Auditing and Compliance: ASX Corporate Governance Principles Analysis

VerifiedAdded on 2021/06/14

|13

|2969

|25

Report

AI Summary

This report provides a comprehensive analysis of auditing and compliance practices, specifically examining the case of AGL, an ASX-listed company. The study begins with an executive summary, followed by a detailed examination of AGL's adherence to the ASX Corporate Governance Principles, evaluating its management structure, board composition, ethical policies, corporate reporting, and shareholder rights. The report further analyzes the risks faced by AGL through financial ratio analysis, including debt-equity, liquidity, and profitability ratios, as well as trend analysis. The assessment also covers AGL's risk management strategies, including its enterprise risk management system and the role of the Audit & Risk Management Committee. The report concludes with an evaluation of AGL's continuous disclosure practices and remuneration policies, providing a holistic view of its corporate governance and compliance framework.

Running head: AUDITING AND COMPLIANCE

Auditing and Compliance

University Name

Student Name

Authors’ Note

Auditing and Compliance

University Name

Student Name

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

AUDITING AND COMPLIANCE

Table of Contents

Executive Summary...................................................................................................................2

ASX Corporate Governance Principles.....................................................................................2

Risk Assessment.........................................................................................................................7

Reference..................................................................................................................................11

AUDITING AND COMPLIANCE

Table of Contents

Executive Summary...................................................................................................................2

ASX Corporate Governance Principles.....................................................................................2

Risk Assessment.........................................................................................................................7

Reference..................................................................................................................................11

3

AUDITING AND COMPLIANCE

Executive Summary

The present study under consideration elucidates in detail the way the formal, methodical and

ordered approach of auditing that can help in understanding effectiveness of procedures and

associated controls. This study also studies compliance necessities that can help in

augmentation of business value. In itself, the primary purpose of the study is to critically

examine scale and extent of conformity of the selected firm AGL to specific dictates of the

corporate governance principles as mentioned by the ASX CGS. Furthermore, the study also

has the intent to examine whether the company under deliberation abides by the rules laid

down by the Corporate Governance Council. Moving further, the current study also analyses

risks faced by the business entity by analysis of financial ratio, analysis of trend and analysis

of the market.

ASX Corporate Governance Principles

The statement of corporate governance of the chosen ASX listed company AGL has made a

commitment to act in accordance with framework, obligations and practices set by the

Council of Corporate Governance of ASX. AGL board of director believes in sustainable

performance. Therefore, they practice the best corporate governance supported by ASX rules.

The structure of the Corporate Governance policy of AGL is as follows:

Enforcing a sturdy and efficient management foundation and oversight:

The management of the AGL includes the boards of directors who are responsible for the

mainlining the various interest of the company and its stakeholders (Craneand, Matten2016).

The corporate governance of the company is also maintained by them. The board of directors

AUDITING AND COMPLIANCE

Executive Summary

The present study under consideration elucidates in detail the way the formal, methodical and

ordered approach of auditing that can help in understanding effectiveness of procedures and

associated controls. This study also studies compliance necessities that can help in

augmentation of business value. In itself, the primary purpose of the study is to critically

examine scale and extent of conformity of the selected firm AGL to specific dictates of the

corporate governance principles as mentioned by the ASX CGS. Furthermore, the study also

has the intent to examine whether the company under deliberation abides by the rules laid

down by the Corporate Governance Council. Moving further, the current study also analyses

risks faced by the business entity by analysis of financial ratio, analysis of trend and analysis

of the market.

ASX Corporate Governance Principles

The statement of corporate governance of the chosen ASX listed company AGL has made a

commitment to act in accordance with framework, obligations and practices set by the

Council of Corporate Governance of ASX. AGL board of director believes in sustainable

performance. Therefore, they practice the best corporate governance supported by ASX rules.

The structure of the Corporate Governance policy of AGL is as follows:

Enforcing a sturdy and efficient management foundation and oversight:

The management of the AGL includes the boards of directors who are responsible for the

mainlining the various interest of the company and its stakeholders (Craneand, Matten2016).

The corporate governance of the company is also maintained by them. The board of directors

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

AUDITING AND COMPLIANCE

has the duty of approving and supervising the company’s strategies along with its

performance. They also set the budget plan as well recruits the CEO of the company.

