

principles and complied with the provisions of the ASX Principles and UK code without any

exceptions (Bhp.com, 2020).

The strategy that Rio Tinto has adopted includes three pillars and these pillars are

operating of the business in a responsible and profitable manner, collaborating for enabling

long-terms economic benefits and pioneering materials which are important for human

progress (Riotinto.com, 2020).

Part B

The role of corporate governance in accounting

The system of rules which helps the business to direct their business decisions and

justify their business actions are pertained by the corporate governance. The corporate

governance is considered as the foundation which helps a business organization to achieve its

goals and objectives within the social and legal environment (Tricker and Tricker, 2015). The

corporate governance play an important role in accounting because the major function of

5

Corporate Governance

accounting tasks is to track the financial performance of a business organization. Therefore,

these tasks accounting tasks are important to determine the role of the company to fulfil the

policies of corporate governance (Armstrong, et al., 2015).

The accounting practices are termed as an effective instrument of corporate

governance as the business organizations are responsible for making advantageous and

intelligent decisions with respect to operation and expansion of the business and the ability to

invest in a project when there is accurate accounting data in the management (Honggowati, et

al., 2017). Similarly, the public limited companies unlike the private companies have the

legal responsibility for disclosing their business practices to the external parties which are

involved in the business. Therefore, such business corporations are needed to release accurate

and honest financial statement like the income statement, balance sheet and statement of

shareholders’ equity for the external users. These information is helpful to the investors as

this will help them to take the decision about investment and at the same time this

information is useful to the government to see whether the companies disclose its operations

fully or not. Thus, the accounting practices play an important role to produce these statements

to the external parties (Kabir and Rahman, 2016).

On the other hand, it is important for the business organizations to release required

and detailed financial information to the shareholders other than the market and the

government. The decisions of the company influence the shareholders whether the

shareholders should hold their shares, buy their shares or sell their shares in the stock of the

firm. The financial statements which are prepared by the accounting department of the

business organization contains the most important and intelligent decisions of the business as

well as the shareholders. Hence, the shareholders rely on the produced financial statement to

a great extent (Larcker and Tayan, 2015).

Corporate Governance

accounting tasks is to track the financial performance of a business organization. Therefore,

these tasks accounting tasks are important to determine the role of the company to fulfil the

policies of corporate governance (Armstrong, et al., 2015).

The accounting practices are termed as an effective instrument of corporate

governance as the business organizations are responsible for making advantageous and

intelligent decisions with respect to operation and expansion of the business and the ability to

invest in a project when there is accurate accounting data in the management (Honggowati, et

al., 2017). Similarly, the public limited companies unlike the private companies have the

legal responsibility for disclosing their business practices to the external parties which are

involved in the business. Therefore, such business corporations are needed to release accurate

and honest financial statement like the income statement, balance sheet and statement of

shareholders’ equity for the external users. These information is helpful to the investors as

this will help them to take the decision about investment and at the same time this

information is useful to the government to see whether the companies disclose its operations

fully or not. Thus, the accounting practices play an important role to produce these statements

to the external parties (Kabir and Rahman, 2016).

On the other hand, it is important for the business organizations to release required

and detailed financial information to the shareholders other than the market and the

government. The decisions of the company influence the shareholders whether the

shareholders should hold their shares, buy their shares or sell their shares in the stock of the

firm. The financial statements which are prepared by the accounting department of the

business organization contains the most important and intelligent decisions of the business as

well as the shareholders. Hence, the shareholders rely on the produced financial statement to

a great extent (Larcker and Tayan, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Corporate Governance

The quality and the accuracy of the accounting data helps the business organization to

take almost every business decisions. This data is helpful for the business organizations since

it helps to make intelligent choices like prioritising of the project and managing of assets. At

the same time, the accounting data helps the managers of the companies to show about their

income level, the source of the income and the when the managers are expected to receive the

same. The accounting data also helps the management to take decision about recruitment,

acquisition of more equipment and to take more debt or not (Armstrong, 2015).

The role of an accountant in corporate governance is wide as it ensures accountability

and transparency in the daily operations of a business organization. The responsibility of a

business organization to provide correct and true information to the shareholders as well as

the stakeholders rests on the shoulders of the accountants and therefore the accountants are

the people who help in building the trust of the stakeholders on the brand of the company.

