Report on Corporate Governance and Ethics: OECD Framework and Analysis

VerifiedAdded on 2023/01/09

|21

|4677

|100

Report

AI Summary

This report provides a detailed examination of corporate governance and ethics, with a specific focus on the framework and regulatory guidelines established by the Organisation for Economic Co-operation and Development (OECD). The introduction emphasizes the crucial role of corporate governance in business success and the importance of global regulatory bodies like the OECD in maintaining transparency and compliance. The report then offers an overview of the OECD, its objectives, and its organizational structure, highlighting its impact on global economic progress and corporate reporting standards. The core of the report analyzes the OECD's regulatory framework, including key principles such as transparency, accountability, prudence, integrity, monitoring, and risk management. These principles are discussed in the context of real-world events, such as the 2008 financial crisis, to illustrate their practical implications. The report also explores the relationship between corporate governance and corporate social responsibility (CSR), concluding with a summary of the key findings and the importance of adhering to the OECD's guidelines for sustainable business practices.

CORPORATE GOVERNANCE & ETHICS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

1.0 Introduction................................................................................................................................3

2.0 Overview of OECD...................................................................................................................5

3.0 Regulatory Framework under OECD........................................................................................8

3.1 Transparency & Accountability.............................................................................................8

3.2 Prudence & Integrity..............................................................................................................9

3.3 Monitoring and Reporting Operations.................................................................................10

3.4 Maintaining Sufficient Resources........................................................................................10

3.5 Ensuring Adequate Internal Control....................................................................................10

3.6 Risk Management................................................................................................................11

3.7 Sound Corporate Governance..............................................................................................11

3.8 Compliance with FR Rules..................................................................................................11

3.9 Producing Accurate Timely Information.............................................................................12

4.0 Corporate Governance and Corporate Social Responsibility..................................................14

5.0 Conclusion...............................................................................................................................16

References......................................................................................................................................18

Page 2 of 21

1.0 Introduction................................................................................................................................3

2.0 Overview of OECD...................................................................................................................5

3.0 Regulatory Framework under OECD........................................................................................8

3.1 Transparency & Accountability.............................................................................................8

3.2 Prudence & Integrity..............................................................................................................9

3.3 Monitoring and Reporting Operations.................................................................................10

3.4 Maintaining Sufficient Resources........................................................................................10

3.5 Ensuring Adequate Internal Control....................................................................................10

3.6 Risk Management................................................................................................................11

3.7 Sound Corporate Governance..............................................................................................11

3.8 Compliance with FR Rules..................................................................................................11

3.9 Producing Accurate Timely Information.............................................................................12

4.0 Corporate Governance and Corporate Social Responsibility..................................................14

5.0 Conclusion...............................................................................................................................16

References......................................................................................................................................18

Page 2 of 21

1.0 Introduction

Corporate governance may be considered to be one of the most crucial and success-critical

aspects of the business as the implementation of the same involves considerations of lots of

factors that are internal and external to the business (Regling and Watson, 2010). Respective

regulatory authorities in the countries aim to maintain the sound corporate governance

environment within the business affairs for the nation in order to ensure compliance with the

global standards. Also, the global authorities responsible for maintaining the transparency in the

corporate reporting, time to time, release various standards for the purpose of country-specific

regulators to comply with the same and thereby attain the global convergence and comparability

of the financial statements in a most efficient manner. As a result, it may be noted that global

regulators play a critical role in ensuring corporate governance at a macro level.

Organisation for Economic Co-operation and Development (hereinafter may be referred to as

“OECD” or the organisation or the regulator, as the case may be) is such a regulatory body, that

attempts to regulate the business transactions by stimulating economic progress and making the

world trade compliant with the global standards set for the purpose.

There have been cases where the business across the world has faced a setback in spite of strong

regulatory framework existing there at. The financial crisis of the year 2008 is such an example

when it was observed that any organisations failed to comply with the respective standards

pronouncements and thus experienced major fall in their operations in terms of non-compliance

and mismanagement that eventually suffered substantial financial loss as well (Wanyama, Burton

and Helliar, 2017).

