Corporate Governance and Business Performance Analysis Report

VerifiedAdded on 2020/04/15

|23

|5979

|34

Report

AI Summary

This report examines the impact of corporate governance on business performance, focusing on the professional firm Tan, Chan and Partners. It explores the definition of corporate governance, the characteristics of good corporate governance, and the benefits it offers, such as improved internal controls, increased accountability, and enhanced shareholder value. The research includes a literature review covering key concepts like leadership, accountability, and sustainability. The report utilizes a case study method to analyze Tan, Chan and Partners, highlighting how corporate governance practices can lead to better business outcomes. The findings suggest that an independent board and alignment of voting rights with cash flow rights can positively influence firm performance. The report also emphasizes the importance of adhering to corporate governance principles for long-term sustainability and competitiveness.

Running head: CORPORATE GOVERNANCE AND BUSINESS PERFORMANCE

Corporate Governance and Business Performance

Name of the student

Name of the University

Author note

Corporate Governance and Business Performance

Name of the student

Name of the University

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CORPORATE GOVERNANCE AND BUSINESS PERFORMANCE

Executive Summary

The primary purpose of this report is to find out how corporate governance has an impact on

business performance. It analyses the corporate management of the professional firm Tan,

Chan and Partners that provides services like statutory audit and taxation planning. It states

how corporate governance helps the organisations to survive in a competitive environment. It

was deduced with the help of research carried out at the firm Tan, Chan and Partners that an

independent board would lead to better performance in an organization and the deviation

between that of voting right along with cash flow right is related in a negative manner to that

of the performance of the firm (Jin and Park 2015).

CORPORATE GOVERNANCE AND BUSINESS PERFORMANCE

Executive Summary

The primary purpose of this report is to find out how corporate governance has an impact on

business performance. It analyses the corporate management of the professional firm Tan,

Chan and Partners that provides services like statutory audit and taxation planning. It states

how corporate governance helps the organisations to survive in a competitive environment. It

was deduced with the help of research carried out at the firm Tan, Chan and Partners that an

independent board would lead to better performance in an organization and the deviation

between that of voting right along with cash flow right is related in a negative manner to that

of the performance of the firm (Jin and Park 2015).

2

CORPORATE GOVERNANCE AND BUSINESS PERFORMANCE

Table of Contents

1. Introduction............................................................................................................................3

1.1 Background......................................................................................................................3

1.2Purpose of research...........................................................................................................3

1.3 Research Questions..........................................................................................................4

2. Literature Review...................................................................................................................4

2.1 Definition of Corporate Governance................................................................................4

2.2 Good Corporate Governance............................................................................................7

2.3 Benefits............................................................................................................................9

3. Research Method..................................................................................................................11

3.1 Research Philosophy......................................................................................................11

3.2 Research approach.........................................................................................................12

3.3 Research Design.............................................................................................................12

3.4 Case Study Method........................................................................................................13

Conclusion................................................................................................................................15

References:...............................................................................................................................17

CORPORATE GOVERNANCE AND BUSINESS PERFORMANCE

Table of Contents

1. Introduction............................................................................................................................3

1.1 Background......................................................................................................................3

1.2Purpose of research...........................................................................................................3

1.3 Research Questions..........................................................................................................4

2. Literature Review...................................................................................................................4

2.1 Definition of Corporate Governance................................................................................4

2.2 Good Corporate Governance............................................................................................7

2.3 Benefits............................................................................................................................9

3. Research Method..................................................................................................................11

3.1 Research Philosophy......................................................................................................11

3.2 Research approach.........................................................................................................12

3.3 Research Design.............................................................................................................12

3.4 Case Study Method........................................................................................................13

Conclusion................................................................................................................................15

References:...............................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CORPORATE GOVERNANCE AND BUSINESS PERFORMANCE

