BUS80017: SEM and OLS Regression Analysis of Corporate Governance

VerifiedAdded on 2023/06/10

|22

|4286

|175

Report

AI Summary

This report replicates and expands upon Mohammed Azim's 2012 study on corporate governance mechanisms and their impact on company performance, utilizing Structural Equation Modelling (SEM) and Ordinary Least Squares (OLS) Regression. The study aims to validate Azim's theories and determine the nature of corporate monitoring mechanisms, including shareholders, external auditors, and the executive board. Using data from 613 Australian companies in 2015, obtained from SIRCA and Morning Star DatAnalysis, the analysis explores the substitution and complementary effects among monitoring structures. The report includes descriptive statistics and correlation analysis, addressing assumptions made during the data analysis process, such as data normality and the absence of missing values, to ensure the originality of the data analysis. The findings provide insights into the relationships between corporate governance practices and firm performance within the Australian context.

1. Introduction

1.1 Background to study

Corporate governance entails advocacy for law compliance as well as ethical conduct

demonstration (Datta, 2018), which, is in order to ensure that the company is well

aligned to both the society’s ethical concerns and existing regulations for both

profitability and sustainability prospects. Over the recent years, business performance

has been associated with a number of factors apart from the number of consumers for

their products. Such factors include corporate governance. Beth (2003) in her article

on corporate governance and firm performance notes that “the belief that governance

best practices lead to superior firm performance is widespread” a notion which Beth

refutes to not always be true. A number of studies to examine whether governance

best practices are reflected in the performance of the company have been conducted,

including Azim (2012) study on “Corporate governance mechanisms

and their impact on company performance”

1.2 Purpose of study

The purpose of our study is to replicate the studies data analysis and output done by

Mohammed Azim on “Corporate governance mechanisms and their impact on

company performance: A structural equation model analysis” Azim (2012) using

Structural equation modelling and Ordinary Least Squares (OLS) Regression. Our

focus will be to prove the theories presented by Azim (2012). Additionally, the study

seeks to determine the nature of corporate monitoring mechanisms also addressed as

structures in this study. The mechanisms include:

i. Shareholders

ii. External auditors

iii. Executive board

1.1 Background to study

Corporate governance entails advocacy for law compliance as well as ethical conduct

demonstration (Datta, 2018), which, is in order to ensure that the company is well

aligned to both the society’s ethical concerns and existing regulations for both

profitability and sustainability prospects. Over the recent years, business performance

has been associated with a number of factors apart from the number of consumers for

their products. Such factors include corporate governance. Beth (2003) in her article

on corporate governance and firm performance notes that “the belief that governance

best practices lead to superior firm performance is widespread” a notion which Beth

refutes to not always be true. A number of studies to examine whether governance

best practices are reflected in the performance of the company have been conducted,

including Azim (2012) study on “Corporate governance mechanisms

and their impact on company performance”

1.2 Purpose of study

The purpose of our study is to replicate the studies data analysis and output done by

Mohammed Azim on “Corporate governance mechanisms and their impact on

company performance: A structural equation model analysis” Azim (2012) using

Structural equation modelling and Ordinary Least Squares (OLS) Regression. Our

focus will be to prove the theories presented by Azim (2012). Additionally, the study

seeks to determine the nature of corporate monitoring mechanisms also addressed as

structures in this study. The mechanisms include:

i. Shareholders

ii. External auditors

iii. Executive board

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.3 Research questions

The research questions for our study are as those used in the original study by Azim.

i. Is there a substitution effect in the corporate monitoring structures? (Azim, 2012)

ii. Is there a complementary effect among the featured monitoring mechanisms?

(Azim, 2012)

1.4 Keywords

Structural equation modelling, Ordinary Least Squares regression, Corporate

governance, Stakeholders

The research questions for our study are as those used in the original study by Azim.

i. Is there a substitution effect in the corporate monitoring structures? (Azim, 2012)

ii. Is there a complementary effect among the featured monitoring mechanisms?

(Azim, 2012)

1.4 Keywords

Structural equation modelling, Ordinary Least Squares regression, Corporate

governance, Stakeholders

2. Methodology

2.1 Data

The sample data used for this study was obtained from SIRCA and Morning Star

DatAnalysis for 613 Australia’s big companies for the financial year of 2015. It

contains details of shareholders’ activities as well as different monitoring bodies such

as auditors. The data has 9 variables with various levels for the 613 companies, hence

the total number of variables is 22.

2.2 Assumptions

During our study we made the following assumptions:

i. The data for the study is normally distributed

ii. In order to ensure originality of data analysis we assumed that were no missing

values in the data-set and therefore did not explore for missing data, impute or

reconstruct

iii. We also assumed that the sample data was representative enough for estimation

of the population distribution as well as sufficient for testing of hypotheses

iv. The dependent and mediating variables for the SEM are continuous

v. The residuals from a SEM analysis are univariate normally distributed

2.1 Data

The sample data used for this study was obtained from SIRCA and Morning Star

DatAnalysis for 613 Australia’s big companies for the financial year of 2015. It

contains details of shareholders’ activities as well as different monitoring bodies such

as auditors. The data has 9 variables with various levels for the 613 companies, hence

the total number of variables is 22.

2.2 Assumptions

During our study we made the following assumptions:

i. The data for the study is normally distributed

ii. In order to ensure originality of data analysis we assumed that were no missing

values in the data-set and therefore did not explore for missing data, impute or

reconstruct

iii. We also assumed that the sample data was representative enough for estimation

