Introduction to Finance: Corporate Governance, Investment Analysis

VerifiedAdded on 2021/02/20

|14

|3501

|38

Report

AI Summary

This report delves into key aspects of finance, beginning with an examination of corporate governance, including its role in directing organizational activities and an evaluation of the UK's current approach, particularly the 'comply or explain' model and the agency theory. The report then proceeds to analyze investment decisions using various capital budgeting techniques, such as Accounting Rate of Return (ARR), Net Present Value (NPV), and Payback Period, comparing two machines and evaluating qualitative factors influencing investment choices. Finally, the report calculates and interprets break-even points and margins of safety for two different scenarios, offering insights into cost structures and profit analysis, alongside detailed calculations of variable costs, profit volume ratios, and fixed costs, providing a comprehensive overview of financial analysis and decision-making.

Introduction to

Finance

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

QUESTION 1...................................................................................................................................1

(a) Corporate Governance used to direct and control for organizational activities.....................1

(b) Critically evaluate the current approach of Corporate Governance in the UK......................2

QUESTION 2...................................................................................................................................2

QUESTION 3...................................................................................................................................5

QUESTION 4...................................................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

QUESTION 1...................................................................................................................................1

(a) Corporate Governance used to direct and control for organizational activities.....................1

(b) Critically evaluate the current approach of Corporate Governance in the UK......................2

QUESTION 2...................................................................................................................................2

QUESTION 3...................................................................................................................................5

QUESTION 4...................................................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION

Finance is the process to provide funding to the organization in order to perform their

business operations task and completed within given time frame. There are various financial

institutions which provide business finance which help the management to fulfil their working

capital requirement (Arratia, 2014). Every organization required funds in terms of capital for

business operations, marketing strategies, promotional activities etc. Basically all the actions and

activities required finance to perform or complete their task. This report cover various questions

which helps the individual to understand the of finances and make them capable to take effective

actions regarding their investments. This project file include the corporate governance which

required to control or direct the company and their activities. In addition include the approaches

of corporate governance in the UK.

MAIN BODY

QUESTION 1

(a) Corporate Governance used to direct and control for organizational activities

Corporate Governance: It is the system by which organizations are controlled or directed

and they fulfil their responsibility in order to governance their business. Here shareholder's play

major role because they appointed director of the company as well as auditor which helps in

analysing the records to satisfy themselves. In order to get growth in the organization,

management have to place a effective corporate governance and make sure to follow all the

compliances which already discussed.

Another responsibility of the board members is to formulate strategic aims, use effective

leadership to achieve business goals & objectives and manager have to supervise all the activities

of business operations. It will be directly reported to the shareholders on annual general meeting.

In context of organization, use of effective corporate governance will help the manager to

manage all the activities or actions and it further provide the benefits of controlling or directing

operational process (Bailey, 2017) .

Good governance positively impact the business and improve transparency &

accountability within existing systems. UK corporate governance build to deal with the

governance of those company who listed and enable to include all organizational types which

have different accountable structure.

1

Finance is the process to provide funding to the organization in order to perform their

business operations task and completed within given time frame. There are various financial

institutions which provide business finance which help the management to fulfil their working

capital requirement (Arratia, 2014). Every organization required funds in terms of capital for

business operations, marketing strategies, promotional activities etc. Basically all the actions and

activities required finance to perform or complete their task. This report cover various questions

which helps the individual to understand the of finances and make them capable to take effective

actions regarding their investments. This project file include the corporate governance which

required to control or direct the company and their activities. In addition include the approaches

of corporate governance in the UK.

MAIN BODY

QUESTION 1

(a) Corporate Governance used to direct and control for organizational activities

Corporate Governance: It is the system by which organizations are controlled or directed

and they fulfil their responsibility in order to governance their business. Here shareholder's play

major role because they appointed director of the company as well as auditor which helps in

analysing the records to satisfy themselves. In order to get growth in the organization,

management have to place a effective corporate governance and make sure to follow all the

compliances which already discussed.

Another responsibility of the board members is to formulate strategic aims, use effective

leadership to achieve business goals & objectives and manager have to supervise all the activities

of business operations. It will be directly reported to the shareholders on annual general meeting.

In context of organization, use of effective corporate governance will help the manager to

manage all the activities or actions and it further provide the benefits of controlling or directing

operational process (Bailey, 2017) .

Good governance positively impact the business and improve transparency &

accountability within existing systems. UK corporate governance build to deal with the

governance of those company who listed and enable to include all organizational types which

have different accountable structure.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Current approach of corporate governance in the UK:

UK adopted code based approach of corporate governance on premium listed

organizations. Those companies who follow the principle of “comply or explain” they does not

include it in the annual report. Now UK become the leader of comply & explain approach, here

organizations have to disclose their accounts in the annual report. It the help or stakeholders of

the company to make their decisions regarding their further actions or activities. Most of the

corporation follow the agency theory which is also consider the principle. With the help of this

theory, company can explain the issues and necessary actions in order to resolve it. It help the

business to maintain their relation between business principles or their agents. For example:

relationship between shareholders and executives of the company (Clark, Lai and Wójcik, 2015).

Agency theory work through resolving issue between two parties and for this

organizations hire agents to perform their task on behalf of company. In this theory, company

provide the decision making authority to the agents because it affect the principle financially.

Along with their, there are various difference in the priorities, interest or opinion.

(b) Critically evaluate the current approach of Corporate Governance in the UK

It has been critically evaluate that, corporate governance used to comply policies and

formulate strategies and make sure that it will be implemented effective which maximise the

production as well as profitability. In the UK, large organizations used agent theory which help

them to identity issues and then hire agents who will be responsible as well as have authority to

take effective decision in context of organization (Goldstein and Hackbarth, 2014).