1. Introduction

1.1 Background

Corporate Governance comprises of the system of rules and practices by taking recourse to

which a company is controlled. It involves the balancing of interests in relation to the

stakeholders, customers, government along with the community. It provides the framework

that helps in obtaining the objectives of the company. Performance Management refers to

analytical process that enables the management of an organisation to achieve the pre-selected

goals. It involves the consolidation in relation to the management information that is relevant

for the progress of the organization (Tricker and Tricker 2015). It takes into account the

interventions that are made by the managers to improve the future performance of the

employees. Tan, Chan and Partners is one of the leading professional firm in Singapore that

is led by Mr. Tan Chin Ren and they provide professional services like statutory audit,

taxation planning and financial advisory. It is also involved in outsourcing, accounting along

with book keeping. The firm is dedicated to serve the client base and provides human service

programs that are innovative (Al-Janadi, Rahman and Omar 2013). The corporate

governance of the firm aims at serving the customer base and at the same time implement

policies that can help in improving the performance of the employees. This report highlights

the corporate governance in relation to Tan Chan and Partners and how it helps in

augmenting the business performance (Van Grembergen and De Haes 2017).

CORPORATE GOVERNANCE AND BUSINESS PERFORMANCE

1. Introduction

1.1 Background

Corporate Governance comprises of the system of rules and practices by taking recourse to

which a company is controlled. It involves the balancing of interests in relation to the

stakeholders, customers, government along with the community. It provides the framework

that helps in obtaining the objectives of the company. Performance Management refers to

analytical process that enables the management of an organisation to achieve the pre-selected

goals. It involves the consolidation in relation to the management information that is relevant

for the progress of the organization (Tricker and Tricker 2015). It takes into account the

interventions that are made by the managers to improve the future performance of the

employees. Tan, Chan and Partners is one of the leading professional firm in Singapore that

is led by Mr. Tan Chin Ren and they provide professional services like statutory audit,

taxation planning and financial advisory. It is also involved in outsourcing, accounting along

with book keeping. The firm is dedicated to serve the client base and provides human service

programs that are innovative (Al-Janadi, Rahman and Omar 2013). The corporate

governance of the firm aims at serving the customer base and at the same time implement

policies that can help in improving the performance of the employees. This report highlights

the corporate governance in relation to Tan Chan and Partners and how it helps in

augmenting the business performance (Van Grembergen and De Haes 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CORPORATE GOVERNANCE AND BUSINESS PERFORMANCE

1.2Purpose of research

The aim of research is to find out about corporate governance, important aspects in relation to

good corporate governance and advantages of good corporate governance (Padachi,

Ramsurrun and Ramen 2017).

1.3 Research Questions

The Research Questions are:

What is corporate governance?

What is considered as good corporate governance?

What are the benefits of good corporate governance?

2. Literature Review

2.1 Definition of Corporate Governance

Corporate governance refers to the system with the help of which the companies are directed.

Board of directors are responsible in a company for governance in relation to the companies.

The main role of shareholders revolves around providing appointment to directors so that

they are satisfied that the structure of government is appropriate (McCahery, Sautner and

Starks 2016). It is the board who sets the strategic aims of the company, provide leadership

so that they can be put into effect and and supervise the management on the arena of

stewardship (Fox, Gilson and Palia 2016).

CORPORATE GOVERNANCE AND BUSINESS PERFORMANCE

1.2Purpose of research

The aim of research is to find out about corporate governance, important aspects in relation to

good corporate governance and advantages of good corporate governance (Padachi,

Ramsurrun and Ramen 2017).

1.3 Research Questions

The Research Questions are:

What is corporate governance?

What is considered as good corporate governance?

What are the benefits of good corporate governance?

2. Literature Review

2.1 Definition of Corporate Governance

Corporate governance refers to the system with the help of which the companies are directed.

Board of directors are responsible in a company for governance in relation to the companies.

The main role of shareholders revolves around providing appointment to directors so that

they are satisfied that the structure of government is appropriate (McCahery, Sautner and

Starks 2016). It is the board who sets the strategic aims of the company, provide leadership

so that they can be put into effect and and supervise the management on the arena of

stewardship (Fox, Gilson and Palia 2016).