of the population distribution as well as sufficient for testing of hypotheses

iv. The dependent and mediating variables for the SEM are continuous

v. The residuals from a SEM analysis are univariate normally distributed

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3. Analysis Results

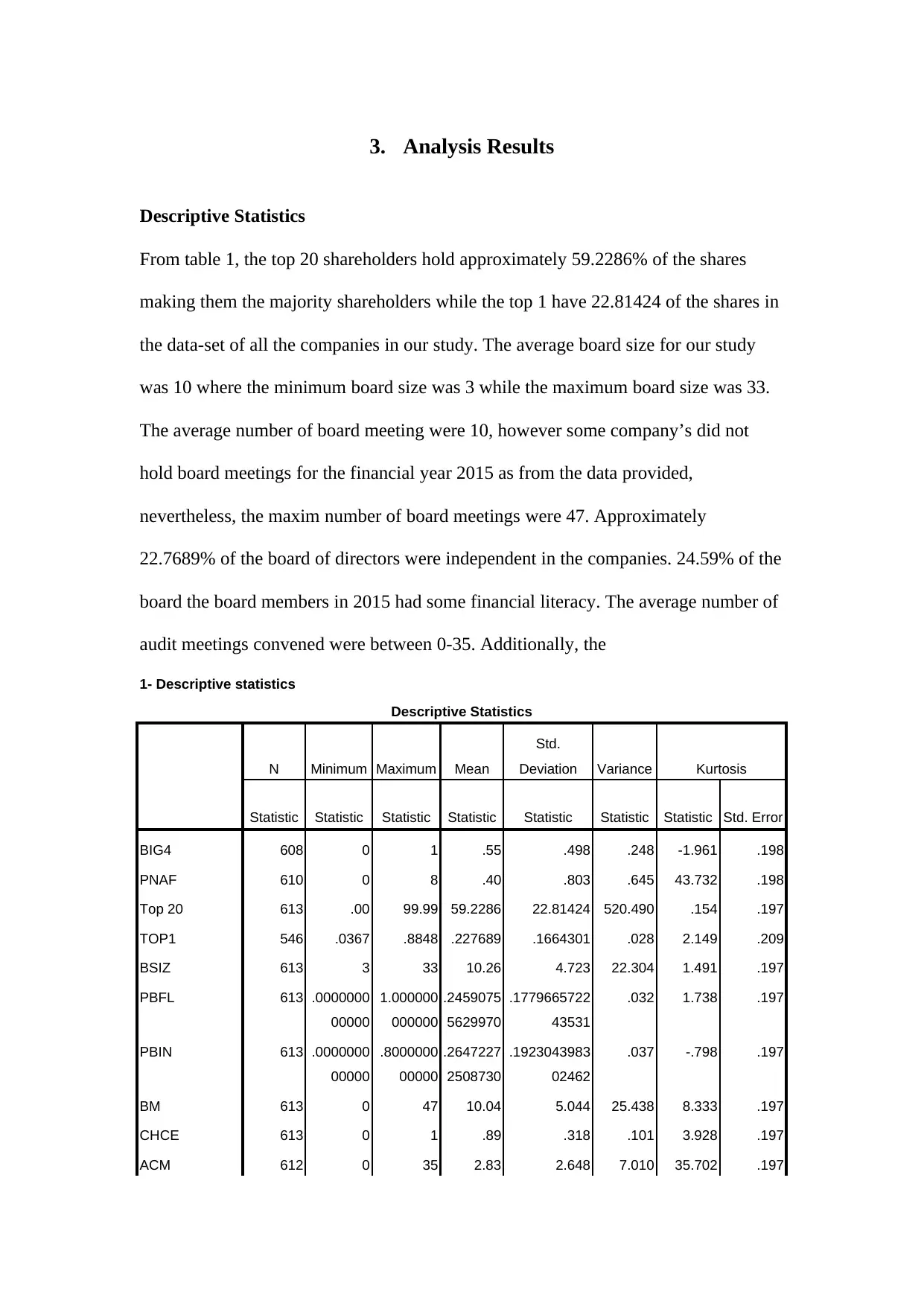

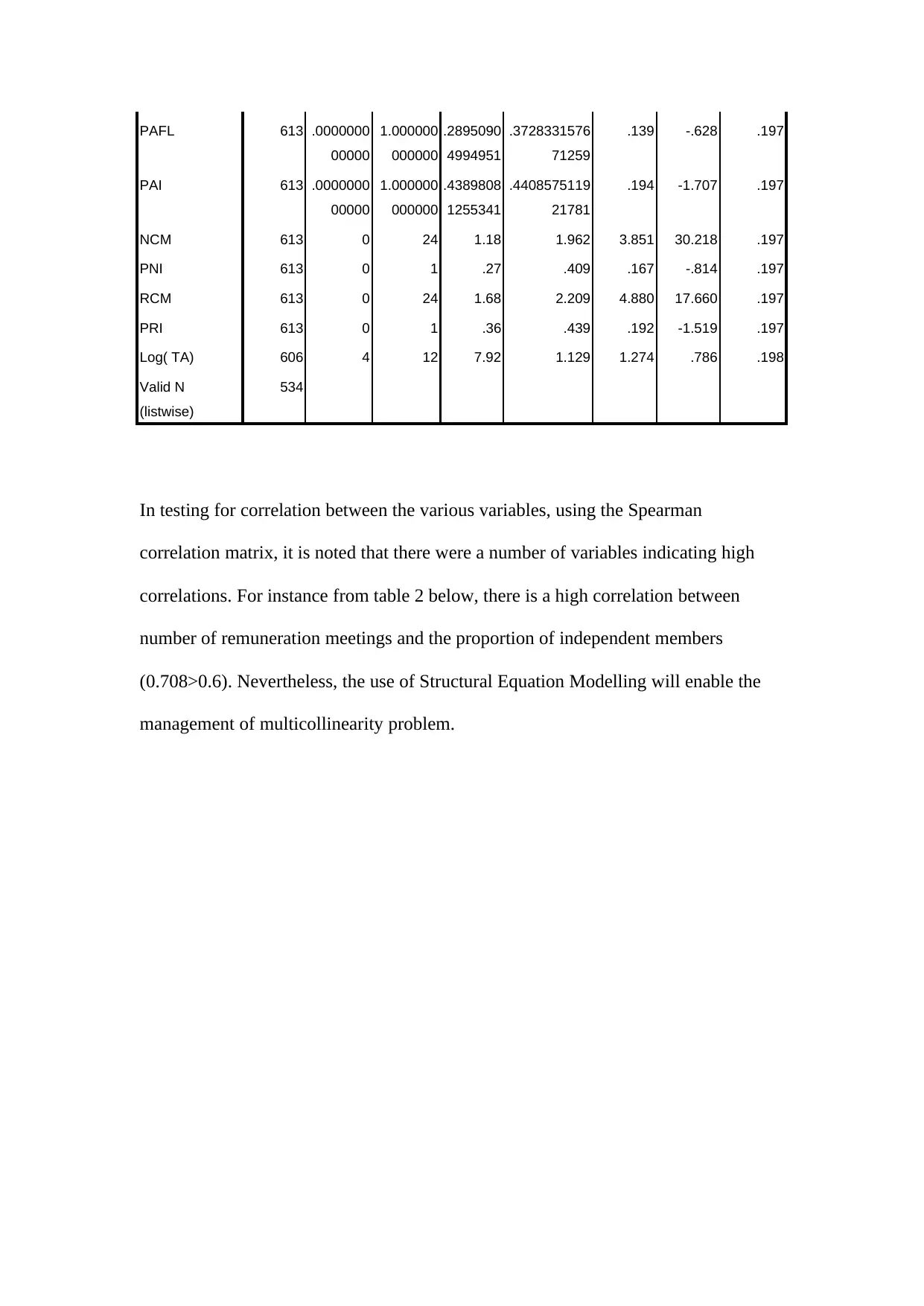

Descriptive Statistics

From table 1, the top 20 shareholders hold approximately 59.2286% of the shares

making them the majority shareholders while the top 1 have 22.81424 of the shares in

the data-set of all the companies in our study. The average board size for our study

was 10 where the minimum board size was 3 while the maximum board size was 33.

The average number of board meeting were 10, however some company’s did not

hold board meetings for the financial year 2015 as from the data provided,

nevertheless, the maxim number of board meetings were 47. Approximately

22.7689% of the board of directors were independent in the companies. 24.59% of the

board the board members in 2015 had some financial literacy. The average number of

audit meetings convened were between 0-35. Additionally, the

1- Descriptive statistics

Descriptive Statistics

N Minimum Maximum Mean

Std.

Deviation Variance Kurtosis

Statistic Statistic Statistic Statistic Statistic Statistic Statistic Std. Error

BIG4 608 0 1 .55 .498 .248 -1.961 .198

PNAF 610 0 8 .40 .803 .645 43.732 .198

Top 20 613 .00 99.99 59.2286 22.81424 520.490 .154 .197

TOP1 546 .0367 .8848 .227689 .1664301 .028 2.149 .209

BSIZ 613 3 33 10.26 4.723 22.304 1.491 .197

PBFL 613 .0000000

00000

1.000000

000000

.2459075

5629970

.1779665722

43531

.032 1.738 .197

PBIN 613 .0000000

00000

.8000000

00000

.2647227

2508730

.1923043983

02462

.037 -.798 .197

BM 613 0 47 10.04 5.044 25.438 8.333 .197

CHCE 613 0 1 .89 .318 .101 3.928 .197

ACM 612 0 35 2.83 2.648 7.010 35.702 .197

Descriptive Statistics

From table 1, the top 20 shareholders hold approximately 59.2286% of the shares

making them the majority shareholders while the top 1 have 22.81424 of the shares in

the data-set of all the companies in our study. The average board size for our study

was 10 where the minimum board size was 3 while the maximum board size was 33.

