Corporate Accounting and Reporting - Essay on Impairment Loss (2015)

VerifiedAdded on 2022/05/23

|7

|1375

|12

Essay

AI Summary

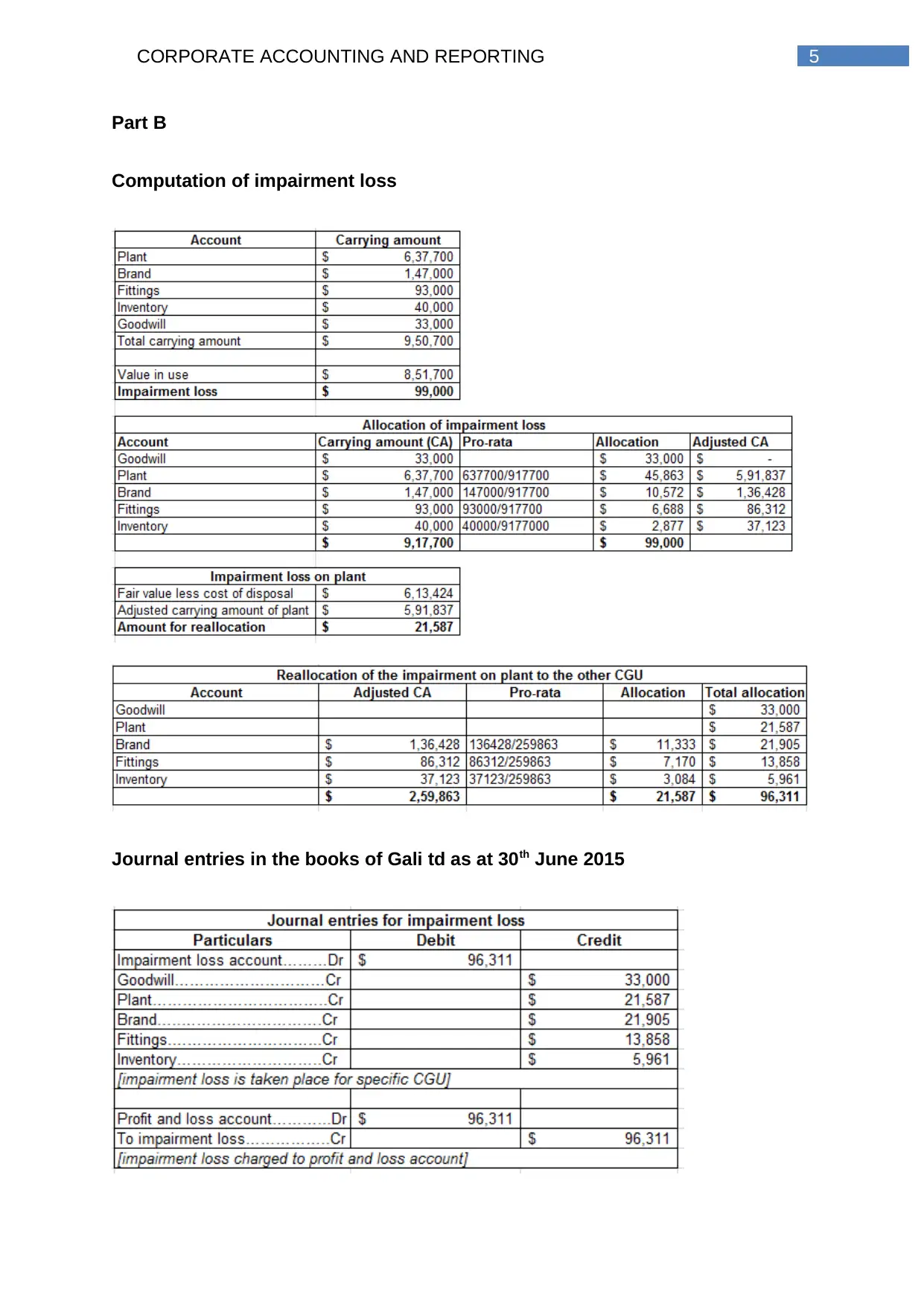

This essay provides a comprehensive analysis of impairment loss in corporate accounting, specifically focusing on cash-generating units (CGUs) and the relevant accounting standard AASB 136. The essay begins with an overview of the basic principles of impairment, including the comparison of an asset's reported value with its recoverable amount, which is the higher of fair value less costs of disposal and value in use (VIU). It explains how impairment loss is recognized and allocated, first to goodwill and then to other assets within the CGU on a pro-rata basis. The essay also discusses the importance of identifying CGUs and the criteria for their recognition, along with the accounting treatment for impairment loss, including the determination of the reported amount, fair value, and VIU. It also explores the re-allocation of goodwill in case of organizational restructuring and the importance of consistent application of accounting principles. The essay concludes with journal entries in the books of Gali Ltd as at 30th June 2015 and a list of references.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.