5

CORPORATE GOVERNANCE AND BUSINESS PERFORMANCE

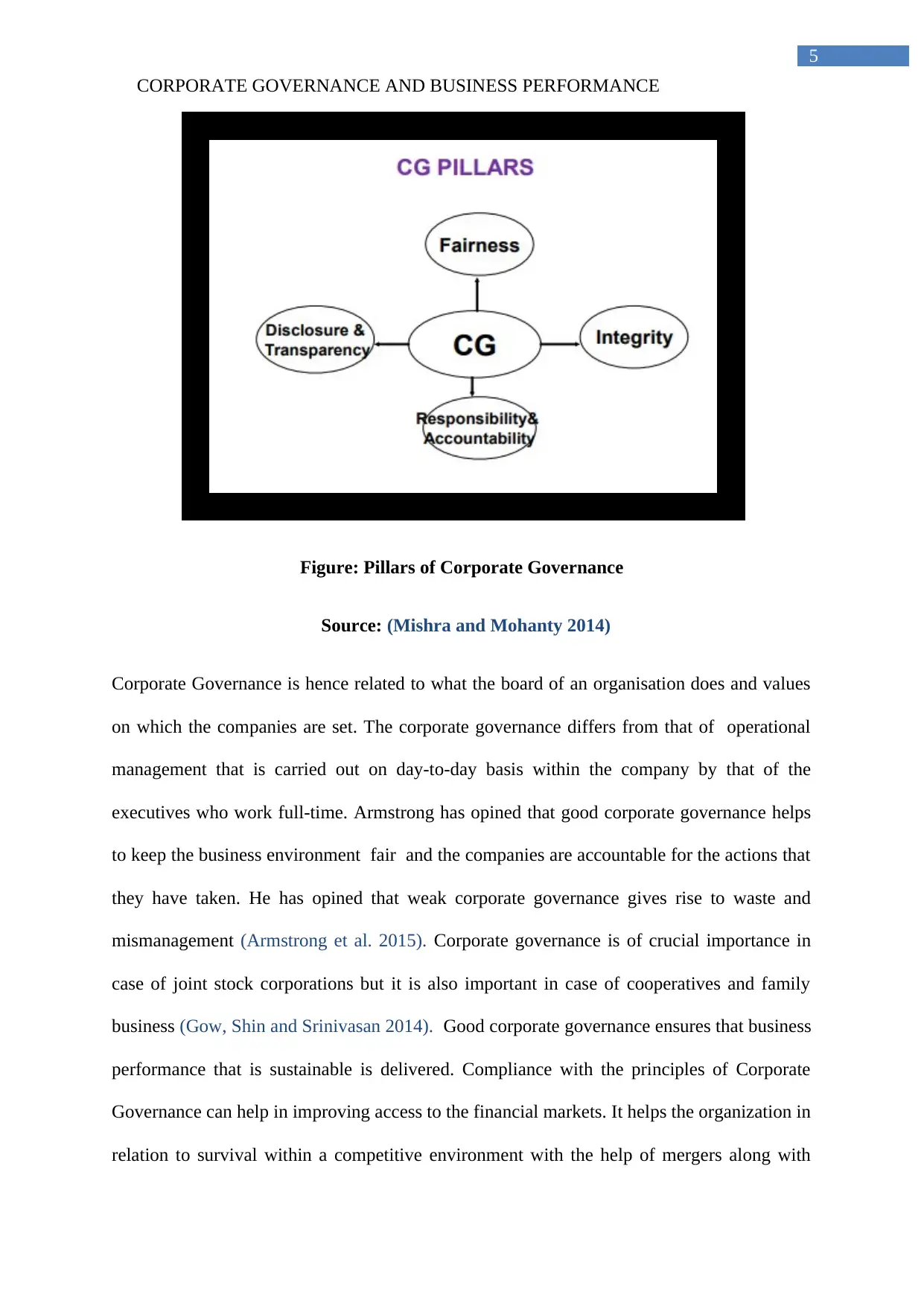

Figure: Pillars of Corporate Governance

Source: (Mishra and Mohanty 2014)

Corporate Governance is hence related to what the board of an organisation does and values

on which the companies are set. The corporate governance differs from that of operational

management that is carried out on day-to-day basis within the company by that of the

executives who work full-time. Armstrong has opined that good corporate governance helps

to keep the business environment fair and the companies are accountable for the actions that

they have taken. He has opined that weak corporate governance gives rise to waste and

mismanagement (Armstrong et al. 2015). Corporate governance is of crucial importance in

case of joint stock corporations but it is also important in case of cooperatives and family

business (Gow, Shin and Srinivasan 2014). Good corporate governance ensures that business

performance that is sustainable is delivered. Compliance with the principles of Corporate