Development of a proper Director board for enriching its value:

The integrated energy business AGL has a sound composition and structure of the board that

consists of the audit and the risk committee, nomination committee, people and performance

committee and a committee for sustainability, safety and corporate social responsibility

(Masonand Simmons 2014). Each of the committee performs their assigned duty along with

sound coordination in order to achieve the organizational goal. The number of directors and

their operations are determined in the annual meetings that are set in the Directors attendance

mentioned in the Annual report.

Morals and ethical policies of the organization

As per the statement of sustainability re approved by the ASX committee, the AGL maintains

a sound code of conduct thatis applicable to its stakeholders that includes the directors,

contractors and the employees engaged in its operations. The code is a collection of the

ethical conduct and a standard of responsibility for its members who are related to the

company (Bowie 2017). According to the code thereare a setof rules abide by them that

induces the members to act with integrity and honesty along with maintaining a sound

professionalism in their operations (William Jr et al. 2016). In addition to that they set the

internal standards, commitments and the various laws along with maintaining confidentiality

in their operations

Protection of the honour of the company by sound corporate reporting

The various financial report of the organization is maintained and regulated by the Board of

directors. The committee of audit and risk management takes care of the financial statements

AUDITING AND COMPLIANCE

has the duty of approving and supervising the company’s strategies along with its

performance. They also set the budget plan as well recruits the CEO of the company.

Development of a proper Director board for enriching its value:

The integrated energy business AGL has a sound composition and structure of the board that

consists of the audit and the risk committee, nomination committee, people and performance

committee and a committee for sustainability, safety and corporate social responsibility

(Masonand Simmons 2014). Each of the committee performs their assigned duty along with

sound coordination in order to achieve the organizational goal. The number of directors and

their operations are determined in the annual meetings that are set in the Directors attendance

mentioned in the Annual report.

Morals and ethical policies of the organization

As per the statement of sustainability re approved by the ASX committee, the AGL maintains

a sound code of conduct thatis applicable to its stakeholders that includes the directors,

contractors and the employees engaged in its operations. The code is a collection of the

ethical conduct and a standard of responsibility for its members who are related to the

company (Bowie 2017). According to the code thereare a setof rules abide by them that

induces the members to act with integrity and honesty along with maintaining a sound

professionalism in their operations (William Jr et al. 2016). In addition to that they set the

internal standards, commitments and the various laws along with maintaining confidentiality

in their operations

Protection of the honour of the company by sound corporate reporting

The various financial report of the organization is maintained and regulated by the Board of

directors. The committee of audit and risk management takes care of the financial statements

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

AUDITING AND COMPLIANCE

and the reporting practices (Shimeld, Williamsand Shimeld2017).They also provide

confirmation that these opinions have been formed on the basis of a sound system of risk

management and internal control, which is operating effectively. Before the Board approves

the financial statements for a financial period, the CEO and CFO provide declarations to the

Board that, in their opinion, the financial records of AGL have been properly maintained and

that the financial statements comply with the Accounting Standards and give a true and fair

view of the financial position and performance of AGL.

Preserve integrity in particularly corporate reporting

Analysis of the corporate governance statement aptly illustrates corporate governance

structure, strategies along with practices. During the entire period of financial year 2017, the

Corporate Governance arrangements of AGL are in agreement with Corporate Governance

Principles along with recommendations (referring to 3 rd Edition) of principles laid down by

Australian Stock Exchange. This is published by the Corporate Governance Council of ASX

that helps in providing a checklist for cross referring to the principles of ASX to the pertinent

disclosures. AGL’s code of conduct can be referred to as vital factor of the firm that can aid

in attaining excellence and securing complete financial soundness, societies as well as

businesses. Management of the corporation follows the values of maintaining integrity,

higher merit, and accountability along with maintaining alliance (William Jr et al. 2016). The

recommendations mentioned in the Corporate Governance Regulations states that Listing

rules along with directives of Corporation Act introduced in the year 2001 helps in the

understanding the fact that administration has devised several controls for maintaining

integrity of system of reporting. The financial assertions of the firm are also prepared as per

the accounting standards leading to presentation of true along with fair view of financial

information. Disclosures are also presented as per recommendations stipulated under ASX

AUDITING AND COMPLIANCE

and the reporting practices (Shimeld, Williamsand Shimeld2017).They also provide

confirmation that these opinions have been formed on the basis of a sound system of risk

management and internal control, which is operating effectively. Before the Board approves

the financial statements for a financial period, the CEO and CFO provide declarations to the

Board that, in their opinion, the financial records of AGL have been properly maintained and

that the financial statements comply with the Accounting Standards and give a true and fair

view of the financial position and performance of AGL.