QUESTION 2

Calculations:

Year Machine A Machine B PV factor @ 7% Cash Flow of A Cash Flow of B

0 120000 110000 1 -120000 -110000

1 24000 24000 0.9345794393 22429.9065420561 22429.9065420561

2 48000 25000 0.8734387283 41925.0589571142 21835.9682068303

3 50000 25000 0.8162978769 40814.8938445426 20407.4469222713

4 25000 50000 0.762895212 19072.3803011881 38144.7606023763

5 50000 0.7129861795 0 35649.3089741834

6 70000 0.6663422238 0 46643.9556671559

2

UK adopted code based approach of corporate governance on premium listed

organizations. Those companies who follow the principle of “comply or explain” they does not

include it in the annual report. Now UK become the leader of comply & explain approach, here

organizations have to disclose their accounts in the annual report. It the help or stakeholders of

the company to make their decisions regarding their further actions or activities. Most of the

corporation follow the agency theory which is also consider the principle. With the help of this

theory, company can explain the issues and necessary actions in order to resolve it. It help the

business to maintain their relation between business principles or their agents. For example:

relationship between shareholders and executives of the company (Clark, Lai and Wójcik, 2015).

Agency theory work through resolving issue between two parties and for this

organizations hire agents to perform their task on behalf of company. In this theory, company

provide the decision making authority to the agents because it affect the principle financially.

Along with their, there are various difference in the priorities, interest or opinion.

(b) Critically evaluate the current approach of Corporate Governance in the UK

It has been critically evaluate that, corporate governance used to comply policies and

formulate strategies and make sure that it will be implemented effective which maximise the

production as well as profitability. In the UK, large organizations used agent theory which help

them to identity issues and then hire agents who will be responsible as well as have authority to

take effective decision in context of organization (Goldstein and Hackbarth, 2014).

QUESTION 2

Calculations:

Year Machine A Machine B PV factor @ 7% Cash Flow of A Cash Flow of B

0 120000 110000 1 -120000 -110000

1 24000 24000 0.9345794393 22429.9065420561 22429.9065420561

2 48000 25000 0.8734387283 41925.0589571142 21835.9682068303

3 50000 25000 0.8162978769 40814.8938445426 20407.4469222713

4 25000 50000 0.762895212 19072.3803011881 38144.7606023763

5 50000 0.7129861795 0 35649.3089741834

6 70000 0.6663422238 0 46643.9556671559

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

NPV 4242.24 75111.35

(a) Accounting rate of return (ARR):

ARR of (A) = Average net profit / Initial Investment

= ( 6750 / 120000 ) * 100

= 5.625 %

ARR of (B) = Average net profit / Initial Investment

= ( 22333.33 / 110000 ) * 100

= 20.30 %

Working Notes:

Average net profit of machinery A = Average cash flow – Depreciation

= 36750 – 30000

= 6750

Average net profit of machinery B = Average cash flow – Depreciation

= 40666.66 – 18333.33

= 22333.33

Average Cash inflow of A = ( 24000 + 48000 + 50000 + 25000 ) / 4

= 36750

Average Cash inflow of B = ( 24000 + 25000 + 25000 + 50000 + 50000 + 70000 ) / 6

= 40666.66

Depreciation of Machinery A = ( Initial investments – Scrap value ) / Life of machinery

= ( 120000 – 0 ) / 4

= 30000.

Depreciation of Machinery B = ( Initial investments – Scrap value ) / Life of machinery

= ( 110000 – 0 ) / 6

= 18333.33

(b) NPV (Net Present Value):

NPV (A) = Cash Inflow – Cash Outflow

= 124242.23 – 120000

= 4242.23

NPV (A) = Cash Inflow – Cash Outflow

3

(a) Accounting rate of return (ARR):

ARR of (A) = Average net profit / Initial Investment

= ( 6750 / 120000 ) * 100

= 5.625 %

ARR of (B) = Average net profit / Initial Investment

= ( 22333.33 / 110000 ) * 100

= 20.30 %

Working Notes:

Average net profit of machinery A = Average cash flow – Depreciation

= 36750 – 30000

= 6750

Average net profit of machinery B = Average cash flow – Depreciation

= 40666.66 – 18333.33

= 22333.33

Average Cash inflow of A = ( 24000 + 48000 + 50000 + 25000 ) / 4

= 36750

Average Cash inflow of B = ( 24000 + 25000 + 25000 + 50000 + 50000 + 70000 ) / 6

= 40666.66

Depreciation of Machinery A = ( Initial investments – Scrap value ) / Life of machinery

= ( 120000 – 0 ) / 4

= 30000.

Depreciation of Machinery B = ( Initial investments – Scrap value ) / Life of machinery

= ( 110000 – 0 ) / 6

= 18333.33

(b) NPV (Net Present Value):

