Corporate Accounting and Reporting 1: Impairment Test Regulations

VerifiedAdded on 2020/05/16

|8

|1446

|59

Report

AI Summary

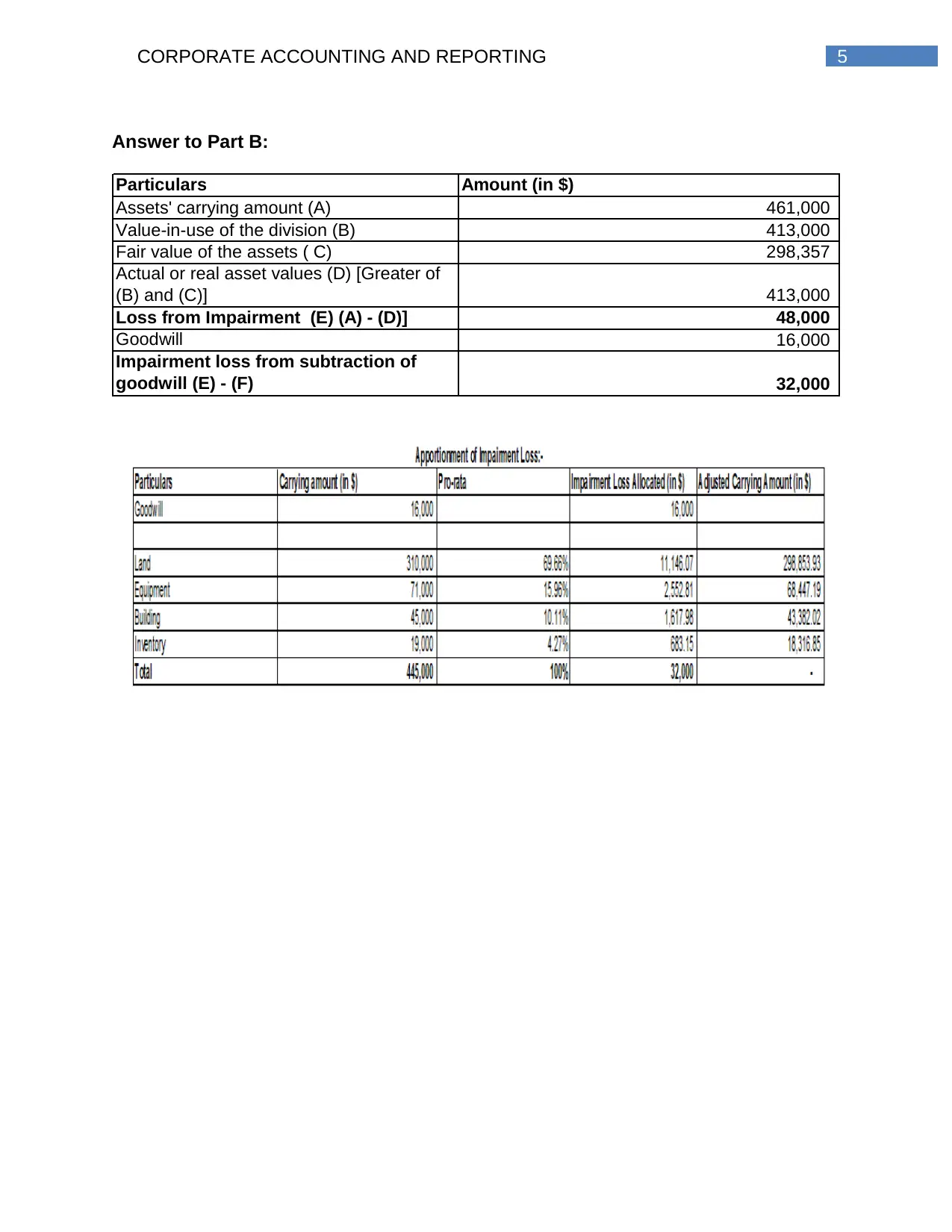

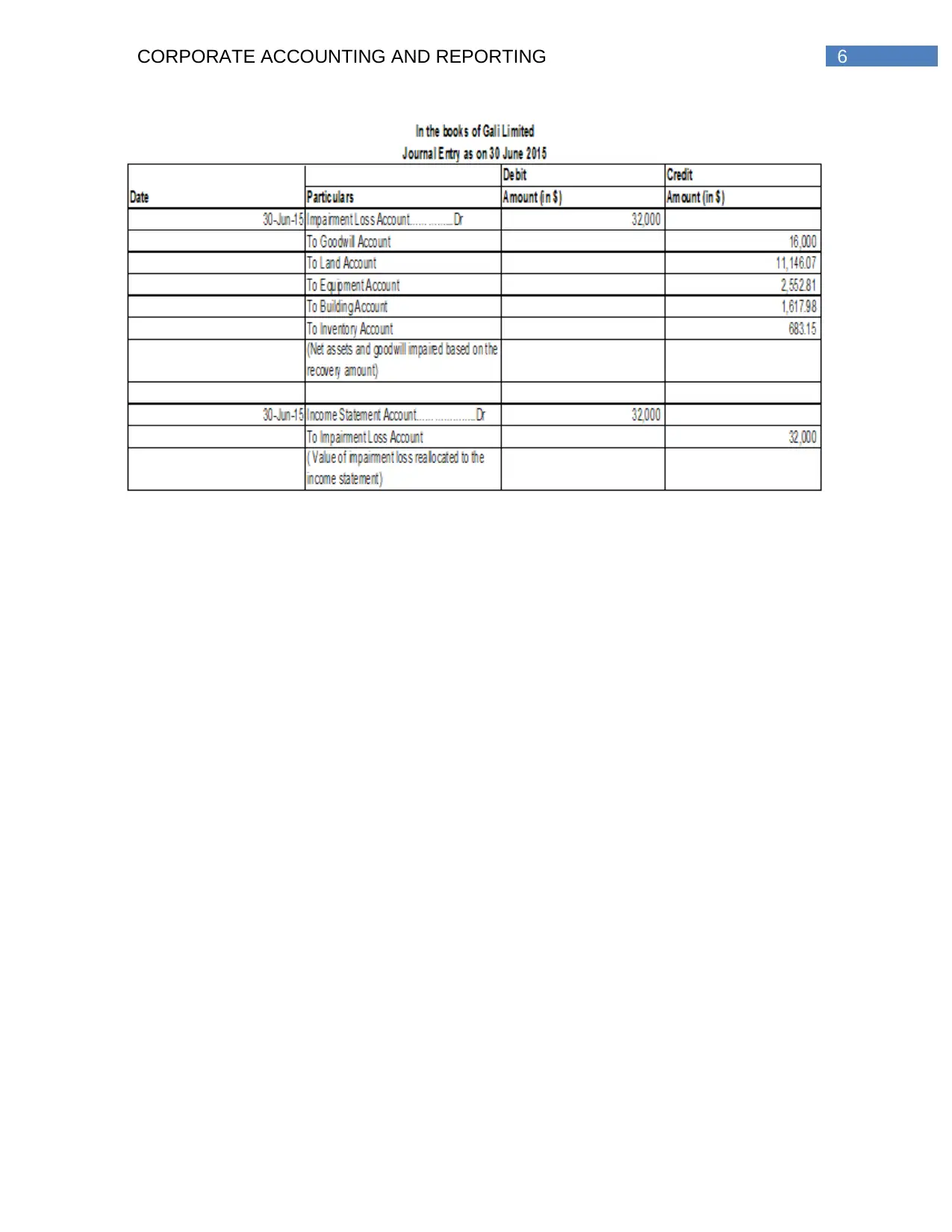

This report provides a comprehensive analysis of corporate accounting and reporting, with a specific focus on impairment testing. It examines the importance of impairment tests in ensuring that assets are not overstated, referencing key accounting standards such as IAS 36 and AASB 136. The report details when impairment tests are mandatory, including for intangible assets with indefinite lives and goodwill. It outlines the indicators of impairment, such as significant declines in asset value, negative changes in the business environment, and rising interest rates. The report also discusses how to determine the recoverable amount of an asset and the circumstances under which an organization may avoid recalculating this amount. It further explores the implications of impairment on the useful life and depreciation methods of an asset. The report is supported by various academic references, providing a robust understanding of the subject matter.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.