Preserve integrity in particularly corporate reporting

Analysis of the corporate governance statement aptly illustrates corporate governance

structure, strategies along with practices. During the entire period of financial year 2017, the

Corporate Governance arrangements of AGL are in agreement with Corporate Governance

Principles along with recommendations (referring to 3 rd Edition) of principles laid down by

Australian Stock Exchange. This is published by the Corporate Governance Council of ASX

that helps in providing a checklist for cross referring to the principles of ASX to the pertinent

disclosures. AGL’s code of conduct can be referred to as vital factor of the firm that can aid

in attaining excellence and securing complete financial soundness, societies as well as

businesses. Management of the corporation follows the values of maintaining integrity,

higher merit, and accountability along with maintaining alliance (William Jr et al. 2016). The

recommendations mentioned in the Corporate Governance Regulations states that Listing

rules along with directives of Corporation Act introduced in the year 2001 helps in the

understanding the fact that administration has devised several controls for maintaining

integrity of system of reporting. The financial assertions of the firm are also prepared as per

the accounting standards leading to presentation of true along with fair view of financial

information. Disclosures are also presented as per recommendations stipulated under ASX

6

AUDITING AND COMPLIANCE

CGS. This in turn can help in preservation of reliability as well as veracity of system of

reporting pecuniary matters (Messier et al. 2014).

Carry out well timed and at the same time balanced disclosure

AGL has a continuous disclosure principle in place. AGL has a External Communication

Policy that elucidates about the continuous disclosure necessities of the company. The board

of the firm AGL intends to make certain that all the shareholders along with the market are

fully informed regarding all credible information along with price sensitive advance along

with alterations that can probably affect overall operations, financial outcomes along with

business prospects. The continuous disclosure necessities can help in making certain that all

the requisite information is divulged to the entire market in a well timed as well as effective

manner (Vasarhelyi et al. 2018). This is done by means of internal system of reporting along

with monitoring procedure of standard information. The company AGL presents periodic

reporting that delivers financial statements prepared by the firm to the shareholders as well as

other interested parties. In addition to this, the company delivers important functional in

addition to different financial performance indicators to the users of information.

Respect security holders’ rights

The board intends to safeguard and shield interests and at the same time promote sustainable

value creation whilst taking into consideration rational shareholder’s interests (Leung et al.

2014). The board of the company has the intention to approve significant pronouncements

made by AGL to particularly ASX as well as other reports to the firm’s shareholders as per

suggestions of Corporation Act as well as other pertinent regulations (Leung et al. 2014). The

chairperson of the company AGL preside board meetings along with shareholder’s meetings.

Thus, in this specific manner, the company can provide material information to shareholders.

AUDITING AND COMPLIANCE

CGS. This in turn can help in preservation of reliability as well as veracity of system of

reporting pecuniary matters (Messier et al. 2014).

Carry out well timed and at the same time balanced disclosure

AGL has a continuous disclosure principle in place. AGL has a External Communication

Policy that elucidates about the continuous disclosure necessities of the company. The board

of the firm AGL intends to make certain that all the shareholders along with the market are

fully informed regarding all credible information along with price sensitive advance along

with alterations that can probably affect overall operations, financial outcomes along with

business prospects. The continuous disclosure necessities can help in making certain that all

the requisite information is divulged to the entire market in a well timed as well as effective

manner (Vasarhelyi et al. 2018). This is done by means of internal system of reporting along

with monitoring procedure of standard information. The company AGL presents periodic

reporting that delivers financial statements prepared by the firm to the shareholders as well as

other interested parties. In addition to this, the company delivers important functional in

addition to different financial performance indicators to the users of information.

Respect security holders’ rights

The board intends to safeguard and shield interests and at the same time promote sustainable

value creation whilst taking into consideration rational shareholder’s interests (Leung et al.