NPV (A) = Cash Inflow – Cash Outflow

= 124242.23 – 120000

= 4242.23

NPV (A) = Cash Inflow – Cash Outflow

3

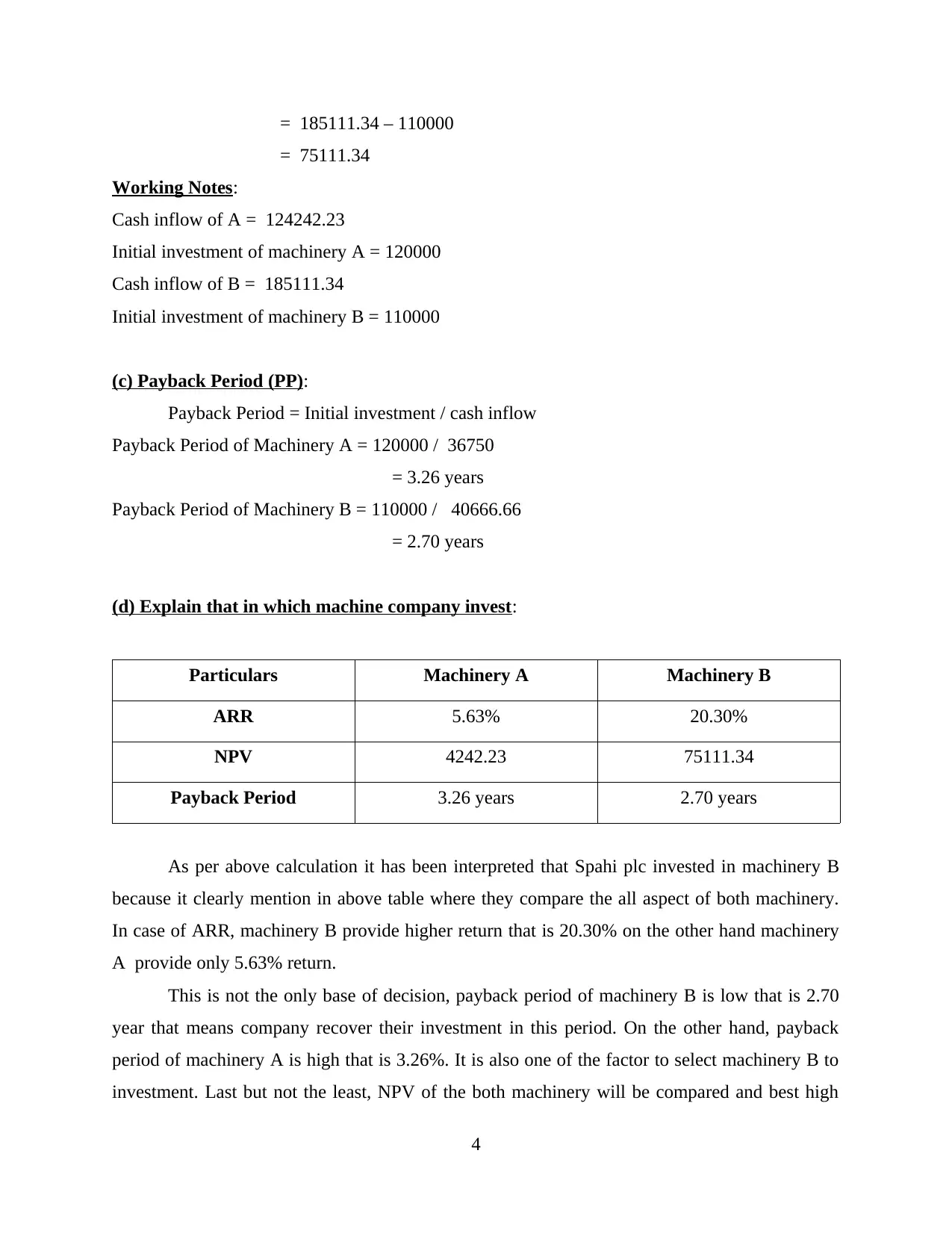

= 185111.34 – 110000

= 75111.34

Working Notes:

Cash inflow of A = 124242.23

Initial investment of machinery A = 120000

Cash inflow of B = 185111.34

Initial investment of machinery B = 110000

(c) Payback Period (PP):

Payback Period = Initial investment / cash inflow

Payback Period of Machinery A = 120000 / 36750

= 3.26 years

Payback Period of Machinery B = 110000 / 40666.66

= 2.70 years

(d) Explain that in which machine company invest:

Particulars Machinery A Machinery B

ARR 5.63% 20.30%

NPV 4242.23 75111.34

Payback Period 3.26 years 2.70 years

As per above calculation it has been interpreted that Spahi plc invested in machinery B

because it clearly mention in above table where they compare the all aspect of both machinery.

In case of ARR, machinery B provide higher return that is 20.30% on the other hand machinery

A provide only 5.63% return.

This is not the only base of decision, payback period of machinery B is low that is 2.70

year that means company recover their investment in this period. On the other hand, payback

period of machinery A is high that is 3.26%. It is also one of the factor to select machinery B to

investment. Last but not the least, NPV of the both machinery will be compared and best high

4

= 75111.34

Working Notes:

Cash inflow of A = 124242.23

Initial investment of machinery A = 120000

Cash inflow of B = 185111.34

Initial investment of machinery B = 110000

(c) Payback Period (PP):

Payback Period = Initial investment / cash inflow

Payback Period of Machinery A = 120000 / 36750

= 3.26 years

Payback Period of Machinery B = 110000 / 40666.66

= 2.70 years

(d) Explain that in which machine company invest:

Particulars Machinery A Machinery B

ARR 5.63% 20.30%

NPV 4242.23 75111.34

Payback Period 3.26 years 2.70 years

As per above calculation it has been interpreted that Spahi plc invested in machinery B

because it clearly mention in above table where they compare the all aspect of both machinery.

In case of ARR, machinery B provide higher return that is 20.30% on the other hand machinery

A provide only 5.63% return.

This is not the only base of decision, payback period of machinery B is low that is 2.70

year that means company recover their investment in this period. On the other hand, payback

period of machinery A is high that is 3.26%. It is also one of the factor to select machinery B to

investment. Last but not the least, NPV of the both machinery will be compared and best high

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

one selected that is machine B and its NPV about 75111.34. After analysing all the factors,

manager of Spahi Plc choose to invest in machinery B. By using capital budgeting method to

evaluate more efficient option for the company.

(e) Evaluate qualitative factors which might be consider by the manager of Spahi Plc:

Other than quantitative factors, manager of Spahi Plc have to consider qualitative factors

as well. Some of them discussed below:

Investors: Before making any decision regarding investment, manager of the company

have to give their reasons to select any one options along with proper evidence. Basically

it is important for Spahi Plc to consider with investors before investing money in the

manufacturing equipments.

