Professional Project: Corporate Governance in Australian Companies

VerifiedAdded on 2020/03/28

|21

|4694

|37

Project

AI Summary

This project, submitted by Jasmeen Kaur, examines the impact of corporate governance on the financial performance of listed Australian companies. The research explores the relationship between corporate governance policies and accounting processes within a sample of ten Australian listed companies. The study investigates whether effective corporate governance leads to positive financial outcomes. The project includes a literature review, outlines the research methodology (including positivism philosophy and a deductive approach), and presents data findings and analysis, leading to conclusions and recommendations. The research aims to identify the impact of corporate governance on accounting processes and determine if effective policies correlate with positive company performance, addressing the core research questions and hypotheses presented in the introduction.

Jasmeen

Kaur, s0274358

BUSN20019 Professional Project

Impact of corporate governance on the performance of listed Australian

companies

SUBMITTED BY:

NAME: Jasmeen Kaur

STUDENT ID: S0274358

1

Kaur, s0274358

BUSN20019 Professional Project

Impact of corporate governance on the performance of listed Australian

companies

SUBMITTED BY:

NAME: Jasmeen Kaur

STUDENT ID: S0274358

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Jasmeen

Kaur, s0274358

BRISBANE CAMPUS

DATE: 25/08/2017

Table of Contents

Chapter 1: Introduction..............................................................................................................4

1.1. Project context.................................................................................................................4

1.2 Statement of problem.......................................................................................................5

1.3 Research aim and objective..............................................................................................6

1.4. Research Questions.........................................................................................................6

1.5. Research Hypothesis.......................................................................................................6

Chapter 2: Literature review......................................................................................................7

Chapter 3: Research Methodology...........................................................................................10

3.1 Introduction....................................................................................................................10

3.2 Research Philosophy......................................................................................................10

3.3 Research Approach........................................................................................................11

3.4 Research Design.............................................................................................................11

3.5 Type of Data...................................................................................................................11

3.6 Data collection...............................................................................................................11

3.7 Research Technique.......................................................................................................12

3.8 Sample............................................................................................................................12

3.9 The variables..................................................................................................................12

3.10 Giant chart of the study................................................................................................12

3.11 Organisation of the study.............................................................................................13

2

Kaur, s0274358

BRISBANE CAMPUS

DATE: 25/08/2017

Table of Contents

Chapter 1: Introduction..............................................................................................................4

1.1. Project context.................................................................................................................4

1.2 Statement of problem.......................................................................................................5

1.3 Research aim and objective..............................................................................................6

1.4. Research Questions.........................................................................................................6

1.5. Research Hypothesis.......................................................................................................6

Chapter 2: Literature review......................................................................................................7

Chapter 3: Research Methodology...........................................................................................10

3.1 Introduction....................................................................................................................10

3.2 Research Philosophy......................................................................................................10

3.3 Research Approach........................................................................................................11

3.4 Research Design.............................................................................................................11

3.5 Type of Data...................................................................................................................11

3.6 Data collection...............................................................................................................11

3.7 Research Technique.......................................................................................................12

3.8 Sample............................................................................................................................12

3.9 The variables..................................................................................................................12

3.10 Giant chart of the study................................................................................................12

3.11 Organisation of the study.............................................................................................13

2

Jasmeen

Kaur, s0274358

Chapter 4: Data Findings and Analysis....................................................................................14

4.1 Introduction....................................................................................................................14

4.2 Analysis..........................................................................................................................14

Chapter 5: Conclusion and Recommendation..........................................................................17

5.1 Conclusion......................................................................................................................17

5.2 Recommendation............................................................................................................17

References................................................................................................................................18

3

Kaur, s0274358

Chapter 4: Data Findings and Analysis....................................................................................14

4.1 Introduction....................................................................................................................14

4.2 Analysis..........................................................................................................................14

Chapter 5: Conclusion and Recommendation..........................................................................17

5.1 Conclusion......................................................................................................................17

5.2 Recommendation............................................................................................................17

References................................................................................................................................18

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Jasmeen

Kaur, s0274358

Chapter 1:Introduction

The profession is determined by the skills, educational background and overall

professional performance. My profession is an “accounting”. Accounting deals with many

aspects in which adoption of “corporate governance policies” is one of them.Corporate

governance has been a key focus over recent times for Australian companies, particularly

following the collapse of some large organisations which resulted in losses of billions of

dollars along with the jobs, investments and the livelihoods of many Australians.