2014). The board of the company has the intention to approve significant pronouncements

made by AGL to particularly ASX as well as other reports to the firm’s shareholders as per

suggestions of Corporation Act as well as other pertinent regulations (Leung et al. 2014). The

chairperson of the company AGL preside board meetings along with shareholder’s meetings.

Thus, in this specific manner, the company can provide material information to shareholders.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

AUDITING AND COMPLIANCE

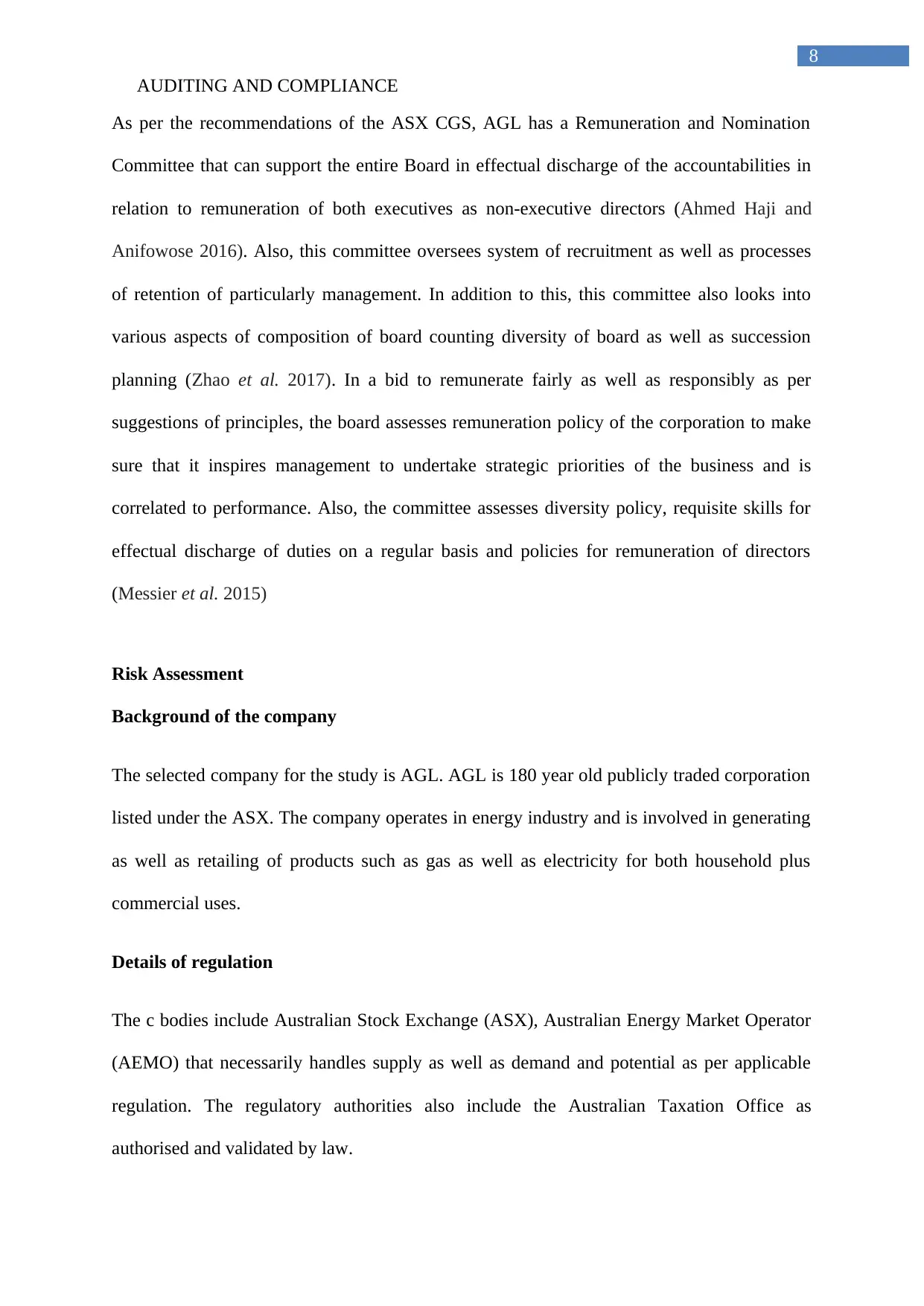

Detect and manage risk

In connection to risk management, the board of the firm AGL assesses and at the same time

recommends Risk Appetite Statement along with various material strategic risks (Simpson et

al. 2016). In addition to this, the study also reviews and tracks execution of various policies

along with procedures for detecting, evaluating, tracking as well as handling risks. In addition

to this, AGL’s board also presents Audit & Risk Management Committee (also referred to as

