Report: Analysis of Malaysian Code of Corporate Governance 2017

VerifiedAdded on 2020/06/04

|9

|2187

|86

Report

AI Summary

This report provides a comprehensive analysis of the Malaysian Code of Corporate Governance (MCCG) 2017. It begins by outlining the ancillary and core concepts of the code, including board leadership, integrity in reporting, stakeholder relationships, and risk management. The report then identifies emerging issues in corporate governance, such as risk oversight, corporate strategy, executive compensation, and transparency. Furthermore, it analyzes the theoretical frameworks of corporate governance, specifically the agency theory and stakeholder theory, and discusses how these theories strive towards the same goals of improved business operations. The report concludes by emphasizing the importance of corporate governance in managing businesses and providing stakeholders with relevant information regarding revenue, investment policies, and returns.

Corporate Governance

(Malaysian Code 2017)

(Malaysian Code 2017)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

1 Ascertaining the ancillary and core concepts of Malaysian Code of Corporate Governance..1

2 Determining the area of issues on emerging the corporate governance...................................3

3 Analysing the following theoretical framework of Corporate governance..............................4

4 Agency Theory and Stakeholder theory striving towards the same goals...............................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION...........................................................................................................................1

1 Ascertaining the ancillary and core concepts of Malaysian Code of Corporate Governance..1

2 Determining the area of issues on emerging the corporate governance...................................3

3 Analysing the following theoretical framework of Corporate governance..............................4

4 Agency Theory and Stakeholder theory striving towards the same goals...............................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION

To illustrate the business operations with the help of appropriate structure and process of

directing, managing and controlling the activities there is need to have adequate corporate

governance. Therefore, with consideration of such operations the business will have appropriate

knowledge, guidance and capital structure with the influence of talented and skilled leaders and

managers who will manage the work and present the adequate solution to any corporate issues.

In the present report there will be discussion based on Malaysian Code of Corporate Governance.

The report will help in making the appropriate analysis over the framework of MCCG with

analysing its role in facilitating the adequate services to the stakeholders.

1 Ascertaining the ancillary and core concepts of Malaysian Code of Corporate Governance

The Malaysian Code or Corporate Governance was issues to reform the previously

existed code. Thus, the motive of government to introduce such corporate governance practice is

to facilitate the adequate framework and enhances their role towards meeting the satisfactory

level of stakeholders. Thus, the main role of governance is to execute the job and duties

performed in an organisation as well as which are need to be recorded clearly. In addition,

MCCG reflects the global principles and internationally accepted practices of corporate

governance which is consisted of statute and regulations which where published by Bursa

Malaysia. Therefore, these are the rules which are applicable to all the public listed companies

with the common practices (Chin, Tang & Ahmad, 2017). However, there are basically three

principles which are meant to be obtained and followed by and industry such as Board leadership

and effectiveness, Integrity in reporting and managing the stakeholder relationship as well as

making the accurate audit of the company's accounts and risk management.

However, in relation with the core concepts of the MCCG there are several points which

were highlighted in the new code such as:

Increasing the independence of the board members:

In relation with the previous code of practice there was not appropriate independence and

rights were assigned to the board members. Therefore, there were not able to design th

framework of the entity as well as make the necessary decision for enhancing the capital

gathering of the firm (Ibrahim, Arif & Paino, 2017). However, the new reform brings them the

1

To illustrate the business operations with the help of appropriate structure and process of

directing, managing and controlling the activities there is need to have adequate corporate

governance. Therefore, with consideration of such operations the business will have appropriate

knowledge, guidance and capital structure with the influence of talented and skilled leaders and

managers who will manage the work and present the adequate solution to any corporate issues.

In the present report there will be discussion based on Malaysian Code of Corporate Governance.

The report will help in making the appropriate analysis over the framework of MCCG with

analysing its role in facilitating the adequate services to the stakeholders.