According to Rezaee (2009) corporate governance is the relationship between

participants such as, shareholders, senior management and the board of directors in

determining the direction and performance of the companies.

The project proposal going to address a relevant accounting aspect of corporate

governance policies in listed companies of Australia. The main objective of this study is to

identify whether the policy of corporate governance will lead positive performance of

companies or not. Moreover, due to lack of timing only 10 Australian listed companies is

taken as a study sample.

1.1.Project context

I am studying Master of Professional Accounting and in general my future profession

is accounting. Accounting is one of the key function of business entities. From the business

context, accounting means identification, recording, formulation and presentation of financial

transactions which is facilitated to fulfil the needs of all relevant entities.

According to American Accounting Association in 1966, “The process of identifying,

measuring and communicating information to permit informed judgments and decisions by

the users of the information”.

4

Kaur, s0274358

Chapter 1:Introduction

The profession is determined by the skills, educational background and overall

professional performance. My profession is an “accounting”. Accounting deals with many

aspects in which adoption of “corporate governance policies” is one of them.Corporate

governance has been a key focus over recent times for Australian companies, particularly

following the collapse of some large organisations which resulted in losses of billions of

dollars along with the jobs, investments and the livelihoods of many Australians.

According to Rezaee (2009) corporate governance is the relationship between

participants such as, shareholders, senior management and the board of directors in

determining the direction and performance of the companies.

The project proposal going to address a relevant accounting aspect of corporate

governance policies in listed companies of Australia. The main objective of this study is to

identify whether the policy of corporate governance will lead positive performance of

companies or not. Moreover, due to lack of timing only 10 Australian listed companies is

taken as a study sample.

1.1.Project context

I am studying Master of Professional Accounting and in general my future profession

is accounting. Accounting is one of the key function of business entities. From the business

context, accounting means identification, recording, formulation and presentation of financial

transactions which is facilitated to fulfil the needs of all relevant entities.

According to American Accounting Association in 1966, “The process of identifying,

measuring and communicating information to permit informed judgments and decisions by

the users of the information”.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Jasmeen

Kaur, s0274358

According to American Institute of Certified Public Accountants accounting is “the

art of recording, classifying and summarizing in a significant manner and in terms of money,

transactions and events which are in part at least of a financial character and interpreting the

result thereof."

1.2Statement of problem

It can be seen that there are two opinions related with the relation between corporate

governance and accounting of the companies. As per one opinion, it can be seen that there is

a positive relation between corporate governance and accounting of the companies (Erkens,

Hung & Matos, 2012). On the other hand, as per another opinion, it can be seen that there is

not any relation between corporate governance and accounting of the companies. In spite of

all these negative points, it can be said that each organization must have a well-structured

corporate governance policy for the help of accounting and finance of the company

(Hermalin & Weisbach, 2012). With the help of effective corporate governance policies, the

business organizations are able to establish effective internal control related to accounting

and finance. In addition, with the help of effective corporate governance policies, business

organizations are able to establish control mechanism in the organizations (McCahery,

Sautner & Starks, 2016). Thus, based on the above discussion, it can be said that the research

program has its importance in solving the conflict that whether there is any positive relation

between corporate governance and accounting of the companies. With the help of this

research, the researcher will be able to establish the effects of corporate governance on the

accounting and financial activities of the companies. Apart from this, this research will be

helpful to develop the idea that whether corporate governance leads to better accosting

performance of the companies or not.

5

Kaur, s0274358

According to American Institute of Certified Public Accountants accounting is “the

art of recording, classifying and summarizing in a significant manner and in terms of money,

transactions and events which are in part at least of a financial character and interpreting the

result thereof."