ARMC). Board of the company also presents risk management structure and there is a risk

management model in place in the company (Zhou et al. 2016). Essentially, AGL encounters

various types of risks owing to nature as well as characteristics of operations. Management of

the firm is necessarily committed towards appropriate risk management. The “Audit,

Compliance and Risk Committee” aids the firm’s board in effectual discharge of

accountabilities in relation to financial affairs counting treasury risks as well as practices,

monitoring of business risks (Hiltz and Pierce 2018). This committee also aids the board in

detection of main financial along with compliance risks encountered by the firm and assesses

the steps for implementation of specific control and processes for mitigating risks (Arens et

al. 2015).

The company has an Enterprise Risk Management system and a framework for control that

includes different controls that include the following:

Remunerate fairly as well as responsibly

AUDITING AND COMPLIANCE

Detect and manage risk

In connection to risk management, the board of the firm AGL assesses and at the same time

recommends Risk Appetite Statement along with various material strategic risks (Simpson et

al. 2016). In addition to this, the study also reviews and tracks execution of various policies

along with procedures for detecting, evaluating, tracking as well as handling risks. In addition

to this, AGL’s board also presents Audit & Risk Management Committee (also referred to as

ARMC). Board of the company also presents risk management structure and there is a risk

management model in place in the company (Zhou et al. 2016). Essentially, AGL encounters

various types of risks owing to nature as well as characteristics of operations. Management of

the firm is necessarily committed towards appropriate risk management. The “Audit,

Compliance and Risk Committee” aids the firm’s board in effectual discharge of

accountabilities in relation to financial affairs counting treasury risks as well as practices,

monitoring of business risks (Hiltz and Pierce 2018). This committee also aids the board in

detection of main financial along with compliance risks encountered by the firm and assesses

the steps for implementation of specific control and processes for mitigating risks (Arens et

al. 2015).

The company has an Enterprise Risk Management system and a framework for control that

includes different controls that include the following:

Remunerate fairly as well as responsibly

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

AUDITING AND COMPLIANCE

As per the recommendations of the ASX CGS, AGL has a Remuneration and Nomination

Committee that can support the entire Board in effectual discharge of the accountabilities in

relation to remuneration of both executives as non-executive directors (Ahmed Haji and

Anifowose 2016). Also, this committee oversees system of recruitment as well as processes

of retention of particularly management. In addition to this, this committee also looks into

various aspects of composition of board counting diversity of board as well as succession

planning (Zhao et al. 2017). In a bid to remunerate fairly as well as responsibly as per

suggestions of principles, the board assesses remuneration policy of the corporation to make

sure that it inspires management to undertake strategic priorities of the business and is

correlated to performance. Also, the committee assesses diversity policy, requisite skills for

effectual discharge of duties on a regular basis and policies for remuneration of directors

(Messier et al. 2015)

Risk Assessment

Background of the company

The selected company for the study is AGL. AGL is 180 year old publicly traded corporation

listed under the ASX. The company operates in energy industry and is involved in generating

as well as retailing of products such as gas as well as electricity for both household plus

commercial uses.

Details of regulation

The c bodies include Australian Stock Exchange (ASX), Australian Energy Market Operator

(AEMO) that necessarily handles supply as well as demand and potential as per applicable

regulation. The regulatory authorities also include the Australian Taxation Office as

authorised and validated by law.