1 Ascertaining the ancillary and core concepts of Malaysian Code of Corporate Governance

The Malaysian Code or Corporate Governance was issues to reform the previously

existed code. Thus, the motive of government to introduce such corporate governance practice is

to facilitate the adequate framework and enhances their role towards meeting the satisfactory

level of stakeholders. Thus, the main role of governance is to execute the job and duties

performed in an organisation as well as which are need to be recorded clearly. In addition,

MCCG reflects the global principles and internationally accepted practices of corporate

governance which is consisted of statute and regulations which where published by Bursa

Malaysia. Therefore, these are the rules which are applicable to all the public listed companies

with the common practices (Chin, Tang & Ahmad, 2017). However, there are basically three

principles which are meant to be obtained and followed by and industry such as Board leadership

and effectiveness, Integrity in reporting and managing the stakeholder relationship as well as

making the accurate audit of the company's accounts and risk management.

However, in relation with the core concepts of the MCCG there are several points which

were highlighted in the new code such as:

Increasing the independence of the board members:

In relation with the previous code of practice there was not appropriate independence and

rights were assigned to the board members. Therefore, there were not able to design th

framework of the entity as well as make the necessary decision for enhancing the capital

gathering of the firm (Ibrahim, Arif & Paino, 2017). However, the new reform brings them the

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ability to make changes in the dividend policies, equity share distribution and better allocation of

the capital resources in the different departments of the organisation.

Reformed voting process:

In relation with developing the better industrial control there has been serious changes

were made in relation with the corporate voting process. However, there is introduction of the 2-

tier voting process which will be based on retaining the adequate directors or leader of the

company (Mohamad-Yusof, Wickramasinghe & Zaman, 2018). However, in the first tier the

votes are to be given by the shareholders of the firm and in the second tier the votes will be given

by other stakeholders of the firm. In addition to these the entity organises the voting to have a

leader or director for executing the business operations as well as making the favourable decision

which will favours the organisation in terms of attaining the adequate goals.

Diversity:

In relation with these reforms in the corporate governance it has been placed there are

need to have 30% of the women employees in the board members as well as the senior managing

posts (Shamsudin, Abdullah & Osman, 2018). Thereof, this will be helpful in promoting the

women empowerment as well as securing the women rights in the corporate practices.

Transparency:

It has been mentioned in the amendments the is need to have transparency in the personal

and professionals income gains by the directors in the firm (The Malaysian Code on Corporate

Governance 2017, 2017). Therefore, an appropriate and accurate disclosure will be helpful in

terms of retaining the faith of the stakeholders as well as they will be loyal and trustworthy to the

entity.

managing Audit committee:

The directors, accounting professionals are committed towards making the adequate

disclosure of the firm's financial statements on the periodical basis (Krishnan & Amin, 2017). In

addition, it can be said that the members and internal stakeholders need to have proper access

towards the operations of the firm and must present the favourable presentation of the data set.

Better risk management:

2

the capital resources in the different departments of the organisation.

Reformed voting process:

In relation with developing the better industrial control there has been serious changes

were made in relation with the corporate voting process. However, there is introduction of the 2-

tier voting process which will be based on retaining the adequate directors or leader of the

company (Mohamad-Yusof, Wickramasinghe & Zaman, 2018). However, in the first tier the

votes are to be given by the shareholders of the firm and in the second tier the votes will be given

by other stakeholders of the firm. In addition to these the entity organises the voting to have a

leader or director for executing the business operations as well as making the favourable decision

which will favours the organisation in terms of attaining the adequate goals.

Diversity:

In relation with these reforms in the corporate governance it has been placed there are

need to have 30% of the women employees in the board members as well as the senior managing

posts (Shamsudin, Abdullah & Osman, 2018). Thereof, this will be helpful in promoting the

women empowerment as well as securing the women rights in the corporate practices.