1.2Statement of problem

It can be seen that there are two opinions related with the relation between corporate

governance and accounting of the companies. As per one opinion, it can be seen that there is

a positive relation between corporate governance and accounting of the companies (Erkens,

Hung & Matos, 2012). On the other hand, as per another opinion, it can be seen that there is

not any relation between corporate governance and accounting of the companies. In spite of

all these negative points, it can be said that each organization must have a well-structured

corporate governance policy for the help of accounting and finance of the company

(Hermalin & Weisbach, 2012). With the help of effective corporate governance policies, the

business organizations are able to establish effective internal control related to accounting

and finance. In addition, with the help of effective corporate governance policies, business

organizations are able to establish control mechanism in the organizations (McCahery,

Sautner & Starks, 2016). Thus, based on the above discussion, it can be said that the research

program has its importance in solving the conflict that whether there is any positive relation

between corporate governance and accounting of the companies. With the help of this

research, the researcher will be able to establish the effects of corporate governance on the

accounting and financial activities of the companies. Apart from this, this research will be

helpful to develop the idea that whether corporate governance leads to better accosting

performance of the companies or not.

5

Jasmeen

Kaur, s0274358

1.3 Research aim and objective

The main aim of this research is to analyse the effect of corporate governance in the

accounting process of the companies. On a more specific note, there are two major

objectives of the research. These two objectives will provide necessary direction to

the research.

The first objective is to identify the impact of corporate governance on the accounting

processes of the business organizations.

The second objective is to determine that whether effective corporate governance

policies lead to positive performance of the companies or not.

1.4. Research Questions

The research questions are as follows:

1. Impact of Corporate Governance on the accounting process of the companies

2. Does Corporate Governance lead to positive financial performance of the business

organizations?

1.5. Research Hypothesis

H0: Corporate Governance does not have any influence on the positive financial performance

of the companies.

H1: Corporate Governance results in the positive financial performance of the companies.

6

Kaur, s0274358

1.3 Research aim and objective

The main aim of this research is to analyse the effect of corporate governance in the

accounting process of the companies. On a more specific note, there are two major

objectives of the research. These two objectives will provide necessary direction to

the research.

The first objective is to identify the impact of corporate governance on the accounting

processes of the business organizations.

The second objective is to determine that whether effective corporate governance

policies lead to positive performance of the companies or not.

1.4. Research Questions

The research questions are as follows:

1. Impact of Corporate Governance on the accounting process of the companies

2. Does Corporate Governance lead to positive financial performance of the business

organizations?

1.5. Research Hypothesis

H0: Corporate Governance does not have any influence on the positive financial performance

of the companies.

H1: Corporate Governance results in the positive financial performance of the companies.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Jasmeen

Kaur, s0274358

Chapter 2:Literature review

Corporate governance is considered as one of the major factors in the process of

accounting and finance of the companies. Corporate governance is a combination of rules,

regulations, practices and processes that helps that provides the necessary directions to the

various operations of the companies (Eccles, Ioannou & Serafeim, 2014). The main objective

of corporate governance is to maintain a balance between the interest of the stakeholders of

the company and the management of the company. With the effective implementation of

corporate governance practices of the companies, the business organizations can get the

necessary competitive advantage. Now, corporate governance in the process of accounting

and finance is considered as a major aspect in the companies (Erkens, Hung & Matos, 2012).

Most of the people all over the world consider that the effective implementation of corporate

governance practices in the companies leads to the positive accounting and financial

performance. However, another group of people believes that there is not any positive

relation between corporate governance and financial performance of the companies. It can be

seen that a large number of research has been done in order to establish the relationship

between corporate governance and accounting of the companies (Tricker & Tricker, 2015).

These kinds of research papers highlight the fact that with the help of effective and efficient

corporate governance policies, the management of the companies can increase the accounting

and financial efficiency of the business organizations. However, some of the studies oppose

this fact and tells that effective corporate governance policies are not always responsible for

the positive performance of various accounting and financial aspects of the companies (Jo &

Harjoto, 2012).

In the business organizations, different kinds of factors can be seen that play crucial

roles for the establishment of effective corporate governance policies in the companies. The

composition of the board of directors of the companies is considered as one of such important

7

Kaur, s0274358

Chapter 2:Literature review

Corporate governance is considered as one of the major factors in the process of

accounting and finance of the companies. Corporate governance is a combination of rules,

regulations, practices and processes that helps that provides the necessary directions to the

various operations of the companies (Eccles, Ioannou & Serafeim, 2014). The main objective

of corporate governance is to maintain a balance between the interest of the stakeholders of

the company and the management of the company. With the effective implementation of

corporate governance practices of the companies, the business organizations can get the

necessary competitive advantage. Now, corporate governance in the process of accounting

and finance is considered as a major aspect in the companies (Erkens, Hung & Matos, 2012).

