Contemporary Issues in Accounting: Research Proposal, ACC320, 2018

VerifiedAdded on 2023/06/04

|10

|2302

|213

Report

AI Summary

This research proposal investigates the relationship between corporate governance, stakeholder interests, and sustainability reporting. The study examines whether corporate governance should prioritize stakeholder interests over shareholders, the increasing provision of sustainability reporting, and accountants' beliefs regarding sustainability reporting. The proposal includes an introduction defining the issue, theoretical and practical motivations, and a literature review of relevant theories such as voluntary disclosure theory. The research aims to contribute to existing literature by exploring the interrelationships between corporate governance, stakeholder concerns, and sustainability reporting, and assesses whether the provision for sustainability reporting has increased. The proposal also formulates hypotheses based on agency theory and voluntary disclosure theory, exploring the impact of corporate governance on sustainability reporting and accountants' beliefs, and provides a table of appendix with key performance indicators.

Contemporary Issues in Accounting1

CONTEMPORARY ISSUES IN ACCOUNTING

By (Your Name)

ACC320 Contemporary Issues in Accounting

Semester 2 2018

Research Proposal

Your Name:

Student ID:

Title:

Submission Date:

CONTEMPORARY ISSUES IN ACCOUNTING

By (Your Name)

ACC320 Contemporary Issues in Accounting

Semester 2 2018

Research Proposal

Your Name:

Student ID:

Title:

Submission Date:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contemporary Issues in Accounting2

Table of Contents

Contemporary Issues in Accounting................................................................................................3

Introduction..................................................................................................................................3

Theoretical Framework....................................................................................................................4

Theoretical Motivation................................................................................................................5

Practical Motivation.....................................................................................................................6

Literature Review............................................................................................................................6

Voluntary Disclosure theory on Sustainability Reporting...........................................................6

Hypothesis.......................................................................................................................................7

References........................................................................................................................................9

Appendix........................................................................................................................................10

Table of Contents

Contemporary Issues in Accounting................................................................................................3

Introduction..................................................................................................................................3

Theoretical Framework....................................................................................................................4

Theoretical Motivation................................................................................................................5

Practical Motivation.....................................................................................................................6

Literature Review............................................................................................................................6

Voluntary Disclosure theory on Sustainability Reporting...........................................................6

Hypothesis.......................................................................................................................................7

References........................................................................................................................................9

Appendix........................................................................................................................................10

Contemporary Issues in Accounting3

Contemporary Issues in Accounting

A Study On Corporate Governance Concern with Stakeholders More than Shareholders, Increase

in the Provision Of Sustainability Reporting And Believes Of Accountants on Sustainability

Reporting

Introduction

This study examines the extent to which corporate governance should be concerned with

the interests of stakeholders more than that of shareholders, increase in provision of

sustainability reporting and believe of accountants in sustainability reporting, (Amran and

Ooi,2014, pp.38-41). Due to increases in levels of public awareness on roles played by firms in

terms of weather changes, companies have been forced to incorporate non-financial reporting in

their financial statements. The corporate governance management is supposed to inform their

stakeholders on reporting about environmental, social and economic performance.

Sustainability reporting has become a normal practice which is driven through by

potential values of business and is generated by improved stakeholder reporting and statement.

Stakeholders are more concerned in understanding performance and approaches used by

companies while managing sustainability reporting (Deegan and Gordon, 1996, pp.187-199).

There is no universally accepted description of sustainability reporting but it simply implies to a

business entity reporting on economic, social and environment performance. Sustainability is the

same as corporate responsibility reporting (CSR) and reporting on triple bottom line (Hahn and

Kuhnem2013, pp.5-21). Non-financial reporting is more widespread due to the fact that, its

reporting affects the material performance of companies and also the stakeholders demand the

disclosure of sustainability reporting in their financial statements.