Page 3 of 21

Corporate governance may be considered to be one of the most crucial and success-critical

aspects of the business as the implementation of the same involves considerations of lots of

factors that are internal and external to the business (Regling and Watson, 2010). Respective

regulatory authorities in the countries aim to maintain the sound corporate governance

environment within the business affairs for the nation in order to ensure compliance with the

global standards. Also, the global authorities responsible for maintaining the transparency in the

corporate reporting, time to time, release various standards for the purpose of country-specific

regulators to comply with the same and thereby attain the global convergence and comparability

of the financial statements in a most efficient manner. As a result, it may be noted that global

regulators play a critical role in ensuring corporate governance at a macro level.

Organisation for Economic Co-operation and Development (hereinafter may be referred to as

“OECD” or the organisation or the regulator, as the case may be) is such a regulatory body, that

attempts to regulate the business transactions by stimulating economic progress and making the

world trade compliant with the global standards set for the purpose.

There have been cases where the business across the world has faced a setback in spite of strong

regulatory framework existing there at. The financial crisis of the year 2008 is such an example

when it was observed that any organisations failed to comply with the respective standards

pronouncements and thus experienced major fall in their operations in terms of non-compliance

and mismanagement that eventually suffered substantial financial loss as well (Wanyama, Burton

and Helliar, 2017).

Page 3 of 21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In such a context, a need was felt by OECD to have a relook into the existing sets of standards

and benchmark practices in terms of corporate governance and corporate reporting for the

purpose of assessing the need of their revaluation against the changing economic backdrop. After

due consultation with other standard setters across the worlds and brainstorming, OCED released

quite a few publications specifying the exact cause of such failures experienced by the

corporations across the globe and probable remedial measures that could have been adopted at

that particular point of time. The reports have also specified the recommendatory actions that

may need to be adhered by the management of the business going forward in order to comply

with the regulations at a global level (Davies, 2016).

The instant report briefly discusses the implications of those publications and the respective

regulatory framework as advised therein for the organisations to be followed. At the very outset

of the study, the background of the study has been explained in brief followed by the overview of

the OECD and their roles in global corporate reporting and corporate governance. In the main

parts of the paper, the researcher intends to identify the theoretical and regulatory framework that

may emerge out of the critical evaluation and thorough analysis of various publications of OCED

and also the journal articles released on the given topic. Such secondary research has also been

supported by a brief discussion on the concept of corporate governance and corporate social

responsibility (CSR) as well. Finally, the researcher wraps up the discussion by way of

concluding note.

Page 4 of 21

and benchmark practices in terms of corporate governance and corporate reporting for the

purpose of assessing the need of their revaluation against the changing economic backdrop. After

due consultation with other standard setters across the worlds and brainstorming, OCED released

quite a few publications specifying the exact cause of such failures experienced by the

corporations across the globe and probable remedial measures that could have been adopted at

that particular point of time. The reports have also specified the recommendatory actions that

may need to be adhered by the management of the business going forward in order to comply

with the regulations at a global level (Davies, 2016).

The instant report briefly discusses the implications of those publications and the respective

regulatory framework as advised therein for the organisations to be followed. At the very outset

of the study, the background of the study has been explained in brief followed by the overview of

the OECD and their roles in global corporate reporting and corporate governance. In the main

parts of the paper, the researcher intends to identify the theoretical and regulatory framework that

may emerge out of the critical evaluation and thorough analysis of various publications of OCED

and also the journal articles released on the given topic. Such secondary research has also been

supported by a brief discussion on the concept of corporate governance and corporate social

responsibility (CSR) as well. Finally, the researcher wraps up the discussion by way of

concluding note.

