Financial Sustainability and Integrated Reporting: Project Report

VerifiedAdded on 2020/04/13

|14

|4371

|36

Project

AI Summary

This project report delves into the critical aspects of integrated reporting and corporate governance. It begins with an introduction highlighting the significance of corporate governance and its evolution, particularly in the context of financial sustainability. The report then explores the concept of integrated reporting, its origins in corporate governance, and its role in enhancing a company's ability to manage value across different time horizons. A literature review provides a comprehensive overview of the subject, citing various studies and articles to explain the concepts. The report further analyzes the relationship between integrated reporting and corporate governance, emphasizing how integrated reporting connects financial and non-financial factors, governance, and environmental considerations. The report also examines the components of corporate governance within integrated reporting, including business models, risk management, strategic objectives, future outlook, performance evaluation, and governance structures. The report concludes by emphasizing the importance of integrated reporting as a communication tool for stakeholders, governments, and management, providing a clear picture of a company's position and performance. The project aims to provide a detailed understanding of integrated reporting and its role in corporate governance for achieving financial sustainability.

Running Head: Financial Sustainability Integrated Reporting 1

Project Report: Financial Sustainability Integrated Reporting

Project Report: Financial Sustainability Integrated Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Sustainability Integrated Reporting 2

Contents

Introduction.......................................................................................................................3

Corporate governance.......................................................................................................3

Literature review...............................................................................................................4

Corporate governance as integrated report’s part:............................................................6

Relationship between integrated reporting and corporate governance.............................8

Conclusion................................................................................................................................10

References.......................................................................................................................12

Contents

Introduction.......................................................................................................................3

Corporate governance.......................................................................................................3

Literature review...............................................................................................................4

Corporate governance as integrated report’s part:............................................................6

Relationship between integrated reporting and corporate governance.............................8

Conclusion................................................................................................................................10

References.......................................................................................................................12

Financial Sustainability Integrated Reporting 3

Introduction:

Corporate governance is crucial for every organization. In the given case, corporate

governance has been analyzed. Ms Serrah was interested to do a course in integrated

reporting but due to some issues, she has moved on and didn’t appear in the course. Now in

this case, she has shown her willingness to know more about integrated reporting and

corporate governance. In this report, the main study has been done over the integrated

reporting. The origin of integrated origin is in corporate governance. It assists the

organization in enhancing the ability of the company in managing the value of the

organization in short term, medium term and long term.

The corporate governance is an internal system which contains the process,

procedure, people and various strategies that serve the needs and requirements of the

stakeholders as well as shareholders by managing, directing and controlling the activities by

the top level management of the company along with savvy, integrity and objectivity of the

company. The main goal of this report is to analyze and explain the importance, relationship

and concepts of the integrated reporting. Further, various other concept of the integrated

reporting has also been analyzed to enlighten the concept of integrated reporting for Ms

Serrah.

Corporate governance:

Corporate governance, corporate reporting, responsibility and integrated reporting are

the significant terms which have been used in an international business to manage the

business. The main motive behind enhancing these terms is the financial crisis and the

various problems in the market. The enhancement incidence behind integrated reporting is of

accounting scandals and environmental disaster (Eccles & Krzus, 2010). Further, business

concepts are quite complex and thus it is required for the businesses to manage and maintain

the corporate reporting. The concept of corporate reporting makes it simple for the business

to enlarge the business.

Earlier, the financial reporting used to be enough for the international business to

manage and analyze the performance and the position in the market. But now the market has

been complex and with the complexity, various problems have also been enhanced in the

market (Jensen & Berg, 2012). So, the concept of integrated reporting would be useful for the

company to manage all the complexity and the problems in the organization.

Introduction:

Corporate governance is crucial for every organization. In the given case, corporate

governance has been analyzed. Ms Serrah was interested to do a course in integrated

reporting but due to some issues, she has moved on and didn’t appear in the course. Now in

this case, she has shown her willingness to know more about integrated reporting and

corporate governance. In this report, the main study has been done over the integrated

reporting. The origin of integrated origin is in corporate governance. It assists the

organization in enhancing the ability of the company in managing the value of the

organization in short term, medium term and long term.

The corporate governance is an internal system which contains the process,

procedure, people and various strategies that serve the needs and requirements of the

stakeholders as well as shareholders by managing, directing and controlling the activities by

the top level management of the company along with savvy, integrity and objectivity of the

company. The main goal of this report is to analyze and explain the importance, relationship

and concepts of the integrated reporting. Further, various other concept of the integrated

reporting has also been analyzed to enlighten the concept of integrated reporting for Ms

Serrah.