Contemporary Issues in Accounting

A Study On Corporate Governance Concern with Stakeholders More than Shareholders, Increase

in the Provision Of Sustainability Reporting And Believes Of Accountants on Sustainability

Reporting

Introduction

This study examines the extent to which corporate governance should be concerned with

the interests of stakeholders more than that of shareholders, increase in provision of

sustainability reporting and believe of accountants in sustainability reporting, (Amran and

Ooi,2014, pp.38-41). Due to increases in levels of public awareness on roles played by firms in

terms of weather changes, companies have been forced to incorporate non-financial reporting in

their financial statements. The corporate governance management is supposed to inform their

stakeholders on reporting about environmental, social and economic performance.

Sustainability reporting has become a normal practice which is driven through by

potential values of business and is generated by improved stakeholder reporting and statement.

Stakeholders are more concerned in understanding performance and approaches used by

companies while managing sustainability reporting (Deegan and Gordon, 1996, pp.187-199).

There is no universally accepted description of sustainability reporting but it simply implies to a

business entity reporting on economic, social and environment performance. Sustainability is the

same as corporate responsibility reporting (CSR) and reporting on triple bottom line (Hahn and

Kuhnem2013, pp.5-21). Non-financial reporting is more widespread due to the fact that, its

reporting affects the material performance of companies and also the stakeholders demand the

disclosure of sustainability reporting in their financial statements.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Contemporary Issues in Accounting4

Organizations produce non-financial information voluntarily. The voluntary production

of these reports implies that the stakeholders might behave opportunistically and therefore not

incorporate poor non-financial information in their sustainability reports. In order for

organizations to produce good quality sustainability reports and reduce the behavior of

opportunistic stakeholders, corporate governance of those firms should be able to come up with

rules and techniques that help in monitoring the activities of the stakeholders. Sustainability

reporting is done internally in organizations while corporate governance is done externally. The

pressures exerted to the stakeholders by corporate governance will push the organizations to be

more responsible in non-financial reporting and consequently giving high level quality of

information. Higher level of concern by corporate governance on stakeholders’ increase reports

on sustainability by accounts and increase its provision, (Minan, Hickox and Gimiliano,2011,

np).

Theoretical Framework

This research positively contributes to literature about corporate governance and

voluntary non-financial reporting in numerous ways (Tirole, 2001, pp.1-35). First, a lot of

literatures have been researched concerning corporate governance and sustainability reporting.

Those literatures do not provide empirical evidence in unfolding the relationships that exists

between, sustainability reporting of accountants and the concern of corporate governance with

the stakeholders. This study ventures in explaining the interrelationships that exist between

corporate governance concern with stakeholders and sustainability reporting. It also endeavors to

find out if the provision for sustainability reporting has increased. Secondly, this study

complements literature in that the research method employed in this research has not been used

in performance of any research. The other types of research majorly involve the level of

Organizations produce non-financial information voluntarily. The voluntary production

of these reports implies that the stakeholders might behave opportunistically and therefore not

incorporate poor non-financial information in their sustainability reports. In order for

organizations to produce good quality sustainability reports and reduce the behavior of

opportunistic stakeholders, corporate governance of those firms should be able to come up with

rules and techniques that help in monitoring the activities of the stakeholders. Sustainability

reporting is done internally in organizations while corporate governance is done externally. The

pressures exerted to the stakeholders by corporate governance will push the organizations to be

more responsible in non-financial reporting and consequently giving high level quality of

information. Higher level of concern by corporate governance on stakeholders’ increase reports

on sustainability by accounts and increase its provision, (Minan, Hickox and Gimiliano,2011,

np).

Theoretical Framework

This research positively contributes to literature about corporate governance and

voluntary non-financial reporting in numerous ways (Tirole, 2001, pp.1-35). First, a lot of

literatures have been researched concerning corporate governance and sustainability reporting.