AUDITING AND COMPLIANCE

As per the recommendations of the ASX CGS, AGL has a Remuneration and Nomination

Committee that can support the entire Board in effectual discharge of the accountabilities in

relation to remuneration of both executives as non-executive directors (Ahmed Haji and

Anifowose 2016). Also, this committee oversees system of recruitment as well as processes

of retention of particularly management. In addition to this, this committee also looks into

various aspects of composition of board counting diversity of board as well as succession

planning (Zhao et al. 2017). In a bid to remunerate fairly as well as responsibly as per

suggestions of principles, the board assesses remuneration policy of the corporation to make

sure that it inspires management to undertake strategic priorities of the business and is

correlated to performance. Also, the committee assesses diversity policy, requisite skills for

effectual discharge of duties on a regular basis and policies for remuneration of directors

(Messier et al. 2015)

Risk Assessment

Background of the company

The selected company for the study is AGL. AGL is 180 year old publicly traded corporation

listed under the ASX. The company operates in energy industry and is involved in generating

as well as retailing of products such as gas as well as electricity for both household plus

commercial uses.

Details of regulation

The c bodies include Australian Stock Exchange (ASX), Australian Energy Market Operator

(AEMO) that necessarily handles supply as well as demand and potential as per applicable

regulation. The regulatory authorities also include the Australian Taxation Office as

authorised and validated by law.

9

AUDITING AND COMPLIANCE

Overview of the market in which AGL operates

The company AGL has a market share of approximately 90%. This company deals in power

as well as energy generation and at the same time retailing of the same for over and above

150 years. AGL is primarily driven by two different strategic essentials that include intention

to develop in a carbon controlled future and to develop customer support with evolving

expectations of customers .

Business Stratagems of the company AGL include

- Sustainable usage of company resources:

- Investment for better generation, storage and sharing of energy

-Development of advanced technologies for maintenance of low levels of emissions

and framing sustainable practices (Cohen and Simnett 2014)

Analysis of risk using key financial ratio and trend analysis: (refer to appendix for

calculations)

- Debt equity ratio calculated for the firm AGL stands at 0.90. A ratio greater than 1

essentially reflects high leverage and greater burden of interest on the part of the firm.

Therefore, AGL is said to be at a favourable financial condition in terms of leverage

(Griffiths 2016).

-The liquidity ratios namely (in this case, current ratio and the quick ratio) of the firm AGL is

registered to be around 1.32 and roughly 1.19 respectively. Standard current ratio is observed

to be 2:1 (Almamy et al. 2016). Therefore, the company has a lower current ratio indicating

poor liquidity condition of the firm. In addition to this, the firm has low quick ratio as well,

AUDITING AND COMPLIANCE

Overview of the market in which AGL operates

The company AGL has a market share of approximately 90%. This company deals in power

as well as energy generation and at the same time retailing of the same for over and above

150 years. AGL is primarily driven by two different strategic essentials that include intention

to develop in a carbon controlled future and to develop customer support with evolving

expectations of customers .

Business Stratagems of the company AGL include

- Sustainable usage of company resources:

- Investment for better generation, storage and sharing of energy

-Development of advanced technologies for maintenance of low levels of emissions

and framing sustainable practices (Cohen and Simnett 2014)

Analysis of risk using key financial ratio and trend analysis: (refer to appendix for

calculations)

- Debt equity ratio calculated for the firm AGL stands at 0.90. A ratio greater than 1

essentially reflects high leverage and greater burden of interest on the part of the firm.

Therefore, AGL is said to be at a favourable financial condition in terms of leverage

(Griffiths 2016).

-The liquidity ratios namely (in this case, current ratio and the quick ratio) of the firm AGL is

registered to be around 1.32 and roughly 1.19 respectively. Standard current ratio is observed

to be 2:1 (Almamy et al. 2016). Therefore, the company has a lower current ratio indicating

poor liquidity condition of the firm. In addition to this, the firm has low quick ratio as well,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

AUDITING AND COMPLIANCE

reflecting lower potential of the firm to repay short term obligations using quick assets

(Chambers and Odar 2015)

-Return on firm’s shareholder’s equity is registered to be 7.12%, while operating margin

stands at 6.07 % and net profit margin of AGL stands at 4.28%. Although the return on equity

shows a favourable condition, both the profit margin ratio does not signify efficiency on the

part of the firm AGL to acquire higher returns (Hines et al. 2015)

-Again, analysis of trend reveals that the firm has an upward moving trajectory in terms of

revenue, while assets of the firm has declined during the financial year 2017 as compared to

the year ago period. On the other hand, liability of the firm has increased during the said

period. Again, equity has also declined by 4.65% during FY 2017 in comparison (Omar et al.