Corporate governance:

Corporate governance, corporate reporting, responsibility and integrated reporting are

the significant terms which have been used in an international business to manage the

business. The main motive behind enhancing these terms is the financial crisis and the

various problems in the market. The enhancement incidence behind integrated reporting is of

accounting scandals and environmental disaster (Eccles & Krzus, 2010). Further, business

concepts are quite complex and thus it is required for the businesses to manage and maintain

the corporate reporting. The concept of corporate reporting makes it simple for the business

to enlarge the business.

Earlier, the financial reporting used to be enough for the international business to

manage and analyze the performance and the position in the market. But now the market has

been complex and with the complexity, various problems have also been enhanced in the

market (Jensen & Berg, 2012). So, the concept of integrated reporting would be useful for the

company to manage all the complexity and the problems in the organization.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Sustainability Integrated Reporting 4

Firstly, the concept of integrated reporting depict that the performance of an

international company bases over various financial and non-financial factors. For analyzing

the better performance of the company, it becomes important for the management of the

company to relate all these aspects and the variables with the help of the integrated reporting

to make a better study and decision (Frias‐Aceituno, Rodriguez‐Ariza & Garcia‐Sanchez,

2013). Interpreted reporting connects governance, financial, non financial, remuneration,

social, environmental and economical factors of a company. The concept of integrated

reporting could also be analyzed through the definition that this concept follows the targets

and strategies of the company to set the business.

Literature review:

The concept of integrated reporting could be understood more briefly through

conducting a study over various articles, study and magazine. Currently, entire corporate

scandals have been taken place due to corporate scandals and the insufficient control system

over the business. This all has impacted the policies and corporate governance power of the

company. Basically corporate governance arises because of conflicts among two parties of

the company and their interest. The associated parties are managers of the company and the

shareholders of the company. de Villiers, Rinaldi & Unerman, (2014) has defined that the

corporate governance is n internal system which contains the process, procedure, people and

various strategies that serves the needs and requirements of the stakeholders as well as

shareholders by managing, directing and controlling the activities by the top level

management of the company along with savvy, integrity and objectivity of the company

(Adams & Simnett, 2011).

Further, various organizations and the corporate governance department of various

countries have explained that the corporate governance is a set of companionship among the

management of the company, board of directors, shareholders of the company and the

stakeholders of the company. Further, Eccles & Saltzman, (2011) has explained in his study

that corporate governance explains the various significant issues which manages and

integrates the social, economical and environmental values and the business operations of the

company.

According to the Flower (2015), it is required for every organization to manage and

maintain the position of the corporate governance in an organization. Corporate governance

must be disclosed by the every organization on the aspect of politics, risk, social values,

Firstly, the concept of integrated reporting depict that the performance of an

international company bases over various financial and non-financial factors. For analyzing

the better performance of the company, it becomes important for the management of the

company to relate all these aspects and the variables with the help of the integrated reporting

to make a better study and decision (Frias‐Aceituno, Rodriguez‐Ariza & Garcia‐Sanchez,

2013). Interpreted reporting connects governance, financial, non financial, remuneration,

social, environmental and economical factors of a company. The concept of integrated

reporting could also be analyzed through the definition that this concept follows the targets

and strategies of the company to set the business.

Literature review:

The concept of integrated reporting could be understood more briefly through

conducting a study over various articles, study and magazine. Currently, entire corporate

scandals have been taken place due to corporate scandals and the insufficient control system

over the business. This all has impacted the policies and corporate governance power of the

company. Basically corporate governance arises because of conflicts among two parties of

the company and their interest. The associated parties are managers of the company and the

shareholders of the company. de Villiers, Rinaldi & Unerman, (2014) has defined that the

corporate governance is n internal system which contains the process, procedure, people and

various strategies that serves the needs and requirements of the stakeholders as well as

shareholders by managing, directing and controlling the activities by the top level

management of the company along with savvy, integrity and objectivity of the company

(Adams & Simnett, 2011).

Further, various organizations and the corporate governance department of various

countries have explained that the corporate governance is a set of companionship among the

management of the company, board of directors, shareholders of the company and the

stakeholders of the company. Further, Eccles & Saltzman, (2011) has explained in his study

that corporate governance explains the various significant issues which manages and

integrates the social, economical and environmental values and the business operations of the

company.

According to the Flower (2015), it is required for every organization to manage and

maintain the position of the corporate governance in an organization. Corporate governance

must be disclosed by the every organization on the aspect of politics, risk, social values,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Sustainability Integrated Reporting 5

stakeholder’s perspective etc. to manage the diversity in the organization. Corporate

governance is a critical aspect of an organization. Nowadays, the principle of integrated

reporting has been more complex with the increased diversity and competition in the market.

Current changes into the corporate governance and integrated reporting have been driven

changes into the global level (Abeysekera, 2013).

Currently corporate governance has been managed and arose by the companies to

reduce the level of complexity. Ruggie (2011) has depicted in a study depict the corporate

governance is a sign of modern technology and changes in an organization. More, Admas

(2015), has briefed in his study that corporate governance explains the various significant

issues which manages and integrates the social, economical and environmental values and the

business operations of the company.