Those literatures do not provide empirical evidence in unfolding the relationships that exists

between, sustainability reporting of accountants and the concern of corporate governance with

the stakeholders. This study ventures in explaining the interrelationships that exist between

corporate governance concern with stakeholders and sustainability reporting. It also endeavors to

find out if the provision for sustainability reporting has increased. Secondly, this study

complements literature in that the research method employed in this research has not been used

in performance of any research. The other types of research majorly involve the level of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contemporary Issues in Accounting5

sustainability and the quality of sustainability reporting instead of focusing on the level of

reporting and how it can be improved. Lastly this study contributes to literature in that in terms

of valuing and determining the level of concern the managers need to put on stakeholders so as

to produce sustainable report and to find out if the provision of sustainable reports have

increased, different variables are used and this will help in producing quality results.

Theoretical Motivation

According to agency theory, the stakeholders have capacity to reduce information

asymmetry on non-financial reporting through producing sustainability reports. In the contrary,

publishing these reports gives the stakeholders room for manipulation of these reports by

avoiding to include information which may temper with the image of their organizations.

According to (Friedman 2007, np), engagement of the stake holders in corporate social

responsibility in terms of non-financial reporting gives rise to what is known as agency

problems. The stakeholders and shareholder’s problem arise because the stakeholders always

want to publish reports which will enable them develop in their careers, boost the image of the

organizations and also develop in their political careers. The stakeholders do these things at the

expense of shareholders who demand reliable presentation of non-financial information. In order

to remove agency problems while reporting on non-financial reporting, corporate governance

should be more concerned on stakeholders more than in shareholders by setting up mechanisms

and exerting pressure on the stakeholders so as to be able to increase the provision of

sustainability reporting and increase the believes of accountants on sustainability reporting.

sustainability and the quality of sustainability reporting instead of focusing on the level of

reporting and how it can be improved. Lastly this study contributes to literature in that in terms

of valuing and determining the level of concern the managers need to put on stakeholders so as

to produce sustainable report and to find out if the provision of sustainable reports have

increased, different variables are used and this will help in producing quality results.

Theoretical Motivation

According to agency theory, the stakeholders have capacity to reduce information

asymmetry on non-financial reporting through producing sustainability reports. In the contrary,

publishing these reports gives the stakeholders room for manipulation of these reports by

avoiding to include information which may temper with the image of their organizations.

According to (Friedman 2007, np), engagement of the stake holders in corporate social

responsibility in terms of non-financial reporting gives rise to what is known as agency

problems. The stakeholders and shareholder’s problem arise because the stakeholders always

want to publish reports which will enable them develop in their careers, boost the image of the

organizations and also develop in their political careers. The stakeholders do these things at the

expense of shareholders who demand reliable presentation of non-financial information. In order

to remove agency problems while reporting on non-financial reporting, corporate governance

should be more concerned on stakeholders more than in shareholders by setting up mechanisms

and exerting pressure on the stakeholders so as to be able to increase the provision of

sustainability reporting and increase the believes of accountants on sustainability reporting.

Contemporary Issues in Accounting6

Practical Motivation

Sustainability reporting is important to many companies and it also assist investors in

decision making. Stakeholders now believe in nonfinancial reporting. In order to come up with

good sustainable report we focus on the internal features of the reporting process. If firms want

to produce good sustainable reports they should have good corporate governance who put up

good mechanisms to help achieve the operational goals and control the stakeholders so as to

reduce conflict of interest. Nonfinancial information is good to both the firm and the investors

who read the sustainability reports. Having good quality sustainability information will mean

that the firm has good corporate governance, good management and accountants who believe in

sustainability reporting.

Literature Review

Voluntary Disclosure theory on Sustainability Reporting

This theory suggests that there is a positive correlation between performance on

sustainability and disclosure of discretionary level of sustainability. The notion behind this

theory is that, organizations which perform well in sustainability reporting give much focus on

their performance indictors which are hard to be imitated by non- performing firms and this

helps the performing firms in improving their image, (Brammer and Pavelin,2006, pp.1168-

1188). Those firms which perform well in sustainability reporting have ability to disclose high

quality non-financial information and this is done in order to distinguish them from non-

performing firms in terms of sustainability reporting. Those firms which disclose less

information in their non-financial reports perform poorly and they are not therefore able to attract

more investors.