2014)

Audit Steps to mitigate the risks:

-Reviewing current ratio, checking register for cash and reconciling the same with bank

statement

-Receivables can be substantiated with days permitted for disbursement, probability of bad

debt

-Debt document can be checked for comprehending sources of finances of the firm and

attempt to lessen payment obligations for debt

-In a bid to increase profit, expenses can be minimised and all vouchers linked to expends can

be verified

AUDITING AND COMPLIANCE

reflecting lower potential of the firm to repay short term obligations using quick assets

(Chambers and Odar 2015)

-Return on firm’s shareholder’s equity is registered to be 7.12%, while operating margin

stands at 6.07 % and net profit margin of AGL stands at 4.28%. Although the return on equity

shows a favourable condition, both the profit margin ratio does not signify efficiency on the

part of the firm AGL to acquire higher returns (Hines et al. 2015)

-Again, analysis of trend reveals that the firm has an upward moving trajectory in terms of

revenue, while assets of the firm has declined during the financial year 2017 as compared to

the year ago period. On the other hand, liability of the firm has increased during the said

period. Again, equity has also declined by 4.65% during FY 2017 in comparison (Omar et al.

2014)

Audit Steps to mitigate the risks:

-Reviewing current ratio, checking register for cash and reconciling the same with bank

statement

-Receivables can be substantiated with days permitted for disbursement, probability of bad

debt

-Debt document can be checked for comprehending sources of finances of the firm and

attempt to lessen payment obligations for debt

-In a bid to increase profit, expenses can be minimised and all vouchers linked to expends can

be verified

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

AUDITING AND COMPLIANCE

Reference

Ahmed Haji, A. and Anifowose, M., 2016. Audit committee and integrated reporting

practice: does internal assurance matter?. Managerial Auditing Journal, 31(8/9), pp.915-948.

Almamy, J., Aston, J. and Ngwa, L.N., 2016. An evaluation of Altman's Z-score using cash

flow ratio to predict corporate failure amid the recent financial crisis: Evidence from the

UK. Journal of Corporate Finance, 36, pp.278-285.

Arens, A.A., Elder, R.J., Beasley, M.S. and Jones, J., 2015. Auditing: The Art and Science of

Assurance Engagements. Pearson Canada.

Chambers, A.D. and Odar, M., 2015. A new vision for internal audit. Managerial Auditing

Journal, 30(1), pp.34-55.

Cohen, J.R. and Simnett, R., 2014. CSR and assurance services: A research agenda. Auditing:

A Journal of Practice & Theory, 34(1), pp.59-74.

Griffiths, P., 2016. Risk-based auditing. Routledge.

Hiltz, A. and Pierce, S., 2018. Quality assurance program for a nuclear pharmacy. The

Canadian journal of hospital pharmacy, 44(1).

Hines, C.S., Masli, A., Mauldin, E.G. and Peters, G.F., 2015. Board risk committees and

audit pricing. Auditing: A Journal of Practice & Theory, 34(4), pp.59-84.

Leung, P., Coram, P., Cooper, B.J. and Richardson, P., 2014. Modern Auditing and

Assurance Services 6e. Wiley.

Messier, W.F., Glover, S.M. and Prawitt, D.F., 2014. Jasa audit dan assurance: pendekatan

sistematis. Jakarta: Sa-lemba Empat.

AUDITING AND COMPLIANCE

Reference

Ahmed Haji, A. and Anifowose, M., 2016. Audit committee and integrated reporting

practice: does internal assurance matter?. Managerial Auditing Journal, 31(8/9), pp.915-948.

Almamy, J., Aston, J. and Ngwa, L.N., 2016. An evaluation of Altman's Z-score using cash

flow ratio to predict corporate failure amid the recent financial crisis: Evidence from the

UK. Journal of Corporate Finance, 36, pp.278-285.

Arens, A.A., Elder, R.J., Beasley, M.S. and Jones, J., 2015. Auditing: The Art and Science of

Assurance Engagements. Pearson Canada.

Chambers, A.D. and Odar, M., 2015. A new vision for internal audit. Managerial Auditing

Journal, 30(1), pp.34-55.