Integrated reporting is suitable for a company for a short term, long term and medium

term for a business. It assists the company to manage and administer the various policies and

the complexity in the operations of a business (Cheng et al, 2014). Integrated reporting

explains about the information of an organization in context of financial and non financial

term. It also expresses about the performance, strategy, prospects and governance which

reflects the commercial, social and environmental context in which the corporate governance

performs. This concept offers the concise and clear picture about the organization. This

concept creates and enhances the value of the company in future (Suter, Oelke, Adair &

Armitage, 2009).

An international committee has also been set by the international organization

community. This organizational committee evaluates the corporate governance and integrated

reporting of an organization and takes further steps accordingly. More, the concept of

integrated reporting depict that the performance of an international company bases over

various financial and non-financial factors (Cheng et al, 2014). For analyzing the better

performance of the company, it becomes important for the management of the company to

relate all these aspects and the variables with the help of the integrated reporting to make a

better study and decision (Busco, 2014).

According to the Admas (2015), it is required for every organization to manage and

maintain the position of the corporate governance in an organization. Current changes into

the corporate governance and integrated reporting have been driven changes into the global

level. Interpreted reporting connects governance, financial, non financial, remuneration,

stakeholder’s perspective etc. to manage the diversity in the organization. Corporate

governance is a critical aspect of an organization. Nowadays, the principle of integrated

reporting has been more complex with the increased diversity and competition in the market.

Current changes into the corporate governance and integrated reporting have been driven

changes into the global level (Abeysekera, 2013).

Currently corporate governance has been managed and arose by the companies to

reduce the level of complexity. Ruggie (2011) has depicted in a study depict the corporate

governance is a sign of modern technology and changes in an organization. More, Admas

(2015), has briefed in his study that corporate governance explains the various significant

issues which manages and integrates the social, economical and environmental values and the

business operations of the company.

Integrated reporting is suitable for a company for a short term, long term and medium

term for a business. It assists the company to manage and administer the various policies and

the complexity in the operations of a business (Cheng et al, 2014). Integrated reporting

explains about the information of an organization in context of financial and non financial

term. It also expresses about the performance, strategy, prospects and governance which

reflects the commercial, social and environmental context in which the corporate governance

performs. This concept offers the concise and clear picture about the organization. This

concept creates and enhances the value of the company in future (Suter, Oelke, Adair &

Armitage, 2009).

An international committee has also been set by the international organization

community. This organizational committee evaluates the corporate governance and integrated

reporting of an organization and takes further steps accordingly. More, the concept of

integrated reporting depict that the performance of an international company bases over

various financial and non-financial factors (Cheng et al, 2014). For analyzing the better

performance of the company, it becomes important for the management of the company to

relate all these aspects and the variables with the help of the integrated reporting to make a

better study and decision (Busco, 2014).

According to the Admas (2015), it is required for every organization to manage and

maintain the position of the corporate governance in an organization. Current changes into

the corporate governance and integrated reporting have been driven changes into the global

level. Interpreted reporting connects governance, financial, non financial, remuneration,

Financial Sustainability Integrated Reporting 6

social, environmental and economical factors of a company (de Villiers, Rinaldi & Unerman,

2014). The concept of integrated reporting could also be analyzed through the definition that

this concept follows the targets and strategies of the company to set the business.

Further, it has been explained by Dumitru, Glavan, Gorgan & Dumitru, 2013) that

Corporate governance, corporate reporting, responsibility and integrated reporting are the

significant terms which have been used in an international business to manage the business.

Moreover, a study of Azapagic, (2003) express that the main motive behind enhancing

Corporate governance and responsibility and integrated reporting are the financial crisis and

the various problems in the market. Further, it has been added by Daub (2007) that the

enhancement incidence behind integrated reporting is of accounting scandals and

environmental disaster. Further, business concepts are quite complex and thus it is required

for the businesses to manage and maintain the corporate reporting (Schaltegger & Wagner,

2006). The concept of corporate reporting makes it simple for the business to enlarge the

business.

Jensen & Berg, (2012) has depicted into his study that in ancient times, financial

reporting was quite enough for the companies which are performing their business in the

international market, to manage and analyze the performance and the position in the market.

But now the market has been complex and with the complexity, various problems have also

been enhanced in the market. Further, as a conclusive study, it has been expressed by OECD

(2017) that the concept of integrated reporting would be useful for the company to manage all

the complexity and the problems in the organization.

Further, according to the study of Burritt, Hahn & Schaltegger, (2002), it has been

found that the integrated reporting is a process which has been founded by the organization

on the perspective of integrated thinking that outcomes in a periodic report of integrated

system by a company about the creation of value over time, communication and other related

factors. More, it has also been defined that the integrated reporting is an integrated

representation and holistic of the company’s performance in terms of responsibility as well as

sustainability and finance of the company.