Production: Investment will be done as per the requirement of production, if business

required to purchase new machinery due change in the technology or demand of

customer regarding products (Kaczynski, Salmona and Smith, 2014).

QUESTION 3

Break even point – This can be defined as a point on which companies cost and

revenues remain same (Wuttke and et.al., 2016). It is calculated in both manners including in

units and in revenues. Herein, below BEP is calculated in both terms as per the given data that is

as follows. It is good method to analysis the value of any project. Through the method measure

profit and loss of the organisation at different level of manufacturing and sales volume. To

predict the possible effect of changes is sales price to integrate with the fixed and variable costs.

There is required to predict the effect and changes in the efficiency on the basis of profitability of

an organisation.

Margin of safety – The term margin of safety can be defined as value of stock and its

market price. Same as the BEP, it is also calculated in both terms including units and revenues.

As well as it is calculated by help of break even point. It is useful technique that apply by the

organisation to know sales before decline and fall into loss. It will help to stay in competitive

environment in effective manner to predict the cots of the product of particular project (Kim, Cin

and Yi, 2015).

Break even point for year 2019 :

(a) Break even point in units – Fixed cost / contribution per unit

= 5430 / 125

5

manager of Spahi Plc choose to invest in machinery B. By using capital budgeting method to

evaluate more efficient option for the company.

(e) Evaluate qualitative factors which might be consider by the manager of Spahi Plc:

Other than quantitative factors, manager of Spahi Plc have to consider qualitative factors

as well. Some of them discussed below:

Investors: Before making any decision regarding investment, manager of the company

have to give their reasons to select any one options along with proper evidence. Basically

it is important for Spahi Plc to consider with investors before investing money in the

manufacturing equipments.

Production: Investment will be done as per the requirement of production, if business

required to purchase new machinery due change in the technology or demand of

customer regarding products (Kaczynski, Salmona and Smith, 2014).

QUESTION 3

Break even point – This can be defined as a point on which companies cost and

revenues remain same (Wuttke and et.al., 2016). It is calculated in both manners including in

units and in revenues. Herein, below BEP is calculated in both terms as per the given data that is

as follows. It is good method to analysis the value of any project. Through the method measure

profit and loss of the organisation at different level of manufacturing and sales volume. To

predict the possible effect of changes is sales price to integrate with the fixed and variable costs.

There is required to predict the effect and changes in the efficiency on the basis of profitability of

an organisation.

Margin of safety – The term margin of safety can be defined as value of stock and its

market price. Same as the BEP, it is also calculated in both terms including units and revenues.

As well as it is calculated by help of break even point. It is useful technique that apply by the

organisation to know sales before decline and fall into loss. It will help to stay in competitive

environment in effective manner to predict the cots of the product of particular project (Kim, Cin

and Yi, 2015).

Break even point for year 2019 :