Most of the people all over the world consider that the effective implementation of corporate

governance practices in the companies leads to the positive accounting and financial

performance. However, another group of people believes that there is not any positive

relation between corporate governance and financial performance of the companies. It can be

seen that a large number of research has been done in order to establish the relationship

between corporate governance and accounting of the companies (Tricker & Tricker, 2015).

These kinds of research papers highlight the fact that with the help of effective and efficient

corporate governance policies, the management of the companies can increase the accounting

and financial efficiency of the business organizations. However, some of the studies oppose

this fact and tells that effective corporate governance policies are not always responsible for

the positive performance of various accounting and financial aspects of the companies (Jo &

Harjoto, 2012).

In the business organizations, different kinds of factors can be seen that play crucial

roles for the establishment of effective corporate governance policies in the companies. The

composition of the board of directors of the companies is considered as one of such important

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Jasmeen

Kaur, s0274358

factors. The business organizations need to make the fact that people who are the part of

managing director’s board should be honest, loyal and they must maintain integrity in their

jobs (Aebi, Sabato & Schmid, 2012). Apart from this, they must have high educational

qualification. These aspects will prevent the scope of accounting and financial frauds from

the business operations of the companies. Apart from this, there are some major financial

factors that establish a connection between the corporate governance and the accounting and

financial aspects of the companies (Walls, Berrone & Phan, 2012). Some of these factors are

return on shareholders’ equity, dividend payments, dividend yield, profitability of the

companies and many others. Thus, from this aspect it can be seen that there is a positive

relation between corporate governance and accounting of the companies. However, it needs

to be mentioned that there is lack of concrete evidence of the presence of corporate

governance and accounting of the companies (Cheng, Ioannou & Serafeim, 2014). According

to many of the researchers all over the world, the business organizations must have effective

corporate governance structured if they want to achieve positive accounting and financial

results. Effective and efficient corporate governance policies in the business organizations

makes it sure that there is not any accounting and financial errors in the organizations. In

addition to implementation, it is required for the companies to properly maintain the

corporate governance policies in order to ensure the accounting and financial performance of

the companies (Peni & Vahamaa, 2012).

According to the earlier discussion, it can be understood that the business

organizations that have been successful in the implementation of effective and efficiency

corporate governance policies enjoys positive accounting and financial performance that

includes higher percentage of return on equity, high percentage of retune on assets, high

percentage of return on capital and others (Servaes & Tamayo, 2013). One of the major

advantages of having efficient corporate governance policy is that it helps to develop proper

8

Kaur, s0274358

factors. The business organizations need to make the fact that people who are the part of

managing director’s board should be honest, loyal and they must maintain integrity in their

jobs (Aebi, Sabato & Schmid, 2012). Apart from this, they must have high educational

qualification. These aspects will prevent the scope of accounting and financial frauds from

the business operations of the companies. Apart from this, there are some major financial

factors that establish a connection between the corporate governance and the accounting and

financial aspects of the companies (Walls, Berrone & Phan, 2012). Some of these factors are

return on shareholders’ equity, dividend payments, dividend yield, profitability of the

companies and many others. Thus, from this aspect it can be seen that there is a positive

relation between corporate governance and accounting of the companies. However, it needs

to be mentioned that there is lack of concrete evidence of the presence of corporate

governance and accounting of the companies (Cheng, Ioannou & Serafeim, 2014). According

to many of the researchers all over the world, the business organizations must have effective

corporate governance structured if they want to achieve positive accounting and financial

results. Effective and efficient corporate governance policies in the business organizations

makes it sure that there is not any accounting and financial errors in the organizations. In

addition to implementation, it is required for the companies to properly maintain the

corporate governance policies in order to ensure the accounting and financial performance of

the companies (Peni & Vahamaa, 2012).

According to the earlier discussion, it can be understood that the business

organizations that have been successful in the implementation of effective and efficiency

corporate governance policies enjoys positive accounting and financial performance that

includes higher percentage of return on equity, high percentage of retune on assets, high

percentage of return on capital and others (Servaes & Tamayo, 2013). One of the major

advantages of having efficient corporate governance policy is that it helps to develop proper

8

Jasmeen

Kaur, s0274358

risk management policy regarding the accounting and financial activities. With the help of

these risk management strategies, the business organizations are able to manage the

accounting as well as financial risks of the companies in the most proper way (Dallas, 2012).