Practical Motivation

Sustainability reporting is important to many companies and it also assist investors in

decision making. Stakeholders now believe in nonfinancial reporting. In order to come up with

good sustainable report we focus on the internal features of the reporting process. If firms want

to produce good sustainable reports they should have good corporate governance who put up

good mechanisms to help achieve the operational goals and control the stakeholders so as to

reduce conflict of interest. Nonfinancial information is good to both the firm and the investors

who read the sustainability reports. Having good quality sustainability information will mean

that the firm has good corporate governance, good management and accountants who believe in

sustainability reporting.

Literature Review

Voluntary Disclosure theory on Sustainability Reporting

This theory suggests that there is a positive correlation between performance on

sustainability and disclosure of discretionary level of sustainability. The notion behind this

theory is that, organizations which perform well in sustainability reporting give much focus on

their performance indictors which are hard to be imitated by non- performing firms and this

helps the performing firms in improving their image, (Brammer and Pavelin,2006, pp.1168-

1188). Those firms which perform well in sustainability reporting have ability to disclose high

quality non-financial information and this is done in order to distinguish them from non-

performing firms in terms of sustainability reporting. Those firms which disclose less

information in their non-financial reports perform poorly and they are not therefore able to attract

more investors.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Contemporary Issues in Accounting7

The present literature on corporate governance and sustainability reporting raises

concerns to different scholars. Critical analysis of corporate sustainability reporting suggests that

there is significant variability in how companies and scholars view the sustainability reporting

process. (Gray, 2002, pp.687-708) provides a great synopsis of accounting literature in the field

of non-financial reporting.

There are also a number of rising empirical studies concerning sustainability reporting. There

is increased publication of careful content analysis on financial statements with perspectives

from data economics, risk managing, stakeholder and the political economies, (Belal and Owen

2007, pp, 472-494). The most general normative topic in the academic literature is that reporting

on sustainability enhances accountability, (Bebbington, Larringa and Moneva, 2008, pp,337-

361). There are numerous scholars who have proposed that the legitimacy theory offers an

explanatory structure, environmental, social and economic disclosures in the financial

statements, (Deegan, 2002, pp,282-311).

There have been a lot of studies which have particularly looked at non-financial reporting

in different firms and countries (Adams et al., 1998, 223-250). Those studies provide evidence of

differences in amount of disclosure of sustainability reporting by different firms. The level of

sustainability report disclosures present difficulties in measurement because of the sizes of firms

and the composition in different industries.

Hypothesis

The theory of voluntary disclosure states that firms which perform well in non-financial

reports disclosures report using high quality information so as to maintain their superiority in the

market and attract more investors. They therefore choose performance indicators which cannot

be copied easily in order to improve their reputation. The socio-political theories on the other

hand indicates that the poor performing firms may report on high quality non-financial

information due to subjection of pressure from the corporate governance and other social

The present literature on corporate governance and sustainability reporting raises

concerns to different scholars. Critical analysis of corporate sustainability reporting suggests that

there is significant variability in how companies and scholars view the sustainability reporting

process. (Gray, 2002, pp.687-708) provides a great synopsis of accounting literature in the field

of non-financial reporting.

There are also a number of rising empirical studies concerning sustainability reporting. There

is increased publication of careful content analysis on financial statements with perspectives

from data economics, risk managing, stakeholder and the political economies, (Belal and Owen

2007, pp, 472-494). The most general normative topic in the academic literature is that reporting

on sustainability enhances accountability, (Bebbington, Larringa and Moneva, 2008, pp,337-

361). There are numerous scholars who have proposed that the legitimacy theory offers an

explanatory structure, environmental, social and economic disclosures in the financial

statements, (Deegan, 2002, pp,282-311).

There have been a lot of studies which have particularly looked at non-financial reporting

in different firms and countries (Adams et al., 1998, 223-250). Those studies provide evidence of

differences in amount of disclosure of sustainability reporting by different firms. The level of

sustainability report disclosures present difficulties in measurement because of the sizes of firms

and the composition in different industries.