Governance can help in improving access to the financial markets. It helps the organization in

relation to survival within a competitive environment with the help of mergers along with

CORPORATE GOVERNANCE AND BUSINESS PERFORMANCE

Figure: Pillars of Corporate Governance

Source: (Mishra and Mohanty 2014)

Corporate Governance is hence related to what the board of an organisation does and values

on which the companies are set. The corporate governance differs from that of operational

management that is carried out on day-to-day basis within the company by that of the

executives who work full-time. Armstrong has opined that good corporate governance helps

to keep the business environment fair and the companies are accountable for the actions that

they have taken. He has opined that weak corporate governance gives rise to waste and

mismanagement (Armstrong et al. 2015). Corporate governance is of crucial importance in

case of joint stock corporations but it is also important in case of cooperatives and family

business (Gow, Shin and Srinivasan 2014). Good corporate governance ensures that business

performance that is sustainable is delivered. Compliance with the principles of Corporate

Governance can help in improving access to the financial markets. It helps the organization in

relation to survival within a competitive environment with the help of mergers along with

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CORPORATE GOVERNANCE AND BUSINESS PERFORMANCE

partnerships. It has been opined by Denis (2016), that corporate Governance provides an exit

policy and ensures that there is a smooth transfer of wealth along with that of divestment of

family assets (Denis 2016).

There are various model of corporate governance within the world. These are different on

account of the variety in relation to capitalism within which they have been embedded. The

Anglo-American model puts more stress on the aspect of interest of shareholders (McCahery,

Sautner and Starks 2016). The coordinated model can be related with that of Continental

Europe and it recognizes the interest of worker, manager and customer. Corporate

governance principles have grown in various countries and they are issued from corporations

and stock exchanges. One important guideline has been provided by the 1999 OECD

Principle of Corporate Governance. The guidelines of OECD are referred by the countries

that have developed local codes (Mishra and Mohanty 2014). On the basis of the work done

by the OECD, other private sector associations have produced Guidance on Good Practices in

Corporate Governance Disclosure (Ginena 2014). This yardstick comprises of fifty different

disclosure items that works across five wide categories:

Auditing

Management Structure along with process

Corporate responsibility along with compliance

Financial transparency

Ownership structure (Gow, Shin and Srinivasan 2014)

In the year 2009, International Finance Corporation along with UN Global Compact brought

out a report called “Corporate Governance” that linked the environmental along with

governance responsibilities of an organisation to that of financial performance. The

guidelines that are issued by corporate managers have a tendency to be voluntary but these

CORPORATE GOVERNANCE AND BUSINESS PERFORMANCE

partnerships. It has been opined by Denis (2016), that corporate Governance provides an exit

policy and ensures that there is a smooth transfer of wealth along with that of divestment of

family assets (Denis 2016).

There are various model of corporate governance within the world. These are different on

account of the variety in relation to capitalism within which they have been embedded. The

Anglo-American model puts more stress on the aspect of interest of shareholders (McCahery,

Sautner and Starks 2016). The coordinated model can be related with that of Continental

Europe and it recognizes the interest of worker, manager and customer. Corporate

governance principles have grown in various countries and they are issued from corporations

and stock exchanges. One important guideline has been provided by the 1999 OECD

Principle of Corporate Governance. The guidelines of OECD are referred by the countries

that have developed local codes (Mishra and Mohanty 2014). On the basis of the work done

by the OECD, other private sector associations have produced Guidance on Good Practices in

Corporate Governance Disclosure (Ginena 2014). This yardstick comprises of fifty different

disclosure items that works across five wide categories:

Auditing

Management Structure along with process

Corporate responsibility along with compliance

Financial transparency

Ownership structure (Gow, Shin and Srinivasan 2014)

In the year 2009, International Finance Corporation along with UN Global Compact brought

out a report called “Corporate Governance” that linked the environmental along with

governance responsibilities of an organisation to that of financial performance. The

guidelines that are issued by corporate managers have a tendency to be voluntary but these

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE GOVERNANCE AND BUSINESS PERFORMANCE

kind of documents can have a greater effect if it prompts the other companies to abide by the

similar kind of practices (Adegbite 2015). In United States, the corporations are directed by

that of state laws wherein the exchange of securities is directed by that of federal legislation.