Page 4 of 21

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

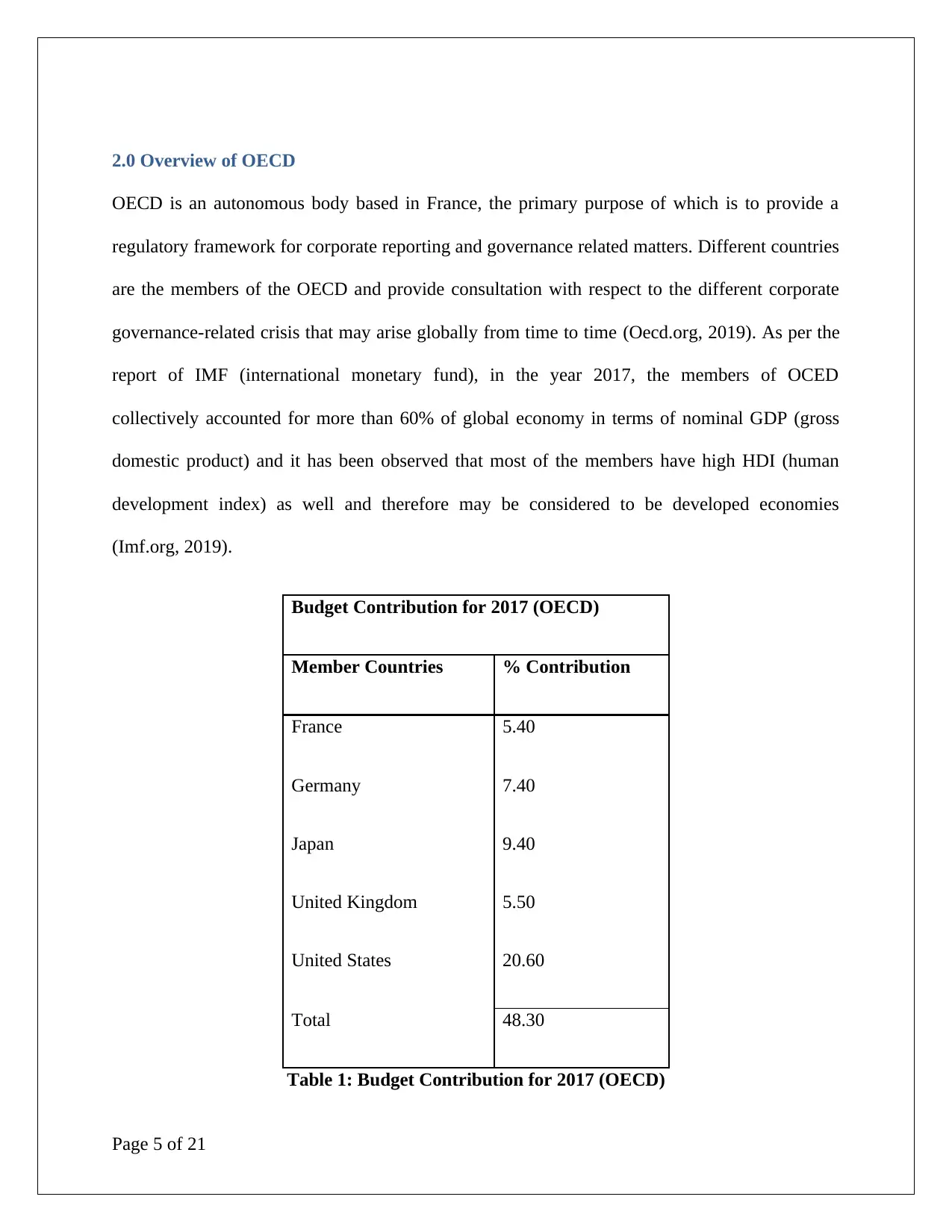

2.0 Overview of OECD

OECD is an autonomous body based in France, the primary purpose of which is to provide a

regulatory framework for corporate reporting and governance related matters. Different countries

are the members of the OECD and provide consultation with respect to the different corporate

governance-related crisis that may arise globally from time to time (Oecd.org, 2019). As per the

report of IMF (international monetary fund), in the year 2017, the members of OCED

collectively accounted for more than 60% of global economy in terms of nominal GDP (gross

domestic product) and it has been observed that most of the members have high HDI (human

development index) as well and therefore may be considered to be developed economies

(Imf.org, 2019).

Budget Contribution for 2017 (OECD)

Member Countries % Contribution

France 5.40

Germany 7.40

Japan 9.40

United Kingdom 5.50

United States 20.60

Total 48.30

Table 1: Budget Contribution for 2017 (OECD)

Page 5 of 21

OECD is an autonomous body based in France, the primary purpose of which is to provide a

regulatory framework for corporate reporting and governance related matters. Different countries

are the members of the OECD and provide consultation with respect to the different corporate

governance-related crisis that may arise globally from time to time (Oecd.org, 2019). As per the

report of IMF (international monetary fund), in the year 2017, the members of OCED

collectively accounted for more than 60% of global economy in terms of nominal GDP (gross

domestic product) and it has been observed that most of the members have high HDI (human

development index) as well and therefore may be considered to be developed economies

(Imf.org, 2019).

