Tesco Plc Accounting Scandal: A Corporate Governance Analysis

VerifiedAdded on 2023/01/23

|14

|4605

|64

Report

AI Summary

This report provides a comprehensive analysis of the Tesco Plc accounting scandal, examining the historical background, overview of the case, and the non-compliance with corporate governance principles. It delves into the specifics of the accounting fraud, the overstatement of profits, and the subsequent impact on the company's share price and reputation. The report explores the roles and responsibilities of the board of directors, the audit committee, and the external auditors, highlighting the failures in corporate governance that contributed to the scandal. It also discusses the lessons learned from the Tesco case, including the need for stronger internal controls, ethical leadership, and independent oversight. The report further examines Tesco's current scenario, including the strategies implemented to recover from the scandal, and concludes with a reflection on the importance of corporate governance in maintaining stakeholder trust and ensuring the long-term sustainability of a business.

Corporate Governance and

Globalization

1

Globalization

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction................................................................................................................................3

Assessment of the case...............................................................................................................3

History / Background.............................................................................................................3

Overview of Case...................................................................................................................4

Non-compliance of corporate governance.............................................................................4

Lesson Learned......................................................................................................................6

Tesco Plc (Current scenario)......................................................................................................7

Restructuring Supplier Relation.............................................................................................9

Role of Auditor......................................................................................................................9

Building a better Tesco........................................................................................................11

Conclusion................................................................................................................................12

Bibliography.............................................................................................................................13

2

Introduction................................................................................................................................3

Assessment of the case...............................................................................................................3

History / Background.............................................................................................................3

Overview of Case...................................................................................................................4

Non-compliance of corporate governance.............................................................................4

Lesson Learned......................................................................................................................6

Tesco Plc (Current scenario)......................................................................................................7

Restructuring Supplier Relation.............................................................................................9

Role of Auditor......................................................................................................................9

Building a better Tesco........................................................................................................11

Conclusion................................................................................................................................12

Bibliography.............................................................................................................................13

2

Introduction

Increasing interest in pressures on national system relating to corporate governance to

congregate which is asserted being developed by the process of globalization1. It has been

assessed that the trend of globalization will lead to the efficient allocation of capital.

However, a significant change has been accessed in national governance system which

eventually led to effective market-driven as well as enhancing procedure. Corporate

governance can be referred to as a set of rules and provision which are applied by a business

organization in order to control the business operations2. The present study emphasizes on

Tesco Plc accounting scandal. Initially,the background of the company has been provided

along with the detailed analysis of the accounting scandal issue of the company. The major

objective of corporate governance is to establish and sustain the balance held among

corporate operations and stakeholder’s interest as well as shareholders of the company. But

even though recent addition to corporate governance scam has been accessed amount which

Tesco –Plc is the most prominent one. Further, the present status of the company and changes

that have been made in the company have been discussed so that a similar conspiracy does

not arise in future. Lastly, the core learning’s from Tesco Plc accounting scandal has been

provided in the form of conclusion.

Assessment of the case

History / Background

Tesco-Plc was formed and introduced in 1919 by Jack Cohen being a group of market stalls.

The company appeared for in the year 1924 when it come up with a tea shipment from Mr T.

E. Stockwell. The expansionary thrust of the company was assessed when it implemented

actions to purchase rival shops. The company initiated its ambitious plans of expansion

1Ruth King and Fitzgerald Lin. "10. Challenges facing the accounting profession: maintaining

relevance in a changing environment." Perspectives on Contemporary Professional Work:

Challenges and Experiences [2016] 176-220.

2Bob Tricker. Corporate governance: Principles, policies, and practices. (Oxford University

Press, USA, 2015).

3

Increasing interest in pressures on national system relating to corporate governance to

congregate which is asserted being developed by the process of globalization1. It has been

assessed that the trend of globalization will lead to the efficient allocation of capital.

However, a significant change has been accessed in national governance system which

eventually led to effective market-driven as well as enhancing procedure. Corporate

governance can be referred to as a set of rules and provision which are applied by a business

organization in order to control the business operations2. The present study emphasizes on

Tesco Plc accounting scandal. Initially,the background of the company has been provided

along with the detailed analysis of the accounting scandal issue of the company. The major

objective of corporate governance is to establish and sustain the balance held among

corporate operations and stakeholder’s interest as well as shareholders of the company. But

even though recent addition to corporate governance scam has been accessed amount which

Tesco –Plc is the most prominent one. Further, the present status of the company and changes

that have been made in the company have been discussed so that a similar conspiracy does

not arise in future. Lastly, the core learning’s from Tesco Plc accounting scandal has been

provided in the form of conclusion.

Assessment of the case

History / Background

Tesco-Plc was formed and introduced in 1919 by Jack Cohen being a group of market stalls.

The company appeared for in the year 1924 when it come up with a tea shipment from Mr T.

E. Stockwell. The expansionary thrust of the company was assessed when it implemented

actions to purchase rival shops. The company initiated its ambitious plans of expansion

1Ruth King and Fitzgerald Lin. "10. Challenges facing the accounting profession: maintaining

relevance in a changing environment." Perspectives on Contemporary Professional Work:

Challenges and Experiences [2016] 176-220.