Corporate governance as integrated report’s part:

Because, nowadays many companies, governments and the stakeholders have already

known the significance of social, environmental, governance information as a huge part of

annual report which is needed by the organization. Integrated reporting is the main part which

social, environmental and economical factors of a company (de Villiers, Rinaldi & Unerman,

2014). The concept of integrated reporting could also be analyzed through the definition that

this concept follows the targets and strategies of the company to set the business.

Further, it has been explained by Dumitru, Glavan, Gorgan & Dumitru, 2013) that

Corporate governance, corporate reporting, responsibility and integrated reporting are the

significant terms which have been used in an international business to manage the business.

Moreover, a study of Azapagic, (2003) express that the main motive behind enhancing

Corporate governance and responsibility and integrated reporting are the financial crisis and

the various problems in the market. Further, it has been added by Daub (2007) that the

enhancement incidence behind integrated reporting is of accounting scandals and

environmental disaster. Further, business concepts are quite complex and thus it is required

for the businesses to manage and maintain the corporate reporting (Schaltegger & Wagner,

2006). The concept of corporate reporting makes it simple for the business to enlarge the

business.

Jensen & Berg, (2012) has depicted into his study that in ancient times, financial

reporting was quite enough for the companies which are performing their business in the

international market, to manage and analyze the performance and the position in the market.

But now the market has been complex and with the complexity, various problems have also

been enhanced in the market. Further, as a conclusive study, it has been expressed by OECD

(2017) that the concept of integrated reporting would be useful for the company to manage all

the complexity and the problems in the organization.

Further, according to the study of Burritt, Hahn & Schaltegger, (2002), it has been

found that the integrated reporting is a process which has been founded by the organization

on the perspective of integrated thinking that outcomes in a periodic report of integrated

system by a company about the creation of value over time, communication and other related

factors. More, it has also been defined that the integrated reporting is an integrated

representation and holistic of the company’s performance in terms of responsibility as well as

sustainability and finance of the company.

Corporate governance as integrated report’s part:

Because, nowadays many companies, governments and the stakeholders have already

known the significance of social, environmental, governance information as a huge part of

annual report which is needed by the organization. Integrated reporting is the main part which

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Sustainability Integrated Reporting 7

offers stakeholders, government and the management of the company about the full picture of

structured around, performance and business model, strategic objective of organization which

includes financial and non financial information of the company. According to the

Schaltegger & Wagner, (2006), an integrated reporting is the summary of communication

about the governance, strategy, policy, prospects, performance in concern of external

environment of the company to lead the value creation in short term, long term and medium

term of the business.

In different words, the concept of integrated reporting is a significant document which

communicates with the companies, governments and the stakeholders about the current

position of the company and the governance, strategy, policy, prospects, performance of the

company. This report expresses the stakeholders about the value creation story of the

organization and policies in an understandable manner. Thus, the reports of integrated

reporting depict about the activities, risks, abilities and opportunities of the company which

has been grabbed by the company or could be grabbed by the company in near future

(Enquist, Johnson & Skålén, 2006).

It has been suggested that the main documents of the company and its communication

level is integrated reporting. It has been suggested that the most significant factors and

guiding principles which refers to the information which is not correct. Following are some

of the elements of the corporate governance:

Business model and organizational overview:

This system assists the organization to analyze that how the sustainable value could be

created in long, short and medium term?

Including risk, operating context and opportunities:

This system assists the organization to analyze that what could be the associated risk,

opportunities and the operating context of the company in order to manage and enhance the

operations and the performance of the company? (IIRC, 2013)

Strategy and strategic objective to achieve the objectives:

This system assists the organization to analyze that what are the objectives and what

could be the strategies to achieve that goals of the company in order to manage and enhance

the operations and the performance of the company?

Future outlook:

offers stakeholders, government and the management of the company about the full picture of

structured around, performance and business model, strategic objective of organization which

includes financial and non financial information of the company. According to the

Schaltegger & Wagner, (2006), an integrated reporting is the summary of communication

about the governance, strategy, policy, prospects, performance in concern of external

environment of the company to lead the value creation in short term, long term and medium

term of the business.

In different words, the concept of integrated reporting is a significant document which

communicates with the companies, governments and the stakeholders about the current

position of the company and the governance, strategy, policy, prospects, performance of the

company. This report expresses the stakeholders about the value creation story of the

organization and policies in an understandable manner. Thus, the reports of integrated

reporting depict about the activities, risks, abilities and opportunities of the company which

has been grabbed by the company or could be grabbed by the company in near future

(Enquist, Johnson & Skålén, 2006).