The average number of board meeting were 10, however some company’s did not

hold board meetings for the financial year 2015 as from the data provided,

nevertheless, the maxim number of board meetings were 47. Approximately

22.7689% of the board of directors were independent in the companies. 24.59% of the

board the board members in 2015 had some financial literacy. The average number of

audit meetings convened were between 0-35. Additionally, the

1- Descriptive statistics

Descriptive Statistics

N Minimum Maximum Mean

Std.

Deviation Variance Kurtosis

Statistic Statistic Statistic Statistic Statistic Statistic Statistic Std. Error

BIG4 608 0 1 .55 .498 .248 -1.961 .198

PNAF 610 0 8 .40 .803 .645 43.732 .198

Top 20 613 .00 99.99 59.2286 22.81424 520.490 .154 .197

TOP1 546 .0367 .8848 .227689 .1664301 .028 2.149 .209

BSIZ 613 3 33 10.26 4.723 22.304 1.491 .197

PBFL 613 .0000000

00000

1.000000

000000

.2459075

5629970

.1779665722

43531

.032 1.738 .197

PBIN 613 .0000000

00000

.8000000

00000

.2647227

2508730

.1923043983

02462

.037 -.798 .197

BM 613 0 47 10.04 5.044 25.438 8.333 .197

CHCE 613 0 1 .89 .318 .101 3.928 .197

ACM 612 0 35 2.83 2.648 7.010 35.702 .197

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PAFL 613 .0000000

00000

1.000000

000000

.2895090

4994951

.3728331576

71259

.139 -.628 .197

PAI 613 .0000000

00000

1.000000

000000

.4389808

1255341

.4408575119

21781

.194 -1.707 .197

NCM 613 0 24 1.18 1.962 3.851 30.218 .197

PNI 613 0 1 .27 .409 .167 -.814 .197

RCM 613 0 24 1.68 2.209 4.880 17.660 .197

PRI 613 0 1 .36 .439 .192 -1.519 .197

Log( TA) 606 4 12 7.92 1.129 1.274 .786 .198

Valid N

(listwise)