Transparency:

It has been mentioned in the amendments the is need to have transparency in the personal

and professionals income gains by the directors in the firm (The Malaysian Code on Corporate

Governance 2017, 2017). Therefore, an appropriate and accurate disclosure will be helpful in

terms of retaining the faith of the stakeholders as well as they will be loyal and trustworthy to the

entity.

managing Audit committee:

The directors, accounting professionals are committed towards making the adequate

disclosure of the firm's financial statements on the periodical basis (Krishnan & Amin, 2017). In

addition, it can be said that the members and internal stakeholders need to have proper access

towards the operations of the firm and must present the favourable presentation of the data set.

Better risk management:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The code also state that the company need to have a risk management team which must

be consisted of board members and leaders which are committed towards designing the policies

and procedure of the business activities (Hussain & Hadi, 2018).

General meetings:

A company need to organise annual meet or a general meeting which has the influence of

all the directors, managers and members of committees together. There will be discussion based

on the performance of organisation through the year as well as the discussion over new policies

must be made (Chin, Tang & Ahmad, 2017). It will be helpful to the entity in terms of gaining

the adequate information regarding various issues and innovative ideas by the professionals.

2 Determining the area of issues on emerging the corporate governance

Her, in the operational practices of the business entity there is need to analyse various

area which are need to be improved by the professionals such as:

Risk Oversight:

In relation with the confidential data and the operational practices of the firm there is

need to have proper business structure which will be helpful in analysing the priorities, agenda,

informational requirements of the firm (Ibrahim, Arif & Paino, 2017). Thus, such data re

essential to be analysed and managed by the professionals in context with having proper risk

control.

Corporate Strategy:

It will be and serious issues in the operational aspects of the business that a firm must

have better corporate strategy which will enable the management and board members in

developing better plans (Mohamad-Yusof, Wickramasinghe & Zaman, 2018). It will be relevant

with designing the costs structure, expansion planing, allocation of the funds, designing the

shareholder policies etc.

Executive Compensation:

In accordance with enhancing the shareholders value on the long term basis there is need

to have appropriate pay packages for the directors, managers and relevant stakeholders of the

3

be consisted of board members and leaders which are committed towards designing the policies

and procedure of the business activities (Hussain & Hadi, 2018).

General meetings:

A company need to organise annual meet or a general meeting which has the influence of

all the directors, managers and members of committees together. There will be discussion based

on the performance of organisation through the year as well as the discussion over new policies

must be made (Chin, Tang & Ahmad, 2017). It will be helpful to the entity in terms of gaining

the adequate information regarding various issues and innovative ideas by the professionals.

2 Determining the area of issues on emerging the corporate governance

Her, in the operational practices of the business entity there is need to analyse various

area which are need to be improved by the professionals such as:

Risk Oversight:

In relation with the confidential data and the operational practices of the firm there is

need to have proper business structure which will be helpful in analysing the priorities, agenda,

informational requirements of the firm (Ibrahim, Arif & Paino, 2017). Thus, such data re

essential to be analysed and managed by the professionals in context with having proper risk

control.

Corporate Strategy:

It will be and serious issues in the operational aspects of the business that a firm must

have better corporate strategy which will enable the management and board members in

developing better plans (Mohamad-Yusof, Wickramasinghe & Zaman, 2018). It will be relevant

with designing the costs structure, expansion planing, allocation of the funds, designing the

shareholder policies etc.

Executive Compensation:

In accordance with enhancing the shareholders value on the long term basis there is need

to have appropriate pay packages for the directors, managers and relevant stakeholders of the

3

firm (Key Areas of Concern in Corporate Governance, 2009). However, it can be said that, a

satisfactory level pay scale will lead board members in terms of having the better independence.

Transparency:

To fetch the maximum attention and favourable numbers of stakeholders to the firm there

is need to have accuracy in the business transactions. Therefore, it can be through determining

the equal pay scale and disclosure of the organisational turnover and the revenue generated by

the directors in a period (Shamsudin, Abdullah & Osman, 2018). Thus, such information will

help in gaining the adequate support and faith from the stakeholders of the firm.

3 Analysing the following theoretical framework of Corporate governance

In accordance with determining the framework of corporate governance there is need to

analyse the bias theories of the same.