It has been suggested that the main documents of the company and its communication

level is integrated reporting. It has been suggested that the most significant factors and

guiding principles which refers to the information which is not correct. Following are some

of the elements of the corporate governance:

Business model and organizational overview:

This system assists the organization to analyze that how the sustainable value could be

created in long, short and medium term?

Including risk, operating context and opportunities:

This system assists the organization to analyze that what could be the associated risk,

opportunities and the operating context of the company in order to manage and enhance the

operations and the performance of the company? (IIRC, 2013)

Strategy and strategic objective to achieve the objectives:

This system assists the organization to analyze that what are the objectives and what

could be the strategies to achieve that goals of the company in order to manage and enhance

the operations and the performance of the company?

Future outlook:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Sustainability Integrated Reporting 8

This system assists the organization to analyze that what are the opportunities,

strategies, threats, challenges, uncertainties and other aspects of the company in order to

manage and enhance the performance of the company?

Performance:

This system assists the organization to analyze that what could be the factors in an

organization which could enhance the performance of a company? (O'Donovan. 2003).

Governance and remuneration:

This system assists the organization to analyze about various policies and governance

structure of an organization in order to manage and enhance the operations and the

performance of the company?

The above details depict that various concepts, performance, position, Performa,

profitability position etc of the company which focuses over the demands and the corporate

governance of the company. It enhances the organization to maintain and manage the full

picture of structured around, performance and business model, strategic objective of

organization which includes financial and non financial information of the company.

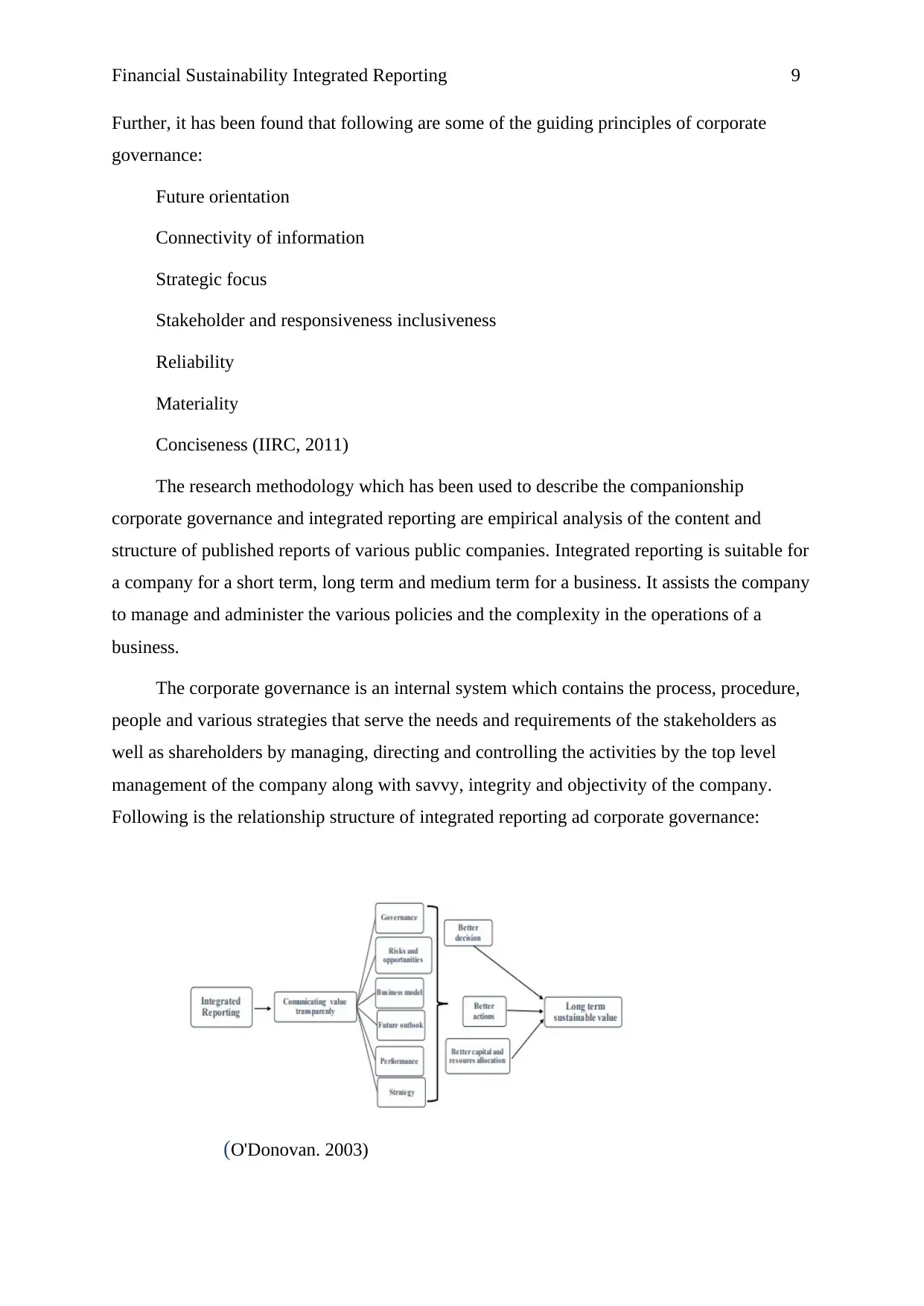

Relationship between integrated reporting and corporate governance:

The companies want to make sustainable values in order to enhance the financial values

and non financial values of the company which is required by the business to manage the

values for stakeholders and for the society to present and offer information to the

stakeholders (IIRC, 2013). Corporate governance is a part of the integrated reports of the

company which is developed by the organization in order to manage and rebuild the faith of

the stakeholders and to manage the feelings of interest of managers in line with owner’s

interest. Basically, the most important principles of the corporate governance are:

Fairness

Responsibility

Transparency

Accountability

The above factors depict that corporate governance mainly stand up over fairness,

transparency, accountability and fairness of the corporation. Accountability is a principle

which emphasize over the responsibility of the business and its impact over the environment.

This system assists the organization to analyze that what are the opportunities,

strategies, threats, challenges, uncertainties and other aspects of the company in order to

manage and enhance the performance of the company?

Performance:

This system assists the organization to analyze that what could be the factors in an

organization which could enhance the performance of a company? (O'Donovan. 2003).

Governance and remuneration:

This system assists the organization to analyze about various policies and governance

structure of an organization in order to manage and enhance the operations and the

performance of the company?

The above details depict that various concepts, performance, position, Performa,

profitability position etc of the company which focuses over the demands and the corporate

governance of the company. It enhances the organization to maintain and manage the full

picture of structured around, performance and business model, strategic objective of

organization which includes financial and non financial information of the company.

Relationship between integrated reporting and corporate governance:

The companies want to make sustainable values in order to enhance the financial values

and non financial values of the company which is required by the business to manage the

values for stakeholders and for the society to present and offer information to the

stakeholders (IIRC, 2013). Corporate governance is a part of the integrated reports of the

company which is developed by the organization in order to manage and rebuild the faith of

the stakeholders and to manage the feelings of interest of managers in line with owner’s

interest. Basically, the most important principles of the corporate governance are:

Fairness

Responsibility

Transparency

Accountability

The above factors depict that corporate governance mainly stand up over fairness,

transparency, accountability and fairness of the corporation. Accountability is a principle

which emphasize over the responsibility of the business and its impact over the environment.

Financial Sustainability Integrated Reporting 9

Further, it has been found that following are some of the guiding principles of corporate

governance:

Future orientation

Connectivity of information

Strategic focus

Stakeholder and responsiveness inclusiveness

Reliability

Materiality

Conciseness (IIRC, 2011)

The research methodology which has been used to describe the companionship

corporate governance and integrated reporting are empirical analysis of the content and

structure of published reports of various public companies. Integrated reporting is suitable for

a company for a short term, long term and medium term for a business. It assists the company

to manage and administer the various policies and the complexity in the operations of a

business.

The corporate governance is an internal system which contains the process, procedure,

people and various strategies that serve the needs and requirements of the stakeholders as

well as shareholders by managing, directing and controlling the activities by the top level

management of the company along with savvy, integrity and objectivity of the company.

Following is the relationship structure of integrated reporting ad corporate governance:

(O'Donovan. 2003)

Further, it has been found that following are some of the guiding principles of corporate

governance:

Future orientation

Connectivity of information

Strategic focus

Stakeholder and responsiveness inclusiveness

Reliability

Materiality

Conciseness (IIRC, 2011)

The research methodology which has been used to describe the companionship

corporate governance and integrated reporting are empirical analysis of the content and

structure of published reports of various public companies. Integrated reporting is suitable for

a company for a short term, long term and medium term for a business. It assists the company

to manage and administer the various policies and the complexity in the operations of a

business.

The corporate governance is an internal system which contains the process, procedure,

people and various strategies that serve the needs and requirements of the stakeholders as

well as shareholders by managing, directing and controlling the activities by the top level

management of the company along with savvy, integrity and objectivity of the company.

Following is the relationship structure of integrated reporting ad corporate governance:

(O'Donovan. 2003)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Sustainability Integrated Reporting 10

Firstly, the concept of integrates reporting is lied over the integrated reporting and

thinking which promotes the internal process for understand the interest and needs of

different stakeholders/ investors. The organizations which assist the integrated documents for

reporting are quite good to communicate the global performance of the company. Further, it

also connects the financial information and non financial information of a company which

includes those factors which focuses towards the future, embedded in integrated reporting

could enhance corporate governance (OECD, 2017).