2Bob Tricker. Corporate governance: Principles, policies, and practices. (Oxford University

Press, USA, 2015).

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

through opening outlets in the US with the name ‘Fresh and easy’, and now the company is

operating in almost thirteen countries.

Overview of Case

The voluntary disclosure of falsification of books of accounts by the management of Tesco-

Plc, a UK based retailer affected the market price of the share as well as the investment value

of its shareholder. In the year 2014, Tesco was pitched into deeper crises, and led to

suspending of four senior executives of the company. Further, the reason behind the same

was the outrage of overstatement of the first half profits by £250 million. The management of

the conducted the overstatement of corporate profits to be £1.1 billion. However, it was later

assessed that the company has experience profits of £ 263 million. The overstatement of

profit was made to influence the shareholders and to enhance the value of the investment as

well as funds to the retailer. Though, legal authorities and management of the company took

specified scandal matter under significant concern and reduced the £2 billion of net value

from Tesco –Plc3. Due to the specified accounting scandal, the company was convicted for

fine of £500 million in the year end. Further, a case was filed by approximately 125 investors

in opposition to the company following the reason for accounting fraud and alleged that the

company had been providing incorrect facts in order to gain funds as well as investments.

Thus, the company faced criticism in the form of investor’s outburst for accepting practices

despite several warnings from analyst regarding aggressive accounting practices.

Non-compliance of corporate governance

Tesco Plc has been acknowledged for compliance with the structure of corporate governance

as well as its concern towards promise towards safety and ethics relating to individuals and

the environment. But, the fraud in the year 2014 is one of the events which declined or had a

significant negative affect on the image of the company. Due to the above specified corporate

governance, a lot of individuals of the company were terminated which comprises 4

executives and several other employees of the company. Even the Chief Finance Officer gave

resignation just before the incident of the accounting scandal was known to the general

public. The same was followed with the resignation of other senior management executives

3Al Jihad Okaily, Dixon Roband SalamaAly. "Corporate governance quality and premature

revenue recognition: evidence from the UK." International Journal of Managerial

Finance, 15.1 , [2019] : 79-99.

4

operating in almost thirteen countries.

Overview of Case

The voluntary disclosure of falsification of books of accounts by the management of Tesco-

Plc, a UK based retailer affected the market price of the share as well as the investment value

of its shareholder. In the year 2014, Tesco was pitched into deeper crises, and led to

suspending of four senior executives of the company. Further, the reason behind the same

was the outrage of overstatement of the first half profits by £250 million. The management of

the conducted the overstatement of corporate profits to be £1.1 billion. However, it was later

assessed that the company has experience profits of £ 263 million. The overstatement of

profit was made to influence the shareholders and to enhance the value of the investment as

well as funds to the retailer. Though, legal authorities and management of the company took

specified scandal matter under significant concern and reduced the £2 billion of net value

from Tesco –Plc3. Due to the specified accounting scandal, the company was convicted for

fine of £500 million in the year end. Further, a case was filed by approximately 125 investors

in opposition to the company following the reason for accounting fraud and alleged that the

company had been providing incorrect facts in order to gain funds as well as investments.

Thus, the company faced criticism in the form of investor’s outburst for accepting practices

despite several warnings from analyst regarding aggressive accounting practices.

Non-compliance of corporate governance

Tesco Plc has been acknowledged for compliance with the structure of corporate governance

as well as its concern towards promise towards safety and ethics relating to individuals and

the environment. But, the fraud in the year 2014 is one of the events which declined or had a

significant negative affect on the image of the company. Due to the above specified corporate

governance, a lot of individuals of the company were terminated which comprises 4

executives and several other employees of the company. Even the Chief Finance Officer gave

resignation just before the incident of the accounting scandal was known to the general

public. The same was followed with the resignation of other senior management executives

3Al Jihad Okaily, Dixon Roband SalamaAly. "Corporate governance quality and premature

revenue recognition: evidence from the UK." International Journal of Managerial

Finance, 15.1 , [2019] : 79-99.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

which is weak corporate governance. Moreover, board of directors of the company did not

pay any attention along with non-executive directors on the increased profits in order to attain

attention from shareholders.

Board of directors is having an evident role in a company in order to indulge corporate

governance in a vigilant manner. Effective corporate governance practices can be continued

or sustained only through efficient application of corporate governance principals by the key

players of the company4. There is a liability of Board of Directors to develop a core

objectives, mission and vision of organization at the same time setting strategies in order to

attain an adequate market position. The specified responsibilities were not fulfilled by the

management of Tesco as BOD was not complying with the required Code of Ethics and the

audit directives which eventually resulted in fraud of accounting. Even no action was taken

against the irregularities relating to strategic decision and emphasis was made only on

revenue generation. It is necessary for senior executives to establish effective standards of

leadership along with strong culture of corporate governance in order to decrease the

possibility of the shaky internal system , which was available in Tesco Plc.