There are plenty of U.S. states that have abided by Model Business Corporation Act. The

state law that is dominant in relation to publicly traded corporation is that of Delaware

(Broughman, Fried and Ibrahim 2014).

2.2 Good Corporate Governance

The primary ideas behind that of corporate governance code are quite straightforward-

intuitive principles that can be easily remembered. Corporate governance serves as a means

that can lead to an end and the end purpose is to help the board so that they can determine

how the company should be steered so that the business purpose can be achieved (Fox,

Gilson and Palia 2016). The five primary principles of good corporate governance are:

Leadership

Capability

Accountability

Sustainability

Integrity (Macve 2015)

Leadership can prove to be of extensive help in steering the company so that the business

objectives can be achieved. The board should be capable enough so that it can carry out

the responsibilities. Accountability helps in communicating the stakeholders the way by

which the company is able to achieve its purpose (Bell, Filatotchev and Aguilera 2014).

It has been stated by Adegbite (2015), that sustainability helps in creating value and

allocating it on fair basis. Integrity will be able to withstand security by that of internal

along with external stakeholders (Adegbite 2015).

CORPORATE GOVERNANCE AND BUSINESS PERFORMANCE

kind of documents can have a greater effect if it prompts the other companies to abide by the

similar kind of practices (Adegbite 2015). In United States, the corporations are directed by

that of state laws wherein the exchange of securities is directed by that of federal legislation.

There are plenty of U.S. states that have abided by Model Business Corporation Act. The

state law that is dominant in relation to publicly traded corporation is that of Delaware

(Broughman, Fried and Ibrahim 2014).

2.2 Good Corporate Governance

The primary ideas behind that of corporate governance code are quite straightforward-

intuitive principles that can be easily remembered. Corporate governance serves as a means

that can lead to an end and the end purpose is to help the board so that they can determine

how the company should be steered so that the business purpose can be achieved (Fox,

Gilson and Palia 2016). The five primary principles of good corporate governance are:

Leadership

Capability

Accountability

Sustainability

Integrity (Macve 2015)

Leadership can prove to be of extensive help in steering the company so that the business

objectives can be achieved. The board should be capable enough so that it can carry out

the responsibilities. Accountability helps in communicating the stakeholders the way by

which the company is able to achieve its purpose (Bell, Filatotchev and Aguilera 2014).

It has been stated by Adegbite (2015), that sustainability helps in creating value and

allocating it on fair basis. Integrity will be able to withstand security by that of internal

along with external stakeholders (Adegbite 2015).

8

CORPORATE GOVERNANCE AND BUSINESS PERFORMANCE

The motive behind research in the corporate governance of financial institution is owing

to the fact that financial crisis are not sudden events but it happens on account of the

decision of individuals who work within a framework of laws and regulations (Bell,

Filatotchev and Aguilera 2014). According to Mason and Simmons (2014), corporate

governance can help in identifying the problem spots that can in due course of time pave

the path for undesired firm behaviour or instability in the system (Mason and Simmons

2014). The principal agent problem can be solved if the management is responsible for

that of value maximisation within a firm. According to ArAs (2016), the compensation

based on equity along with market for corporate control can further provide incentive for

the management so that it aligns their interest with that of the shareholders (ArAs 2016).

Executives are held responsible to that of board of directors and their constituents are that

of the shareholders who belong to the firm. In the opinion of Wang et al. (2014), value

maximisation can prove to be a powerful conceptual tool that can address problems of the

financial organisations (Wang et al. 2014) According to Shrives and Brennan (2015), in a

world where there is perfect information, interest of shareholders should be aligned to that

of the broader society. Banks can increase their profitability by pursuing productive

activities that can help in improving the quality of the financial intermediation (Shrives

and Brennan 2015).