Further, it has been explained by Admas (2015) that Corporate governance, corporate

reporting, responsibility and integrated reporting are the significant terms which have been

used in an international business to manage the business. Moreover, a study of Daub (2007)

express that the main motive behind enhancing Corporate governance and responsibility and

integrated reporting are the financial crisis and the various problems in the market. Further, it

has been added by Azapagic, (2003) that the enhancement incidence behind integrated

reporting is of accounting scandals and environmental disaster. Further, business concepts are

quite complex and thus it is required for the businesses to manage and maintain the corporate

reporting. The concept of corporate reporting makes it simple for the business to enlarge the

business.

Further, it has also been analyzed that the main focuses of the company is in integrated

reporting as integrated reporting is the main part which offers stakeholders, government and

the management of the company about the full picture of structured around, performance and

business model, strategic objective of organization which includes financial and non financial

information of the company. According to the Eccles, Krzus, Rogers & Serafeim, (2012), an

integrated reporting is the summary of communication about the governance, strategy, policy,

prospects, performance in concern of external environment of the company to lead the value

creation in short term, long term and medium term of the business.

Further, it has been found through the study of Busco (2014) that in ancient times,

financial reporting was quite enough for the companies which are performing their business

in the international market, to manage and analyze the performance and the position in the

market. But now the market has been complex and with the complexity, various problems

have also been enhanced in the market (Cheng et al, 2014). It assists the company to manage

and administer the various policies and the complexity in the operations of a business.

Conclusion:

Firstly, the concept of integrates reporting is lied over the integrated reporting and

thinking which promotes the internal process for understand the interest and needs of

different stakeholders/ investors. The organizations which assist the integrated documents for

reporting are quite good to communicate the global performance of the company. Further, it

also connects the financial information and non financial information of a company which

includes those factors which focuses towards the future, embedded in integrated reporting

could enhance corporate governance (OECD, 2017).

Further, it has been explained by Admas (2015) that Corporate governance, corporate

reporting, responsibility and integrated reporting are the significant terms which have been

used in an international business to manage the business. Moreover, a study of Daub (2007)

express that the main motive behind enhancing Corporate governance and responsibility and

integrated reporting are the financial crisis and the various problems in the market. Further, it

has been added by Azapagic, (2003) that the enhancement incidence behind integrated

reporting is of accounting scandals and environmental disaster. Further, business concepts are

quite complex and thus it is required for the businesses to manage and maintain the corporate

reporting. The concept of corporate reporting makes it simple for the business to enlarge the

business.

Further, it has also been analyzed that the main focuses of the company is in integrated

reporting as integrated reporting is the main part which offers stakeholders, government and

the management of the company about the full picture of structured around, performance and

business model, strategic objective of organization which includes financial and non financial

information of the company. According to the Eccles, Krzus, Rogers & Serafeim, (2012), an

integrated reporting is the summary of communication about the governance, strategy, policy,

prospects, performance in concern of external environment of the company to lead the value

creation in short term, long term and medium term of the business.

Further, it has been found through the study of Busco (2014) that in ancient times,

financial reporting was quite enough for the companies which are performing their business

in the international market, to manage and analyze the performance and the position in the

market. But now the market has been complex and with the complexity, various problems

have also been enhanced in the market (Cheng et al, 2014). It assists the company to manage

and administer the various policies and the complexity in the operations of a business.

Conclusion:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Sustainability Integrated Reporting 11

Through the above study, it has been found that the various changes have taken place

into the position of corporate governance. Because, nowadays many companies, governments

and the stakeholders have already known the significance of social, environmental,

governance information as a huge part of annual report which is needed by the organization.

Integrated reporting and corporate governance is the main part which offers stakeholders,

government and the management of the company about the full picture of structured around,

performance and business model, strategic objective of organization which includes financial

and non financial information of the company. An integrated reporting is the summary of

communication about the governance, strategy, policy, prospects, performance in concern of

external environment of the company to lead the value creation in short term, long term and

medium term of the business.

In ancient times, financial reporting was quite enough for the companies which are

performing their business in the international market, to manage and analyze the performance

and the position in the market. But now the market has been complex and with the

complexity, various problems have also been enhanced in the market. It assists the company

to manage and administer the various policies and the complexity in the operations of a

business. The origin of integrated origin is in corporate governance. It assists the organization

in enhancing the ability of the company in managing the value of the organization in short

term, medium term and long term.

Through the above study, it has been found that the various changes have taken place

into the position of corporate governance. Because, nowadays many companies, governments

and the stakeholders have already known the significance of social, environmental,

governance information as a huge part of annual report which is needed by the organization.