Organizational audit committee is obligatory for attaining the characteristic of variant

integrity in books of accounts along with procedure relating to the assessment of decision,

business operation and financial control so that fair financial view can be presented to the

stakeholders and shareholders5. Though, in Tesco-Plc scenerio, the books of accounts were

audited by PwC which paid no significant concern to the inflated profits due to which

company had to take the decision to remove the external audit committee’s PwC of Tesco

PLC. Furthermore, the company’s internal as well as external audit committee is liable for

assessing financial activities which comprises internal and external audit procedures. Further,

assessment relating to disclosure and monitoring of financial activities is also accountable in

4Ruth King and Fitzgerald Lin. "10. Challenges facing the accounting profession: maintaining

relevance in a changing environment." Perspectives on Contemporary Professional Work:

Challenges and Experiences [2016] 176-220.

5Barry Evans and Mason Robert. The lean supply chain: managing the challenge at Tesco.

(Kogan Page Publishers, 2018).

5

pay any attention along with non-executive directors on the increased profits in order to attain

attention from shareholders.

Board of directors is having an evident role in a company in order to indulge corporate

governance in a vigilant manner. Effective corporate governance practices can be continued

or sustained only through efficient application of corporate governance principals by the key

players of the company4. There is a liability of Board of Directors to develop a core

objectives, mission and vision of organization at the same time setting strategies in order to

attain an adequate market position. The specified responsibilities were not fulfilled by the

management of Tesco as BOD was not complying with the required Code of Ethics and the

audit directives which eventually resulted in fraud of accounting. Even no action was taken

against the irregularities relating to strategic decision and emphasis was made only on

revenue generation. It is necessary for senior executives to establish effective standards of

leadership along with strong culture of corporate governance in order to decrease the

possibility of the shaky internal system , which was available in Tesco Plc.

Organizational audit committee is obligatory for attaining the characteristic of variant

integrity in books of accounts along with procedure relating to the assessment of decision,

business operation and financial control so that fair financial view can be presented to the

stakeholders and shareholders5. Though, in Tesco-Plc scenerio, the books of accounts were

audited by PwC which paid no significant concern to the inflated profits due to which

company had to take the decision to remove the external audit committee’s PwC of Tesco

PLC. Furthermore, the company’s internal as well as external audit committee is liable for

assessing financial activities which comprises internal and external audit procedures. Further,

assessment relating to disclosure and monitoring of financial activities is also accountable in

4Ruth King and Fitzgerald Lin. "10. Challenges facing the accounting profession: maintaining

relevance in a changing environment." Perspectives on Contemporary Professional Work:

Challenges and Experiences [2016] 176-220.

5Barry Evans and Mason Robert. The lean supply chain: managing the challenge at Tesco.

(Kogan Page Publishers, 2018).

5

the hands of the audit committee6. In Tesco Plc case, as audit committee has not

accomplished their responsibilities due to which it gave birth to an accounting fraud of the

company. Following to this company’s CFO gave resignation and Tesco was left over with

no control from the side of CFO.

Lesson Learned

The corporate governance framework of Tesco Plc was not strong, and thus no concern was

provided to the inflated profits which resulted in heavy penalties for the company. Along

with same it also had negatively affected the overall image of the company in front of

shareholders and other stakeholders. The decision of Tesco Plcis evident to the fact that

internal as well as external board of director are accountable for making better decisions in

order to evade misstatement in financial reports as well as disclosure in the financial

statement of the company. The lesson can be taken from the fraud of accounting incident of

Tesco Plc that it is necessary for an organization to evolve effectual regulations and

appropriate accounting practices to avoid fraud such as accounting scandal7. Further, it is also

necessary to incorporate adequate governing practices in the corporate governance so that

adequate check on employees can be kept8. It will assist in ascertaining whether the

employees and management in meeting up organizational goals and whether appropriate

importance is given to stakeholder’s right and legal rights or not.

In case the corporate structure and board of directors have provided adequate importance to

stakeholder’s value and would have set aside their personal interest than possibility exist that

6Bradley Rudkin, , et al. "Hide-and-seek in corporate disclosure: evidence from negative

corporate incidents." Corporate Governance: The International Journal of Business in

Society [2019], 19.1, 158-175.

7Francesca Cuomo, Mallin Christine, and Zattoni Alessandro. "Corporate governance codes:

A review and research agenda." Corporate governance: an international review (2016)

24.3 , 222-241.

8LimaVicente Crisóstomo and BrandãoFreitasIsac de. "The ultimate controlling owner and

corporate governance in United States." Corporate Governance: The International Journal of

Business in Society , (2019) 19.1 , 120-140.

6

accomplished their responsibilities due to which it gave birth to an accounting fraud of the

company. Following to this company’s CFO gave resignation and Tesco was left over with

no control from the side of CFO.