Budget Contribution for 2017 (OECD)

Member Countries % Contribution

France 5.40

Germany 7.40

Japan 9.40

United Kingdom 5.50

United States 20.60

Total 48.30

Table 1: Budget Contribution for 2017 (OECD)

Page 5 of 21

(Source: Oecd.org, 2019)

OECD prepares a budget for every year in order to provide its planning, implementation and

financial support to any counties or any issues that may adversely affect the global corporate

governance structure. As per the report of OECD, the 1st part budget for the year 2017 is

approximately Euro 200 million (Oecd.org, 2019). 2nd part of the budget has also been developed

where different participating counties have contributed to the tent of Euro 98 million

approximately (Oecd.org, 2019).

The aims and objectives of OECD are primarily centred on maintaining the compliance

framework with respect to the corporate affairs in respect of corporate governance, taxation,

financial reporting and also sustainability reporting at the global level. Few of the activities that

OECD has undertaken are briefly mentioned below:

On a regular basis, OECD releases publication on various model income tax convention that may

be applied globally addressing some specific international taxation related issues like transfer

pricing and so on,. In this context, it may be noted that OECD has a large number of books and

online materials in their database which is accessible to anyone from member countries (Oecd-

ilibrary.org, 2019). The library contains various publications for various sectors like agriculture,

energy, education, employment, taxation, transport, governance etc. (Oecd-ilibrary.org, 2019).

There is a number of books, journals and working papers available in the database which may be

referred time to time.

The mission statement of OCED indicates that the objective of the organisation is to promote

various policies related to corporate governance that may significantly impact and improve the

Page 6 of 21

OECD prepares a budget for every year in order to provide its planning, implementation and

financial support to any counties or any issues that may adversely affect the global corporate

governance structure. As per the report of OECD, the 1st part budget for the year 2017 is

approximately Euro 200 million (Oecd.org, 2019). 2nd part of the budget has also been developed

where different participating counties have contributed to the tent of Euro 98 million

approximately (Oecd.org, 2019).

The aims and objectives of OECD are primarily centred on maintaining the compliance

framework with respect to the corporate affairs in respect of corporate governance, taxation,

financial reporting and also sustainability reporting at the global level. Few of the activities that

OECD has undertaken are briefly mentioned below:

On a regular basis, OECD releases publication on various model income tax convention that may

be applied globally addressing some specific international taxation related issues like transfer

pricing and so on,. In this context, it may be noted that OECD has a large number of books and

online materials in their database which is accessible to anyone from member countries (Oecd-

ilibrary.org, 2019). The library contains various publications for various sectors like agriculture,

energy, education, employment, taxation, transport, governance etc. (Oecd-ilibrary.org, 2019).

There is a number of books, journals and working papers available in the database which may be

referred time to time.

The mission statement of OCED indicates that the objective of the organisation is to promote

various policies related to corporate governance that may significantly impact and improve the

Page 6 of 21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

economic and social well-being of the people across the globe. The objectives of OCED may be

summarised herein:

o Restoring public confidence in the market and financial institutions

o Re-establishing the public finance framework for the purpose of sustainable economic

development

o Initiating new and innovative growth model that is both environmentally green and also

economically strong in order to foster the development of emerging economies

o Ensuring access to technical education and related skills by the people and thereby

enhancing the employability in order to reduce the unemployment rate throughout the