Hypothesis

The theory of voluntary disclosure states that firms which perform well in non-financial

reports disclosures report using high quality information so as to maintain their superiority in the

market and attract more investors. They therefore choose performance indicators which cannot

be copied easily in order to improve their reputation. The socio-political theories on the other

hand indicates that the poor performing firms may report on high quality non-financial

information due to subjection of pressure from the corporate governance and other social

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contemporary Issues in Accounting8

pressures. These two theories end up providing different estimations. From the theories, we can

get two hypotheses as follows,

Hypothesis 1 a. corporate governance is positively related to sustainability reporting

Hypothesis 1 b. corporate governance is negatively related to sustainability reporting

Corporate governance is directly related to good non-financial reporting. The independence of

the board members will make the firms stakeholders and accountants to report on sustainability

through demanding accountability and set mechanisms which will make the stakeholders to

achieve the corporate social responsibility targets. Corporate governance influences the reporting

quality of firms because they put emphasis on importance of nonfinancial reporting by

accountants and by so doing increase the provision of sustainability reports. The expertise of

corporate governance will make them pressure the stakeholders towards performing well with

regards to sustainability reporting. When the members of corporate governance are more diverse,

they are able to put more concern on stakeholders and in return more attention will be given to

sustainability reporting which will therefore improve the performance of non-financial reporting.

The corporate governance strengths give general indications of the extent to which it will be able

to govern the firm effectively in order to achieve sustainability reporting. From the above

discussions we expect the following hypothesis.

H2a. Corporate governance is positively related to increased believe of accountant’s in

Sustainability reporting.

H2b. corporate governance is negatively related to increased believe of accountant’s in

Sustainability reporting.

pressures. These two theories end up providing different estimations. From the theories, we can

get two hypotheses as follows,

Hypothesis 1 a. corporate governance is positively related to sustainability reporting

Hypothesis 1 b. corporate governance is negatively related to sustainability reporting

Corporate governance is directly related to good non-financial reporting. The independence of

the board members will make the firms stakeholders and accountants to report on sustainability

through demanding accountability and set mechanisms which will make the stakeholders to

achieve the corporate social responsibility targets. Corporate governance influences the reporting

quality of firms because they put emphasis on importance of nonfinancial reporting by

accountants and by so doing increase the provision of sustainability reports. The expertise of

corporate governance will make them pressure the stakeholders towards performing well with

regards to sustainability reporting. When the members of corporate governance are more diverse,

they are able to put more concern on stakeholders and in return more attention will be given to

sustainability reporting which will therefore improve the performance of non-financial reporting.

The corporate governance strengths give general indications of the extent to which it will be able

to govern the firm effectively in order to achieve sustainability reporting. From the above

discussions we expect the following hypothesis.

H2a. Corporate governance is positively related to increased believe of accountant’s in

Sustainability reporting.

H2b. corporate governance is negatively related to increased believe of accountant’s in

Sustainability reporting.

Contemporary Issues in Accounting9

References

Adams, C. (2002) A. Internal organizational factors influencing corporate social and ethical

reporting: Beyond current theorizing. Accounting, Auditing & Accountability Journal, 15 (2):

223-50.

Amran, A. and Ooi, S. K. (2014). Sustainability reporting: meeting stakeholder demands.

Strategic Direction, 30:7, pp. 38-41.

Bebbington, J., Larringa, C., Moneva, J. M. (2008) Corporate social reporting andreputation risk

management. Accounting, Auditing & Accountability Journal, 21 (3): 337-361.

Belal, A. R., Owen, D. L(2007). The views of corporate managers on the current state of, and

future prospects for, social reporting in Bangladesh. Accounting, Auditing & Accountability

Journal (2007), 20 (3): 472-494.

Brammer, S. and Pavelin, S. (2006). Voluntary environmental disclosures by large UK

companies. Journal of Business Finance & Accounting, 33, pp. 1168-1188.

Deegan, C. and Gordon, B. (1996). A Study of the Environmental Disclosure Practices of

Australian Corporations. Accounting and Business Research, 26:3, pp. 187-199.