Lesson Learned

The corporate governance framework of Tesco Plc was not strong, and thus no concern was

provided to the inflated profits which resulted in heavy penalties for the company. Along

with same it also had negatively affected the overall image of the company in front of

shareholders and other stakeholders. The decision of Tesco Plcis evident to the fact that

internal as well as external board of director are accountable for making better decisions in

order to evade misstatement in financial reports as well as disclosure in the financial

statement of the company. The lesson can be taken from the fraud of accounting incident of

Tesco Plc that it is necessary for an organization to evolve effectual regulations and

appropriate accounting practices to avoid fraud such as accounting scandal7. Further, it is also

necessary to incorporate adequate governing practices in the corporate governance so that

adequate check on employees can be kept8. It will assist in ascertaining whether the

employees and management in meeting up organizational goals and whether appropriate

importance is given to stakeholder’s right and legal rights or not.

In case the corporate structure and board of directors have provided adequate importance to

stakeholder’s value and would have set aside their personal interest than possibility exist that

6Bradley Rudkin, , et al. "Hide-and-seek in corporate disclosure: evidence from negative

corporate incidents." Corporate Governance: The International Journal of Business in

Society [2019], 19.1, 158-175.

7Francesca Cuomo, Mallin Christine, and Zattoni Alessandro. "Corporate governance codes:

A review and research agenda." Corporate governance: an international review (2016)

24.3 , 222-241.

8LimaVicente Crisóstomo and BrandãoFreitasIsac de. "The ultimate controlling owner and

corporate governance in United States." Corporate Governance: The International Journal of

Business in Society , (2019) 19.1 , 120-140.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the company would not have faced serious accounting scandal. Recruiting an unbiased third

party for bookkeeping of an organization might assist in assuring non-occurrence of another

mishappening or scandal relating to the recording of accounting transactions. The fact cannot

be denied that internal bookkeepers of Tesco have played around with numbers in order to

provide significant profit in books of accounts. Thus, in the case specified operation relating

to bookkeeping is outsourced that there would be no pressure from higher authorities in order

to present higher profits as their livelihood is not dependable on agreeing on inappropriate

orders of the executives9. Further, books of accounts prepared by third party accountants

would be more appropriate as it would be developed on the basis of impartiality and on the

grounds of closely acceptable accounting practices.

Tesco Plc (Current scenario)

The present time has been very challenging for Tesco. The recent accounting scandal of

Tesco led to a decrease in customer confidence in the food industry and affected the overall

reputation of the company. After considering all initiatives to recover from the effects of

accounting wrongdoings, the Tesco management has now signed an agreement of deferred

prosecution for compensating and paying fines. This states that the stores of Tesco would

now be out of the legal issues on a temporary basis. Similarly, the company signed to an

agreement of making payment of £129 million in lieu of being prosecuted. Currently, the

company has considered various initiatives, strategies, company changes so as to stabilize its

financial position and reputation.

9Rading Erick Outa and Waweru M. Nelson.. "Corporate governance guidelines compliance

and firm financial performance: United States."Managerial Auditing Journal , ,( 2016) , 31,

8/9, 891-914.

7

party for bookkeeping of an organization might assist in assuring non-occurrence of another

mishappening or scandal relating to the recording of accounting transactions. The fact cannot

be denied that internal bookkeepers of Tesco have played around with numbers in order to

provide significant profit in books of accounts. Thus, in the case specified operation relating

to bookkeeping is outsourced that there would be no pressure from higher authorities in order

to present higher profits as their livelihood is not dependable on agreeing on inappropriate

orders of the executives9. Further, books of accounts prepared by third party accountants

would be more appropriate as it would be developed on the basis of impartiality and on the

grounds of closely acceptable accounting practices.

Tesco Plc (Current scenario)

The present time has been very challenging for Tesco. The recent accounting scandal of

Tesco led to a decrease in customer confidence in the food industry and affected the overall

reputation of the company. After considering all initiatives to recover from the effects of

accounting wrongdoings, the Tesco management has now signed an agreement of deferred

prosecution for compensating and paying fines. This states that the stores of Tesco would

now be out of the legal issues on a temporary basis. Similarly, the company signed to an

agreement of making payment of £129 million in lieu of being prosecuted. Currently, the

company has considered various initiatives, strategies, company changes so as to stabilize its

financial position and reputation.

9Rading Erick Outa and Waweru M. Nelson.. "Corporate governance guidelines compliance

and firm financial performance: United States."Managerial Auditing Journal , ,( 2016) , 31,