globe

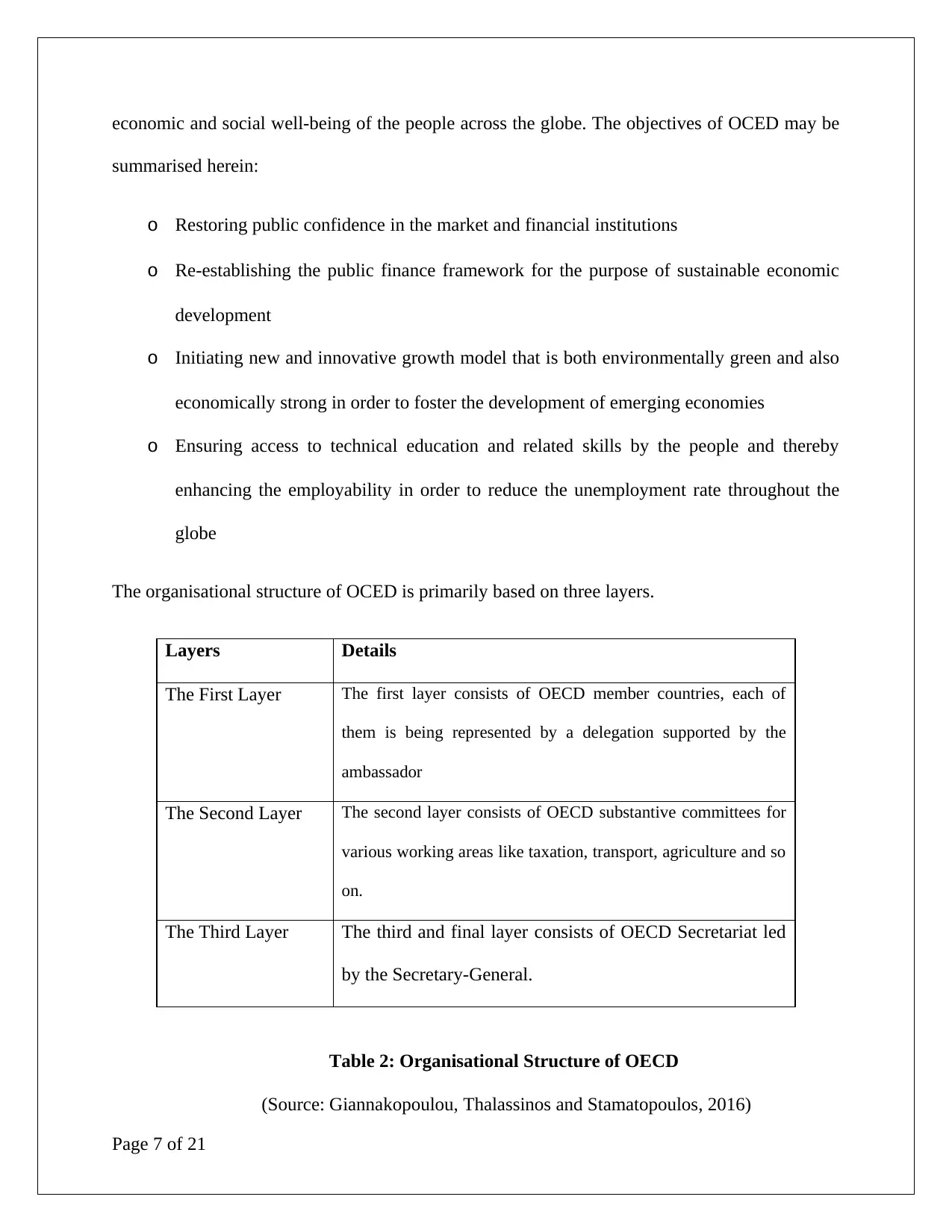

The organisational structure of OCED is primarily based on three layers.

Layers Details

The First Layer The first layer consists of OECD member countries, each of

them is being represented by a delegation supported by the

ambassador

The Second Layer The second layer consists of OECD substantive committees for

various working areas like taxation, transport, agriculture and so

on.

The Third Layer The third and final layer consists of OECD Secretariat led

by the Secretary-General.

Table 2: Organisational Structure of OECD

(Source: Giannakopoulou, Thalassinos and Stamatopoulos, 2016)

Page 7 of 21

summarised herein:

o Restoring public confidence in the market and financial institutions

o Re-establishing the public finance framework for the purpose of sustainable economic

development

o Initiating new and innovative growth model that is both environmentally green and also

economically strong in order to foster the development of emerging economies

o Ensuring access to technical education and related skills by the people and thereby

enhancing the employability in order to reduce the unemployment rate throughout the

globe

The organisational structure of OCED is primarily based on three layers.

Layers Details

The First Layer The first layer consists of OECD member countries, each of

them is being represented by a delegation supported by the

ambassador

The Second Layer The second layer consists of OECD substantive committees for

various working areas like taxation, transport, agriculture and so

on.

The Third Layer The third and final layer consists of OECD Secretariat led

by the Secretary-General.