Deegan, C.(2002)The legitimising effect of social and environmental disclosures - a theoretical

foundation.Accounting, Auditing & Accountability Journal, 15 (3): 282-311.

Friedman, M. (2007). The Social Responsibility of Business is to Increase its Profits. New York:

Gray, R.(2002)The social accounting project and Accounting Organizations and Society

Hahn, R. and Kühnen, M. (2013). Determinants of sustainability reporting: a review of results,

trends, theory, and opportunities in an expanding field of research. Journal of Cleaner

Production, 59, pp. 5-21.

Minan, P., Hickox, J., & Gimigliano, J. (2011). Sustainability reporting--What you should know.

Amstelveen, Netherlands:

Privileging engagement, imaginings, new accountings and pragmatism over critique?

Accounting, Organizations and Society, 27: 687–708.

References

Adams, C. (2002) A. Internal organizational factors influencing corporate social and ethical

reporting: Beyond current theorizing. Accounting, Auditing & Accountability Journal, 15 (2):

223-50.

Amran, A. and Ooi, S. K. (2014). Sustainability reporting: meeting stakeholder demands.

Strategic Direction, 30:7, pp. 38-41.

Bebbington, J., Larringa, C., Moneva, J. M. (2008) Corporate social reporting andreputation risk

management. Accounting, Auditing & Accountability Journal, 21 (3): 337-361.

Belal, A. R., Owen, D. L(2007). The views of corporate managers on the current state of, and

future prospects for, social reporting in Bangladesh. Accounting, Auditing & Accountability

Journal (2007), 20 (3): 472-494.

Brammer, S. and Pavelin, S. (2006). Voluntary environmental disclosures by large UK

companies. Journal of Business Finance & Accounting, 33, pp. 1168-1188.

Deegan, C. and Gordon, B. (1996). A Study of the Environmental Disclosure Practices of

Australian Corporations. Accounting and Business Research, 26:3, pp. 187-199.

Deegan, C.(2002)The legitimising effect of social and environmental disclosures - a theoretical

foundation.Accounting, Auditing & Accountability Journal, 15 (3): 282-311.

Friedman, M. (2007). The Social Responsibility of Business is to Increase its Profits. New York:

Gray, R.(2002)The social accounting project and Accounting Organizations and Society

Hahn, R. and Kühnen, M. (2013). Determinants of sustainability reporting: a review of results,

trends, theory, and opportunities in an expanding field of research. Journal of Cleaner

Production, 59, pp. 5-21.

Minan, P., Hickox, J., & Gimigliano, J. (2011). Sustainability reporting--What you should know.

Amstelveen, Netherlands:

Privileging engagement, imaginings, new accountings and pragmatism over critique?

Accounting, Organizations and Society, 27: 687–708.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Contemporary Issues in