A large body in relation to the research has stated that there is link between that of

finance and growth in developing along with that of developed economies. There are

various mechanisms that direct the financial institutions. The firms operate within a

system of social mores and laws (Christensen et al. 2015). Financial institutions have to

face the added burden of supervisory action. Every important decision within the firm like

investment and growth is greatly influenced by the internal governors like board of

directors along with that of external governor like regulator. For governing the financial

CORPORATE GOVERNANCE AND BUSINESS PERFORMANCE

The motive behind research in the corporate governance of financial institution is owing

to the fact that financial crisis are not sudden events but it happens on account of the

decision of individuals who work within a framework of laws and regulations (Bell,

Filatotchev and Aguilera 2014). According to Mason and Simmons (2014), corporate

governance can help in identifying the problem spots that can in due course of time pave

the path for undesired firm behaviour or instability in the system (Mason and Simmons

2014). The principal agent problem can be solved if the management is responsible for

that of value maximisation within a firm. According to ArAs (2016), the compensation

based on equity along with market for corporate control can further provide incentive for

the management so that it aligns their interest with that of the shareholders (ArAs 2016).

Executives are held responsible to that of board of directors and their constituents are that

of the shareholders who belong to the firm. In the opinion of Wang et al. (2014), value

maximisation can prove to be a powerful conceptual tool that can address problems of the

financial organisations (Wang et al. 2014) According to Shrives and Brennan (2015), in a

world where there is perfect information, interest of shareholders should be aligned to that

of the broader society. Banks can increase their profitability by pursuing productive

activities that can help in improving the quality of the financial intermediation (Shrives

and Brennan 2015).

A large body in relation to the research has stated that there is link between that of

finance and growth in developing along with that of developed economies. There are

various mechanisms that direct the financial institutions. The firms operate within a

system of social mores and laws (Christensen et al. 2015). Financial institutions have to

face the added burden of supervisory action. Every important decision within the firm like

investment and growth is greatly influenced by the internal governors like board of

directors along with that of external governor like regulator. For governing the financial