Thus, based on the above discussion, it can be said that in the presence of effective corporate

governance policies, business organizations enjoy many accounting and financial advantages

(Tolman, 2012). In spite of all these aspects, many people believe that there is not any

positive connection between corporate governance and accounting of the companies.

Different kinds of massive accounting and financial scandals can be held responsible behind

this. As per different kinds of research, it has been seen that the lack of effective corporate

governance policies is the main reason behind all these scandals and frauds. Thus, based on

the above discussion, it can be said that corporate governance is major aspect for the business

organizations and it is required for the business organizations to develop the effective and

efficient corporate governance policies (Pearl, 2014).

9

Kaur, s0274358

risk management policy regarding the accounting and financial activities. With the help of

these risk management strategies, the business organizations are able to manage the

accounting as well as financial risks of the companies in the most proper way (Dallas, 2012).

Thus, based on the above discussion, it can be said that in the presence of effective corporate

governance policies, business organizations enjoy many accounting and financial advantages

(Tolman, 2012). In spite of all these aspects, many people believe that there is not any

positive connection between corporate governance and accounting of the companies.

Different kinds of massive accounting and financial scandals can be held responsible behind

this. As per different kinds of research, it has been seen that the lack of effective corporate

governance policies is the main reason behind all these scandals and frauds. Thus, based on

the above discussion, it can be said that corporate governance is major aspect for the business

organizations and it is required for the business organizations to develop the effective and

efficient corporate governance policies (Pearl, 2014).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Jasmeen

Kaur, s0274358

Chapter 3: Research Methodology

3.1 Introduction

This is mainly a secondary research. The study will be conducted by taking help of

the secondary data throughout the year of 2013 to 2016. In general, the annual reports of all

the selected companies will be examined (Kiel & Nicholson, 2003).

The research methodology of the paper has a significant role as it assists the

researcher in gathering the data and constructing a path and a guideline that would be

influential for the completion of the paper. This section of the paper explains the research

process that would be used for the initiating the process of data analysis. It is seen that the

research methodology consists of the hypothetical evaluation of the numerous mechanisms

and the ideologies that are inter-related with the topic that is under consideration(Haug,

2017). This paper explains in detail the research approach, the research philosophy, the

design of the research and the source of data collection and the mechanism that would be

used for the completion of the paper. This will be helpful for the researcher to understand the

impact of corporate governance on the accounting process of the selected Australian

organizations.

3.2 Research Philosophy

The research philosophy that is related to this paper is used in order to understand the

ideologies that have been exploited by the researcher in order to collect the data and to

understand the processes that would be precise for the collection of the data. In accordance to

this topic it has been observed that positivism philosophy would be undertaken as it assists in

giving out the precise ideology that would be fundamental for the collection of the data with

respect to corporate governance(Muhammad et al., 2015).

10

Kaur, s0274358

Chapter 3: Research Methodology

3.1 Introduction

This is mainly a secondary research. The study will be conducted by taking help of

the secondary data throughout the year of 2013 to 2016. In general, the annual reports of all

the selected companies will be examined (Kiel & Nicholson, 2003).

The research methodology of the paper has a significant role as it assists the

researcher in gathering the data and constructing a path and a guideline that would be

influential for the completion of the paper. This section of the paper explains the research

process that would be used for the initiating the process of data analysis. It is seen that the

research methodology consists of the hypothetical evaluation of the numerous mechanisms

and the ideologies that are inter-related with the topic that is under consideration(Haug,

2017). This paper explains in detail the research approach, the research philosophy, the

design of the research and the source of data collection and the mechanism that would be

used for the completion of the paper. This will be helpful for the researcher to understand the

impact of corporate governance on the accounting process of the selected Australian

organizations.

3.2 Research Philosophy

The research philosophy that is related to this paper is used in order to understand the

ideologies that have been exploited by the researcher in order to collect the data and to

understand the processes that would be precise for the collection of the data. In accordance to

this topic it has been observed that positivism philosophy would be undertaken as it assists in

giving out the precise ideology that would be fundamental for the collection of the data with

respect to corporate governance(Muhammad et al., 2015).