8/9, 891-914.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

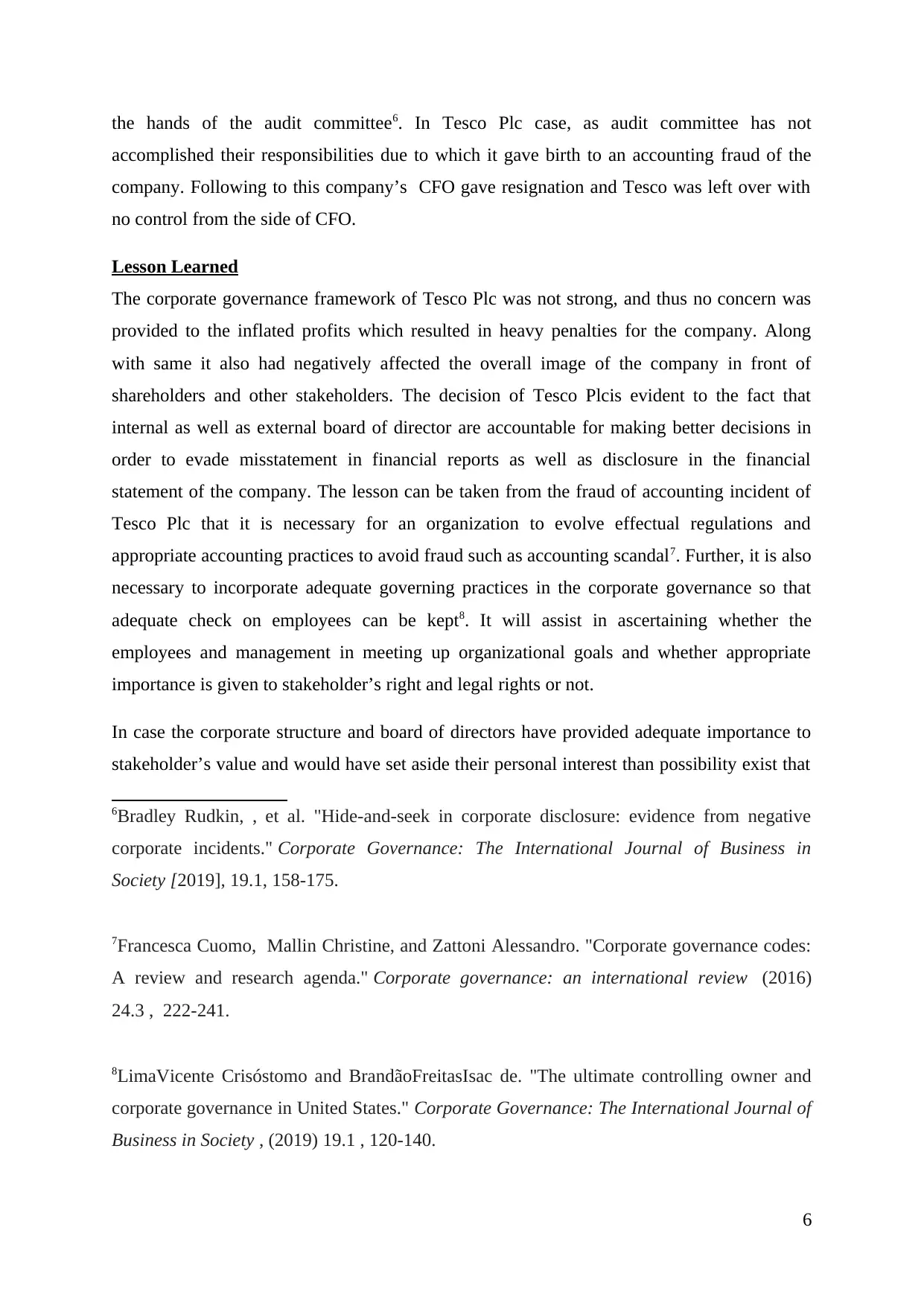

Figure 1: Assessment of trend of the share price of Tesco Plc

(Source: Thomas, 2019)

The news relating to accounting scandal provided shock waves throughout the city in the year

2014 and arose significant queries relating to the performance of the company and its share

prices. Thus, the company suspended eight directors, and three former executives were

alleged as the Serious Fraud Office with fraud after the ascertainment of a black hole10. In the

year 2017, the company made a payout of £85 million relating to compensation payout to the

investor and £ 129 million relating to penalties and related cost. The company has initiated to

take steps in order to improve stores considering the variants such as prices and range of

products11. A three-year turnaround plan has been developed in order to reboot the business,

and a positive impact can be assessed as margins were increased in a significant manner last

year.

The current status of the company is in the middle of challenging and being progressive. This

is a critical time for the company to enhance and repair its position, performance, image and

10Daniel Thomas, ‘Tesco profits rebound as turnaround continues’ (Business, 11 April

2018)<https://www.bbc.com/news/business-43722494> accessed on 19 April 2019

11Francis Awolowo, Ifedapo. "Financial statement fraud: The need for a paradigm shift to

forensic accounting." system 7.10 (Routledge, 2016) : 23.

8

(Source: Thomas, 2019)

The news relating to accounting scandal provided shock waves throughout the city in the year

2014 and arose significant queries relating to the performance of the company and its share

prices. Thus, the company suspended eight directors, and three former executives were

alleged as the Serious Fraud Office with fraud after the ascertainment of a black hole10. In the

year 2017, the company made a payout of £85 million relating to compensation payout to the

investor and £ 129 million relating to penalties and related cost. The company has initiated to

take steps in order to improve stores considering the variants such as prices and range of

products11. A three-year turnaround plan has been developed in order to reboot the business,

and a positive impact can be assessed as margins were increased in a significant manner last

year.