(a) Break even point in units – Fixed cost / contribution per unit

= 5430 / 125

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

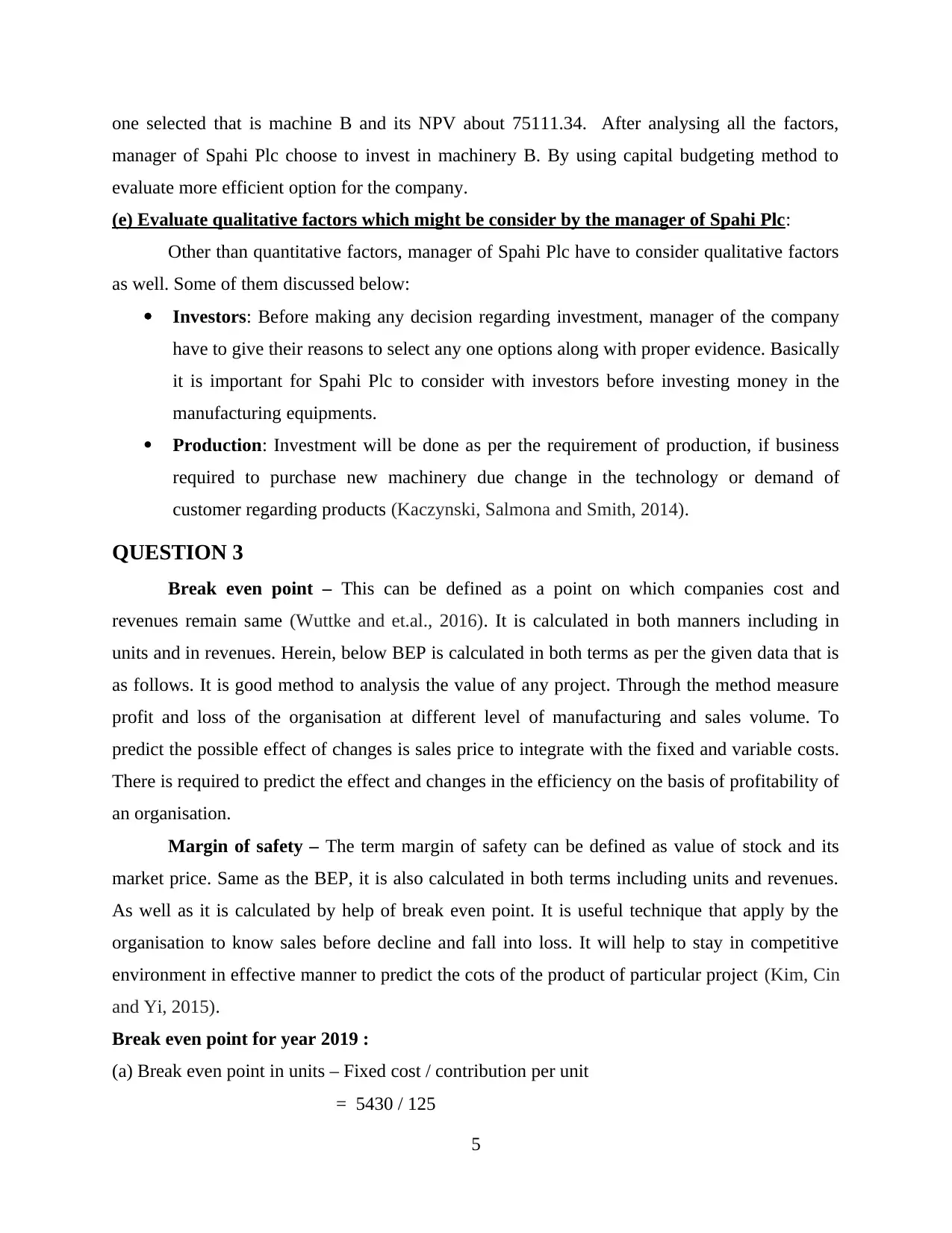

= 43.44 per unit

Break even point in revenue = Fixed cost / Profit volume ratio * 100

= 5430 / 41.66 * 100

= £ 13034

Margin of safety in units = Sales unit – break even in point in units

= 45000 – 43.44

= 44956.56 units

Margin of safety in revenues = Total sales – break even point in revenue

= 13500000 – 13034

= £ 13486966

Break even point for year 2020 :

Selling price (300*20 %) = £ 360 per unit

Fixed cost (5430 + 1450) = £ 6880

Break even point in units = Fixed cost / contribution per unit

= 6880 / 125

= 55.04 units

Contribution per unit = Selling price per unit – variable cost per unit

= 360 – 175

= 125 per unit

Break even point in revenue = Fixed cost / profit volume ratio

= 6880 / 34.72 * 100

= £ 19815.66

Profit volume ratio = Contribution per unit / selling price per unit * 100

= 125 / 360 * 100

= 34.72 %

6

Break even point in revenue = Fixed cost / Profit volume ratio * 100

= 5430 / 41.66 * 100

= £ 13034

Margin of safety in units = Sales unit – break even in point in units

= 45000 – 43.44

= 44956.56 units

Margin of safety in revenues = Total sales – break even point in revenue

= 13500000 – 13034

= £ 13486966

Break even point for year 2020 :