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Jasmeen

Kaur, s0274358

3.3 Research Approach

In accordance to this paper, it has been observed that deductive method of research

approach has been used as this mechanism assists in the process of development of the

specific hypotheses of the research by looking at the ideologies of the researcher(Bae Choi et

al., 2013). The deductive method aids in the construction and designing of a strategy out of

an existing strategy and does not try to invent something totally new. The data regarding

corporate governance and how it has an impact on the process of accounting can be

understood.

3.4 Research Design

In this paper descriptive research design has been used in order to collect the data as

this method supports in the explanation, determination and recognition of the present factors

with the help of the explanation of the data that has been acquired for this paper.

3.5 Type of Data

It is seen that this paper is associated with the evolution of the data for various

companies that have been operating in Australia. Such data can only be extracted from

various articles and websites and even from the annual reports of the companies and

therefore, this paper has made use of the secondary data so that precise results can be attained

with respect to this paper.

3.6 Data collection

As a secondary data base research. Data will be collected from the selected companies’ as

per as mention bellow;

ASX Web sites (officially recorded data)

Their annual reports, published corporate governance

Relevant previous research papers, articles and journals

11

Kaur, s0274358

3.3 Research Approach

In accordance to this paper, it has been observed that deductive method of research

approach has been used as this mechanism assists in the process of development of the

specific hypotheses of the research by looking at the ideologies of the researcher(Bae Choi et

al., 2013). The deductive method aids in the construction and designing of a strategy out of

an existing strategy and does not try to invent something totally new. The data regarding

corporate governance and how it has an impact on the process of accounting can be

understood.

3.4 Research Design

In this paper descriptive research design has been used in order to collect the data as

this method supports in the explanation, determination and recognition of the present factors

with the help of the explanation of the data that has been acquired for this paper.

3.5 Type of Data

It is seen that this paper is associated with the evolution of the data for various

companies that have been operating in Australia. Such data can only be extracted from

various articles and websites and even from the annual reports of the companies and

therefore, this paper has made use of the secondary data so that precise results can be attained

with respect to this paper.

3.6 Data collection

As a secondary data base research. Data will be collected from the selected companies’ as

per as mention bellow;

ASX Web sites (officially recorded data)

Their annual reports, published corporate governance

Relevant previous research papers, articles and journals

11

Jasmeen

Kaur, s0274358

3.7 Research Technique

In accordance to this paper, it has been observed that quantitative research technique

has been used for the gathering of the data so that effective results can be attained with

respect to the impact of corporate governance in the accounting process can be understood as

this paper looks to gather information from the secondary resources and hence quantitative

technique can be resourceful for the collection of the precise data(Horne, 2015).

3.8 Sample

The annual reports of 5 Australian listed companies will be examined. Using the

research facility in the connected 5 databases, a search of these reports will be conducted on

the words “corporate” and “governance” (Collett & Hrasky, 2005).

3.9 The variables

Company size variable: there are three variables to measure company size, these are,

namely, total assets, revenue and market capitalisation.

Corporate performance: there are many variables to measure corporate performance

such as, stakeholder’s satisfaction (Clarkson, 1995) and also return on assets (ROA).

Profitability of the company (Collett & Hrasky, 2005).