However, in terms of corporate governance the role of the accountants is two-folded. The

first responsibility of the accountants include to report on the flow of the capital in various

departments of the organization and to monitor those activities which are undertaken for

carrying out with the capital and where the capital is getting invested. On the other hand, the

second responsibility of the accountant is concerned with the ensuring of the proper and

detailed framework of the accountability and transparency for the purpose of addressing the

interests of the stakeholders (Larcker and Tayan, 2015).

The Corporate Law Economic Reform Program is the latest proposal of the

government that has been released into the environment which is keen to see that there are

tighter control in the corporate governance. This has been issued by the federal government

on October 8, 2013 for the next stage of Corporate Law Economic Reform Program (CLERP

9). The CLERP 9 issues paper which contains the Corporate Disclosure for strengthening the

framework of financial reporting (Giofré, 2016). On the other hand, the Australian Securities

Corporate Governance

The quality and the accuracy of the accounting data helps the business organization to

take almost every business decisions. This data is helpful for the business organizations since

it helps to make intelligent choices like prioritising of the project and managing of assets. At

the same time, the accounting data helps the managers of the companies to show about their

income level, the source of the income and the when the managers are expected to receive the

same. The accounting data also helps the management to take decision about recruitment,

acquisition of more equipment and to take more debt or not (Armstrong, 2015).

The role of an accountant in corporate governance is wide as it ensures accountability

and transparency in the daily operations of a business organization. The responsibility of a

business organization to provide correct and true information to the shareholders as well as

the stakeholders rests on the shoulders of the accountants and therefore the accountants are

the people who help in building the trust of the stakeholders on the brand of the company.

However, in terms of corporate governance the role of the accountants is two-folded. The

first responsibility of the accountants include to report on the flow of the capital in various

departments of the organization and to monitor those activities which are undertaken for

carrying out with the capital and where the capital is getting invested. On the other hand, the

second responsibility of the accountant is concerned with the ensuring of the proper and

detailed framework of the accountability and transparency for the purpose of addressing the

interests of the stakeholders (Larcker and Tayan, 2015).

The Corporate Law Economic Reform Program is the latest proposal of the

government that has been released into the environment which is keen to see that there are

tighter control in the corporate governance. This has been issued by the federal government

on October 8, 2013 for the next stage of Corporate Law Economic Reform Program (CLERP

9). The CLERP 9 issues paper which contains the Corporate Disclosure for strengthening the

framework of financial reporting (Giofré, 2016). On the other hand, the Australian Securities

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

Corporate Governance

and Investments Commission acts as a corporate regulator of Australia and it is an

independent government body of Australia. The purpose of ASIC is to regulate and enforce

the company law and the financial services law for protecting the consumers, creditors and

investors of Australia. The directors as well as the officers of the company play an important

role in the maintenance of the standard of the corporate governance of the company and the

corporate governance has been considered as the driver of the operations as well as the

performance of the business organization (Kabir and Rahman, 2016). The guidelines of ASIC

helps in assisting the entities along with the individuals to comply with the rules and

regulations of ASIC and to take proper decisions in the best interests for the investors. The

ASIC maintains relationship with the stakeholders regarding the issues related to corporate

governance with the help of external publications, speeches and events (Comino, 2015).

However, sometimes companies fail to keep pace with the corporate governance and

the reasons why they fail is discussed below-

Experience in Leadership- There are many organizations which are having ill-trained

and poor directors and therefore they lack in their commitment. They focus mainly on

the short-term profitability, management of assets, cost-cutting initiatives over the

less-tangible challenge which helps in the enhancement of the culture of the company.

Therefore, the cultural issues of the company receive less attention and the KPIs and

goals are not in place hence it creates conflict and chaos for the stakeholders at all

levels.

Confusion about the role of the good governance- There are many organizations

which do not understand the importance of governance and fails to admit it as a

business philosophy. As a result, there is no change in the attitude and practices of the

personnel of the organization. Mostly, the business organizations set up a compliance

department and think this will help to set up a good corporate governance but this

Corporate Governance

and Investments Commission acts as a corporate regulator of Australia and it is an

independent government body of Australia. The purpose of ASIC is to regulate and enforce

the company law and the financial services law for protecting the consumers, creditors and

investors of Australia. The directors as well as the officers of the company play an important

role in the maintenance of the standard of the corporate governance of the company and the

corporate governance has been considered as the driver of the operations as well as the

performance of the business organization (Kabir and Rahman, 2016). The guidelines of ASIC

helps in assisting the entities along with the individuals to comply with the rules and

regulations of ASIC and to take proper decisions in the best interests for the investors. The

ASIC maintains relationship with the stakeholders regarding the issues related to corporate

governance with the help of external publications, speeches and events (Comino, 2015).