The current status of the company is in the middle of challenging and being progressive. This

is a critical time for the company to enhance and repair its position, performance, image and

10Daniel Thomas, ‘Tesco profits rebound as turnaround continues’ (Business, 11 April

2018)<https://www.bbc.com/news/business-43722494> accessed on 19 April 2019

11Francis Awolowo, Ifedapo. "Financial statement fraud: The need for a paradigm shift to

forensic accounting." system 7.10 (Routledge, 2016) : 23.

8

reputation. It must involve honesty, integrity, trustworthiness and fairness in all its aspects

and giving less weight to personal interest simultaneously.

It has been stated by Lewis that this year reflected strong progress, with the 9th growth’s

consecutive quarter. Further, Tesco is on the growth again, generating considerable cash and

recovering its profits. Its performance has been improving gradually from 2014 at the time

when it made reporting the most horrible outcomes in history with the amount of losses

subjected to £6.4bn.

Restructuring Supplier Relation

The new Chief executive of Tesco, named Dave Lewis, has promised to overhaul the

relationship of the company with the supplier after sales slump and the detection of a £263m

accounting scandal. Since then, Lewis has worked to simplify the business of Tesco and has

modified its supplier relationship to make sure that there is no repetition of the scandal. It has

declared changes to manner payment are made to a supplier that will lead to smaller suppliers

with quick payment than is normal in the grocery sector. This is considered as the best

alternative for cash flow for these suppliers. As per the investigations for its possibly

fraudulent engagement with main suppliers, this tends to be fairly considerable step by the

company is attempting to reestablish a relationship with the supply chain.

Regaining the trust from shareholder, supplier and public is now should be the topmost

priority of Tesco, alongside repairing the supplier and shareholder relationship. In pursuit of

the same, Tesco is attempting to re-establish its relationship with suppliers by introducing

new online network where the business will be capable of doing better interaction as the

biggest retailer . Further, the supermarket Group has formed the Tesco Supplier Network,

claiming to assist 5000 members in interacting with the related suppliers and retailers

regarding a variety of issues, possibly offering the best of a platform for suppliers to make

complaints, provide feedback or make an enquiry about anything.

In order to improve the performance and position of Tesco, it is essential for the company to

rebuild its relationship with suppliers and regain the trust and confidence from the side of

suppliers. The centre of the success of Tesco lies in restructuring supplier relation.

Role of Auditor

Auditors have a significant role in saving Tesco from such crises as well as scandals. They

are required to form strict as well as transparent rules amd policies in aligned with the

9

and giving less weight to personal interest simultaneously.

It has been stated by Lewis that this year reflected strong progress, with the 9th growth’s

consecutive quarter. Further, Tesco is on the growth again, generating considerable cash and

recovering its profits. Its performance has been improving gradually from 2014 at the time

when it made reporting the most horrible outcomes in history with the amount of losses

subjected to £6.4bn.

Restructuring Supplier Relation

The new Chief executive of Tesco, named Dave Lewis, has promised to overhaul the

relationship of the company with the supplier after sales slump and the detection of a £263m

accounting scandal. Since then, Lewis has worked to simplify the business of Tesco and has

modified its supplier relationship to make sure that there is no repetition of the scandal. It has

declared changes to manner payment are made to a supplier that will lead to smaller suppliers

with quick payment than is normal in the grocery sector. This is considered as the best

alternative for cash flow for these suppliers. As per the investigations for its possibly

fraudulent engagement with main suppliers, this tends to be fairly considerable step by the

company is attempting to reestablish a relationship with the supply chain.

Regaining the trust from shareholder, supplier and public is now should be the topmost

priority of Tesco, alongside repairing the supplier and shareholder relationship. In pursuit of

the same, Tesco is attempting to re-establish its relationship with suppliers by introducing

new online network where the business will be capable of doing better interaction as the

biggest retailer . Further, the supermarket Group has formed the Tesco Supplier Network,

claiming to assist 5000 members in interacting with the related suppliers and retailers

regarding a variety of issues, possibly offering the best of a platform for suppliers to make

complaints, provide feedback or make an enquiry about anything.

In order to improve the performance and position of Tesco, it is essential for the company to

rebuild its relationship with suppliers and regain the trust and confidence from the side of

suppliers. The centre of the success of Tesco lies in restructuring supplier relation.

Role of Auditor

Auditors have a significant role in saving Tesco from such crises as well as scandals. They

are required to form strict as well as transparent rules amd policies in aligned with the

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

application of corporate reporting, internal supervision, risk management and preserving

strong relationships with suppliers and shareholders12. In this aspect, the auditors are

responsible for assessing the corporate financial statement, structure and announcement

integrity13. It can be asserted that auditors are considered as the main players to prevent fraud

as a whole. By considering the Tesco case, and the results of not complying to relevant

standards of auditing professional, yet Tesco Plc’s audit committee of was extensively

preventing their duties which further led to the massisve fraud in the year 2014 The internal

as well as external auditors of the company are liable for management of all the financial

activities of company like financial reporting, proper disclosures, regulatory operations

management and check on internal and external audit14. Thus, auditors are primarily needed

to review and check audit and financial aspects, so that fair, true and accurate representation

of financial statements and account is present15.Therefore, the auditors must conduct the

application of ethical standards, supervision over quality and relevant auditing in best

ineterst, and adopt the International Standards on Quality Control, International Standards on

Auditing and ethical standards16.