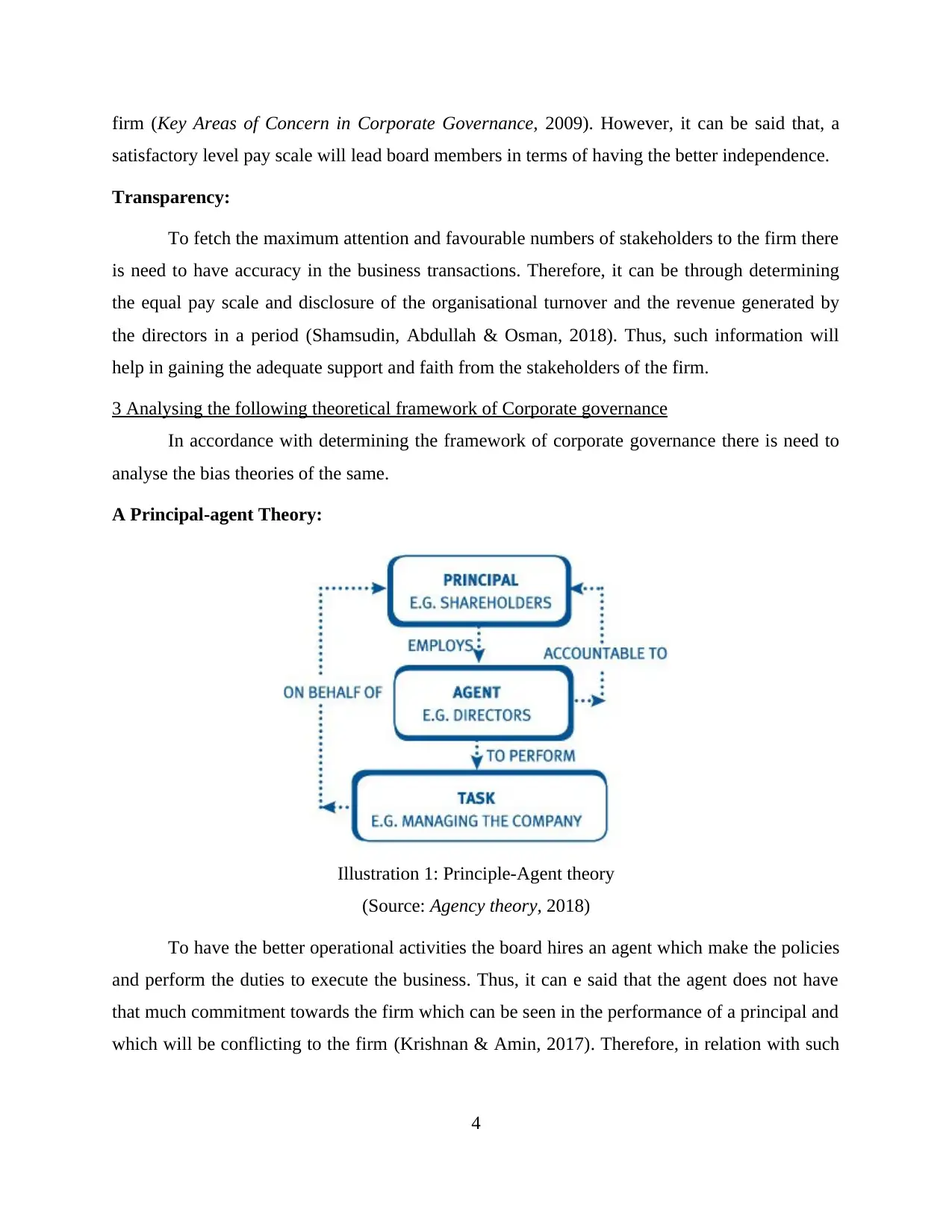

A Principal-agent Theory:

Illustration 1: Principle-Agent theory

(Source: Agency theory, 2018)

To have the better operational activities the board hires an agent which make the policies

and perform the duties to execute the business. Thus, it can e said that the agent does not have

that much commitment towards the firm which can be seen in the performance of a principal and

which will be conflicting to the firm (Krishnan & Amin, 2017). Therefore, in relation with such

4

satisfactory level pay scale will lead board members in terms of having the better independence.