Selling price (300*20 %) = £ 360 per unit

Fixed cost (5430 + 1450) = £ 6880

Break even point in units = Fixed cost / contribution per unit

= 6880 / 125

= 55.04 units

Contribution per unit = Selling price per unit – variable cost per unit

= 360 – 175

= 125 per unit

Break even point in revenue = Fixed cost / profit volume ratio

= 6880 / 34.72 * 100

= £ 19815.66

Profit volume ratio = Contribution per unit / selling price per unit * 100

= 125 / 360 * 100

= 34.72 %

6

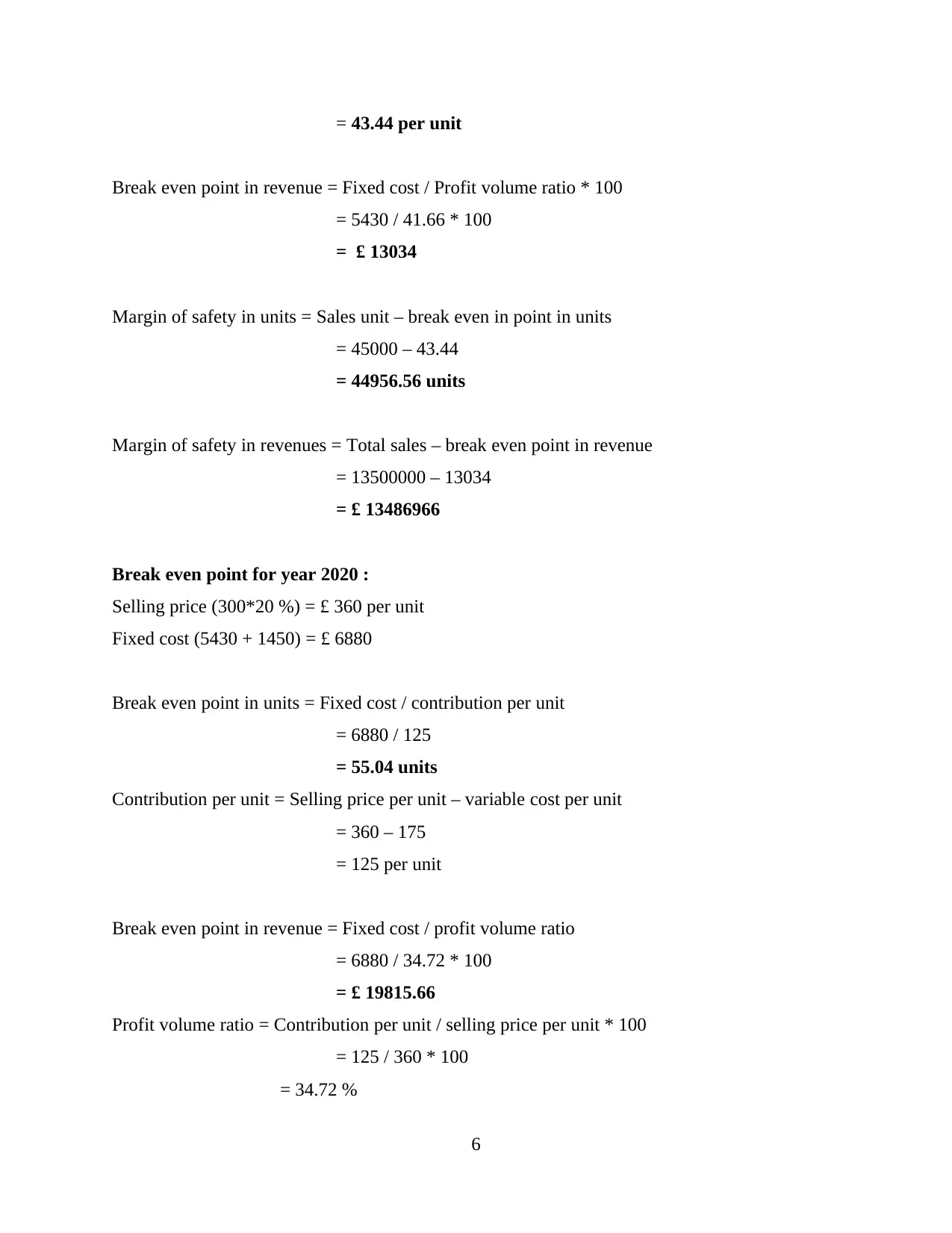

Margin of safety in units = Sales unit – break even in point in units

= 45000 – 55.04

= 44944.96 units

Margin of safety in revenues = Total sales* – break even point in revenue

= 16200000 – 19815.66

= £ 16180184.34

Calculation of total sales (45000 * 368) = 16200000

Working Note *

1. Contribution Per Unit:

Contribution per unit = Selling price per unit – variable cost per unit

= 300 – 175

= 125 per unit

2. Calculation of variable cost :

Particulars Amount (Per unit)

Direct material 125

Direct labour* 5

Variable manufacturing overhead 20

Variable selling expenses 15

Variable administrative expenses 10

Total 175

3. Calculation of direct labour :

Time taken to produce one unit = 20 minutes

Time taken to produce 45000 units (45000 * 20) = 900000 minutes or 15000 hours

Total direct labour cost (15000 * 15) = £ 225000

Thus, per unit labour cost (225000 / 45000) = 5 per unit

7

= 45000 – 55.04

= 44944.96 units

Margin of safety in revenues = Total sales* – break even point in revenue

= 16200000 – 19815.66

= £ 16180184.34

Calculation of total sales (45000 * 368) = 16200000

Working Note *

1. Contribution Per Unit:

Contribution per unit = Selling price per unit – variable cost per unit

= 300 – 175

= 125 per unit

2. Calculation of variable cost :

Particulars Amount (Per unit)