However, sometimes companies fail to keep pace with the corporate governance and

the reasons why they fail is discussed below-

Experience in Leadership- There are many organizations which are having ill-trained

and poor directors and therefore they lack in their commitment. They focus mainly on

the short-term profitability, management of assets, cost-cutting initiatives over the

less-tangible challenge which helps in the enhancement of the culture of the company.

Therefore, the cultural issues of the company receive less attention and the KPIs and

goals are not in place hence it creates conflict and chaos for the stakeholders at all

levels.

Confusion about the role of the good governance- There are many organizations

which do not understand the importance of governance and fails to admit it as a

business philosophy. As a result, there is no change in the attitude and practices of the

personnel of the organization. Mostly, the business organizations set up a compliance

department and think this will help to set up a good corporate governance but this

8

Corporate Governance

actually push the business away from culture of excellence towards the culture of

compliance and the organization misses its opportunity to improve.

These organizational failure can be solved by the chief compliance officer by

developing strategies for leadership engagement. The leadership engagement strategies

should include mentoring of work force and establishing key metrics of performance for

the purpose of measuring the performance of the business organization and to

demonstrate the value of the good corporate governance (Rossouw and Styan, 2019). The

bankruptcy and the financial failures are caused due to mismanagement, poor ethical

leadership, lack of integrity, violation of corporate governance rules, corruption and fraud

and most of the corporate governance programs make things worse and creates a more

stable situation for corruption (Boda and Zsolnai, 2016).

It can be inferred from the above discussion that accounting and corporate governance

go hand in hand and one cannot function without the other. The good corporate

governance has been considered as the deciding factor which helps the business

organization to maintain a strong financial position in the market. However, when there is

a failure in the corporate governance the failure mainly occurs due to flaws and faults in

the accounting department and therefore, the accounting department has been considered

as the “gatekeeper of all the activities of corporate governance” in the business

organizations. The good corporate governance is helpful for the business as good

corporate governance helps to build faith of the customers in the business organization

and leads to lower capital costs in the investments. On the other hand, accounting also

helps in the improvement of corporate governance of an organization and it is the key

enabler of the good corporate governance. Lastly, it can be concluded that accounting

helps to provide a clear picture of the organizations after undertaking several tasks and

therefore the accountant sets the code of conduct according to which the processes of

Corporate Governance

actually push the business away from culture of excellence towards the culture of

compliance and the organization misses its opportunity to improve.

These organizational failure can be solved by the chief compliance officer by

developing strategies for leadership engagement. The leadership engagement strategies

should include mentoring of work force and establishing key metrics of performance for

the purpose of measuring the performance of the business organization and to

demonstrate the value of the good corporate governance (Rossouw and Styan, 2019). The

bankruptcy and the financial failures are caused due to mismanagement, poor ethical

leadership, lack of integrity, violation of corporate governance rules, corruption and fraud

and most of the corporate governance programs make things worse and creates a more

stable situation for corruption (Boda and Zsolnai, 2016).

It can be inferred from the above discussion that accounting and corporate governance

go hand in hand and one cannot function without the other. The good corporate

governance has been considered as the deciding factor which helps the business

organization to maintain a strong financial position in the market. However, when there is

a failure in the corporate governance the failure mainly occurs due to flaws and faults in

the accounting department and therefore, the accounting department has been considered

as the “gatekeeper of all the activities of corporate governance” in the business

organizations. The good corporate governance is helpful for the business as good

corporate governance helps to build faith of the customers in the business organization

and leads to lower capital costs in the investments. On the other hand, accounting also

helps in the improvement of corporate governance of an organization and it is the key

enabler of the good corporate governance. Lastly, it can be concluded that accounting

helps to provide a clear picture of the organizations after undertaking several tasks and

therefore the accountant sets the code of conduct according to which the processes of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Corporate Governance

governance are carried out. It is also the role of the accountant to ensure that the program

of fraud management are in place and conducting of regular assessments of the risk

exposure of the organization and implementation of techniques of prevention for avoiding

fraudulent activities.