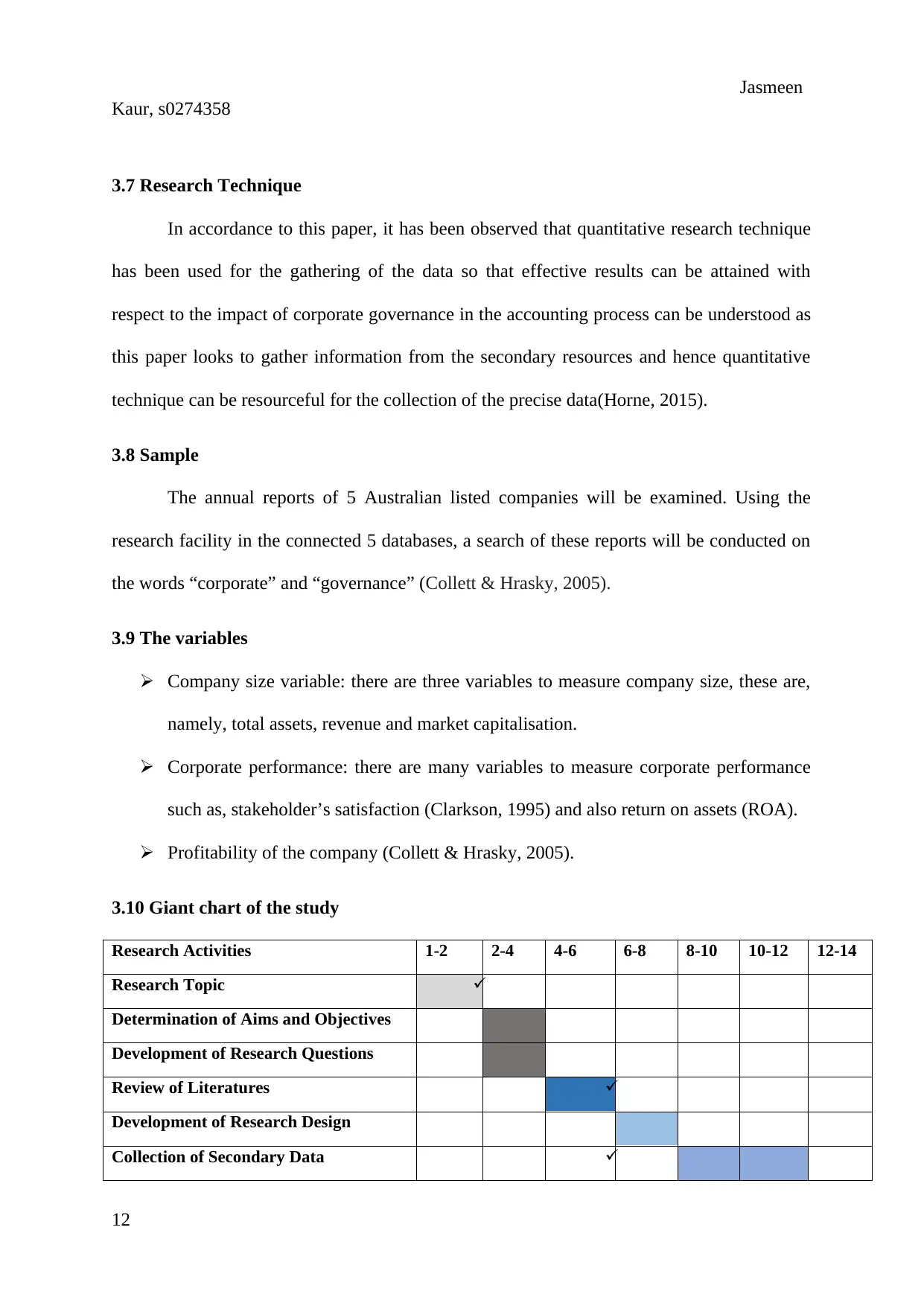

3.10 Giant chart of the study

Research Activities 1-2 2-4 4-6 6-8 8-10 10-12 12-14

Research Topic

Determination of Aims and Objectives

Development of Research Questions

Review of Literatures

Development of Research Design

Collection of Secondary Data

12

Kaur, s0274358

3.7 Research Technique

In accordance to this paper, it has been observed that quantitative research technique

has been used for the gathering of the data so that effective results can be attained with

respect to the impact of corporate governance in the accounting process can be understood as

this paper looks to gather information from the secondary resources and hence quantitative

technique can be resourceful for the collection of the precise data(Horne, 2015).

3.8 Sample

The annual reports of 5 Australian listed companies will be examined. Using the

research facility in the connected 5 databases, a search of these reports will be conducted on

the words “corporate” and “governance” (Collett & Hrasky, 2005).

3.9 The variables

Company size variable: there are three variables to measure company size, these are,

namely, total assets, revenue and market capitalisation.

Corporate performance: there are many variables to measure corporate performance

such as, stakeholder’s satisfaction (Clarkson, 1995) and also return on assets (ROA).

Profitability of the company (Collett & Hrasky, 2005).

3.10 Giant chart of the study

Research Activities 1-2 2-4 4-6 6-8 8-10 10-12 12-14

Research Topic

Determination of Aims and Objectives

Development of Research Questions

Review of Literatures

Development of Research Design

Collection of Secondary Data

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.