Table 2: Organisational Structure of OECD

(Source: Giannakopoulou, Thalassinos and Stamatopoulos, 2016)

Page 7 of 21

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3.0 Regulatory Framework under OECD

As stated earlier, there have been various initiatives by OECD that had been implemented in the

past in order to counter with the global issues that may adversely economic development of the

countries. With respect to the acute financial crisis that has emerged in the year 2008, OECD

observed that there were certain regulatory failures as well as administrative and managerial

inefficiencies that could have been avoided and the crisis could have been fought back in a more

efficient manner. The sections below identify some of the key and success-critical areas for the

business and also for the economy as a whole that may have been considered by the stakeholders

in future in order to prevent such crisis (Honoré, Munari and de La Potterie, 2015). It is needless

to mention that these key features or considerations have been referred from the recommendation

and analysis performed by the OECD only in this regard.

3.1 Transparency & Accountability

Transparency refers to the environment in which the data and information are being provided to

the related stakeholders in most comprehensible, accessible in a timely manner (Directorate,

2019).

Accountability, on the other hand, refers to the key concept in managerial accounting theory

which suggests that the managers are responsible for carrying out the stipulated task of managing

the operations in line with the interests of the owner groups and larger stakeholder horizon as a

whole (Directorate, 2019).

The functions of the banking system were not following the transparent approach in terms of

reporting which was a cause of concern for the regulatory bodies (Regling and Watson, 2010).

Page 8 of 21

As stated earlier, there have been various initiatives by OECD that had been implemented in the

past in order to counter with the global issues that may adversely economic development of the

countries. With respect to the acute financial crisis that has emerged in the year 2008, OECD

observed that there were certain regulatory failures as well as administrative and managerial

inefficiencies that could have been avoided and the crisis could have been fought back in a more

efficient manner. The sections below identify some of the key and success-critical areas for the

business and also for the economy as a whole that may have been considered by the stakeholders

in future in order to prevent such crisis (Honoré, Munari and de La Potterie, 2015). It is needless

to mention that these key features or considerations have been referred from the recommendation

and analysis performed by the OECD only in this regard.

3.1 Transparency & Accountability

Transparency refers to the environment in which the data and information are being provided to

the related stakeholders in most comprehensible, accessible in a timely manner (Directorate,

2019).

Accountability, on the other hand, refers to the key concept in managerial accounting theory

which suggests that the managers are responsible for carrying out the stipulated task of managing

the operations in line with the interests of the owner groups and larger stakeholder horizon as a

whole (Directorate, 2019).

The functions of the banking system were not following the transparent approach in terms of

reporting which was a cause of concern for the regulatory bodies (Regling and Watson, 2010).

Page 8 of 21

There had been warnings flagged off in this regard; however, the crisis led to the fall of the

operations in no time.

3.2 Prudence & Integrity

Prudence generally refers to a logical framework in which the business operations will have to be

carried out considering the legality as well as practicality in a combined manner. In this context,

the concept of “substance over form” is worth to mention which states that the convention and

judgment should prevail over the legality and hence there has to be an application of common

sense that may create the corporate reporting more user-friendly for the stakeholders. For

example, the assets taken under the lease are being shown in the balance sheet in spite of the fact

that those assets do not belong to the business and the rights to the title of those assets may

remain in the hands of lessor only.

Integrity refers to the value systems and principles inculcated by the management that may be

reflected in their actions which, in turn, satisfies the interest of users in the agency producing the

given statistics and data. In short, honesty and integrity may be considered to be synonymous

(Directorate, 2019).

In the context of the financial crisis in Ireland in the year 2008, it may be noted that OECD

raised issues relating to the credit risks for greater prudence much earlier. However, the same

was not being adhered to by the banks and financial institutions. It was noted that some of the

banks in the Canadian region were doing fairly good as there was strong prudence in disbursing

the loan to the consumers (Regling and Watson, 2010). The management of such banks exercised

judicial judgments before sanctioning the loans. However, there were some banks also for which

FR raised concerns for their lack of prudence and integrity in the operations.

Page 9 of 21

operations in no time.

3.2 Prudence & Integrity

Prudence generally refers to a logical framework in which the business operations will have to be

carried out considering the legality as well as practicality in a combined manner. In this context,

the concept of “substance over form” is worth to mention which states that the convention and

judgment should prevail over the legality and hence there has to be an application of common

sense that may create the corporate reporting more user-friendly for the stakeholders. For

example, the assets taken under the lease are being shown in the balance sheet in spite of the fact

that those assets do not belong to the business and the rights to the title of those assets may

remain in the hands of lessor only.