Direct material 125

Direct labour* 5

Variable manufacturing overhead 20

Variable selling expenses 15

Variable administrative expenses 10

Total 175

3. Calculation of direct labour :

Time taken to produce one unit = 20 minutes

Time taken to produce 45000 units (45000 * 20) = 900000 minutes or 15000 hours

Total direct labour cost (15000 * 15) = £ 225000

Thus, per unit labour cost (225000 / 45000) = 5 per unit

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

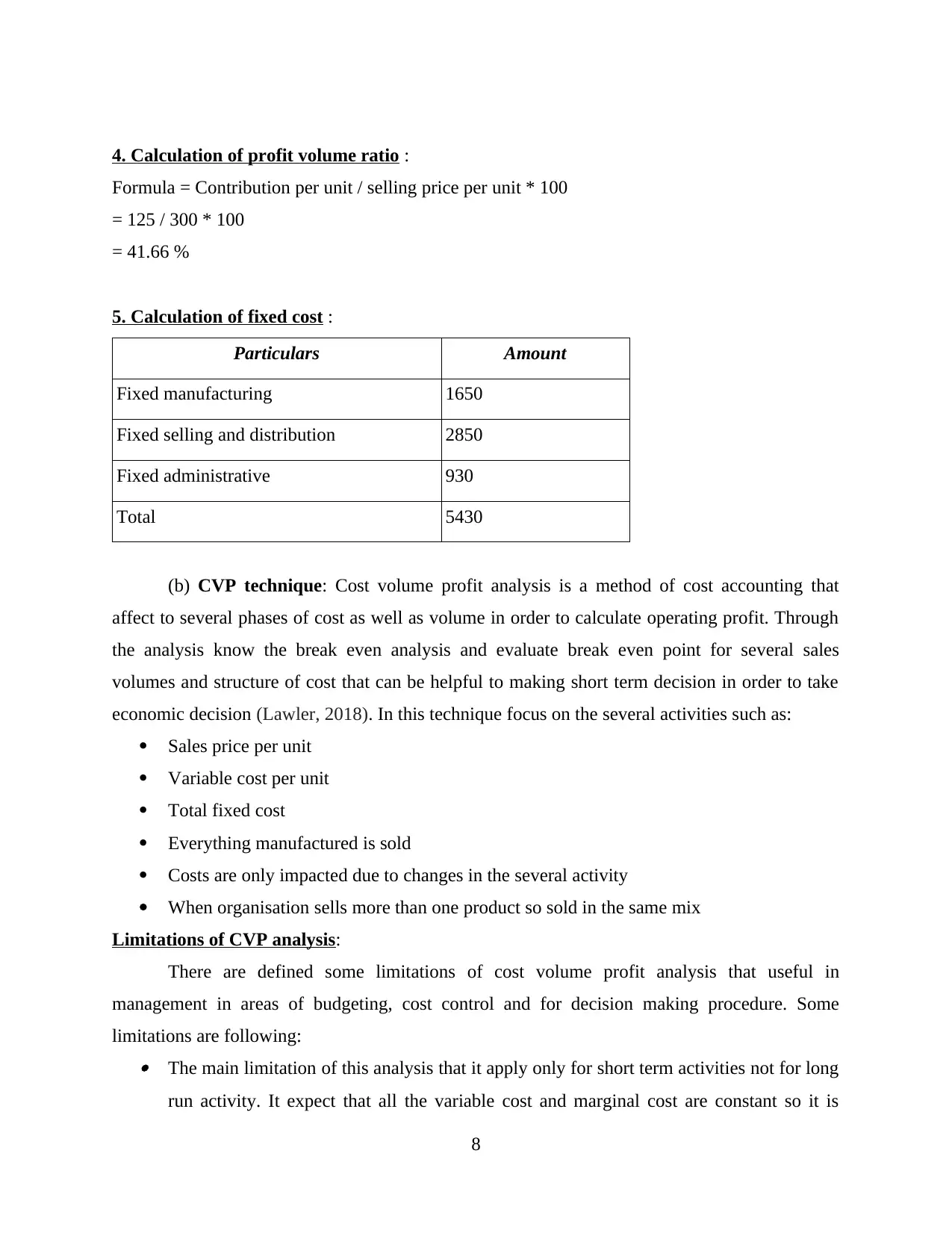

4. Calculation of profit volume ratio :

Formula = Contribution per unit / selling price per unit * 100

= 125 / 300 * 100

= 41.66 %

5. Calculation of fixed cost :

Particulars Amount

Fixed manufacturing 1650

Fixed selling and distribution 2850

Fixed administrative 930

Total 5430

(b) CVP technique: Cost volume profit analysis is a method of cost accounting that

affect to several phases of cost as well as volume in order to calculate operating profit. Through

the analysis know the break even analysis and evaluate break even point for several sales

volumes and structure of cost that can be helpful to making short term decision in order to take

economic decision (Lawler, 2018). In this technique focus on the several activities such as:

Sales price per unit

Variable cost per unit

Total fixed cost

Everything manufactured is sold

Costs are only impacted due to changes in the several activity

When organisation sells more than one product so sold in the same mix

Limitations of CVP analysis:

There are defined some limitations of cost volume profit analysis that useful in

management in areas of budgeting, cost control and for decision making procedure. Some

limitations are following: The main limitation of this analysis that it apply only for short term activities not for long

run activity. It expect that all the variable cost and marginal cost are constant so it is

8

Formula = Contribution per unit / selling price per unit * 100

= 125 / 300 * 100

= 41.66 %

5. Calculation of fixed cost :

Particulars Amount

Fixed manufacturing 1650

Fixed selling and distribution 2850

Fixed administrative 930

Total 5430

(b) CVP technique: Cost volume profit analysis is a method of cost accounting that

affect to several phases of cost as well as volume in order to calculate operating profit. Through

the analysis know the break even analysis and evaluate break even point for several sales

volumes and structure of cost that can be helpful to making short term decision in order to take

economic decision (Lawler, 2018). In this technique focus on the several activities such as:

Sales price per unit

Variable cost per unit

Total fixed cost

Everything manufactured is sold

Costs are only impacted due to changes in the several activity

When organisation sells more than one product so sold in the same mix

Limitations of CVP analysis:

There are defined some limitations of cost volume profit analysis that useful in

management in areas of budgeting, cost control and for decision making procedure. Some

limitations are following: The main limitation of this analysis that it apply only for short term activities not for long

run activity. It expect that all the variable cost and marginal cost are constant so it is

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

apply in small deviations where anticipate that set division in between fixed cost and

variable cost (Ruppert, 2014). Human error: In this technique increase chances of human error where plug in variable

cost to set future performance in rage of possibilities. The main disadvantage of this

manager can not keep data in detailed manner due to record in short way. The project of

the organisation based on the predication of cost instead of precise numbers and

inaccurate projections. Limited for multi product operation: This technique is advantageous but in limited

manner due to get short information about multi product operation (Soros, 2015). Due to

more determination it is done by the business manager where applied this approach on

the single product. Several product in the company like restaurants has face critical time

regarding to CVP analysis due to set menu items that divided through variable cost ratios.

It is challenging for CVP analysis due to face more difficulties and it must be done for

every product.

Approximation with CVP: This analysis mainly based on the particular data where

needed to tremendous attention for the detail information. So it will provide approximate

answer of each question instead of accurate answer. These answers are based on the

hypothetical basis so it is better than it offers right answer for problem solving. So fir the

judgement require to investigate answer of each question that will take more time or

create problem for organisation.

Economist model of CVP:

As per the economy gain attention regarding to problem in order to analysis the optimum

level of a organisation. The main aim of the profit maximisation to reach on optimum level for

the activity is when marginal cost similar to marginal revenue. The particular analysis based on

the following assumptions like:

The economic approach thinks that the utility of total cost is curvilinear and not linear

based on the accounting approach.

The economic approach is equally to accounting approach where understand that volume

is the sole that analysis for cost and change profit (Tanzi, 2016).

As per the both economic approach it is analysed that two assumption are related to cost

function where set the range of activity that anticipate in economic model as well as accounting

9

variable cost (Ruppert, 2014). Human error: In this technique increase chances of human error where plug in variable

cost to set future performance in rage of possibilities. The main disadvantage of this

manager can not keep data in detailed manner due to record in short way. The project of

the organisation based on the predication of cost instead of precise numbers and

inaccurate projections. Limited for multi product operation: This technique is advantageous but in limited

manner due to get short information about multi product operation (Soros, 2015). Due to

more determination it is done by the business manager where applied this approach on

the single product. Several product in the company like restaurants has face critical time

regarding to CVP analysis due to set menu items that divided through variable cost ratios.

It is challenging for CVP analysis due to face more difficulties and it must be done for

every product.

Approximation with CVP: This analysis mainly based on the particular data where

needed to tremendous attention for the detail information. So it will provide approximate

answer of each question instead of accurate answer. These answers are based on the

hypothetical basis so it is better than it offers right answer for problem solving. So fir the

judgement require to investigate answer of each question that will take more time or

create problem for organisation.

Economist model of CVP:

As per the economy gain attention regarding to problem in order to analysis the optimum

level of a organisation. The main aim of the profit maximisation to reach on optimum level for

the activity is when marginal cost similar to marginal revenue. The particular analysis based on

the following assumptions like:

The economic approach thinks that the utility of total cost is curvilinear and not linear

based on the accounting approach.