534

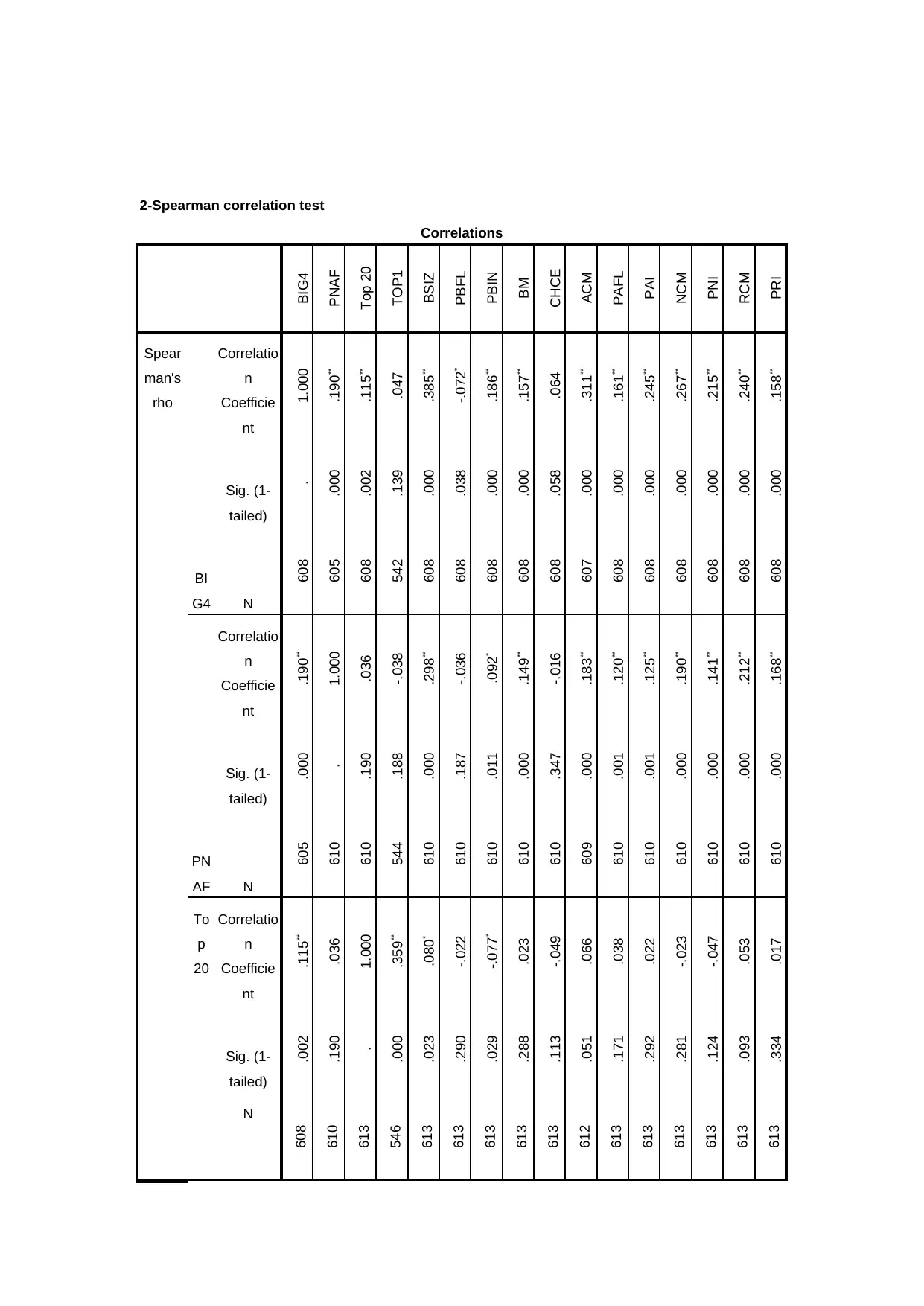

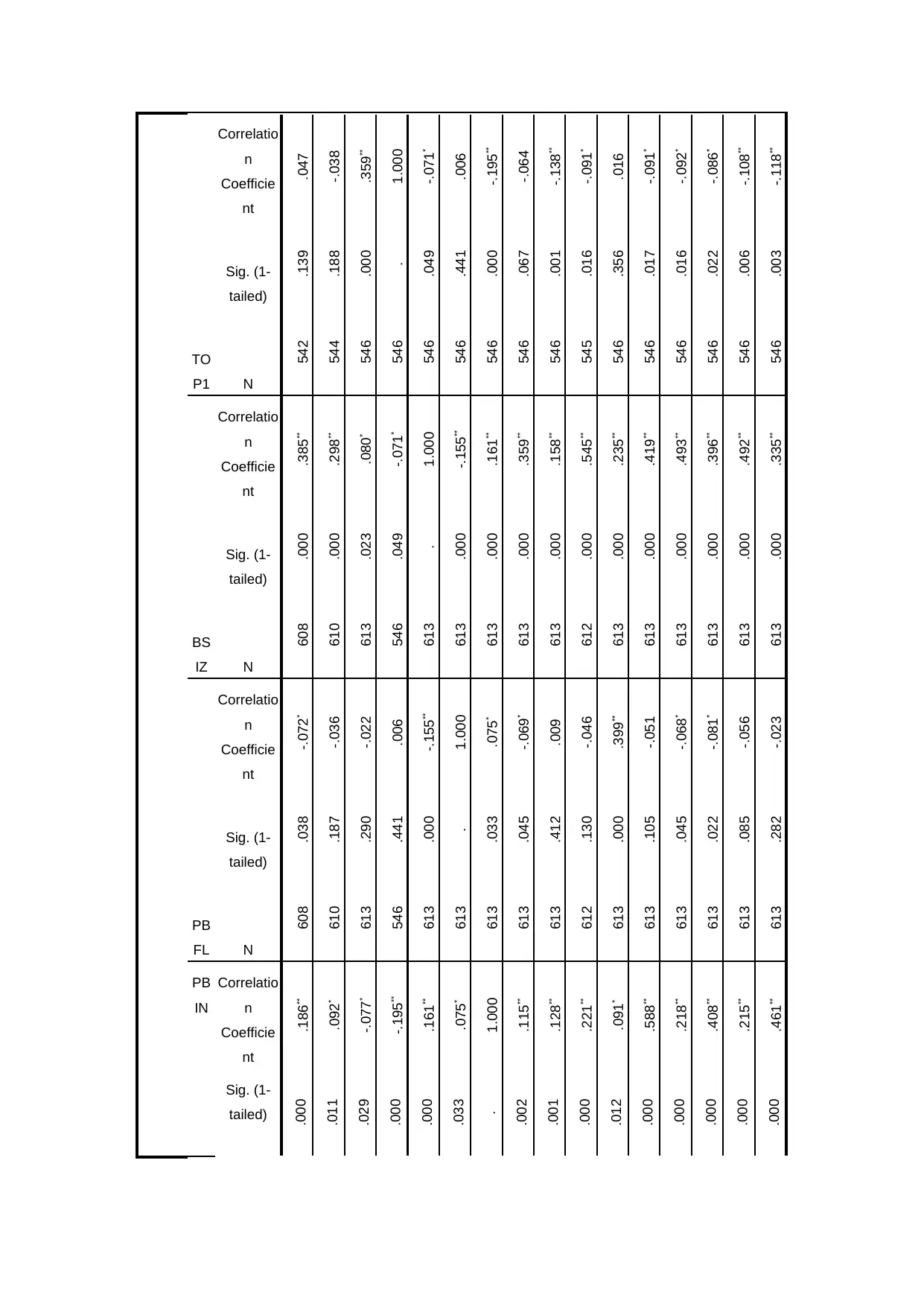

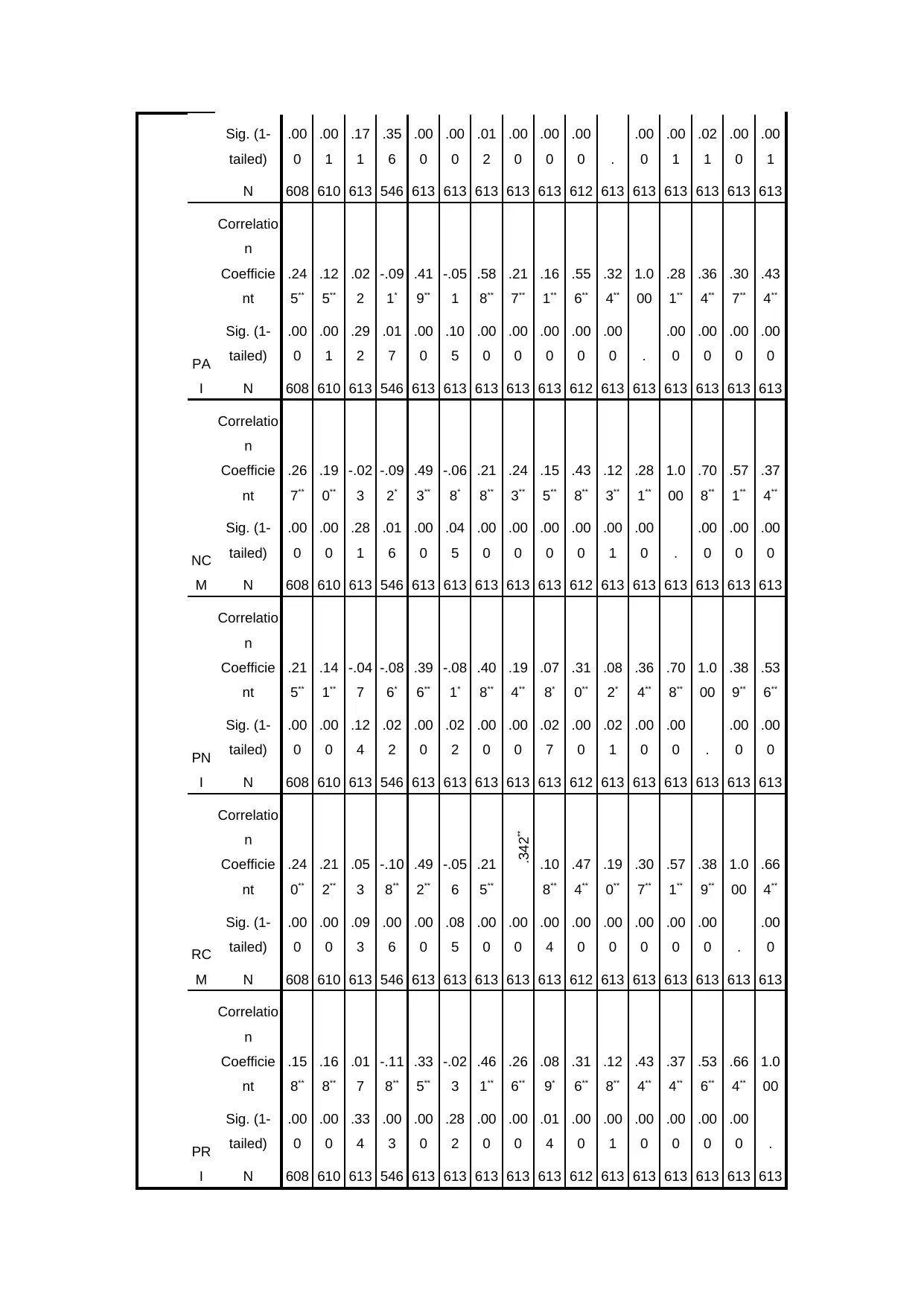

In testing for correlation between the various variables, using the Spearman

correlation matrix, it is noted that there were a number of variables indicating high

correlations. For instance from table 2 below, there is a high correlation between

number of remuneration meetings and the proportion of independent members

(0.708>0.6). Nevertheless, the use of Structural Equation Modelling will enable the

management of multicollinearity problem.

00000

1.000000

000000

.2895090

4994951

.3728331576

71259

.139 -.628 .197

PAI 613 .0000000

00000

1.000000

000000

.4389808

1255341

.4408575119

21781

.194 -1.707 .197

NCM 613 0 24 1.18 1.962 3.851 30.218 .197

PNI 613 0 1 .27 .409 .167 -.814 .197

RCM 613 0 24 1.68 2.209 4.880 17.660 .197

PRI 613 0 1 .36 .439 .192 -1.519 .197

Log( TA) 606 4 12 7.92 1.129 1.274 .786 .198

Valid N

(listwise)

534

In testing for correlation between the various variables, using the Spearman

correlation matrix, it is noted that there were a number of variables indicating high

correlations. For instance from table 2 below, there is a high correlation between

number of remuneration meetings and the proportion of independent members

(0.708>0.6). Nevertheless, the use of Structural Equation Modelling will enable the

management of multicollinearity problem.