12Ruth VAguilera, and Crespi-CladeraRafel. "Global corporate governance: On the relevance

of firms’ ownership structure." Journal of World Business (2016), 51.1 , 50-57.

13H. Lars Gulbrandsen, . Globalization, Governance Gaps, and the Emergence of New

Institutions for Political Consumerism. The Oxford Handbook of Political Consumerism,

[2019]. 227.

14GrażynaŚmigielska,."A business case for sustainable development." CES Working Papers

[2018], 10.1, 49-66.

15BradleyRudkin, et al. "Hide-and-seek in corporate disclosure: evidence from negative

corporate incidents." Corporate Governance: The International Journal of Business in

Society (2019), 19.1, 158-175.

16LeBaron, Genevieve, Jane Lister, and Peter Dauvergne."Governing global supply chain

sustainability through the ethical audit regime." Globalizations (2017), 14.6 , 958-975.

10

strong relationships with suppliers and shareholders12. In this aspect, the auditors are

responsible for assessing the corporate financial statement, structure and announcement

integrity13. It can be asserted that auditors are considered as the main players to prevent fraud

as a whole. By considering the Tesco case, and the results of not complying to relevant

standards of auditing professional, yet Tesco Plc’s audit committee of was extensively

preventing their duties which further led to the massisve fraud in the year 2014 The internal

as well as external auditors of the company are liable for management of all the financial

activities of company like financial reporting, proper disclosures, regulatory operations

management and check on internal and external audit14. Thus, auditors are primarily needed

to review and check audit and financial aspects, so that fair, true and accurate representation

of financial statements and account is present15.Therefore, the auditors must conduct the

application of ethical standards, supervision over quality and relevant auditing in best

ineterst, and adopt the International Standards on Quality Control, International Standards on

Auditing and ethical standards16.

12Ruth VAguilera, and Crespi-CladeraRafel. "Global corporate governance: On the relevance

of firms’ ownership structure." Journal of World Business (2016), 51.1 , 50-57.

13H. Lars Gulbrandsen, . Globalization, Governance Gaps, and the Emergence of New

Institutions for Political Consumerism. The Oxford Handbook of Political Consumerism,

[2019]. 227.

14GrażynaŚmigielska,."A business case for sustainable development." CES Working Papers

[2018], 10.1, 49-66.

15BradleyRudkin, et al. "Hide-and-seek in corporate disclosure: evidence from negative

corporate incidents." Corporate Governance: The International Journal of Business in

Society (2019), 19.1, 158-175.

16LeBaron, Genevieve, Jane Lister, and Peter Dauvergne."Governing global supply chain

sustainability through the ethical audit regime." Globalizations (2017), 14.6 , 958-975.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Building a better Tesco

Building a better Tesco strategy has been initiated by Chief Executive of Tesco, wherein they

have made greater investments in services, staff, stores and business format17. This business

strategyincludes the formation of a faster store refresh programme, establishment of effective

promotions and prices, having more customized offers and offerings inclusive of the

relaunching of ‘Tesco brands,i.e. ‘better, clearer, more relevant’ communications with

suppliers and customers.

For building a better Tesco, it is necessary that tesco include startegic regulations and

relevant accounting practices in order to prevent future frauds18. In this way, they should

involve corporate governance practices and leadership to keep the employees on track to

satisfy the mission and vision of the organization and valuing the interests of shareholders at

the same time19. Along with this, initially the company is required to keep its personal gains

and interest aside and consider public and shareholder interest so as to prevent itself from

indulging in these frauds. Thus, it can be stated that the company must take best of corporate

governance structure into account while including proper provisions based of Governance

Code and possible board members to prevent accounting scandals. Hence, the company

should focus on the customer as well as on staff, and come up with fighting from the recent

crises. The company for building a better future must mitigate the controversial crisis by

dealing with the issues quickly20.

17John D Sullivan., et al. "Stress Testing Corporate Governance." (2018).

18Jihad AlOkailyDixonRob, and SalamaAly. "Corporate governance quality and premature

revenue recognition: evidence from the UK." International Journal of Managerial Finance

(2019), 15.1 , 79-99.

19Steve Wood, WrigleyNeil, and CoeNeil M.. "Capital discipline and financial market

relations in retail globalization: insights from the case of Tesco plc." Journal of Economic

Geography (2016) 17.1, 31-57.

20ShrivesPhilip J., and Niamh MBrennan. "Explanations for corporate governance non-

compliance: A rhetorical analysis." Critical Perspectives on Accounting (2017), 49, 31-56.