Accounting10

Tirole, J. (2001), "Corporate Governance," Econometrica, 69, 1, pp. 1-35

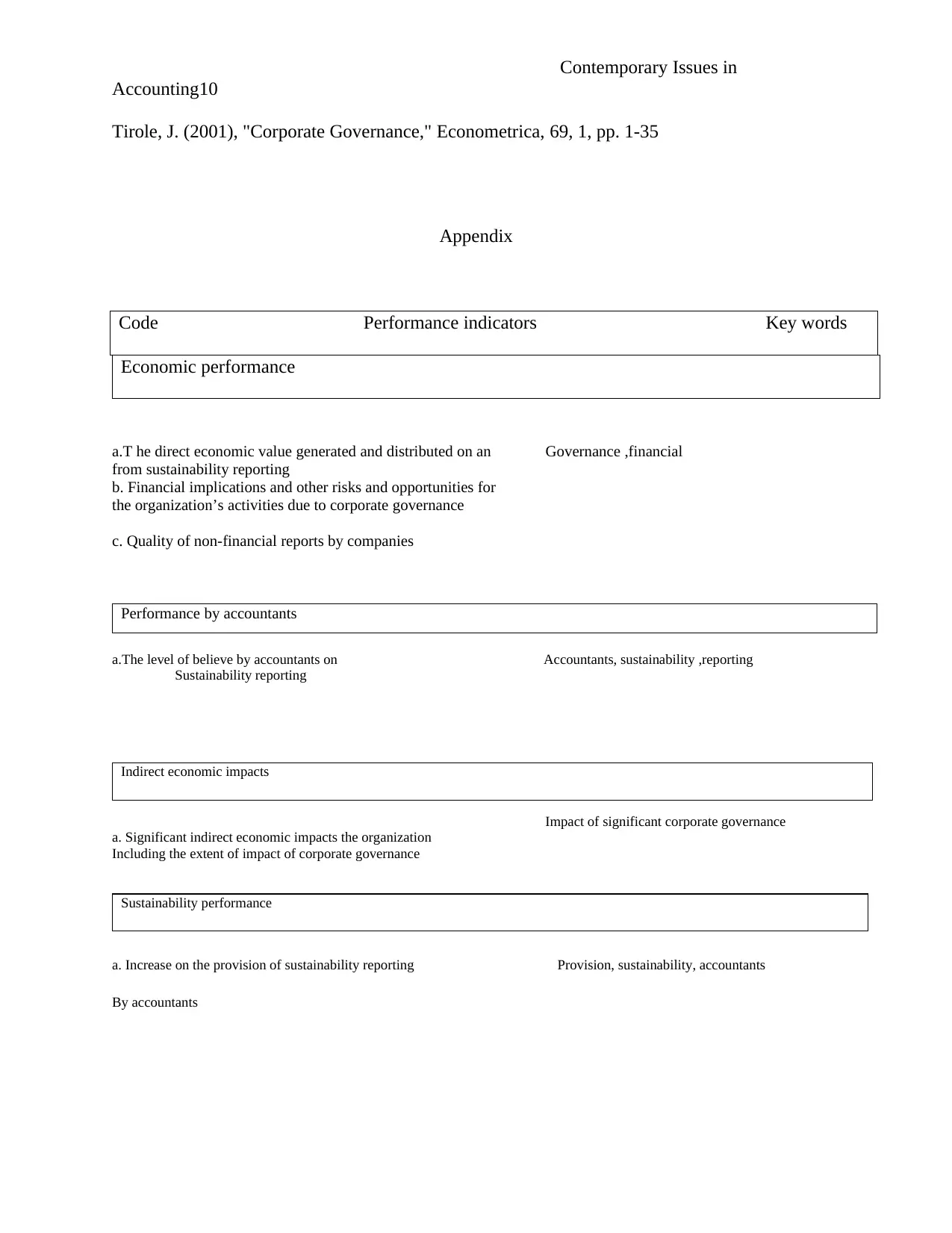

Appendix

Code Performance indicators Key words

Economic performance

a.T he direct economic value generated and distributed on an Governance ,financial

from sustainability reporting

b. Financial implications and other risks and opportunities for

the organization’s activities due to corporate governance

c. Quality of non-financial reports by companies

Performance by accountants

a.The level of believe by accountants on Accountants, sustainability ,reporting

Sustainability reporting

Indirect economic impacts

Impact of significant corporate governance

a. Significant indirect economic impacts the organization

Including the extent of impact of corporate governance

Sustainability performance

a. Increase on the provision of sustainability reporting Provision, sustainability, accountants

By accountants

Accounting10

Tirole, J. (2001), "Corporate Governance," Econometrica, 69, 1, pp. 1-35

Appendix

Code Performance indicators Key words

Economic performance

a.T he direct economic value generated and distributed on an Governance ,financial

from sustainability reporting

b. Financial implications and other risks and opportunities for

the organization’s activities due to corporate governance

c. Quality of non-financial reports by companies

Performance by accountants

a.The level of believe by accountants on Accountants, sustainability ,reporting

Sustainability reporting

Indirect economic impacts

Impact of significant corporate governance

a. Significant indirect economic impacts the organization

Including the extent of impact of corporate governance

Sustainability performance

a. Increase on the provision of sustainability reporting Provision, sustainability, accountants

By accountants

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.