Cohen, J.R. and Simnett, R., 2014. CSR and assurance services: A research agenda. Auditing:

A Journal of Practice & Theory, 34(1), pp.59-74.

Griffiths, P., 2016. Risk-based auditing. Routledge.

Hiltz, A. and Pierce, S., 2018. Quality assurance program for a nuclear pharmacy. The

Canadian journal of hospital pharmacy, 44(1).

Hines, C.S., Masli, A., Mauldin, E.G. and Peters, G.F., 2015. Board risk committees and

audit pricing. Auditing: A Journal of Practice & Theory, 34(4), pp.59-84.

Leung, P., Coram, P., Cooper, B.J. and Richardson, P., 2014. Modern Auditing and

Assurance Services 6e. Wiley.

Messier, W.F., Glover, S.M. and Prawitt, D.F., 2014. Jasa audit dan assurance: pendekatan

sistematis. Jakarta: Sa-lemba Empat.

12

AUDITING AND COMPLIANCE

Messier, W.F., Glover, S.M. and Prawitt, D.F., 2015. Auditing & Assurance Services: A

Systematic Approach. Qing hua da xue chu ban she.

Omar, N., Koya, R.K., Sanusi, Z.M. and Shafie, N.A., 2014. Financial statement fraud: A

case examination using Beneish Model and ratio analysis. International Journal of Trade,

Economics and Finance, 5(2), p.184.

Simpson, S.N.Y., Aboagye-Otchere, F. and Lovi, R., 2016. Internal auditing and assurance of

corporate social responsibility reports and disclosures: perspectives of some internal auditors

in Ghana. Social Responsibility Journal, 12(4), pp.706-718.

Vasarhelyi, M.A., Alles, M.G. and Kogan, A., 2018. Principles of analytic monitoring for

continuous assurance. In Continuous Auditing: Theory and Application (pp. 191-217).

Emerald Publishing Limited.

William Jr, M., Glover, S. and Prawitt, D., 2016. Auditing and assurance services: A

systematic approach. McGraw-Hill Education.

Zhao, M., Vaartjes, I., Klipstein-Grobusch, K., Kotseva, K., Jennings, C., Grobbee, D.E. and

Graham, I., 2017. Quality assurance and the need to evaluate interventions and audit

programme outcomes. European journal of preventive cardiology, 24(3_suppl), pp.123-128.

Zhou, S., Simnett, R. and Hoang, H., 2016. Combined assurance as a new assurance

approach: is it beneficial to analysts. In 26th Audit and Assurance conference-Thursday 5

May 2016.

AUDITING AND COMPLIANCE

Messier, W.F., Glover, S.M. and Prawitt, D.F., 2015. Auditing & Assurance Services: A

Systematic Approach. Qing hua da xue chu ban she.

Omar, N., Koya, R.K., Sanusi, Z.M. and Shafie, N.A., 2014. Financial statement fraud: A

case examination using Beneish Model and ratio analysis. International Journal of Trade,

Economics and Finance, 5(2), p.184.

Simpson, S.N.Y., Aboagye-Otchere, F. and Lovi, R., 2016. Internal auditing and assurance of

corporate social responsibility reports and disclosures: perspectives of some internal auditors

in Ghana. Social Responsibility Journal, 12(4), pp.706-718.

Vasarhelyi, M.A., Alles, M.G. and Kogan, A., 2018. Principles of analytic monitoring for

continuous assurance. In Continuous Auditing: Theory and Application (pp. 191-217).

Emerald Publishing Limited.

William Jr, M., Glover, S. and Prawitt, D., 2016. Auditing and assurance services: A

systematic approach. McGraw-Hill Education.

Zhao, M., Vaartjes, I., Klipstein-Grobusch, K., Kotseva, K., Jennings, C., Grobbee, D.E. and

Graham, I., 2017. Quality assurance and the need to evaluate interventions and audit

programme outcomes. European journal of preventive cardiology, 24(3_suppl), pp.123-128.

Zhou, S., Simnett, R. and Hoang, H., 2016. Combined assurance as a new assurance

approach: is it beneficial to analysts. In 26th Audit and Assurance conference-Thursday 5

May 2016.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.