11

Building a better Tesco strategy has been initiated by Chief Executive of Tesco, wherein they

have made greater investments in services, staff, stores and business format17. This business

strategyincludes the formation of a faster store refresh programme, establishment of effective

promotions and prices, having more customized offers and offerings inclusive of the

relaunching of ‘Tesco brands,i.e. ‘better, clearer, more relevant’ communications with

suppliers and customers.

For building a better Tesco, it is necessary that tesco include startegic regulations and

relevant accounting practices in order to prevent future frauds18. In this way, they should

involve corporate governance practices and leadership to keep the employees on track to

satisfy the mission and vision of the organization and valuing the interests of shareholders at

the same time19. Along with this, initially the company is required to keep its personal gains

and interest aside and consider public and shareholder interest so as to prevent itself from

indulging in these frauds. Thus, it can be stated that the company must take best of corporate

governance structure into account while including proper provisions based of Governance

Code and possible board members to prevent accounting scandals. Hence, the company

should focus on the customer as well as on staff, and come up with fighting from the recent

crises. The company for building a better future must mitigate the controversial crisis by

dealing with the issues quickly20.

17John D Sullivan., et al. "Stress Testing Corporate Governance." (2018).

18Jihad AlOkailyDixonRob, and SalamaAly. "Corporate governance quality and premature

revenue recognition: evidence from the UK." International Journal of Managerial Finance

(2019), 15.1 , 79-99.

19Steve Wood, WrigleyNeil, and CoeNeil M.. "Capital discipline and financial market

relations in retail globalization: insights from the case of Tesco plc." Journal of Economic

Geography (2016) 17.1, 31-57.

20ShrivesPhilip J., and Niamh MBrennan. "Explanations for corporate governance non-

compliance: A rhetorical analysis." Critical Perspectives on Accounting (2017), 49, 31-56.

11

Conclusion

With the consideration towards above facts, it can be stated that Tesco Plc has been struggled

long for its profit misstatement in the books of accounts gain false profiting image and

shareholder investment to increase profits. This has taken place due to the poor framework of

corporate governance and unconcern towards the auditors, audit committee and board of

directors21. Thus, the study shows that the company must considered working corporate

governance structure in their accounting and auditing processes and have reflected a true

presentation of financial information. The study reflects that only a mere overstatement of

profits can lead to huge financial crises, and can damage the names of even leading

companies, while it is a serious breach in terms of law and provisions22.

Based on above analysis, It can be concluded that auditors were needed to be well-organized

by the Tesco, with placing experienced and skilled audit committee established to avoid

scandals while upholding appropriate internal control as well as financial statement23. The

efficiency of the auditors are majorily associated with the efficiency of top management and

board of directors. Henceforth, corporate governance is a major aspect to be considered by

any organization to stabilize their financial aspects, while adhering to related provisions and

laws to operate reasonably and fairly24.

21RorySullivan, and GouldsonAndy. "The governance of corporate responses to climate

change: An international comparison." Business Strategy and the Environment [2017], 26.4:

413-425.

22KhondkarKarim,, et al. "Corporate social responsibility: Evidence from the United

Kingdom." Journal of International Business Research [2015], 14.1 , 85.

23Kate JEElliot,."Investor case study." The Business of Farm Animal Welfare in association

with GSE Research., [2018]. 97-101

24GaganKukreja,, and GuptaSanjay. "Tesco Accounting Misstatements: Myopic Ideologies

Overshadowing Larger Organisational Interests." SDMIMD Journal of Management [2016]:

7.1 , 9-18.

12

With the consideration towards above facts, it can be stated that Tesco Plc has been struggled

long for its profit misstatement in the books of accounts gain false profiting image and

shareholder investment to increase profits. This has taken place due to the poor framework of

corporate governance and unconcern towards the auditors, audit committee and board of

directors21. Thus, the study shows that the company must considered working corporate

governance structure in their accounting and auditing processes and have reflected a true

presentation of financial information. The study reflects that only a mere overstatement of

profits can lead to huge financial crises, and can damage the names of even leading

companies, while it is a serious breach in terms of law and provisions22.

Based on above analysis, It can be concluded that auditors were needed to be well-organized

by the Tesco, with placing experienced and skilled audit committee established to avoid

scandals while upholding appropriate internal control as well as financial statement23. The

efficiency of the auditors are majorily associated with the efficiency of top management and

board of directors. Henceforth, corporate governance is a major aspect to be considered by

any organization to stabilize their financial aspects, while adhering to related provisions and

laws to operate reasonably and fairly24.

21RorySullivan, and GouldsonAndy. "The governance of corporate responses to climate

change: An international comparison." Business Strategy and the Environment [2017], 26.4:

413-425.

22KhondkarKarim,, et al. "Corporate social responsibility: Evidence from the United

Kingdom." Journal of International Business Research [2015], 14.1 , 85.

23Kate JEElliot,."Investor case study." The Business of Farm Animal Welfare in association

with GSE Research., [2018]. 97-101

24GaganKukreja,, and GuptaSanjay. "Tesco Accounting Misstatements: Myopic Ideologies

Overshadowing Larger Organisational Interests." SDMIMD Journal of Management [2016]:

7.1 , 9-18.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.