The economic approach is equally to accounting approach where understand that volume

is the sole that analysis for cost and change profit (Tanzi, 2016).

As per the both economic approach it is analysed that two assumption are related to cost

function where set the range of activity that anticipate in economic model as well as accounting

9

level. It become reason of range of outputs enough due to reason of important changes in

efficiency whereas CVP relation fictitious in a set small range of activity.

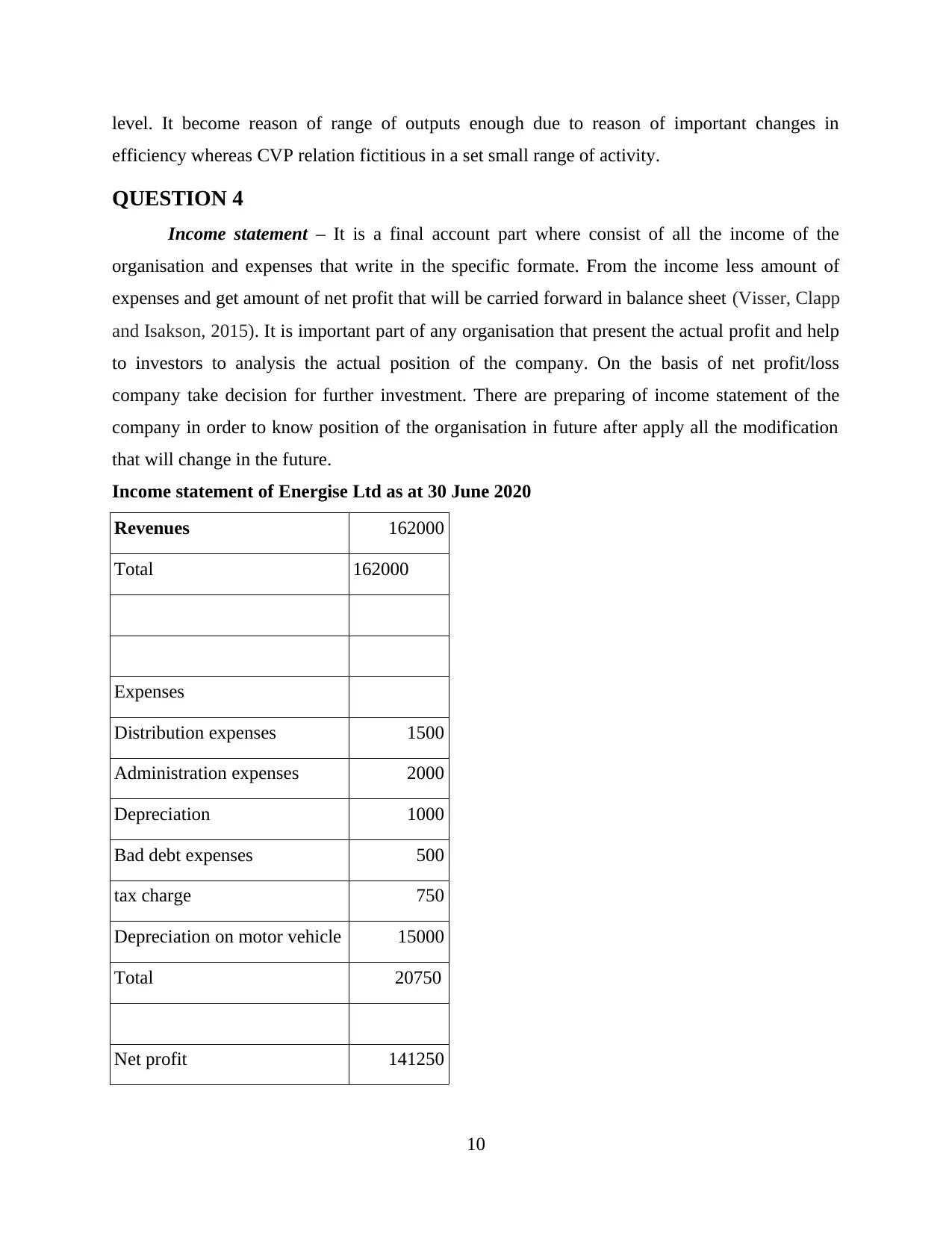

QUESTION 4

Income statement – It is a final account part where consist of all the income of the

organisation and expenses that write in the specific formate. From the income less amount of

expenses and get amount of net profit that will be carried forward in balance sheet (Visser, Clapp

and Isakson, 2015). It is important part of any organisation that present the actual profit and help

to investors to analysis the actual position of the company. On the basis of net profit/loss

company take decision for further investment. There are preparing of income statement of the

company in order to know position of the organisation in future after apply all the modification

that will change in the future.

Income statement of Energise Ltd as at 30 June 2020

Revenues 162000

Total 162000

Expenses

Distribution expenses 1500

Administration expenses 2000

Depreciation 1000

Bad debt expenses 500

tax charge 750

Depreciation on motor vehicle 15000

Total 20750

Net profit 141250

10

efficiency whereas CVP relation fictitious in a set small range of activity.

QUESTION 4

Income statement – It is a final account part where consist of all the income of the

organisation and expenses that write in the specific formate. From the income less amount of

expenses and get amount of net profit that will be carried forward in balance sheet (Visser, Clapp

and Isakson, 2015). It is important part of any organisation that present the actual profit and help

to investors to analysis the actual position of the company. On the basis of net profit/loss

company take decision for further investment. There are preparing of income statement of the

company in order to know position of the organisation in future after apply all the modification

that will change in the future.

Income statement of Energise Ltd as at 30 June 2020

Revenues 162000

Total 162000

Expenses

Distribution expenses 1500

Administration expenses 2000

Depreciation 1000

Bad debt expenses 500

tax charge 750

Depreciation on motor vehicle 15000

Total 20750

Net profit 141250

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.