Transparency:

To fetch the maximum attention and favourable numbers of stakeholders to the firm there

is need to have accuracy in the business transactions. Therefore, it can be through determining

the equal pay scale and disclosure of the organisational turnover and the revenue generated by

the directors in a period (Shamsudin, Abdullah & Osman, 2018). Thus, such information will

help in gaining the adequate support and faith from the stakeholders of the firm.

3 Analysing the following theoretical framework of Corporate governance

In accordance with determining the framework of corporate governance there is need to

analyse the bias theories of the same.

A Principal-agent Theory:

Illustration 1: Principle-Agent theory

(Source: Agency theory, 2018)

To have the better operational activities the board hires an agent which make the policies

and perform the duties to execute the business. Thus, it can e said that the agent does not have

that much commitment towards the firm which can be seen in the performance of a principal and

which will be conflicting to the firm (Krishnan & Amin, 2017). Therefore, in relation with such

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

issues it has been ascertained that the board will have the access to analyse the job performed by

the agent and they can have rights to monitor, supervise and execute their duties.

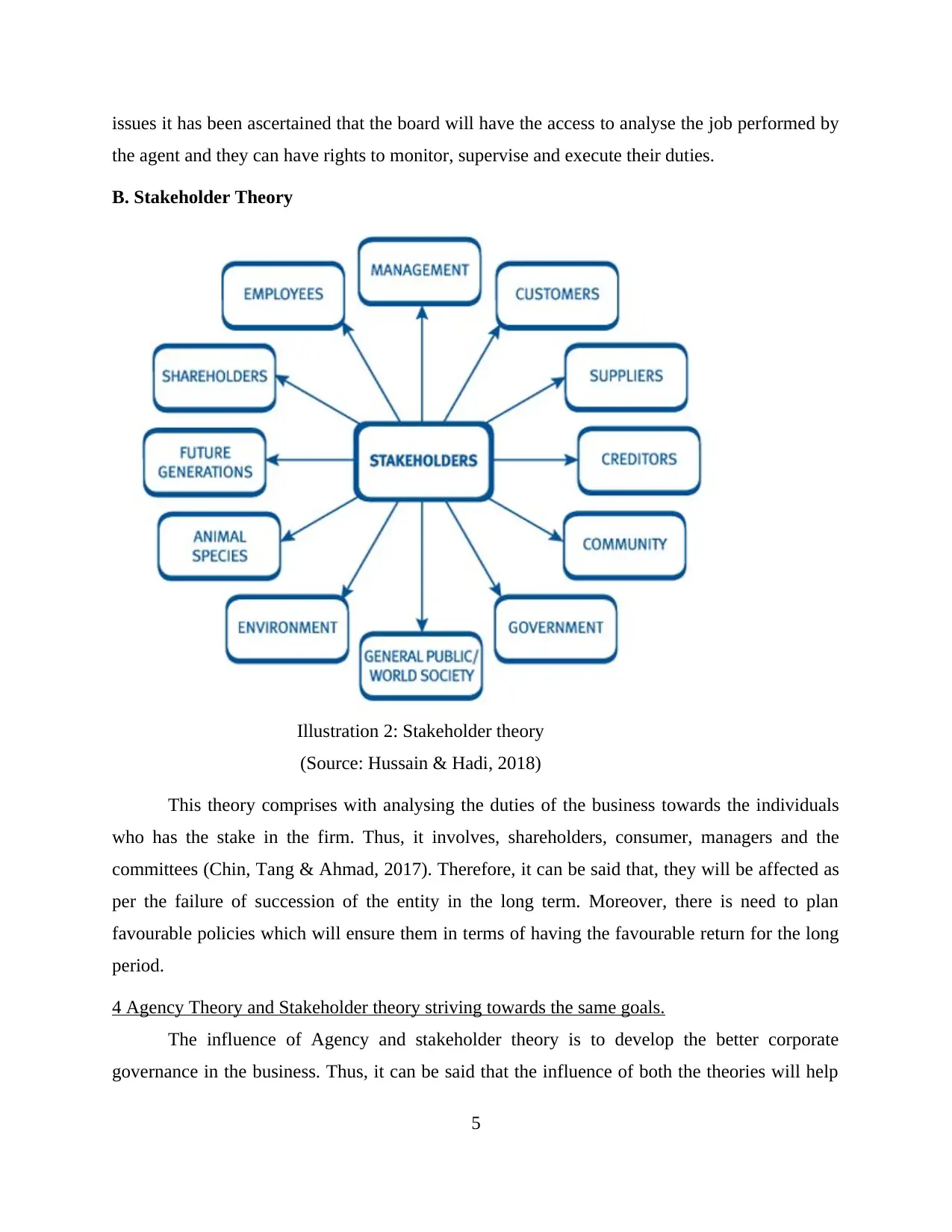

B. Stakeholder Theory

Illustration 2: Stakeholder theory

(Source: Hussain & Hadi, 2018)

This theory comprises with analysing the duties of the business towards the individuals

who has the stake in the firm. Thus, it involves, shareholders, consumer, managers and the

committees (Chin, Tang & Ahmad, 2017). Therefore, it can be said that, they will be affected as

per the failure of succession of the entity in the long term. Moreover, there is need to plan

favourable policies which will ensure them in terms of having the favourable return for the long

period.

4 Agency Theory and Stakeholder theory striving towards the same goals.

The influence of Agency and stakeholder theory is to develop the better corporate

governance in the business. Thus, it can be said that the influence of both the theories will help

5

the agent and they can have rights to monitor, supervise and execute their duties.

B. Stakeholder Theory

Illustration 2: Stakeholder theory

(Source: Hussain & Hadi, 2018)

This theory comprises with analysing the duties of the business towards the individuals

who has the stake in the firm. Thus, it involves, shareholders, consumer, managers and the