Integrity refers to the value systems and principles inculcated by the management that may be

reflected in their actions which, in turn, satisfies the interest of users in the agency producing the

given statistics and data. In short, honesty and integrity may be considered to be synonymous

(Directorate, 2019).

In the context of the financial crisis in Ireland in the year 2008, it may be noted that OECD

raised issues relating to the credit risks for greater prudence much earlier. However, the same

was not being adhered to by the banks and financial institutions. It was noted that some of the

banks in the Canadian region were doing fairly good as there was strong prudence in disbursing

the loan to the consumers (Regling and Watson, 2010). The management of such banks exercised

judicial judgments before sanctioning the loans. However, there were some banks also for which

FR raised concerns for their lack of prudence and integrity in the operations.

Page 9 of 21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3.3 Monitoring and Reporting Operations

The financial crisis in Ireland may also be observed from the viewpoint of monitoring and

reporting practices. The bank supervisors in the country were not being called upon to explain

the lacuna. The regulators, in short, did not pay much attention to the administrative framework

of the country’s banking system.

As per the pronouncements of FR, there were issues with respect to the monitoring and reporting

functions of the bank's operations, The hierarchy followed within the banking operations of

banks were not sufficient enough to allow actions taking and hence the matters so identified went

unnoticed many times.

3.4 Maintaining Sufficient Resources

Resourcing here primary construes the financial resources that the banks were maintaining for

the people. It was argued by many researchers that the banks in Ireland raised funds from the

outside market (primarily European arena) to inject the same into the deficit in the income of

households and corporate ion the domestic field. When the crisis started to merge out of the

borrowers’ inability to repay the loan, the banking system collapsed because of the loan burden

on them (Regling and Watson, 2010).

3.5 Ensuring Adequate Internal Control

As stated earlier also, there was no evidence of internal control of the banks that may be

considered to be the strong enough to identify the possibility of credit risks and thereby mitigate

the risk by way of transferring, rejecting or mitigating the risks. In addition, the lack of internal

control over financial reporting (ICFR) was also clearly evident in the operations and reporting

which further aggravated the concerns of FR and OECD.

Page 10 of 21

The financial crisis in Ireland may also be observed from the viewpoint of monitoring and

reporting practices. The bank supervisors in the country were not being called upon to explain

the lacuna. The regulators, in short, did not pay much attention to the administrative framework

of the country’s banking system.

As per the pronouncements of FR, there were issues with respect to the monitoring and reporting

functions of the bank's operations, The hierarchy followed within the banking operations of

banks were not sufficient enough to allow actions taking and hence the matters so identified went

unnoticed many times.

3.4 Maintaining Sufficient Resources

Resourcing here primary construes the financial resources that the banks were maintaining for

the people. It was argued by many researchers that the banks in Ireland raised funds from the

outside market (primarily European arena) to inject the same into the deficit in the income of

households and corporate ion the domestic field. When the crisis started to merge out of the

borrowers’ inability to repay the loan, the banking system collapsed because of the loan burden

on them (Regling and Watson, 2010).

3.5 Ensuring Adequate Internal Control

As stated earlier also, there was no evidence of internal control of the banks that may be

considered to be the strong enough to identify the possibility of credit risks and thereby mitigate

the risk by way of transferring, rejecting or mitigating the risks. In addition, the lack of internal

control over financial reporting (ICFR) was also clearly evident in the operations and reporting

which further aggravated the concerns of FR and OECD.

Page 10 of 21

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3.6 Risk Management

It is needless to mention that banks may act as risk buffers and shock absorbers in the time of

depression. Due to the funding capability and liquidity position, the banking system may be

regarded as the helping hand for the Government during the turbulent times in the economy.

However, the case of 2008 was radically different for Ireland (Regling and Watson, 2010). The

banks’ intrusiveness towards the risk mitigation strategy (RMS) was considered too lightly, In

addition, it may also be noted that the internal risk management framework of the banks was also

not strong enough in terms of evaluation of creditworthiness of borrowers by way of stress-

testing, credit risk assessment and also the proper loan documentation.

3.7 Sound Corporate Governance

It may be stated that the governance in the banking and financial institutions had been considered

weak in Ireland during 2008 (Nyberg, 2011). The credit risk was not being closely monitored

which accounted for a large amount of accumulated losses for the banks. Concentration on the

lending habits towards the property should have been managed with under the strict rules and

relevant regulatory guidelines as pronounced by the regulators (Regling and Watson, 2010).