Integrated reporting and corporate governance is the main part which offers stakeholders,

government and the management of the company about the full picture of structured around,

performance and business model, strategic objective of organization which includes financial

and non financial information of the company. An integrated reporting is the summary of

communication about the governance, strategy, policy, prospects, performance in concern of

external environment of the company to lead the value creation in short term, long term and

medium term of the business.

In ancient times, financial reporting was quite enough for the companies which are

performing their business in the international market, to manage and analyze the performance

and the position in the market. But now the market has been complex and with the

complexity, various problems have also been enhanced in the market. It assists the company

to manage and administer the various policies and the complexity in the operations of a

business. The origin of integrated origin is in corporate governance. It assists the organization

in enhancing the ability of the company in managing the value of the organization in short

term, medium term and long term.

Financial Sustainability Integrated Reporting 12

References:

Abeysekera, I. (2013). A template for integrated reporting. Journal of Intellectual

Capital, 14(2), 227-245.

Adams, C. (2015). Understanding integrated reporting: The concise guide to integrated

thinking and the future of corporate reporting. Do Sustainability.

Adams, S., & Simnett, R. (2011). Integrated Reporting: An opportunity for Australia's not‐

for‐profit sector. Australian Accounting Review, 21(3), 292-301.

Azapagic, A. (2003). Systems approach to corporate sustainability: a general management

framework. Process Safety and Environmental Protection, 81(5), 303-316.

Burritt, R. L., Hahn, T., & Schaltegger, S. (2002). Towards a comprehensive framework for

environmental management accounting—Links between business actors and

environmental management accounting tools. Australian Accounting Review, 12(27),

39-50.

Busco, C. A. (2014). Integrated reporting. Springer,.

Cheng, M., Green, W., Conradie, P., Konishi, N., & Romi, A. (2014). The international

integrated reporting framework: key issues and future research opportunities. Journal of

International Financial Management & Accounting, 25(1), 90-119.

Cheng, M., Green, W., Conradie, P., Konishi, N., & Romi, A. (2014). The international

integrated reporting framework: key issues and future research opportunities. Journal of

International Financial Management & Accounting, 25(1), 90-119.

Daub, C. H. (2007). Assessing the quality of sustainability reporting: an alternative

methodological approach. Journal of Cleaner Production, 15(1), 75-85.

de Villiers, C., Rinaldi, L., & Unerman, J. (2014). Integrated Reporting: Insights, gaps and an

agenda for future research. Accounting, Auditing & Accountability Journal, 27(7),

1042-1067.

Dumitru, M., Glavan, M. E., Gorgan, C., & Dumitru, V. F. (2013). International integrated

reporting framework: a case study in the software industry. Annales Universitatis

Apulensis: Series Oeconomica, 15(1), 24.

Eccles, R. G., & Krzus, M. P. (2010). One report: Integrated reporting for a sustainable

strategy. John Wiley & Sons.

References:

Abeysekera, I. (2013). A template for integrated reporting. Journal of Intellectual

Capital, 14(2), 227-245.

Adams, C. (2015). Understanding integrated reporting: The concise guide to integrated

thinking and the future of corporate reporting. Do Sustainability.

Adams, S., & Simnett, R. (2011). Integrated Reporting: An opportunity for Australia's not‐

for‐profit sector. Australian Accounting Review, 21(3), 292-301.

Azapagic, A. (2003). Systems approach to corporate sustainability: a general management

framework. Process Safety and Environmental Protection, 81(5), 303-316.

Burritt, R. L., Hahn, T., & Schaltegger, S. (2002). Towards a comprehensive framework for

environmental management accounting—Links between business actors and

environmental management accounting tools. Australian Accounting Review, 12(27),

39-50.

Busco, C. A. (2014). Integrated reporting. Springer,.

Cheng, M., Green, W., Conradie, P., Konishi, N., & Romi, A. (2014). The international

integrated reporting framework: key issues and future research opportunities. Journal of

International Financial Management & Accounting, 25(1), 90-119.

Cheng, M., Green, W., Conradie, P., Konishi, N., & Romi, A. (2014). The international

integrated reporting framework: key issues and future research opportunities. Journal of

International Financial Management & Accounting, 25(1), 90-119.

Daub, C. H. (2007). Assessing the quality of sustainability reporting: an alternative

methodological approach. Journal of Cleaner Production, 15(1), 75-85.

de Villiers, C., Rinaldi, L., & Unerman, J. (2014). Integrated Reporting: Insights, gaps and an

agenda for future research. Accounting, Auditing & Accountability Journal, 27(7),

1042-1067.

Dumitru, M., Glavan, M. E., Gorgan, C., & Dumitru, V. F. (2013). International integrated

reporting framework: a case study in the software industry. Annales Universitatis

Apulensis: Series Oeconomica, 15(1), 24.

Eccles, R. G., & Krzus, M. P. (2010). One report: Integrated reporting for a sustainable

strategy. John Wiley & Sons.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.