committees (Chin, Tang & Ahmad, 2017). Therefore, it can be said that, they will be affected as

per the failure of succession of the entity in the long term. Moreover, there is need to plan

favourable policies which will ensure them in terms of having the favourable return for the long

period.

4 Agency Theory and Stakeholder theory striving towards the same goals.

The influence of Agency and stakeholder theory is to develop the better corporate

governance in the business. Thus, it can be said that the influence of both the theories will help

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the professionals in analysing their roles and responsibilities towards attaining the goals of the

business (Ibrahim, Arif & Paino, 2017). The agency theory is consisted of facilitating the

operational information of the firm to the rest of the members and have debate over planing the

strategies as well as operations which are need to be performed. The stakeholder theory will

benefit the business to present better policies and make disclosure of the gains of the firm.

CONCLUSION

On the basis of above report it can be said that, it is essential to have the influence of the

corporate governance to manage business as well as analysing the necessities of the firm. The

report consist of all the major components which are need to be addressed by the professional of

the firm to give the better information to the stakeholder relevant with the revenue, investment

policies and the return on their investment in the business.

6

business (Ibrahim, Arif & Paino, 2017). The agency theory is consisted of facilitating the

operational information of the firm to the rest of the members and have debate over planing the

strategies as well as operations which are need to be performed. The stakeholder theory will

benefit the business to present better policies and make disclosure of the gains of the firm.

CONCLUSION

On the basis of above report it can be said that, it is essential to have the influence of the

corporate governance to manage business as well as analysing the necessities of the firm. The

report consist of all the major components which are need to be addressed by the professional of

the firm to give the better information to the stakeholder relevant with the revenue, investment

policies and the return on their investment in the business.

6

REFERENCES

Books and Journals

Chin, S. F., Tang, K. B., & Ahmad, A. C. (2017). Financial restatement and firm performance in

family controlled and CEO duality companies: evidence from post 2007 Malaysian Code

of Corporate Governance. In SHS Web of Conferences (Vol. 34). EDP Sciences.