Corporate Governance

governance are carried out. It is also the role of the accountant to ensure that the program

of fraud management are in place and conducting of regular assessments of the risk

exposure of the organization and implementation of techniques of prevention for avoiding

fraudulent activities.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Corporate Governance

References

Armstrong, C.S., Blouin, J.L., Jagolinzer, A.D. and Larcker, D.F. Corporate governance,

incentives, and tax avoidance. Journal of Accounting and Economics, 2015

Bhp.com. [online] Available at: https://www.bhp.com/-/media/documents/investors/annual-

reports/2018/bhpannualreport2018.pdf, 2020 [Accessed 21 Jan. 2020].

Boda, Z. and Zsolnai, L. The failure of business ethics. Society and Business Review, 2016

Comino, V. Australia's' Company Law Watchdog': ASIC and Corporate Regulation. V

Comino, Company Law Watchdog-ASIC and Corporate Regulation (Thomson Reuters,

Australia 2015), 2015

Giofré, M. Comparative corporate governance and international portfolios. The European

Journal of Finance, 22(8-9), pp.756-781, 2016.

Honggowati, S., Rahmawati, R., Aryani, Y.A. and Probohudono, A.N. Corporate governance

and strategic management accounting disclosure. Indonesian Journal of Sustainability

Accounting and Management, 1(1), pp.23-30, 2017

Kabir, H. and Rahman, A. The role of corporate governance in accounting discretion under

IFRS: Goodwill impairment in Australia. Journal of Contemporary Accounting &

Economics, 12(3), pp.290-308, 2016

Larcker, D. and Tayan, B. Corporate governance matters: A closer look at organizational

choices and their consequences. Pearson education, 2015

Riotinto.com. Annual Report. [online] Available at:

https://www.riotinto.com/en/invest/reports/annual-report, 2020 [Accessed 21 Jan. 2020].

Corporate Governance

References

Armstrong, C.S., Blouin, J.L., Jagolinzer, A.D. and Larcker, D.F. Corporate governance,

incentives, and tax avoidance. Journal of Accounting and Economics, 2015

Bhp.com. [online] Available at: https://www.bhp.com/-/media/documents/investors/annual-

reports/2018/bhpannualreport2018.pdf, 2020 [Accessed 21 Jan. 2020].

Boda, Z. and Zsolnai, L. The failure of business ethics. Society and Business Review, 2016

Comino, V. Australia's' Company Law Watchdog': ASIC and Corporate Regulation. V

Comino, Company Law Watchdog-ASIC and Corporate Regulation (Thomson Reuters,

Australia 2015), 2015

Giofré, M. Comparative corporate governance and international portfolios. The European

Journal of Finance, 22(8-9), pp.756-781, 2016.

Honggowati, S., Rahmawati, R., Aryani, Y.A. and Probohudono, A.N. Corporate governance

and strategic management accounting disclosure. Indonesian Journal of Sustainability

Accounting and Management, 1(1), pp.23-30, 2017

Kabir, H. and Rahman, A. The role of corporate governance in accounting discretion under

IFRS: Goodwill impairment in Australia. Journal of Contemporary Accounting &

Economics, 12(3), pp.290-308, 2016

Larcker, D. and Tayan, B. Corporate governance matters: A closer look at organizational

choices and their consequences. Pearson education, 2015

Riotinto.com. Annual Report. [online] Available at:

https://www.riotinto.com/en/invest/reports/annual-report, 2020 [Accessed 21 Jan. 2020].

11

Corporate Governance

Rossouw, J. and Styan, J. Steinhoff collapse: a failure of corporate governance. International

Review of Applied Economics, 33(1), pp.163-170, 2019

Tricker, R.B. and Tricker, R.I. Corporate governance: Principles, policies, and practices.

Oxford University Press, 2015

Corporate Governance

Rossouw, J. and Styan, J. Steinhoff collapse: a failure of corporate governance. International

Review of Applied Economics, 33(1), pp.163-170, 2019

Tricker, R.B. and Tricker, R.I. Corporate governance: Principles, policies, and practices.

Oxford University Press, 2015

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.