2-Spearman correlation test

Correlations

BIG4

PNAF

Top 20

TOP1

BSIZ

PBFL

PBIN

BM

CHCE

ACM

PAFL

PAI

NCM

PNI

RCM

PRI

Spear

man's

rho

BI

G4

Correlatio

n

Coefficie

nt

1.000

.190**

.115**

.047

.385**

-.072*

.186**

.157**

.064

.311**

.161**

.245**

.267**

.215**

.240**

.158**

Sig. (1-

tailed)

.

.000

.002

.139

.000

.038

.000

.000

.058

.000

.000

.000

.000

.000

.000

.000

N

608

605

608

542

608

608

608

608

608

607

608

608

608

608

608

608

PN

AF

Correlatio

n

Coefficie

nt

.190**

1.000

.036

-.038

.298**

-.036

.092*

.149**

-.016

.183**

.120**

.125**

.190**

.141**

.212**

.168**

Sig. (1-

tailed)

.000

.

.190

.188

.000

.187

.011

.000

.347

.000

.001

.001

.000

.000

.000

.000

N

605

610

610

544

610

610

610

610

610

609

610

610

610

610

610

610

To

p

20

Correlatio

n

Coefficie

nt

.115**

.036

1.000

.359**

.080*

-.022

-.077*

.023

-.049

.066

.038

.022

-.023

-.047

.053

.017

Sig. (1-

tailed)

.002

.190

.

.000

.023

.290

.029

.288

.113

.051

.171

.292

.281

.124

.093

.334

N

608

610

613

546

613

613

613

613

613

612

613

613

613

613

613

613

Correlations

BIG4

PNAF

Top 20

TOP1

BSIZ

PBFL

PBIN

BM

CHCE

ACM

PAFL

PAI

NCM

PNI

RCM

PRI

Spear

man's

rho

BI

G4

Correlatio

n

Coefficie

nt

1.000

.190**

.115**

.047

.385**

-.072*

.186**

.157**

.064

.311**

.161**

.245**

.267**

.215**

.240**

.158**

Sig. (1-

tailed)

.

.000

.002

.139

.000

.038

.000

.000

.058

.000

.000

.000

.000

.000

.000

.000

N

608

605

608

542

608

608

608

608

608

607

608

608

608

608

608

608

PN

AF

Correlatio

n

Coefficie

nt

.190**

1.000

.036

-.038

.298**

-.036

.092*

.149**

-.016

.183**

.120**

.125**

.190**

.141**

.212**

.168**

Sig. (1-

tailed)

.000

.

.190

.188

.000

.187

.011

.000

.347

.000

.001

.001

.000

.000

.000

.000

N

605

610

610

544

610

610

610

610

610

609

610

610

610

610

610

610

To

p

20

Correlatio

n

Coefficie

nt

.115**

.036

1.000

.359**

.080*

-.022

-.077*

.023

-.049

.066

.038

.022

-.023

-.047

.053

.017

Sig. (1-

tailed)

.002

.190

.

.000

.023

.290

.029

.288

.113

.051

.171

.292

.281

.124

.093

.334

N

608

610

613

546

613

613

613

613

613

612

613

613

613

613

613

613

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TO

P1

Correlatio

n

Coefficie

nt

.047

-.038

.359**

1.000

-.071*

.006

-.195**

-.064

-.138**

-.091*

.016

-.091*

-.092*

-.086*

-.108**

-.118**

Sig. (1-

tailed)

.139

.188

.000

.

.049

.441

.000

.067

.001

.016

.356

.017

.016

.022

.006

.003

N

542

544

546

546

546

546

546

546

546

545

546

546

546

546

546

546

BS

IZ

Correlatio

n

Coefficie

nt

.385**

.298**

.080*

-.071*

1.000

-.155**

.161**

.359**

.158**

.545**

.235**

.419**

.493**

.396**

.492**

.335**

Sig. (1-

tailed)

.000

.000

.023

.049

.

.000

.000

.000

.000

.000

.000

.000

.000

.000

.000

.000

N

608

610

613

546

613

613

613

613

613

612

613

613

613

613

613

613

PB

FL

Correlatio

n

Coefficie

nt

-.072*

-.036

-.022

.006

-.155**

1.000

.075*

-.069*

.009

-.046

.399**

-.051

-.068*

-.081*

-.056

-.023

Sig. (1-

tailed)

.038

.187

.290

.441

.000

.

.033

.045

.412

.130

.000

.105

.045

.022

.085

.282

N

608

610

613

546

613

613

613

613

613

612

613

613

613

613

613

613

PB

IN

Correlatio

n

Coefficie

nt

.186**

.092*

-.077*

-.195**

.161**

.075*

1.000

.115**

.128**

.221**

.091*

.588**

.218**

.408**

.215**

.461**

Sig. (1-

tailed)

.000

.011

.029

.000

.000

.033

.

.002

.001

.000

.012

.000

.000

.000

.000

.000

P1

Correlatio

n

Coefficie

nt

.047

-.038

.359**

1.000

-.071*

.006

-.195**

-.064

-.138**

-.091*

.016

-.091*

-.092*

-.086*

-.108**

-.118**

Sig. (1-

tailed)

.139

.188

.000

.

.049

.441

.000

.067

.001

.016

.356

.017

.016

.022

.006

.003

N

542

544

546

546

546

546

546

546

546

545

546

546

546

546

546

546

BS

IZ

Correlatio

n

Coefficie

nt

.385**

.298**

.080*

-.071*

1.000

-.155**

.161**

.359**

.158**

.545**

.235**

.419**

.493**

.396**

.492**

.335**

Sig. (1-

tailed)

.000

.000

.023

.049

.

.000

.000

.000

.000

.000

.000

.000

.000

.000

.000

.000

N

608

610

613

546

613

613

613

613

613

612

613

613

613

613

613

613

PB

FL

Correlatio

n

Coefficie

nt

-.072*

-.036

-.022

.006

-.155**

1.000

.075*

-.069*

.009

-.046

.399**

-.051

-.068*

-.081*

-.056

-.023

Sig. (1-

tailed)

.038

.187

.290

.441

.000

.

.033

.045

.412

.130

.000

.105

.045

.022

.085

.282

N

608

610

613

546

613

613

613

613

613

612

613

613

613

613

613

613

PB

IN

Correlatio

n

Coefficie

nt

.186**

.092*

-.077*

-.195**

.161**

.075*

1.000

.115**

.128**

.221**

.091*

.588**

.218**

.408**

.215**

.461**

Sig. (1-

tailed)

.000

.011

.029

.000

.000

.033

.

.002

.001

.000

.012

.000

.000

.000

.000

.000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

N

608

610

613

546

613

613

613

613

613

612

613

613

613

613

613

613

BM

Correlatio

n

Coefficie

nt

.157**

.149**

.023

-.064

.359**

-.069*

.115**

1.000

.152**

.358**

.138**

.217**

.243**

.194**

.342**

.266**

Sig. (1-

tailed)

.000

.000

.288

.067

.000

.045

.002

.

.000

.000

.000

.000

.000

.000

.000

.000

N

608

610

613

546

613

613

613

613

613

612

613

613

613

613

613

613

CH

CE

Correlatio

n

Coefficie

nt

.064

-.016

-.049

-.138**

.158**

.009

.128**

.152**

1.000

.199**

.151**

.161**

.155**

.078*

.108**

.089*

Sig. (1-

tailed)

.058

.347

.113

.001

.000

.412

.001

.000

.