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

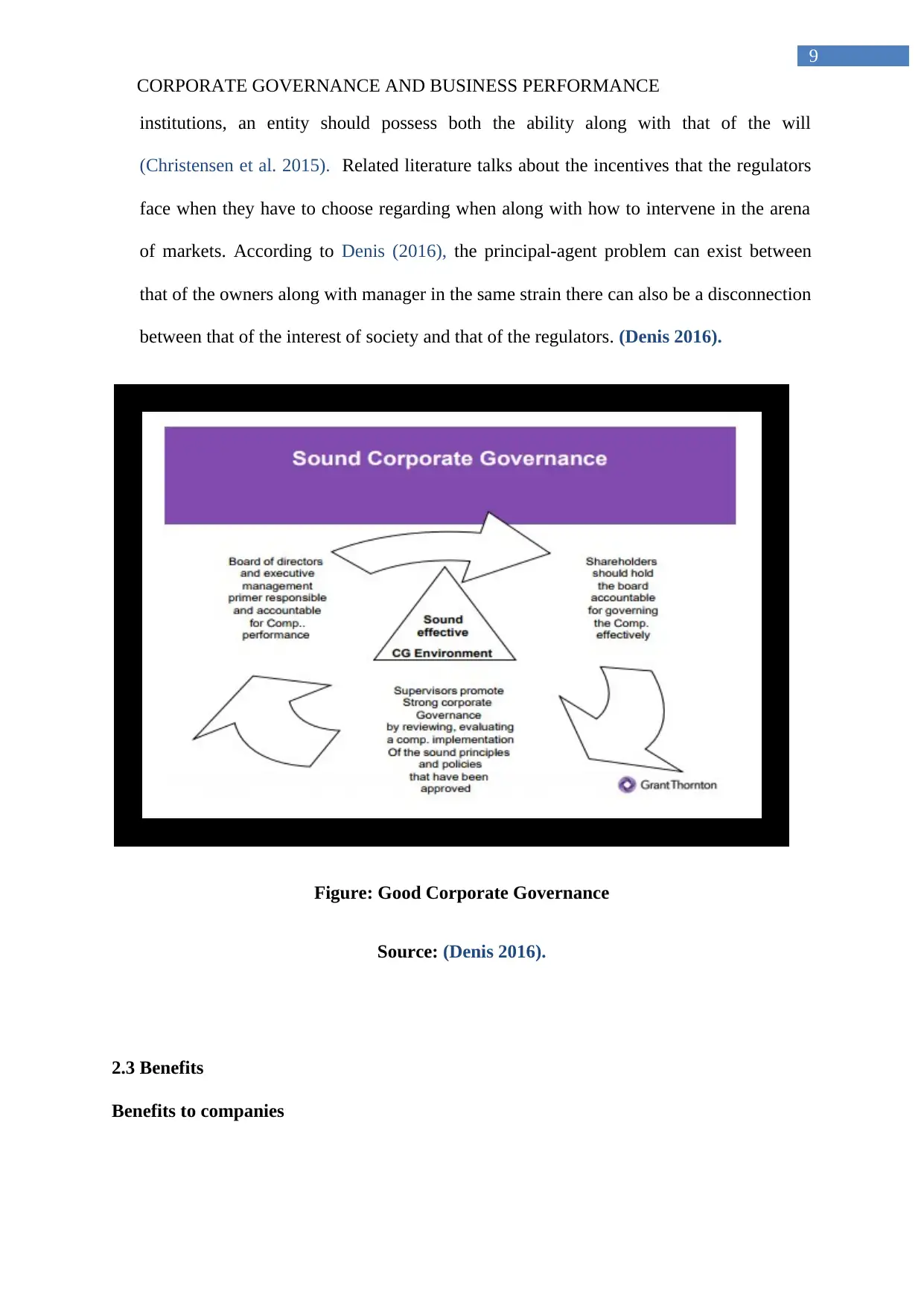

CORPORATE GOVERNANCE AND BUSINESS PERFORMANCE

institutions, an entity should possess both the ability along with that of the will

(Christensen et al. 2015). Related literature talks about the incentives that the regulators

face when they have to choose regarding when along with how to intervene in the arena

of markets. According to Denis (2016), the principal-agent problem can exist between

that of the owners along with manager in the same strain there can also be a disconnection

between that of the interest of society and that of the regulators. (Denis 2016).

Figure: Good Corporate Governance

Source: (Denis 2016).

2.3 Benefits

Benefits to companies

CORPORATE GOVERNANCE AND BUSINESS PERFORMANCE

institutions, an entity should possess both the ability along with that of the will

(Christensen et al. 2015). Related literature talks about the incentives that the regulators

face when they have to choose regarding when along with how to intervene in the arena

of markets. According to Denis (2016), the principal-agent problem can exist between

that of the owners along with manager in the same strain there can also be a disconnection

between that of the interest of society and that of the regulators. (Denis 2016).

Figure: Good Corporate Governance

Source: (Denis 2016).

2.3 Benefits

Benefits to companies

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CORPORATE GOVERNANCE AND BUSINESS PERFORMANCE

Corporate Governance practices can lead to a better process in relation to internal control and

thus lead to greater accountability. It has been stated by Pindado and Requejo (2015), that

corporate governance can be of great help in improving the profit margins of an organisation.

Corporate governance that is smooth can create the way for future growth and the ability to

attract the equity investors-both nationally and also from abroad. It provides extensive help

in reducing the cost of credit for the corporation (Pindado and Requejo 2015). There are

businesses that look out for funds and they are often forced to adopt reforms of government at

a very high cost in case of demand of outsider during crisis. In the opinion of Ayuso et al.

(2014), on account of the foundations being in the right place, investors along with potential

partners can get more confidence so that they can invest and expand the operations of the

company (Ayuso et al. 2014).

Benefits to Shareholders

Good corporate governance can be of great help in providing incentives for board so that

they can pursue objectives which will be in the company’s interests and help in monitoring

in the effective manner. Corporate governance that is better can provide the shareholders with

greater amount of security in relation to their investment. Good corporate governance helps in

ensuring that the shareholders are made known about decisions that are concerned with issues

like amendment of statutes and sale of the assets (Ayuso et al. 2014).

Empirical research that has been carried out in the recent years supports the idea that

it is extremely important to possess good corporate governance. Research carried out has

shown that 84% of global institutional investor want to pay a premium for shares of the

company that is governed in the right direction as compared to that of one that is poorly

governed (Ginena 2014). Adoption of principles in relation to corporate governance can play

a pivotal role in augmenting corporate value in relation to the companies (Larcker et al.

CORPORATE GOVERNANCE AND BUSINESS PERFORMANCE

Corporate Governance practices can lead to a better process in relation to internal control and

thus lead to greater accountability. It has been stated by Pindado and Requejo (2015), that

corporate governance can be of great help in improving the profit margins of an organisation.