However, the same did not happen in reality which further aggravated the deficiencies in the

governance system within the banking institutions (Honohan, 2010).

3.8 Compliance with FR Rules

The expert team of OECD has been formulating several rules regarding suitable financial

regulation (FR). In such a scenario, it is crucial for the business houses to follow the same with

utmost sincerity. It has been observed, especially, during the time of the financial crisis of 2008

in Ireland, that the policies were not being followed strictly. There was lacuna from the

supervision perspective and the compliance in terms of recognition, measurement, disclosure and

Page 11 of 21

It is needless to mention that banks may act as risk buffers and shock absorbers in the time of

depression. Due to the funding capability and liquidity position, the banking system may be

regarded as the helping hand for the Government during the turbulent times in the economy.

However, the case of 2008 was radically different for Ireland (Regling and Watson, 2010). The

banks’ intrusiveness towards the risk mitigation strategy (RMS) was considered too lightly, In

addition, it may also be noted that the internal risk management framework of the banks was also

not strong enough in terms of evaluation of creditworthiness of borrowers by way of stress-

testing, credit risk assessment and also the proper loan documentation.

3.7 Sound Corporate Governance

It may be stated that the governance in the banking and financial institutions had been considered

weak in Ireland during 2008 (Nyberg, 2011). The credit risk was not being closely monitored

which accounted for a large amount of accumulated losses for the banks. Concentration on the

lending habits towards the property should have been managed with under the strict rules and

relevant regulatory guidelines as pronounced by the regulators (Regling and Watson, 2010).

However, the same did not happen in reality which further aggravated the deficiencies in the

governance system within the banking institutions (Honohan, 2010).

3.8 Compliance with FR Rules

The expert team of OECD has been formulating several rules regarding suitable financial

regulation (FR). In such a scenario, it is crucial for the business houses to follow the same with

utmost sincerity. It has been observed, especially, during the time of the financial crisis of 2008

in Ireland, that the policies were not being followed strictly. There was lacuna from the

supervision perspective and the compliance in terms of recognition, measurement, disclosure and

Page 11 of 21

treatment went non-monitored. Such a scenario created a severe crisis in the banking sector of

the country (Nyberg, 2011).

In this context, it may be stated that the financial regulators provided for 9 different principles

that may need to be strictly followed by the banking houses. These nine principles are as listed

below:

Conducting the functions of banks in a transparent and accountable manner. Acting with prudence and integrity Maintaining sufficient financial resources Having a strong corporate governance structure. Having an oversight in the operations Having a strong and effective internal control subsystem in place Maintaining an efficient risk management policies Providing accurate, complete and timely information and Complying with all the FR guidelines as noted herein.

3.9 Producing Accurate Timely Information

Producing accurate information through corporate reporting is extremely important for

management Nyberg, 2011). It has often been observed, and for quite obvious reason, that the

failure on the part of the management to provide accurate and timely information to the

stakeholder may lead to the dissatisfaction among the interest groups (Regling and Watson,

2010). In this context, it may be noted that the management must act as an agent of the owner

groups. In other words, they must execute the operation in their fiduciary capacities and hence

responsibility lies on them only to provide a clear picture about the business, operations, social

Page 12 of 21

the country (Nyberg, 2011).

In this context, it may be stated that the financial regulators provided for 9 different principles

that may need to be strictly followed by the banking houses. These nine principles are as listed

below:

Conducting the functions of banks in a transparent and accountable manner. Acting with prudence and integrity Maintaining sufficient financial resources Having a strong corporate governance structure. Having an oversight in the operations Having a strong and effective internal control subsystem in place Maintaining an efficient risk management policies Providing accurate, complete and timely information and Complying with all the FR guidelines as noted herein.

3.9 Producing Accurate Timely Information

Producing accurate information through corporate reporting is extremely important for

management Nyberg, 2011). It has often been observed, and for quite obvious reason, that the

failure on the part of the management to provide accurate and timely information to the

stakeholder may lead to the dissatisfaction among the interest groups (Regling and Watson,

2010). In this context, it may be noted that the management must act as an agent of the owner

groups. In other words, they must execute the operation in their fiduciary capacities and hence

responsibility lies on them only to provide a clear picture about the business, operations, social

Page 12 of 21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.