.000

.000

.000

.000

.027

.004

.014

N

608

610

613

546

613

613

613

613

613

612

613

613

613

613

613

613

AC

M

Correlatio

n

Coefficie

nt

.311**

.183**

.066

-.091*

.545**

-.046

.221**

.358**

.199**

1.000

.445**

.556**

.438**

.310**

.474**

.316**

Sig. (1-

tailed)

.000

.000

.051

.016

.000

.130

.000

.000

.000

.

.000

.000

.000

.000

.000

.000

N

607

609

612

545

612

612

612

612

612

612

612

612

612

612

612

612

PA

FL

Correlatio

n

Coefficie

nt

.16

1**

.12

0**

.03

8

.01

6

.23

5**

.39

9**

.09

1*

.13

8**

.15

1**

.44

5**

1.0

00

.32

4**

.12

3**

.08

2*

.19

0**

.12

8**

608

610

613

546

613

613

613

613

613

612

613

613

613

613

613

613

BM

Correlatio

n

Coefficie

nt

.157**

.149**

.023

-.064

.359**

-.069*

.115**

1.000

.152**

.358**

.138**

.217**

.243**

.194**

.342**

.266**

Sig. (1-

tailed)

.000

.000

.288

.067

.000

.045

.002

.

.000

.000

.000

.000

.000

.000

.000

.000

N

608

610

613

546

613

613

613

613

613

612

613

613

613

613

613

613

CH

CE

Correlatio

n

Coefficie

nt

.064

-.016

-.049

-.138**

.158**

.009

.128**

.152**

1.000

.199**

.151**

.161**

.155**

.078*

.108**

.089*

Sig. (1-

tailed)

.058

.347

.113

.001

.000

.412

.001

.000

.

.000

.000

.000

.000

.027

.004

.014

N

608

610

613

546

613

613

613

613

613

612

613

613

613

613

613

613

AC

M

Correlatio

n

Coefficie

nt

.311**

.183**

.066

-.091*

.545**

-.046

.221**

.358**

.199**

1.000

.445**

.556**

.438**

.310**

.474**

.316**

Sig. (1-

tailed)

.000

.000

.051

.016

.000

.130

.000

.000

.000

.

.000

.000

.000

.000

.000

.000

N

607

609

612

545

612

612

612

612

612

612

612

612

612

612

612

612

PA

FL

Correlatio

n

Coefficie

nt

.16

1**

.12

0**

.03

8

.01

6

.23

5**

.39

9**

.09

1*

.13

8**

.15

1**

.44

5**

1.0

00

.32

4**

.12

3**

.08

2*

.19

0**

.12

8**

Sig. (1-

tailed)

.00

0

.00

1

.17

1

.35

6

.00

0

.00

0

.01

2

.00

0

.00

0

.00

0 .

.00

0

.00

1

.02

1

.00

0

.00

1

N 608 610 613 546 613 613 613 613 613 612 613 613 613 613 613 613

PA

I

Correlatio

n

Coefficie

nt

.24

5**

.12

5**

.02

2

-.09

1*

.41

9**

-.05

1

.58

8**

.21

7**

.16

1**

.55

6**

.32

4**

1.0

00

.28

1**

.36

4**

.30

7**

.43

4**

Sig. (1-

tailed)

.00

0

.00

1

.29

2

.01

7

.00

0

.10

5

.00

0

.00

0

.00

0

.00

0

.00

0 .

.00

0

.00

0

.00

0

.00

0

N 608 610 613 546 613 613 613 613 613 612 613 613 613 613 613 613

NC

M

Correlatio

n

Coefficie

nt

.26

7**

.19

0**

-.02

3

-.09

2*

.49

3**

-.06

8*

.21

8**

.24

3**

.15

5**

.43

8**

.12

3**

.28

1**

1.0

00

.70

8**

.57

1**

.37

4**

Sig. (1-

tailed)

.00

0

.00

0

.28

1

.01

6

.00

0

.04

5

.00

0

.00

0

.00

0

.00

0

.00

1

.00

0 .

.00

0

.00

0

.00

0

N 608 610 613 546 613 613 613 613 613 612 613 613 613 613 613 613

PN

I

Correlatio

n

Coefficie

nt

.21

5**

.14

1**

-.04

7

-.08

6*

.39

6**

-.08

1*

.40

8**

.19

4**

.07

8*

.31

0**

.08

2*

.36

4**

.70

8**

1.0

00

.38

9**

.53

6**

Sig. (1-

tailed)

.00

0

.00

0

.12

4

.02

2

.00

0

.02

2

.00

0

.00

0

.02

7

.00

0

.02

1

.00

0

.00

0 .

.00

0

.00

0

N 608 610 613 546 613 613 613 613 613 612 613 613 613 613 613 613

RC

M

Correlatio

n

Coefficie

nt

.24

0**

.21

2**

.05

3

-.10

8**

.49

2**

-.05

6

.21

5**

.342**

.10

8**

.47

4**

.19

0**

.30

7**

.57

1**

.38

9**

1.0

00

.66

4**

Sig. (1-

tailed)

.00

0

.00

0

.09

3

.00

6

.00

0

.08

5

.00

0

.00

0

.00

4

.00

0

.00

0

.00

0

.00

0

.00

0 .

.00

0

N 608 610 613 546 613 613 613 613 613 612 613 613 613 613 613 613

PR

I

Correlatio

n

Coefficie

nt

.15

8**

.16

8**

.01

7

-.11

8**

.33

5**

-.02

3

.46

1**

.26

6**

.08

9*

.31

6**

.12

8**

.43

4**

.37

4**

.53

6**

.66

4**

1.0

00

Sig. (1-

tailed)

.00

0

.00

0

.33

4

.00

3

.00

0

.28

2

.00

0

.00

0

.01

4

.00

0

.00

1

.00

0

.00

0

.00

0

.00

0 .

N 608 610 613 546 613 613 613 613 613 612 613 613 613 613 613 613

tailed)

.00

0

.00

1

.17

1

.35

6

.00

0

.00

0

.01

2

.00

0

.00

0

.00

0 .

.00

0

.00

1

.02

1

.00

0

.00

1

N 608 610 613 546 613 613 613 613 613 612 613 613 613 613 613 613

PA

I

Correlatio

n

Coefficie

nt

.24

5**

.12

5**

.02

2

-.09

1*

.41

9**

-.05

1

.58

8**

.21

7**

.16

1**

.55

6**

.32

4**

1.0

00

.28

1**

.36

4**

.30

7**

.43

4**

Sig. (1-

tailed)

.00

0

.00

1

.29

2

.01

7

.00

0

.10

5

.00

0

.00

0

.00

0

.00

0

.00

0 .

.00

0

.00

0

.00

0

.00

0

N 608 610 613 546 613 613 613 613 613 612 613 613 613 613 613 613

NC

M

Correlatio

n

Coefficie

nt

.26

7**

.19

0**

-.02

3

-.09

2*

.49

3**

-.06

8*

.21

8**

.24

3**

.15

5**

.43

8**

.12

3**

.28

1**

1.0

00

.70

8**

.57

1**

.37

4**

Sig. (1-

tailed)

.00

0

.00

0

.28

1

.01

6

.00

0

.04

5

.00

0

.00

0

.00

0

.00

0

.00

1

.00

0 .