Corporate governance that is smooth can create the way for future growth and the ability to

attract the equity investors-both nationally and also from abroad. It provides extensive help

in reducing the cost of credit for the corporation (Pindado and Requejo 2015). There are

businesses that look out for funds and they are often forced to adopt reforms of government at

a very high cost in case of demand of outsider during crisis. In the opinion of Ayuso et al.

(2014), on account of the foundations being in the right place, investors along with potential

partners can get more confidence so that they can invest and expand the operations of the

company (Ayuso et al. 2014).

Benefits to Shareholders

Good corporate governance can be of great help in providing incentives for board so that

they can pursue objectives which will be in the company’s interests and help in monitoring

in the effective manner. Corporate governance that is better can provide the shareholders with

greater amount of security in relation to their investment. Good corporate governance helps in

ensuring that the shareholders are made known about decisions that are concerned with issues

like amendment of statutes and sale of the assets (Ayuso et al. 2014).

Empirical research that has been carried out in the recent years supports the idea that

it is extremely important to possess good corporate governance. Research carried out has

shown that 84% of global institutional investor want to pay a premium for shares of the

company that is governed in the right direction as compared to that of one that is poorly

governed (Ginena 2014). Adoption of principles in relation to corporate governance can play

a pivotal role in augmenting corporate value in relation to the companies (Larcker et al.

11

CORPORATE GOVERNANCE AND BUSINESS PERFORMANCE

2014). Arthur Levitt who is the chairman of US Securities and Exchange Commission has

said that when a country does not have sound practices in relation to corporate governance

then the capital will flow in another direction. If the investors do not feel confident with that

of level of disclosure then the capital will also flow in another place (Klettner, Clarke and

Boersma 2014). When a country wants lax accounting along with reporting standard then the

capital will flow to other place. In this kind of a case, all the enterprises in a country have to

suffer for the results (Macve 2015).

The principles in relation to corporate governance are essential in the following areas:

Internal controls along with internal auditors

Independence in relation to the external auditor and their quality of audits

Management of the factor of risk

Oversight in relation to the preparation of the financial statements of entity (Kato, Li

and Skinner 2017).

Review of compensation arrangement for the CEO along with other senior executive

Resources available to the directors so that they can carry out their duty

3. Research Method

3.1 Research Philosophy

There are four kinds of research philosophy- positivism, epistemology, Interpretivism and

realism. Positivism makes use of the philosophical stance in relation to the natural scientist.

Realism is related to that of the scientific enquiry. Essence in relation to the realism revolves

around the fact that what is perceived by the senses as reality is the actual truth.

Epistemology is concerned with how reality is represented in the form of objects which is

considered real like that of computer and machines (Wang et al. 2014). Social actors are

CORPORATE GOVERNANCE AND BUSINESS PERFORMANCE

2014). Arthur Levitt who is the chairman of US Securities and Exchange Commission has

said that when a country does not have sound practices in relation to corporate governance

then the capital will flow in another direction. If the investors do not feel confident with that

of level of disclosure then the capital will also flow in another place (Klettner, Clarke and

Boersma 2014). When a country wants lax accounting along with reporting standard then the

capital will flow to other place. In this kind of a case, all the enterprises in a country have to

suffer for the results (Macve 2015).

The principles in relation to corporate governance are essential in the following areas:

Internal controls along with internal auditors

Independence in relation to the external auditor and their quality of audits

Management of the factor of risk

Oversight in relation to the preparation of the financial statements of entity (Kato, Li

and Skinner 2017).

Review of compensation arrangement for the CEO along with other senior executive

Resources available to the directors so that they can carry out their duty

3. Research Method

3.1 Research Philosophy

There are four kinds of research philosophy- positivism, epistemology, Interpretivism and

realism. Positivism makes use of the philosophical stance in relation to the natural scientist.

Realism is related to that of the scientific enquiry. Essence in relation to the realism revolves

around the fact that what is perceived by the senses as reality is the actual truth.

Epistemology is concerned with how reality is represented in the form of objects which is

considered real like that of computer and machines (Wang et al. 2014). Social actors are

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.