Hussain, M. A., & Hadi, A. R. A. (2018). Corporate Governance, Small Medium Enterprises

(SMEs) and Firm’s Performance: Evidence from Construction Business, Construction

Industry Development Board (CIDB) Malaysia. International Journal of Business and

Management. 13(2). 14.

Ibrahim, S. N. S., Arif, H. M., & Paino, H. (2017). The Relationship between Corporate

Governance Disclosures and Balance Sheet Ratios. Gading Journal for the Social

Sciences. 11(02). 33-40.

Krishnan, S., & Amin, A. M. M. (2017). Empirical Study of Corporate Governance on Public

Listed Companies in Malaysia. Human Resource Management Research. 7(1). 17-27.

Mohamad-Yusof, N. Z., Wickramasinghe, D., & Zaman, M. (2018). Corporate governance,

critical junctures and ethnic politics: Ownership and boards in Malaysia. Critical

Perspectives on Accounting.

Shamsudin, S. M., Abdullah, W. R. W., & Osman, A. H. (2018). Corporate Governance

Practices and Firm Performance After Revised Code of Corporate Governance: Evidence

from Malaysia. In State-of-the-Art Theories and Empirical Evidence (pp. 49-63). Springer,

Singapore.

Online

The Malaysian Code on Corporate Governance 2017. 2017. [Online]. Available

through :<https://www.christopherleeong.com/media/2803/clo-2017-05-the-malaysian-

code-onf.pdf>.

Key Areas of Concern in Corporate Governance. 2009. [Online]. Available through

:<https://erm.ncsu.edu/library/article/key-concerns-governance>.

Agency theory. 2018. [Online]. Available through

:<http://kfknowledgebank.kaplan.co.uk/KFKB/Wiki%20Pages/Agency%20theory.aspx>.

7

Books and Journals

Chin, S. F., Tang, K. B., & Ahmad, A. C. (2017). Financial restatement and firm performance in

family controlled and CEO duality companies: evidence from post 2007 Malaysian Code

of Corporate Governance. In SHS Web of Conferences (Vol. 34). EDP Sciences.

Hussain, M. A., & Hadi, A. R. A. (2018). Corporate Governance, Small Medium Enterprises

(SMEs) and Firm’s Performance: Evidence from Construction Business, Construction

Industry Development Board (CIDB) Malaysia. International Journal of Business and

Management. 13(2). 14.

Ibrahim, S. N. S., Arif, H. M., & Paino, H. (2017). The Relationship between Corporate

Governance Disclosures and Balance Sheet Ratios. Gading Journal for the Social

Sciences. 11(02). 33-40.

Krishnan, S., & Amin, A. M. M. (2017). Empirical Study of Corporate Governance on Public

Listed Companies in Malaysia. Human Resource Management Research. 7(1). 17-27.

Mohamad-Yusof, N. Z., Wickramasinghe, D., & Zaman, M. (2018). Corporate governance,

critical junctures and ethnic politics: Ownership and boards in Malaysia. Critical

Perspectives on Accounting.

Shamsudin, S. M., Abdullah, W. R. W., & Osman, A. H. (2018). Corporate Governance

Practices and Firm Performance After Revised Code of Corporate Governance: Evidence

from Malaysia. In State-of-the-Art Theories and Empirical Evidence (pp. 49-63). Springer,

Singapore.

Online

The Malaysian Code on Corporate Governance 2017. 2017. [Online]. Available

through :<https://www.christopherleeong.com/media/2803/clo-2017-05-the-malaysian-

code-onf.pdf>.

Key Areas of Concern in Corporate Governance. 2009. [Online]. Available through

:<https://erm.ncsu.edu/library/article/key-concerns-governance>.

Agency theory. 2018. [Online]. Available through

:<http://kfknowledgebank.kaplan.co.uk/KFKB/Wiki%20Pages/Agency%20theory.aspx>.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.