.00

0

.00

0

.00

0

N 608 610 613 546 613 613 613 613 613 612 613 613 613 613 613 613

PN

I

Correlatio

n

Coefficie

nt

.21

5**

.14

1**

-.04

7

-.08

6*

.39

6**

-.08

1*

.40

8**

.19

4**

.07

8*

.31

0**

.08

2*

.36

4**

.70

8**

1.0

00

.38

9**

.53

6**

Sig. (1-

tailed)

.00

0

.00

0

.12

4

.02

2

.00

0

.02

2

.00

0

.00

0

.02

7

.00

0

.02

1

.00

0

.00

0 .

.00

0

.00

0

N 608 610 613 546 613 613 613 613 613 612 613 613 613 613 613 613

RC

M

Correlatio

n

Coefficie

nt

.24

0**

.21

2**

.05

3

-.10

8**

.49

2**

-.05

6

.21

5**

.342**

.10

8**

.47

4**

.19

0**

.30

7**

.57

1**

.38

9**

1.0

00

.66

4**

Sig. (1-

tailed)

.00

0

.00

0

.09

3

.00

6

.00

0

.08

5

.00

0

.00

0

.00

4

.00

0

.00

0

.00

0

.00

0

.00

0 .

.00

0

N 608 610 613 546 613 613 613 613 613 612 613 613 613 613 613 613

PR

I

Correlatio

n

Coefficie

nt

.15

8**

.16

8**

.01

7

-.11

8**

.33

5**

-.02

3

.46

1**

.26

6**

.08

9*

.31

6**

.12

8**

.43

4**

.37

4**

.53

6**

.66

4**

1.0

00

Sig. (1-

tailed)

.00

0

.00

0

.33

4

.00

3

.00

0

.28

2

.00

0

.00

0

.01

4

.00

0

.00

1

.00

0

.00

0

.00

0

.00

0 .

N 608 610 613 546 613 613 613 613 613 612 613 613 613 613 613 613

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

**. Correlation is significant at the 0.01 level (1-tailed).

*. Correlation is significant at the 0.05 level (1-tailed).

*. Correlation is significant at the 0.05 level (1-tailed).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

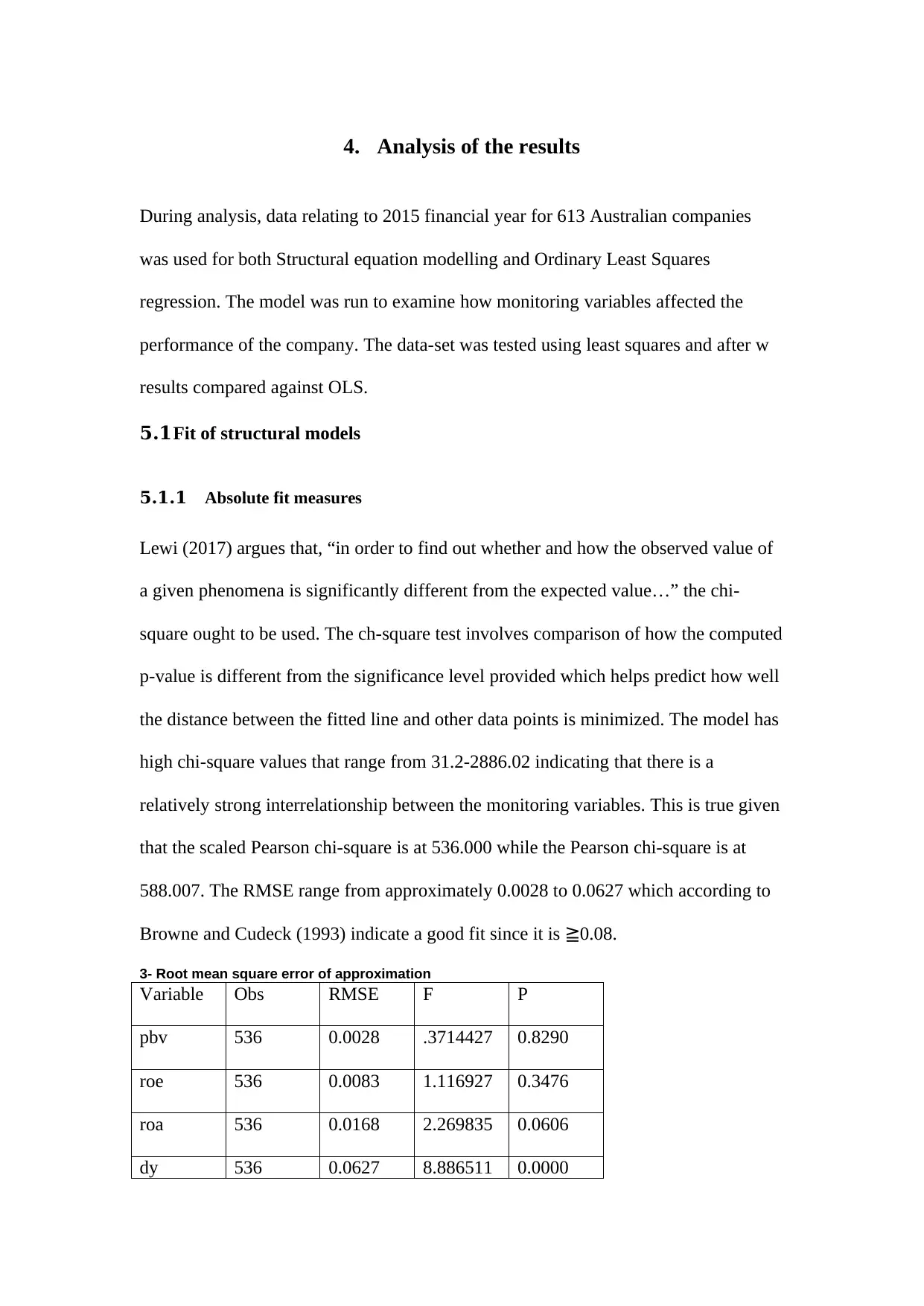

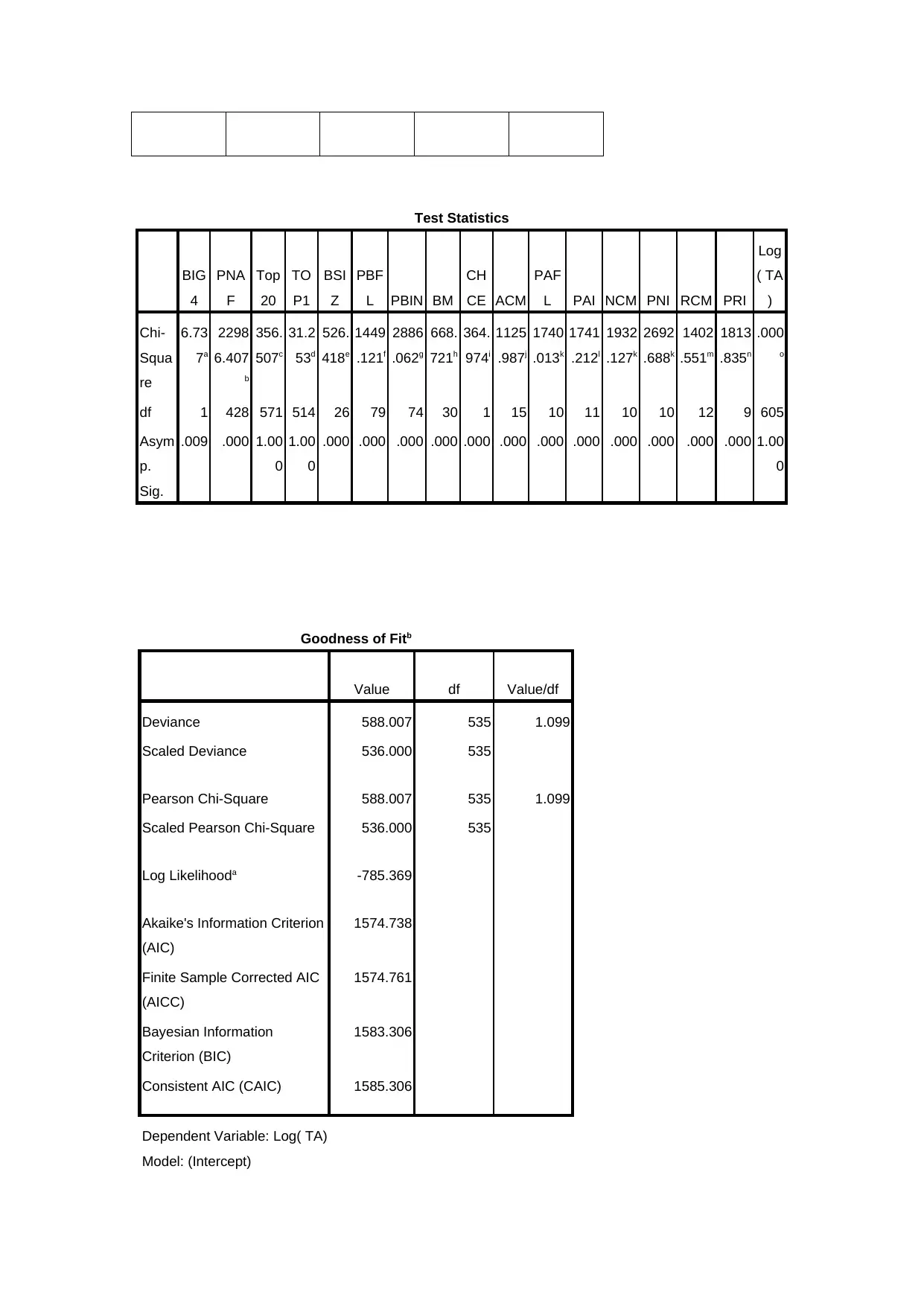

4. Analysis of the results

During analysis, data relating to 2015 financial year for 613 Australian companies

was used for both Structural equation modelling and Ordinary Least Squares

regression. The model was run to examine how monitoring variables affected the

performance of the company. The data-set was tested using least squares and after w

results compared against OLS.

5.1Fit of structural models

5.1.1 Absolute fit measures

Lewi (2017) argues that, “in order to find out whether and how the observed value of

a given phenomena is significantly different from the expected value…” the chi-

square ought to be used. The ch-square test involves comparison of how the computed

p-value is different from the significance level provided which helps predict how well

the distance between the fitted line and other data points is minimized. The model has

high chi-square values that range from 31.2-2886.02 indicating that there is a

relatively strong interrelationship between the monitoring variables. This is true given

that the scaled Pearson chi-square is at 536.000 while the Pearson chi-square is at

588.007. The RMSE range from approximately 0.0028 to 0.0627 which according to

Browne and Cudeck (1993) indicate a good fit since it is ≧0.08.

3- Root mean square error of approximation

Variable Obs RMSE F P

pbv 536 0.0028 .3714427 0.8290

roe 536 0.0083 1.116927 0.3476

roa 536 0.0168 2.269835 0.0606

dy 536 0.0627 8.886511 0.0000

During analysis, data relating to 2015 financial year for 613 Australian companies

was used for both Structural equation modelling and Ordinary Least Squares

regression. The model was run to examine how monitoring variables affected the

performance of the company. The data-set was tested using least squares and after w

results compared against OLS.

5.1Fit of structural models

5.1.1 Absolute fit measures

Lewi (2017) argues that, “in order to find out whether and how the observed value of

a given phenomena is significantly different from the expected value…” the chi-

square ought to be used. The ch-square test involves comparison of how the computed

p-value is different from the significance level provided which helps predict how well

the distance between the fitted line and other data points is minimized. The model has

high chi-square values that range from 31.2-2886.02 indicating that there is a

relatively strong interrelationship between the monitoring variables. This is true given

that the scaled Pearson chi-square is at 536.000 while the Pearson chi-square is at

588.007. The RMSE range from approximately 0.0028 to 0.0627 which according to

Browne and Cudeck (1993) indicate a good fit since it is ≧0.08.

3- Root mean square error of approximation

Variable Obs RMSE F P

pbv 536 0.0028 .3714427 0.8290

roe 536 0.0083 1.116927 0.3476

roa 536 0.0168 2.269835 0.0606

dy 536 0.0627 8.886511 0.0000

Test Statistics

BIG

4

PNA

F

Top

20

TO

P1

BSI

Z

PBF

L PBIN BM

CH

CE ACM

PAF

L PAI NCM PNI RCM PRI

Log

( TA

)

Chi-

Squa

re

6.73

7a

2298

6.407

b

356.

507c

31.2

53d

526.

418e

1449

.121f

2886

.062g

668.

721h

364.

974i

1125

.987j

1740

.013k

1741

.212l

1932

.127k

2692

.688k

1402

.551m

1813

.835n

.000

o

df 1 428 571 514 26 79 74 30 1 15 10 11 10 10 12 9 605

Asym

p.

Sig.

.009 .000 1.00

0

1.00

0

.000 .000 .000 .000 .000 .000 .000 .000 .000 .000 .000 .000 1.00

0

Goodness of Fitb

Value df Value/df

Deviance 588.007 535 1.099

Scaled Deviance 536.000 535

Pearson Chi-Square 588.007 535 1.099

Scaled Pearson Chi-Square 536.000 535

Log Likelihooda -785.369

Akaike's Information Criterion

(AIC)

1574.738

Finite Sample Corrected AIC

(AICC)

1574.761

Bayesian Information

Criterion (BIC)

1583.306

Consistent AIC (CAIC) 1585.306

Dependent Variable: Log( TA)

Model: (Intercept)

BIG

4

PNA

F

Top

20

TO

P1

BSI

Z

PBF

L PBIN BM

CH

CE ACM

PAF

L PAI NCM PNI RCM PRI

Log

( TA

)

Chi-

Squa

re

6.73

7a

2298

6.407

b

356.

507c

31.2

53d

526.

418e

1449

.121f

2886

.062g

668.

721h

364.

974i

1125

.987j

1740

.013k

1741

.212l

1932

.127k

2692

.688k

1402

.551m

1813

.835n

.000

o

df 1 428 571 514 26 79 74 30 1 15 10 11 10 10 12 9 605

Asym

p.

Sig.

.009 .000 1.00

0

1.00

0

.000 .000 .000 .000 .000 .000 .000 .000 .000 .000 .000 .000 1.00

0

Goodness of Fitb

Value df Value/df

Deviance 588.007 535 1.099

Scaled Deviance 536.000 535

Pearson Chi-Square 588.007 535 1.099

Scaled Pearson Chi-Square 536.000 535

Log Likelihooda -785.369

Akaike's Information Criterion

(AIC)

1574.738

Finite Sample Corrected AIC

(AICC)

1574.761

Bayesian Information

Criterion (BIC)

1583.306

Consistent AIC (CAIC) 1585.306

Dependent Variable: Log( TA)

Model: (Intercept)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.